Lloyd’s Register: Transportation Introducing Lloyd’s Register Transportation.

1

Shipping Tomorrow

Thursday, 29th November 2007

Host: Ince & Co., International House, 1 St Katherine’s Way, London, E1 The seminar is organised by the London Shipping Law Centre (LSLC), Ince & Co. and the British Chamber of Commerce in Germany

Programme 14.25 Welcome by the Chairman of the Event- Jonathan Lux, Partner - Ince & Co., Steering Committee Member of LSLC and BCCG

14.30 Panel Discussion 1 - Malacca Max or More

Panellists: Jesper Kjaedegaard – CEO, The Maersk Co. Ltd. Tim Kent – Manager, Marine Business at Lloyd’s Register Issues:

• The mega-containerships’ future: impact on ports and their

operations

• The perspective of the naval architect in mega - containerships’

structures

Chairman: Jonathan Lux - Partner, Ince & Co.

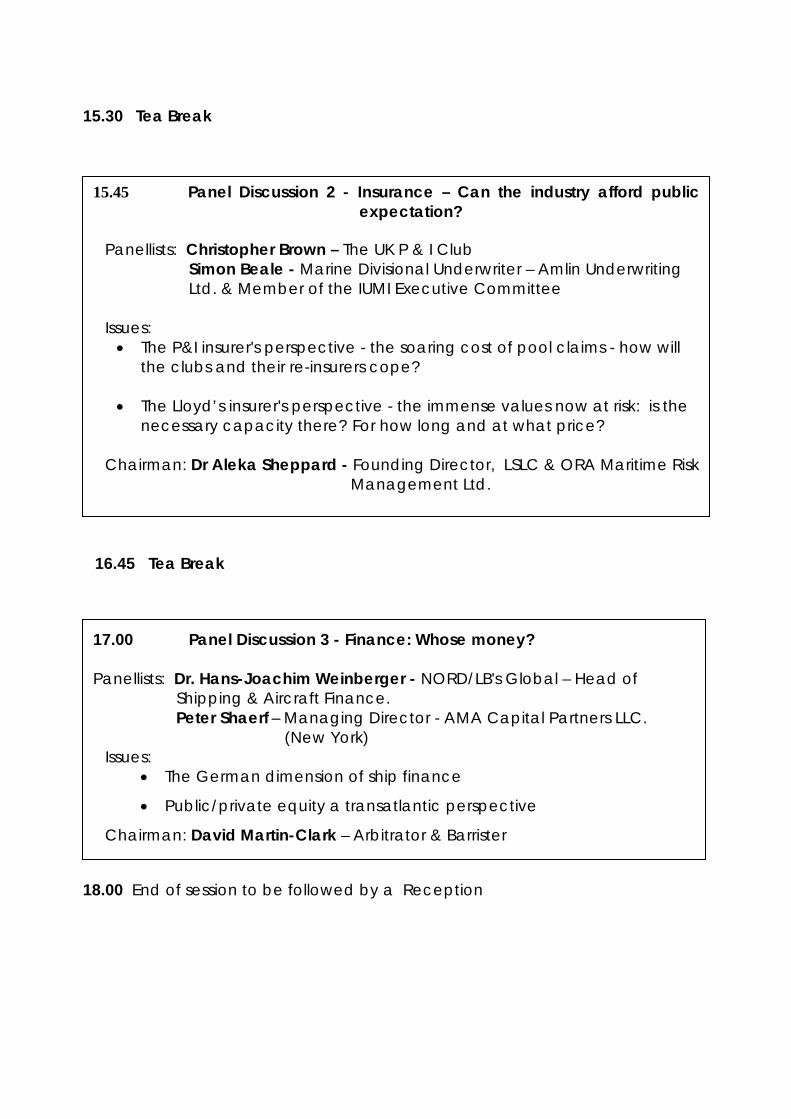

15.30 Tea Break

15.45 Panel Discussion 2 - Insurance – Can the industry afford public expectation?

Panellists: Christopher Brown – The UK P & I Club Simon Beale - Marine Divisional Underwriter – Amlin Underwriting Ltd. & Member of the IUMI Executive Committee Issues: • The P&I insurer's perspective - the soaring cost of pool claims - how will

the clubs and their re-insurers cope? • The Lloyd’s insurer's perspective - the immense values now at risk: is the

necessary capacity there? For how long and at what price?

Chairman: Dr Aleka Sheppard - Founding Director, LSLC & ORA Maritime Risk Management Ltd.

16.45 Tea Break

17.00 Panel Discussion 3 - Finance: Whose money?

Panellists: Dr. Hans-Joachim Weinberger - NORD/LB's Global – Head of Shipping & Aircraft Finance.

Peter Shaerf – Managing Director - AMA Capital Partners LLC. (New York) Issues:

• The German dimension of ship finance

• Public/private equity a transatlantic perspective

Chairman: David Martin-Clark – Arbitrator & Barrister

18.00 End of session to be followed by a Reception

1

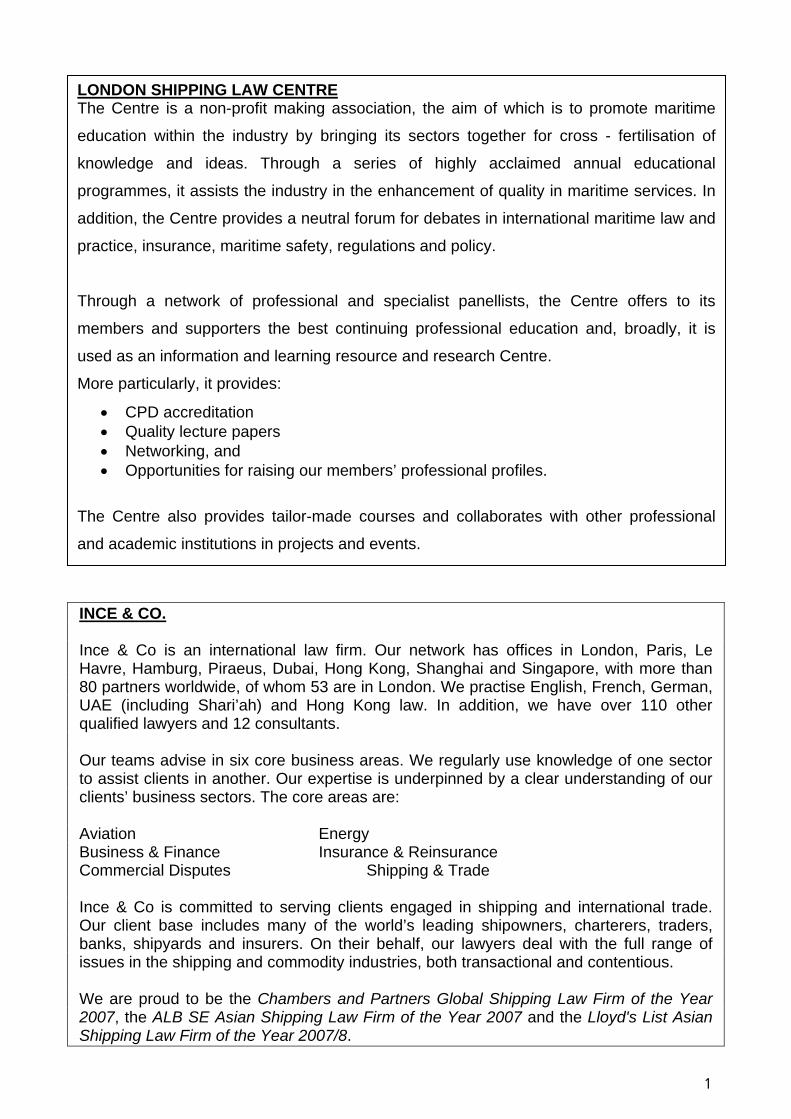

LONDON SHIPPING LAW CENTRE The Centre is a non-profit making association, the aim of which is to promote maritime

education within the industry by bringing its sectors together for cross - fertilisation of

knowledge and ideas. Through a series of highly acclaimed annual educational

programmes, it assists the industry in the enhancement of quality in maritime services. In

addition, the Centre provides a neutral forum for debates in international maritime law and

practice, insurance, maritime safety, regulations and policy.

Through a network of professional and specialist panellists, the Centre offers to its

members and supporters the best continuing professional education and, broadly, it is

used as an information and learning resource and research Centre.

More particularly, it provides:

• CPD accreditation • Quality lecture papers • Networking, and • Opportunities for raising our members’ professional profiles.

The Centre also provides tailor-made courses and collaborates with other professional

and academic institutions in projects and events.

INCE & CO. Ince & Co is an international law firm. Our network has offices in London, Paris, Le Havre, Hamburg, Piraeus, Dubai, Hong Kong, Shanghai and Singapore, with more than 80 partners worldwide, of whom 53 are in London. We practise English, French, German, UAE (including Shari’ah) and Hong Kong law. In addition, we have over 110 other qualified lawyers and 12 consultants. Our teams advise in six core business areas. We regularly use knowledge of one sector to assist clients in another. Our expertise is underpinned by a clear understanding of our clients’ business sectors. The core areas are: Aviation Energy Business & Finance Insurance & Reinsurance Commercial Disputes Shipping & Trade Ince & Co is committed to serving clients engaged in shipping and international trade. Our client base includes many of the world’s leading shipowners, charterers, traders, banks, shipyards and insurers. On their behalf, our lawyers deal with the full range of issues in the shipping and commodity industries, both transactional and contentious. We are proud to be the Chambers and Partners Global Shipping Law Firm of the Year 2007, the ALB SE Asian Shipping Law Firm of the Year 2007 and the Lloyd's List Asian Shipping Law Firm of the Year 2007/8.

