Shifting Property Taxes - Tax Admin Property Taxes: ... [email protected] 2 1 Presentation...

18

1 Shifting Property Taxes: A Case Study of Minnesota’s “Limited Market Value” Presentation to Federation of Tax Administrators Revenue Estimated Conference Tax Research Division Minnesota Department of Revenue September 18, 2007 [email protected] 2 1 Presentation Outline What is “Limited Market Value”? Limited Value by Property Type and Region Tax Impact by Property Type Tax Impact on Individual Home and Cabin Owners (parcel level analysis) Tax impact variation by home value

Transcript of Shifting Property Taxes - Tax Admin Property Taxes: ... [email protected] 2 1 Presentation...

1

Shifting Property Taxes:

A Case Study ofMinnesota’s “Limited Market Value”

Presentation toFederation of Tax AdministratorsRevenue Estimated Conference

Tax Research DivisionMinnesota Department of Revenue

September 18, [email protected]

2 1

Presentation Outline

What is “Limited Market Value”?

Limited Value by Property Type and Region

Tax Impact by Property Type

Tax Impact on Individual Home and CabinOwners (parcel level analysis)

Tax impact variation by home value

2

3

What is “Limited Market Value?”

2

________________________________Ramsey County 2003 Property Tax StatementProperty Tax and Revenue 2003 Value Notice Information

16 Assessment Date, January 2, 2001, January 2, 2002, January 2, 2003, Taxes payable year payable 2002 payable 2003 payable 2004

17 Estimated Market Value $129,000 $139,600 $161,000

18 Limited Market Value $113,600 $125,000 $140,000

________________________________

Taxable Value reduced about 15%, so my taxes are down about 15% too.

4

Preview: Three Surprises

Surprise #1: Homeowners as a group arenet losers in 2007! (They pay more tax.)

Surprise #2: One-third of homeownerswhose value is limited are still losers!

Surprise #3: Taxable value rose fasterthan market value in 2007 (because ofLMV).

Will LMV be allowed to expirefor taxes payable in 2010?

3

5

What is “Limited Market Value?”

A limit on annual growth in the dollar valuesubject to property taxation.

LMV applies only to “preferred classes”: Residential homestead and non-homestead; Agricultural homestead and non-homestead; Seasonal recreational residential (cabins); and Timberland (added in 2001).

2

6

Does not apply to an increase in value dueto improvements.

Not owner-specific. LMV applies to theparcel, so carries over to a new owner.

Value limit restricts neither the property taxrate nor the property tax levy.

If the property tax levy is fixed, then LMVshifts tax burden to other properties.

3

Limited Market Value

4

7

For assessment year 2006 (taxes payable2007), the increase in taxable value cannotexceed the larger of:

15% of previous year’s TMV; or 25% of the difference between new EMV

and previous year’s TMV.

where TMV = Taxable Market Value EMV = Estimated Market Value

(full market value, assessed annually)

4

8

Limited Market Value (LMV) – Example 1

5

$200 $200 $200 $200

$30 $40 $50

$120$150

$20

$30

$0

$100

$200

$300

$400

$500

10% 30% 80% 100%

Percent Increase in EMV for Pay 2007

2005 TMV Increase in TMV Untaxed Value

($ T

hous

ands

)

TMV+10%

TMV+15%

TMV+20%

TMV+25%

Impact of Limited Market Value for Pay 2007 TaxesHome with TMV = EMV = $200,000 for Pay 2006 Taxes

