SHREE CEMENT LIMITED Cement Presentation Jun 2010.… · India was growing at about 7% and the...

39

1 June 2010 SHREE CEMENT LIMITED

Transcript of SHREE CEMENT LIMITED Cement Presentation Jun 2010.… · India was growing at about 7% and the...

1

June 2010

SHREE CEMENT LIMITED

2

Indian Cement Industry

3

Overview

� India was growing at about 7% and the national policy makers are

targeting GDP growth at 8-9%. Such high GDP growth should translate

into cement demand growth rate of double digits annually

� Government of India has fixed an infrastructure spend target of 10% of

GDP which translates to around USD 300 billion annually

� The basic needs of the urban populace is almost satiated. Savings are

flowing into housing and related amenities.

� The social benefit schemes like National Rural Employment Guarantee

Act is also making the development process an inclusive one cascading

into overall prosperity

� Cement demand is at an inflexion point today in India

4

Economic Super Cycle

� As per McKinsey Global Institute, April 2010, the key drivers of India’s

urbanization till 2030 are:

� GDP will grow by 5 times from present

� 590 million people will live in cities (twice the population of

present US)

� 270 million people net increase in working age population

� 70% of net new employment will be generated in cities

� 91 million urban households will be middle class, up from 22 million

today

� 68 cities will have population of 1 million plus, up from 42 today

� 700-900 million square meters of commercial & residential space needs

to be built

� 7,400 kilometers of metros and subways will need to be constructed

(20 times the capacity added in past decade)