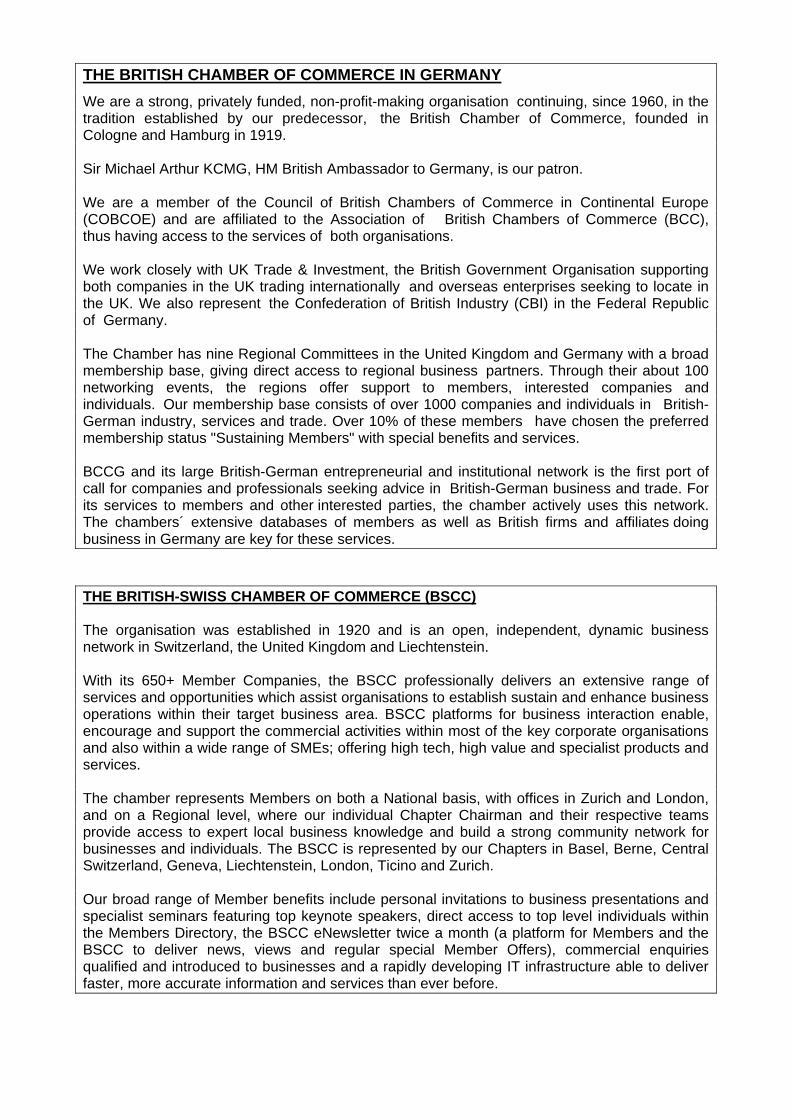

THE BRITISH CHAMBER OF COMMERCE IN GERMANY We are a strong, privately funded, non-profit-making organisation continuing, since 1960, in the tradition established by our predecessor, the British Chamber of Commerce, founded in Cologne and Hamburg in 1919. Sir Michael Arthur KCMG, HM British Ambassador to Germany, is our patron. We are a member of the Council of British Chambers of Commerce in Continental Europe (COBCOE) and are affiliated to the Association of British Chambers of Commerce (BCC), thus having access to the services of both organisations. We work closely with UK Trade & Investment, the British Government Organisation supporting both companies in the UK trading internationally and overseas enterprises seeking to locate in the UK. We also represent the Confederation of British Industry (CBI) in the Federal Republic of Germany. The Chamber has nine Regional Committees in the United Kingdom and Germany with a broad membership base, giving direct access to regional business partners. Through their about 100 networking events, the regions offer support to members, interested companies and individuals. Our membership base consists of over 1000 companies and individuals in British-German industry, services and trade. Over 10% of these members have chosen the preferred membership status "Sustaining Members" with special benefits and services. BCCG and its large British-German entrepreneurial and institutional network is the first port of call for companies and professionals seeking advice in British-German business and trade. For its services to members and other interested parties, the chamber actively uses this network. The chambers´ extensive databases of members as well as British firms and affiliates doing business in Germany are key for these services. THE BRITISH-SWISS CHAMBER OF COMMERCE (BSCC) The organisation was established in 1920 and is an open, independent, dynamic business network in Switzerland, the United Kingdom and Liechtenstein. With its 650+ Member Companies, the BSCC professionally delivers an extensive range of services and opportunities which assist organisations to establish sustain and enhance business operations within their target business area. BSCC platforms for business interaction enable, encourage and support the commercial activities within most of the key corporate organisations and also within a wide range of SMEs; offering high tech, high value and specialist products and services. The chamber represents Members on both a National basis, with offices in Zurich and London, and on a Regional level, where our individual Chapter Chairman and their respective teams provide access to expert local business knowledge and build a strong community network for businesses and individuals. The BSCC is represented by our Chapters in Basel, Berne, Central Switzerland, Geneva, Liechtenstein, London, Ticino and Zurich. Our broad range of Member benefits include personal invitations to business presentations and specialist seminars featuring top keynote speakers, direct access to top level individuals within the Members Directory, the BSCC eNewsletter twice a month (a platform for Members and the BSCC to deliver news, views and regular special Member Offers), commercial enquiries qualified and introduced to businesses and a rapidly developing IT infrastructure able to deliver faster, more accurate information and services than ever before.

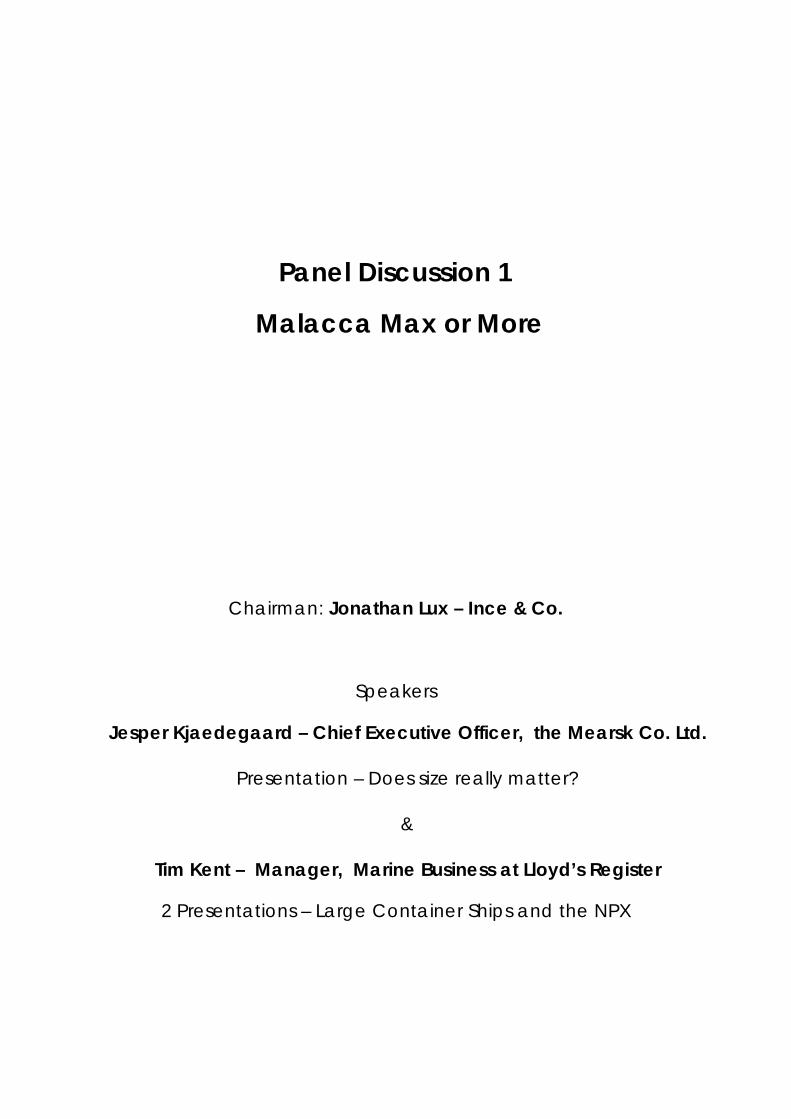

Panel Discussion 1

Malacca Max or More

Chairman: Jonathan Lux – Ince & Co.

Speakers

Jesper Kjaedegaard – Chief Executive Officer, the Mearsk Co. Ltd.

Presentation – Does size really matter?

&

Tim Kent – Manager, Marine Business at Lloyd’s Register

2 Presentations – Large Container Ships and the NPX

Jesper Kjaedegaard – Chief Executive Officer, the Mearsk Co. Ltd.

Presentation – Does size really matter?

1

1

Mr Jesper Kjaedegaard

CEO of The Maersk Company Ltd.

Does size really matter?

The World’s largest container vessel - Emma Maersk

- Where should we go from here...

1

1

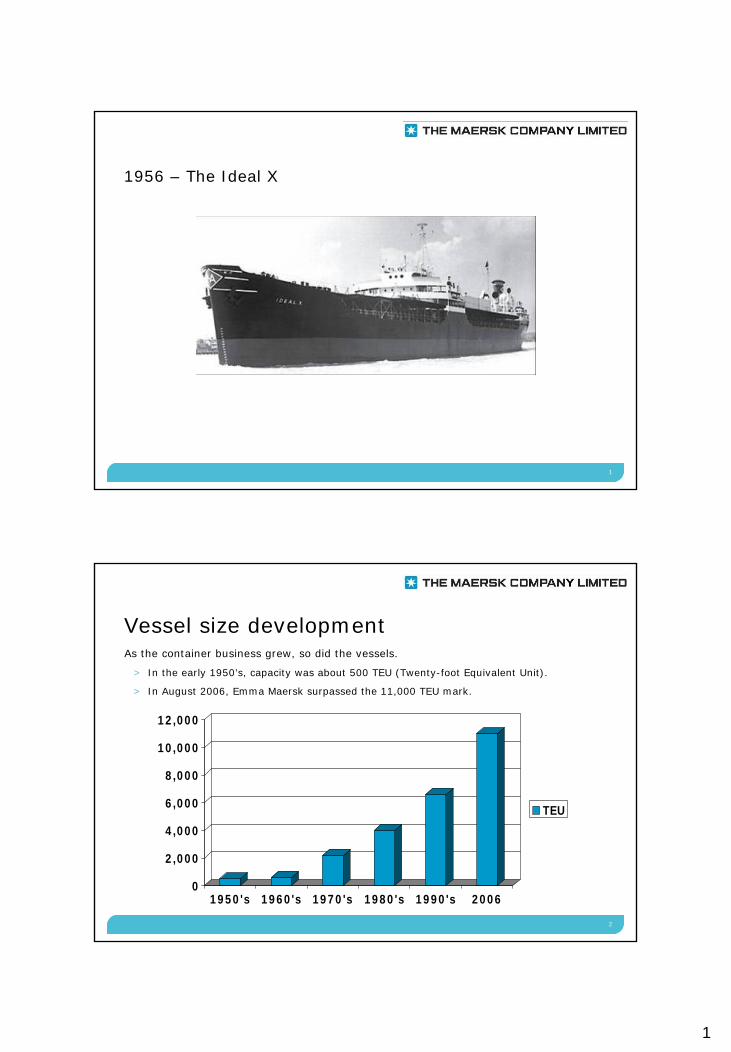

1956 – The Ideal X

2

Vessel size developmentAs the container business grew, so did the vessels.

> In the early 1950’s, capacity was about 500 TEU (Twenty-foot Equivalent Unit).

> In August 2006, Emma Maersk surpassed the 11,000 TEU mark.

0

2,000

4,000

6,000

8,000

10,000

12,000

1950's 1960's 1970's 1980's 1990's 2006

TEU

2

3

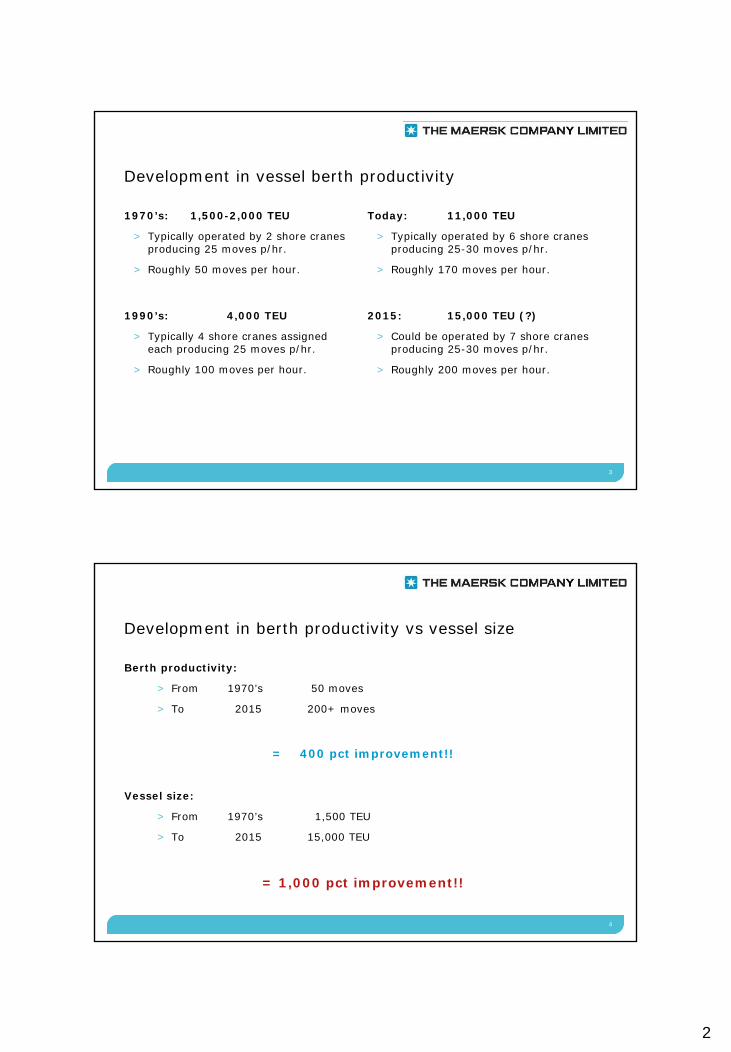

Development in vessel berth productivity

1970’s: 1,500-2,000 TEU

> Typically operated by 2 shore cranes producing 25 moves p/hr.

> Roughly 50 moves per hour.

1990’s: 4,000 TEU

> Typically 4 shore cranes assigned each producing 25 moves p/hr.

> Roughly 100 moves per hour.

Today: 11,000 TEU

> Typically operated by 6 shore cranes producing 25-30 moves p/hr.

> Roughly 170 moves per hour.

2015: 15,000 TEU (?)

> Could be operated by 7 shore cranes producing 25-30 moves p/hr.

> Roughly 200 moves per hour.

4

Development in berth productivity vs vessel size

Berth productivity:

> From 1970’s 50 moves

> To 2015 200+ moves

= 1,400 pct improvement!!

Vessel size:

> From 1970’s 1,500 TEU

> To 2015 15,000 TEU

= 1,000 pct improvement!!

