Shekha & Mufti · The tax memorandum contains the ... 250 square yards or more or a flat of any...

42

Tax Memorandum 2017 Shekha & Mufti Chartered Accountants Shekha & Mufti is an independent member firm of Moore Stephens International Limited, members in principal cities throughout the world.

-

Upload

truongminh -

Category

Documents

-

view

214 -

download

0

Transcript of Shekha & Mufti · The tax memorandum contains the ... 250 square yards or more or a flat of any...

Tax Memorandum 2017

Shekha & Mufti Chartered Accountants

Shekha & Mufti is an independent member firm of Moore Stephens

International Limited, members in principal cities throughout the world.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 2 of 42

PREFACE

This tax memorandum summarizes crucial changes proposed in the Finance Bill 2017 in Income

Tax, Sales Tax, Federal Excise Duty and Customs Duty Laws.

All changes through the Finance Bill 2017 are effective from 01 July 2017 except where specifically

indicated.

The tax memorandum contains the comments, which represent our interpretation of the

legislation. We, therefore, recommend that while considering their application to any particular

case, reference be made to the specific wordings of the relevant statute(s).

The memorandum can also be accessed on our website www.shekhamufti.com

May 26, 2017

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 3 of 42

TABLE OF CONTENTS PAGE

INCOME TAX ORDINANCE, 2001

Changes In Provisions of Individual Taxation 4

Changes in Taxation of Companies 7

Changes in Income Tax Exemptions 9

Changes in Taxation of Non for Profit Organizations (NPOs); 10

Changes In Taxation of Non Residents 11

Other Important Changes; 12

Change in Withholding Provisions 15

Withholding Tax Chart 16

SALES TAX ACT, 1990 20

FEDERAL EXCISE ACT, 2005 35

CUSTOMS ACT, 1969 38

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 4 of 42

1- CHANGES IN PROVISIONS OF INDIVIDUAL TAXATION

INCOME TAX RETURN NOT TO BE FILED

(Section 115)

At present, income tax return is not required to be filed by the following;

1) A widow,

2) An orphan (under 25 years),

3) A disabled person,

4) A non-resident person

This applies, where the sole reason of filing the return was the ownership of immovable property of

250 square yards or more or a flat of any size located in areas falling under municipality or in any

cantonment or in Islamabad.

It is now proposed to excuse the above four (04) persons from filing even if they;

i) Own immovable property of 500 square yards or more;

ii) Own a flat of 2000 square feet or more in a rating area;

iii) Own a motor vehicle of more than 1000cc

REVISION OF WEALTH STATEMENT ONLY BEFORE NOTICE

(Section 116)

Currently, the wealth statement can be revised at any time before the assessment order under

Section 122 is issued and that too without any permission of the Commissioner.

It has now been proposed that Wealth Statement can only been revised before any notice is

issued. This means that even if the notice under section 122 has been issued, the door for revision

would close and the assessment proceedings will follow accordingly. This has perhaps been

intended to curb any mala fide practice on part of the taxpayer.

The provision for Commissioner approval remains the same. It is still not required.

LIMIT OF TAX FREE LOAN TO EMPLOYEE INCREASED TO RUPEES 1,000,000/-

[Section 13(7)]

Where a Company loan is given to any employee without interest or with lower interest than the

prescribed interest rate, the difference becomes part of his taxable salary and is called as notional

interest income of the employee.

At present, such loan is not chargeable under the head salary if the amount of loan is up to Rupees

500,000/-.

It has now been proposed that, this monetary limit of Rupees 500,000/- should now been enhanced

to Rupees 1,000,000/-.

The effective date of the above change is July 01, 2017.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 5 of 42

LIMIT FOR ELIGIBLE SALARY for EDUCATION ALLOWANCE INCREASED to Rs.1,500,000/- p.a.

(Section 64AB)/ (Section 60D)

Section 64AB has now been proposed to be renumbered as Section 60D.

At present, the tuition fee (education expense) is eligible for deduction from the taxable income.

Further this allowance is available only to one of the parent. However, this rebate/allowance could

only be claimed by individuals earning not more Rupees 1,000,000/- of Annual Income. It has now

been proposed this entitlement limit of Annual Income be enhanced from Rupees 1,000,000/- to

Rupees 1,500,000/-.

This is certainly a necessary change and in line with increasing education expenses to be

incentivized through tax law, however, the non-permission of adjustment of this education

allowance against the monthly tax deduction on Salary merely jeopardizes the whole scheme of

passing any practical tax benefit to employee.

TAX REBATE ON PURCHASE OF HEALTH INSURANCE POLICY

(Section 62A)

At present purchase of health insurance policy is entitled for tax Credit/Rebate which is allowed

on payment of premium to any health insurance company. The health insurance rebate is strictly

allowed only in case of salary income and / or business income.

The mechanism for calculation of tax rebate is based on the average rate of tax applicable on

the person with upper limit on the amount of eligible health insurance premium at the lower of

following:-

i) Actual Premium Payment

ii) 5% of Amount Taxable Income

iii) Rs.100,000/-

It has now been proposed that limit of the eligible Premium is enhanced from Rs.100,000/- to

Rs.150,000/-.

QUARTERLY ADVANCE TAX

(Section 147)

At present, an Individual person is not required to pay quarterly advance tax if its last taxable

income was not more than Rupees 500,000/-.

In the budget, the limit of taxable income has now been proposed to be enhanced from Rs.

500,000/- to Rs.1000,000/-.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 6 of 42

HIGHER TAX ON INTEREST INCOME

(Sections 7B)

In the budget, a new slab of rates has been suggested, whereby the tax incidence has been

increased.

SECTION HEAD

INDIVIDUAL/AOP

TAX RATES

EXISTING PROPOSED

Section

7B & 151

Interest

on

Income

Up to 25,000,000 10% Up to 5,000,000 10%

25,000,000 to

50,000,000

2,500,000 plus 12.5%

on exceeding of

25,000,000

5,000,000 to

25,000,000 12.5%

Up to 50,000,000

5,625,000 plus 15%

on exceeding of

50,000,000

Up to 25,000,000 15%

INTEREST ON INCOME (INDIVIDUAL/AOP)

COMPARISON BETWEEN EXISTING & PROPOSED

SLAB PROFIT INCOME TAX YEAR 2017 TAX YEAR 2018 INCREASE/(DECREASE)

1 5,000,000 500,000 500,000 -

2 10,000,000 1,000,000 1,250,000 250,000

3 20,000,000 2,000,000 2,500,000 500,000

4 25,000,000 2,500,000 3,125,000 625,000

5 30,000,000 3,125,000 4,500,000 1,375,000

6 40,000,000 4,375,000 6,000,000 1,625,000

7 50,000,000 5,625,000 7,500,000 1,875,000

8 60,000,000 7,125,000 9,000,000 1,875,000

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 7 of 42

2- CHANGES IN TAXATION OF COMPANIES

MINIMUM TAX ON SERVICE COMPANIES TO CONTINUE;

(Clause 94 of Part IV of Second Schedule)

Clause 94 of Part IV, was introduced by the Income Tax (Second Amendment) which provides

exemption from applicability of Minimum tax under section 153 b of the Ordinance on specified

corporate service sectors from 1st July‐2015 till 30 June 2016. However, specified service sectors will

be subjected to 2% Minimum tax if they file irrevocable undertaking to the Commissioner‐ IR for

submission of its accounts for income tax affairs for Tax Year 2016 or 2017, as the case may be.

Upon filing such undertaking, the Commissioner‐IR was empowered to issue exemption certificate

from withholding tax under section 153 by collecting 2% tax on entire turnover from all sources.

It has now been proposed by the Finance Bill to get it exempt from 8% minimum taxation by

extending the scheme of reduced tax rate of 2% up to 30th June of 2018. However, a company is

mandatorily required to submit the undertaking by November 2017.

It has, further, been proposed that services rendered by stock exchange will also enjoy the

exemption as available to other twelve (12) service sector for getting benefit under Clause 94 of

Part I of the Second Schedule.

TAX ON LISTED COMPANIES ON NON-PAYMENT OF DIVIDEND;

(Section 5A)

The tax @ 10% was imposed on Public Companies (other than a scheduled bank or a modaraba)

that do not distribute cash dividend equal to either forty per cent of its after tax profits or fifty per

cent of its paid up capital, whichever is less, within six months of the end of the tax year on their

reserves which are in excess of 100% of its paid up capital.

The bill has proposed to revamp this section entirely by replacing the undistributed reserves with

the undistributed profit of the Company. This is perhaps is in view of the litigation being faced by

tax authorities on the basis that reserves being accumulated from after tax profit cannot be taxed

again.

It has further been proposed to withdraw the minimum distribution limit of 50% of Paid up Capital

thereby increasing the tax burden on those companies availing concession previously by having

low paid up capital.

Further, the distribution option was restricted to cash dividend only which is now been proposed

to include bonus shares as well for the purpose of distribution to cater for those companies having

liquidity problems.

