SHARIAH CHALLENGES IN SUKUK CHALLENGES IN SUKUK ... Maqasid Agenda Shariah Issues in Sukuk . ......

23

SHARIAH CHALLENGES IN SUKUK Prof. Dr. Mohamad Akram Laldin Executive Director, ISRA

Transcript of SHARIAH CHALLENGES IN SUKUK CHALLENGES IN SUKUK ... Maqasid Agenda Shariah Issues in Sukuk . ......

SHARIAH CHALLENGES

IN SUKUK

Prof. Dr. Mohamad Akram Laldin Executive Director, ISRA

Introduction

• Sukuk is one of innovative instruments in Islamic capital market to fund long-term financing in a Sharīʿah compliant way.

• It provides an alternative for corporate and government for funding national and international development projects to the predominantly interest debt-based instruments of bonds.

• The successful of its development in the global scene is a result of exhaustive efforts from Islamic financial institutions and fiqh councils to provide a substitute for riba-based instruments to meet the ever-increasing demand for large-scale Sharīʿah-compliant financing.

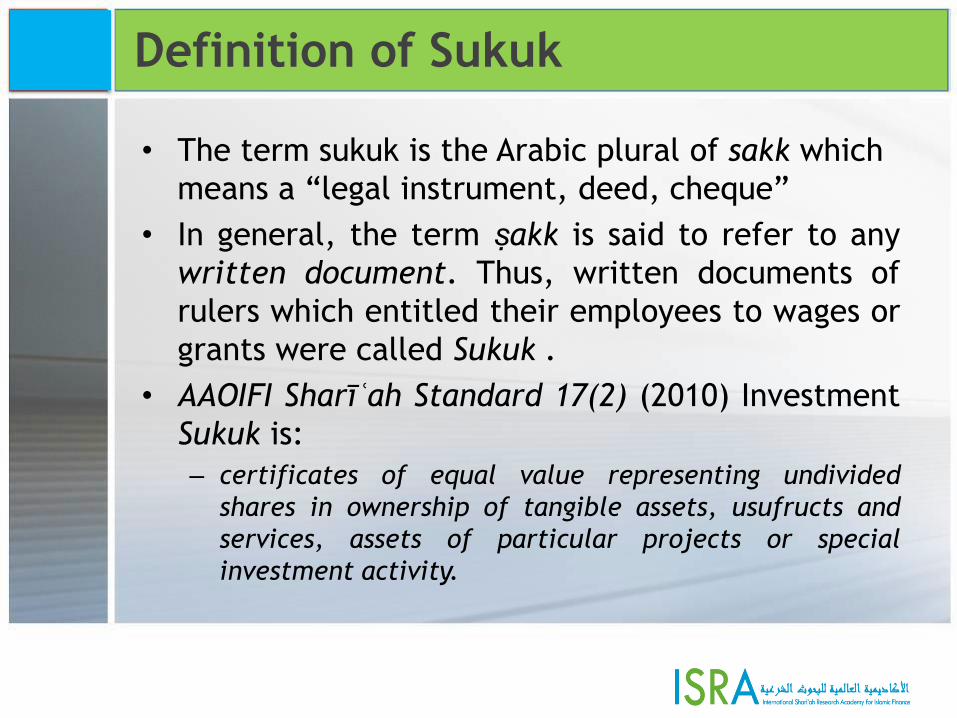

• The term sukuk is the Arabic plural of sakk which

means a “legal instrument, deed, cheque”

• In general, the term ṣakk is said to refer to any

written document. Thus, written documents of

rulers which entitled their employees to wages or

grants were called Sukuk .

• AAOIFI Sharīʿah Standard 17(2) (2010) Investment

Sukuk is:

– certificates of equal value representing undivided

shares in ownership of tangible assets, usufructs and

services, assets of particular projects or special

investment activity.

Definition of Sukuk

Definition of Sukuk

• Certificates of equal value

representing undivided shares in

ownership of tangible assets,

usufruct and services or (in the

ownership of) the assets of

particular projects or special

investment activity

AAOIFI (Shariah Standard 17 (2)

2015)

• Certificates of equal value which

evidence undivided ownership or

investment in the assets using

Shariah principles and concepts

approved by the SAC

SAC-SC

(Guidelines on Sukuk, 2012)