3

5

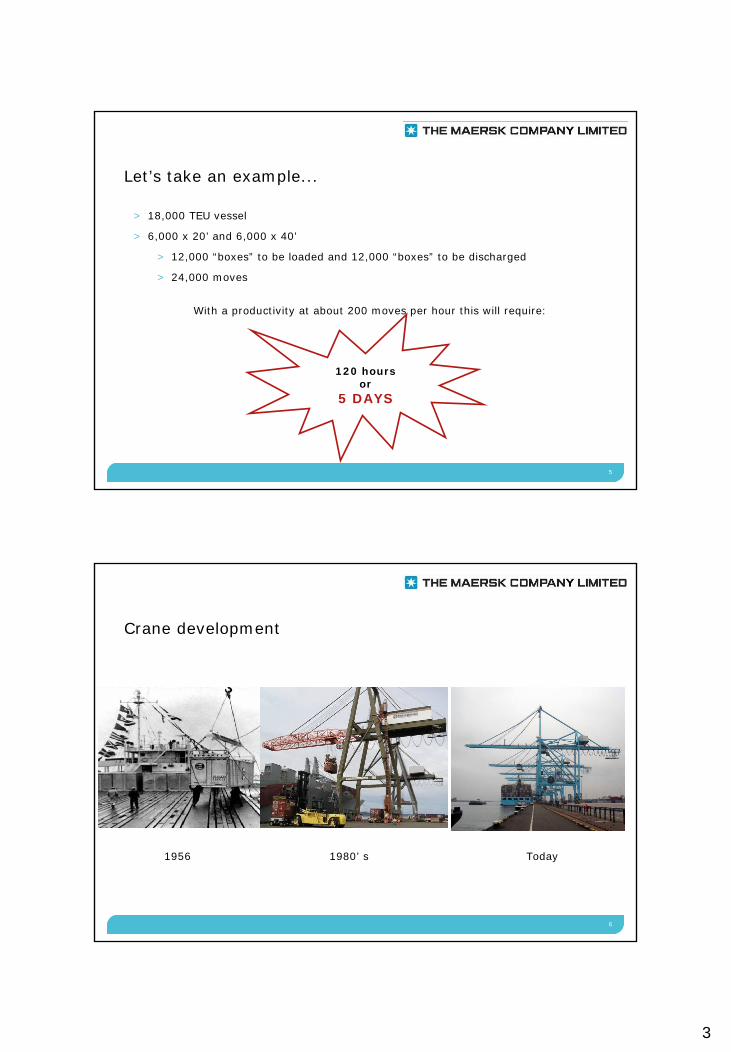

Let’s take an example...

> 18,000 TEU vessel

> 6,000 x 20’ and 6,000 x 40’

> 12,000 “boxes” to be loaded and 12,000 “boxes” to be discharged

> 24,000 moves

With a productivity at about 200 moves per hour this will require:

120 hoursor

5 DAYS

6

Crane development

1956 Today1980’ s

4

7

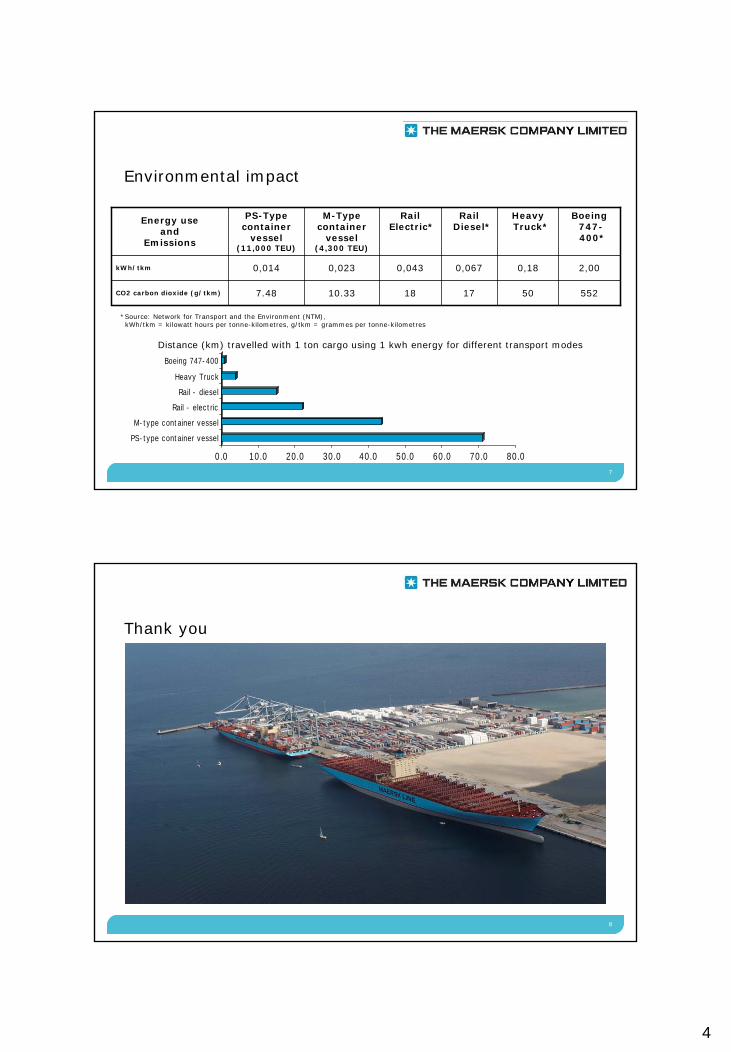

Environmental impact

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0

PS-type container vessel

M-type container vessel

Rail - electric

Rail - diesel

Heavy Truck

Boeing 747-400

Distance (km) travelled with 1 ton cargo using 1 kwh energy for different transport modes

Energy use and

Emissions

PS-Type container

vessel (11,000 TEU)

M-Type container

vessel (4,300 TEU)

RailElectric*

RailDiesel*

Heavy Truck*

Boeing 747-400*

kWh/tkm 0,014 0,023 0,043 0,067 0,18 2,00

CO2 carbon dioxide (g/tkm) 7.48 10.33 18 17 50 552

*Source: Network for Transport and the Environment (NTM), kWh/tkm = kilowatt hours per tonne-kilometres, g/tkm = grammes per tonne-kilometres

8

Thank you

Tim Kent – Manager, Marine Business at Lloyd’s Register

2 Presentations – Large Container Ships and the NPX

Large Container Ships & the NPX November 2007

© Lloyd’s Register

LARGE CONTAINER SHIPS & THE NPX

- a classification society perspective

SHIPPING TOMORROW

LARGE CONTAINER SHIPS & THE NPX

Tim KentDirector, Marine Strategy & PlanningLloyd’s Register

London, 29 November 2007

LARGE CONTAINER SHIPS & THE NPX

Market for prospect container ship tonnage

Large Container Ships & the NPX November 2007

© Lloyd’s Register

LARGE CONTAINER SHIPS & THE NPX

Seaborne Unitised Cargo

0

500

1,000

1,500

2,000

2,500

3,00019

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

1420

15

mill

ion

tonn

e

0

50

100

150

200

% o

f 200

7 va

lue

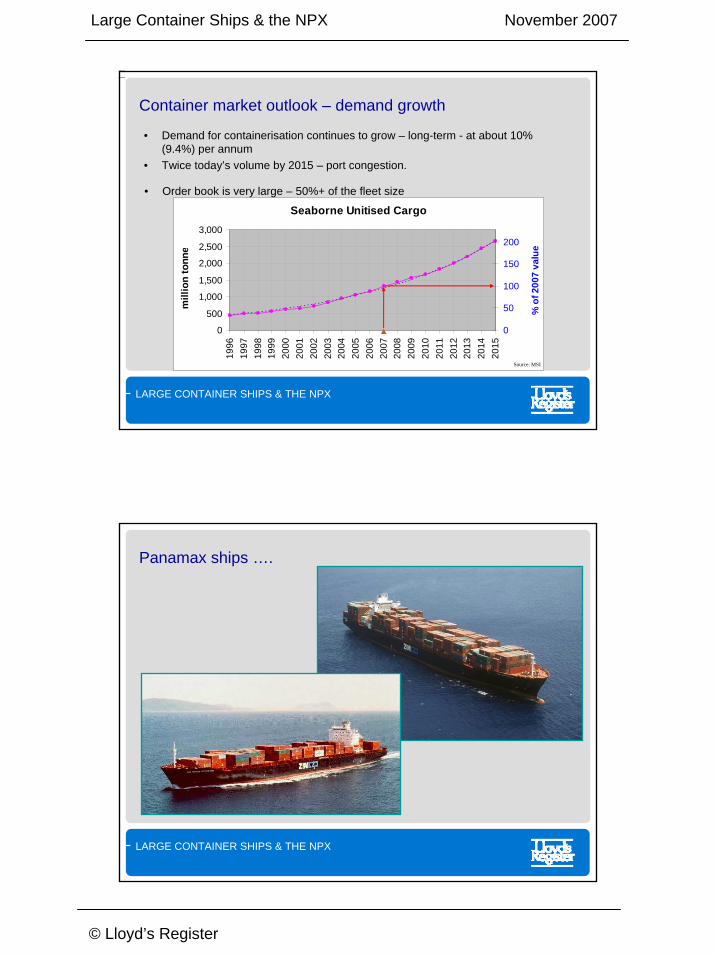

• Demand for containerisation continues to grow – long-term - at about 10% (9.4%) per annum

• Twice today’s volume by 2015 – port congestion.

• Order book is very large – 50%+ of the fleet size

Container market outlook – demand growth

Source: MSI

LARGE CONTAINER SHIPS & THE NPX

Panamax ships ….

Large Container Ships & the NPX November 2007

© Lloyd’s Register

LARGE CONTAINER SHIPS & THE NPX

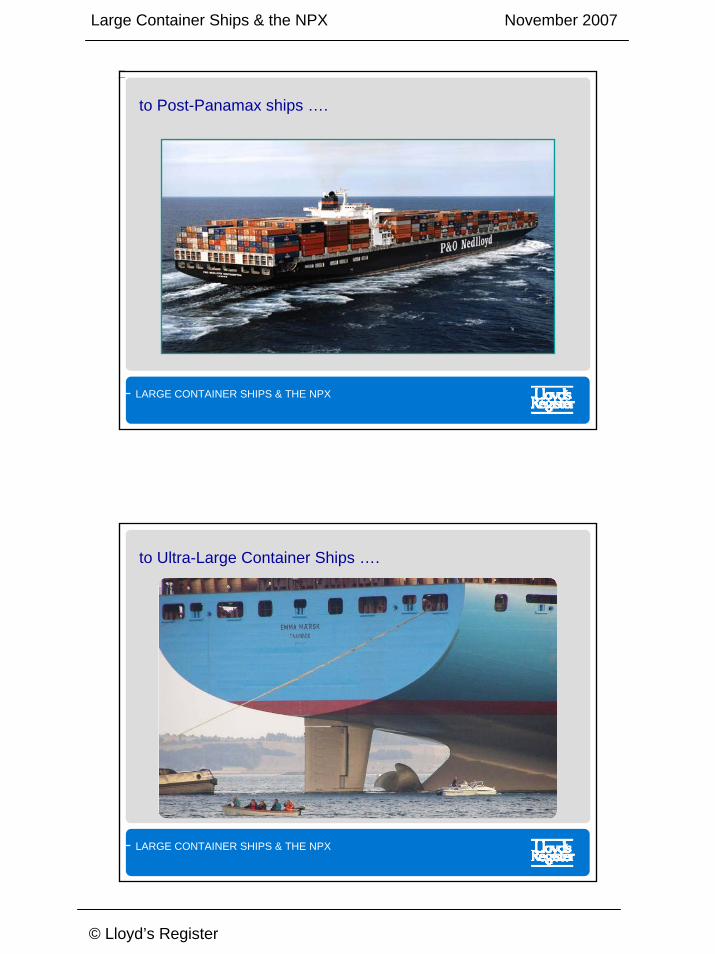

to Post-Panamax ships ….

LARGE CONTAINER SHIPS & THE NPX

to Ultra-Large Container Ships ….

