SHANGHAITECH SEM WORKING PAPER SERIES No. 2021-006

38

SHANGHAITECH SEM WORKING PAPER SERIES No. 2021-006 A Merger with a Maverick Firm: Examining the Coordinated Effects in the AA/USAir Merger Soo Jin Kim School of Entrepreneurship and Management, ShanghaiTech University Yongjoon Park Department of Resource Economics, University of Massachusetts, Amherst June 30, 2021 https://ssrn.com/abstract=3877895 School of Entrepreneurship and Management ShanghaiTech University http://sem.shanghaitech.edu.cn

Transcript of SHANGHAITECH SEM WORKING PAPER SERIES No. 2021-006

SHANGHAITECH SEM WORKING PAPER SERIES No. 2021-006

A Merger with a Maverick Firm:

Examining the Coordinated Effects in the AA/USAir Merger

Soo Jin Kim

School of Entrepreneurship and Management, ShanghaiTech University

Yongjoon Park

Department of Resource Economics, University of Massachusetts, Amherst

June 30, 2021

https://ssrn.com/abstract=3877895

School of Entrepreneurship and Management

ShanghaiTech University http://sem.shanghaitech.edu.cn

A Merger with a Maverick Firm: Examining the Coordinated Effects

in the AA/USAir Merger

Soo Jin Kim∗ Yongjoon Park†

June 30, 2021

Abstract

This paper studies the coordinated effects of the merger between American Airlines and USAirways by examining the extent to which the connecting prices of the nonmerging legacy carriers(Delta and United) evolved when the merger eliminated Advantage Fares, a connecting flight pricediscounting program offered by US Airways. In our empirical analysis, we find that postmergernonmerging legacy carriers substantially increased their connecting flight prices in routes where USAirways had a dominant position, and a similar pattern can be found for the merging carriers inroutes where nonmerging legacy carriers had a dominant position. We next conduct a theoreticalanalysis in which we show that these empirical findings can be explained by the elimination ofmaverick firms and how such elimination facilitates coordinated conduct among legacy carriers.Finally, we note the potential importance of connecting services in merger analysis in the airlineindustry.

Keywords: Airline Mergers, Merger Analysis, Coordinated Effects, Maverick FirmJEL Classification Numbers: L93, L41, L44

∗[email protected]; School of Entrepreneurship and Management, ShanghaiTech University, Room 436,393 Middle Huaxia Road, Shanghai.

†[email protected]; Department of Resource Economics, University of Massachusetts, Amherst.

1 Introduction

Competitive authorities investigate anticompetitive effects in markets when evaluating proposed merg-

ers. The anticompetitive effects of mergers arise from the elimination of competition between merging

entities, which increases their market power; this is referred to as the unilateral effects of mergers.

Mergers can also diminish market competition by facilitating coordinated conduct among merging

and nonmerging firms; this is referred to as the coordinated effects of mergers. In merger evaluations,

although the authorities have a formal quantitative procedure to examine the unilateral effects via

merger simulation, there is no systematic procedure for evaluating the coordinated effects largely be-

cause there are many collusive behaviors; therefore, the effect is reviewed case by case (Porter (2020);

Miller and Weinberg (2017); Greenfield et al. (2019)).

Anticompetitive concerns regarding a merger become more relevant when it involves a maverick

firm. A maverick firm—a firm that plays a disruptive role in a market to the benefit of customers—

typically fosters competition and brings innovation to markets; therefore, a proposed merger absorbing

a maverick firm may have substantial unilateral effects. In addition, because a maverick firm can ob-

struct collusive conduct among established firms in concentrated markets, there is a serious concern

that such a merger would increase coordinated interaction among incumbents postmerger. As Hor-

izontal Merger Guidelines (Department of Justice) (2010) explicitly notes, a merger eliminating a

maverick firm that takes place in a market more vulnerable to coordinated conduct, namely, the air-

line industry, is likely to result in anticompetitive effects, particularly those driven by coordinated

effects. Although this concern regarding the coordinated effect has been shown in a wide range of

high profile merger cases in which maverick firms are acquired (ABI/Modelo; H&R Block-TaxACT;

T-Mobile/Sprint; American Airlines/US Airways), the academic literature tends to focus more on the

unilateral effects that can be examined with standardized quantitative approaches.

In this paper, we study the coordinated effects of a merger that involves a maverick firm in the

context of the merger between American Airlines (AA) and US Airways (USAir). Specifically, we

examine the extent to which the connecting prices of nonmerging legacy carriers—Delta Air Lines

(DL) and United Airlines (UA)—evolved when the merger eliminated the Advantage Fares employed

by USAir. There are two reasons we focus on the AA/USAir merger case in the U.S. airline industry.

First, the AA/USAir merger provides an ideal setting for studying the coordinated effect. Prior

to the AA/USAir merger which was completed in December 2013, USAir was considered a maverick

firm due to an attractive lower fare option called Advantage Fares that it offered in its connecting

routes (Department of Justice. (2013)). USAir offered the Advantage Fares that provided discounts

1

on connecting flights for price-sensitive passengers by undercutting rivals’ nonstop prices, especially

for last-minute bookings.1 The USAir pricing strategy, according to the U.S. Department of Justice

(DOJ), was different from the industry norms in which a legacy carrier would respect its rival legacy

carrier’s nonstop pricing for the rival’s dominant route by not aggressively pricing its connecting service

on the route. The carrier would do this with the hope that the rival would adopt the same strategy in

the legacy carrier’s dominant nonstop route (Department of Justice. (2013)). The DOJ claimed that,

in response to the USAir’s disruptive pricing strategy, three other legacy rivals—AA, DL, and UA

(henceafter, Major3 )—also discounted their connecting flight prices in routes where USAir offered

nonstop service, leading to a price war between USAir and those legacy carriers. Merger opponents

argued that the merger would deter aggressive discounting and facilitate collusive conduct among

merging and nonmerging legacy carriers, as the merger would eliminate the Advantage Fares.

Our second reason for focusing on this merger is the U.S. airline industry context, as it has

several unique features that could facilitate coordinated conduct. First, a series of mergers in recent

decades have made the industry more concentrated, with fewer carriers. In theory, collusion is more

sustainable when there are fewer participants. Moreover, carriers can easily monitor the pricing and

seat availability of their rivals in nearly real time. This price and capacity transparency can facilitate

collusion, making the airline industry vulnerable to coordinated conduct. (Department of Justice.

(1993); Horizontal Merger Guidelines (Department of Justice) (2010); Porter (2020)) Additionally,

carriers concomitantly operate services in a large number of markets, leading to a high amount of

multimarket contact; and there is an extensive understanding in the literature that multimarket contact

can facilitate collusive behaviors (Berheim and Whinston (1990); Evans and Kessides (1994); Ciliberto

and Williams (2014); Porter (2020)).2

We first document that around the AA/USAir merger, the connecting service prices of nonmerging

legacy carriers (e.g., DL and UA) dramatically changed in routes where USAir had a dominant posi-

tion. Specifically, premerger, the 90th quantile price of connecting services offered by the nonmerging

legacy carriers, a proxy for tickets transacted at the last minute, was substantially lower in routes

where USAir was the only carrier offering nonstop service (henceafter, USAir nonstop routes) than

1The underlying driving factor that allowed USAir to implement the Advantage Fares is that its hubs, located inCharlotte, Philadelphia, Phoenix, and Washington D.C., generate less revenues from offering nonstop services due tolower traffic than the hubs of other legacy carriers. Note that some previous studies treat USAir as a legacy carrier(e.g., Berry and Jia (2010)), whereas we view it as an example of a maverick carrier because of its innovative ‘AdvantageFares’ pricing strategy. This difference reflects that there is no standard definition of a maverick firm. For example,while Horizontal Merger Guidelines (Department of Justice) (2010) defines one as “a firm that plays a disruptive role inthe market to the benefit of customers,” Ivaldi et al. (2003) views it as “a firm with a drastically different cost structure,which is thus unwilling to participate in a collusive action.”

2These industry features are potentially related to the fairly recent allegation regarding the industry’s “capacitydiscipline”—carriers have limited the growth of seat availability gradually over time and increased prices.

2

in routes where one of the Major3 carriers was the nonstop monopolist (henceafter, Major3 nonstop

routes). However, after the merger, the connecting prices in USAir nonstop routes increased by 27.7%

relative to those in Major3 nonstop routes. We also find that some reciprocity exists for merging

carriers. In routes where DL or UA was the nonstop monopolist premerger (henceafter, nonmerging

legacy nonstop routes), the 90th quantile connecting prices of merging carriers were 10.4% lower than

those of the nonmerging legacy carriers in the same route group, which reflect the discounts of the

Advantage Fares by USAir. Postmerger in the same routes, however, the merging carriers’ connecting

prices increased by 6.6% relative to those of the nonmerging carrier.

We then move on to develop an intuitive theoretical model to characterize the conditions under

which the empirical patterns that we find can be supported. By using the nested logit utility speci-

fication with three airlines (AA, DL, and USAir) that operate in three different markets, we derive

the market share for each carrier. Given that airlines compete in prices in multimarket, we consider a

conduct parameter when defining each airline’s profit function, as in Bresnahan (1982) and Berheim

and Whinston (1990), to capture the degree of coordination among legacy carriers (DL and AA).

In this main theoretical model, we find that when nonmerging entity DL provides a connecting

service, it charges a relatively higher airfare against nonstop legacy carrier AA than nonstop maverick

carrier USAir absent the merger. Furthermore, we find that such strategic pricing behavior by DL

against USAir becomes more aggressive as coordination between DL and AA becomes more feasible.

However, post merger, this aggressive pricing strategy against nonstop maverick carriers disappears.

Additionally, in the market in which DL is the nonstop monopolist, the merged entity of AA and

USAir raises prices postmerger, which suggests that USAir is no longer a maverick firm that provides

a substantial price discount. We also find that the postmerger price for the merging entity increases

in the conduct parameter: that is, as it becomes easier for legacy carriers to engage in collusion, the

merged entity faces less competitive pressure and therefore charges higher prices. In Appendix B, we

extend our theory model by taking cost asymmetry between nonstop and connecting and/or between

legacy and maverick carriers into consideration. From the extended model, we find qualitatively similar

results.