The due date for distribution for Companies having special year under Section 74 of the Ordinance

for the Tax Year 2017 would be in consonance with the due date for filing of Annual income tax

return.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 8 of 42

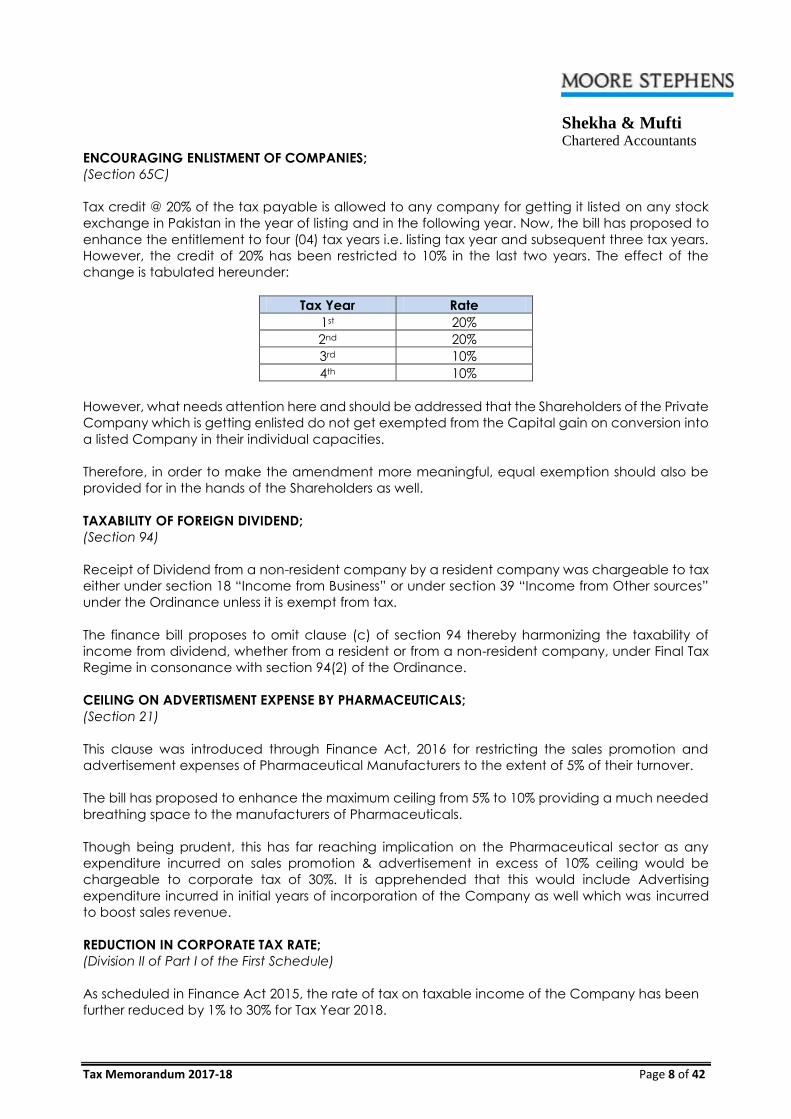

ENCOURAGING ENLISTMENT OF COMPANIES;

(Section 65C)

Tax credit @ 20% of the tax payable is allowed to any company for getting it listed on any stock

exchange in Pakistan in the year of listing and in the following year. Now, the bill has proposed to

enhance the entitlement to four (04) tax years i.e. listing tax year and subsequent three tax years.

However, the credit of 20% has been restricted to 10% in the last two years. The effect of the

change is tabulated hereunder:

Tax Year Rate

1st 20%

2nd 20%

3rd 10%

4th 10%

However, what needs attention here and should be addressed that the Shareholders of the Private

Company which is getting enlisted do not get exempted from the Capital gain on conversion into

a listed Company in their individual capacities.

Therefore, in order to make the amendment more meaningful, equal exemption should also be

provided for in the hands of the Shareholders as well.

TAXABILITY OF FOREIGN DIVIDEND;

(Section 94)

Receipt of Dividend from a non-resident company by a resident company was chargeable to tax

either under section 18 “Income from Business” or under section 39 “Income from Other sources”

under the Ordinance unless it is exempt from tax.

The finance bill proposes to omit clause (c) of section 94 thereby harmonizing the taxability of

income from dividend, whether from a resident or from a non-resident company, under Final Tax

Regime in consonance with section 94(2) of the Ordinance.

CEILING ON ADVERTISMENT EXPENSE BY PHARMACEUTICALS;

(Section 21)

This clause was introduced through Finance Act, 2016 for restricting the sales promotion and

advertisement expenses of Pharmaceutical Manufacturers to the extent of 5% of their turnover.

The bill has proposed to enhance the maximum ceiling from 5% to 10% providing a much needed

breathing space to the manufacturers of Pharmaceuticals.

Though being prudent, this has far reaching implication on the Pharmaceutical sector as any

expenditure incurred on sales promotion & advertisement in excess of 10% ceiling would be

chargeable to corporate tax of 30%. It is apprehended that this would include Advertising

expenditure incurred in initial years of incorporation of the Company as well which was incurred

to boost sales revenue.

REDUCTION IN CORPORATE TAX RATE;

(Division II of Part I of the First Schedule)

As scheduled in Finance Act 2015, the rate of tax on taxable income of the Company has been

further reduced by 1% to 30% for Tax Year 2018.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 9 of 42

3- CHANGES IN INCOME TAX EXEMPTIONS

NEW EXEMPTION TO LOCAL IT STARTUPS

(Clause 144 of Part I)

It is another convivial stance of legislator to nourish the Technological Driven Industry whereby, the

income earned by a Technology Driven Startup is fully exempt for three (03) years once after the

following criteria are met;

a) Registered Person (Individual, AOP or Company)

b) Incorporated on or after July 01, 2012

c) Engaged in only Technology Driven Products / Services.

d) Registered and Certified by Pakistan Software Export Board (PSEB).

e) Turnover is less than 100 million in each of the last five (05) years.

It is undoubtedly a welcoming drive towards expanding the Technology Driven Services in Pakistan.

Moreover, it is further proposed to be exempted from Minimum Tax under Section 113 and from

withholding of tax as well under the newly introduced Clause (43F) under Part IV of Second

Schedule to the Ordinance.

It is relevant to mention here that Technology Driven Products and Services need to be explained

specifically to get this exemption, otherwise the same will result in unnecessary assessment /

litigation proceedings.

LIMIT OF TAX FREE IMPORT OF RAW MATERIAL INCREASED.

(Clause 72B of Part IV)

Manufacturers cum importers have been enjoying the benefit of tax exemption at import stage

under Section 148 of the Ordinance which is restricted up to 110% of last year’s imports. The finance

bill proposes an increase in threshold from current 110% to 125% of raw materials as imported last

year.

EXEMPTION TO POLITICAL PARTIES

(Clause 142 of Part I)

It is interesting to note that this finance bill has for the first time in Pakistan’s budgetary history

proposes tax exemption to Political Parties in the country provided these are registered under the

Political Parties Order 2002 with the Election Commission of Pakistan.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 10 of 42

4- CHANGES IN TAXATION OF NON FOR PROFIT ORGANIZATIONS (NPOs);

Revenue measures have been proposed through this Finance Bill-2017-18 wherein 100% tax credit

available to NPOs have been further restricted and subjected to tax as follows:

1. Administration and Management Expenditures will be restricted to 15% of total receipts,

otherwise NPOs would not be entitled for 100% tax credit; and.

2. Surplus funds would not be entitled for 100% tax credit and instead will be subjected to

tax @ 10%.

We understand that the first condition of restricting expenditure to 15% appears encouraging as it

will promote more spending on welfare activities instead of disbursements on luxuries under the

garb of administration and management of the Trusts. However this condition along with others as

given in Section 100C(1) of the Ordinance could possibly have been routed through Rule 213 of

the Income Tax Rules, 2002. This Rule gives exhaustive list of conditions which need to be abided

by, otherwise approval as NPO will be refused by the concerned Commissioner-IR. As a result of

this proposed amendment, the NPO(s), we understand, which obtained the approval after fulfilling

the comprehensive requirements under Rule 213 will remain restrained from getting 100% tax

credit.

In respect of the Surplus funds the Finance Act proposes gross tax @ 10% whereby funds kept for

NPO activities would go to national kitty instead of utilizing to welfare / charitable functions. Funds

received during the year not utilized for charitable or welfare activities are defined as surplus funds.

Moreover there appears drafting error while defining the meaning of Surplus as ceiling of 25% of

the total receipts is also proposed to be taxed @ 10% without mentioning higher or lower of the

two.

It would not be out of place to mention here that in the past the exemption were duly granted to

NPO(s) under Second Schedule of the Ordinance which was done away through the Finance Act,

2014 by replacing 100% tax credit against tax payable by the NPO(s) under Section 100C of the

Ordinance. What now appears that after proposed amendment are in place the NPO(s) will fall

out from 100% tax credits and will, consequentially, be chargeable to 10% tax on surplus funds

subject to new conditions being proposed.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 11 of 42

5- CHANGES IN TAXATION OF NON RESIDENTS

ADVANCE RULING (NON-RESIDENT WITH PE CAN APPLY FOR)

(Section 206A)

Nonresidents are entitled for securing advance ruling for tax implication on a particular transaction

from FBR. However nonresidents having PE in Pakistan are forbidden for the same. The reason is

given that as foreign company with a PE in Pakistan is taxed as a resident company, therefore

advance ruling in such cases is likely to be attracted in the cases of resident companies as well.

Therefore in order to bring clarity in the application of advance ruling, nonresidents with PE in

Pakistan are currently barred for advance ruling, Circular 07/2011 to refer in this respect. However

disregarding earlier instance nonresidents having PE in Pakistan are now proposed to be entitled

for the advance ruling as well.

In such a case residents would be unfavorable situation therefore it is advisable that equal level

playing field can be provided to the residents by providing the facility of advance ruling to the

residents as well. This will further save the burdensome costs as incurred by taxpayers for securing

consultancy services. Not out of place to mention that advisory board of FBR may need to be

developed / fortified by engaging tax specialists and representations from the varied industries as

well.