Large Container Ships & the NPX November 2007

© Lloyd’s Register

LARGE CONTAINER SHIPS & THE NPX

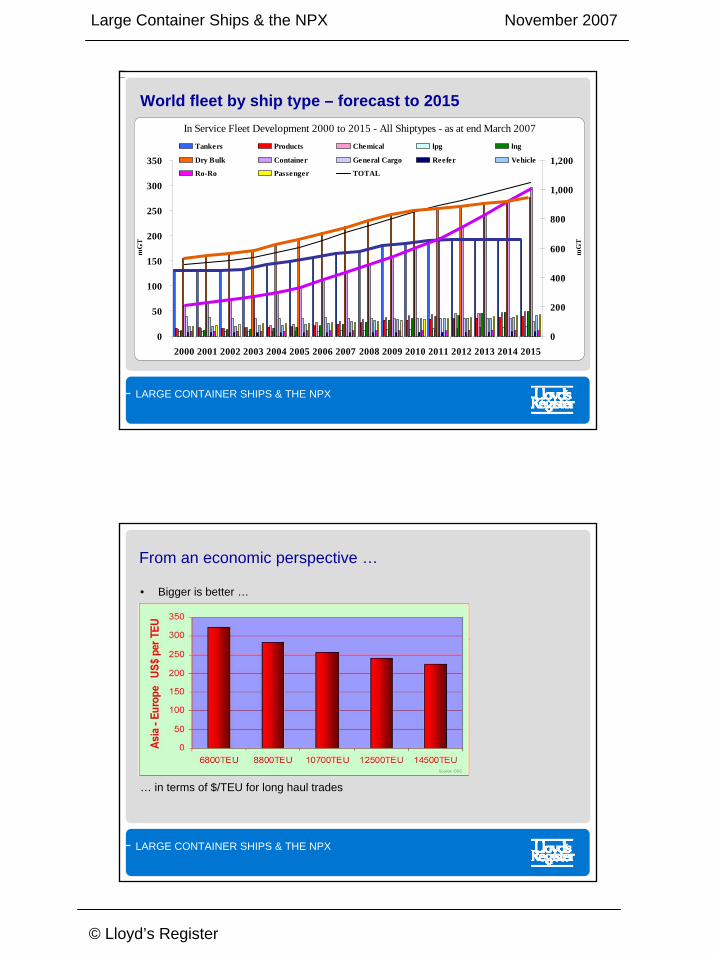

World fleet by ship type – forecast to 2015In Service Fleet Development 2000 to 2015 - All Shiptypes - as at end March 2007

0

50

100

150

200

250

300

350

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

mG

T

0

200

400

600

800

1,000

1,200

mG

T

Tankers Products Chemical lpg lng

Dry Bulk Container General Cargo Reefer Vehicle

Ro-Ro Passenger TOTAL

LARGE CONTAINER SHIPS & THE NPX

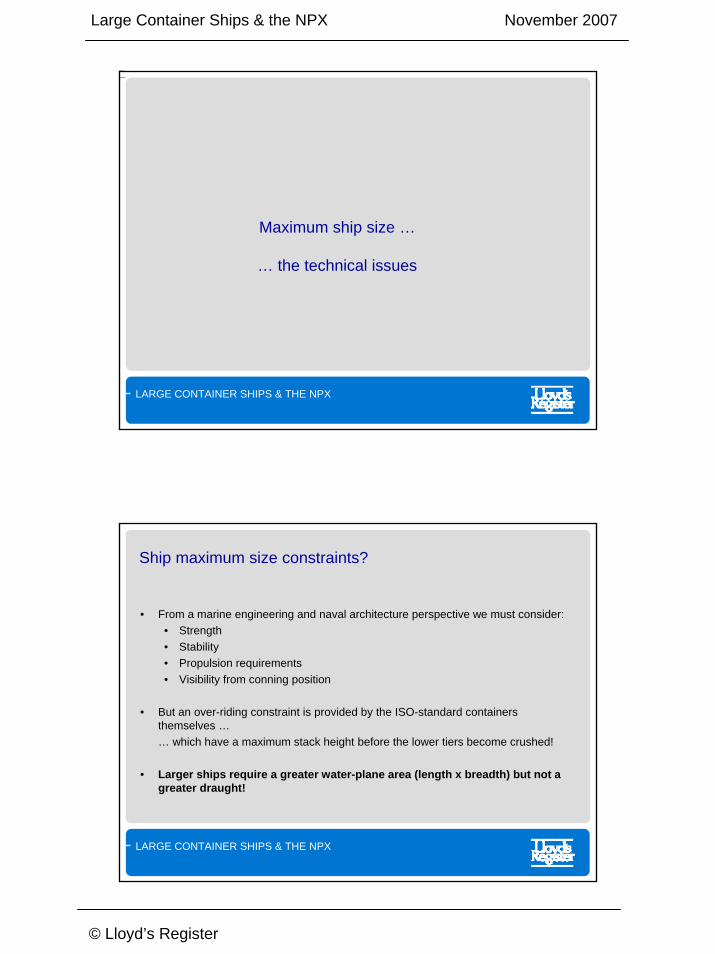

From an economic perspective …

• Bigger is better …

… in terms of $/TEU for long haul tradesSource: OSC

Large Container Ships & the NPX November 2007

© Lloyd’s Register

LARGE CONTAINER SHIPS & THE NPX

Maximum ship size …

… the technical issues

LARGE CONTAINER SHIPS & THE NPX

Ship maximum size constraints?

• From a marine engineering and naval architecture perspective we must consider:• Strength• Stability• Propulsion requirements• Visibility from conning position

• But an over-riding constraint is provided by the ISO-standard containers themselves …… which have a maximum stack height before the lower tiers become crushed!

• Larger ships require a greater water-plane area (length x breadth) but not a greater draught!

Large Container Ships & the NPX November 2007

© Lloyd’s Register

LARGE CONTAINER SHIPS & THE NPX

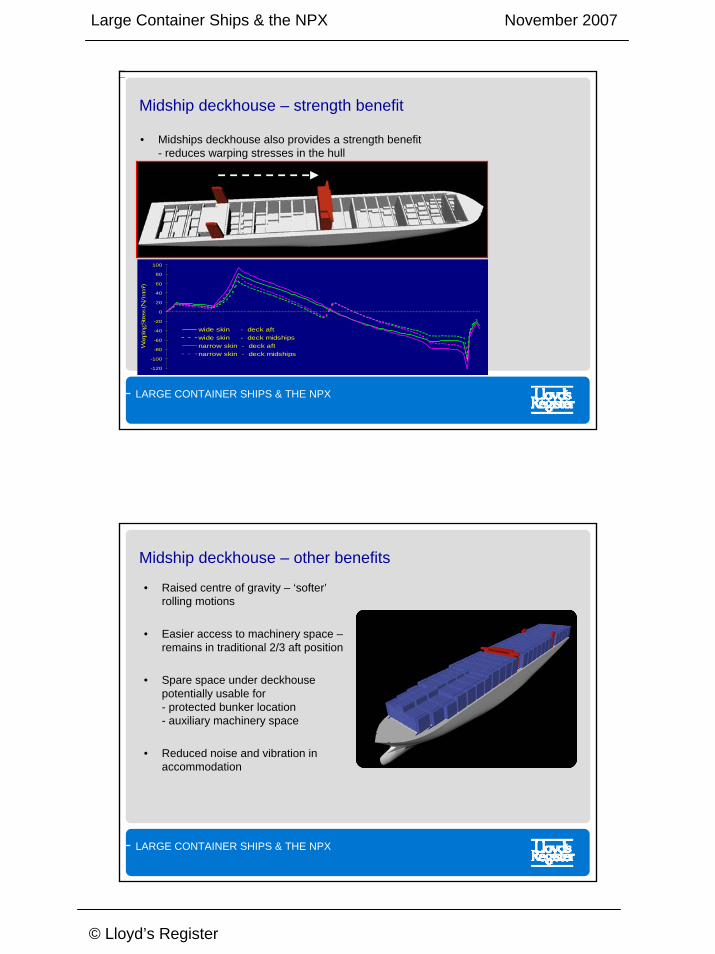

• Lloyd’s Register / Ocean Shipping Consultants Ltd study

Ultra-Large Container Ships (ULCS) :designing to the limit of current and projected terminal infrastructure capabilities (2001)

• Conclusion:Likely maximum capacity12,500 TEU (9’-6” ‘high-cube’ boxes)14,000 TEU (8’-6” ‘standard’ boxes)

Likely dimensionsLength Overall around 400mBreadth about 57m (22 boxes abreast)Design draught 14.4m

Ultra-Large Container Ship study

LARGE CONTAINER SHIPS & THE NPX

Midship deckhouse - Maximising capacity

• Moving deckhouse forward provides an improved conning position, reducing visibility-related constraints on forward stack height

TEU

Cap

acity

Position of deckhouse

Large Container Ships & the NPX November 2007

© Lloyd’s Register

LARGE CONTAINER SHIPS & THE NPX

Midship deckhouse – strength benefit

• Midships deckhouse also provides a strength benefit - reduces warping stresses in the hull

-120

-100

-80

-60

-40

-20

0

20

40

60

80

100

War

ping

Str

ess (

N/m

m²)

wide skin - deck aftwide skin - deck midshipsnarrow skin - deck aftnarrow skin - deck midships

LARGE CONTAINER SHIPS & THE NPX

• Raised centre of gravity – ‘softer’rolling motions

• Easier access to machinery space –remains in traditional 2/3 aft position

• Spare space under deckhouse potentially usable for- protected bunker location- auxiliary machinery space

• Reduced noise and vibration in accommodation

Midship deckhouse – other benefits

Large Container Ships & the NPX November 2007

© Lloyd’s Register

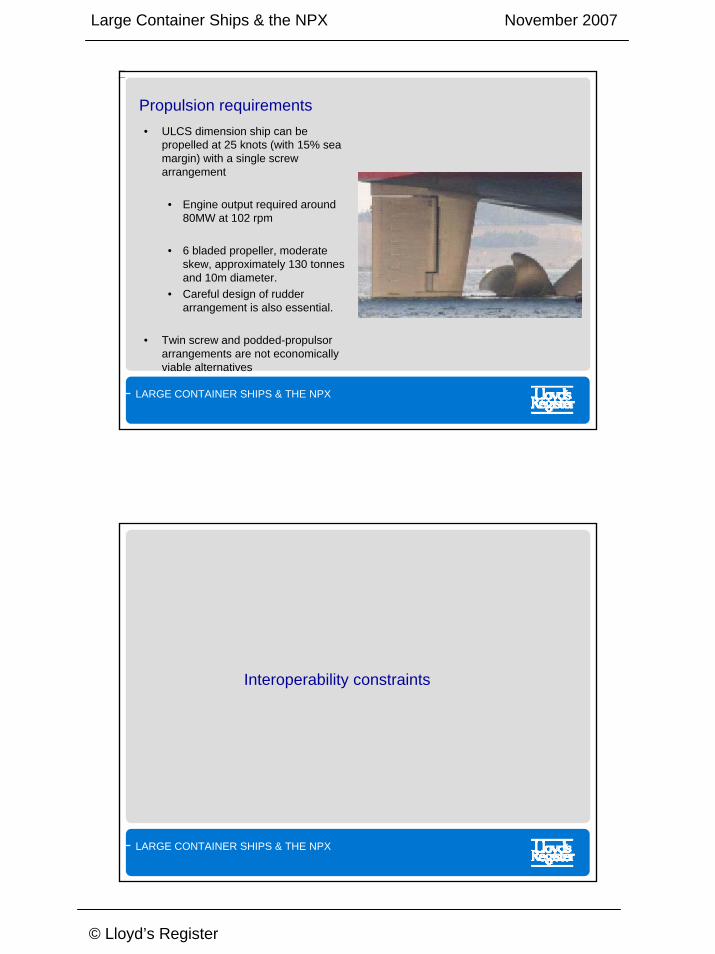

LARGE CONTAINER SHIPS & THE NPX

• ULCS dimension ship can be propelled at 25 knots (with 15% sea margin) with a single screw arrangement

• Engine output required around 80MW at 102 rpm

• 6 bladed propeller, moderate skew, approximately 130 tonnes and 10m diameter.

• Careful design of rudder arrangement is also essential.