We conclude by remarking on the importance of connecting flights in airline merger analysis and

discussing relevant policy implications. Airline merger analysis primarily focuses on a set of routes

where merging carriers are a nonstop duopoly. On the other hand, a connecting flight is considered a

low-quality product and has a limited ability to constrain market power; hence, it has been of second

order importance in merger analysis. While the nonstop routes represent substantial anticompetitive

concerns, their passenger share is very small (e.g., 1% of passengers were in AA/USAir nonstop

3

duopoly routes). Additionally, given that 20-30% of passengers were in the connecting routes affected

by the elimination of Advantage Fares due to the AA/USAir merger, consumer surplus losses due to

a connecting flight price increase in those routes may be substantial enough to raise anticompetitive

concerns. This potentially suggests that it is important for merger control to consider potential

consumer harm through a wider range of routes rather than focusing on a few sets of local routes in

airline merger analysis.

Literature review This paper contributes to the literature on the coordinated effect of mergers.

Porter (2020) notes that unlike unilateral effects, coordinated effects do not lend themselves to a

standardized merger review procedure. Focusing on the Miller/Coors merger in the U.S. brewing

industry, Miller and Weinberg (2017) find that the postmerger prices are 6 to 8 percent higher than

they would have been if the merger impacted pricing through only unilateral effects and not through

coordinated effects. Miller et al. (2021) extend the previous work by considering price leadership in

the U.S. brewing industry to explain the coordinated effects of the Miller/Coors merger. Focusing

on a merger in the Swedish analgesics market, Bjornerstedt and Verboven (2016) show that partial

coordination explains some of the price increase for nonmerging firms that did not face a marginal cost

increase. Brito et al. (2018) propose an empirical structural methodology to quantify the coordinated

effects of partial horizontal acquisitions. Loertscher and Marx (2021) first develop a theory of collusive

behavior to quantify the adverse effects of such conduct. Then, Loertscher and Marx (2021) not only

identify tradeoffs between unilateral and coordinated effects but also show that whether a merger

involving a maverick firm harms market competition via coordinated effects depends on market-specific

aspects.

Our work is also related to antitrust issues in the U.S. airline industry. A series of mergers and

acquisitions of airline carriers in recent decades have led to more concentrated markets. Accordingly,

there has been a large body of literature on airline mergers (Ashenfelter et al. (2014); Li et al. (2021);

Park (2020); Das (2019)). There are several studies regarding the issues around collusive behaviors in

the industry. Related to multimarket contact, Evans and Kessides (1994) find that a higher amount of

market contact is positively associated with airline ticket prices. Ciliberto and Williams (2014) build a

structural model in which a conduct parameter is a function of carrier-pair multimarket contacts and

explores to what extent the contacts facilitate tacit collusion among airlines. Other studies focus on

“capacity disciplines.” Aryal et al. (2020) study the relationship of public communication via earning

calls with a carrier’s capacity reduction. Hazel (2018) finds that there is a negative relationship

between airline capacity and average domestic revenue per available seat mile.

Our work contributes to the literature in several ways. First, to the best of our knowledge,

4

this is the first study in the literature documenting an unusual price increase of nonmerging legacy

carriers after the AA/USAir merger, which is a merger with a maverick firm, and showing that it

can be theoretically explained by the coordinated effects of mergers. In addition, we emphasize that

connecting flights can play a crucial role in airline merger reviews, which have been overlooked in the

existing framework. Nonstop flight services in concentrated markets (e.g., routes in which merging

carriers are a nonstop duopoly) have been typically at the core of merger reviews due to its strong

consumer preference over connecting services. However, this paper suggests that connecting services

can be used to deter competition among rivals across different markets and anti-competitive effects

may be understated when overlooking the role of connecting services.

Section 2 describes the institutional background for the Advantage Fares and the AA/USAir

merger. Section 3 describes the empirical analysis, followed by Section 4, in which we introduce a

theoretical model to examine the conditions under which the merger softens price competition via

coordinated effects. Section 5 discusses several important aspects of our approach along with the

relevant policy implications, and finally, Section 6 concludes.

2 Institutional Background

In this section, we discuss the Advantage Fares employed by US Airways and the anticompetitive

concerns around the AA/USAir merger by focusing on the merger’s coordinated effect.

2.1 Advantage Fares

Prior to the AA/USAir merger, USAir had adopted “Advantage Fares,” a strategy that provided

cheap connecting services by undercutting other legacy carrier’s nonstop fares, and its main target

was price-sensitive passengers making last-minute bookings. This pricing strategy by USAir was

considered outside an industry norm in which legacy carriers respect the pricing of other legacy nonstop

carrier by offering connecting services at approximately the same price as the rival’s nonstop service.

USAir did not follow the industry norm and adopted this aggressive discounting strategy, which

is often called a cross-market initiative, largely because nonstop traffic at its hub airports was less

lucrative, and it needed to increase its revenue stream (Department of Justice. (2013)).

Figure 1 shows an actual example of Advantage Fares and how the response of other legacy carriers

for a last-minute booking. Figure 1a, for example, shows the price listing of a route from Miami to

Cincinnati one day before the departure date in August 2013. In this route where AA is the only

nonstop carrier, USAir undercut AA’s nonstop fare substantially with its connecting service, whereas

5

(a) Miami to Cincinnati

(b) Charlotte to Syracuse

Note: The screenshots above are taken from Department of Justice. (2013) on the AA/USAir merger.

Figure 1: Connecting Flights on August 13, 2013 (screenshot taken on August 12, 2013)

the prices of connecting services provided by DL and UA are similar to the nonstop fare. Other legacy

carriers responded to the USAir’s Advantage Fares by setting their connecting service prices low in

routes where USAir offered nonstop service. Figure 1b shows that DL and UA offered connecting

services at a price that substantially undercut USAir’s nonstop fare ($685) for a route from Charlotte

to Syracuse.

2.2 AA/USAir Merger and Elimination of Advantage Fares

One of the main anticompetitive concerns in the AA/USAir merger was that the merger would elim-

inate the Advantage Fares employed by USAir, leading to a change in the postmerger competitive

environment. While this merger had unilateral effects in routes where AA and USAir were competing

head-to-head on nonstop services, the merger effects were not directly associated with USAir’s mav-

erick behavior; concerns were more related to coordinated effects in which coordinated conduct among

nonmerging and merging carriers could be facilitated postmerger after the merging entities removed

the disruptive discount program.

To better understand the effects, Figure 2 keeps track of connecting flight prices over time, where

the vertical gray line indicates the date at which the AA/USAir merger was completed. The left panel

keeps track of the mean of the 90th quantile of connecting flight prices by carrier in routes in which

6

Routes where either AA, DL, or UA is nonstop (solid line) Routes where USAir is nonstop (dashed line)

2012 2014 2016 2018 2020 2012 2014 2016 2018 2020

5.6

5.8

6.0

Log(

90th

Qua

ntile

Con

nect

ing

Flig

ht P

rice)

Connecting Carrier AA/USAir Delta or United Other

Figure 2: Connecting flights

AA, DL, or UA was the only consistent nonstop carrier prior to the merger (hereinafter, Major3

nonstop routes).3 We use the 90th quantile of connecting ticket prices of a carrier for a route because

connecting tickets sold at the last minutes tend to be in the highest price range of all connecting

tickets that are purchased. In the figure, the 90th quantile connecting prices offered by USAir in the

Major3 nonstop routes (green solid line) are roughly 20% cheaper than those offered by DL or UA (red

solid line) for the same route group before the merger.4 It is worth noting that this is a descriptive

figure that does not control product- or route-specific characteristics, such as distance flown, that

could be reflected in the price gap between the two groups. However, after the merger, the connecting

flight prices tend to increase and converge. This postmerger price increase appears to be uniquely

related to the legacy carriers, if we compare the two groups (red and green lines) with the connecting

prices offered by other carriers (including Southwest, JetBlue, Alaska) in the Major3 nonstop routes,

marked with the blue solid line.

We also examine the extent to which the connecting flight prices offered by DL or UA, i.e.,

nonmerging legacy carriers, have evolved for different route groups. The right panel of Figure 2

indicates that premerger, the mean of the 90th quantile connecting flight prices by DL or UA in

USAir nonstop routes (red dashed line), routes in which USAir was the only consistent nonstop

carrier prior to the AA/USAir merger, was substantially lower than that by the same carriers in

3Note that the set of routes in the route group is fixed in the entire sample.4We group AA and USAir together to keep track of their prices over the entire period, because we are not able to

see only USAir’s prices postmerger.

7

the Major3 nonstop routes (red solid line). Postmerger, however, the two lines tend to increase and

converge. Additionally, while the connecting flight prices offered by other nonmerging carriers in

USAir nonstop routes (i.e., blue dashed line) tend to increase, the price increase is somewhat mild

compared to that of DL and UA’s connecting flight prices in the same group. This may indicate that

the merger softened competition by allowing nonmerging legacy carriers to compete less aggressively

against USAir.

Motivated by Figure 2, we further analyze the empirical patterns by performing a retrospective

merger analysis using a difference-in-differences regression approach. We find that our regression

results agree with the patterns we see in Figure 2 that nonmerging legacy carriers (DL and UA),

premerger, set more aggressive connecting prices and serve more passengers in USAir nonstop routes

than in Major3 nonstop routes. However, their prices and the level at which they serve passengers in

the two groups of routes converge postmerger at a higher price level and a lower passenger level. It

is worth noting that while other nonlegacy carriers do not seem to have this distinct pattern in the

two route groups around the merger, we find that Southwest’s price pattern is similar to non-merging

legacy carriers, which is in line with the 2015 lawsuit in which Southwest was alleged to limit the

available seats and increase ticket prices with the three legacy carriers (Stevens (2018)).

