“Sharing Experience : IR Challenge and Opportunity” · -3-Disclosure Quality (Speed, Relevant,...

21

-1- “Sharing Experience : IR Challenge and Opportunity” คุณภัทรลดา สง่าแสง รองกรรมการผู ้จัดการใหญ่ ด้านการเงินและบัญชี บมจ. ไทยออยล์ (TOP) 30 พฤษภาคม 2561

-

Upload

vuongthien -

Category

Documents

-

view

213 -

download

0

Transcript of “Sharing Experience : IR Challenge and Opportunity” · -3-Disclosure Quality (Speed, Relevant,...

-1-

“Sharing Experience :

IR Challenge and Opportunity”

คณภทรลดา สงาแสงรองกรรมการผจดการใหญ ดานการเงนและบญช

บมจ. ไทยออยล (TOP)30 พฤษภาคม 2561

-2-

Free PowerPoint Templates

Free PowerPoint

Templates

External challenge that impact TOP Group in the past

2008 2014 2018

Subprime mortgage

crisis ???

1998

TOM YUM GOONG Crisis

Oil Price shock of

2014

Profit improvement Cost saving

-3-

Disclosure Quality (Speed,

Relevant, Accuracy

andMeaningful

IR responsibilities

Internal System

o Internal understanding

o MIS Process

o Two way report

TOP Group

Outcome : Stakeholder buy in, Fair valuation

External Challenge

ex. interest rates move up

Big Data

Peers

Key Content

o Business structure external challenge & strategy

o Industry & Performance

o Financial Performance

o Sustainability

o New Project

o Etc.

Channel

o AGM / EGM

o Roadshow

o Call meeting/ Visit

o Website

o Notification

Investment Community

Big Data

Big Data

-4-

• ความตองการพลงงาน

• เทคโนโลย

• ทางสงคมและการเมอง

ความคาดหวงของผมสวนไดเสยทมากขน

• ผลตอบแทนและการเตบโต

• ปลอดภย

• ความย งยน

ความทาทายของอตสาหกรรม

• การแขงขนดานขนาดและตนทน

• คแขงขนใหม & พลงงานทดแทน

• การขยายธรกจไปสธรกจข นปลาย

แนวโนมโลก:ความไมแนนอนมากขน

Implication to TOP

• ความเปนเลศในการด าเนนงาน

• เพมประสทธภาพและเรงการลงทน

• คนพบเทคโนโลยใหมๆ

• การบรหารความเสยง

• AEC

• ความรวมมอในกลม ปตท.

• ขยายธรกจไปสธรกจข นปลาย (Integrated Downstream)

• พลงงานทย งยนในอนาคต

จดแขงโอกาส

External challenge & strategy

-5--5-

Year on Year Y2016(B) Y2017(B) 3M/18(B)

VS 3M/17Y2018F(C)

Mogas (A) +9.8% +3.7% +4.7% +3.8%

Jet/Kero +6.8% +4.4% +7.6% +3.8%

Diesel (A) +3.1% +2.9% +3.4% +3.1%

Total +5.4% +3.4% +4.5% +3.4%

GDP +3.2% +3.9%(D) N.A. +4.1%(E)

Remarks: (A) Mogas and Diesel includes Ethanol and Biodiesel, respectively

(B) DOEB Statistics

(C) PTT’s Preliminary and TOP Estimation (May-18)

(D) NESDB

(E) BOT’s Estimate (BOT Monetary Report as of Mar-18)