5

Economic Super Cycle

� In 2008-09 the Indian Cement industry growth was at around 8%

and the housing infrastructure boon has increased it to around

11% for the year ended March 31, 2010

� The cement demand over last decade has grown at 1.2 to 1.3x

GDP growth rate

� Urbanization is increasing and urban population is set to grow

� The infrastructure boom coupled with faster urbanization

should increase GDP to cement CAGR to 1.4 to 1.5x

� The cement demand for next 5 years is expected to grow

between 11-12% CAGR

6

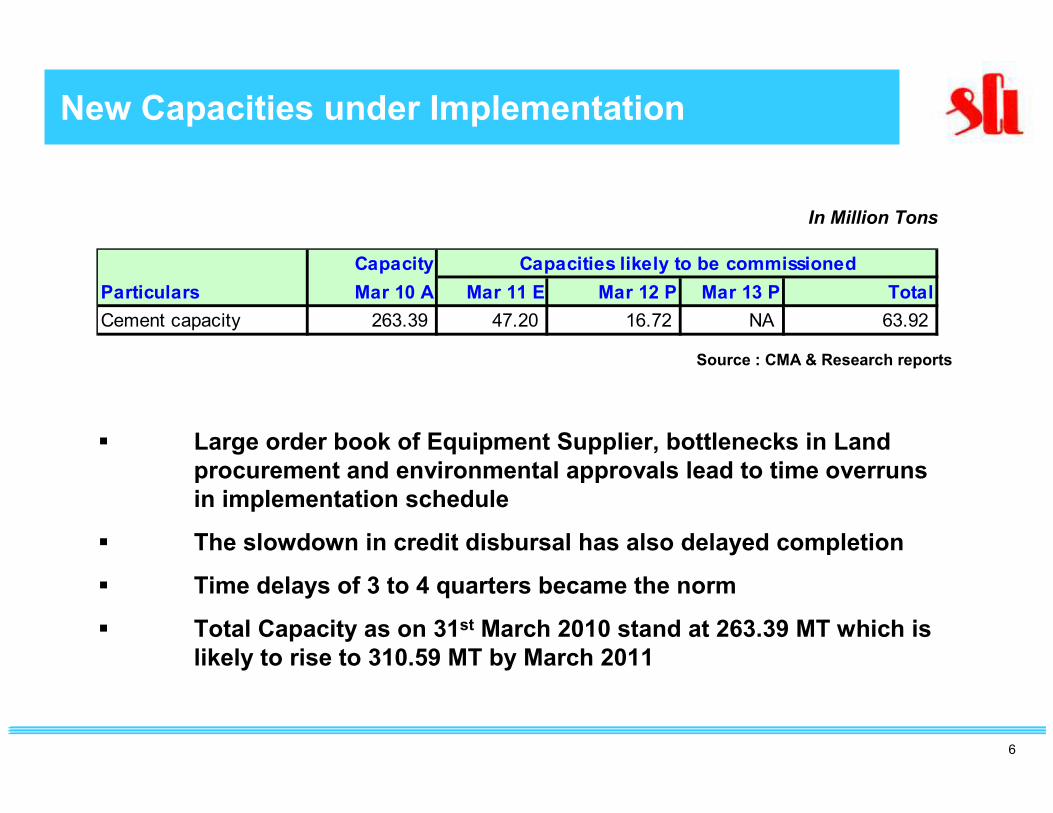

New Capacities under Implementation

� Large order book of Equipment Supplier, bottlenecks in Land

procurement and environmental approvals lead to time overruns

in implementation schedule

� The slowdown in credit disbursal has also delayed completion

� Time delays of 3 to 4 quarters became the norm

� Total Capacity as on 31st March 2010 stand at 263.39 MT which is

likely to rise to 310.59 MT by March 2011

In Million Tons

Capacity

Particulars Mar 10 A Mar 11 E Mar 12 P Mar 13 P Total

Cement capacity 263.39 47.20 16.72 NA 63.92

Capacities likely to be commissioned

Source : CMA & Research reports

7

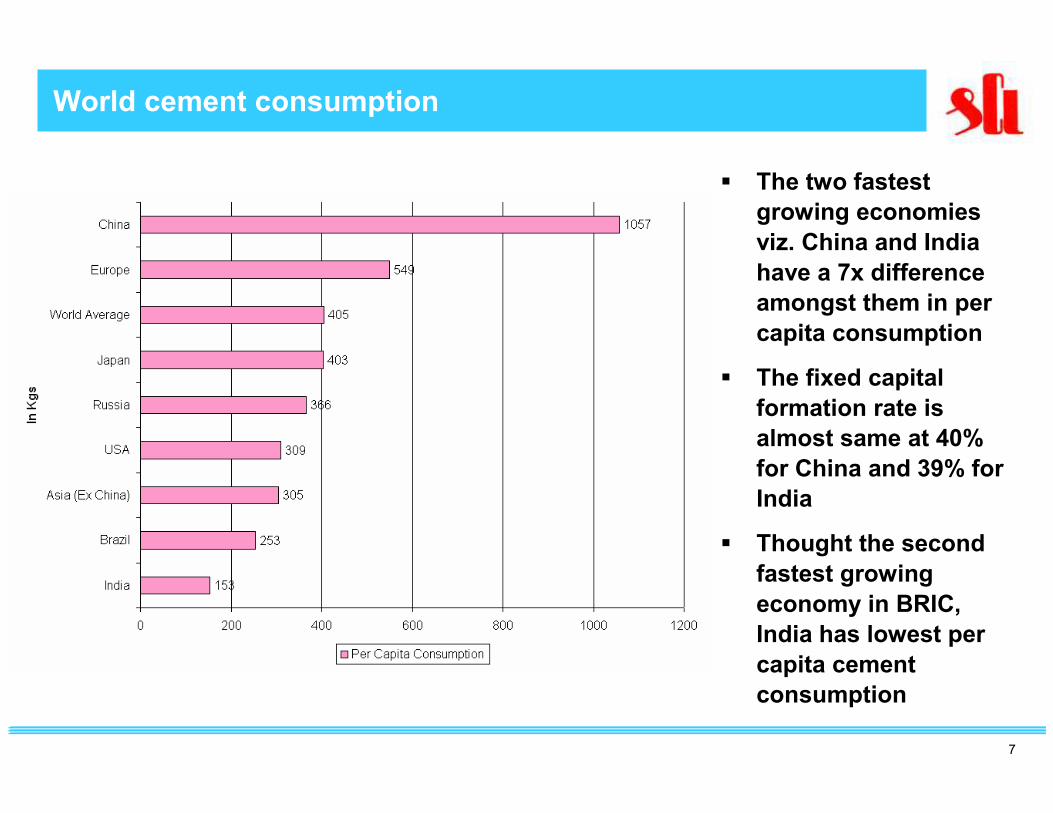

World cement consumption

Sorce : Indepensdent Economic survey reports

� The two fastest

growing economies

viz. China and India

have a 7x difference

amongst them in per

capita consumption

� The fixed capital

formation rate is

almost same at 40%

for China and 39% for

India

� Thought the second

fastest growing

economy in BRIC,

India has lowest per

capita cement

consumption

8

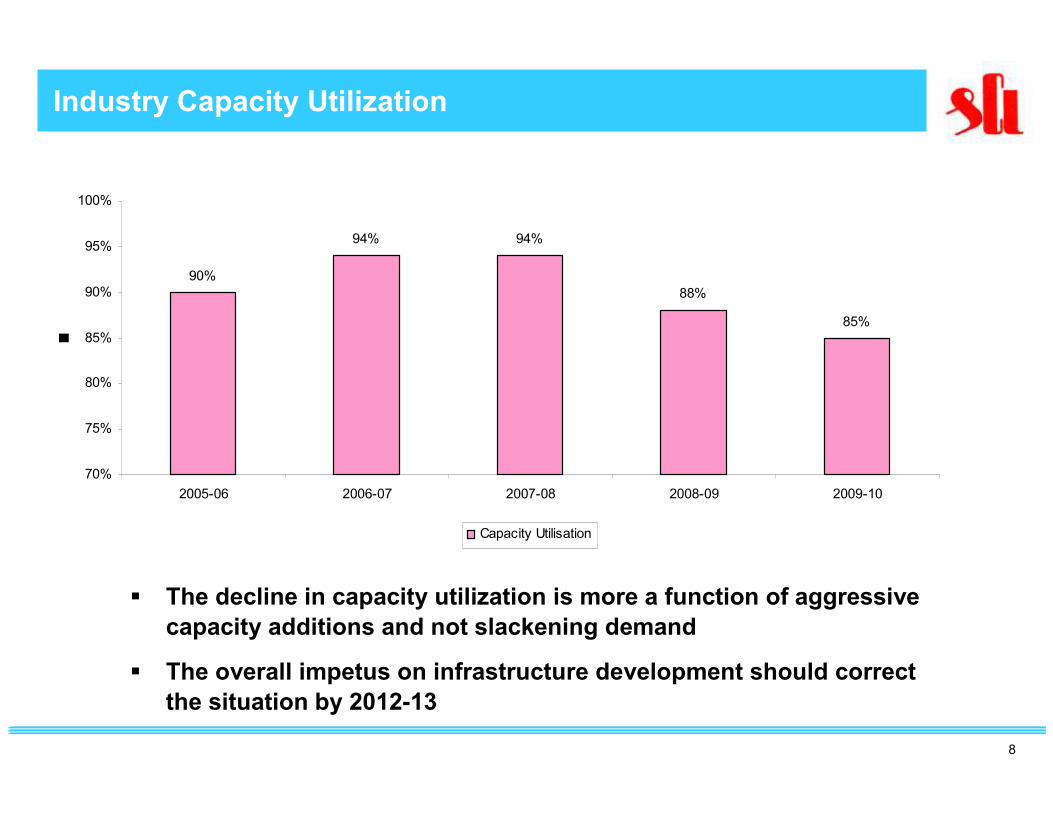

Industry Capacity Utilization

90%

94% 94%

88%

85%

70%

75%

80%

85%

90%

95%

100%

2005-06 2006-07 2007-08 2008-09 2009-10

Capacity Utilisation

� The decline in capacity utilization is more a function of aggressive

capacity additions and not slackening demand

� The overall impetus on infrastructure development should correct

the situation by 2012-13

9

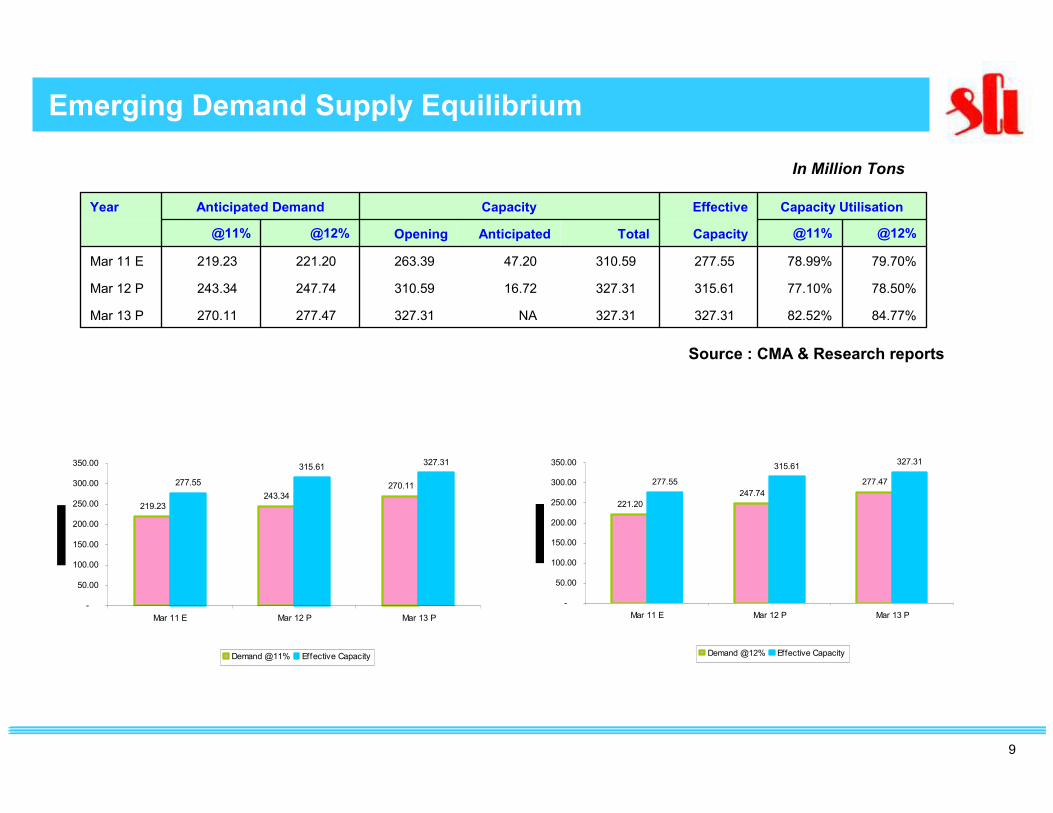

Emerging Demand Supply Equilibrium

In Million Tons

Source : CMA & Research reports

84.77%82.52%327.31 327.31 NA 327.31 277.47 270.11 Mar 13 P

78.50%77.10%315.61 327.31 16.72 310.59 247.74 243.34 Mar 12 P

79.70%78.99%277.55 310.59 47.20 263.39 221.20 219.23 Mar 11 E

@12%@11%CapacityTotalAnticipatedOpening@12%@11%

Capacity UtilisationEffective CapacityAnticipated DemandYear

221.20

247.74

277.47277.55

315.61327.31

-

50.00

100.00

150.00

200.00

250.00

300.00

350.00

Mar 11 E Mar 12 P Mar 13 P

Demand @12% Effective Capacity

219.23

243.34

270.11277.55

315.61327.31

-

50.00

100.00

150.00

200.00

250.00

300.00

350.00

Mar 11 E Mar 12 P Mar 13 P

Demand @11% Effective Capacity

10

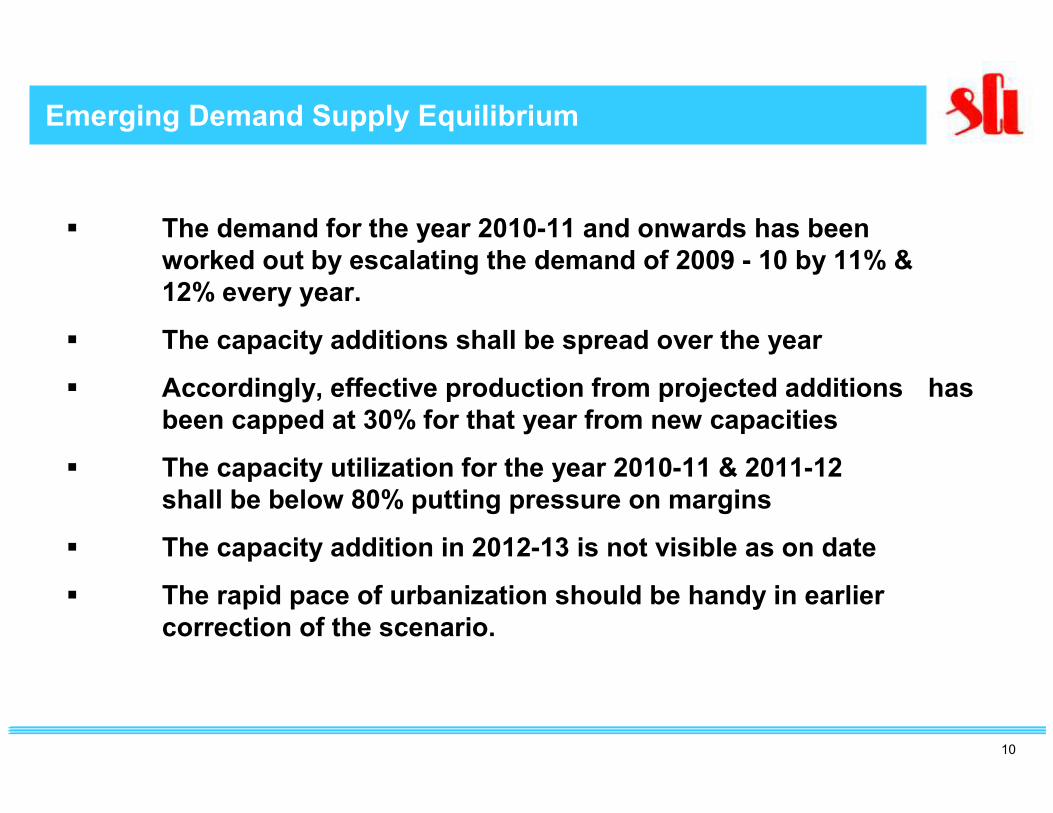

Emerging Demand Supply Equilibrium

� The demand for the year 2010-11 and onwards has been

worked out by escalating the demand of 2009 - 10 by 11% &

12% every year.

� The capacity additions shall be spread over the year

� Accordingly, effective production from projected additions has

been capped at 30% for that year from new capacities

� The capacity utilization for the year 2010-11 & 2011-12

shall be below 80% putting pressure on margins

� The capacity addition in 2012-13 is not visible as on date

� The rapid pace of urbanization should be handy in earlier

correction of the scenario.

11

Shree Cement Limited

12

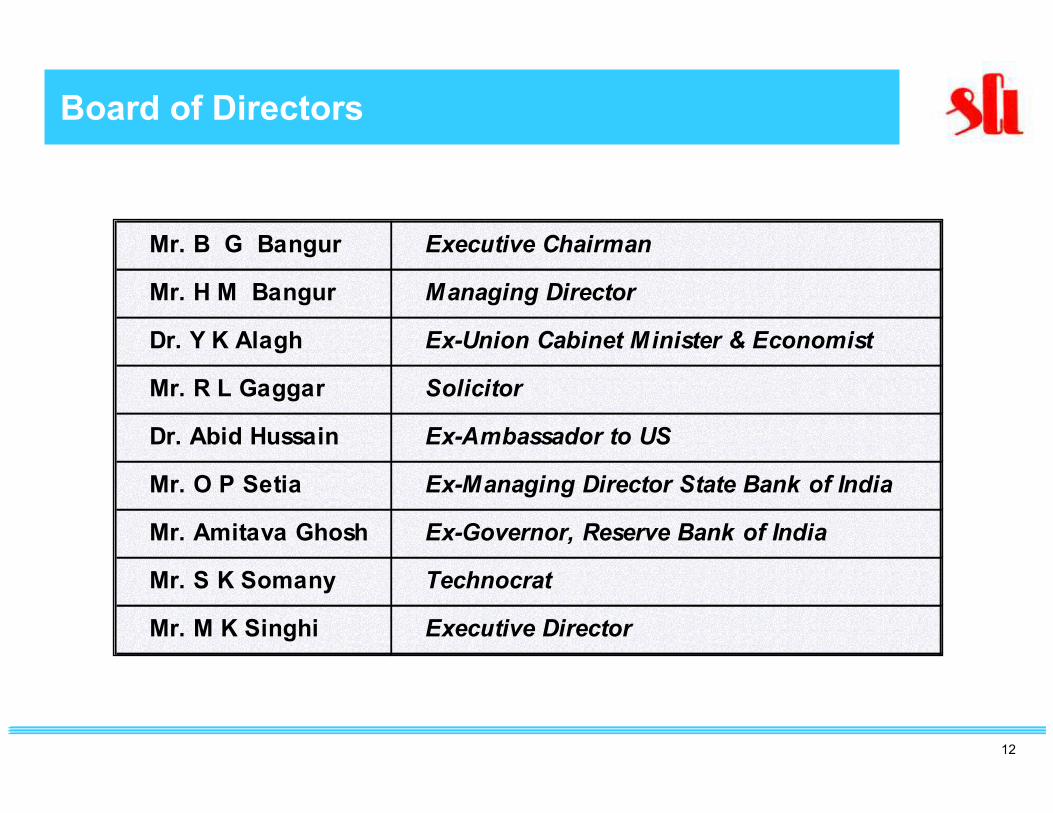

Mr. B G Bangur Executive Chairman

Mr. H M Bangur Managing Director

Dr. Y K Alagh Ex-Union Cabinet Minister & Economist

Mr. R L Gaggar Solicitor

Dr. Abid Hussain Ex-Ambassador to US

Mr. O P Setia Ex-Managing Director State Bank of India

Mr. Amitava Ghosh Ex-Governor, Reserve Bank of India

Mr. S K Somany Technocrat

Mr. M K Singhi Executive Director

Shree – Professionally ManagedBoard of Directors

13

Shree - Awards & Recognition received in 2009-10

� First prize for National Energy conservation by bureau of Energy, Ministry of Power

� National award for excellence in water management 2009 by Confideration of Indian Industries (CII)

� CII Energy Efficiency Award

� NCCBM Award for best Quality Excellence

� Golden peacock award for Climate Security

� Certificate of Excellence by Employer Association of Rajasthan for Best Employer in Large Industry segment

� Commendation certificate for strong commitment for sustainability by CII

� Polycom Intelligent Enterprise Award for the Indian Manufacturing & General Industries Segment

H. E. Pratibha Patil, Hon’ble President of India

presenting Award for Energy Conservation

to Mr. H. M. Bangur, Managing Director

14

Shree - IRR to ShareholdersShree – International Accredition

� International Cement Consultants Whitehopleman (UK) have

been rating cement plants on various operating parameters

� Shree Cement since 2000 is scoring 20 out of maximum of 25

and rated as a Four Star Cement Plant manifesting upper quartile

performance.