3 Empirical Analysis

In this section, we document the distinct connecting price patterns of nonmerging legacy carriers (DL

and UA) in USAir nonstop routes and Major3 nonstop routes around the time of the AA/USAir

merger. Additionally, we look at the connecting prices of different carrier groups in routes where

either DL or UA offers nonstop service.

3.1 Data

For this analysis, we mainly use the Airline Origin and Destination Survey (DB1B), a publicly available

dataset from the U.S. Department of Transportation. The DB1B contains a 10% sample of all air travel

passenger itineraries in the U.S. domestic airline industry. This quarterly dataset includes information

on the origin, destination, and connecting (if an itinerary has multiple connections) airports, ticket

prices, the number of passengers, flight distance, and the carriers that ticket and operate the itinerary.

Additionally, we use the Air Carrier Statistics (T-100) that contain monthly flight level information

on the numbers of flights, available seats, and passengers served by carriers given a route. We match

DB1B and T-100 to compute the flight frequency of nonstop flights. When matching, the regional

8

affiliates shown in T-100 are converted to their affiliated ticketing carriers in DB1B.

Following the literature (Ciliberto and Williams (2014); Li et al. (2021)), we define an airline market

as a directional airport pair. This implies that one direction of an airport pair market is different from

the opposite direction of the same pair market. Our dataset spans from the first quarter of 2011 to the

last quarter of 2019, which reasonably captures airline products and markets before and after the 2013

AA/USAir merger. We drop itineraries whose prices are below $12.5 or higher than $1,250, as they

are likely coding errors. In regard to itineraries including connections, we consider those with up to

one connection because those with multiple connections are rare in the data (less than 1% of total U.S.

domestic passengers). However, because it is a common practice for carriers to offer multiple itinerary

options in a market via different connecting airports (e.g., US Airways’ connecting flight from Boston

to Miami via Washington D.C. or via Philadelphia), we group any multiple itineraries offered by the

same carrier in a market into a single connecting product because the prices of these itineraries are

similar and our focus is on carrier’s overall connecting traffic in a route around the time of the merger

rather than on the carrier’s connecting traffic substitution among its individual hub airports.

Route Group We divide routes into several groups to see the extent to which ticket prices are

different in routes with a different nonstop monopolist. Let k be a carrier group and let route m be k’s

nonstop route if one of the carrier members in k is the only carrier who offered at least daily nonstop

flights in route m for twelve consecutive quarters before the AA/USAir merger. For example, the

route from Philadelphia (PHL) to Austin (AUS) is a USAir nonstop route because US Airways is the

only nonstop carrier from 2011Q1 to 2013Q4 with more than one flight a day, while other carriers in

the route either only partially provided nonstop flights or offered connecting services only. Similarly,

route m is a Major3 nonstop route if the only nonstop carrier in the route is one of AA, DL, or UA

and a Southwest nonstop route if the only nonstop carrier is Southwest. Last, route m is an Others

nonstop route if the only nonstop carrier in m is one other than the Major3, US Airways or Southwest.

Carriers in this group are mostly low-cost carriers, such as JetBlue, Frontier, Sprint, Virgin America,

and Alaska Airlines.

It is worth noting that the AA/USAir merger integrated AA and USAir into a single carrier at

the onset of the first quarter of 2014. However, since we classify the route group based on consistent

nonstop service offered before the AA/USAir merger, we can keep track of the extent to which the

merger led to distinct price changes among nonmerging legacy carriers, DL and UA, in USAir nonstop

routes relative to other route groups (e.g., Major3 nonstop routes). There are 442 markets in USAir

nonstop routes, and most of these markets include USAir’s hub airports as end points (e.g. Charlotte

(CLT); Philadelphia (PHL); Phoenix (PHX); and Washington Reagan National (DCA)).

9

Table 1: Summary Statistics of Connecting Flights Offered By Delta or United

Whose Nonstop Routes?

Variable Statistics Major3 USAir Southwest Others

Pre-Merger (2011Q1-2013Q4)Mean 619.921 1188.245 1116.991 1519.340

N. PassengersStd. Dev. 629.978 1245.397 1103.336 1692.718

Mean 274.517 196.860 191.651 215.402Ticket Price (U.S. dollar)

Std. Dev. 68.028 47.140 35.511 49.206

Mean 1.482 1.317 1.384 1.940Distance (1,000 miles)

Std. Dev. 0.587 0.716 0.534 0.716

Observations - 17,187 4,245 7,531 2,213

Postmerger (2014Q1-2019Q4)Mean 747.657 976.460 921.549 1498.079

N. PassengersStd. Dev. 743.199 1110.559 823.338 1448.903

Mean 276.372 233.788 230.011 233.189Ticket Price (U.S. dollar)

Std. Dev. 69.353 49.998 46.419 54.267

Mean 1.476 1.396 1.310 1.860Distance (1,000 miles)

Std. Dev. 0.594 0.753 0.522 0.719

Observations - 37,325 7,820 14,638 4,503

Note: ‘Major3’ column refers to Major3 nonstop routes — a set of routes in which one of three legacy carriers,AA, DL, and UA, was the only carrier offering at least daily nonstop service from 2011Q1 to 2013Q4. Analo-gously, the ‘USAir’, ‘Southwest’ and ‘Others’ columns refer to USAir nonstop routes, Southwest nonstop routes,and Others nonstop routes, respectively.

Table 1 shows the summary statistics of connecting flights offered by DL or UA, nonmerging legacy

carriers, in the different types of nonstop route groups. The table indicates that the average number

of connecting passengers served by DL or UA premerger is 620 in the Major3 nonstop routes, which

is roughly half of the number served in the USAir nonstop routes and Southwest nonstop routes,

or less than half of those served in the Others nonstop routes. After the AA/USAir merger, DL’s

or UA’s connecting passenger level, on average, increased to 747 in the Major3 nonstop routes but

decreased to 976 and 921 in the USAir nonstop routess and Southwest nonstop routes, respectively. In

terms of connecting service prices, the average premerger price is the highest in the Major3 nonstop

routes ($274), followed by that in the Others nonstop routes ($215), USAir nonstop routes ($196),

and Southwest nonstop routes ($191). Whereas the average prices of the nonmerging legacy carriers

increase postmerger in routes where USAir, Southwest, or Others is the only nonstop carrier, the price

tends to stay the same postmerger in Major3 nonstop routes. The average distance of a connecting

10

Table 2: Summary Statistics of Connecting Flights in Delta or United’s Nonstop Routes

Connecting Service Carriers

Variable Statistics DL or UA AA or USAir Southwest Others

Pre-Merger (2011Q1-2013Q4)Mean 592.985 1014.389 1593.642 907.349

N. PassengersStd. Dev. 470.784 931.808 1133.845 639.404

Mean 254.917 244.468 215.658 202.724Ticket Price (U.S. dollar)

Std. Dev. 56.242 43.223 34.694 35.001

Mean 1.501 1.322 1.347 1.642Distance (1,000 miles)

Std. Dev. 0.598 0.626 0.532 0.504

Observations - 4,908 10,368 3,144 1,128

Postmerger (2014Q1-2019Q4)Mean 896.361 1581.530 1525.540 797.339

N. PassengersStd. Dev. 737.641 1307.400 1099.507 698.830

Mean 255.825 250.482 217.024 177.217Ticket Price (U.S. dollar)

Std. Dev. 48.232 42.160 34.573 49.197

Mean 1.545 1.623 1.365 1.598Distance (1,000 miles)

Std. Dev. 0.595 0.554 0.517 0.524

Observations - 9,637 7,207 6,170 1,819

Note: Each column refers to the group of connecting flight services offered by the carrier in the column name in a non-merging legacy carrier’s nonstop routes.

flight is the highest in the Others nonstop routes across all time periods, but the distance in the

remaining route groups looks similar, ranging from 1,310 miles to 1,480 miles.

Table 2 shows the summary statistics for the connecting flight services offered by any carriers in

DL’s or UA’s nonstop routes. In those routes, the average connecting ticket prices are the highest for

the nonmerging legacy carriers and the lowest for other carriers (e.g., low-cost carriers). The price for

the merging carriers (AA or USAir) is $244 premerger, and increases to $250 postmerger, whereas

the other carriers’ prices remain the same or decrease. The merger led to an increase in the average

number of passengers for AA or USAir in the routes by approximately 50%, which partly reflects that

the connecting passengers using the flight services of the two merging carriers were aggregated in the

transition time period immediately after the merger was completed. The samples shown in Table 1

and 2 are used to examine the AA/USAir merger’s coordinated effects.

11

3.2 Econometrics Methods

3.2.1 Connecting Flights Offered by Delta or United

To examine whether the AA/USAir merger led to heterogeneous changes in the connecting flight ticket

prices and passenger shares of nonmerging legacy carriers across different route groups, we employ a

simple difference-in-differences regression analysis. Conditional on those connecting flights offered by

DL or UA in four nonstop route groups (Major3, USAir, Southwest, and Others nonstop routes), we

run the following regression:

yimt =β11{Postmerger}t +∑g∈G

β2,g1{Nonstop Route: g}m

+∑g∈G

β3,g1{Postmerger}t × 1{Nonstop Route: g}m

+Ximtγ + τq + ηm + εimt, (1)

where subscript i is the carrier, m is the market, and t is time. 1{Nonstop Route: g}m is a dummy

variable for carrier group g ∈ G = {USAir,Major3, Southwest,Others}, which takes one if route m

is g’s nonstop route and 0 otherwise. We use the log transformed 90th quantile ticket prices as a main

variable for y because connecting tickets sold at the last minute tend to be in the highest price range

of all purchased connecting tickets.

Premerger, if the nonmerging legacy carriers set more aggressive prices on USAir nonstop routes

in response to USAir’s Advantage Fares, their connecting prices in USAir nonstop routes will be

sufficiently different from those in Major3 nonstop routes after controlling for product- and route-

specific characteristics. β2,g will capture the baseline differences premerger. If the AA/USAir merger

facilitates collusive behaviors among legacy carriers due to the elimination of the Advantage Fares, we

would expect DL or UA to increase its prices in USAir nonstop routes, and the β3,g in the interaction

term between postmerger and nonstop route dummies will capture this effect.