• Twin screw and podded-propulsorarrangements are not economically viable alternatives

Propulsion requirements

LARGE CONTAINER SHIPS & THE NPX

Interoperability constraints

Large Container Ships & the NPX November 2007

© Lloyd’s Register

LARGE CONTAINER SHIPS & THE NPX

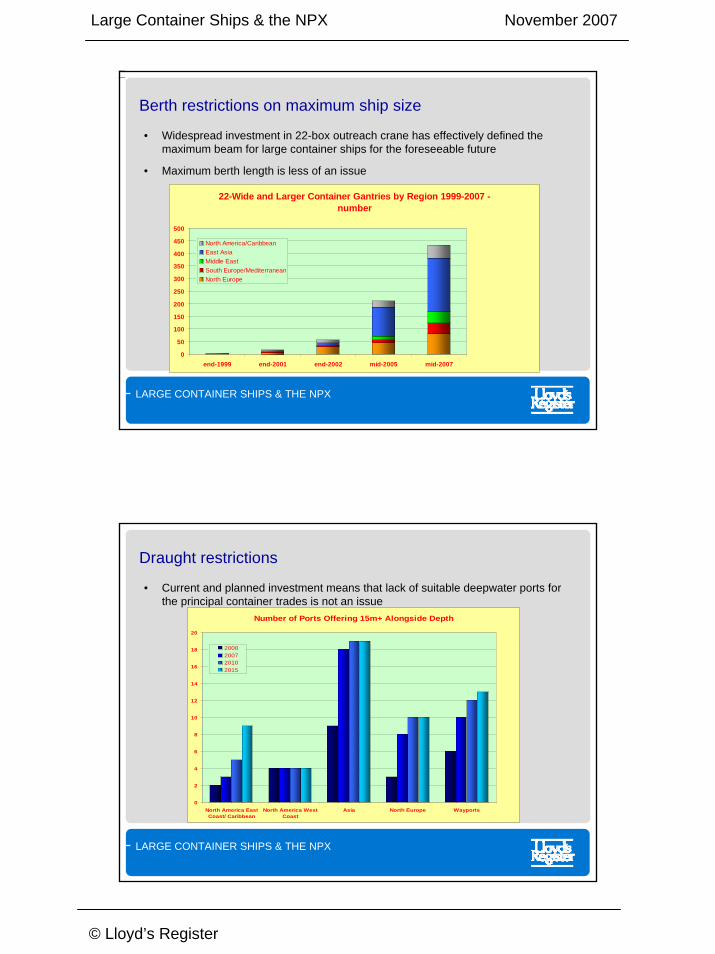

Berth restrictions on maximum ship size

• Widespread investment in 22-box outreach crane has effectively defined the maximum beam for large container ships for the foreseeable future

• Maximum berth length is less of an issue

22-Wide and Larger Container Gantries by Region 1999-2007 - number

0

50

100

150

200

250

300

350

400

450

500

end-1999 end-2001 end-2002 mid-2005 mid-2007

North America/CaribbeanEast AsiaMiddle EastSouth Europe/MediterraneanNorth Europe

LARGE CONTAINER SHIPS & THE NPX

Draught restrictions

• Current and planned investment means that lack of suitable deepwater ports for the principal container trades is not an issue

Number of Ports Offering 15m+ Alongside Depth

0

2

4

6

8

10

12

14

16

18

20

North America EastCoast/ Caribbean

North America WestCoast

Asia North Europe Wayports

2000200720102015

Large Container Ships & the NPX November 2007

© Lloyd’s Register

LARGE CONTAINER SHIPS & THE NPX

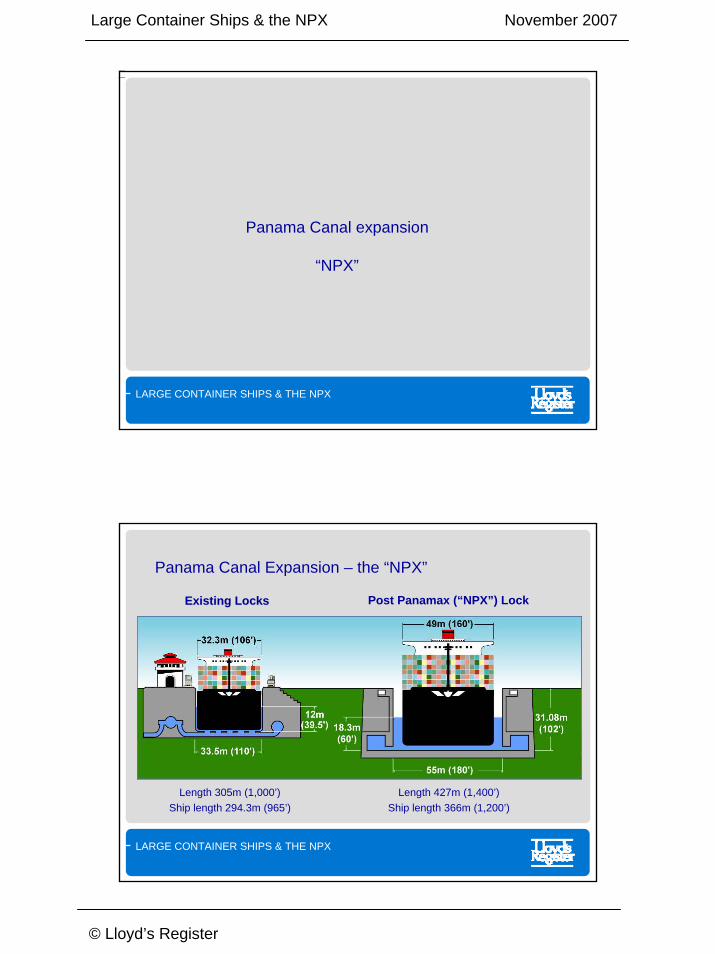

Panama Canal expansion

“NPX”

LARGE CONTAINER SHIPS & THE NPX

Existing LocksExisting Locks Post Panamax (“NPX”) Lock

Length 305m (1,000’)Ship length 294.3m (965’)

Length 427m (1,400’)Ship length 366m (1,200’)

Panama Canal Expansion – the “NPX”

Large Container Ships & the NPX November 2007

© Lloyd’s Register

LARGE CONTAINER SHIPS & THE NPX

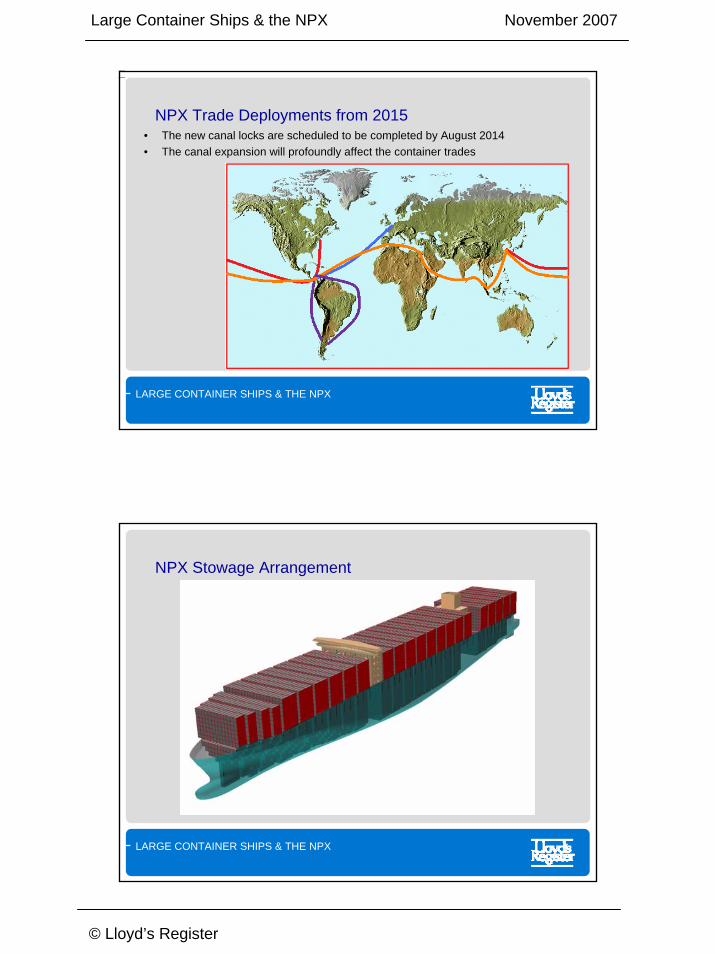

NPX Trade Deployments from 2015• The new canal locks are scheduled to be completed by August 2014• The canal expansion will profoundly affect the container trades

LARGE CONTAINER SHIPS & THE NPX

NPX Stowage Arrangement

Large Container Ships & the NPX November 2007

© Lloyd’s Register

LARGE CONTAINER SHIPS & THE NPX

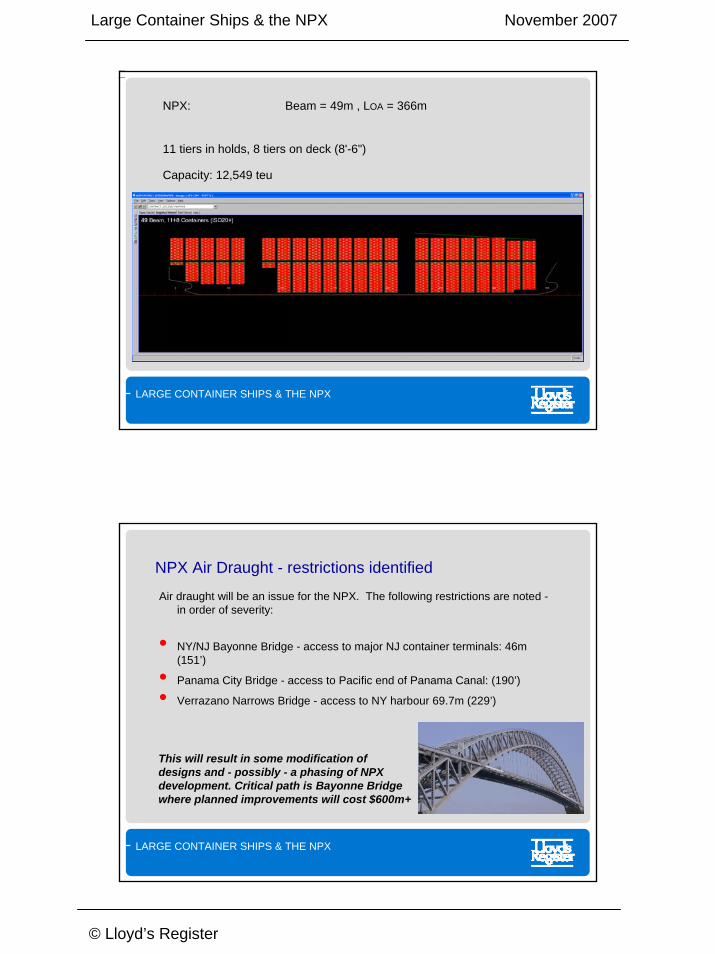

NPX: Beam = 49m , LOA = 366m

11 tiers in holds, 8 tiers on deck (8'-6")

Capacity: 12,549 teu

LARGE CONTAINER SHIPS & THE NPX

NPX Air Draught - restrictions identified

Air draught will be an issue for the NPX. The following restrictions are noted -in order of severity:

• NY/NJ Bayonne Bridge - access to major NJ container terminals: 46m (151’)

• Panama City Bridge - access to Pacific end of Panama Canal: (190’)

• Verrazano Narrows Bridge - access to NY harbour 69.7m (229’)

This will result in some modification of designs and - possibly - a phasing of NPX development. Critical path is Bayonne Bridge where planned improvements will cost $600m+

Large Container Ships & the NPX November 2007

© Lloyd’s Register

LARGE CONTAINER SHIPS & THE NPX

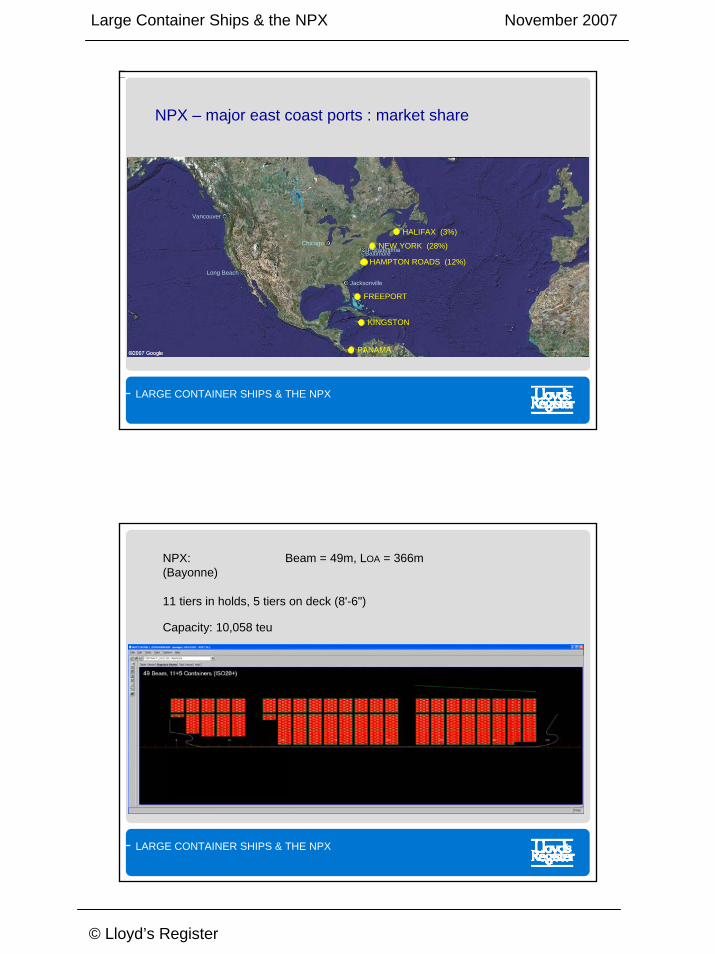

HALIFAX (3%)

FREEPORT

KINGSTON

NEW YORK (28%)

HAMPTON ROADS (12%)BaltimorePhiladelphia

Jacksonville

Chicago

PANAMA

Long Beach

Vancouver

NPX – major east coast ports : market share

LARGE CONTAINER SHIPS & THE NPX

NPX: Beam = 49m, LOA = 366m (Bayonne)

11 tiers in holds, 5 tiers on deck (8'-6")

Capacity: 10,058 teu

Large Container Ships & the NPX November 2007

© Lloyd’s Register

LARGE CONTAINER SHIPS & THE NPX

NPX Air Draught - likely phased development

• Stage I - until the Bayonne Bridge is improved, the maximum room for superstructure over top tier of just 2.6m will be available, and this may force the superstructure forward - or restrict capacity of the NPX

• Stage 2 - after the Bayonne Bridge is improved there will be no real constraint in this respect and a more conventional design could be achieved

Timing of bridge improvement will be a critical design input.