� Whitehopleman 2008 report states

“Shree Cement remains one of the best performing cement

companies in the world. This has been the case throughout the 10

years that the company has participated in Whitehopleman’s

benchmarking service. No other cement company has been able to

sustain such standards of performance throughout this period”

� First Process & Cement manufacturing industry in the world to be

awarded BS-EN 16001 - 2009 certification, an Energy Management

System instituted by British Standard Institute - UK

15

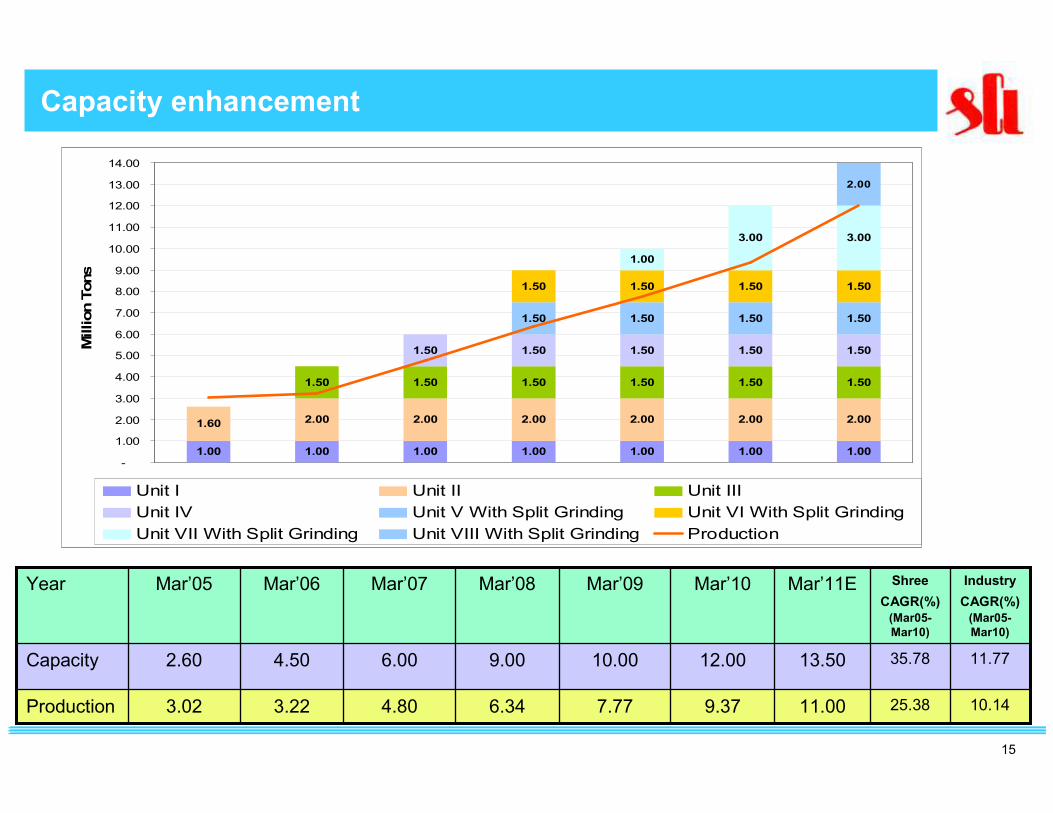

Capacity enhancement

25.38

35.78

Shree

CAGR(%)

(Mar05-

Mar10)

10.14

11.77

Industry

CAGR(%)

(Mar05-

Mar10)