Ximt indicates observable product characteristics, including travel distance and airport presence.5

Additionally, Ximt includes variables associated with market structures such as the number of nonstop

carriers and the number of low-cost legacy carriers, to capture the changes in the postmerger market

structure of those routes that were predefined based on the premerger market structure. We include

quarter fixed effects τq (q ∈ {Q1, Q2, Q3, Q4}), which control for seasonal variation. We also include

5Airport presence of a carrier at an airport is defined as the fraction of nonstop destinations offered by the carrier tothe nonstop destinations offered by all carriers at the airport.

12

Table 3: Regression Result: Connecting Prices and Passengers from Delta or United

Sample: connecting flights offered by Delta or Unitedlog(90th price) log(passengers)

(1) (2) (3) (4) (5) (6)

1{Postmerger} −0.048∗∗∗ −0.007 −0.050∗∗∗ −0.015 0.291∗∗∗ 0.246∗∗∗

(0.006) (0.007) (0.008) (0.010) (0.024) (0.027)

1{NonstopRoute : Others} −0.285∗∗∗ −0.271∗∗∗ −0.211∗∗∗ −0.207∗∗∗ 0.110 0.097(0.018) (0.017) (0.034) (0.036) (0.092) (0.097)

1{NonstopRoute : USAir} −0.283∗∗∗ −0.280∗∗∗ −0.233∗∗∗ −0.234∗∗∗ 0.455∗∗∗ 0.458∗∗∗

(0.030) (0.032) (0.031) (0.034) (0.082) (0.090)

1{NonstopRoute : Southwest} −0.294∗∗∗ −0.288∗∗∗ −0.238∗∗∗ −0.238∗∗∗ 0.129∗ 0.098(0.018) (0.018) (0.023) (0.023) (0.072) (0.079)

1{Postmerger} × 1{NonstopRoute : Others} 0.149∗∗∗ 0.137∗∗∗ 0.140∗∗∗ 0.143∗∗∗ −0.121∗ −0.050(0.018) (0.020) (0.032) (0.038) (0.073) (0.092)

1{Postmerger} × 1{NonstopRoute : USAir} 0.245∗∗∗ 0.286∗∗∗ 0.201∗∗∗ 0.248∗∗∗ −0.578∗∗∗ −0.619∗∗∗

(0.022) (0.027) (0.029) (0.037) (0.053) (0.063)

1{Postmerger} × 1{NonstopRoute : Southwest} 0.245∗∗∗ 0.264∗∗∗ 0.181∗∗∗ 0.201∗∗∗ −0.365∗∗∗ −0.391∗∗∗

(0.011) (0.012) (0.015) (0.017) (0.056) (0.059)

Balanced? N N Y Y Y Y2014-2015 Excluded? N Y N Y N YObservations 74,337 57,032 24,226 18,043 24,226 18,043R2 0.392 0.430 0.315 0.357 0.289 0.310

∗p<0.1; ∗∗p<0.05; ∗∗∗p<0.01

Note: This table shows the regression result of relevant variables when the sample is restricted to those connecting flights offered by DL or UA.The omitted reference group is Major3 nonstop routes. ‘Balanced’ indicates whether the sample includes only those connecting products sur-vived in the entire sample period. ‘2014-2015 Excluded?’ is whether the sample excludes two years of data immediately following the merger.The full regression result can be found in Table A1 in Appendix A.

a market fixed effect ηm to absorb market-specific unobservable characteristics. εimt indicates the

idiosyncratic error term. Last, we exclude any connecting services of a carrier who is also the nonstop

monopolist in a route to rule out the possibility that it sets higher connecting prices to steer passengers

to buy its nonstop service. For example, Delta’s connecting flights in Delta nonstop routes are not

included in the sample.

Table 3 presents the regression results from Equation (1). The coefficients in column (1) indicate

that premerger the 90th quantile prices of the nonmerging legacy carriers in Major3 nonstop routes,

the baseline route group, is 32.7 percent (because exp(0.283)− 1 = 0.327) higher than those in USAir

nonstop routes. However, after merging, their prices in USAir nonstop routes increase by 27.7 percent

(relative to the baseline), placing the connecting service prices in both route groups at a similar level.

This pattern of increase in connecting prices (relative to those in Major3 nonstop routes) is also

shown in Southwest and Other nonstop routes, although the relative price increase is much smaller

in Other nonstop routes. The results for the price regression are essentially unchanged under various

regression specifications. Column (2) excludes the two years of data immediately following the merger,

13

a transition time period in which the merging entities integrated their systems. Column (3) shows the

results when the sample includes only those connecting products that survived over the entire sample

period, which may address the concern that carrier entry/exit could drive the regression result. Last,

Column (4) combines the two restrictions in columns (2) and (3) together.

The change in connecting flight price patterns is negatively correlated with passenger level. Columns

(5) and (6) show the regression results when the dependent variable is the log transformed number

of passengers. The coefficients in those columns indicate that DL or UA carry, on average, 57.6

percent more connecting passengers in the USAir nonstop routes than in the Major3 nonstop routes.

Additionally, they seem to carry more connecting passengers in the Southwest and Others nonstop

routes, but the magnitude is relatively low and statistically insignificant. After the merger, however,

the average level of those connecting passengers dropped significantly in USAir nonstop routes, even

lower than those in Major3 nonstop routes (11.6 percent lower exp(0.455− 0.578)− 1 = 0.116). While

this pattern seems to hold for Southwest nonstop routes, there is not as much change in the level of

nonmerging legacy carrier connecting passengers in Others nonstop routes after the merger. The full

regression results can be found in Table A1 in Appendix A.

3.2.2 Any Connecting Flights in Delta or United’s Nonstop Routes

Next, we examine the extent to which the connecting prices of different carrier groups evolve over time

in Delta’s or United nonstop routes. For this, we restrict our sample to any connecting flights in those

routes in which DL or UA was the only nonstop carrier prior to the AA/USAir merger. For carrier i

in market m at time t, the regression equation is as follows:

yimt =β11{Postmerger}t +∑g∈G

β2,g1{Carrier: g}i

+∑g∈G

β3,g1{Postmerger}t × 1{Carrier: g}i

+Ximtγ + τq + ηm + εimt, (2)

where the notations follow those of Equation (1), by replacing 1{Nonstop Route: g}m with 1{Carrier: g}i,

an indicator function taking 1 if connecting service provider i is from one of the following four carrier

groups—i) DL or UA; ii) AA or USAir; iii) Southwest; or iv) Others.

Table 4 reports the regression results when the sample includes all connecting flights offered by

different carriers in Nonmerging legacy nonstop routes. The dummy for DL or UA is omitted and

served as the reference group. The results indicate that prior to the AA/USAir merger, the connecting

14

Table 4: Regression Result: Connecting Prices and Passengers in Delta or United’s Nonstop Routes

Sample: all connecting flights in Delta or United’s nonstop routeslog(90th price) log(passengers)

(1) (2) (3) (4) (5) (6)

1{Postmerger} −0.063∗∗∗ −0.029∗∗∗ −0.065∗∗∗ −0.035∗∗∗ 0.352∗∗∗ 0.308∗∗∗

(0.007) (0.008) (0.010) (0.012) (0.031) (0.030)

1{Carrier : AAorUSAir} −0.104∗∗∗ −0.106∗∗∗ −0.105∗∗∗ −0.106∗∗∗ 1.166∗∗∗ 1.169∗∗∗

(0.007) (0.007) (0.012) (0.012) (0.047) (0.047)

1{Carrier : Others} −0.398∗∗∗ −0.398∗∗∗ −0.392∗∗∗ −0.392∗∗∗ 0.596∗∗∗ 0.596∗∗∗

(0.014) (0.014) (0.020) (0.020) (0.067) (0.068)

1{Carrier : Southwest} −0.310∗∗∗ −0.307∗∗∗ −0.318∗∗∗ −0.320∗∗∗ 1.007∗∗∗ 0.987∗∗∗

(0.012) (0.012) (0.017) (0.018) (0.050) (0.048)

1{Postmerger} × 1{Carrier : AAorUSAir} 0.066∗∗∗ 0.095∗∗∗ 0.084∗∗∗ 0.111∗∗∗ −0.446∗∗∗ −0.618∗∗∗

(0.007) (0.008) (0.012) (0.013) (0.045) (0.046)

1{Postmerger} × 1{Carrier : Others} −0.099∗∗∗ −0.159∗∗∗ −0.081∗∗∗ −0.134∗∗∗ −0.636∗∗∗ −0.685∗∗∗

(0.015) (0.017) (0.018) (0.020) (0.053) (0.061)

1{Postmerger} × 1{Carrier : Southwest} 0.081∗∗∗ 0.065∗∗∗ 0.092∗∗∗ 0.082∗∗∗ −0.400∗∗∗ −0.402∗∗∗

(0.009) (0.010) (0.014) (0.016) (0.093) (0.091)

Balanced? N N Y Y Y Y2014-2015 Excluded? N Y N Y N YObservations 77,600 60,872 44,726 35,223 44,726 35,223R2 0.420 0.452 0.410 0.445 0.361 0.370

∗p<0.1; ∗∗p<0.05; ∗∗∗p<0.01

Note: This table shows the regression result of relevant variables when the sample is restricted to those connecting flights offered by DL orUA. The omitted carrier dummy is whether DL or UA. ‘Balanced’ indicates whether the sample includes only those connecting productssurvived in the entire sample period. ‘2014-2015 Excluded?’ is whether the sample excludes two years of data immediately following themerger. The full regression result can be found in Table A2 in Appendix A.

flights offered by DL or UA (baseline dummy) are 9.8% more expensive than those offered by AA or

USAir. Postmerger, however, the merged carrier increased its prices to match the price level of the

connecting prices of nonmerging legacy carriers. A similar pattern can be found for Southwest, even

though its premerger price level is much lower (26.6%) than that of the nonmerging legacy carriers.