LARGE CONTAINER SHIPS & THE NPX

• Larger ships on major long-haul trades offer good economies of scale

• There are significant design challenges to continually increasing the maximum size of container ships … but these are being overcome

• Interoperability with established and future port infrastructure is the limiting factor on ship size today.

• The new Panama Canal development is redefining the maximum dimensions of ships for fully flexible global trade. These “NPX” dimensions are bigger than most container ships in service today.

• The very largest ULCS container ships in service or on order exceed the maximum “NPX” dimensions. ULCS tonnage will continue to offer attractive prospects for major Asia-Europe trades due to their economy of scale.

• Prospect of serious undersupply of feeder tonnage must be addressed for the largecontainer ship trade to fully realise itspotential.

Container ships – some concluding comments

Large Container Ships & the NPX November 2007

© Lloyd’s Register

Services are provided by members of the Lloyd’s Register Group Lloyd’s Register, Lloyd’s Register EMEA and Lloyd’s Register Asia are exempt charities under the UK Charities Act 1993.

The Lloyd’s Register Group works to enhance safety and approve assets and systems at sea, on land and in the air –because life matters.

LARGE CONTAINER SHIPS & THE NPX

BOXSHIP Conference Hamburg, Germany. 15th to 17th October 2007 _______________________________________________________________________

LARGE CONTAINER SHIPS AND THE NPX David Tozer, Lloyd’s Register, UK Andrew Penfold, Ocean Shipping Consultants Ltd, UK SYNOPSIS

In October 2006 the people of Panama voted in favour of constructing larger locks at each end of the Panama Canal, which will be able to accommodate some of the largest container ships which are in service and on order today. Lloyd's Register research, in association with Ocean Shipping Consultants Ltd, indicates that this is likely to completely redefine the global container trades.

This paper describes the enhancements to the Panama Canal and key features of the largest container ships which will be able to take advantage of the increased capacity. A solution is described for the problematic air draught issue for vessels trading into New York / New Jersey.

SYNOPSIS...........................................................................................................................1 1. Introduction ................................................................................................................1 2. The Expansion of the Panama Canal ............................................................................2 3. NPX Container Ships for the New Locks.......................................................................3 4. Trading Patterns and the Bayonne Bridge ....................................................................6 5. Conclusions.................................................................................................................8 6. Acknowledgements.....................................................................................................8 7. References ..................................................................................................................8 8. Authors’ Biographies ...................................................................................................9

1. INTRODUCTION

The growth of the container trades is remarkable, not only in terms of the total capacity of the container ship fleet which has now surged past 10 million teu, but also in terms of ship size. The largest container ships in service today have capacities greater than 10,000 teu, which seemed unthinkable just a few years ago.

In 1999 Lloyd’s Register, then classing the largest container ships in the world, embarked on a comprehensive study[1,2] to examine the future prospects for ultra-large container ships (ULCS) and predicted the introduction into service of ships like the Emma Mærsk, the largest container ship in service today by a significant margin.

The current investigation, again with Ocean Shipping Consultants Ltd (OSC), assesses the implications of the next major influence on the container trades – the development of the Panama Canal to accommodate container ships almost as large as the ULCS.

Our first discussions with the canal authority (ACP) took place a number years ago. The current study commenced early in 2007 and is still under way; it is scheduled to complete later this year.

With larger ships able to transit Panama, routes between Asia and the US East Coast will be the most cost-effective means to move freight in and out of the American Midwest. There is

also scope for the redevelopment of Round-the-World (RTW) services that were a feature of deepsea container trades in the late 1980s and early 1990s.

Central to the success of the revitalised trades will be the ability of ships to call at New York. However, ships entering the most important of the New York and New Jersey container terminals will need to pass under the Bayonne Bridge. With an air draught of 46 metres (151 feet), this bridge currently poses a problem for nearly all post-Panamax ships currently in service and on order.

2. THE EXPANSION OF THE PANAMA CANAL

The expansion of the capacity of the Panama Canal, the “Third Set of Locks” project, is a major feat of engineering, anticipated to cost some $5.25 billion.

On 22nd October 2006 Panamanians voted in favour of the proposal to expand the Panama Canal. By law, expansion had to be put to a vote in a popular referendum. The Panama Canal Authority (ACP) presented its formal proposal to the Panamanian government in April, and on the day of the vote 77% voted for expansion. According to the ACP’s report “Proposal for the Expansion of the Panama Canal - Third Set of Locks Project”[3], the containerised cargo trade between Northeast Asia and the US East Coast reflects the highest canal transit growth rate. This route currently represents more than 50% of the PCUMS – Panama Canal Universal Measurement System – volume of all containerised cargo transiting the canal and is anticipated to become a key growth driver for the canal.

The Miraflores Locks Today Courtesy of the Panama Canal Authority

If all goes according to plan, the third set of locks should be operational by 2015. In fact, the perfect target would be August 2014, the 100th anniversary of the first transit of a ship through the canal. (Apparently the first ship to navigate through the canal was SS Cristibal on 3rd August 1914, although official records show the first ship to use the canal to be the SS Ancon on 15th August 1914.)

The container trades are a major driving force behind the proposal to expand the capacity of the canal, in terms of throughput and vessel size.

2

Two sets of locks will be constructed, one at the Atlantic end of the canal, east of the Gatun locks, and the other at the Pacific end to the south-west of the Miraflores locks. Each set of locks will have three chambers, similar to the configuration of the existing Gatun locks. The chambers will be 427 metres (1,400 feet) long, by 55 metres (180 feet) wide and 18.3 metres (60 feet) deep, allowing transit of vessels with a beam of up to 49 metres (160 feet), an overall length of up to 366 metres (1,200 feet) and a draught of up to 15 metres (50 feet).

The new locks will use rolling gates. Each chamber of the new locks will be connected to three water reutilisation basins – 18 basins in total. The use of these basins to conserve water, together with the increased capacity produced by deepening Gatun Lake and Gaillard Cut and raising Gatun Lake’s maximum operating level by approximately 0.45 metres (1.5 feet), will provide an additional 10 million tonnes of water daily, enabling approximately 48 additional lockages per day.

The existing two strings of locks, which can accommodate ships up to 106 feet (32.3 metres) beam, will remain in use throughout the development work; they will continue to be used once the work is complete, ultimately providing a total of three strings of locks at each end of the canal. Thus the canal will not only be able to accept larger ships but the total annual tonnage passing through the canal will be greatly increased.

We can expect increasing speculation on the effect that this project will have on the container trades. The proposed expansion plans are not compatible with the largest container ships of 14,000 teu which are expected to be in service by 2015, with 22 boxes across the breadth of the ship and a beam of about 56 metres. However, such vessels are most suited to the Asia-Europe trades, so it is likely that 12,000 to 13,000 teu vessels will become the new panamaxes – “NPX” container ships.

3. NPX CONTAINER SHIPS FOR THE NEW LOCKS

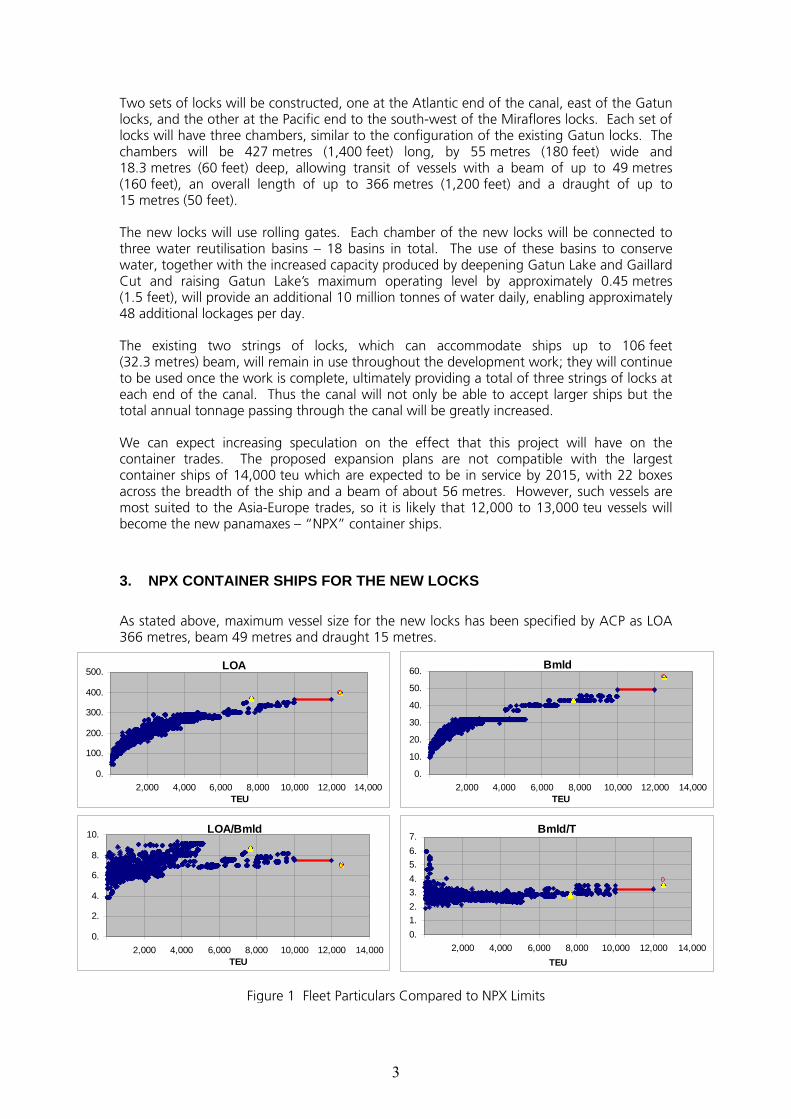

As stated above, maximum vessel size for the new locks has been specified by ACP as LOA 366 metres, beam 49 metres and draught 15 metres.

LOA/Bmld

0.

2.

4.

6.

8.

10.

2,000 4,000 6,000 8,000 10,000 12,000 14,000TEU

Bmld/T

0.1.2.3.4.5.6.7.

2,000 4,000 6,000 8,000 10,000 12,000 14,000TEU

LOA

0.

100.

200.

300.

400.

500.

2,000 4,000 6,000 8,000 10,000 12,000 14,000TEU

Bmld

0.

10.

20.

30.

40.

50.

60.

2,000 4,000 6,000 8,000 10,000 12,000 14,000TEU

Figure 1 Fleet Particulars Compared to NPX Limits

3

Figure 1 compares these limiting dimensions with the dimensions of the 4,000 container ships comprising today’s fleet. It is apparent that the dimensions accord well with the larger super-post-panamax container ships in service today and are likely to be suitable for ships with capacities up to 12 or 13,000 teu.

Today there are two series of ships in service which will not be able to transit the new canal locks. They are the Emma Mærsk, soon to be joined by her seven sisters, and the somewhat smaller Gudrun Mærsk and her sisters. The Lloyd’s Register ULCS[1,2] concept, whilst ideally suited to global trade particularly between Asia and Europe, is also too large for the new canal locks.