5

9

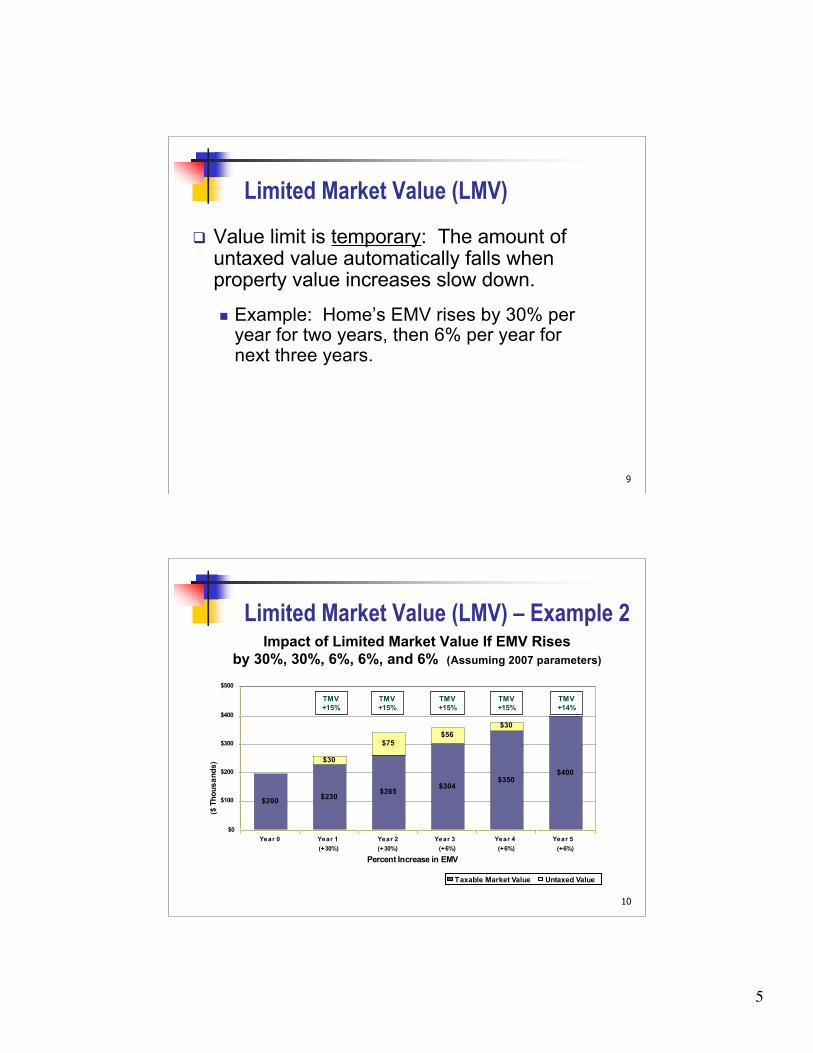

Value limit is temporary: The amount ofuntaxed value automatically falls whenproperty value increases slow down.

Example: Home’s EMV rises by 30% peryear for two years, then 6% per year fornext three years.

Limited Market Value (LMV)

6

10

Limited Market Value (LMV) – Example 2

($ T

hous

ands

)

$200$230

$265$304

$350$400

$75$56

$30

$30

$0

$100

$200

$300

$400

$500

Year 0 Year 1

(+30%)

Year 2

(+30%)

Year 3

(+6%)

Year 4

(+6%)

Year 5

(+6%)

Percent Increase in EMV

Taxable Market Value Untaxed Value

TMV+15%

TMV+15%

TMV+15%

TMV+15%

TMV+14%

Impact of Limited Market Value If EMV Risesby 30%, 30%, 6%, 6%, and 6% (Assuming 2007 parameters)