On the other hand, other carriers, which are mostly low-cost carriers, further decreased their price

postmerger relative to DL or UA. The price regression in Table 4 is robust to various specifications,

similar to the previous regression results. In terms of passengers levels, Columns (5) and (6) show that

premerger, the number of passengers using AA or USAir or Southwest is more than twice the number

using DL’s or UA’s connecting services, whereas postmerger, their passenger numbers decrease by 50%

to 60%, relative to the baseline.

3.2.3 Discussion and Robustness Check

Southwest and Legacy Carriers In our empirical analysis, we find that the connecting prices of

nonmerging legacy carriers have evolved in a very similar way in both USAir and Southwest nonstop

15

routes (Table 3). In addition, in Table 4, postmerger, both merging carriers and Southwest Airlines

increase their connecting prices (6.6% and 8.1%) relative to the baseline, while other (low-cost) carriers’

prices decrease. These findings raise the natural question of whether Southwest and the three legacy

carriers have formed some sort of coordination that could soften competition. In a 2015 lawsuit, in

fact, it was alleged that Southwest limited the available seats and increased ticket prices with the three

legacy carriers. While the carrier settled with members of a class-action lawsuit in 2018, Southwest

denied that it had any unlawful agreements with AA, DL, and UA (Stevens (2018)).

Robustness Check We perform a series of robustness checks. The first main concern is that

flight service entry/exit around the AA/USAir merger may act as a confounding factor that changes

the price or passenger level. To address this concern, we run the regressions with a balanced panel

(‘Balanced’ in Table 3 and 4), a set of connecting products that survive across the entire sample period,

and the results are robust. Second, there is a possibility that how we define a carrier’s nonstop route

affects the regression results. While we chose our definition which helps identify routes in which there

is only one carrier who persistently offers nonstop services prior to the merger, we vary the threshold

of definition such as 8 or 4 quarters instead of 12 quarters or at least two daily nonstop flights instead

of one. With various definitions, our results are robust, as in Table A3 in Appendix A. Last, there

is a concern that the price we have examined may not represent a general connecting service. To

address this, we run the same regression as (Table 3) by replacing the 90th quantile prices with the

average prices which represent a general ticket price. The regression results are reported in Table

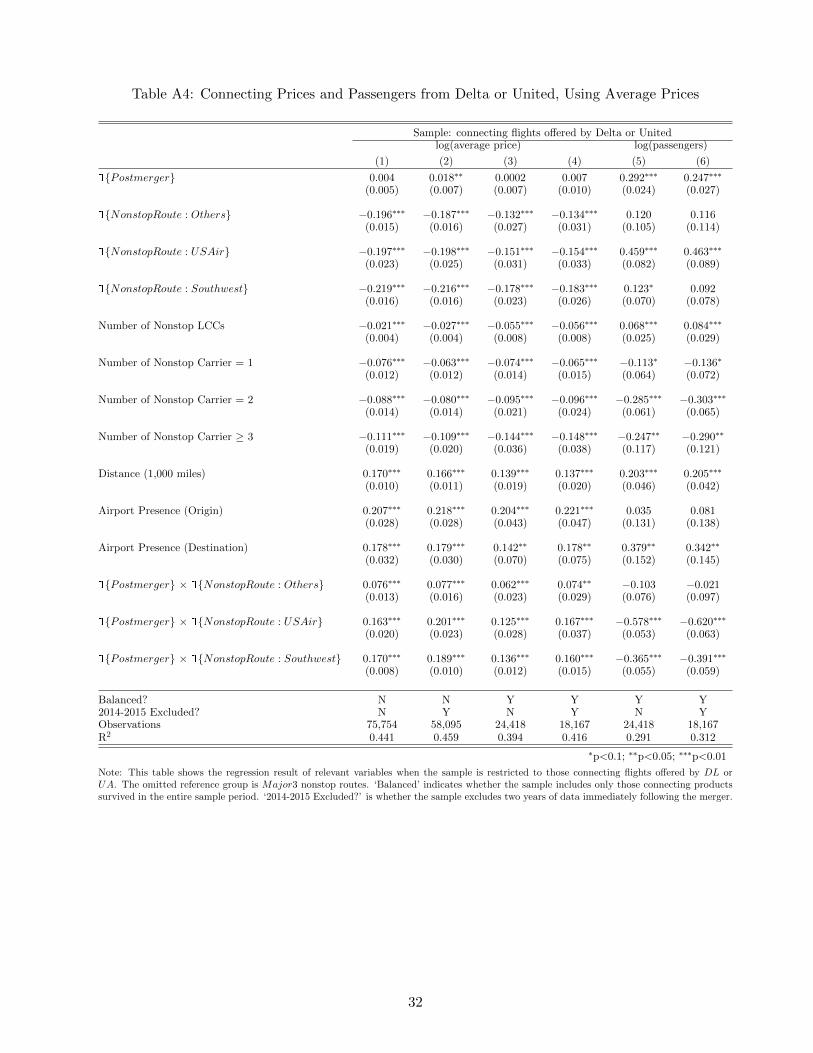

A4 in Appendix A, and they are robust. With these consistent empirical findings, we move on to a

theoretical model that can help us better understand the coordinated effects of the merger.

4 Theoretical Model

In this section, we provide a theoretical model to explain the conditions under which the AA/USAir

merger weakened market competition via coordinated effects.

4.1 Primitives

Airlines A consumer in the unit mass chooses one airline from among three alternatives, denoted

as AA, DL, and USAir, respectively. Thus, the set of alternatives conditional on flying is F =

{AA,DL,USAir}. The net utility arising from the outside option, i.e., not flying, denoted as NF , is

normalized to zero.

Markets There are three different markets, m ∈ M, where M = {1, 2, 3}, in which all three

16

airlines operate. We assume that in each market, one of the airlines serves as a nonstop monopolist,

while the remaining two carriers operate connecting flights. Specifically, we assume that DL in m = 1,

USAir in m = 2, and AA in m = 3 are nonstop monopolists in that market. This market structure

reflects the earlier definition of a carrier’s nonstop routes. We also assume that the three markets

have identical characteristics, such as origin/destination airport size and nonstop distance. Given

these three markets with three airlines setups, we examine how the AA/USAir merger affects the

competitive structure across markets. Specifically, our analysis allows us to see how nonmerging

legacy carriers, such as DL, and merging entities, AA and USAir, change their pricing behaviors

before and after the merger. The market structure is summarized in Figure 3.

Figure 3: The market structure

Consumer Utility Specification Consider each market in which three airlines compete with

each other. The indirect utility of a consumer who takes airline j ∈ F in market m is given as follows.

ujm = δjm + αpjm + γ1CONNjm + ξjm︸ ︷︷ ︸≡Vjm

+(1− σ)εjm, (3)

where 1CONNjm is one if j offers connecting flight service in market m and zero otherwise, and γ ≤

0 captures the disutility obtained by a passenger when taking connecting flights, such as a longer

flight time. α ≤ 0 is the service-specific price sensitivity, pjm is airfare for j in market m, and

δjm captures other observable service characteristics. For notational convenience, Vjm represents the

quality of product j including its price. Additionally, ξjm captures unobservable product quality, which

we normalize to zero for all j in m, and εjm is an independent and identically distributed random

unobserved component of consumer utility, which follows a Type I Extreme Value distribution. The

parameter σ represents the degree of independence in unobserved utility among alternatives within a

nest: the higher the value of σ is, the greater the differentiation between products in the same nest.

That is, 1− σ measures the degree of substitution.

A consumer will choose airline j over k if ujm > ukm ∀ k ∈ F \ j. The choice probability of a

17

consumer choosing airline j in market m ∈M is given as follows.

xjm = Pjm|F ×PF (4)

=exp

(Vjm1−σ

)∑

k∈F exp(Vkm1−σ

) ×[∑

k∈F exp(Vkm1−σ

)]1−σ

1 +[∑

k∈F exp(Vkm1−σ

)]1−σ ,

where Pjm|F is the conditional probability of choosing airline j given that a consumer takes a flight,

and PF is the probability of choosing to fly over not flying.

Airline’s Problem Each airline chooses the optimal price pjm as follows.

maxpjm

∑m∈M

(pjm − cjm)xjm(pm)︸ ︷︷ ︸=πjm

+θjk × 1j,k∈L∑

m∈M,j 6=k(pkm − ckm)xkm(pm)︸ ︷︷ ︸

=πkm

, (5)

where pm is a vector of product prices in market m, and cjm is the marginal cost of operation for airline

j in market m. The profit maximization problem first reflects multimarket business strategies. To

emphasize on airline’s strategic choices in multimarket, we allow each airline to maximize its aggregate

profit across markets. That is, airline j chooses pj1, pj2, and pj3 by solving maxpj1,pj2,pj3 πj1+πj2+πj3:

this profit maximization allows airline j to cross-subsidize across markets.

Additionally, we consider a conduct parameter, θjk ∈ [0, 1] for j 6= k, where θjk = θkj , to capture

the degree of coordination among carriers j and k (Bresnahan (1982); Berheim and Whinston (1990);

Ciliberto and Williams (2014); Miller and Weinberg (2017)). If θ is one, it implies perfect coordination,

such that airline j sets pjm by fully internalizing the prices of any relevant rival airlines, whereas θ = 0

indicates that the market returns to a competitive structure without direct coordination. If θ ∈ (0, 1),

firms partially internalize their price externalities. The indicator function, 1j,k∈L, is one if airlines j

and k are AA or DL (i.e., L = {AA,DL}). For notational simplicity, we denote θAA,DL = θDL,AA ≡ θ.

The aforementioned cross-market initiatives among legacy carriers can be described in the model

by a positive conduct parameter between AA and DL, θAA,DL > 0. However, given that USAir’s

Advantage Fares pose a considerable competitive threat, those carriers may not be able to engage

in stable collusive conduct with USAir. Thus, we assume that, as a baseline, there is no collusive

conduct between legacy and maverick carriers, which means that θAA,USAir = θDL,USAir = 0.