CONSTRCUTION AND OTHER CONTRUCTS OF NON-RESIDENTS

(Section 152 (1A)

Nonresidents undertaking construction, assembly or installation contracts including services

thereto are subject to final tax. This can be done by filing the option for the same. However this

facility is subject to the condition that the same be filed within 03 months of the commencement

of the tax year, which will remain irrevocable for three years as given in Clause 41, Part IV, 2nd

Schedule to the Ordinance. This condition is done away by proposing deletion of the said

exemption clause. Option for assessment as final tax remains intact.

In cases where the above contracts continues for more than 90 days within any twelve month the

same will constitute the Permanent establishment (PE) of the nonresident which is subject to tax on

net profit basis instead of final tax on gross receipts. The bill now proposes that in such cases

nonresidents can apply for the tax exemption or lower rate certificate as well.

This amendment appears to be superfluous as PE of nonresidents are already entitled for

exemption / lower rate certificate for withholding taxes for the supply of goods, services and

contractual receipts.

ENHANCED TAX RATES FOR NON-FILERS (NON-RESIDENTS)

[Section (181 1A)]

The bill proposes enhanced withholding taxes in cases of nonresidents who are non-filer as well.

However this will have limited effect as FBR itself clarified that in cases of non-residents covered

under the tax treaty with the respective country will not be subject to higher tax due to protection

under the respective tax treaty.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 12 of 42

6- OTHER IMPORTANT CHANGES;

PROVISIONAL ASSESSMENT SUBSUMED INTO EXPARTE ASSESSMENT;

(Sections 122C & 21)

The Tax Officer is currently empowered to pass a provisional assessment of the taxpayer based on

available information with him and to the best of his/her judgment, if the taxpayer does not file his

tax return even after his notice.

This assessment would become invalid if the taxpayer would file the tax return within the period of

45 days. On the other hand, the provisional assessment would be treated as final assessment and

the recovery provisions of the Ordinance would apply after a lapse of another 30 days without the

right of appeal to the defaulting taxpayer.

Through this Budget 2017-18, it has been proposed to do away with the concept of provisional

assessment in isolation. It has be made part of the provisions contained under Section 121 of the

Ordinance for “Best Judgment Assessment”. The Taxation Officer is proposed to be empowered

under Section 121 of the Ordinance to make an assessment of the taxable income as per available

information or to the best of his judgment if the taxpayer fails to file his return.

What needs a serious attention by the taxpayers is that now there won’t be any long period of 45

days to linger on with the filing as after the Order passed by the Officer under Section 121 of the

Ordinance, the taxpayer will though have the right of appeal but will be assessed like any other

proceedings.

SUPER TAX CONTINUES TO CREEP IN 2017

(Section 4B)

The Federal Board of Revenue has constantly been applying / imposing this Super Tax on every

year. If we recall that the levy of Super Tax was introduced in the Tax Year 2015 and restricted

strictly for that Tax Year alone. However, it further enhanced and reintroduced the same in Tax

Year 2016.

Now with this Budget the Companies have once again been proposed to pay for super tax for the

Tax Year 2017 as well while filing their return of income for Tax Year 2017.

Here it is necessary to recap that super tax is payable @ 4% by banking companies without any

income ceiling and @ 3% by non‐banking companies with income more than Rupees 500 million.

The other details of the mechanism of this levy have remained the same. Income shall be the sum

of the following:

Profit on debts

Dividend Income

Capital Gains

Brokerage & Commission Income

Taxable income excluding above

Imputable income

Income under 4th, 5th, 7th and 8th Schedule

It remains important to mention here that after the decision of Apex Court on the issue of WWF,

the companies have opted to file a suit / petition in the Sindh High Court against the levy of Super

Tax instead of paying. The decision of Sindh High Court is still in pending.

It is likely that the companies / banks may further seek to file another Suit / Petition against the

Super Tax against this year as well.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 13 of 42

3% TAX CREDIT ON REGISTERED SALES TAKEN BACK

(Section 65A)

Through the Finance Act, 2009, the FBR introduced that every manufacturer registered under the

Sales Tax Act, 1990 would be entitled to claim tax credit @2.5% of the tax payable, if the 90% of its

sales are made to the registered persons.

In Finance Act, 2016, the rate of tax credit was further enhanced from 2.5% to 3% to promote and

encourage documentation of economy.

It is a case nothing short of irrational withdrawal of a very prudent and sane tax credit and that

too without any warning that instead of further enhancing the rate of tax credit or at least

maintaining the same, the FBR has surprisingly proposed to withdraw the whole of the 3% tax credit

altogether. This amendment has negative impact towards achieving the target of moving to

documented economy.

15% FLAT RATE OF TAX ON CAPITAL GAIN ON SHARES

(Section 37A)

Capital gain on shares has constantly been subject to varied and constant charges in its taxation

since it was firstly introduced in 2011. For e.g. Last Year, the tax rate on capital gain though

proposed to remain the same, the exemption as available in case of 48 months of holding of shares

however mere withdrawn.

This Year, the FBR took perhaps the lost attempt to withdraw the various holding periods starts from

less than 12 month to 48 months and has replaced all with a single rate of 15% invariably to all

periods of holding.

Meaning thereby, a flat rate of 15% would be applied on the capital gain of shares irrespective of

any holding period.

The adjustment and refund of excess tax deduction suffered on account of non‐filers which they

could get back once they file the returns remains the same.

A comparison of CGT rates between Tax Year 2017 and Tax Year 2018 and onwards in line with Filer

& Non‐Filer is being tabulated hereunder;

HOLDING PERIOD OF SECURITIES

TAX

YEAR

LESS THAN TWELVE

(12) MONTHS

BETWEEN TWELVE TO

TWENTY FOUR

MONTHS

TWENTY FOUR MONTHS OR

MORE BUT ACQUIRING

ON OR AFTER

1ST JULY, 2013

BEFORE

1ST JULY, 2013

Filer Non-Filer Filer Non-Filer Filer Non-Filer

2017 15% 18% 12.5% 16% 7.5% 11% Exempt

2018 15% 20% 15% 20% 15% 20% Exempt

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 14 of 42

ADVANCE TAX ON SALE OF PROPERTY WITHIN A YEAR IS MINIMUM TAX;

Societies to recover advance tax as well

(Section 236C)

Through the Federal Budget, 2012-2013, the Federal Board of Revenue introduced the collection

of Advance Tax by the person responsible for registering or attesting the immovable property at

the time of Sales / transfer of Property from the seller. This Advance Tax is adjustable for the Seller

at the time of filing of Tax Return.

If the proposition for including the word “recording” is placed in this Section, the person responsible

for recording the immoveable Property as well shall be liable to collect this Advance Tax at time

of recording transfer. After this amendment is in place, we understand that all the societies and

housing scheme societies, shall be covered under this Section.

It has further been proposed that the Advance Tax would be considered as minimum tax if the

Seller acquires and disposes off the Property within the same Tax Year.

It remains important to mention here that this minimum tax would not affect the taxation of Capital

gain on sales of immoveable property under Section 37 of the Ordinance.

CHIEF COMMISSIONER MAY GRANT EXTENSION

[Section 119(4)]

Currently the taxpayers approach the Chief Commissioner – IR office for getting the extension of

time after getting refusal / rejection from the concerned Commissioner - IR, which generally

remanded back to the concerned Commissioner on the ground that he does not have power to

grant the extension of time to file the Tax Return & Wealth Statement.

Since, there was no remedy available for the taxpayers, in the event if the concerned

Commissioner IR refuses / rejects to grant extension of time to file the Tax Return & Wealth

Statement, this Budget proposes to addressed this issue and proposes to empower the Chief

Commissioner – IR for granting the extension of time for filing of Income Tax Return or wealth

statement after getting refused / rejected by the concerned Commissioner – IR.

After this amendment, the Chief Commissioner – IR may grant the extension & further extension of

time for the period not exceeding 15 days’ time unless there are exceptional circumstances for

more extensions.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 15 of 42

7- CHANGE IN WITHHOLDING PROVISIONS

REVISION OF WITHHOLDING STATEMENTS ALLOWED

(Section 165 2A)

A new sub-section 2A under section 165 has been proposed hereunder the withholding statement

can be revised. This would be the first time ever that revision of withholding tax statement has been

proposed to be allowed. It has been proposed that withholding statement can be revised within

the sixty (60) days. Under the current, there was no such provision to revise withholding tax

statement in case of any omission or wrong statement e-filed.

Lastly, the revision is proposed to be allowed without any prior approval from the Commissioner of

Income Tax.

ADVANCE TAX ON TOBACCO

[Section 236X]

The Bills proposes to insert a new section, whereby, Pakistan Tobacco Board, at the time of

collecting cess on tobacco, directly or indirectly, shall collect advance tax @ 5% (five percent) of

the purchase value of tobacco from every person purchasing tobacco including manufacturers

of cigarettes. The tax so collected will be adjustable.

ADVANCE TAX ON PRIVATE MOTOR VEHICLES

(Section 231B)

Under the present law, advance tax is to be collected from non-filers @ 3% of value of the motor

vehicle where the vehicle is being leased by a leasing company, scheduled bank, investment

bank, Development Financial Institution or a Modaraba.

The Bill seeks to include non-banking financial institution in this list and leasing under Islamic mode

of financing to cover vehicles being leased under shariah compliant or conventional mode, either

through Ijara or otherwise.

It is further proposed that such tax will not be collected in case of vehicle leased under the Prime

Minister’s Youth Business Loan Scheme.

COLLECTION OF TAX BY STOCK EXCHANGE

(Section 233A)

Currently, advance tax is collected by Pakistan Stock Exchange Limited (PSX) on sale and

purchase of shares in lieu of Commission by its members @ 0.02% on the gross value of sales or

purchase, which is adjustable tax. The Bill seeks of this collection of advance tax as a final tax

liability.

