Day 1 C2C - Deloitte - Government Support for ICT Development, Success strategies

Upload

trinhthuanCategory

view

223download

2

SHARING SUCCESS –

DELOITTE 2015 GLOBAL

SHARE PLAN SURVEY

19 MAY 2016

Jay Foley > Computershare

Bill Cohen > Deloitte

Lisa Williamson > Deloitte

Deloitte 2015 Global

Share Plans Survey

Bill Cohen and Lisa Williamson

19 May 2016

Agenda

• Background

• Methodology

• Executive plans

• Broad-based plans

• Operational trends

2

Deloitte UK screen 4:3 (19.05 cm x 25.40 cm)

© 2013 Deloitte LLP. Private and confidential.

Background

Source: 2015 survey by European

Federation of Employee Share

Ownership (“EFES”)

% of

listed

companies

Market Capitalisation>Euro200m

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Share Plans Broad-based Executives

4

Methodology 2015 participants - demographics

• 177 companies operating a total of 436 equity plans, consisting of:

• 274 executive plans

• 162 broad-based plans

• Companies are headquartered in the following locations:

• Australia

• Belgium

• Bermuda

• Brazil

• Canada

• Denmark

• Finland

• Germany

• Hong Kong

• Hungary

• Iceland

• Ireland

• Luxembourg

• Malaysia

• Netherlands

• Papua New

Guinea

• Russia

• Singapore

• South Africa

• Spain

• Sweden

• Switzerland

• UK

• US

Source: Deloitte 2015 GSP survey 4

Consumer Goods

Industrials Healthcare

Oil and Gas

Consumer and Business

Services

Media

Property

Other

Finance

Technology and

Communications

Methodology Participants - respondent profile

23%

34%

25%

8%

10% Less than 5,000

5,000 – 20,000

20,001 – 50,000

50,001 – 100,000

More than 100,000

Source: Deloitte 2015 GSP survey

Number of employees Industry

% of respondents % of respondents

5

27% 18%

15%

10%

10% 8%

5%

3%

3%

1%

Executive plans

7

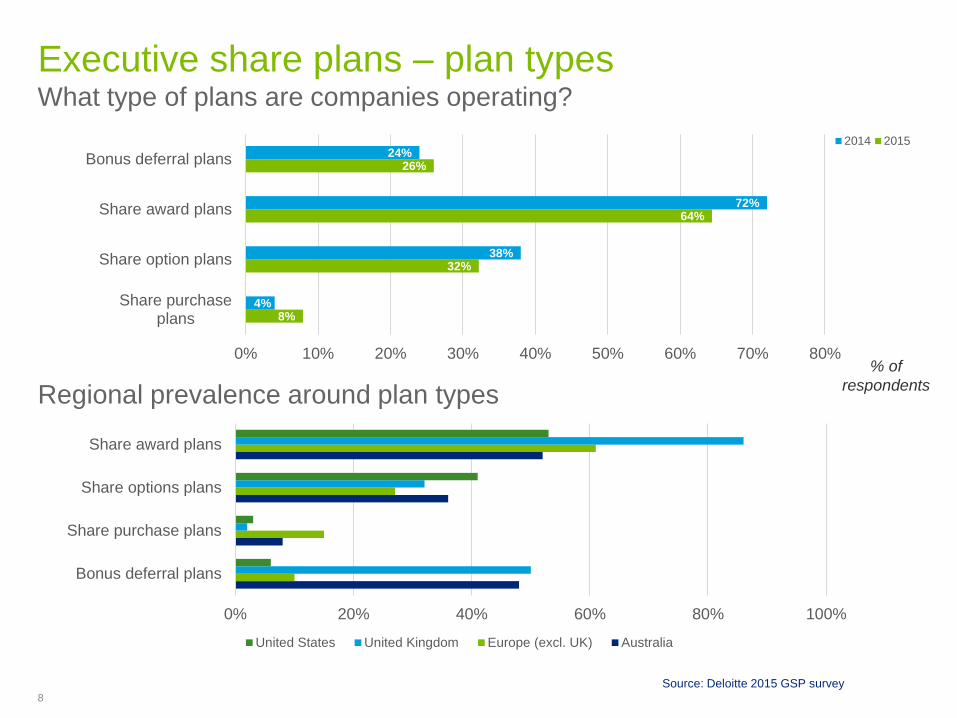

Executive share plans – plan types What type of plans are companies operating?