Thailand Oil Demand Growth

Thailand Oil Demand Growth

Thailand oil demand growth at 3.4% YoY in 2018

Industry

-6-

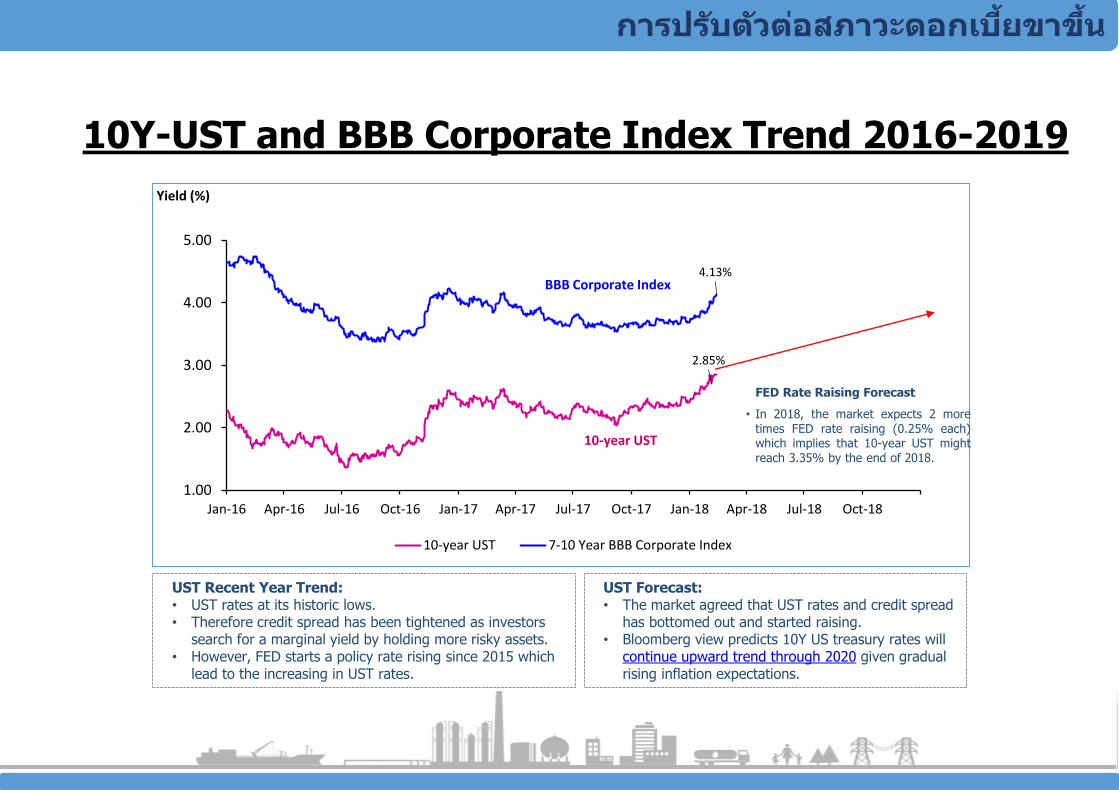

10Y-UST and BBB Corporate Index Trend 2016-2019

2.85%

4.13%

1.00

2.00

3.00

4.00

5.00

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18

Yield (%)

10-year UST 7-10 Year BBB Corporate Index

BBB Corporate Index

10-year UST

UST Recent Year Trend:• UST rates at its historic lows.• Therefore credit spread has been tightened as investors

search for a marginal yield by holding more risky assets.• However, FED starts a policy rate rising since 2015 which

lead to the increasing in UST rates.

UST Forecast:• The market agreed that UST rates and credit spread

has bottomed out and started raising.• Bloomberg view predicts 10Y US treasury rates will

continue upward trend through 2020 given gradual rising inflation expectations.

*Bloomberg consensus on 10Y-UST on 14 February 2018 23

FED Rate Raising Forecast

• In 2018, the market expects 2 moretimes FED rate raising (0.25% each)which implies that 10-year UST mightreach 3.35% by the end of 2018.

การปรบตวตอสภาวะดอกเบยขาขน

-7--7-

49.1%

20.8%

11.1%

19.0%

PTT

Foreign Investors

Local Investors

NVDR

As of 2 Mar 2018

Equity holders breakdown Roadshow Plan

Investor Relations Plano Proactively reach out stakeholder.o Develop effective communication to support key

corporate decision making. o Focus on disclosure and sustainability.o Develop IR communication process.

การปรบตวตอสภาวะดอกเบยขาขน

Thailand21%

Europe & Asia 48%

U.S. 31%

Thailand Europe & Asia U.S.

Thai Oil’s Bond Holder

-8--8-

TOP average debt life

การปรบตวตอสภาวะดอกเบยขาขน

-9--9-การปรบตวตอสภาวะดอกเบยขาขน

-10-การปรบตวตอสภาวะดอกเบยขาขน

IR as part of Symphony (Target set up workshop)

-11-

11

การปรบตวตอสภาวะดอกเบยขาขน

Achievement in Liability Management

-12--12-Digital IR Example

-13--13-Example digitalize by Moody’s

-14--14-

-15-

Thank you

-16-

Back Up

16

-17--17-ความทาทายและโอกาสของงาน IR ในปจจบน

MiFID IIกระทบกบแผนงาน IR อยางไร

1. Conference with Bank 2. Business Trip 3. เขาหานกลงทนโดยตรง

Machine Learning กระทบกบการท างานของ IR อยางไร

1. Big Data Feed data to social media

2. เขาใจตรรกกะการท างานและกระบวณการตดสนใจของคอมพวเตอร แลวปรบกระบวณการท างานและกจกรรมตางๆใหสอดคลองกน

3. The Real you มาจาก Big Data 4. Odyssey project Symphony5. Channel interactive Approach

กระแส Digital Disruption ในอตสาหกรรมตางๆกระทบตอการท างานของ IR อยางไร มค าถามเกยวกบเรองดงกลาวจากนกลงทน นกวเคราห มากนอยแคไหน-