ADVANCE TAX ON ELECTRICITY BILL BY A CNG STATION

(Section 234A & 235)

Currently, advance tax collected on consumption of electricity by industrial or commercial user is

adjustable. The Bill proposes that advance tax on electricity consumption by CNG station may be

made final tax liability on income of CNG stations in addition to 4% advance tax liability on their

gas consumption.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 16 of 42

INCOME TAX WITHHOLDING CHART

(Income Tax Ordinance, 2001)

TAX YEAR 2018

w.e.f. July 01, 2017

IMPORTS

SALARY

DIVIDEND

INTEREST

NON-RESIDENT

GOODS, SERVICE & CONTRACTS

EXPORTS

RENT

PRIZE AND WINNINGS

PETROL & CNG

TOBACCO

WITHDRAWALS FROM BANK

PURCHASE OF MOTOR VEHICLES

BROKERAGE AND COMMISSION

SHARES SALE & PURCHASE

ELECTRICITY

PHONE & INTERNET

AIR TICKET

PROPERTY SALE & PURCHASE

DISTRIBUTORS, DEALERS, WHOLESALERS

EDUCATION EXPENSE

OTHERS

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 17 of 42

Section Payment / Transaction Withholding Tax Rates

A. IMPORTS Individuals & AOPs (Manufacturers)

Individuals and AOPs (Non-Manufacturers)

Companies (Manufacturers or not) IM

PO

RTS

148 Imports Filer Non Filer Filer Non Filer Filer Non Filer

5.5% 8% 6% 9% 5.5% 8%

B. SALARY Slabs Rates

S A L A

R Y

149 Salary

Slab Rate on

Exceeding Amount Fixed Tax

Up to 400,000 Nil Nil

400,001 to 500,000 2% Nil

500,001 to 750,000 5% 2,000

750,001 to 1,400,000 10% 14,500

1,400,001 to 1,500,000 12.5% 79,500

1,500,001 to 1,800,000 15% 92,000

1,800,001 to 2,500,000 17.5% 137,000

2,500,001 to 3,000,000 20% 259,500

3,000,001 to 3,500,000 22.5% 359,500

3,500,001 to 4,000,000 25% 472,000

4,000,001 to 7,000,000 27.5% 597,000

7,000,001 and above 30% 1,422,000

C. DIVIDEND IND./AOP Companies

DIV

IDEN

D

150

Cash Dividend

Filer Non Filer Filer Non Filer

15% 20% 15% 20%

Stock Fund 12.5%

Money Market Fund, Income Fund or REIT Scheme or any other fund

12.5% 15% 25%

236M Bonus Shares (Quoted) 5%

236N Bonus Shares (Un-Quoted)

236S Specie Dividend 12.5% 20%

D. INTEREST Filer Non Filer

INTER

EST

151 Interest

10% 17.5% (If > 500,000/- p.a.)

151(1)(a) Interest on National Saving Scheme (NSS)

151(1)(b) Interest on Bank Account

151(1)(c) Interest on Federal Government, Provincial Government & Local Government Bonds

151(1)(d) Interest on Company Loans

E. NON-RESIDENT

NO

N - R

ESIDEN

T

152(1) Royalty or Fee for Technical Services 15%

152(1A) Construction Contract

Filer Non Filer

7% 13% Construction Services

Advertisement by TV Satellite Channels

152(1AAA) Media Person Advertisement Services 10%

152(2A)

(a) Supply Of Goods

Companies IND./AOP

Filer Non Filer Filer Non Filer

4% 7% 4.5% 7.75%

(b) Services 8% 14% 10% 17.5%

(c) Contract 7% 13% 7% 13%

Sportsman 10%

152A Foreign Produced Commercial 20%

F. GOODS , SERVICES & CONTRACTS Companies IND./AOP

GO

OD

S , SERV

ICES &

CO

NTR

AC

TS

153(1)(a)

Rice, Cotton Seed Oil, Edible Oils

Filer Non Filer Filer Non Filer

1.5%

Other Goods 4% 7% 4.5% 7.75%

153(1)(ab) Distributors of FMCG (excluding durable goods) 2% 2.5%

153(1)(b)

Services 8% 14.5% 10% 17.5%

Transport Services 2%

Electronic and Print Media Advertising Services 1.5% 12% 1.5% 15%

153(1)(c ) Contracts 7% 12% 7.5% 12.5%

Sportsman 10%

153(2) Stitching, Dying, Printing, Embroidery etc. 1%

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 18 of 42

G. EXPORTS Filer Non Filer

EXP

OR

TS

154 Exports 1%

154(1) Export of Goods 1%

154(2) Export Commission 5%

154(3) Inland Bank to Bank Letter of Credit 1%

154(3A) Export Processing Zone 1%

154(3B) Indirect Exporter; SPO 1%

H. RENT Company IND./AOP

R E N

T

155 Rent (On Gross Rental Payment)

Filer Non-Filer Slabs Rate on

Exceeding Amount Fixed Tax

15% 17.5%

Up to 200,000 Nil Nil

200,000 to 600,000 5% Nil

600,000 to 1,000,000 10% 20,000

1,000,000 to 2,000,000 15% 60,000

Above 2,000,000 20% 210,000

I. PRIZE AND WINNINGS Companies/ IND./AOP

PR

IZE &

WIN

NIN

G

156 Prize Bonds

Filer Non Filer

15% 25%

Prizes, Winning, Lottery, Raffles 20%

J. PETROL AND CNG Companies/ IND./AOP

PETR

OL

& C

NG

156A Petrol & Petroleum Products Filer Non Filer

12% 17.5%

234A CNG Stations 4% 6%

K. WITHDRAWALS FROM BANK Filer Non Filer

BA

NK

231A Cash Withdrawal 0.3% (if > 50k pd) 0.6% (if> 50k pd)

231AA Bearer Banking Transaction 0.3% 0.6%

236P Crossed Banking Transaction 0% 0.4% (if > 50k) (Ext. till 31st Aug 2016)

L. PURCHASE OF MOTOR VEHICLES Engine Capacity Filer Non Filer

PU

RC

HA

SE OF M

OTO

R V

EHIC

LES

231B(1A) At the time of Motor Vehicle Leasing Any Motor Vehicle - 3%

231B(1) & (3)

On Registration by Excise & Taxation Dept.

&

On Sale by Manufacturer (Car or Jeep)

Up to 850cc 7,500 10,000

851cc to 1000cc 15,000 25,000

1001 to 1300cc 25,000 40,000

1301cc to 1600cc 50,000 100,000

1601cc to 1800cc 75,000 150,000

1801cc to 2000cc 100,000 200,000

2000cc to 2500cc 150,000 300,000

2500cc to 3000cc 200,000 400,000

Above 3000cc 250,000 450,000

231B(2) Transfer or Ownership (Tax rate shall be reduced by 10% each year from the date of 1st registration)

Engine Capacity Filer Non Filer

Up to 850cc - 5,000

851cc to 1000cc 5,000 15,000

1001 to 1300cc 7,500 25,000

1301cc to 1600cc 12,500 65,000

1601cc to 1800cc 18,750 100,000

1801cc to 2000cc 25,000 135,000

2000cc to 2500cc 37,500 200,000

2500cc to 3000cc 50,000 270,000

Above 3000cc 62,500 300,000

234 Private Motor Vehicle

Engine Capacity Filer Non Filer

Up to 1000cc 800 1,200

1001cc to 1199cc 1,500 4,000

1200cc to 1299cc 1,750 5,000

1300cc to 1499cc 2,500 7,500

1500cc to 1599cc 3,750 12,000

1600cc to 1999cc 4,500 15,000

2000cc & above 10,000 30,000

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 19 of 42

M. BROKERAGE AND COMMISSION Companies/ IND./AOP

BR

OK

ERA

GE A

ND

CO

MM

ISSION

233 Advertising Agents

Filer Non Filer

10% 15%

Life Insurance Agent (If < 0.5 million) 8% 16%

Other Commissions 12% 15%

236J Commission Agents (Fruits & Vegetables) and Arhatis

Group Amount of Tax (p.a.)

Group or Class A 10,000

Group or Class B 7,500

Group or Class C 5,000

Any Other Category 5,000

N. SHARES SALE & PURCHASE Description Rate

SHA

RES

233A Collection by Pakistan Stock Exchange Purchase of Shares 0.02% of Purchase Value

Sale of Shares 0.02% of Sale Value

233AA Collection by NCCPL 10%

O. ELECTRICITY (ON GROSS)

ELECTR

I

CITY

235 Commercial 12%

Industrial Not < 75,000 0%

235A Domestic Exceeding 75,000 7.5%

P. PHONE & INTERNET

PH

ON

E &

INTER

NET

236

Telephone Bill

12.5% Internet Bills

Phone Cards

Q. AIR TICKETS

AIR

TICK

ET

236B Domestic Air Tickets (Except Baluchistan Coastal Belt, Azad Jammu Kashmir, FATA Gilgit, Baltistan and Chitral)

5%

236L

International Air Tickets Companies/ IND./AOP

First/Executive Class 16,000/- Per Person

Others Excluding Economy 12,000/- Per Person

Economy 0

R. PROPERTY SALE AND PURCHASE Filer Non Filer

PR

OP

ERT

Y

236C Sale of Property 1% 2%

236K Purchase of Property Up to 3 million 0%

More than 3 million 2% 4%

S. DISTRIBUTORS, DEALERS, WHOLESALERS Filer Non Filer

DISTR

IBU

TOR

S

DEA

LER

236G Fertilizers 0.7% 1.4%

Other than Fertilizers 0.1% 0.2%

236H

Sales to Retailers/Wholesalers by Distributors/Dealer

Electronics 1% 1%

Others 0.5% 1%

T. EDUCATION EXPENSES

EDU

C

ATION

236I For Institutions in Pakistan 5%

236R For Institutions outside Pakistan

U. TOBACCO

TOB

A

CC

O

236X On the purchase value of Tobacco 5%

V. OTHERS

O T H

E R S

156B Voluntarily Pension Scheme 3 years Average 3 years Average

235B Steel Melters, Re-roller etc. 1/- per unit of Electricity

236D Functions and Gatherings 5%

236F Cable Operators As per slab.