8%

32%

64%

26%

4%

38%

72%

24%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Share purchaseplans

Share option plans

Share award plans

Bonus deferral plans

2014 2015

Source: Deloitte 2015 GSP survey 8

Regional prevalence around plan types

0% 20% 40% 60% 80% 100%

Bonus deferral plans

Share purchase plans

Share options plans

Share award plans

United States United Kingdom Europe (excl. UK) Australia

% of

respondents

Executive share plans – share award plans How are share awards structured?

9

22% 16%

62%

0%

10%

20%

30%

40%

50%

60%

70%

Nil cost options/nominalvalue options

Restricted shares Restricted stock units% of plans

11%

36%

11% 12%

17%

4%

17% 35%

72% 60%

72% 53%

0%

20%

40%

60%

80%

100%

United States United Kingdom Europe (excl. UK) Australia

Nil cost option/nominal value option Restricted shares Restricted stock units

% of plans

% of plans in

that region

Source: Deloitte 2015 GSP survey

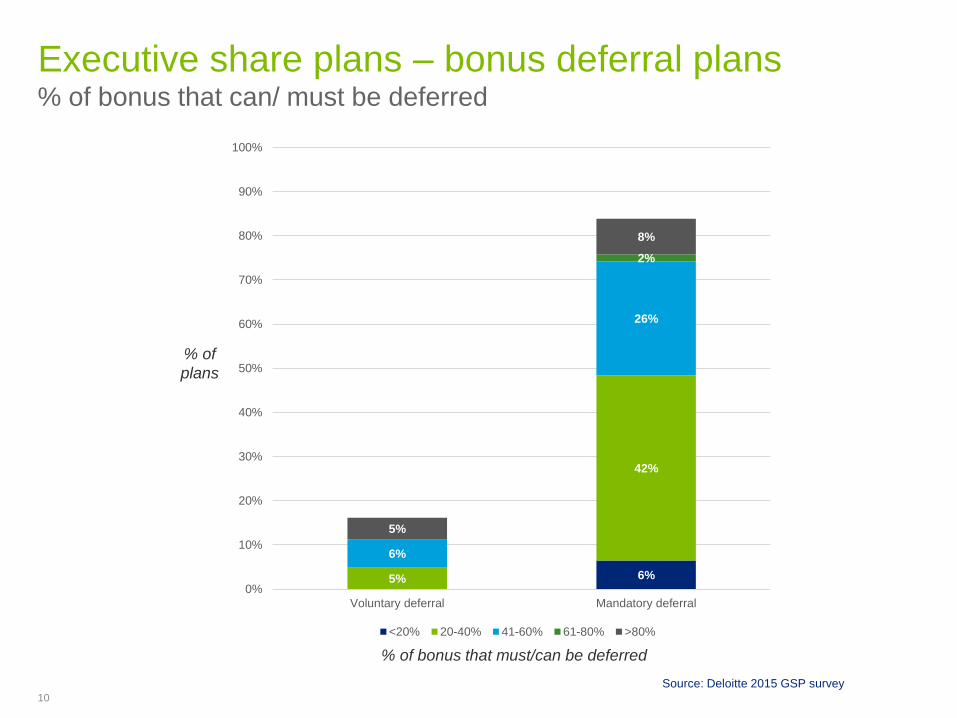

Executive share plans – bonus deferral plans % of bonus that can/ must be deferred

6% 5%

42%

6%

26%

2%

5%

8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Voluntary deferral Mandatory deferral

<20% 20-40% 41-60% 61-80% >80%

% of bonus that must/can be deferred

Source: Deloitte 2015 GSP survey 10

% of

plans

Executive share plans – retention periods

11

Are shares acquired on vesting of a share

award subject to a further retention period?

Are shares acquired through the options subject

to a further retention period following exercise?

Are shares acquired

subject to a further

retention period

following

exercise/delivery?

14%

86%

Yes No12%

88%

Yes No

0%

5%

10%

15%

20%

25%

United Kingdom United States Australia Europe (excl. UK)