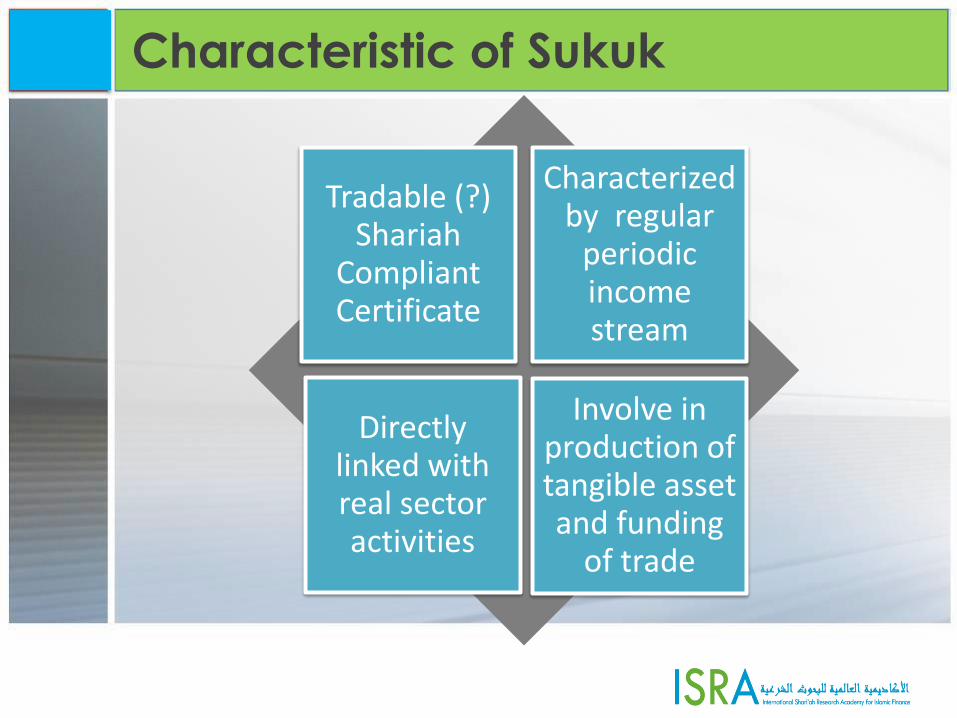

Characteristic of Sukuk

Tradable (?) Shariah

Compliant Certificate

Characterized by regular

periodic income stream

Directly linked with real sector activities

Involve in production of tangible asset and funding

of trade

SHARIAH ISSUES IN

SUKUK STRUCTURING

Documentation

Underlying Assets

Ownership

Right of Disposal

Sukuk Proceeds

Return

Secondary Market Trading

Purchase Undertaking

Maqasid Agenda

Shariah Issues in Sukuk

A. Documentation:

• Proposal form and contractual agreement should conform to

Sharīʿah requirements.

• Observe the requirement of Islamic contract – general principles of fiqh muamalat .

• Avoid prohibitions in Shariah (riba, gharar, maysir etc)

• Clear and transparent specification of rights and obligations of all parties to the transaction, in particular the originator (customer) and sukukholders.

• Income from securities must be related to the purpose for which the funding is used, and not simply comprise of interest.

• Securities must be backed by real underlying assets – rather than being simply paper derivatives.

• Approved by Shari’ah advisors.

• Material information that must be disclosed in the issuance of Islamic securities:

Details of utilisation of proceeds

Underlying/ identified assets

Shariah principles used Name of Shariah advisor Declaration statement from

Shariah advisor Description of facility /

structure Prices i.e. sale & purchase

price Details on primary &

secondary sukuk

B. Underlying Assets

• It is a fundamental requirement of underlying assets

in ṣukūk issuance must be Sharīʿah compliant (SAC-

SC, 7th meeting, 1995)

– Zarqā (2004, p.426): Assets should be subject to intrinsic

value of the contract.

– SAC-SC (2007, p.77): Assets in ṣukūk takes the rule of

māl in Sharīʿah.

– Māl can be movable and immovable (Bāshā, Muḥamad

Qadrī, 1308A.H, p.3-4).

C. Ownership of Underlying Assets

AAOIFI Pronouncement on Sukuk (2008):

• Investors have an undivided interest in the

underlying assets and are therefore entitled to

share jointly the related returns/cashflows.

• Sukuk must represent proportionate ownership

of the Sukuk investors in the underlying asset,

project, right/services.

• This ownership must entail both the rights and

obligations of the investors. As such there must

be a transfer of assets to the investors.

Legal and Beneficial Ownership

• From Sharīʿah perspective, al-milkiyyah (ownership) is all inclusive.