3.02

2.60

Mar’05

3.22

4.50

Mar’06

4.80

6.00

Mar’07

6.34

9.00

Mar’08

7.77

10.00

Mar’09

9.37

12.00

Mar’10

11.00

13.50

Mar’11E

Production

Capacity

Year

1.00 1.00 1.00 1.00 1.00 1.00 1.00

1.60 2.00 2.00 2.00 2.00 2.00 2.00

1.50 1.50 1.50 1.50 1.50 1.50

1.50 1.50 1.50 1.50 1.50

1.50 1.50 1.50 1.50

1.50 1.50 1.50 1.50

1.00

3.00 3.00

2.00

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

12.00

13.00

14.00

Million Tons

Unit I Unit II Unit III

Unit IV Unit V With Split Grinding Unit VI With Split Grinding

Unit VII With Split Grinding Unit VIII With Split Grinding Production

16

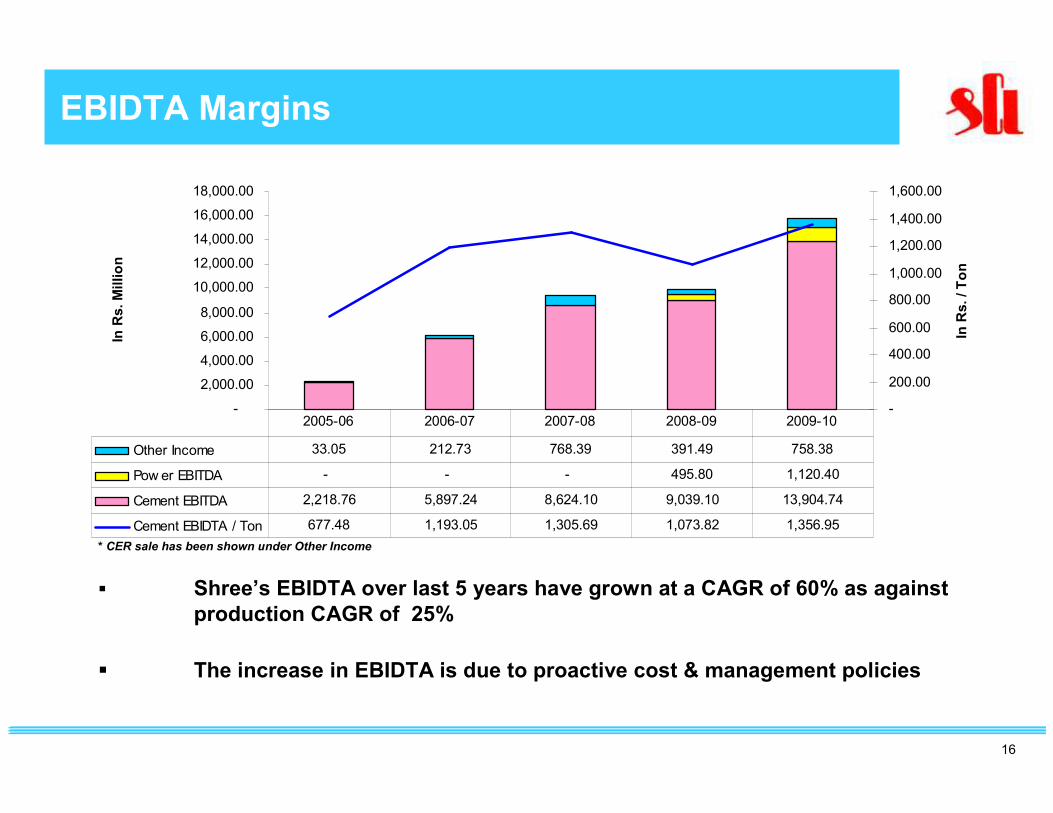

EBIDTA Margins

� Shree’s EBIDTA over last 5 years have grown at a CAGR of 60% as against

production CAGR of 25%

� The increase in EBIDTA is due to proactive cost & management policies

-

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

14,000.00

16,000.00

18,000.00

In Rs. Million

-

200.00

400.00

600.00

800.00

1,000.00

1,200.00

1,400.00

1,600.00

In Rs. / Ton

Other Income 33.05 212.73 768.39 391.49 758.38

Pow er EBITDA - - - 495.80 1,120.40

Cement EBITDA 2,218.76 5,897.24 8,624.10 9,039.10 13,904.74

Cement EBIDTA / Ton 677.48 1,193.05 1,305.69 1,073.82 1,356.95

2005-06 2006-07 2007-08 2008-09 2009-10

* CER sale has been shown under Other Income

17

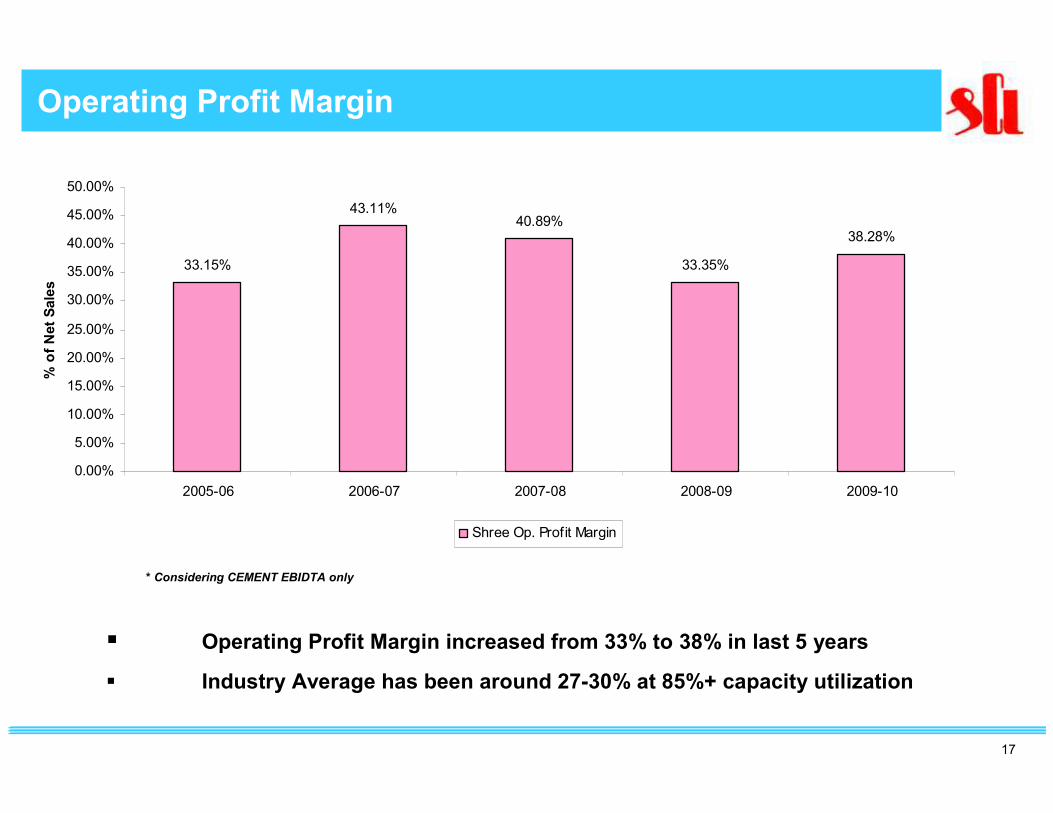

Operating Profit Margin

� Operating Profit Margin increased from 33% to 38% in last 5 years

� Industry Average has been around 27-30% at 85%+ capacity utilization

* Considering CEMENT EBIDTA only

33.15%

43.11%40.89%

33.35%

38.28%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

2005-06 2006-07 2007-08 2008-09 2009-10

% of Net Sales

Shree Op. Profit Margin

18

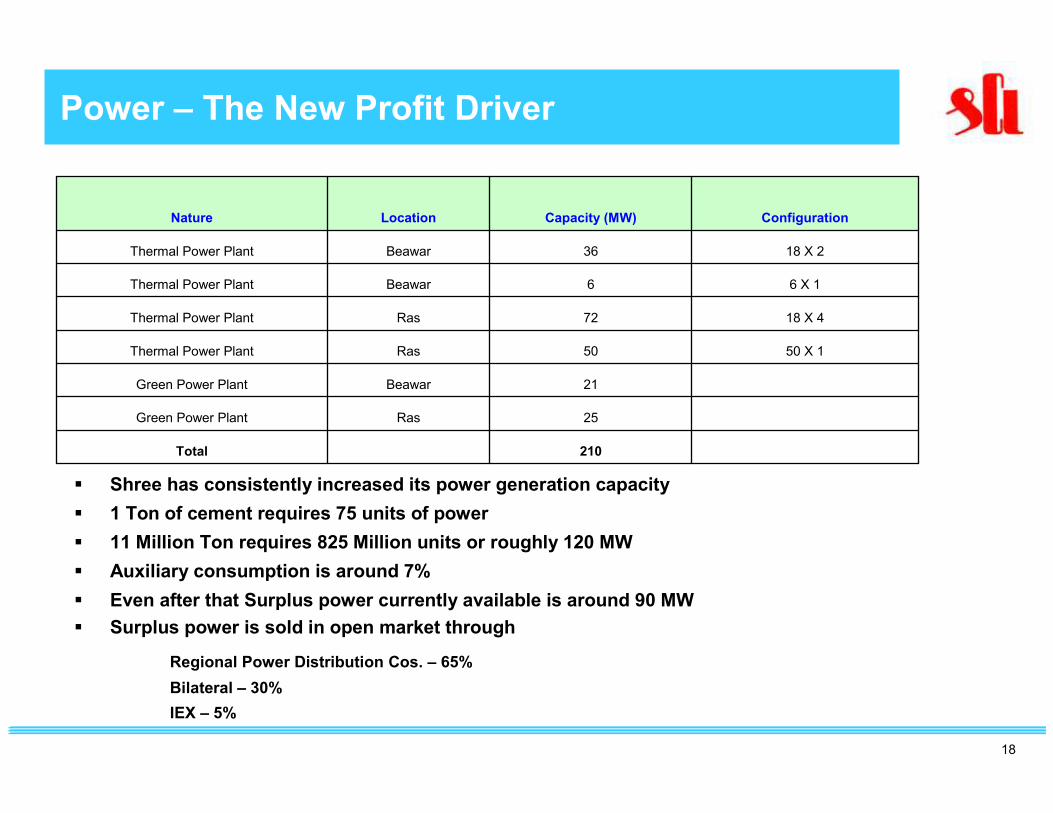

Power – The New Profit Driver

� Shree has consistently increased its power generation capacity

� 1 Ton of cement requires 75 units of power

� 11 Million Ton requires 825 Million units or roughly 120 MW

� Auxiliary consumption is around 7%

� Even after that Surplus power currently available is around 90 MW

� Surplus power is sold in open market through

Regional Power Distribution Cos. – 65%

Bilateral – 30%

IEX – 5%

210Total

25RasGreen Power Plant

21BeawarGreen Power Plant

50 X 150RasThermal Power Plant

18 X 472RasThermal Power Plant

6 X 16BeawarThermal Power Plant

18 X 236BeawarThermal Power Plant

ConfigurationCapacity (MW)LocationNature

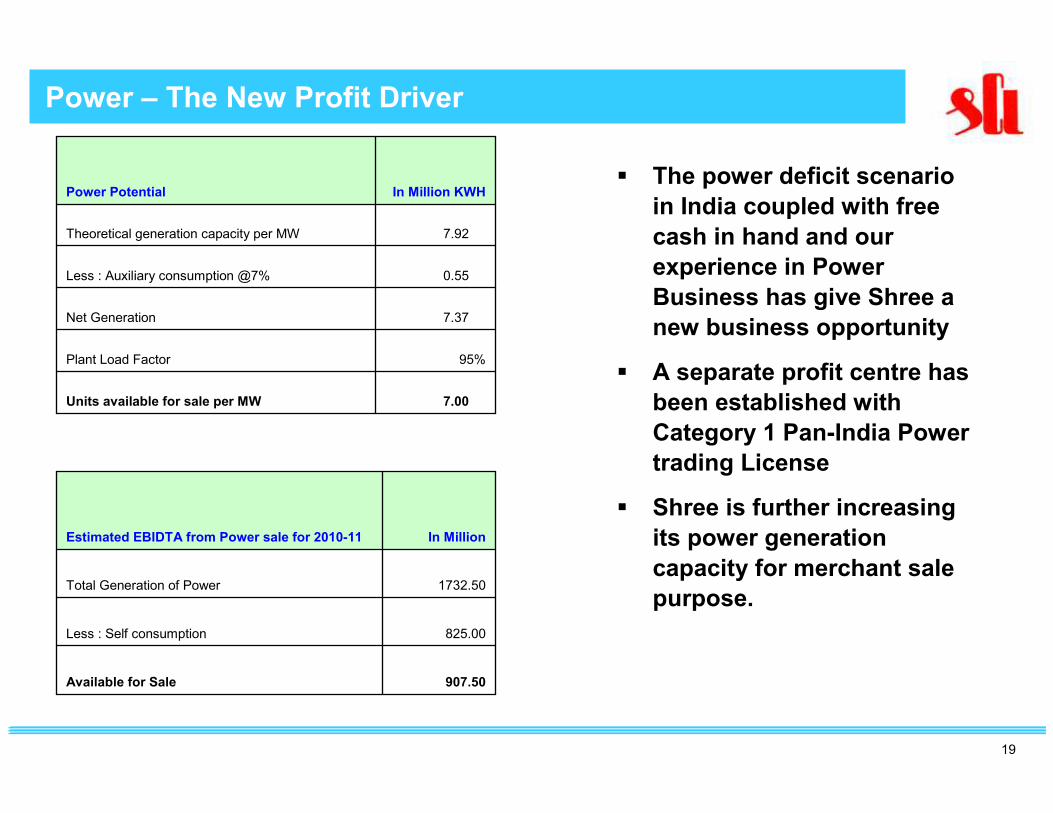

19

Power – The New Profit Driver

7.00 Units available for sale per MW

95%Plant Load Factor

7.37 Net Generation

0.55 Less : Auxiliary consumption @7%

7.92 Theoretical generation capacity per MW

In Million KWHPower Potential

907.50Available for Sale

825.00Less : Self consumption

1732.50Total Generation of Power

In MillionEstimated EBIDTA from Power sale for 2010-11

� The power deficit scenario

in India coupled with free

cash in hand and our

experience in Power

Business has give Shree a

new business opportunity

� A separate profit centre has

been established with

Category 1 Pan-India Power

trading License

� Shree is further increasing

its power generation

capacity for merchant sale

purpose.

20

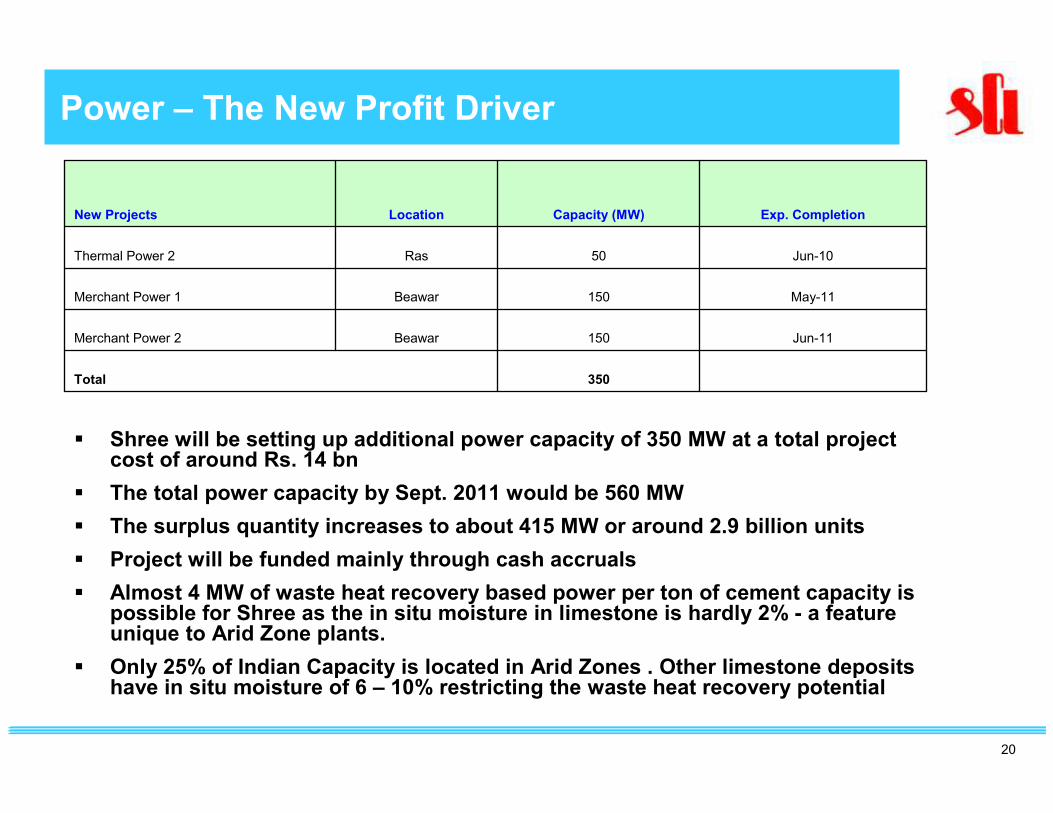

Power – The New Profit Driver

� Shree will be setting up additional power capacity of 350 MW at a total project cost of around Rs. 14 bn

� The total power capacity by Sept. 2011 would be 560 MW

� The surplus quantity increases to about 415 MW or around 2.9 billion units

� Project will be funded mainly through cash accruals

� Almost 4 MW of waste heat recovery based power per ton of cement capacity is possible for Shree as the in situ moisture in limestone is hardly 2% - a feature unique to Arid Zone plants.