6

11

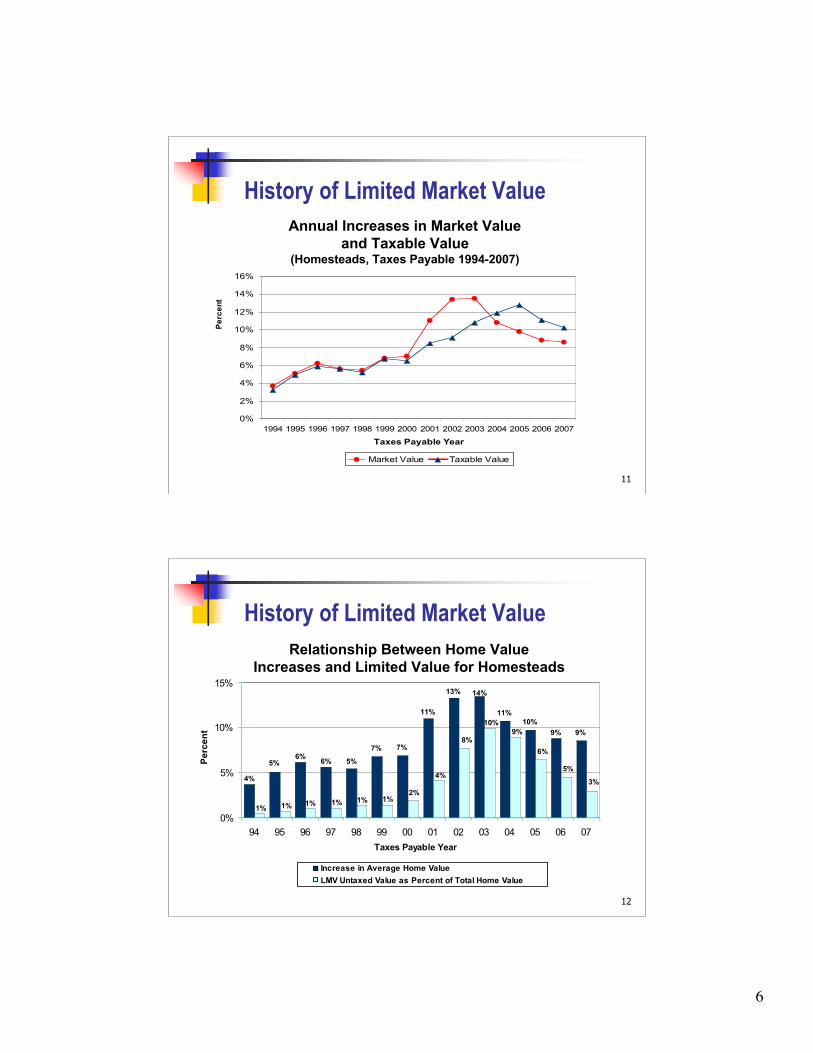

Annual Increases in Market Valueand Taxable Value

(Homesteads, Taxes Payable 1994-2007)

0%

2%

4%

6%

8%

10%

12%

14%

16%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Taxes Payable Year

Market Value Taxable Value

Perc

ent

8

History of Limited Market Value

12

History of Limited Market Value

7% 7%

11%

10%

9%

6%

9%

11%

13% 14%

4%

5% 5%6%

3%

2%

6%

5%

9%

10%

4%

8%

1%1%1%1%1%1%

0%

5%

10%

15%

94 95 96 97 98 99 00 01 02 03 04 05 06 07

Taxes Payable Year

Increase in Average Home Value

LMV Untaxed Value as Percent of Total Home Value

Perc

ent

Relationship Between Home ValueIncreases and Limited Value for Homesteads

7

1310

History of Limited Market Value

Percent Increase

Above Previous

Year's TMV

or

Percent of Difference

Between EMV and

Previous Year's TMV

1973-74 5% -

1975-79 10% 25%

1980 10% 50%

1993-96 10% 33%

1997-02 10% 15%

2003 12% 20%

2004 15% 20%

2005-07 15% 25%

2008 15% 33%

2009 15% 50%

NO LMV 2010 AND AFTER

Residential, agriculture, and cabins.

All Property

Residential, agriculture, and cabins

(plus timber starting 2001).

Preferred Classes

Maximum increase in taxable market value

is larger of:

Payable

Year(s)

NO LMV 1981-1992

14

History of Limited Market ValueTotal Nontaxable Market Value due to LMV

(all property types combined)Highest in 2004, but very little decline.