• It embraces mainly three elements, the substance of Sharīʿah (ḥaqīqah Sharʿiyyah); subject and effects of the ownership; relationship between owner and the object owned.

• In reference to authority, ownership can be complete ownership and incomplete ownership.

Continue…

• Complete ownership gives

authority to asset, its

usufructs and unconditional

rights to the asset.

• Characteristics:

rights to disposal of assets;

rights to usufructs;

first ownership;

not timing;

subject to transfer;

no liability for defects by

owner

Incomplete ownership

gives either legal or

beneficial and/or usufruct

rights.

Characteristics:

legal ownership only:

transferrable; no timing;

separable from beneficial

rights; can be banished.

beneficial ownership:

subject to restriction in

time, place, and manner of

usage.

it is personal right to

usufructs without ownership.

Continue…

Sharʿīah Principles of the same characters on the

ownership issues:

1) Bayʿ al-Wafāʾ which is allowed by some medieval scholars of

Ḥanafī and Shāfiʿī based on customary practices, need and

avoidance of ribā.

2) ʿAqd Tamalluk al-Zamanī (Time Sharing)

– Ownership of assert via lease or sale by way of time sharing. It

is approved by OIC-Fiqh Academy.

3) Ḥaqq Hikr (Right to monopolize Waqf Landed Property)

It is a contract in which waqf property is leased for long-term

period to a lessee.

Ibn ʿĀbidīn, it is a kind of lease contract with the aim to prevent

others from accessing the waqf property by use of long-term

lease known as (ḥikr).

Restriction in right of Sukuk holders to dispose asset

Since Sukuk holders do not have interest in the underlying asset,

they cannot dispose the asset to third parties

They rely on Purchase Undertaking which promises principal +

unpaid profit

In most cases, the asset used to facilitate an asset based

Sukuk will continue to stay on the balance sheet of the

obligor.

Although this restriction is not explicitly mentioned in Shariah

related documents, it is clearly indicated in the offering

circular’s risk section and the enforcement and exercise of

rights clause.

D. Right of Asset Disposal

E. Sukuk Proceeds

• Funds raised must be used for Shariah compliant (halal) activities.

• Fund raised may be used to finance needed tangible assets.

• Specificity of assets is important, since Sukuk unlike conventional bonds cannot be used for general financial needs of the issuer.

F. Return/profit Payment

• Income received by sukukholders (investors) must

be derived from the cash flows generated by the

underlying.

• Loan provided by the Issuer to the investors to

smoothen the profit payment is not permissible.

However, the Issuer can:

– Establish reserve account; or

– Apply “profit on account” methodology; or

– Assist the sukuk investors to get Islamic financing to

smoothen the profit payment.

– Hence, no liquidity facility, top-up payment

G. Secondary Market Trading

Type Features Tradability

Murabahah Sakk represents assets purchased & intended for sale. Once sale is made, the sakk represents a debt. In M’sia – this is short term debt security

Sukuk are only tradable under Malaysian rules

Ijarah Sakk must lay title claim to asset. The claim may be direct or beneficial.

Sukuk are universally tradable

Musharakah Sakk must lay title claim to asset, but this may include participation in business ownership or operations. Frequently, an undertaking is added to make musharakah operation more debt like.

Depending on the underlying asset, these sukuk are tradable. In M’sia, the underlying asset may be a permissible debt form such as a murabahah receivable.

BBA Sakk represents assets purchased and intended for sale. Once the sale is made, the sakk represents a debt. In M’sia – this is a long term debt security

Sukuk are only tradable under Malaysian rules.

Wakalah Sukuk holders appoint the beneficiary of funds as their agent to perform certain business operations.

Depending on the underlying asset, these sukuk are tradable. In M’sia, the underlying asset may be a permissible debt form such as a murabahah receivable.

Bay al-Dayn in debt based sukuk in secondary

market trading

• AAOIFI (Shariah Standard No 17,

para 5/2/15) on Sukuk

Murabahah:

– The sukuk is acknowledged

– It can be traded after

purchasing of asset and before

selling it to the buyer.

– It can not be traded after the

delivery of the asset to the

buyer.

– Reason: The subject matter is

considered as financial asset

(receivable). Issue on sale of

debt (bay’ al-dayn)

Shariah Advisory Council of

Securities Commission,

Malaysia:

Can be sold at a discount in a

securitization exercise.

Bay’ al-dayn is adopted based

on the views of some scholars

(Malikis & Shafiites) who

allowed this principle subject to

certain conditions.

