Session III Market Risk / Introduction to Insurance Risk

57

Session III Market Risk / Introduction to Insurance Risk Dr. Peter Kandl April 23, 2007

-

Upload

rae-roberson -

Category

Documents

-

view

25 -

download

1

description

Session III Market Risk / Introduction to Insurance Risk. Dr. Peter Kandl April 23, 2007. Objectives. To have a basic understanding of the measurement of market and insurance risk To be able to compute Value-at-Risk To be able to outline a model verification strategy. - PowerPoint PPT Presentation

Transcript of Session III Market Risk / Introduction to Insurance Risk

Session IIIMarket Risk / Introduction to Insurance Risk

Dr. Peter Kandl

April 23, 2007

2

Objectives

• To have a basic understanding of the measurement of market and insurance risk

• To be able to compute Value-at-Risk

• To be able to outline a model verification strategy

3

Financial risk - General remarks

• Modern parlance: danger of loss

• Finance theory: dispersion of unexpected outcomes due to movements in financial / market variable

– Implies that both, positive and negative deviations, should be viewed as sources of risk

– Extraordinary performance, both good and bad, should raise red flags

• Measurement of risk therefore requires definition of the variable of interest

– Portfolio value, earnings, capital, particular cash flow

4

Variable of interest (risk metric)

• Portfolio Value:

• Capital(*) (Surplus) : Assets ./. Liabilities:

• Earnings:

• Cash flow: Particular item(s) from earnings statement

ii

iI AvwAAV ,...,1

+Revenues./.Variable costs of operations./.Fixed cash cost (administrative costs, real estate taxes)./.Non cash charges (depreciation, deferred taxes)./.Interest on debt./.Taxes

KI LLVAAV ,...,,..., 11

TIDNCFCVCRE

(*) needs capital model

5

Market risk

• Usually captures effect on portfolio value

• Four main types of market risk:

– Interest rate risk, exchange rate risk, equity risk, commodity risk

• Risk is measured by standard deviation of unexpected outcomes, also called volatility

• Losses can occur through combination of two factors:

– Volatility of underlying financial variable

– Exposure to this source

6

Market jargon

• Measurement of linear exposures to movements in underlying financial variables:

– Fixed income market: Duration

– Stock market: Systematic risk (Beta)

– Derivatives market: Delta

• Second derivatives (measure quadratic exposure):

– Fixed income market: Convexity

– Derivatives market: Gamma

7

Source of loss: principle

• Can we decompose market loss into its constituent pieces, exposure and adverse movement of its most influencing financial variable?

Market Loss = (Exposure) x (Adverse Movement in Financial Variable)

8

Source of loss: useful approximations

Change in bond price =-(Dollar duration) x (Shift in yield)yPDP )( *

Miiii RPPRP )( Change in price = (Beta-position) x (Relative change in market)

S

dSSdf Change in option value =

(Delta-position) x (Relative change in underlying)

Bond-Position

Equity-Position

Option-Position

9

Measuring asset returns

• Random component: change relative to today‘s price (level)

• Build random sample from rates of changes in the spot rate:

• Total return:

, where dividend or coupon , reinvested at every end-of-period

11 /)( ttttTot SSDSRt

11 /)( tttt SSSR

tD

10

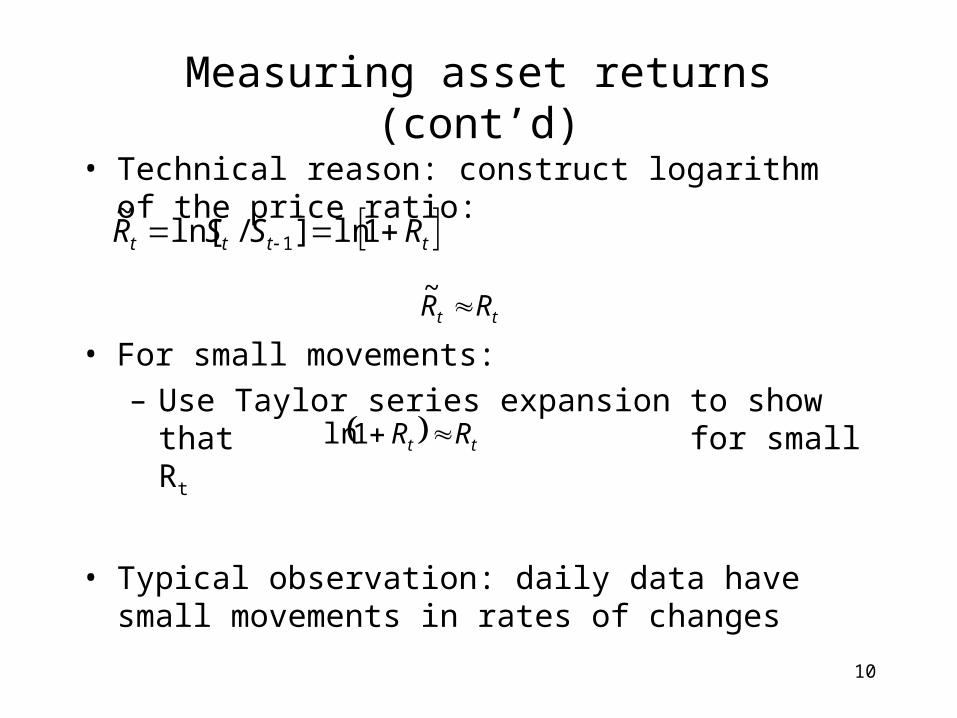

Measuring asset returns (cont’d)

• Technical reason: construct logarithm of the price ratio:

• For small movements:

– Use Taylor series expansion to show that for small Rt

• Typical observation: daily data have small movements in rates of changes

tttt RSSR 1ln]/ln[~

1

tt RR 1ln

tt RR ~

11

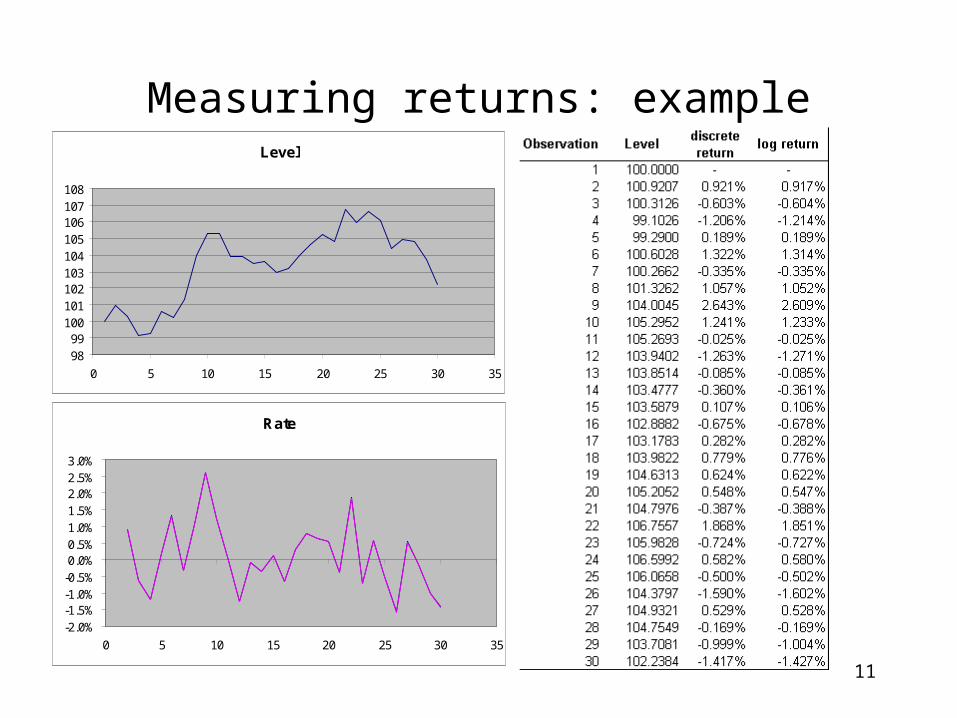

Measuring returns: exampleLevel

9899

100101102103104105106107108

0 5 10 15 20 25 30 35

Rate

-2.0%-1.5%-1.0%-0.5%0.0%0.5%1.0%1.5%2.0%2.5%3.0%

0 5 10 15 20 25 30 35

12

Sample estimates: mean

• Working assumption: T observations of (i.i.d.)random variables (e.g. daily returns in EUR/USD rates)

• Estimate the (unknown!) expected return or mean by the sample mean:

• Principle: Assign to each observation a constant weightsince all observations have the same probability of occurrence

TiiR 1

RE

T

iiR

Tm

1

1̂

T1

13

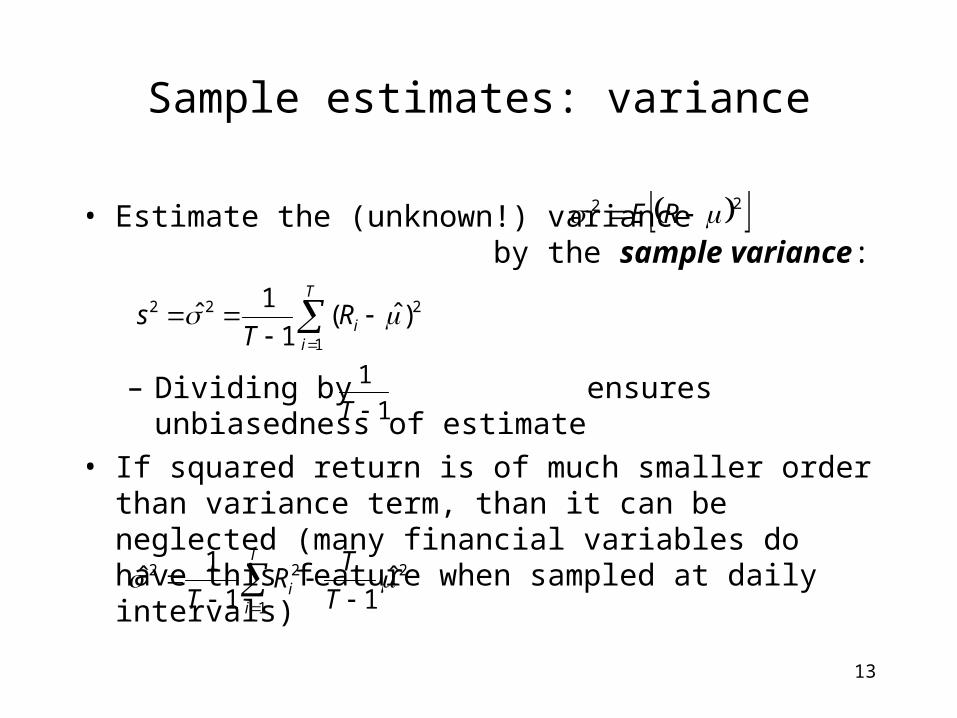

Sample estimates: variance

• Estimate the (unknown!) variance by the sample variance:

– Dividing by ensures unbiasedness of estimate

• If squared return is of much smaller order than variance term, than it can be neglected (many financial variables do have this feature when sampled at daily intervals)

22 RE

T

iiR

Ts

1

222 )ˆ(1

1ˆ

1

1

T

2

1

22 ˆ11

1ˆ

T

TR

T

T

ii

14

Time aggregation

• Parameters can be (under certain conditions) adapted to other time horizons

• Example: extend daily mean return to monthly mean return (easy with logarithmic returns!) by using

to conclude that

12010112

01120202

)]/ln[()]/ln[(

)]/)(/ln[(]/ln[

RRSSSS

SSSSSSR

TRERE T )()( 1

i.i.d. (!)