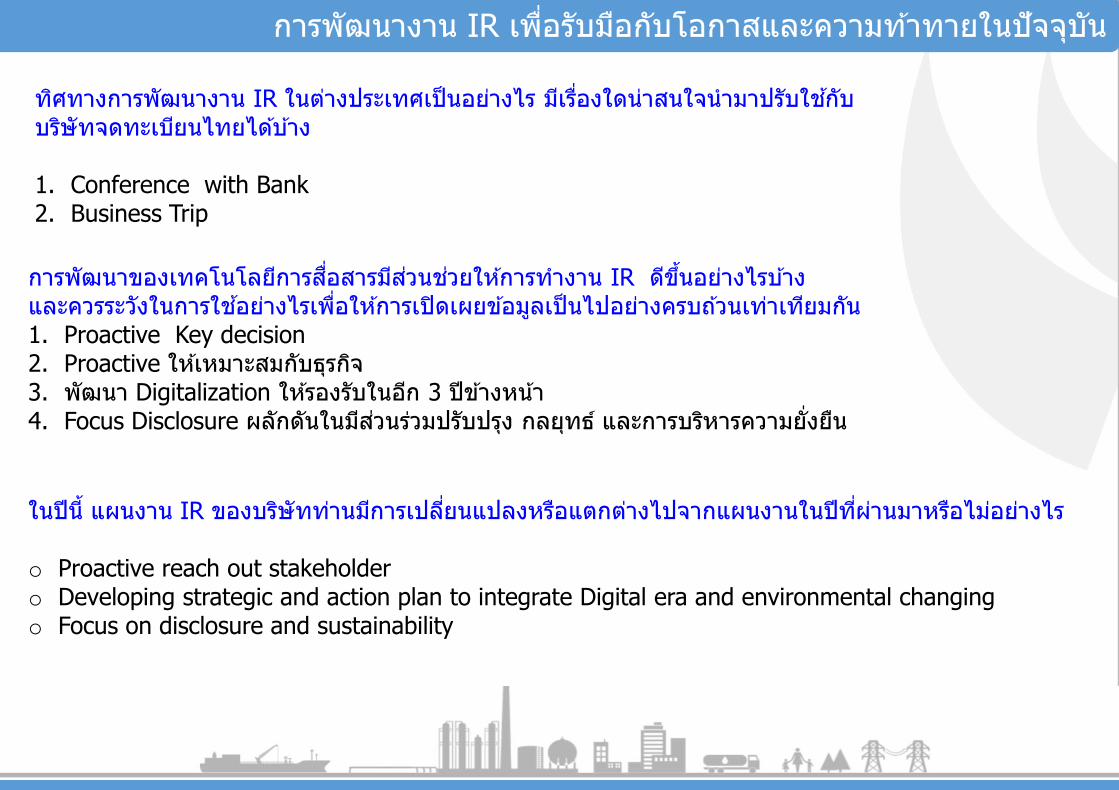

-18--18-การพฒนางาน IR เพอรบมอกบโอกาสและความทาทายในปจจบน

ทศทางการพฒนางาน IR ในตางประเทศเปนอยางไร มเรองใดนาสนใจน ามาปรบใชกบบรษทจดทะเบยนไทยไดบาง

1. Conference with Bank 2. Business Trip

การพฒนาของเทคโนโลยการสอสารมสวนชวยใหการท างาน IR ดขนอยางไรบาง และควรระวงในการใชอยางไรเพอใหการเปดเผยขอมลเปนไปอยางครบถวนเทาเทยมกน1. Proactive Key decision2. Proactive ใหเหมาะสมกบธรกจ3. พฒนา Digitalization ใหรองรบในอก 3 ปขางหนา4. Focus Disclosure ผลกดนในมสวนรวมปรบปรง กลยทธ และการบรหารความยงยน

ในปน แผนงาน IR ของบรษททานมการเปลยนแปลงหรอแตกตางไปจากแผนงานในปทผานมาหรอไมอยางไร

o Proactive reach out stakeholdero Developing strategic and action plan to integrate Digital era and environmental changingo Focus on disclosure and sustainability

-19--19-

TOP : บรษท ไทยออยล จ ำกด (มหำชน)