In capital market, these

conditions are met with a

transparent regulatory system

which can safeguard the

interest of the market

participants

However, the securitisation of HYBRID ASSET is acceptable if it consists of at least 30%

of physical asset (refer to AAOIFI Shariah Standard no 21.)

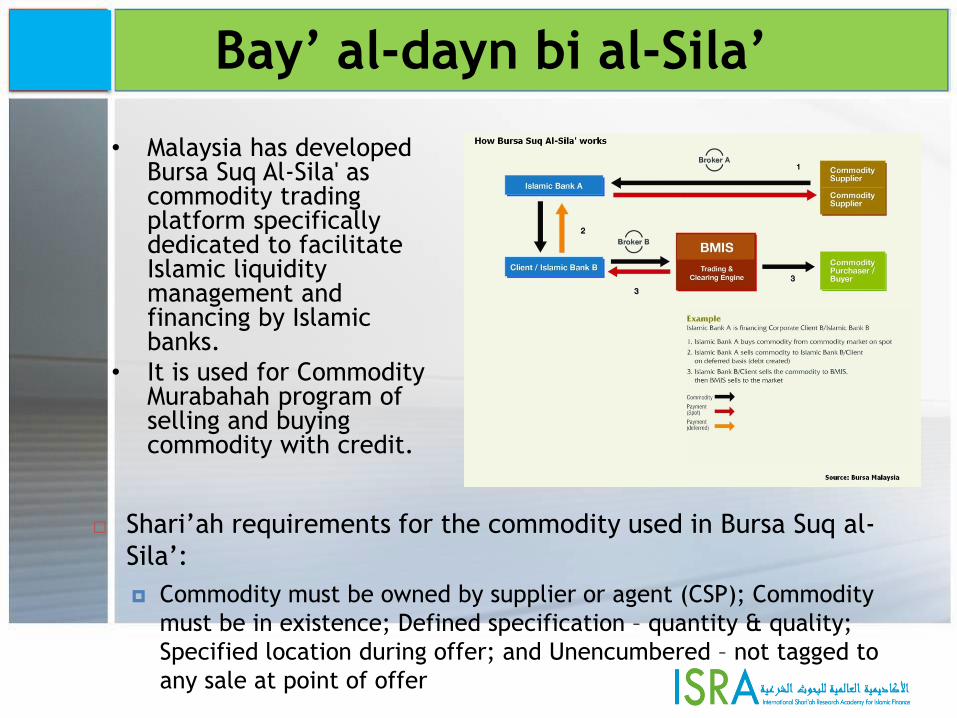

Bay’ al-dayn bi al-Sila’

• Malaysia has developed Bursa Suq Al-Sila' as commodity trading platform specifically dedicated to facilitate Islamic liquidity management and financing by Islamic banks.

• It is used for Commodity Murabahah program of selling and buying commodity with credit.

Shari’ah requirements for the commodity used in Bursa Suq al-

Sila’:

Commodity must be owned by supplier or agent (CSP); Commodity

must be in existence; Defined specification – quantity & quality;

Specified location during offer; and Unencumbered – not tagged to

any sale at point of offer

H. Purchase Undertaking

• Purchase undertaking is an agreement that states the obligor

shall execute a purchase undertaking in favor of the trustee on

or about the closing date all of the Trustee’s rights, title and

interest in and to the investment Assets at the exercise price.

• Purchase undertaking is actually intended to dissolve the

contract relating to the Sukuk whereby the Sukuk issuers buy

back all of the Sukuk from the investor and the investor will

recover his principal investment by getting the cash.

• The agreement of purchase undertaking is developed based on

the concept of promise (wa’d) between the issuers and investors

to buy back the ownership of The agreement of purchase

undertaking is developed based on the concept of promise

(wa’d) between the issuers and investors to buy back the

ownership of sukuk.

• Securities Commission Malaysia (2012: 161) views the promise (wa’d) for purchase undertaking is legitimate and binding upon the promisor (issuer who give promise).

• However the exercise prices, according to AAOIFI in their Pronouncement (2008) “shall be based either market value; or Fair value; or a price to be agreed at the time of exercise”.

• Any agreement to purchase the assets at face value/ nominal value is not permissible.

• This is only permissible in the case of negligence and misconduct of the Issuer

I. Maqasid Agenda

• Maqasid should be given consideration apart from

fiqh legal requirements

• Ethical & ESG Sukuks

• Real economics impact

• Benefit to all segment of the societies

• Its timely for Islamic finance to move away from

conventional practices and introduce a better holistic

solutions.