15

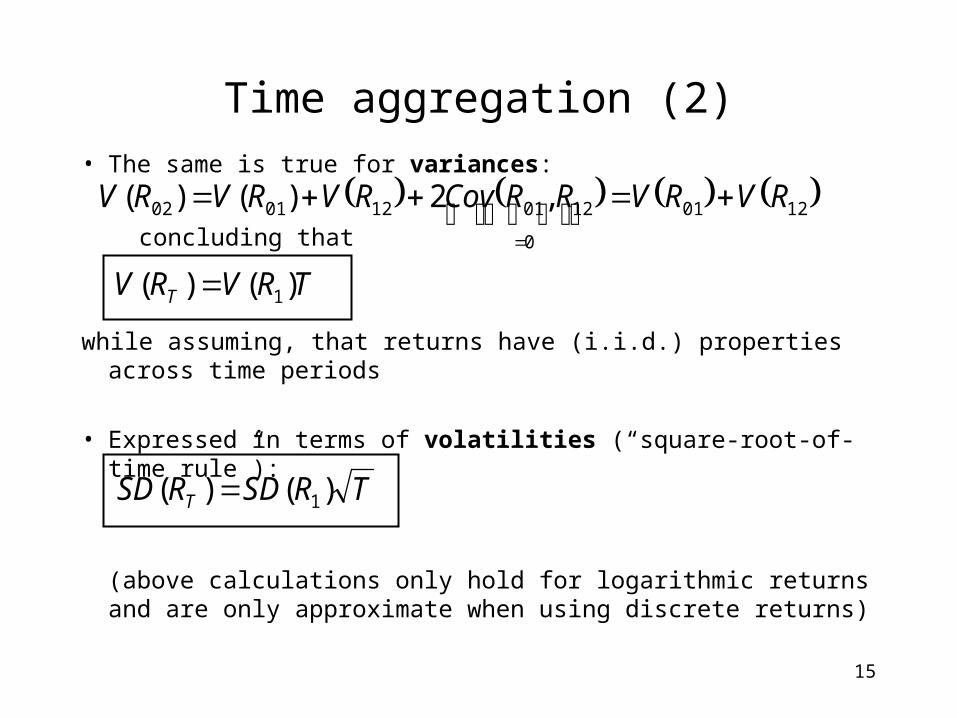

Time aggregation (2)

• The same is true for variances:

concluding that

while assuming, that returns have (i.i.d.) properties across time periods

• Expressed in terms of volatilities (“square-root-of-time rule”):

(above calculations only hold for logarithmic returns and are only approximate when using discrete returns)

TRVRV T )()( 1

TRSDRSD T )()( 1

1201

0

1201120102 ,2)()( RVRVRRCovRVRVRV

16

VaR: motivation

• Common task in (market) risk management: Quantify risk of losses due to movements in financial market variables

• Past concepts

– Notional amounts, sensitivity measures, scenarios

– Well suited for implementation in their defined areas

– Cannot be compared across methods and financial instruments

• Fundamental question: Is there a method that is more general for quantifying potential losses in a (arbitrarily chosen) portfolio?

• Question is too general, must be more specified

17

VaR as downside risk

• VaR (Definition): VaR is the maximum loss over a target horizon such that there is a low, prespecified probability that the actual loss will be larger

• Definition requires:

– Specifying loss distribution for a given target horizon

– Choosing an appropriate confidence level

18

VaR (general distributions)

• Define initial setting:

– W0: initial investment, R: rate of return

– Value at end of period: W=W0(1+R)

– R is random variable with (, 2)

• W*=W0(1+R*): lowest value for given confidence level c

• VaR (mean) = E(W)-W* = -W0(R*-) (relative to mean)

• VaR (zero) = W0-W* = - W0R* (absolute loss)

• Relative VaR conceptually more appealing• For general distributions, cdf must be inverted to find cut-off value R*

(percentile)

19

VaR (parametric distributions)

• Assume pdf belongs to parametric family (e.g. normal)