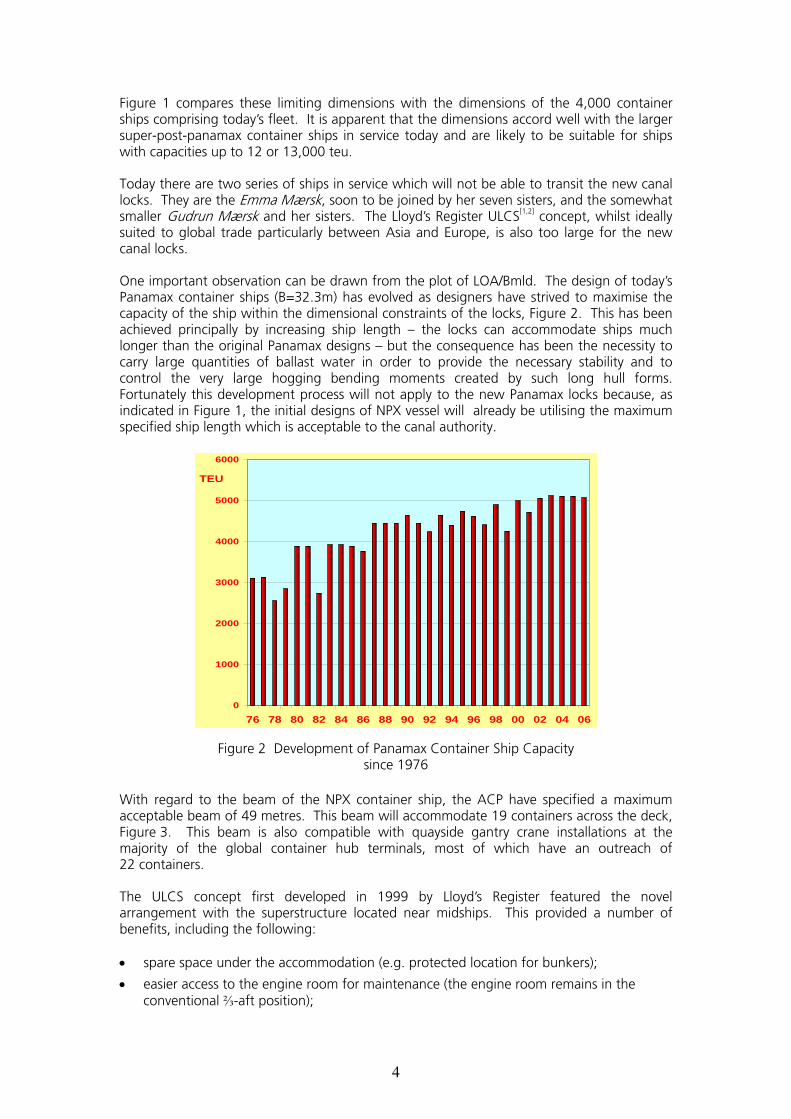

One important observation can be drawn from the plot of LOA/Bmld. The design of today’s Panamax container ships (B=32.3m) has evolved as designers have strived to maximise the capacity of the ship within the dimensional constraints of the locks, Figure 2. This has been achieved principally by increasing ship length – the locks can accommodate ships much longer than the original Panamax designs – but the consequence has been the necessity to carry large quantities of ballast water in order to provide the necessary stability and to control the very large hogging bending moments created by such long hull forms. Fortunately this development process will not apply to the new Panamax locks because, as indicated in Figure 1, the initial designs of NPX vessel will already be utilising the maximum specified ship length which is acceptable to the canal authority.

0

1000

2000

3000

4000

5000

6000

76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06

TEU

Figure 2 Development of Panamax Container Ship Capacity since 1976

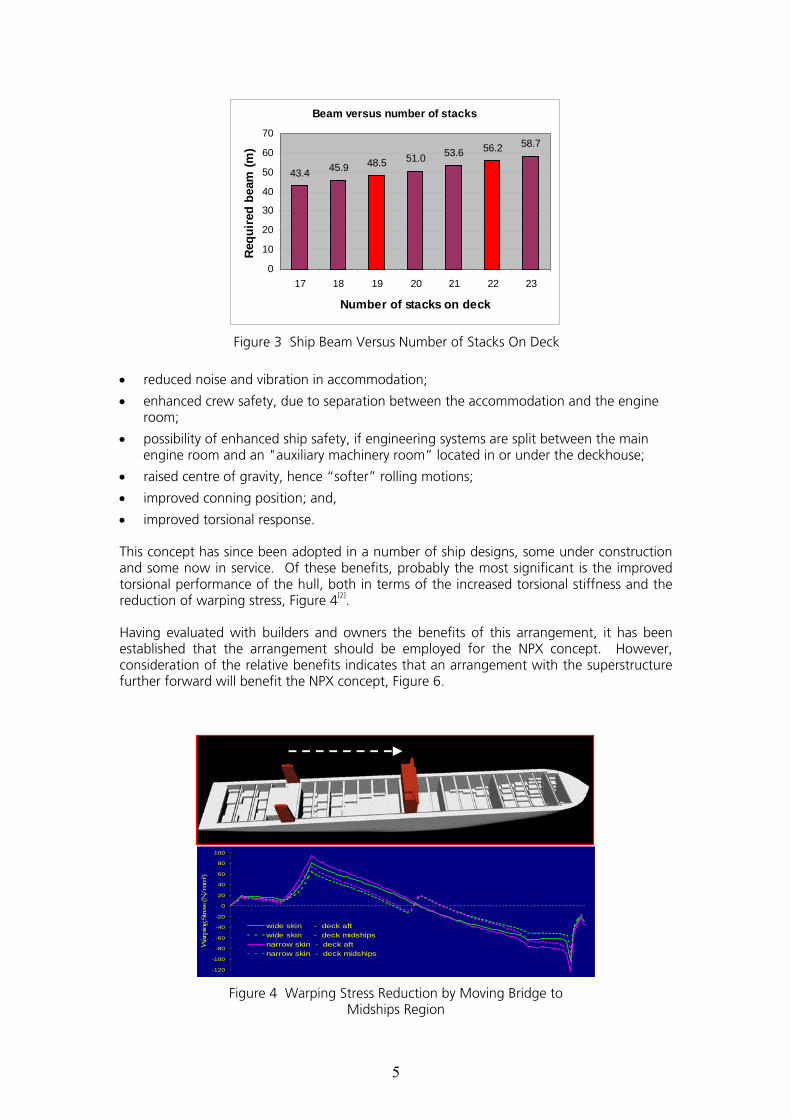

With regard to the beam of the NPX container ship, the ACP have specified a maximum acceptable beam of 49 metres. This beam will accommodate 19 containers across the deck, Figure 3. This beam is also compatible with quayside gantry crane installations at the majority of the global container hub terminals, most of which have an outreach of 22 containers.

The ULCS concept first developed in 1999 by Lloyd’s Register featured the novel arrangement with the superstructure located near midships. This provided a number of benefits, including the following:

• spare space under the accommodation (e.g. protected location for bunkers);

• easier access to the engine room for maintenance (the engine room remains in the conventional ⅔-aft position);

4

Beam versus number of stacks

43.4 45.9 48.5 51.0 53.6 56.2 58.7

0

10

20

30

40

50

60

70

17 18 19 20 21 22 23

Number of stacks on deck

Req

uire

d be

am (m

)

Figure 3 Ship Beam Versus Number of Stacks On Deck

• reduced noise and vibration in accommodation;

• enhanced crew safety, due to separation between the accommodation and the engine room;

• possibility of enhanced ship safety, if engineering systems are split between the main engine room and an "auxiliary machinery room” located in or under the deckhouse;

• raised centre of gravity, hence “softer” rolling motions;

• improved conning position; and,

• improved torsional response.

This concept has since been adopted in a number of ship designs, some under construction and some now in service. Of these benefits, probably the most significant is the improved torsional performance of the hull, both in terms of the increased torsional stiffness and the reduction of warping stress, Figure 4[2].

Having evaluated with builders and owners the benefits of this arrangement, it has been established that the arrangement should be employed for the NPX concept. However, consideration of the relative benefits indicates that an arrangement with the superstructure further forward will benefit the NPX concept, Figure 6.

-120

-100

-80

-60

-40

-20

0

20

40

60

80

100

War

ping

Str

ess (

N/m

m²)

wide skin - deck aftwide skin - deck midshipsnarrow skin - deck aftnarrow skin - deck midships

Figure 4 Warping Stress Reduction by Moving Bridge to Midships Region

5

4. TRADING PATTERNS AND THE BAYONNE BRIDGE

Following the confirmation that the planned Panama Canal expansion is going ahead, significant new opportunities and trading patterns are now likely for container ships, according to the in-depth research by Lloyd’s Register / OSC. The increasing demand for the economies of scale offered by large post-Panamax ships has already led to a large leap in ship size. The largest container ship built in Asia, the COSCO Asia, was delivered recently by Hyundai Heavy Industries Ltd, to Lloyd's Register class. She has a capacity of 10,050 teu. She will be joined in 2008 by 3 sisters.

The orderbook for ships with declared capacities of over 10,000 teu is now filling rapidly, with more than 180 ships on order in this size range. As a consequence, the expansion of the Panama Canal is now likely to lead to a complete redefinition of container trades.

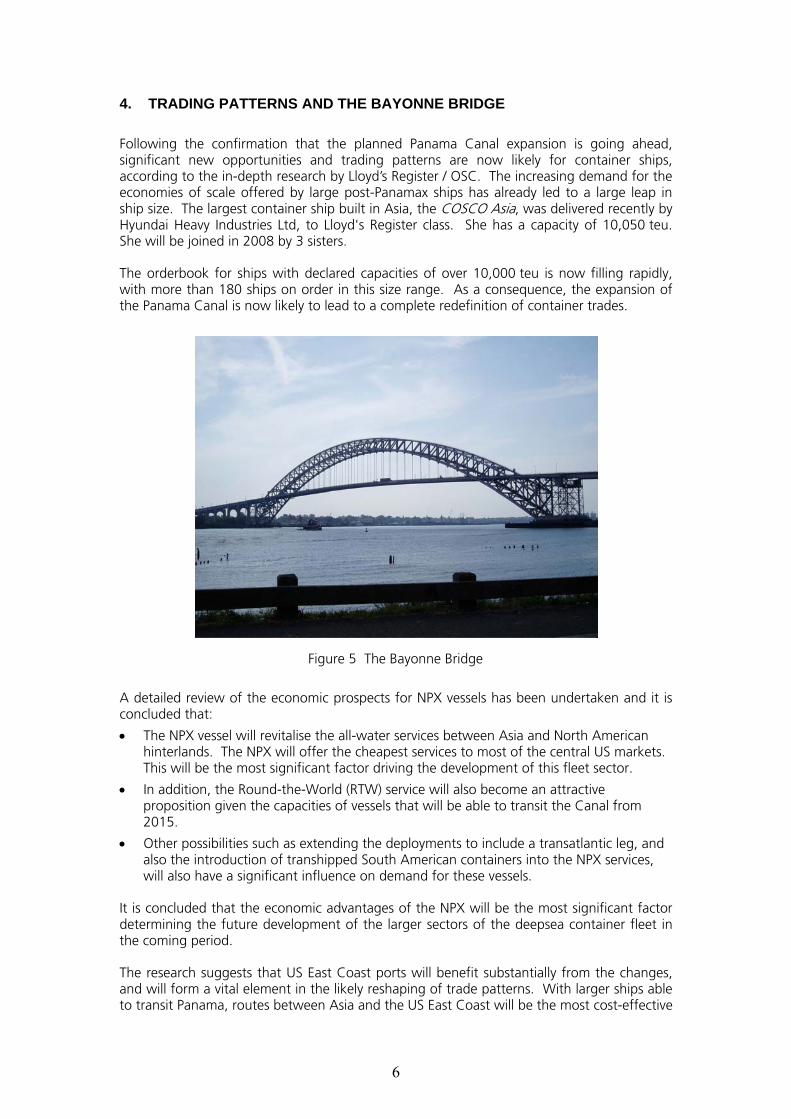

Figure 5 The Bayonne Bridge

A detailed review of the economic prospects for NPX vessels has been undertaken and it is concluded that:

• The NPX vessel will revitalise the all-water services between Asia and North American hinterlands. The NPX will offer the cheapest services to most of the central US markets. This will be the most significant factor driving the development of this fleet sector.

• In addition, the Round-the-World (RTW) service will also become an attractive proposition given the capacities of vessels that will be able to transit the Canal from 2015.

• Other possibilities such as extending the deployments to include a transatlantic leg, and also the introduction of transhipped South American containers into the NPX services, will also have a significant influence on demand for these vessels.

It is concluded that the economic advantages of the NPX will be the most significant factor determining the future development of the larger sectors of the deepsea container fleet in the coming period.