$1.0 $1.6 $2.0 $2.5 $3.4$5.6

$10.6

$21.0

$30.9

$34.9$33.1

$32.5$33.0

$0

$5

$10

$15

$20

$25

$30

$35

$40

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Taxes Payable Year

($ B

illio

ns)

11

8

15

History of Limited Market Value

0%

5%

10%

15%

20%

25%

30%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Taxes Payable Year

Farms Seasonal Rec. Resid. Total Residential Total Statewide

Perc

ent

Statewide Limitation as a Percentof Estimated Market Value

(Before Limitation)

12

16

Statewide Market Value Limitationby Type of Property (2007)

Seasonal Rec.

16.6%

Non-homestead

11.3%

Homestead

29.9%

Timber

2.2%

Farms

40.1%

13

Limited Value by Property Type

9

17

Perc

ent o

f Sta

tew

ide

Lim

ited

Valu

e

Shares of Statewide Limited Market Valueby Property Type (2000-2007)

27

0%

25%

50%

75%

100%

2000 2001 2002 2003 2004 2005 2006 2007

Taxes Payable Year

Timber

Farm

Seasonal

Recreation

Non-Homestead

Residential

Homestead

18

Change in Market Value Limitationby Region

14

($ B

illio

ns)

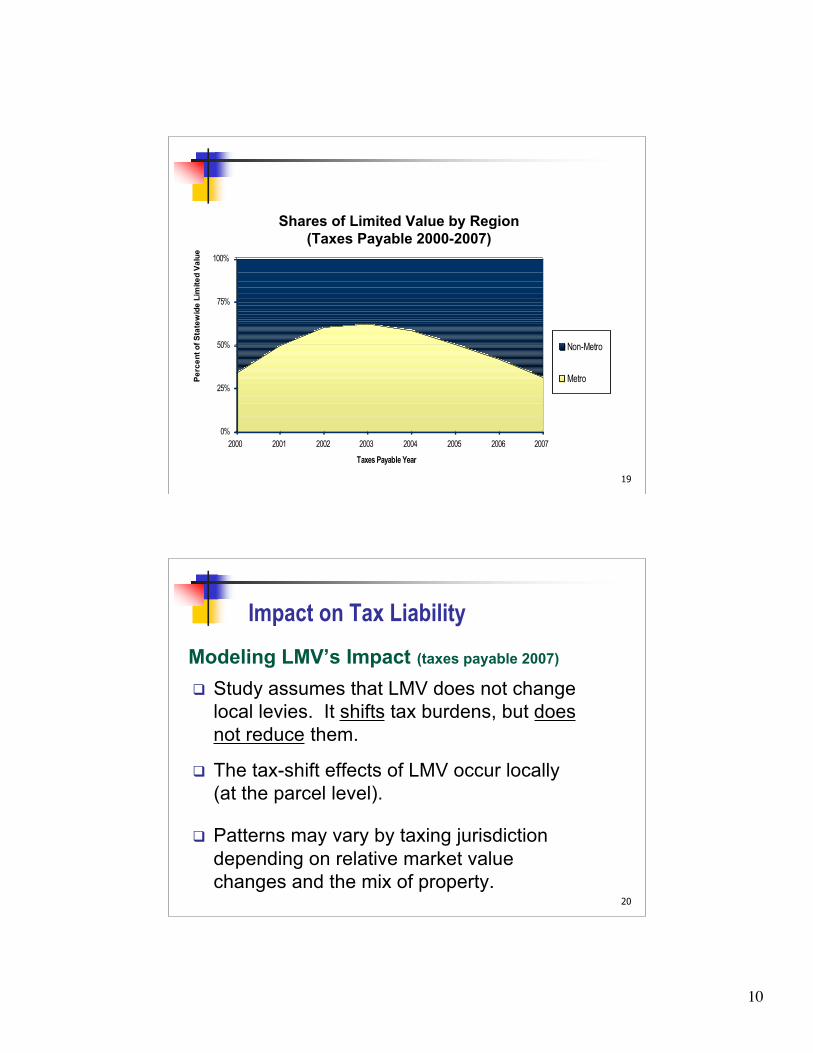

Limited Value by Region

10

19

Perc

ent o

f Sta

tew

ide

Lim

ited

Valu

e

Shares of Limited Value by Region(Taxes Payable 2000-2007)