0

200

400

600

800

1000

1200

1400

1600

1800

2000

0

20

40

60

80

100

120

26

-Oct

-04

10

-Jan

-05

22

-Mar

-05

09

-Ju

n-0

52

3-A

ug-

05

02

-No

v-0

51

6-J

an-0

62

8-M

ar-0

61

9-J

un

-06

30

-Au

g-0

61

0-N

ov-

06

25

-Jan

-07

09

-Ap

r-0

72

5-J

un

-07

05

-Se

p-0

71

5-N

ov-

07

31

-Jan

-08

16

-Ap

r-0

83

0-J

un

-08

11

-Se

p-0

82

1-N

ov-

08

06

-Fe

b-0

92

4-A

pr-

09

13

-Ju

l-0

92

2-S

ep

-09

02

-Dec

-09

16

-Fe

b-1

00

6-M

ay-1

02

1-J

ul-

10

05

-Oct

-10

17

-Dec

-10

02

-Mar

-11

23

-May

-11

03

-Au

g-1

11

3-O

ct-1

12

7-D

ec-1

10

9-M

ar-1

22

8-M

ay-1

20

8-A

ug-

12

18

-Oct

-12

03

-Jan

-13

15

-Mar

-13

03

-Ju

n-1

31

5-A

ug-

13

25

-Oct

-13

10

-Jan

-14

24

-Mar

-14

10

-Ju

n-1

42

5-A

ug-

14

04

-No

v-1

42

0-J

an-1

50

1-A

pr-

15

22

-Ju

n-1

50

3-S

ep

-15

13

-No

v-1

52

8-J

an-1

61

1-A

pr-

16

29

-Ju

n-1

61

3-S

ep

-16

23

-No

v-1

60

7-F

eb

-17

24

-Ap

r-1

70

5-J

ul-

17

18

-Se

p-1

73

0-N

ov-

17

14

-Fe

b-1

8

TOP VS SET TOP Share Price SET Index

-20--20-

51% 25% 13% 11%

Thai Oil Group Business Structure

Net Profit Contribution

(Avg. from 2006 – 2017)

IRPC 20.0%

• 4 Oil & Chemical TankersCapacity : 20,100 DWT

• Crude Tankers: 3VLCCsCapacity: 881,050 DWT

• 14 crew & utility boats (120 DWT each)

• 2 Large vessels for crude, feedstock & product storage and transportation servicesCapacity: 200,000 DWT

• Ship management services

9.2 %

Principal power plant of PTTTotal Equity Capacity 1,922 MW of electricity 1,582 tons/hour of steam 2,080 Cu.m./hour of Industrial water 12,000 RT of Chilled water

PTT Group 80.0%

100.0% 100.0% 74.0% 100.0%

Thaioil (TOP)Thai Lube Base

(TLB)Thaioil Power

(TP)

Global Power Synergy Public Company Limited

Thaioil Energy Services(TES)

Thaioil Marine(TM)

Capacity : 275,000 barrels/day Small Power Producer

Program3-on-1 Combined CycleElectricity 118 MWSteam 216 tons/hour

PTT 26.0%

Proceeds the business on various professional of management services

100.0%

Thappline (THAP)

Multi-product PipelineCapacity:26,000 m.lts/y

20.0%

PTT 40.4%

Others 50.4%

Lube Base Oil Capacity :Base Oil 267,015 tons/annumBitumen350,000 tons/annumTDAE67,520 tons/annum

Thaioil SolventThrough TOP Solvent (TS)

100.0%

100.0%

Thaioil Ethanol(TET)

Solvent manufacturerCapacity : 141,000tons/annum

Thai Paraxylene(TPX)

100.0%80.5%

Solvent distribute in Thailand

Sak Chaisidhi (SAKC)

Top Solvent Vietnam

Solvent distribute in Vietnam

Sapthip (SAP)

Cassava Based EthanolCapacity : 200,000 lts/day

50.0%

Ubon Bio Ethanol (UBE)

21.3%

Cassava/Molasses Based PlantCapacity : 400,000 lts/day

PTT Energy Solutions(PTTES)

Provides engineering technique consulting services

20.0%

PTT 40.0%PTTGC 20.0%

BCP 21.3%

Others57.4%

Aromatics Capacity:Paraxylene 527,000 tons/annumMixed Xylene52,000 tons/annumBenzene 259,000 tons/annumTotal 838,000 tons/annum

LABIX Company Limited (LABIX)

LAB producer and distributorCapacity: 120 KTA COD: 2016

Mitsui 25.0%75.0% TOP SPP

2 Small Power Producers Total capacity: 239 MWSteam capacity 498 T/HCOD 2016

100.0%

Sells Electricity/Steam to Group

PTT Digital Solutions(PTT Digital)

PTT 22.6%

Thaioil & TP 29.7%

PTTGC 22.7%

Thaioil Treasury Center(TTC)

100.0%

Increases financial efficiency of Thaioil group

Supports execution of social enterprise of PTT group

15.0%PTT Group 85.0%

Sarn Palung Social Enterprise

-21-