% of

plans

Source: Deloitte 2015 GSP survey

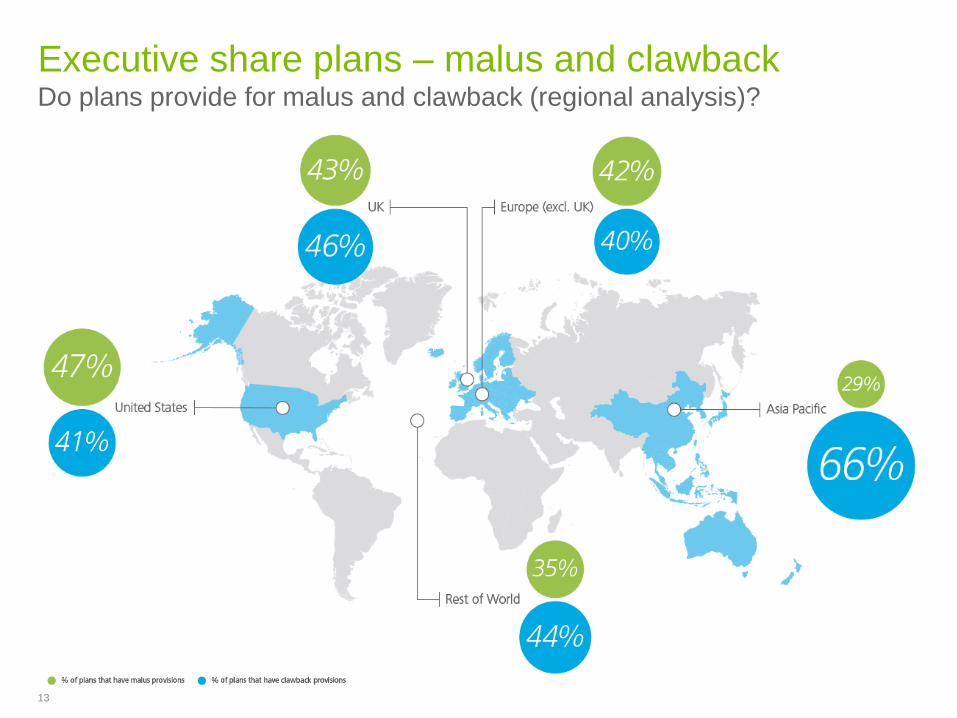

Executive share plans – malus and clawback Do plans provide for malus and clawback?

80%

85%

66%

56%

40%

20%

15%

34%

44%

60%

0% 20% 40% 60% 80% 100%

Voluntary bonus deferral plans

Mandatory bonus deferral plans

Share award plans

Share option plans

Share purchase plansYes No

50%

62%

56%

37%

27%

50%

38%

44%

63%

73%

Voluntary bonus deferral plans

Mandatory bonus deferral plans

Share award plans

Share option plans

Share purchase plans

Malus

Clawback

Source: Deloitte 2015 GSP survey 12

% of

plans

Executive share plans – malus and clawback Do plans provide for malus and clawback (regional analysis)?

13

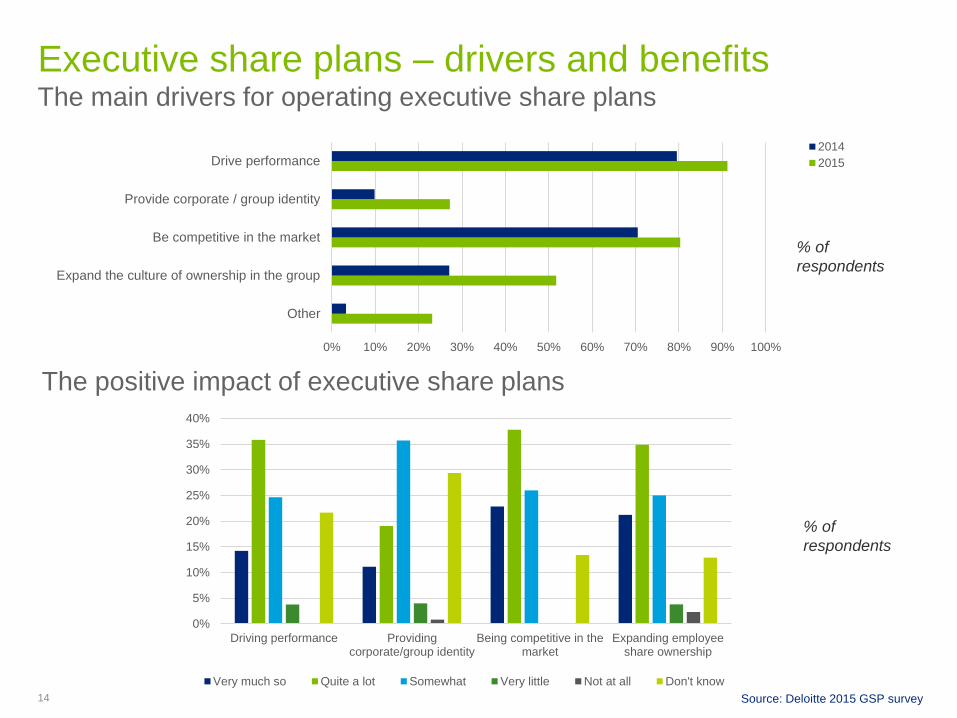

Executive share plans – drivers and benefits The main drivers for operating executive share plans