27

0%

25%

50%

75%

100%

2000 2001 2002 2003 2004 2005 2006 2007

Taxes Payable Year

Non-Metro

Metro

20

Impact on Tax Liability

Modeling LMV’s Impact (taxes payable 2007)

Study assumes that LMV does not changelocal levies. It shifts tax burdens, but doesnot reduce them.

The tax-shift effects of LMV occur locally(at the parcel level).

Patterns may vary by taxing jurisdictiondepending on relative market valuechanges and the mix of property.

15

11

21

Impact on Tax Liability

Parcel-level data for assessment year 2006.

Calculates tax impact for taxes payable 2007: Add untaxed value (due to LMV) back to tax

base. Recalculate local tax rates (levies unchanged). Compute “no LMV” tax amounts for each

homestead and cabin parcel. Compute “no LMV” aggregate tax amounts for

other classes (not parcel-level).

Study Methodology

16

22

Impact on Tax Liability by Property Class

Average Percent Change in Property TaxDue to LMV, By Class of Property

Taxes Payable 2007 (Statewide)

-23.3%

-10.7%

-8.3%

-5.5%

1.3% 2.2% 3.8% 4.1%

13.2%

-24%

-20%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

16%

Metro

Timberland

Farms

Cabins

Non-Hmstd.

Hmstd.

C/I

Pub. Utilities

Apart.

Seasonal

Comm.

Perc

ent C

hang

e

17

12

23

Impact on Tax Liability – Homes

Tax Effects on Residential HomesteadsTaxes Payable 2007 (1.43 Million Parcels)

227,000 (16%) homeowners paid $64 millionless tax.

1,203,000 (84%) homeowners paid$110 million more tax. One-third of homes with limited value actually

paid more in tax (one-half for non-metro).

$46 million net loss to homeowners wasshifted on to homes from other classes.

18

24

Impact on Tax Liability –Homes

19

Limited Market Value Impactson Residential Homesteads

(Payable 2007)

0

100

200

300

400

500

600

-5,000

-3,000

-2,000

-1,000

-500

-300

-200

-100 -5

0 0 50 100

200

300

500

1,000

2,000

3,000

5,000

Estimated Homeowner Tax Change in Dollars

Coun

t of P

rope

rtie

s in

Tho

usan

ds

1,203,000 homeownerspay, on average, $92more tax.

227,000 homeowners pay,on average, $282 less tax.

Total TaxDecrease$64 Million

Total Tax Increase$110 Million

13

25

Percent with Limitation (Overall 25%) and

Percent who Gain (Overall 16%)Statewide (Pay 2007)

26% 25% 25%21% 22%

25%

33%

14% 16% 17%14% 14% 16%

23%

0%

10%

20%

30%

40%

50%

Under

$100

$100 to

$150

$150 to

200

$200 to

$250

$250 to

$300

$300 to

$400

Over

$400

Market Value of Home ($1000s)

Percent w ith

Value Limited

Percent

Gainers

LMV Variation by Home Market Value

30% of homes < $150,000.18% over $300,000 (and 8% over $400,000).

26

Percent with Limitation (Overall 24%) and

Percent who Gain (Overall 12%)Non-Metro (Pay 2007)

25%

18% 18%23%

30%

45%

13%10% 9% 11%

14%

25%

0%

10%

20%

30%

40%

50%

Under

$100

$100 to

$150

$150 to

200

$200 to

$250

$250 to

$300

Over

$300

Market Value of Home ($1000s)

Percent w ith

Value Limited

Percent

Gainers

57% of non-metro homes < $150,000.Only 8% over $300,000.