Merger Analysis We assume that AA is merged with USAir, whileDL remains an independent

airline. Postmerger, the merged entity maximizes the joint profit of AA and USAir in each market.

We do not endogenize AA’s decision on whether to merge with any rival airline because we place more

emphasis on how the merger between legacy and maverick carriers affects the market’s competitive

18

structure, especially through its impact on nonmerging entity DL, taking the merger between AA and

USAir as given.

As shown in Sections 2.2 and 3, before the AA/USAir merger, major legacy carriers set relatively

low connecting airfares, thereby capturing a greater market share, in USAir nonstop routes, compared

to their prices in the Major3 nonstop routes. However, after the merger, this discrepancy in legacy

carriers’ relative pricing strategies disappeared, such that their connecting price ratios to USAir’s

nonstop service are no longer lower than those to other legacy carriers’ nonstop service. In this

finding, our concern is whether the AA/USAir merger, a merger with a maverick firm, eliminates

intense competition in USAir nonstop routes. In particular, our focus is on the effects of mergers on

nonmerging entities’ pricing strategies, namely, the coordinated effects of mergers.

4.2 Equilibrium

Given the choice probability in Equation (3), each airline j chooses the optimal pjm by solving Equation

(5). As mentioned earlier, our setup views any changes in postmerger competitive structure, followed

by changes in pricing strategies, as resulting from the elimination of the maverick firm. To investigate

the extent to which nonmerging carriers change their connecting flight prices and passenger shares

in different groups of routes over time, we focus on how DL’s pricing strategies change postmerger.

Specifically, in Section 4.2.1, we first focus on markets in which DL offers connecting service while

competing with either USAir as the maverick nonstop monopolist or AA as the legacy nonstop

monopolist. In Section 4.2.2, we focus on the market in which DL is the nonstop monopolist and other

carriers offer connecting flights. Note that both DL and UA are classified as the same nonmerging

legacy carriers; for the sake of discussion, we focus on the effect of the merger on DL below.

4.2.1 Connecting Flights Offered by Delta

To see general effects of maverick firm-driven intense competition on nonmerging entity DL as a

connecting carrier, we focus on markets 2 and 3, in which USAir and AA are nonstop monopolists,

respectively. We compare the price ratio of DL’s connecting to AA’s nonstop service in m = 3 with

the ratio of DL’s connecting to USAir’s nonstop in m = 2, in order to investigate whether DL as

a nonintegrated entity also competes less aggressively against USAir in terms of pricing after the

AA/USAir merger. If so, this suggests that the competition-reducing effects of the merger become

prevalent for all players in the markets, implying coordinated effects.

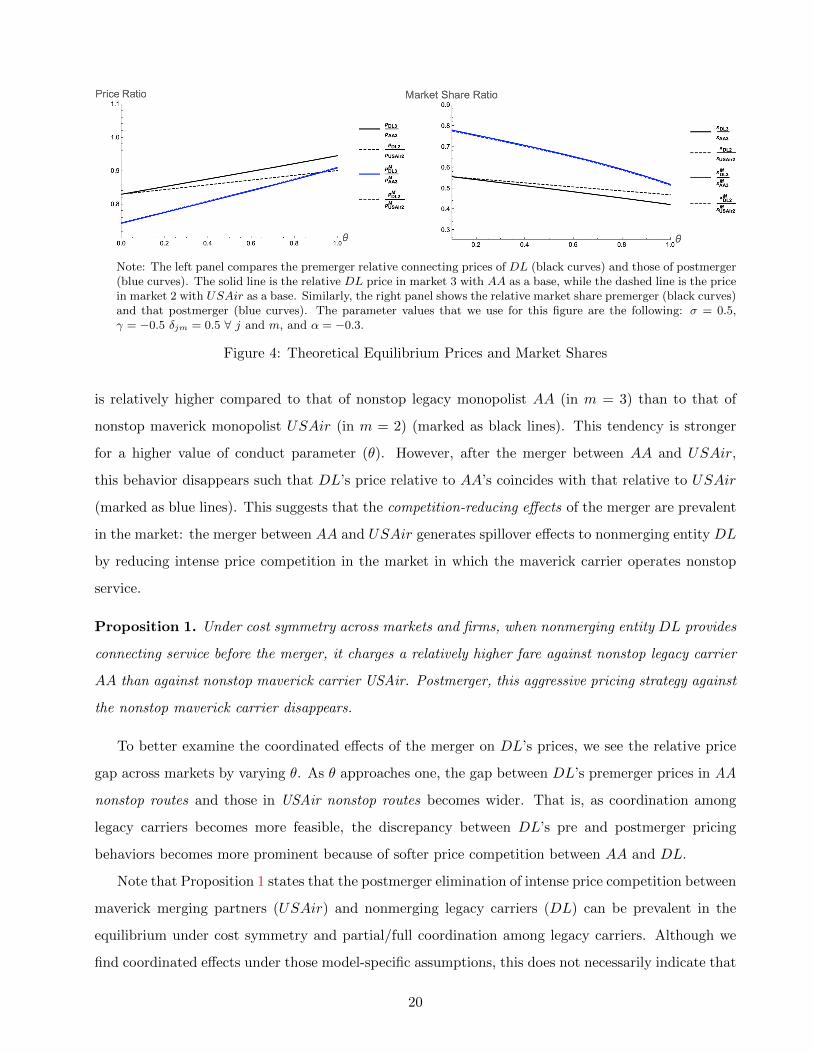

As depicted in the left panel of Figure 4, premerger, DL as a connecting carrier sets a fare that

19

Note: The left panel compares the premerger relative connecting prices of DL (black curves) and those of postmerger(blue curves). The solid line is the relative DL price in market 3 with AA as a base, while the dashed line is the pricein market 2 with USAir as a base. Similarly, the right panel shows the relative market share premerger (black curves)and that postmerger (blue curves). The parameter values that we use for this figure are the following: σ = 0.5,γ = −0.5 δjm = 0.5 ∀ j and m, and α = −0.3.

Figure 4: Theoretical Equilibrium Prices and Market Shares

is relatively higher compared to that of nonstop legacy monopolist AA (in m = 3) than to that of

nonstop maverick monopolist USAir (in m = 2) (marked as black lines). This tendency is stronger

for a higher value of conduct parameter (θ). However, after the merger between AA and USAir,

this behavior disappears such that DL’s price relative to AA’s coincides with that relative to USAir

(marked as blue lines). This suggests that the competition-reducing effects of the merger are prevalent

in the market: the merger between AA and USAir generates spillover effects to nonmerging entity DL

by reducing intense price competition in the market in which the maverick carrier operates nonstop

service.

Proposition 1. Under cost symmetry across markets and firms, when nonmerging entity DL provides

connecting service before the merger, it charges a relatively higher fare against nonstop legacy carrier

AA than against nonstop maverick carrier USAir. Postmerger, this aggressive pricing strategy against

the nonstop maverick carrier disappears.

To better examine the coordinated effects of the merger on DL’s prices, we see the relative price

gap across markets by varying θ. As θ approaches one, the gap between DL’s premerger prices in AA

nonstop routes and those in USAir nonstop routes becomes wider. That is, as coordination among

legacy carriers becomes more feasible, the discrepancy between DL’s pre and postmerger pricing

behaviors becomes more prominent because of softer price competition between AA and DL.

Note that Proposition 1 states that the postmerger elimination of intense price competition between

maverick merging partners (USAir) and nonmerging legacy carriers (DL) can be prevalent in the

equilibrium under cost symmetry and partial/full coordination among legacy carriers. Although we

find coordinated effects under those model-specific assumptions, this does not necessarily indicate that

20

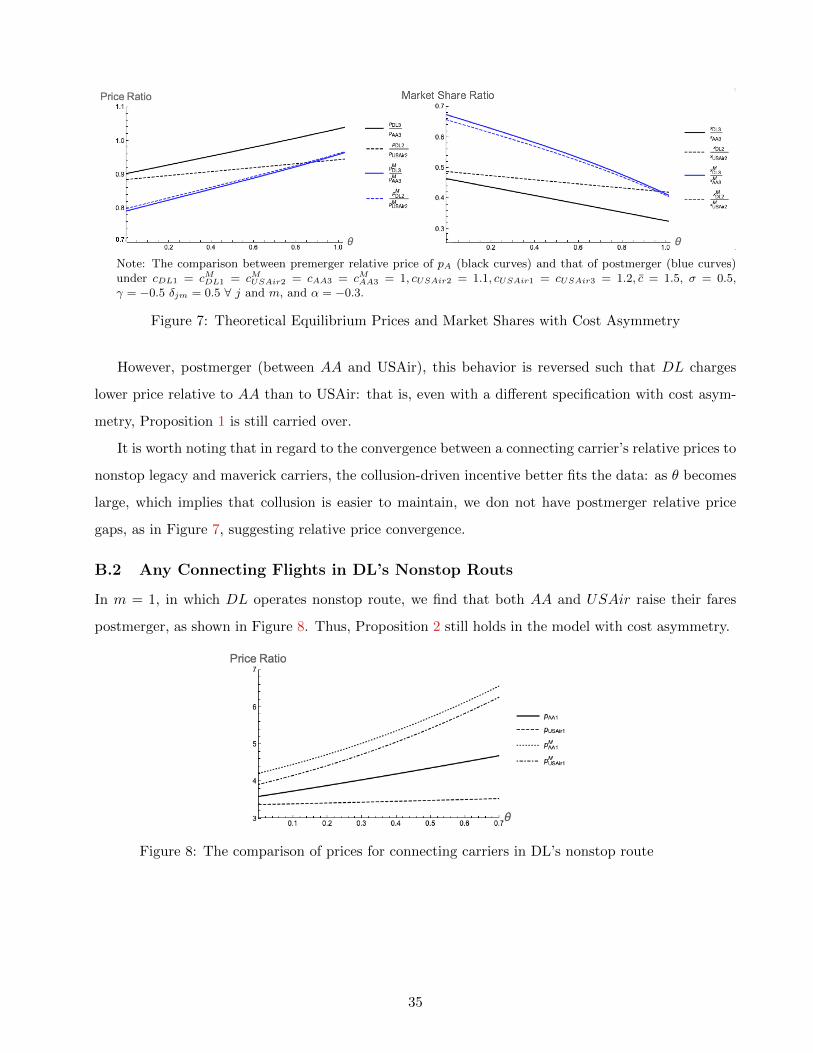

the main result is sensitive to the particular way the market is modeled. Indeed, the model with cost

asymmetry between legacy and maverick carriers and/or between nonstop and connecting carriers also

finds such coordinated effects, as shown in Appendix B.