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Other

Expand the culture of ownership in the group

Be competitive in the market

Provide corporate / group identity

Drive performance2014

2015

14

% of

respondents

0%

5%

10%

15%

20%

25%

30%

35%

40%

Driving performance Providingcorporate/group identity

Being competitive in themarket

Expanding employeeshare ownership

Very much so Quite a lot Somewhat Very little Not at all Don't know

% of

respondents

The positive impact of executive share plans

Source: Deloitte 2015 GSP survey

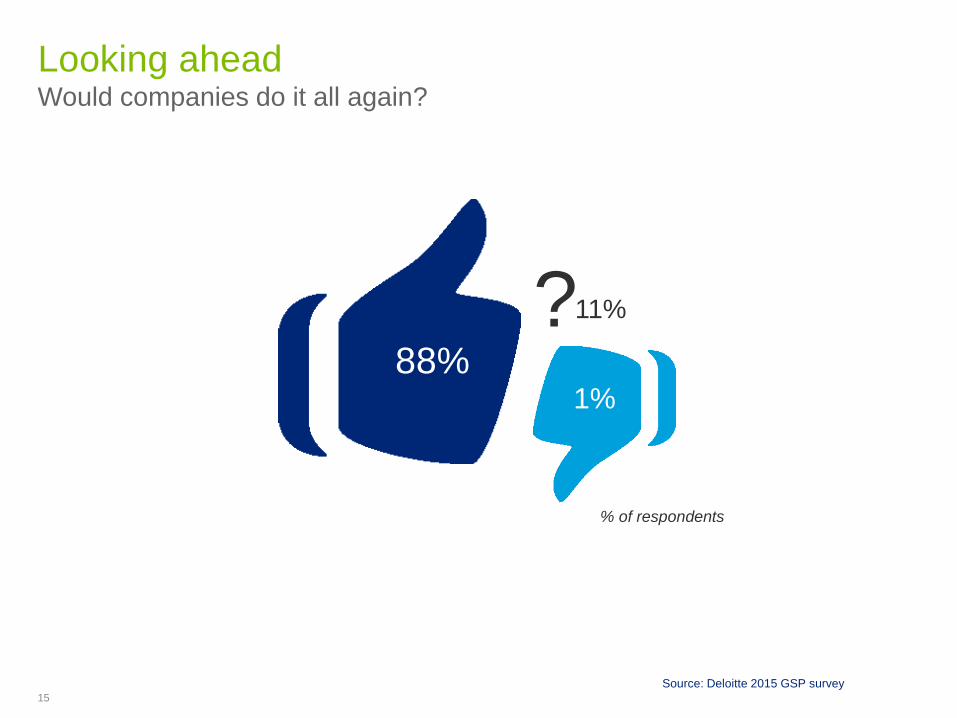

Looking ahead Would companies do it all again?

88% 1%

89%

? 11%

Source: Deloitte 2015 GSP survey 15

% of respondents

Broad-based plans

16

Deloitte UK screen 4:3 (19.05 cm x 25.40 cm)

© 2013 Deloitte LLP. Private and confidential.

Context

“Ever widening differentials are often

difficult to credibly justify and boards

should be mindful of the possible negative

impact on corporate culture and staff

morale of widening inequality within the

organisation” NAPF Guidelines

16

Deloitte UK screen 4:3 (19.05 cm x 25.40 cm)

© 2013 Deloitte LLP. Private and confidential.

% of European companies having employee share

plans / broad-based plans

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Employee share plans Broad-based plans Source: 2015 survey by EFES

53%

86%

18

Deloitte UK screen 4:3 (19.05 cm x 25.40 cm)

© 2013 Deloitte LLP. Private and confidential.

Broad-based share plans – plan types

What type of plans are companies operating?

36%

17%

25%

6%

42%

16%

21%

4%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Share purchase plans

Share option plans

Share award plans

Bonus deferral plans

19

% of

respondents

0% 10% 20% 30% 40% 50% 60%

Bonus deferral plans

Share purchase plans

Share options plans

Share award plans

United States United Kingdom Europe (excl. UK) Australia

Regional prevalence of plan types

Source: Deloitte 2015 GSP survey

Broad-based share plans – share purchase plans Match or discount?