14

27

Percent with Limitation (Overall 26%) and

Percent who Gain (Overall 19%)Metro (Pay 2007)

39%

30%

20% 20% 21%

29%

34%

23%

15% 14% 14%

21%

0%

10%

20%

30%

40%

50%

Under

$150

$150 to

200

$200 to

$250

$250 to

$300

$300 to

$400

Over

$400

Market Value of Home ($1000s)

Percent w ith

Value Limited

Percent

Gainers

Only 7% of metro homes < $150,000.28% over $300,000 (and 13% over $400,000).

28

Average Limitation for Homes with LimitationStatewide

$7$14

$19$23

$28$36

$80

12%11%

11%10% 10% 10%

13%

0

20

40

60

80

100

120

Under $100 $100 to $150 $150 to 200 $200 to $250 $250 to $300 $300 to $400 Over $400

Market Value ($1000s)

$ T

ho

us

an

ds

0%

2%

4%

6%

8%

10%

12%

14%

Average ($1000s)

Ave. % of Value

15

29

Impact on Tax Liability – Cabins

LMV’s Effect on CabinsTaxes Payable 2007 (203,000 Parcels)

140,000 (69%) parcels paid $25 millionless tax.

63,000 (31%) parcels paid $7 millionmore tax.

$17.2 million net gain was shifted to otherclasses, and off of cabins.

20

30

Impact on Tax Liability – Cabins

21

0

10

20

30

40

50

60

-5,000

-3,000

-2,000

-1,000

-500

-300

-200

-100 -5

0 0 50 100

200

300

500

1,000

2,000

3,000

5,000

Estimated Seasonal Recreational Residential Tax Change in Dollars*

Coun

t of P

rope

rtie

s in

Tho

usan

ds 63,000 seasonalrecreational residentialproperties pay, onaverage, $110 more tax.

140,000 seasonalrecreational residentialproperties pay, onaverage, $179 less tax.

*Includes state tax. State tax rate adjusted to hold state tax amount constant.

Total Tax Decrease$25 Million

Total Tax Increase$7 Million

Limited Market Value Impactson Seasonal Recreational Residential Property

(Payable 2007)

16

31

LMV illustrates the distributional impacts ofshifts in property tax burdens. Fiscal illusion – many who think they benefit

really do not. Many who think they areunaffected are really losers.

Benefits shift to type of property that is risingmost rapidly (farms and cabins).

22

Conclusions

32

Impact much different in metro than non-metro. Typical impact varies by home value – but not

in extreme way. Always some uneasiness with cutting taxes for

those whose home values are rising faster atthe expense of those whose home values arestagnant.

Better understood by policymakers, and manyseem to prefer expanding targeted relief(circuit breaker).

23

Prospects for Completion of Phase-Out?

17

3324

Annual Increases in Taxable Value and Net Tax(Homesteads, 1996-2007)

-20%

-10%

0%

10%

20%

30%

40%

76 79 82 85 88 91 94 97 00 03 06

Taxes Payable Year

Pe

rce

nt

Taxable Value Net Tax

34

Annual Increases in Market Value and Taxable Value(Homesteads, 1996-2007)

0%

5%

10%

15%

20%

25%

30%

35%

40%

76 79 82 85 88 91 94 97 00 03 06

Taxes Payable Year

Pe

rce

nt

Market Value Taxable Value

25

18

35

0%

5%

10%

15%

20%

25%

30%

35%

40%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Taxes Payable Year

Farms Seasonal Rec. Resid. Total Residential Total Metro

Perc

ent

Limitation as a Percentage ofEstimated Market Value (Before Limitation)

Metro Area

26

36

0%

5%

10%

15%

20%

25%

30%

35%

40%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Taxes Payable Year

Farms Seasonal Rec. Resid. Total Residential Total Non-Metro

Perc

ent

Limitation as a Percentage ofEstimated Market Value (Before Limitation)

Non-Metro Area

27