236Q Rent of Machinery and Equipment 10%

236U Premium by Insurance Companies

Non Filer Only

Types of Premium Rate

General Insurance Premium 4%

Life Insurance Premium if exceeding of Rs.0.3 Million per annum

1%

Others 0%

236V Extraction of Minerals Filer Non Filer

0% 5%

236A Auction 10% 15%

236O Advance tax under this chapter shall not be collected from

Federal Government , Provincial Government Foreign Diplomats, Diplomatic Mission Exemption Certificate

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 20 of 42

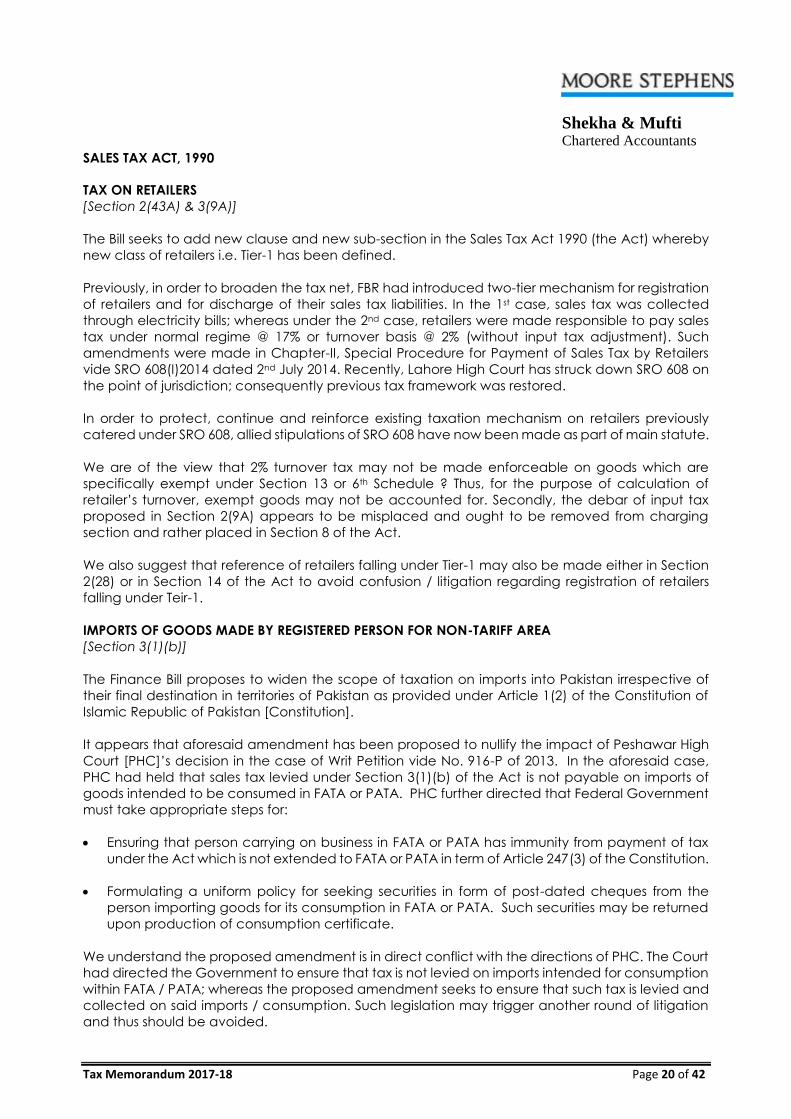

SALES TAX ACT, 1990

TAX ON RETAILERS

[Section 2(43A) & 3(9A)]

The Bill seeks to add new clause and new sub-section in the Sales Tax Act 1990 (the Act) whereby

new class of retailers i.e. Tier-1 has been defined.

Previously, in order to broaden the tax net, FBR had introduced two-tier mechanism for registration

of retailers and for discharge of their sales tax liabilities. In the 1st case, sales tax was collected

through electricity bills; whereas under the 2nd case, retailers were made responsible to pay sales

tax under normal regime @ 17% or turnover basis @ 2% (without input tax adjustment). Such

amendments were made in Chapter-II, Special Procedure for Payment of Sales Tax by Retailers

vide SRO 608(I)2014 dated 2nd July 2014. Recently, Lahore High Court has struck down SRO 608 on

the point of jurisdiction; consequently previous tax framework was restored.

In order to protect, continue and reinforce existing taxation mechanism on retailers previously

catered under SRO 608, allied stipulations of SRO 608 have now been made as part of main statute.

We are of the view that 2% turnover tax may not be made enforceable on goods which are

specifically exempt under Section 13 or 6th Schedule ? Thus, for the purpose of calculation of

retailer’s turnover, exempt goods may not be accounted for. Secondly, the debar of input tax

proposed in Section 2(9A) appears to be misplaced and ought to be removed from charging

section and rather placed in Section 8 of the Act.

We also suggest that reference of retailers falling under Tier-1 may also be made either in Section

2(28) or in Section 14 of the Act to avoid confusion / litigation regarding registration of retailers

falling under Teir-1.

IMPORTS OF GOODS MADE BY REGISTERED PERSON FOR NON-TARIFF AREA

[Section 3(1)(b)]

The Finance Bill proposes to widen the scope of taxation on imports into Pakistan irrespective of

their final destination in territories of Pakistan as provided under Article 1(2) of the Constitution of

Islamic Republic of Pakistan [Constitution].

It appears that aforesaid amendment has been proposed to nullify the impact of Peshawar High

Court [PHC]’s decision in the case of Writ Petition vide No. 916-P of 2013. In the aforesaid case,

PHC had held that sales tax levied under Section 3(1)(b) of the Act is not payable on imports of

goods intended to be consumed in FATA or PATA. PHC further directed that Federal Government

must take appropriate steps for:

Ensuring that person carrying on business in FATA or PATA has immunity from payment of tax

under the Act which is not extended to FATA or PATA in term of Article 247(3) of the Constitution.

Formulating a uniform policy for seeking securities in form of post-dated cheques from the

person importing goods for its consumption in FATA or PATA. Such securities may be returned

upon production of consumption certificate.

We understand the proposed amendment is in direct conflict with the directions of PHC. The Court

had directed the Government to ensure that tax is not levied on imports intended for consumption

within FATA / PATA; whereas the proposed amendment seeks to ensure that such tax is levied and

collected on said imports / consumption. Such legislation may trigger another round of litigation

and thus should be avoided.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 21 of 42

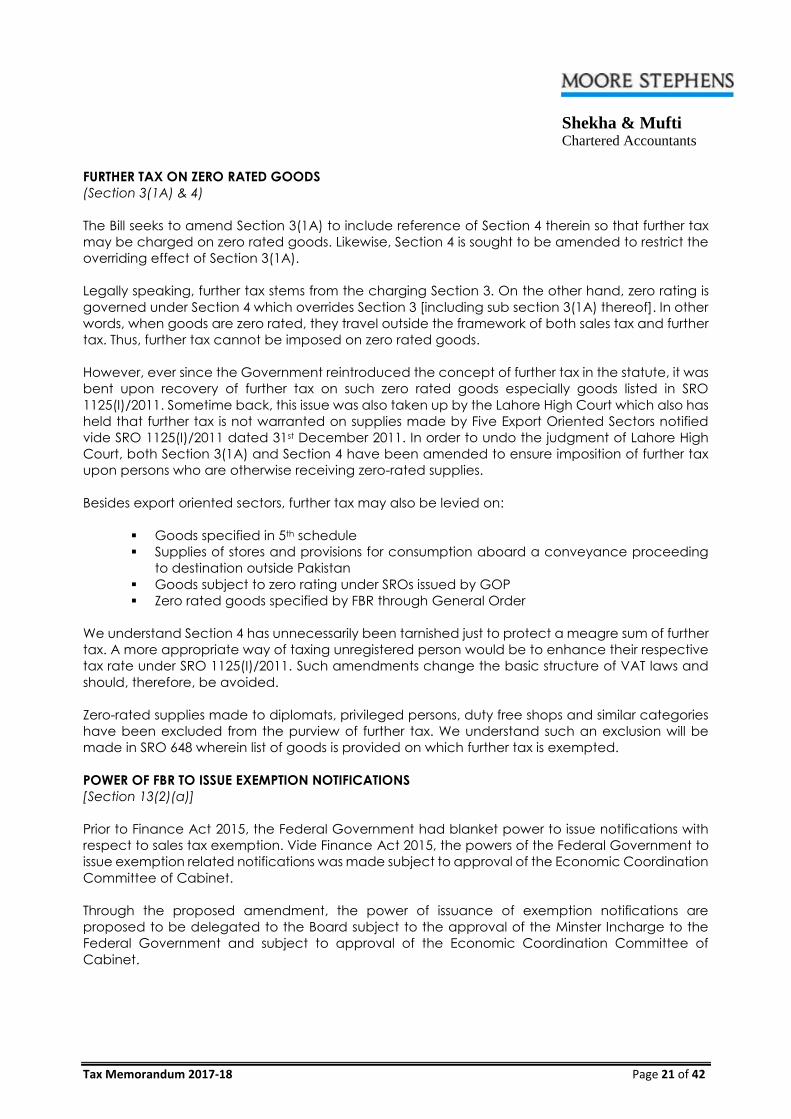

FURTHER TAX ON ZERO RATED GOODS

(Section 3(1A) & 4)

The Bill seeks to amend Section 3(1A) to include reference of Section 4 therein so that further tax

may be charged on zero rated goods. Likewise, Section 4 is sought to be amended to restrict the

overriding effect of Section 3(1A).