Source: Deloitte 2015 GSP survey 20

% of

respondents

100%

32% 25%

36%

63% 68% 46%

5% 7%

18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

United States United Kingdom Europe (excl. UK) Australia

Share purchase plan at a discount Share purchase plan with a match Combination of both

Deloitte UK screen 4:3 (19.05 cm x 25.40 cm)

© 2013 Deloitte LLP. Private and confidential.

Broad-based share plans – share purchase plans Match or discount/ level of match

Match vs. Discount Level of

match

3%

51%

46%

Combination Discount Match

15%

21%

9%

6% 9%

40%

1 matching share for every 1 purchased1 matching share for every 2 purchased1 matching share for every 3 purchased1 matching share for every 4 purchased2 matching shares for every 1 purchsedOther

Source: Deloitte 2015 GSP survey

21

% of plans % of plans

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Other

Expand the culture of ownership in the group

Be competitive in the market

Provide corporate / group identity

Drive performance

2014

2015

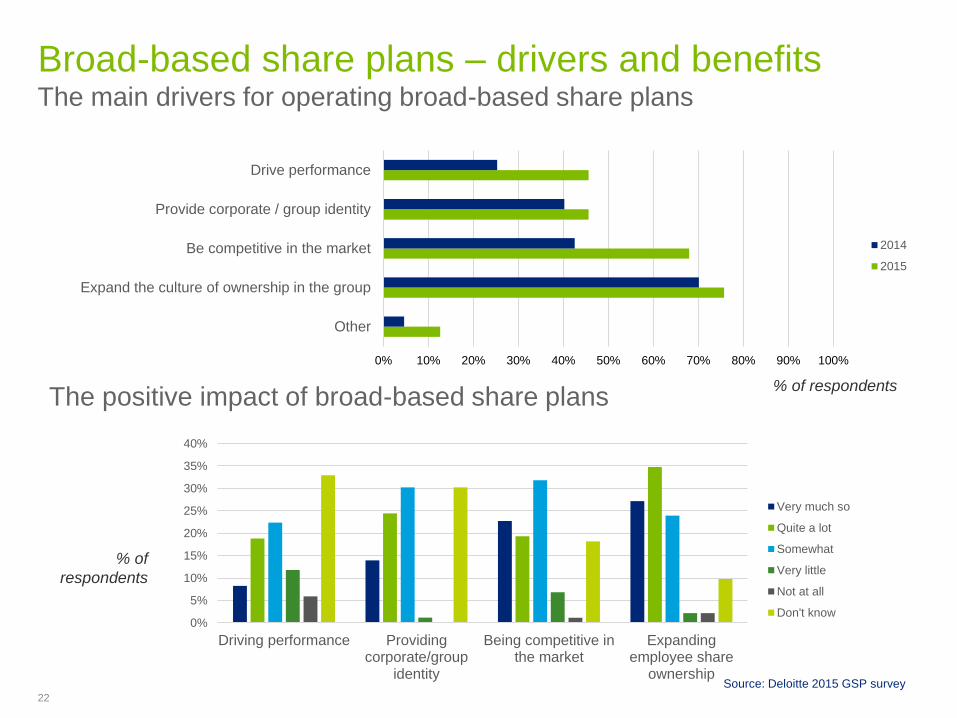

Broad-based share plans – drivers and benefits The main drivers for operating broad-based share plans

22

% of respondents

0%

5%

10%

15%

20%

25%

30%

35%

40%

Driving performance Providingcorporate/group

identity

Being competitive inthe market

Expandingemployee share

ownership

Very much so

Quite a lot

Somewhat

Very little

Not at all

Don't know

% of

respondents

The positive impact of broad-based share plans

Source: Deloitte 2015 GSP survey

Looking ahead Would companies do it all again?

88% 89%

2%

? 9%

Source: Deloitte 2015 GSP survey 23

% of respondents

Operational trends

24

Financing of share plans Do companies net settle awards under global share plans?

38%

48%

29%

25%

33%

26%

Never Sometimes Always

Executive plans

Broad-based plans

Source: Deloitte 2015 GSP survey 25

% of respondents

Taking advantage of local tax breaks Do companies change plan design or operation to get tax breaks?

Source: Deloitte 2015 GSP survey 26

% of

respondents

6% 3%

16%

29%

41%

31%

24%

71%

53%

66% 61%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

United States United Kingdom Europe (excl. UK) Australia

No

Some countries

All countries (where tax breaks available) Some countries No

Mobile employees What tax approach do companies take for mobile employees?