� Only 25% of Indian Capacity is located in Arid Zones . Other limestone deposits have in situ moisture of 6 – 10% restricting the waste heat recovery potential

350Total

Jun-11150BeawarMerchant Power 2

May-11150BeawarMerchant Power 1

Jun-1050RasThermal Power 2

Exp. CompletionCapacity (MW)LocationNew Projects

21

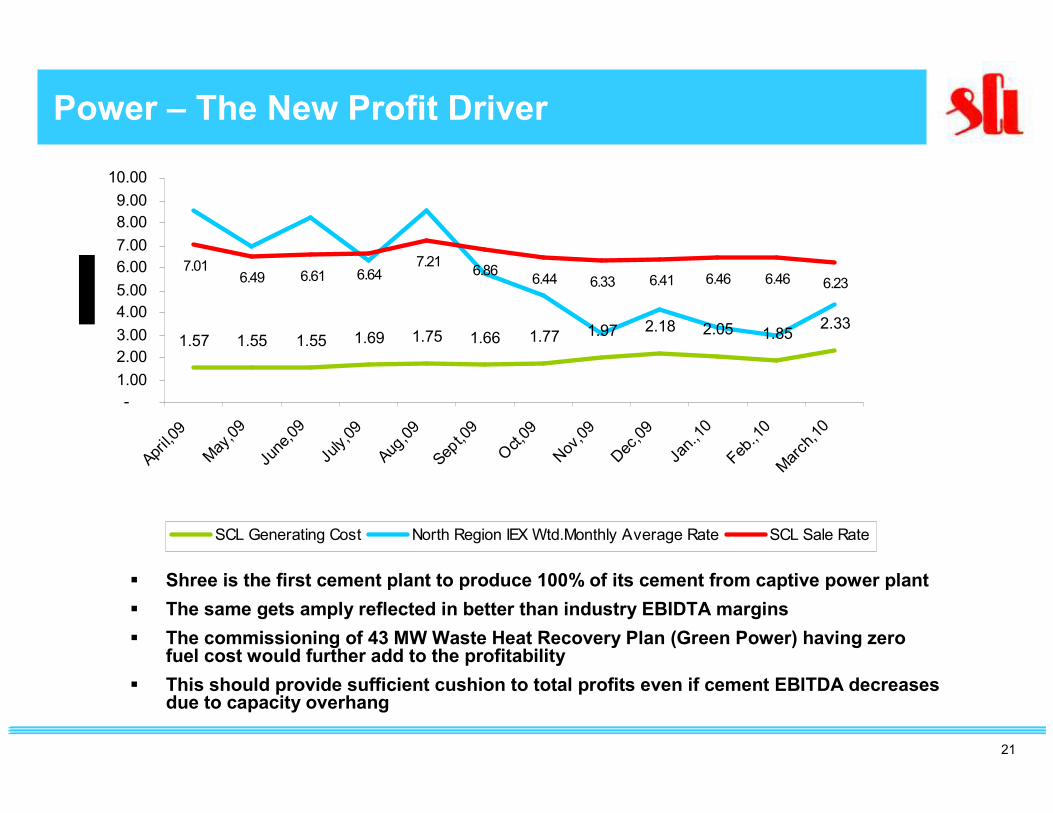

Power – The New Profit Driver

� Shree is the first cement plant to produce 100% of its cement from captive power plant

� The same gets amply reflected in better than industry EBIDTA margins

� The commissioning of 43 MW Waste Heat Recovery Plan (Green Power) having zero fuel cost would further add to the profitability

� This should provide sufficient cushion to total profits even if cement EBITDA decreases due to capacity overhang

1.57 1.55 1.55 1.69 1.75 1.66 1.77 1.97 2.18 2.05 1.852.33

7.016.49 6.61 6.64

7.216.86

6.44 6.33 6.41 6.46 6.46 6.23

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

April

,09

May

,09

June

,09

July

,09

Aug,

09

Sept

,09

Oct

,09

Nov

,09

Dec

,09

Jan.

,10

Feb.

,10

Mar

ch,1

0

SCL Generating Cost North Region IEX Wtd.Monthly Average Rate SCL Sale Rate

22

Power – The New Profit Driver

� Low efficiency boilers have been chosen by Shree to:

� Reduce the capital cost of the power plants

� To recover full fuel content of the fuel by using its ash in the cement

kilns

� High efficiency boilers leave 8 – 10% un - burnt carbon whereas low

efficiency boiler leave around 30%

� Low un-burnt carbon ash cannot be used in the cement kiln and go

waste

� Seven boilers have already been commissioned. The eighth and ninth

boiler along with boilers for the two 150 MW shall all be AFBC & CFBC

type to have flexibility of using all kinds of fuel including agri / tyre

wastes - an emerging trend in India.

23

Higher Profitability due to :

A Use of Alternate Fuel (Pet Coke)

B Market Strategy

C Logistic Advantage

D Split Grinding Location

E Own Railway Siding

F Human Resources

24

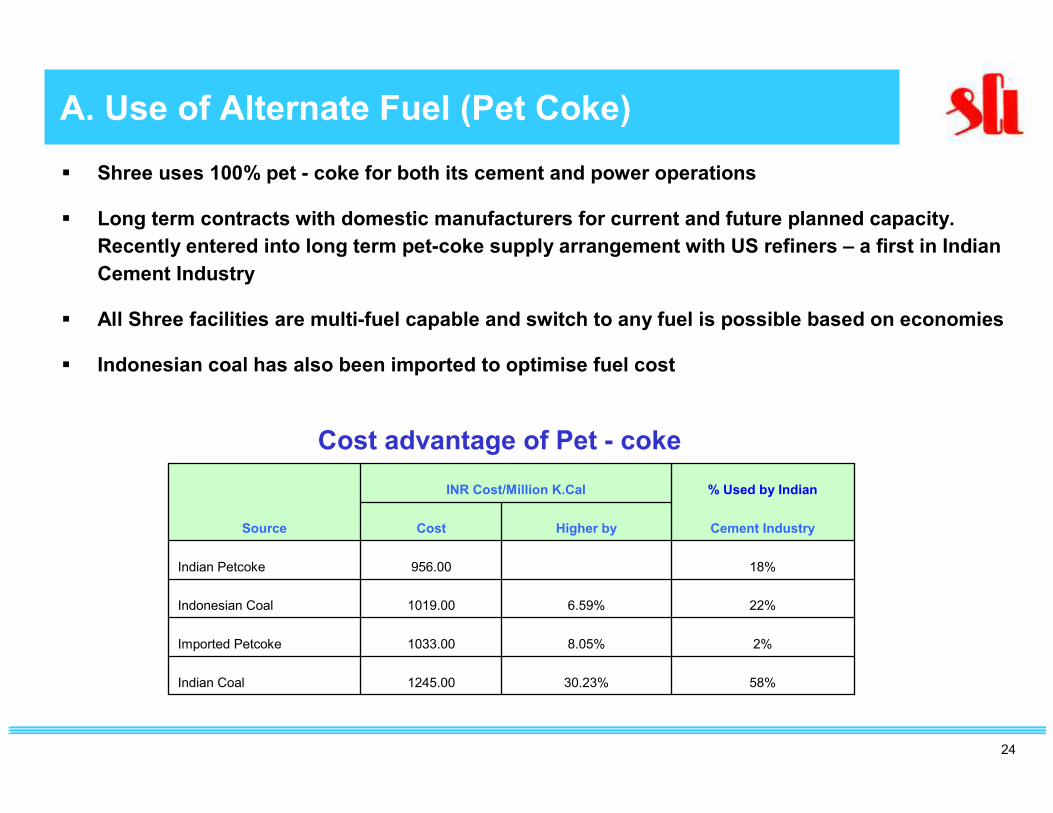

A. Use of Alternate Fuel (Pet Coke)

� Shree uses 100% pet - coke for both its cement and power operations

� Long term contracts with domestic manufacturers for current and future planned capacity.

Recently entered into long term pet-coke supply arrangement with US refiners – a first in Indian

Cement Industry

� All Shree facilities are multi-fuel capable and switch to any fuel is possible based on economies

� Indonesian coal has also been imported to optimise fuel cost

Cost advantage of Pet - coke

58%30.23%1245.00Indian Coal

2%8.05%1033.00Imported Petcoke

22%6.59%1019.00Indonesian Coal

18%956.00Indian Petcoke

Cement IndustryHigher byCostSource

% Used by IndianINR Cost/Million K.Cal

25

E. Branding Strategy

� Multiple brands created to capture market share as our

entire production is in the same area

� It helps in retaining more number of dealers / retailers

thereby making the supply chain very powerful

B. Market Strategy

26

F. Logistic Advantage

Shree Plants

Other Cement Plants

Cement Grinding Plants

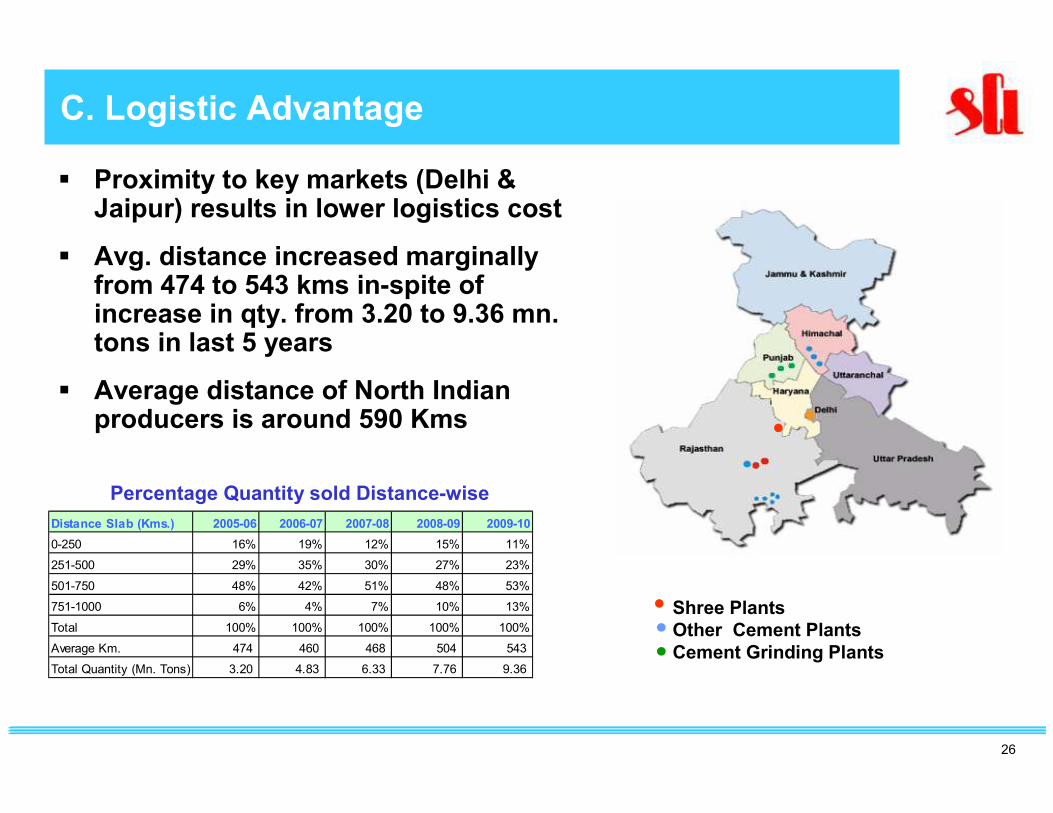

C. Logistic Advantage

� Proximity to key markets (Delhi & Jaipur) results in lower logistics cost

� Avg. distance increased marginally from 474 to 543 kms in-spite of increase in qty. from 3.20 to 9.36 mn. tons in last 5 years