The research suggests that US East Coast ports will benefit substantially from the changes, and will form a vital element in the likely reshaping of trade patterns. With larger ships able to transit Panama, routes between Asia and the US East Coast will be the most cost-effective

6

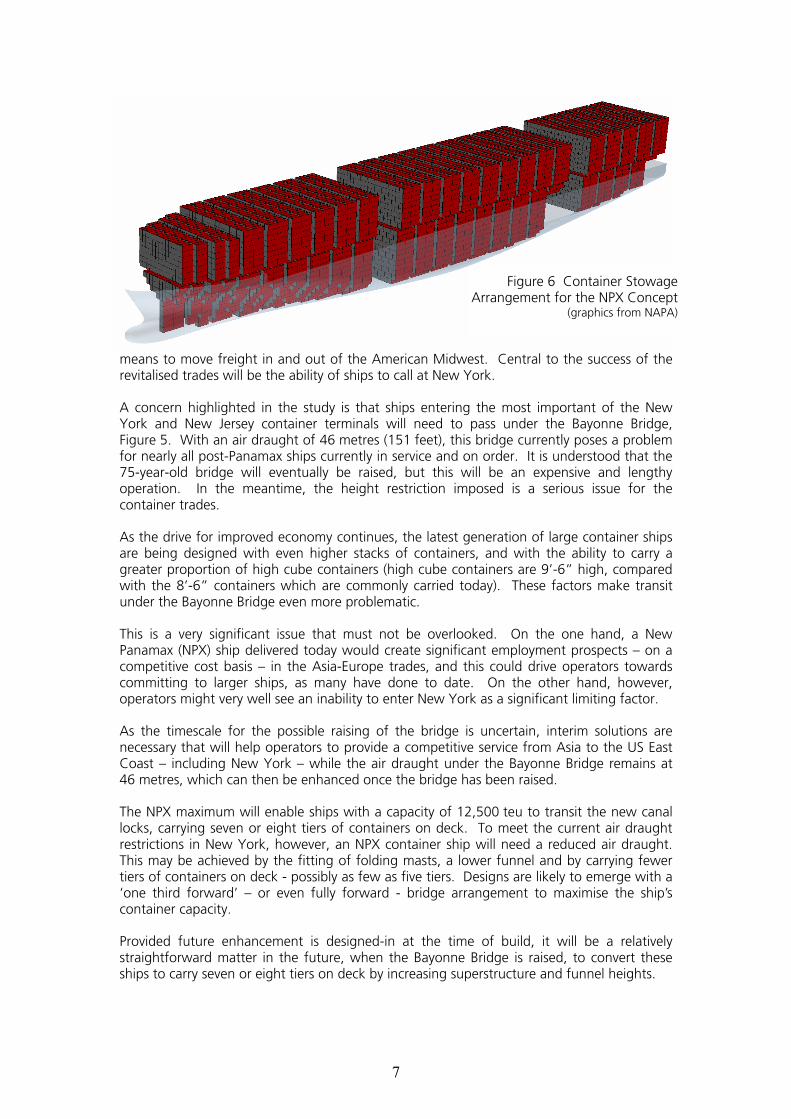

Figure 6 Container Stowage Arrangement for the NPX Concept

(graphics from NAPA)

means to move freight in and out of the American Midwest. Central to the success of the revitalised trades will be the ability of ships to call at New York.

A concern highlighted in the study is that ships entering the most important of the New York and New Jersey container terminals will need to pass under the Bayonne Bridge, Figure 5. With an air draught of 46 metres (151 feet), this bridge currently poses a problem for nearly all post-Panamax ships currently in service and on order. It is understood that the 75-year-old bridge will eventually be raised, but this will be an expensive and lengthy operation. In the meantime, the height restriction imposed is a serious issue for the container trades.

As the drive for improved economy continues, the latest generation of large container ships are being designed with even higher stacks of containers, and with the ability to carry a greater proportion of high cube containers (high cube containers are 9’-6” high, compared with the 8’-6” containers which are commonly carried today). These factors make transit under the Bayonne Bridge even more problematic.

This is a very significant issue that must not be overlooked. On the one hand, a New Panamax (NPX) ship delivered today would create significant employment prospects – on a competitive cost basis – in the Asia-Europe trades, and this could drive operators towards committing to larger ships, as many have done to date. On the other hand, however, operators might very well see an inability to enter New York as a significant limiting factor.

As the timescale for the possible raising of the bridge is uncertain, interim solutions are necessary that will help operators to provide a competitive service from Asia to the US East Coast – including New York – while the air draught under the Bayonne Bridge remains at 46 metres, which can then be enhanced once the bridge has been raised.

The NPX maximum will enable ships with a capacity of 12,500 teu to transit the new canal locks, carrying seven or eight tiers of containers on deck. To meet the current air draught restrictions in New York, however, an NPX container ship will need a reduced air draught. This may be achieved by the fitting of folding masts, a lower funnel and by carrying fewer tiers of containers on deck - possibly as few as five tiers. Designs are likely to emerge with a ‘one third forward’ – or even fully forward - bridge arrangement to maximise the ship’s container capacity.

Provided future enhancement is designed-in at the time of build, it will be a relatively straightforward matter in the future, when the Bayonne Bridge is raised, to convert these ships to carry seven or eight tiers on deck by increasing superstructure and funnel heights.

7

5. CONCLUSIONS

The new Panama Canal locks will be compatible with some of the largest container ships currently on order and under construction today. It is anticipated that by 2014, when the new locks are scheduled to be complete, large numbers of NPX container ships will be in service. Whilst these ships will be able to trade competitively alongside the ULCS vessels, it is important that they are able to pass under New York’s Bayonne Bridge, at least in the short term, if they are to achieve the maximum benefit from the canal expansion.

6. ACKNOWLEDGEMENTS

The authors acknowledge the contributions to this study by colleagues.

© Lloyd’s Register 2007. All rights reserved.

Lloyd’s Register retains the right of subsequent publication. However, any opinions expressed and statements made in this paper and in the subsequent discussions are those of the individuals and do not necessarily represent the views of Lloyd’s Register.

Enquiries should be addressed to Lloyd’s Register, 71 Fenchurch Street, London EC3M 4BS, England.

Lloyd’s Register is an exempt charity under the UK Charities Act 1993

7. REFERENCES

[1] Tozer, D.R. and Penfold, A. “Container Ships: Design Aspects of Larger Vessels”, Lloyd’s Register and Ocean Shipping Consultants Ltd., RINA/IMarE Presentation, London, March 2000.

[2] Tozer, D.R. and Penfold, A. “Ultra-Large Container Ships (ULCS) : designing to the limit of current and projected terminal infrastructure capabilities”, Lloyd’s Register Technical Association paper no.5¸Session 2001-2002.

[3] Proposal for the Expansion of the Panama Canal - Third Set of Locks Project, Panama Canal Authority, April 2006.

8

8. AUTHORS’ BIOGRAPHIES

David Tozer trained with the Royal Corps of Naval Constructors before moving to Newcastle to work for BSRA, where his work in the structural analysis group included studies of the Kurdistan and Derbyshire. When he joined Lloyd’s Register in 1984, he was involved in development of torsional analysis procedures and software. He was also a member of the team which studied the “long thin/short fat” warship hull design inquiry. After 5 years he transferred to Class Computational Services and, until autumn 2001, worked in the Dry Cargo/Ship Structures group where his primary involvement was with container ships. As a Senior Principal Specialist, he is currently Lloyd’s Register’s Business Manager for Container Ships.

Andrew Penfold is a Director of Ocean Shipping Consultants Ltd. with responsibility for container shipping and port development studies. Mr Penfold has twenty-seven years of experience in these markets and has produced numerous studies with regard to shipping market investments and port-feasibility. He is directly concerned with the interface between container shipping and ports and terminals.

Mr Penfold has been working on the ULCS project in conjunction with Lloyd's Register since 1999 and has been responsible for the shipping economics input into these studies. The issues of effective port turnaround times and vessel scale economies have been at the centre of the analyses.

Lloyd's Register, its affiliates and subsidiaries and their respective officers, employees or agents are, individually and collectively, referred to in this clause as the ‘Lloyd's Register Group’. The Lloyd's Register Group assumes no responsibility and shall not be liable to any person for any loss, damage or expense caused by reliance on the information or advice in this document or howsoever provided, unless that person has signed a contract with the relevant Lloyd's Register Group entity for the provision of this information or advice and in that case any responsibility or liability is exclusively on the terms and conditions set out in that contract.

9

Panel Discussion 1 – Curricula Vitae

Chairman Jonathan Lux – Ince & Co. Partner, London

Practice Areas: Shipping & Trade, Commercial Disputes, Energy, Insurance & Reinsurance An expert on fuel supply and co-author of a text book on bunkers, Jonathan specialises in maritime, energy, marine insurance, international trade and international commercial arbitration and litigation. He heads Ince's Logistics team in London. Jonathan acts for, among others, oil industry and cargo interests, the sellers and buyers of oil and gas, the major P&I Clubs, their shipowner and charterer members, and major insurers. A pioneer in the introduction of ADR into his fields of practice and an accredited mediator, he is also a practising arbitrator and Fellow of the Institute of Arbitrators. Jonathan is author of a number of leading texts in the law of shipping, insurance, corporate social responsibility and ADR. He is a member of the Steering Group of the London Shipping Law Centre and is listed in Chambers Global Directory as a leading international shipping lawyer in London. His experience as a racing driver assists him in his motorsports practice. He was instrumental in setting up and then served for two years as senior partner of the Hamburg office of Ince & Co, returning to London in 2004. Specialist areas: Alternative Dispute Resolution, Arbitration, Asset Recovery, Cargo Recovery & Defence, Charterparties, E-Commerce, Energy Insurance, EU & Competition, International Trade & Commodities, Litigation, Marine Insurance, Contract Disputes, Passenger and Cruise Ships, Protection & Indemnity Insurance, Renewable Energy, Shipbuilding, Ship Finance and Sale & Purchase, Sport, Bunkers and Yachts & Superyachts [email protected]

~~~~~~

Jesper Kjaedegaard - The Maersk Co. Ltd Jesper Kjaedegaard, born in 1958 in Denmark, was appointed Chief Executive Officer of The Maersk Company Limited in 2005. He has been with the A.P.Moller - Maersk Group for 29 years and has spent 16 of those years in various management positions overseas, most recently in the Far East and Middle East. He is a member of the Board of the British Chamber of Shipping, the Moller Centre/Churchill College, Cambridge, Chairman of the Pentalver Group and Roadways Container Logistics (RCL). He also holds directorships in several other companies within the A.P.Moller-Maersk Group. Jesper holds a degree from Copenhagen School of Commerce and has supplemented this education with post graduate studies at Insead in France, Cornell University and Harvard Business School (AMP). Hobbies include golf and football.

~~~~~~

Tim Kent – Lloyd’s Register A professional engineer with significant practical experience of design, development and production within heavy engineering industries, now in a senior strategic planning role within the marine business of Lloyd’s Register, a leading ship classification society. Employment history 4/2007 – Present Director, Marine Strategy & Planning, Lloyd’s Register, London 4/2000 – 4/2007 Manager, Marine Business Development, Lloyd’s Register, London Responsible for ensuring Lloyd’s Register maintains a thorough understanding of the current - and probable future - commercial, regulatory and technical environment within the marine industry – and that a practical strategy and plan is in place to ensure our overall purpose ‘to protect life and the marine environment’ can be met and sustained for the long term. This is achieved through leading a multi-professional, multi-national, team of engineers, finance, knowledge management, and business professionals, all collaborating closely with colleagues globally.

Since early 2007 and the establishment of a Global Marine Management Team as part of our strategy, this role has become far more ‘hands-on’! 6/1998 – 4/2000 Manager, Business Systems Integration, Lloyd’s Register, London Global project manager for implementation and integration of new business management and technical reporting systems. 1/1996 – 6/1998 Senior Surveyor, Lloyd’s Register, Yokohama & Kobe, Japan Classification and statutory surveys on ships and equipment under construction and ships in-service. 1/1994 – 12/1995 Assistant to Chief Engineer Surveyor, Lloyd’s Register, London General management and technical assistance to executive director. 3/1992 – 12/1993 Surveyor, Machinery Design & Dynamics, Lloyd’s Register, Croydon Design appraisal & approval of propulsion & auxiliary machinery. 9/1988 – 2/1992 Design Engineer, Hayward Tyler Ltd, Luton, UK Design of rotating equipment & pressure plant for power and offshore. 6/1987 – 8/1988 Design Engineer, Xerox Corporation, UK Electro-mechanical transmission design. 9/1985 – 6/1987 Development Engineer, Ricardo Consulting Engineers, UK Propulsion, auxiliary and automotive engine R&D projects. 9/1981 – 6/1985 Student Apprentice, Ministry of Defence, UK Professional qualifications 1992 MSc, Cranfield Institute of Technology, Machinery Design, Noise & Vibration 1991 CEng Chartered Engineer & Member, Institution of Mechanical Engineers 1985 BSc (hons) University of Southampton, Mechanical Engineering

~~~~~~

![Enforcement QBD (Comm Ct)] The “Prestige” LLOYD’S ... Lines Ltd v High Seas Shipping Ltd (The Eastern Navigator) [2005] EWHC 3020 (Comm); [2006] 1 Lloyd’s Rep 537; Dallah Real](https://static.fdocuments.net/doc/165x107/5af782877f8b9a9e5990d2a9/enforcement-qbd-comm-ct-the-prestige-lloyds-lines-ltd-v-high-seas.jpg)