Legally speaking, further tax stems from the charging Section 3. On the other hand, zero rating is

governed under Section 4 which overrides Section 3 [including sub section 3(1A) thereof]. In other

words, when goods are zero rated, they travel outside the framework of both sales tax and further

tax. Thus, further tax cannot be imposed on zero rated goods.

However, ever since the Government reintroduced the concept of further tax in the statute, it was

bent upon recovery of further tax on such zero rated goods especially goods listed in SRO

1125(I)/2011. Sometime back, this issue was also taken up by the Lahore High Court which also has

held that further tax is not warranted on supplies made by Five Export Oriented Sectors notified

vide SRO 1125(I)/2011 dated 31st December 2011. In order to undo the judgment of Lahore High

Court, both Section 3(1A) and Section 4 have been amended to ensure imposition of further tax

upon persons who are otherwise receiving zero-rated supplies.

Besides export oriented sectors, further tax may also be levied on:

Goods specified in 5th schedule

Supplies of stores and provisions for consumption aboard a conveyance proceeding

to destination outside Pakistan

Goods subject to zero rating under SROs issued by GOP

Zero rated goods specified by FBR through General Order

We understand Section 4 has unnecessarily been tarnished just to protect a meagre sum of further

tax. A more appropriate way of taxing unregistered person would be to enhance their respective

tax rate under SRO 1125(I)/2011. Such amendments change the basic structure of VAT laws and

should, therefore, be avoided.

Zero-rated supplies made to diplomats, privileged persons, duty free shops and similar categories

have been excluded from the purview of further tax. We understand such an exclusion will be

made in SRO 648 wherein list of goods is provided on which further tax is exempted.

POWER OF FBR TO ISSUE EXEMPTION NOTIFICATIONS

[Section 13(2)(a)]

Prior to Finance Act 2015, the Federal Government had blanket power to issue notifications with

respect to sales tax exemption. Vide Finance Act 2015, the powers of the Federal Government to

issue exemption related notifications was made subject to approval of the Economic Coordination

Committee of Cabinet.

Through the proposed amendment, the power of issuance of exemption notifications are

proposed to be delegated to the Board subject to the approval of the Minster Incharge to the

Federal Government and subject to approval of the Economic Coordination Committee of

Cabinet.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 22 of 42

POWER OF FBR TO ISSUE EXEMPTION NOTIFICATIONS

[Section 13(6)]

Through the proposed amendment, FBR with approval of the Minster Incharge to the Federal

Government will present exemption related notifications in a financial year before the National

Assembly.

EXTENSION TO EXEMPTION PERIODS

[Section 13(7)]

Vide Finance Act 2015, Section 13(7) was introduced to auto rescind exemption notifications (if

not rescinded earlier) issued after 1st July 2015 after expiry of the financial year in which such

notifications were issued.

a) Through Finance Bill, a proviso has been added which provide a new lease of life to all

notifications issued between 1st July 2015 upto 30 June 2016, which were auto rescinded

on 30 June 2016.

All such notifications shall now be valid till 30 June 2018, if not rescinded earlier. We reckon

the following issues would emanate out of the proposed amendment:

Whether tax charged and paid in treasury after 30 June 2016 till todate shall be

refundable to such persons ?

Whether cases framed against taxpayers for illegal claim of exemption on said

notifications after 30 June 2016 would be dropped ? The first proviso has clarified that

any tax not paid during the period 2015-2016 may not be questioned by the filed

formation since the tax exemption will have retrospective effect.

b) Another proviso has been added which provide extension to all notifications issued 1st July

2016 onward, which were to auto rescind on 30 June 2017. All such notifications shall now

be valid till 30 June 2018, if not rescinded earlier.

APPOINTMENT OF AUTHORITIES

(Section 30)

The bill proposes to create new posts of ‘District Taxation Officer’ and ‘Assistant Director Audit’.

The bill proposes that Chief Commissioner Inland Revenue shall perform their functions in respect

of persons or class of persons of such areas as the Board may direct. Accordingly, Commissioners

Inland Revenue shall perform their functions in respect of such persons or classes of persons of such

areas as their concerned Chief Commissioner directs.

OFFENCES & PENALTIES

[Section 33(23)]

An amendment has been proposed by inserting a new Serial No. 23 in Section 33 of the Act. This

appears to be clarificatory in nature whereby penalties have been imposed in such cases where

penalty against an offence has not been specifically prescribed.

By this amendment “any person who manufactures, possesses, transports, distributes, stores or sells

cigarette packs without, or with counterfeited, tax stamps, banderoles, stickers, labels or barcodes

shall be liable to pay penalty under various conditions as mentioned in below chart.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 23 of 42

S. No. OFFENCE PENALTY

23 Any person who manufactures,

possesses, transports, distributes, stores

or sells cigarette packs without, or

with counterfeited, tax stamps,

banderoles, stickers, labels or barcodes.

(i) Such cigarette stock shall be liable to

outright confiscation and destruction.

Any person committing the offence shall

pay a penalty of twenty-five thousand

rupees or one hundred per cent of the

amount of tax involved, whichever is

higher. He shall, further be liable, upon

conviction by a Special Judge, to

imprisonment for a term which may

extend to five years, or with additional

fine which may extend to an amount

equal to the loss of tax involved, or with

both.

(ii) In case of transport of cigarettes

without, or with counterfeited, tax

stamps, banderoles, stickers, labels or

barcodes, permanent seizure of the

vehicle used for transportation of non-

conforming or counterfeit cigarette

packs; and

(iii) In case of repeat sale of cigarettes

without or with counterfeited, tax stamps,

banderoles, stickers, labels or barcodes,

the premises used for such sale be sealed

for a period not exceeding 15 days.

AUTOMATIC STAY AGAINST DEMAND

(Section 48)

It is proposed that the Commissioner shall not issue the recovery notice to the taxpayer for recovery

of assessed tax till the decision of Commissioner (Appeals), if the taxpayer pays 25% of tax due

framed in the assessment order.

This provision proposes harmonization of recovery provisions between Sales Tax and Income Tax

Laws since similar provision was inserted through Finance Act 2016 in Section 140 of the Income

Tax Ordinance, 2001.

The term ‘tax due’ include principal amount of liability, default surcharge and penalty. Practically,

we understand that this option may not be feasible for the taxpayer as condition of 25% payment

of the gross liability appears to be on higher side. We, therefore, suggest that instead of targeting

‘tax due’, the recovery may be modified to the extent of principal tax liability with a lower

percentage of 15%, as has been in vogue in federal excise laws.

The proposed change also appears to be in disharmony with Section 48(1) of the Act whereby an

Officer of Inland Revenue is empowered to initiate the recovery proceedings. On the other hand,

after the payment of 25% of tax due, only the Commissioner is proposed to halt the recovery

notice. This appears to be a drafting mistake which needs correction. We understand that since

the recovery notice can be issued by all Officers of Inland Revenue; therefore, the Officer Inland

Revenue (including Commissioner) should also be empowered to halt recovery proceedings after

25% of payment of tax due till the decision of Commissioner (Appeals).

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 24 of 42

SERVICE OF ORDERS, DECISIONS, ETC.

(Section 56)

The bill has introduced new clause “d” in sub-Sections 1 & 2 of Section 56 of the Act to provide

legal coverage to various notices, orders and decisions sent to taxpayers though electronic

medium. By this arrangement, electronically transmitted notices via email or in the e-folder

available at Sales Tax-cum-Federal Excise returns shall be construed as proper service of such

document to both public and private limited companies.

The plain reading of the proposed amendment transpires that the amendment is applicable only

on public and private limited companies. Accordingly, service of electronically transmitted notices

to AOP, Individual and to withholding agents may continue to be serviced through courier or

registered post.

We suggest identical benefit should also be extended to taxpayers / counsels so that they may

also become eligible to file their replies via emails.

VALIDATION

(Section 74A)

A new Section 74A is proposed to be inserted in the Act. The insertion of Section 74A is to provide

legal coverage and protection to all notification and order issued in exercise of the powers

conferred upon the Federal Governments before the commencement of Finance Act, 2017.

Previously, many SROs / Notifications were issued under sole approval of Secretory or Advisor of

the Revenue Division (i.e. executive authority) instead of competent authority. Some of which

(listed below) were challenged before Superior Courts. The Courts have held that such SROs can

only be issued after the approval of Federal Governments which comprises of Prime Ministers and

Federal Ministers (i.e. cabinet). Hence, these SROs were struck down for their respective

applications and declared as ultra vires to the Constitution of Pakistan.

1. SRO.460(I)/2013 - Struck down by SCP

2. SRO 280(I)/2013 - Struck down by SCP

3. SRO 682(I)/ 2013 - Struck down by SCP

4. SRO 490 - Struck down by LHC

5. SRO 608 - Struck down by LHC

Enabling the aforesaid proposition through Finance Act, 2017 would not only make the aforesaid

SROs legalized but also reactivated / revalidated.

THIRD SCHEDULE

Section 3(2)(a) - Sales Tax on Ice Cream

Ice Cream is covered at Serial No. 2 of Third Schedule to the Act. Through proposed amendment,

its Tariff Heading No.21.05 has been replaced with Tariff Heading 2105.0000. The proposed

amendment is a corrective measure in line with Tariff Heading as envisaged at Custom Tariff.