59%

55%

19%

19%

23%

26%

Apportion income between countries based on relevant legislation applicable for eachcountry

Apportion income between countries using a generic approach (e.g. grant to vest in allcountries)

Tax in full in the country in which they are at the tax point

Executive plans

Broad-based plans

Source: Deloitte 2015 GSP survey 27

% of respondents

Recharging share plan costs to employing entities Do companies recharge share plan costs?

61% of respondents recharge the costs of their share plan to the local entities.

Of the 39% of companies not recharging, complexity of operating recharges is cited

as the main reason.

44%

23%

15%

18%

Complexities of operating recharges Potential saving not considered sufficient

Have not had time to consider yet Other

Source: Deloitte 2015 GSP survey 28

% of respondents

Communication for global share plans Quotes from the 2015 Deloitte Global Share Plan Survey

Communication

is really the key

to the success

of a plan

Effective

communication is

critical but challenging

Education and

communication

is critical

The industry as a whole

is not very good at

communicating with

employees, we need to

do a better job

Communication is

the key element

Communicate, communicate,

communicate!

Do not

underestimate the

communication

Keep it simple with

clear concise

communications in

plain English

Invest heavily in

communication

Source: Deloitte 2015 GSP survey 29

Communication for global share plans What is driving companies to invest in new methods of communications?

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Better engagementwith employees

To reduce costs andadministration in the

communicationprocess

Be seen to beinnovative/different

Demand/expectationfrom employees

Other

Executive

Broad-based

Source: Deloitte 2015 GSP survey 30

% of

respondents

Generational trends Which generations value participation in share plans?

2%

4%

13%

18%

14%

27%

39%

33%

14%

7%

2%

1%

68%

62%

49%

49%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Generation Z

Generation Y

Generation X

Employees born before 1960

Strongly Agree Agree Disagree Strongly disagree Don't know

(born 1961 – 1980)

(born 1981 – 1995)

(born from 1995)

Source: Deloitte 2015 GSP survey 31

% of respondents

Equity team

32

Lisa Williamson is an Associate Director within Deloitte’s Compensation & Benefits

practice and has been with the firm for thirteen years.

Lisa began her career in our International Assignment Services group, advising

clients across a broad range of issues affecting globally mobile employees. She began

advising on equity plans in 2007. More recently, Lisa has worked within our Global

Incentives group with a focus on the global tax compliance issues associated with

various types of equity compensation plans. She has also been involved in the design

and implementation of Global Advantage Incentives, Deloitte's automated global tax

withholding solution.

Lisa Williamson

Tel: +44 20 7007 1478

Email: [email protected]

Bill Cohen is a senior partner in Deloitte’s Global Reward Group. He also lead’s

Deloitte’s Global Equity practice.

Bill has over twenty-five years’ experience in this area, and has wide experience in

advising companies in the structuring and implementation of their remuneration

strategies. Bill is particularly well known for his expertise in the area of global share

plans and has worked with numerous of the world’s largest companies in developing

their global share plan strategies.

Bill has written numerous articles dealing with compensation and tax issues which have

been published in journals, newspapers and books. He has also broadcast on the

subject.

Bill has an LLB (Hons) from Nottingham University. He is also qualified as both a

barrister and a solicitor. He is a scholar and prize-winner of Lincoln’s Inn. Bill is a past

secretary to the Society of Share Scheme Practitioners, and a member of the Global

Equity Organisation and the Advanced Share Scheme Study Group.

Bill Cohen

Tel: + 44 20 7007 2952

E-mail: [email protected]

People are at the heart of Global Employer Services delivered by Deloitte. People

who look beyond numbers to focus on individuals, each with individual challenges

and needs.

Deloitte teams pride themselves on being able to support you through every step

of your journey, from compliance to operational excellence, from insight to

implementation. Experience our collaborative working, our connected services and

tools, making an impact that matters for you and your employees.

We continue to build our reputation on understanding our client’s needs, today and

tomorrow. We innovate with purpose, translating leading edge ideas into industry-

leading solutions. Our perspective and action helps you anticipate and navigate

your challenges. Even those yet to arise.

Deloitte Global Employer Services is looking ahead, to help you get ahead:

Moving together. Making tomorrow.

33

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of

which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Deloitte LLP is the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the

particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication.

Deloitte LLP would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte LLP accepts no duty of

care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

© 2016 Deloitte LLP. All rights reserved.

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street Square, London

EC4A 3BZ, United Kingdom. Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198.