4.2.2 Any Connecting Flights in DL’s Nonstop Routes

Next, we examine how the connecting flights offered by other carriers (i.e., merging entities AA and

USAir) in m = 1 (i.e., DL nonstop routes) are affected by the merger. As Figure 5 shows, both

AA and USAir raise their fares postmerger. This price increase is mostly driven by the unilateral

effects of the merger. Importantly, this suggests that, postmerger, USAir, which had previously been

providing substantial price discounts for connecting routes premerger, is no longer a maverick airline.

Additionally, the gap between pre and postmerger prices becomes wider as θ approaches one. This

implies that as coordination among carriers becomes easier, AA and USAir, as merging entities, tend

to set higher prices, which widens the price gap.

Note: The solid and dashed curves show AA’s and USAir’s premerger prices in m = 1, respectively. The dottedcurve shows their postmerger prices in the same market.

Figure 5: A comparison of prices for connecting carriers in DL’s nonstop routes

Proposition 2. Under cost asymmetry across markets and firms, AA and USAir, as merging entities,

raise prices postmerger in the market in which nonmerging entity DL is the nonstop monopolist

Discussion of conduct parameter θ In Section 4, we focus on the coordinated effects of the

AA/USAir merger by introducing the conduct parameter θ, which reflects the degree of collusion among

legacy carriers. However, it is worth noting that we can find similar coordinated effects from other

specifications. For instance, as shown in Appendix B, the model with cost asymmetry between legacy

and maverick carriers and/or between nonstop and connecting carriers also results in implications

qualitatively similar to those in the main specification. This suggests that our theoretical findings on

21

coordinated effects are robust to different specifications. Additionally, there can be several different,

and potentially complementary, factors driving coordinated effects, such as collusion-driven and cost-

driven.6

4.2.3 Merger with Maverick Carrier vs. Legacy Carrier

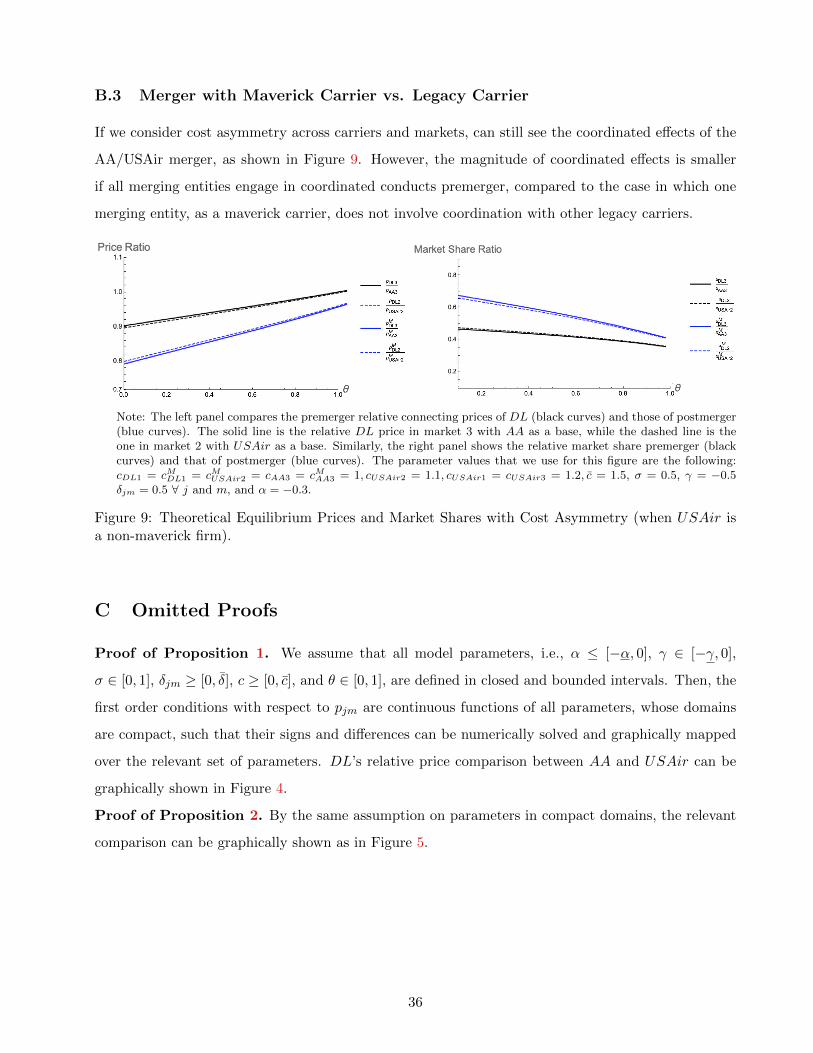

Our main findings show coordinated effects from the AA/USAir merger that are driven by the elim-

ination of maverick carrier USAir’s price innovation, represented by Advantage Fares. Given that

the coordinated effects of mergers can be more salient in the case of a merger involving a maverick

firm, it is worth examining how much this type of merger facilitates postmerger coordinated conduct

compared to a merger between legacy carriers. In the main model, the only difference between legacy

and maverick carriers is the incentive to coordinate: that is, the cross-market initiatives are observ-

able only among legacy carriers, which are reflected by a positive conduct parameter θ. To see how a

merger involving a maverick firm, represented by zero conduct parameter in the relevant profit func-

tions, is different from one involving a non-maverick/legacy firm, represented by a positive conduct

parameter, we compare premerger relative connecting prices of DL with those of postmerger assuming

that there are coordinated conducts between legacy carriers (DL and AA) and USAir. Specifically,

this assumption implies that θAA,USAir = θDL,USAir = θ: all three airlines share the same conduct

parameter.

Note: The left panel compares the premerger relative connecting prices of DL (black curves) and those of postmerger(blue curves). The solid line is the relative DL price in market 3 with AA as a base, while the dashed line is theone in market 2 with USAir as a base. Similarly, the right panel shows the relative market share premerger (blackcurves) and that of postmerger (blue curves). The parameter values that we use for this figure are the following:σ = 0.5, γ = −0.5 δjm = 0.5 ∀ j and m, and α = −0.3.

Figure 6: Theoretical Equilibrium Prices and Market Shares (when USAir is a non-maverick firm).

Unlike in the main finding, as shown in Figure 4, in which USAir is a maverick carrier such that

there is no coordination with other legacy carriers premerger, Figure 6 shows that DL does not price

6However, we do not try to determine what is driving the coordinated effects of mergers because it is beyond thescope of our paper.

22

aggressively in USAir nonstop routes premerger: given that AA and USAir are now symmetric from

DL’s perspective, we do not find merger-driven coordinated effects because the three already engage

in coordinated conduct premerger. This result emphasizes how a merger involving a maverick firm,

which is more likely to lead to coordinated effects, is different from other types of mergers involving

non-disruptive legacy firms.

5 Discussion

In this section, we discuss the potential importance of connecting flights to airline antitrust issues and

the merger remedies imposed in the AA/USAir merger.

5.1 Connecting vs. Nonstop

In the airline industry, while nonstop services are typically effective in constraining rivals’ market

power, connecting flights are considered a poor substitute and that have a limited ability to restrain

rivals from raising prices. For that reason, nonstop flight services in concentrated markets have been

the core elements of analysis in merger reviews in the industry (e.g., routes in which merging carriers are

a nonstop duopoly). However, connecting service options can play a crucial role in market competition

and a careful examination is often required. As documented in this paper, connecting flight services

with a substantial discount (i.e., Advantage Fares) disrupted markets and induced intense competition

across multiple routes. Then, when the AA/USAir merger eliminated the price discounting program,

we witnessed that the market competition originating from those connecting flights became softened.

One might think that only a small number of passengers in a route would be affected by this margin,

but the regression results in Section 3 indicate that postmerger, the number of connecting passengers

of nonmerging legacy carriers, on average, decreased by 50% (or 400 passengers) in USAir nonstop

routes, relative to those in Major3 nonstop routes. In addition, one important factor to consider is the

sheer number of routes and aggregated number of passengers across all affected markets.

Table 5 tabulates the number of markets and passengers in the second quarter of 2013. It shows

that there are, in total, 8,665 markets with 95.2 million passengers, and connecting passengers account

for 25% of the total passengers. When we focus on the set of routes in which AA and USAir are

a nonstop duopoly, these represent only 1.2 million passengers in 24 markets (or 1.26% of the total

passengers). In regard to those routes affected by Advantage Fares, which are routes in which one of

the three legacy carriers offers nonstop service and USAir offers connecting service or vice-versa, there

are approximately 1,700 markets (Group C) with 42.2 million passengers in total. Even if we restrict

23

Table 5: Tabulation of Routes by Market Group in 2013Q2

2013Q2 Passengers (mil.)