Section 3(2)(a) - Sales Tax on Fertilizes

Currently, fertilizers falling under Third Schedule of the Act are chargeable to sales tax @ 17% on

retail price. In terms of Special Procedure Adjustment of Sales Tax due on Fertilizers Rules 2015 as

enacted vide SRO 1198 dated 3rd December 2015, manufacturers and importers of various types

of fertilizers may claim subsidy on supply of fertilizers from the Federal Government.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 25 of 42

Through Finance Bill, certain specified fertilizers are proposed to be included at Eighth Schedule to

the Act and are suggested to be liable for fixed sales tax instead of taxation @ ad val. The new

proposed rates of fixed sales tax on such fertilizers alongwith respective purchases are as follows:

S. No. Description Rate of sales tax Condition

35 DAP Rs.100 per 50 kg bag NIL

36 NP (22-20) Rs.168 per 50 kg bag If manufactured from gas

other than imported LNG

37 NP (18-18) Rs.165 per 50 kg bag - do -

38 NPK- Rs.251 per 50 kg bag - do -

39 NPK-II Rs.222 per 50 kg bag - do -

40 NPK-III Rs.341 per 50 kg bag - do -

41 SSP Rs.31 per 50 kg bag - do -

42 CAN Rs.98 per 50 kg bag - do -

43 Natural gas 10% If supplied to fertilizer plants for

manufacturing of urea

44 Phosphoric acid 5%

If imported by fertilizer

company for manufacturing

of DAP

However, there is no change in rate of sales tax on Urea Fertilizers and will continue at the existing

rate of 5%.

Sales tax on fertilizers was subject to retail price under 3rd Schedule. Now, shifting to fixed tax

scheme would reduce the sale price. However, we understand further tax would also be levied on

all sales made to unregistered persons.

FIFTH SCHEDULE

Serial No. Existing Entry Proposed Entry

12(xvii) Preparations for infant use put up

for retail sale

Preparations suitable for infants or

young children, put up for retail sale

The above change is of clarificatory nature.

SIXTH SCHEDULE

TABLE – I

Serial No Existing Entry PCT

Heading Proposed Amendment

84 Preparations for infant use,

put up for retail sale 1901.1000

It is proposed to exempt

reparations for young children,

use, put up for retail sale as well.

97 Pens and ball pens 96.08 It is proposed to exempt markers

and porous tipped pens as well.

100A.

Materials and equipment

for construction and

operation of Gwadar Port

and development of Free

Zone for Gwadar Port

-

It is proposed to extent the

exemption to plant, machinery,

appliances, and accessories.

130. Premixes for growth stunting - Condition for availing exemption

has been proposed to change.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 26 of 42

NEW TAX EXEMPTIONS

Serial No Proposed Entry PCT Heading

100C

Vehicles imported by China Overseas Ports Holding

Company Limited (COPHCL) and its operating companies

namely (i) China Overseas Ports Holding Company

Pakistan (Private) Limited (ii) Gwadar International

Terminal Limited, (iii) Gwadar Marine Services Limited and

(iv) Gwadar Free Zone Company Limited, for a period of

twenty three years for construction, development and

operations of Gwadar Port and Free Zone Area subject to

21 limitations, conditions prescribed under PCT heading

9917

-

134

Gifts and donations received from foreign governments

and organizations to the Federal and Provincial

Governments and public sector organizations.

9908

135

Exemption from payment of sales tax is being provided on

import of sunflower and canola hybrid seeds meant for

sowing.

Respective

heading

136 Combined harvesters upto five years old 8433.5100

137

Single cylinder agriculture diesel engines (compression-

ignition internal combustion piston engines) of 3 to 36 HP,

and CKD kits thereof

8408.9000

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 27 of 42

TABLE – 3

Existing exemption available to items for renewable sources of energy is proposed to be aligned

with exemption available to these items under the Customs Act, 1969.

S.No. Proposed Entry Tariff

Heading

14 Following items for use with solar energy:-

Solar Power Systems.

8501.3110

8501.3210

Off–grid/On-grid solar power system (with or without provision for

USB/charging port) comprising of :

(i) PV Module.

(ii) Charge controller.

(iii) Batteries for specific utilization with the system (not exceeding 50

Ah in case of portable system).

(iv) Essential connecting wires (with or without switches).

(v) Inverters (off-grid/ on-grid/ hybrid with provision for direct

connection/ input renewable energy source and with Maximum

Power Point Tracking (MPPT).

(vi) Bulb holder (2) Water purification plants operating on solar energy.

8541.4000

9032.8990

8507.2090

8507.3000

8507.6000

8544.4990

8504.4090

8536.6100

8421.2100

14A

Following systems and items for dedicated use with renewable source

of energy like solar, wind, geothermal etc.

1. (a) Solar Parabolic Trough Power Plants.

(b) Parts for Solar Parabolic Power Plants.

(i) Parabolic Trough collector’s modules.

(ii) Absorbers/Receivers tubes.

(iii) Steam turbine of an output exceeding 40MW.

(iv) Steam turbine of an output not exceeding 40MW.

(v) Sun tracking control system.

(vi) Control panel with other accessories.

8502.3900

8503.0010

8503.0090

8406.8100

8406.8200

8543.7090

8537.1090

2. (a) Solar Dish Stirling Engine.

(b) Parts for Solar Dish Stirling Engine.

(i) Solar concentrating dish.

(ii) Sterling engine.

(iii) Sun tracking control system.

(iv) Control panel with accessories.

(v) Stirling Engine Generator

8412.8090

8543.7000

8543.7000

8543.7090

8406.8200

8501.6100

3. (a) Solar Air Conditioning Plant

(b) Parts for Solar Air Conditioning Plant

(i) Absorption chillers.

(ii) Cooling towers.

(iii) Pumps.

(iv) Air handling units.

(v) Fan coils units.

(vi) Charging & testing equipment.

8415.1090

8418.6990

8419.8910

8413.3090

8415.8200

8415.9099

9031.8000

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 28 of 42

S.No. Proposed Entry Tariff

Heading

4. (a) Solar Desalination System (b) Parts for Solar Desalination System

(i) Solar photo voltaic panels.

(ii) Solar water pumps.

(iii) Deep Cycle Solar Storage batteries.

(iv) Charge controllers.

(v) Inverters (off grid/on grid/ hybrid) with provision for direct

connection/input from renewable energy source and with

Maximum Power Point Tracking (MPPT)

8421.2100

8541.4000

8413.3090

8507.2090

9032.8990

8504.4090

5. Solar Thermal Power Plants with accessories. 8502.3900

6. (a) Solar Water Heaters with accessories.

(b) Parts for Solar Water Heaters

(i) Insulated tank

(ii) Vacuum tubes (Glass)

(iii) Mounting stand

(iv) Copper and Aluminum tubes

(c) Accessories:

(i) Electronic controller

(ii) Assistant/ feeding tank

(iii) Circulation Pump

(iv) Electric heater/ immersion rod (one piece with one solar water

heater)

(v) Solenoid valve (one piece with one solar water heater) (vi)

Selective coating for absorber plates

8419.1900

7309.0000

7310.0000

7020.0090

Respective

headings

Respective

heading

7. (a) PV Modules. (b) Parts for PV Modules

(i) Solar cells.

(ii) Tempered Glass.

(iii) Aluminum frames.

(iv) O-Ring.

(v) Flux.

(vi) Adhesive labels.

(vii) Junction box & cover.

(viii) Sheet mixture of paper and plastic

(ix) Ribbon for PV Modules (made of silver &Lead).

(x) Bypass diodes.

(xi) EVA (Ethyl Vinyl Acetate) Sheet (Chemical).

8541.4000

8541.4000

7007.2900

7610.9000

4016.9990

3810.1000

3919.9090

8538.9090

3920.9900

Respective

headings

8541.1000

3920.9900

8. Solar Cell Manufacturing Equipment.

(i) Crystal (Grower) Puller (if machine).

(ii) Diffusion furnace.

(iii) Oven.

(iv) Wafering machine.

(v) Cutting and shaping machines for silicon ingot.

(vi) Solar grade polysilicon material.

(vii) Phosphene Gas.

8479.8990

8514.3000

8514.3000

8486.1000

8461.9000

3824.9999

2853.9000

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 29 of 42

S.No. Proposed Entry Tariff

Heading

(vii) Aluminum and silver paste.

Respective

headings

9. Pyranometers and accessories for solar data collection. 9030.8900

10. Solar chargers for charging electronic devices. 8504.4020

11. Remote control for solar charge controller. 8543.7010

12. Wind Turbines.

(a) Wind Turbines for grid connected solution above 200 KW (complete

system).

(b) Wind Turbines upto 200 KW for off-grid solutions comprising of:

(i) Turbine with Generator/ Alternator.

(ii) Nacelle with rotor with or without tail.

(iii) Blades.

(iv) Pole/ Tower.

(v) Inverter for use with Wind Turbine.

(vi) Deep Cycle Cell/ Battery (for use with wind turbine).

8412.8090

8412.8090

Respective

headings

8507.2090

13. Wind water pump 8413.8100

14. Geothermal energy equipment.

(i) Geothermal heat pumps.

(ii) Geothermal Reversible Chillers.

(iii) Air handlers for indoor quality control equipment.

(iv) Hydronic heat pumps.

(v) Slim Jim heat exchangers.

(vi) HDPE fusion tools.

(vii) Geothermal energy installation tools and equipment.

(viii) Dehumidification equipment.

(viii) Thermostats and intellizone.