� Average distance of North Indian producers is around 590 Kms

Percentage Quantity sold Distance-wise

Distance Slab (Kms.) 2005-06 2006-07 2007-08 2008-09 2009-10

0-250 16% 19% 12% 15% 11%

251-500 29% 35% 30% 27% 23%

501-750 48% 42% 51% 48% 53%

751-1000 6% 4% 7% 10% 13%

Total 100% 100% 100% 100% 100%

Average Km. 474 460 468 504 543

Total Quantity (Mn. Tons) 3.20 4.83 6.33 7.76 9.36

27

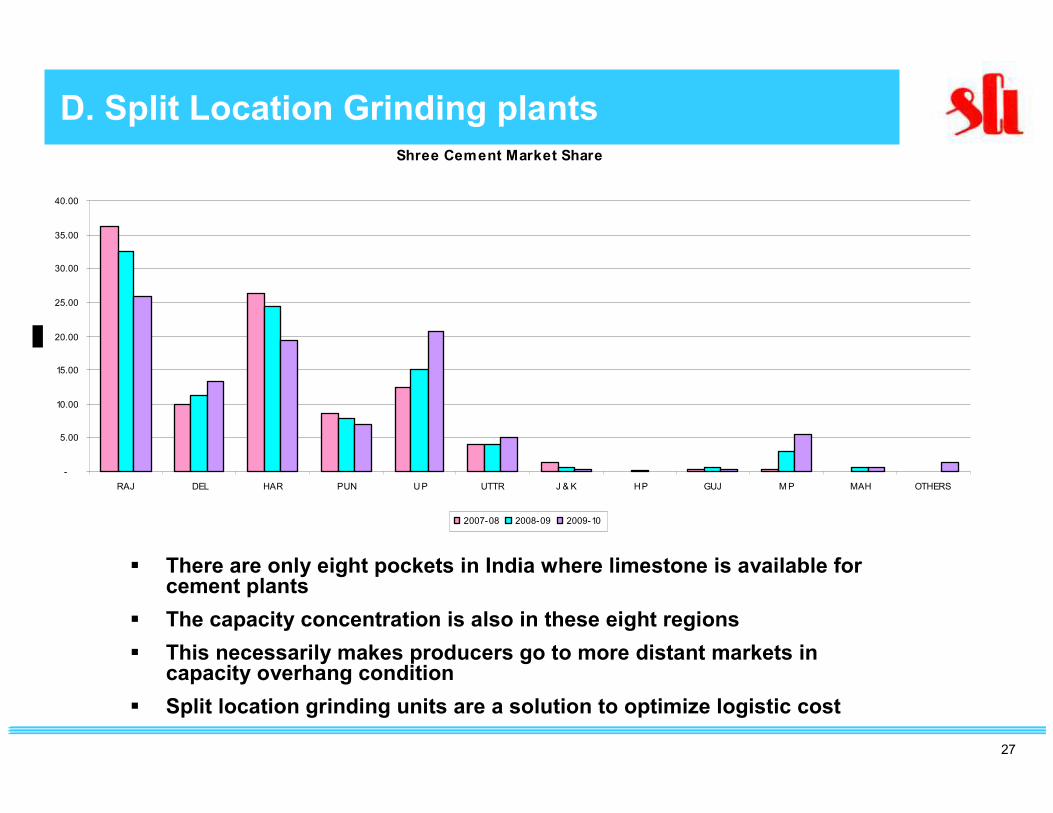

F. Logistic AdvantageD. Split Location Grinding plantsShree Cement Market Share

-

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

RAJ DEL HAR PUN U P UTTR J & K H P GUJ M P MAH OTHERS

2007-08 2008-09 2009-10

� There are only eight pockets in India where limestone is available for cement plants

� The capacity concentration is also in these eight regions

� This necessarily makes producers go to more distant markets in capacity overhang condition

� Split location grinding units are a solution to optimize logistic cost

28

4

6

12

3

5

PRESENT

6

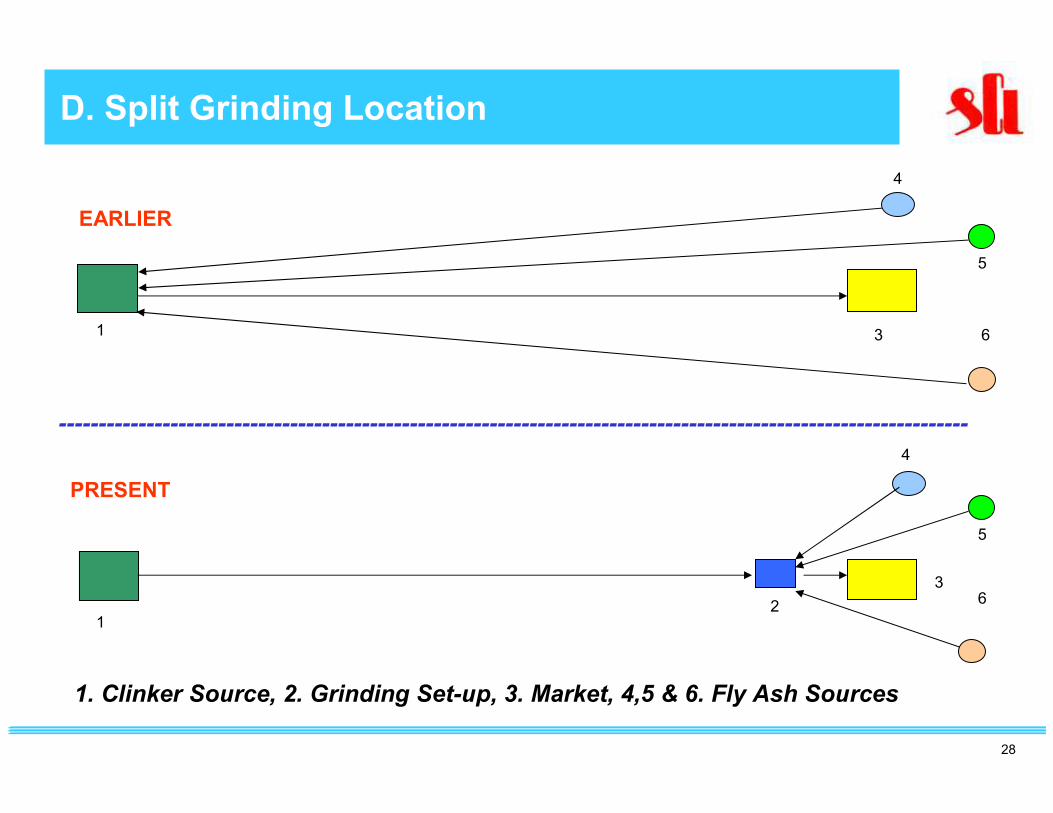

D. Split Grinding Location

4

4

3

5

1

EARLIER

6

------------------------------------------------------------------------------------------------------------------

1. Clinker Source, 2. Grinding Set-up, 3. Market, 4,5 & 6. Fly Ash Sources

29

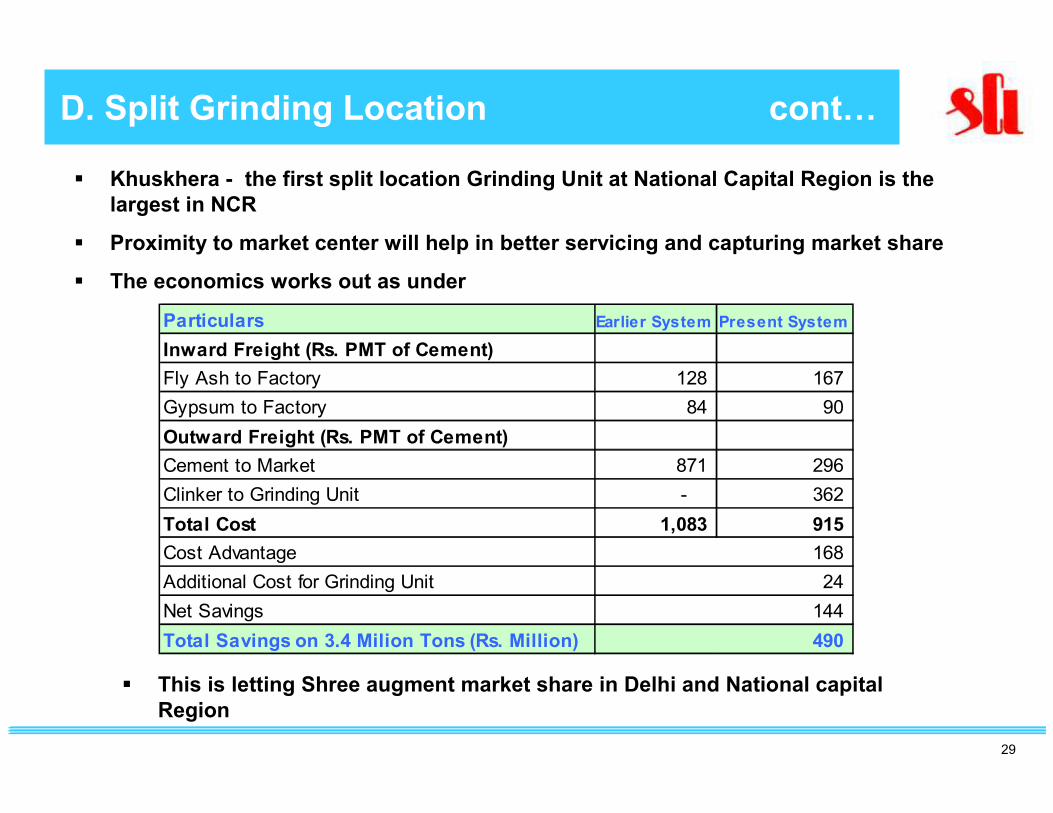

D. Split Grinding Location cont…

� Khuskhera - the first split location Grinding Unit at National Capital Region is the

largest in NCR

� Proximity to market center will help in better servicing and capturing market share

� The economics works out as under

Particulars Earlier System Present System

Inward Freight (Rs. PMT of Cement)

Fly Ash to Factory 128 167

Gypsum to Factory 84 90

Outward Freight (Rs. PMT of Cement)

Cement to Market 871 296

Clinker to Grinding Unit - 362

Total Cost 1,083 915

Cost Advantage

Additional Cost for Grinding Unit

Net Savings

Total Savings on 3.4 Milion Tons (Rs. Million)

168

24

144

490

� This is letting Shree augment market share in Delhi and National capital

Region

30

D. Split Grinding Location cont…

• Three new grinding units were taken up for implementation:

I. 1.2 million ton at Suratgarh has been commissioned

II. 1.8 Million ton at Roorkee has been commissioned

III. 1.5 million ton at Jaipur shall be commissioned in Q3 FY 11

� Suratgarh shall give logistic advantage for Punjab & Haryana

� Roorkee shall be beneficial for Uttararnchal and Uttar Pradesh. It

also gives some fiscal beneits like:

� 100% Excise duty exemption for a period of 10 years

� 100% Income Tax exemption for a period of initial 5 years

� Therafter 30% exemption for a further period of 5 years

� The Jaipur Grinding plant shall cater to Rajasthan market

� This should further increase the market share of the company

31

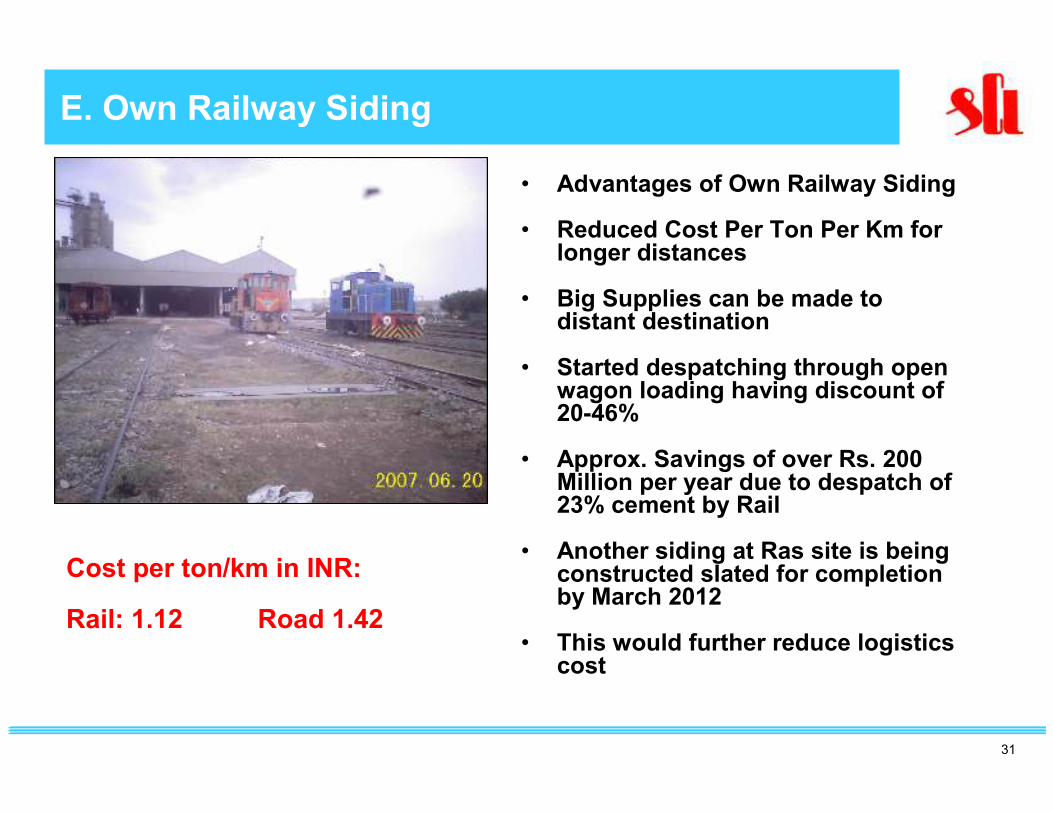

E. Own Railway Siding

• Advantages of Own Railway Siding

• Reduced Cost Per Ton Per Km for longer distances

• Big Supplies can be made to distant destination

• Started despatching through open wagon loading having discount of 20-46%

• Approx. Savings of over Rs. 200 Million per year due to despatch of 23% cement by Rail

• Another siding at Ras site is being constructed slated for completion by March 2012

• This would further reduce logistics cost

Cost per ton/km in INR:

Rail: 1.12 Road 1.42

32

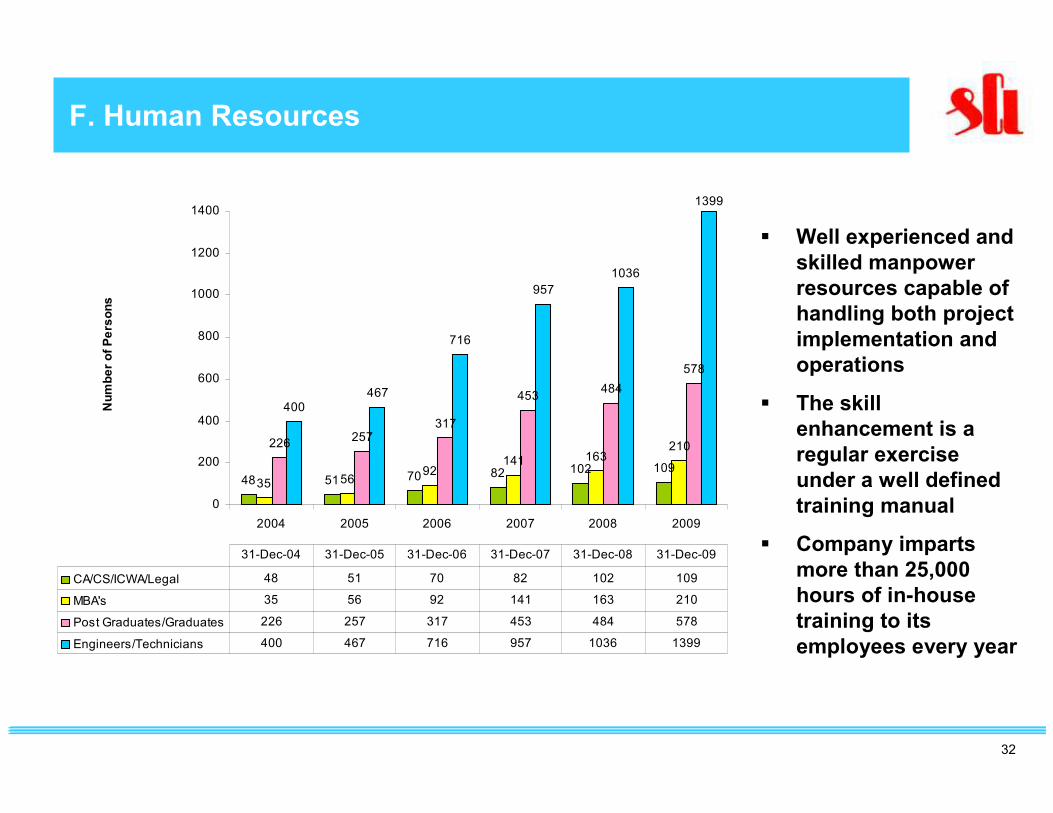

F. Human Resources

� Well experienced and

skilled manpower

resources capable of

handling both project

implementation and

operations

� The skill

enhancement is a

regular exercise

under a well defined

training manual

� Company imparts

more than 25,000

hours of in-house

training to its

employees every year

48 51 70 82 102 109

35 5692

141 163210226

257317

453484

578

400467

716

957

1036

1399

0

200

400

600

800

1000

1200

1400

2004 2005 2006 2007 2008 2009

Number of Persons

CA/CS/ICWA/Legal 48 51 70 82 102 109

MBA's 35 56 92 141 163 210

Post Graduates/Graduates 226 257 317 453 484 578

Engineers/Technicians 400 467 716 957 1036 1399

31-Dec-04 31-Dec-05 31-Dec-06 31-Dec-07 31-Dec-08 31-Dec-09

33

Shree Cement – Financial Section

34

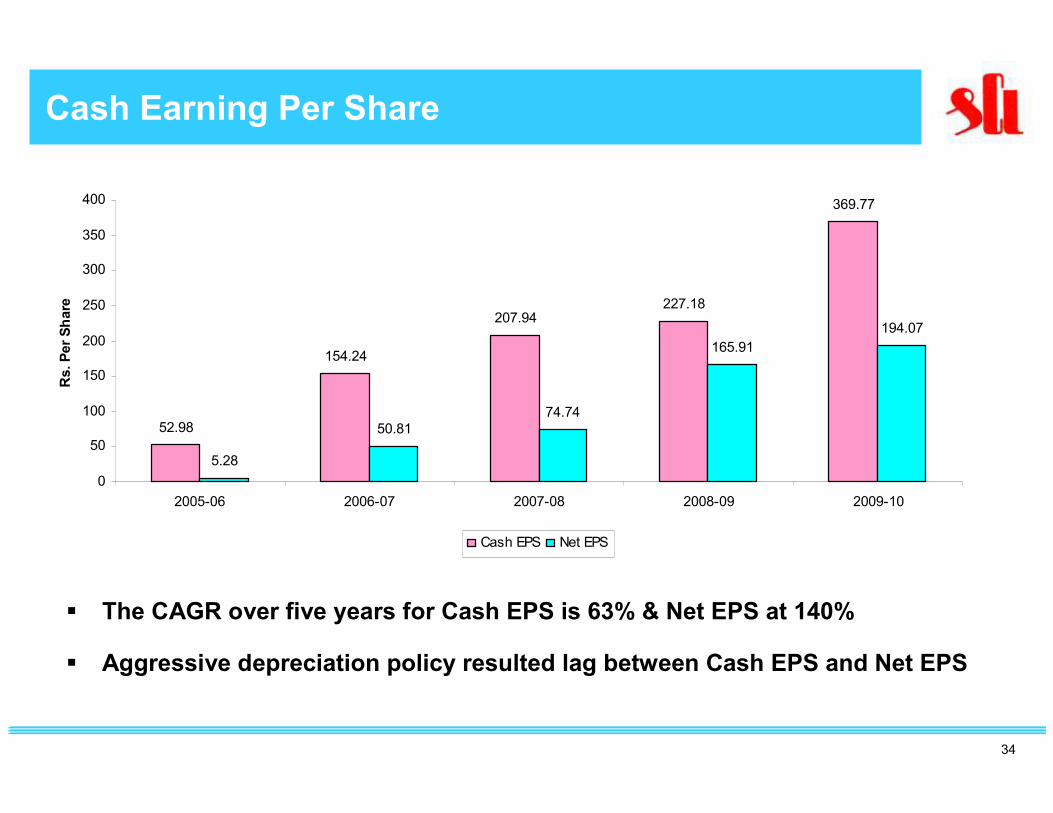

Cash Earning Per Share

� The CAGR over five years for Cash EPS is 63% & Net EPS at 140%

� Aggressive depreciation policy resulted lag between Cash EPS and Net EPS

52.98

154.24

207.94227.18

369.77

5.28

50.81

74.74

165.91

194.07

0

50

100

150

200

250

300

350

400

2005-06 2006-07 2007-08 2008-09 2009-10

Rs. Per Share

Cash EPS Net EPS

35

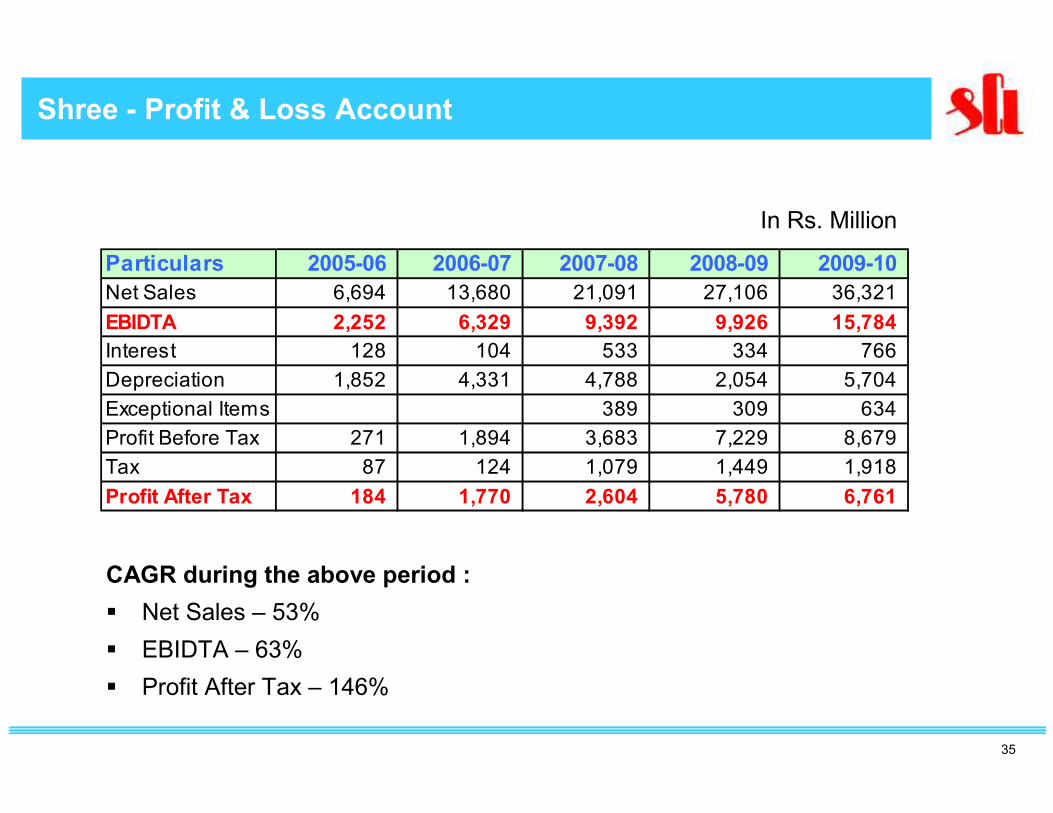

Shree - Profit & Loss Account

In Rs. Million

Particulars 2005-06 2006-07 2007-08 2008-09 2009-10

Net Sales 6,694 13,680 21,091 27,106 36,321

EBIDTA 2,252 6,329 9,392 9,926 15,784

Interest 128 104 533 334 766

Depreciation 1,852 4,331 4,788 2,054 5,704

Exceptional Items 389 309 634

Profit Before Tax 271 1,894 3,683 7,229 8,679

Tax 87 124 1,079 1,449 1,918

Profit After Tax 184 1,770 2,604 5,780 6,761

CAGR during the above period :

� Net Sales – 53%

� EBIDTA – 63%

� Profit After Tax – 146%

36

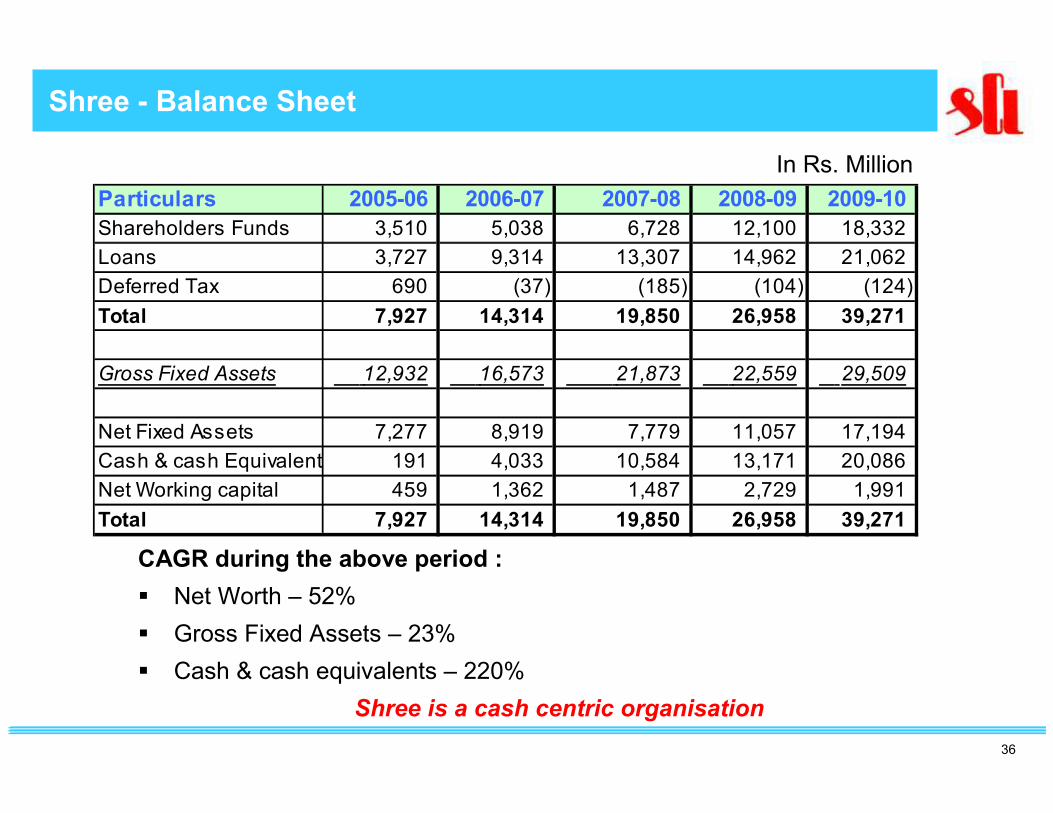

Shree - Balance Sheet

In Rs. Million

Particulars 2005-06 2006-07 2007-08 2008-09 2009-10

Shareholders Funds 3,510 5,038 6,728 12,100 18,332

Loans 3,727 9,314 13,307 14,962 21,062

Deferred Tax 690 (37) (185) (104) (124)

Total 7,927 14,314 19,850 26,958 39,271

Gross Fixed Assets 12,932 16,573 21,873 22,559 29,509

Net Fixed Assets 7,277 8,919 7,779 11,057 17,194

Cash & cash Equivalents 191 4,033 10,584 13,171 20,086

Net Working capital 459 1,362 1,487 2,729 1,991

Total 7,927 14,314 19,850 26,958 39,271

CAGR during the above period :

� Net Worth – 52%

� Gross Fixed Assets – 23%

� Cash & cash equivalents – 220%

Shree is a cash centric organisation

37

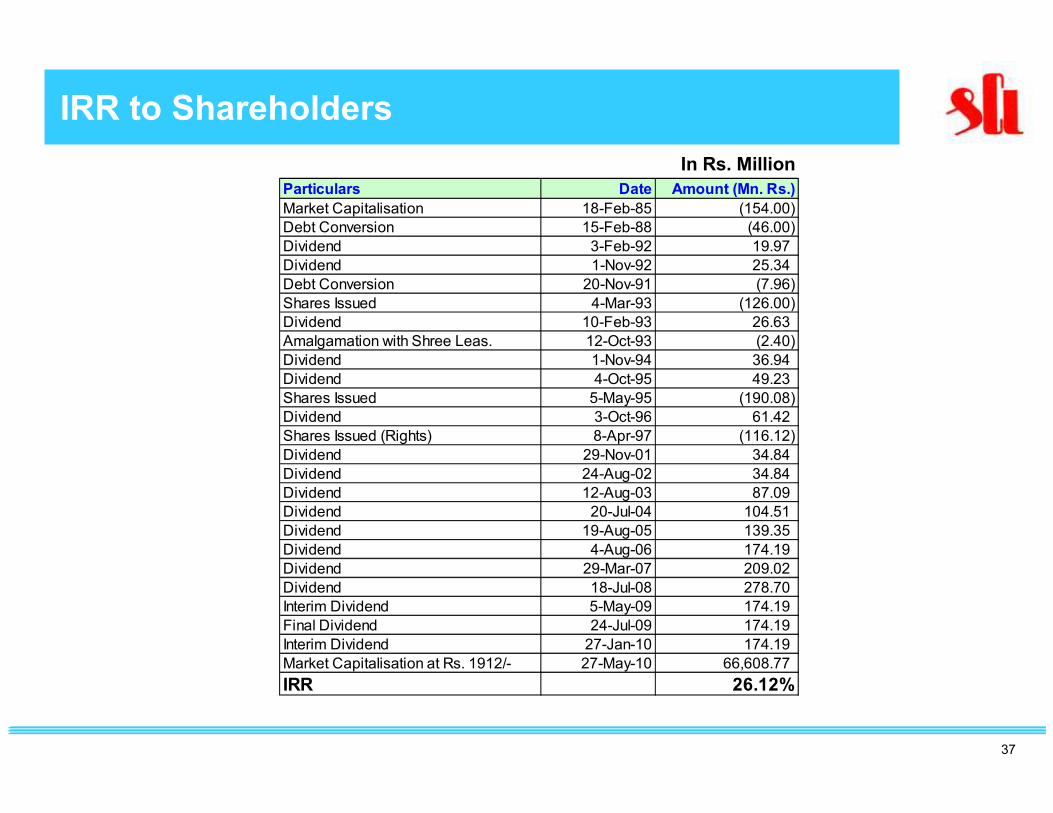

In Rs. Million

Particulars Date Amount (Mn. Rs.)

Market Capitalisation 18-Feb-85 (154.00)

Debt Conversion 15-Feb-88 (46.00)

Dividend 3-Feb-92 19.97

Dividend 1-Nov-92 25.34

Debt Conversion 20-Nov-91 (7.96)

Shares Issued 4-Mar-93 (126.00)

Dividend 10-Feb-93 26.63

Amalgamation with Shree Leas. 12-Oct-93 (2.40)

Dividend 1-Nov-94 36.94

Dividend 4-Oct-95 49.23

Shares Issued 5-May-95 (190.08)

Dividend 3-Oct-96 61.42

Shares Issued (Rights) 8-Apr-97 (116.12)

Dividend 29-Nov-01 34.84

Dividend 24-Aug-02 34.84

Dividend 12-Aug-03 87.09

Dividend 20-Jul-04 104.51

Dividend 19-Aug-05 139.35

Dividend 4-Aug-06 174.19

Dividend 29-Mar-07 209.02

Dividend 18-Jul-08 278.70

Interim Dividend 5-May-09 174.19

Final Dividend 24-Jul-09 174.19

Interim Dividend 27-Jan-10 174.19

Market Capitalisation at Rs. 1912/- 27-May-10 66,608.77

IRR 26.12%

Shree - IRR to ShareholdersIRR to Shareholders

38

Disclaimer

� This presentation contains forward-looking statements which may be identified by their use of words like “plans”, “expects”, “will”, “anticipates”, “believes”, “intends”, “projects”, “estimates” or other words of similar meaning. All statements that address expectations or projections about the future, including, but not limited to, statements about the strategy for growth, product development, market position, expenditures and financial results are forward-looking statements.

� Forward-looking statements are based on certain assumptions and expectations of future events. The company does not guarantee that these assumptions and expectations are accurate or will be realised, The actual results, performance or achievements could thus differ materially form those projected in any such forward-looking statements. The company assumes no responsibility to publicly amend, modify or revise any forward-looking statements, on the basis of any subsequent developments, information or events, or otherwise.

39

Thank You

SHREE CEMENT LIMITED