Group Category N. Markets Connecting Nonstop Total

A All Markets 8665 23.6 71.6 95.2

B Both AA and USAir Nonstop 24 0.0 1.2 1.2

Major3 NS and USAir Conn 1344 4.9 30.5 35.4CUSAir NS and Major3 Conn 341 1.3 5.4 6.8

Note: This table shows the number of routes and passengers in different types of market groups. ‘All Markets’in Group A indicates the entire market. ‘Both AA and USAir Nonstop’ in Group B refers to the set of routes inwhich American and US Airways are nonstop duopolists. ‘Major3 NS and USAir Conn’ shows the set of routes inwhich one of three major legacy carriers (American, Delta, and United) is the one and only nonstop carrier and USAirways offers connecting services. Similarly, ‘USAir NS and Major3 Conn’ refers to the set of routes in which USAirways is the only nonstop service provider and at least one of the three legacy carriers offers connecting services.

our focus to connecting passengers, 26.3% of the total connecting passengers are in this category. This

implies that potential consumer harm due to the AA/USAir merger in nonstop duopoly routes (Group

B) could be huge in a small number of markets, whereas the harm due to the elimination of Advantage

Fares (Group C) could be small at the route level but considerably large if we aggregate the welfare

losses from all connecting routes and their passengers. This suggests that it is crucial for a merger

control to consider potential consumer harm across a wider range of routes rather than focusing on

a few sets of local routes in airline merger analysis. However, the AA/USAir merger was completed

without addressing the coordinated effects of the merger.

5.2 Merger Remedies

The AA/USAir merger was approved with remedies that mainly addressed the merger’s potential

unilateral effects without considering the specific effect of eliminating a maverick firm or the coordi-

nated effects. Before the trial started, the parties settled through a set of structural remedies that

include requiring merging carriers to divest some of their airport landing slots and gate accesses at

a few slot-controlled airports (e.g., Washington D.C. Reagan National Airport (DCA) and New York

LaGuardia Airport (LGA)) to low-cost carriers (LCCs). Divestitures would allow LCCs to increase

their operating capacity at those airports and mitigate potential consumer harm from merging carri-

ers obtaining greater market power, but they are not designed to block rival carriers from engaging

in collusive conducts (Peterman (2014)). Although the DOJ claimed that the potential benefits of

LCC entry and expansion through divestitures could be comparable to those of the Advantage Fares

(Department of Justice. (2014)), ex post LCC route expansion focused on a limited number of routes

24

based on DCA and LGA.7 Furthermore, as Loertscher and Marx (2021) mentions, asset divestitures as

a merger remedy can raise greater concerns about coordinated effects, although it resolves unilateral

effects.

Our analysis suggests that it is important not to overlook the coordinated effects. If a merger

involving a maverick firm can potentially soften price competition by eliminating disruptive innovation,

such as Advantage Fares, competitive authorities need to take extra care in considering whether to

challenge the merger by quantifying the market harm originating from the acquisition of the maverick

firm. As Horizontal Merger Guidelines (Department of Justice) (2010) notes, if a merger partner

acquires a maverick firm, it can be evidence of the adverse effects of the merger. As we stated earlier,

in the AA/USAir merger, the DOJ’s effort to resolve the merger’s anticompetitive effects did not focus

on the coordinated effects. This could be partly because connecting flights were not crucial aspects of

the airline merger reviews or partly because any remedies that could preserve Advantage Fares would

be costly (e.g., behavioral remedies that force the merged entity to continue to provide Advantage

Fares postmerger may require a high monitoring cost). However, as stated in Section 5.1, the low

consumer harm due to the elimination of Advantage Fares can be substantial when aggregated across

all affected routes; therefore any remedies to address the harm can be rationalized if the aggregated

harm is higher than any costs arising from those remedies. If this is the case, the authorities might take

remedies into account when they do not want to reject the proposed merger but do aim to preserve

disruptive innovation that the maverick firm brings to market.

6 Concluding Remarks

This paper studies the coordinated effects of a merger involving a maverick firm in the context of

the merger between American Airlines (AA) and US Airways (USAir). We find, both theoretically

and empirically, that the merger, which eliminated the Advantage Fares employed by USAir, softens

price competition between the merging and nonmerging carriers. Specifically, nonmerging legacy

carriers (i.e., DL and UA), which had previously set lower prices in USAir’s nonstop monopoly

market premerger, no longer employed such aggressive pricing after the merger. This evidence on a

postmerger price increase for nonmerging entities is supported by a theory of coordinated effects.

Even if it is likely that the elimination of Advantage Fares weakened the market competition

7For example, although divestitures at DCA allowed low-cost carriers to increase their passenger share from 13.7%in 2013 to 24.8% in 2016, the overall passenger growth at the airport was similar to nationwide growth Park (2020). Inregard to entry, low-cost carriers who receive airport slots tend to add leisure-based destinations from DCAs, such asFort Lauderdale and Tampa (Southwest) and Palm Beach (JetBlue).

25

through both unilateral and coordinated effects, less attention has been paid to the latter: although

settlement remedies requiring the divestiture of slots and gates at several airports resolved unilateral

effects, they did not eliminate the anticompetitive harm from coordinated effects. For airline merger

evaluations, in particular, one possible reason for such neglect is that competitive authorities overlook

the importance of connecting flights: given that Advantage Fares only applied to connecting routes,

which are known to be less effective in restricting rivals’ market power, the adverse effects of elim-

inating Advantage Fares following the merger is likely to have underestimated. We emphasize that

the aggregate effects of connecting services, if summed over all markets, are likely to have a signifi-

cant impact on market competition, which is a subject deserving more attention. In this regard, we

primarily focus on the effects of mergers on connecting routes and find substantial price increases of

nonmerging carriers, which are likely to be driven by the Advantage Fares.

Overall, our findings offer evidence supporting the coordinated effects of mergers. In particular,

when a market is more vulnerable to coordinated conduct, such as the airline industry with its price

transparency, coordination among firms is likely to exist even premerger. In this case, postmerger

coordination is rather obvious, and it thus requires more careful merger reviews. Furthermore, if a

proposed merger involves a maverick firm, competitive authorities may need to examine more closely.

Although a maverick firm may only take up a small part of the market and thus seem to have a

negligible impact, its aggregate effect may be significant when we consider the competition-enhancing

effects arising from its disruptive role.

References

Aryal, G., Ciliberto, F., and Leyden, B. T. (2020). Coordinated Capacity Reductions and Public

Communication in the Airline Industry. Working Paper.

Ashenfelter, O., Hosken, D., and Weinberg, M. (2014). Did robert bork understate the competitive

impact of mergers? evidence from consummated mergers. The Journal of Law and Economics,

57(S3):S67–S100.

Berheim, B. and Whinston, M. (1990). Multimarket contact and collusive behavior. The RAND

Journal of Economics, pages 1–26.

Berry, S. and Jia, P. (2010). Tracing the Woes: An Empirical Analysis of the Airline Industry.

American Economic Journal: Microeconomics, 2(3):1–43.

26

Bjornerstedt, J. and Verboven, F. (2016). Does Merger Simulation Work? Evidence from the Swedish

Analgesics Market. American Economic Journal: Applied Economics, 8(4):125–164.

Bresnahan, T. F. (1982). The oligopoly solution concept is identified. Economics Letters, 10(1-2):87–

92.

Brito, D., Ribeiro, R., and Vasconcelos, H. (2018). Quantifying the Coordinated Effects of Partial

Horizontal Acquisitions. European Economic Review, 110:108–149.

Ciliberto, F. and Williams, J. (2014). Does Multimarket Contact Facilitate Tacit Collusion? Inference

on Conduct Parameters in the Airline Industry. The RAND journal of economics, 45(4):764–791.

Das, S. (2019). Effect of Merger on Market Price and Product Quality: American and US Airways.

Review of Industrial Organization, 55(3):339–374.

Department of Justice. (1993). Final Judgement for United States of America v. Airline Tariff Publish-

ing Company. https://www.justice.gov/atr/case-document/file/483626/download. Accessed: 2021-

06-15.

Department of Justice. (2013). Complaint for U.S., et al. v. US Airways Group, Inc. and AMR

Corporation. https://www.justice.gov/atr/case-document/file/514531/download. Accessed: 2021-

05-13.

Department of Justice. (2014). Response of Plaintiff United States to Public Comments on The

Proposed Final Judgement for U.S., et al. v. US Airways Group, Inc. and AMR Corporation.

https://www.justice.gov/atr/case-document/file/514496/download. Accessed: 2021-06-05.

Evans, W. N. and Kessides, I. N. (1994). Living by the “golden rule”: Multimarket contact in the us

airline industry. The Quarterly Journal of Economics, 109(2):341–366.

Greenfield, D., Kobayashi, B., Sandford, J., Taylor, C., and Wilson, N. (2019). Economics at the FTC:

Quantitative Analyses of Two Chemical Manufacturing Mergers. Review of Industrial Organization,

55(4):607–623.

Hazel, R. (2018). Airline capacity discipline in the U.S. domestic market. Journal of Air Transport

Management, 66:76–86.

Horizontal Merger Guidelines (Department of Justice) (2010). Horizontal Merger Guidelines.

27

Ivaldi, M., Jullien, B., Rey, P., Seabright, P., and Tirole, J. (2003). The Economics of Tacit Collusion.

IDEI Working Papers.

Li, S. Y., Mazur, J., Park, Y., Roberts, J., Sweeting, A., and Zhang, J. (2021). Repositioning and

Market Power After Airline Mergers. Working Paper, pages 1–83.

Loertscher, S. and Marx, L. (2021). Coordinated Effects in Merger Review. Journal of Law and

Economics (Forthcoming).

Miller, N., Sheu, G., and Weinber, M. (2021). Oligopolistic Price Leadership and Mergers: The United

States Beer Industry. Working Ppaer.

Miller, N. H. and Weinberg, M. (2017). Understanding the price effects of the MillerCoors joint

venture. Econometrica: Journal of the Econometric Society.

Olley, G. and Town, R. (2018). End of an era: The american airlines–us airways merger. The Antitrust

Revolution: Economics, Competition, and Policy, pages 448–470.

Park, Y. (2020). Structural Remedies in Network Industries: An Assessment of Slot Divestitures in

the American Airlines/US Airways Merger. Working Paper.

Peterman, C. A. (2014). The future of airline mergers after the US Airways and American Airlines