8418.6100

8418.6990

8415.8300

8418.6100

8419.5000

8515.8000

8419.8990

8479.6000

9032.1090

15. Any other item approved by the Alternative Energy Development

Board (AEDB) and concurred to by the FBR.

Respective

headings

15

Following items for promotion of renewable energy technologies or for

conservation of energy:-

(i) SMD/LED/LVD lights with or without ballast, fittings and fixtures.

(ii) SMD/LED/LVD street lights, with or without ballast, PV module, fitting

and fixtures

(iii) Tubular day lighting device.

(iv) Wind turbines including alternators and mast.

(v) Solar torches.

(vi) Lanterns and related instruments.

(vii) LVD induction lamps.

(viii) LED bulb/tube lights.

9405.1090

8539.3290

8543.7090

9405.4090

8539.3290

8543.7090

9405.5010

8502.3100

8513.1040

8513.1090

8539.3290

8543.7090

8541.4000

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 30 of 42

S.No. Proposed Entry Tariff

Heading

(ix) PV module, with or without, the related components including

invertors (off grid/on grid/hybrid) with provision for direct

connection/input from renewable energy source and with

Maximum Power Point Tracking (MPPT), charge controllers and

solar batteries.

(x) Light emitting diodes (light emitting in different colors). (xi) Water

pumps operating on solar energy along with solar pump controllers

(xii) Energy saver lamps of varying voltages

(xiii) Energy Saving Tube Lights.

(xiv) Sun Tracking Control System

(xv) Invertors (off-grid/on grid/hybrid) with provision for direct

connection/input from renewable energy source and with

Maximum Power Point Tracking (MPPT).

(xvi) Charge controller/ current controller. Provided that exemption

under this serial shall be available with effect from 01.07.2016.

8504.4090

9032.8990

8507.0000

8541.5000

8413.7010

8413.7090

8504.4090

8539.3110

8539.3210

8539.3120

8539.3220

8543.7090

8504.4090

9032.8990

15A

Parts and components for manufacturing LED lights:

(i) Aluminum housing/ shell for LED (LED light fixture)

(ii) Metal clad printed circuit boards (MCPCB) for LED

(iii) Constant current power supply for of LED lights (1-300W) (iv) Lenses

for LED lights

9405.1090

8543.0000

8504.4090

9001.9000

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 31 of 42

EIGHTH SCHEDULE

Change in Scope of Exemptions & other changes.

Serial No

Existing Condition Proposed Amendment

34 Subject to type approval by PEMRA. This concession shall be available upto 30th June 2017.

Exemption is proposed from 30 June 2017 to 30 June 2018

S. No. Description Respective

Heading

Rate of sales

tax Condition

45 Following machinery for poultry

sector :

Respective

heading

Import and

supply

(i) Machinery for preparing

feeding stuff 8436.1000 7%

(ii) Poultry incubators and brooders 8436.2100

8436.2900 7%

(iii) Insulated sandwich panels 9406.0090 7%

(iv) Poultry sheds 9406.0020 7%

(v) Evaporative air cooling system 8479.6000 7%

(vi) Evaporative cooling pad 8479.9010 7%

46. Multimedia projectors 8528.6210 10%

If imported by

educational

institution

47. Locally produced coal 27.01

Rs. 425 per

metric tonne

or 17% ad

valorem,

whichever is

higher

Nil”; and

NINTH SCHEDULE

The Bill proposed to change the fixed amount of sales tax on following categories of mobile

phones in Serial No. (3) & (4):

Existing

Rate (3)

Proposed

Rate (3)

Existing

Rate (4)

Proposed

Rate (4)

A. Low Priced Cellular Mobile Phones or

Satellite Phones

All cameras: 2.0 mega-pixels or less

Screen size: 2.6 inches or less

Key pad

Rs.300

Rs.650

Rs.300

Rs.650

B. Medium Priced Cellular Mobile Phones or

Satellite Phones

One or two cameras: between 2.1 to 10

mega-pixels

Screen size: between 2.6 inches and 4.2

inches

Micro-processor: less than 2 GHZ

Rs.1,000 Rs.650 Rs.1,000 Rs.650

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 32 of 42

SALES TAX SPECIAL PROCEDURE RULES, 2007

Extra Tax on Lubricants

In terms of Serial No. 5 of Table to Chapter XIII of Sales Tax Special Procedure Rules 2007, specific

items which include industrial lubricants and others are subject to 2% extra sales tax in addition to

sales tax @17% when supplied by manufacturers or importers in local market. Such specified goods

on which extra sales tax is paid in the prescribed manner are exempt from payment of sales tax

on subsequent supplies including those made by distributor / trader and retailer.

At times, lubricating oil is used in production of taxable goods. Such buyers are exposed to output

tax on their taxable supplies but are unable to claim benefit of sales tax paid on purchase of

Lubricating Oil from distributors and traders. This way cost of purchase increases which adversely

affects profitability. On the other hand, sales of exempt Lubricating Oil by distributors also

unnecessarily increase the distributor’s overall sale price (with the absorption of sales tax and extra

tax). This aspect not only derives the distributors out of competition and market but also lead to

enhanced cost of production.

Consequent to such amendment, the lube business will be classified under normal tax regime.

Hence, the buyers of such lubricants would be able to claim input tax thereon even if procured

from distributors / traders.

IMPORT AND LOCAL SUPPLY OF HYBRID ELECTRIC VEHICLES

Reduction in sales tax

The Bill proposes an amendment in SRO 499 (I)/2013 dated 12 June 2013 through a notification to

be issued on 01 July 2017. Through the aforesaid amendment, rate of sales tax on import of Hybrid

Electric Vehicles [HEV] with engine capacity upto 1800cc would remain unchanged. However,

previous reduction in sales tax of 25% from standard rate on import of HEV exceeding 1800cc has

now been restricted. Consequent of aforesaid amendment, HEV with engine capacity more than

2500cc are now exposed to standard sales tax. The aforesaid position is being summarized in the

table as below:

HEV with engine

capacity

Existing concession

is rate of sales tax

Proposed concession

is rate of sales tax

Upto 1800cc 50% 50%

Exceeding 1800cc 25% -

1800cc to 2500cc - 25%

2500cc and above - -

Further, it is proposed that above said reduction of sales tax rate would also be applicable for local

supply of HEV.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 33 of 42

ZERO RATED SECTORS

SRO 1125(I)/2011

An amendment has been proposed in SRO 1125(I)/2011 dated 31 December 2011 through

notification to be issued on 01 July 2017 whereby commercial import of fabrics will be subject to

sales tax @ 6%. Presently, such fabric is exposed to 0% sales tax.

In line with the above announcement, sales tax @ 6% will be imposed on commercial import of all

fabrics imported for subsequent supply to traders. Commercial importers of fabrics, who make

supply to manufacturers @ zero rate, may need to file sales tax refund which is against the spirit of

‘no tax no refund’ policy.

Further, tax rate of sales made by retailers has been enhanced from 5% to 6%.

SALES TAX WITHHOLDING FROM REGISTERED PERSON

SRO 660(I)/2007 [To Be Amended]

Salient Features Documents reveal that sales tax withholding on transactions between registered

persons is proposed to be withdrawn, except for advertisement services.

The aim of introducing withholding tax rules was cross matching of declaration of buyers and

suppliers to safeguard the revenue collection when manual tax returns were filed by businesses.

After launching of STRIVE system last year, the purpose of sales tax withholding rules became

redundant to the extent of transactions between registered persons. Since then, it was highlighted

to FBR on numerous occasion that sales tax withholding on transactions between registered

persons has no revenue impact; rather it creates cumbersomeness both for withholding agents

and tax authorities and yield unnecessary litigation.

In line with FBR’s earlier ruling, it appears that the aforesaid amendment will be applicable on

invoices issued by the registered persons to other registered person w.e.f. 01 July 2017.

We also suggest withholding from unregistered persons may not be made a revenue tool; rather

should be taken as a tool to broaden the tax net. Thus, tax deducted on transactions made with

unregistered persons may be allowed as input tax in the hands of respective buyers in the same

manner as it was in vogue under SRO 603/2009.

We reckon a legal question emanating out of the proposed amendment vis.a.vis application of

sales tax withholding rules on taxable services including advertisement services covered under

Islamabad Capital Territory (Tax on Services) Ordinance, 2001. Last year, FBR became empowered

to issue notification under Sections 3(2)(b), 3(6), and 3(7) of the Act for the purposes of reducing /

increasing tax rates, imposing any other tax in lieu of normal tax , and deduction of sales tax

withholding, respectively. However, no notification has been issued by FBR so far except for

reduced rate on services.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 34 of 42

ISLAMABAD CAPITAL TERRITORY (TAX ON SERVICES) ORDINANCE, 2001

The ‘Salient features” presented with Finance Bill 2017-18 suggests more services being brought

into the tax net. The taxability of such services would depend on respective turnover, with no input

tax adjustment. Such tax measures would be in line with the provincial statutes so that a level

playing field is made available to the service providers across the country.

Under the provincial statutes, construction services, restaurant services, services provided by

workshop for electric or electrical equipment etc. are taxed on the basis of turnover.

The list of services and their turnover limits would be provided through SRO to be issued in July 2017.

The Finance Bill also proposes exemption on export of IT Services on the same pattern as are

available under Sindh and Punjab Sales Tax Laws.

Shekha & Mufti Chartered Accountants

Tax Memorandum 2017-18 Page 35 of 42

FEDERAL EXCISE ACT, 2005

EXEMPTIONS

Sections 16(2), (5), (6)

Amendments Identical to those made in Section 13 of Sales Tax Act 1990 have been replicated in

Federal Excise Act 2005 (FED Act).

STAY AGAINST RECOVERY

Section 37