• Standardize R by

• Find appropriate value for confidence level)

• Then R*=- +

• More generally, parameters and are expressed on annual basis. Then use time aggregation results to show

• VaR(mean) = -W0(R*-) = W0

• VaR(zero) = -W0R* = W0(t)

R

t

t

20

Standard Normal Distribution

• Standardization of distribution X~N(, 2) by

• Then, Y~N(0,1): standard normal distribution

• Percentiles of normal distribution

– 66% of distribution between [-, ]

– 95% of distribution between [-2, 2 ]

– 95% of distribution below 1.65– 99% of distribution below 2.33– 99.5% of distribution below 2.58

X

Y

21

Parametric VaR: examples

• Volatilities of financial variables are usually given on a yearly basis

• Order of magnitudes– Stock / market indices: 12% - 50%– FX (against USD): 5% -15%– IR (yield changes): 0.6% - 1.2%– Commodity (base metals, energy): 10% - 100%

• Given a confidence level of and a fixed position in a financial variable, what is the “maximum” potential loss over the next z days? Provide examples!

22

Alternative measures

• Conventional VaR measure is a quantile-estimator of the loss distribution

• Alternative measures

– Entire distribution: report, e.g., range of VaR numbers for increasing confidence levels

– Conditional VaR (expected shortfall, Tail VaR): Expected loss given that loss exceeds VaR

– Standard deviation

– Semi-standard deviation

)( VaRXXE

N

i i XExN

XSD1

2

1

1

N

i iL

L XExMinN

XSD1

20,1

1

23

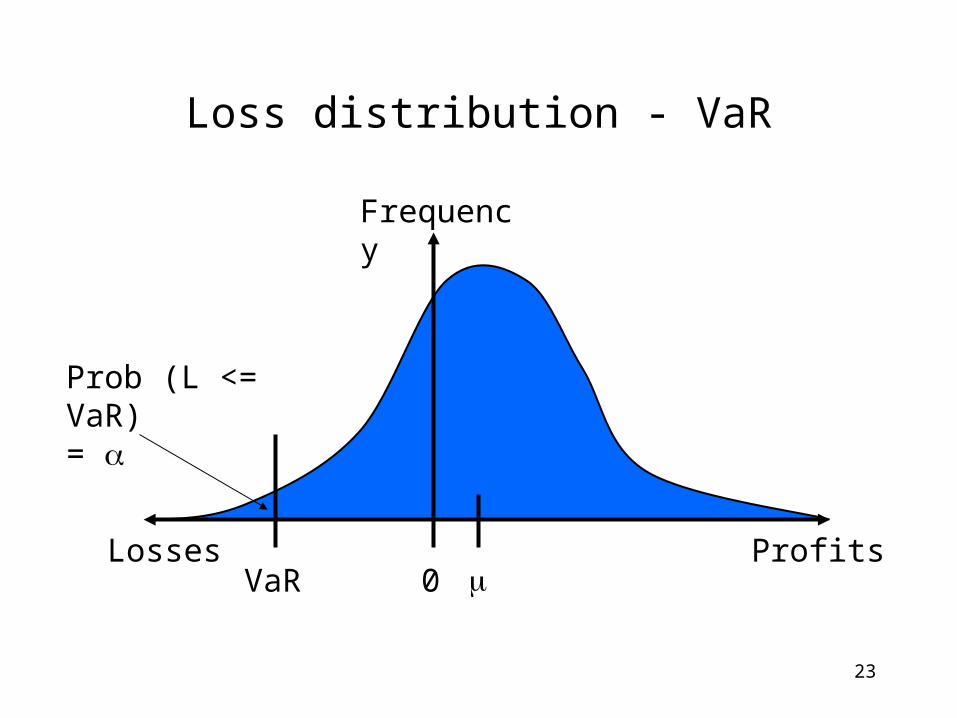

Loss distribution - VaR

ProfitsLosses0

Frequency

Prob (L <= VaR)=

VaR

24

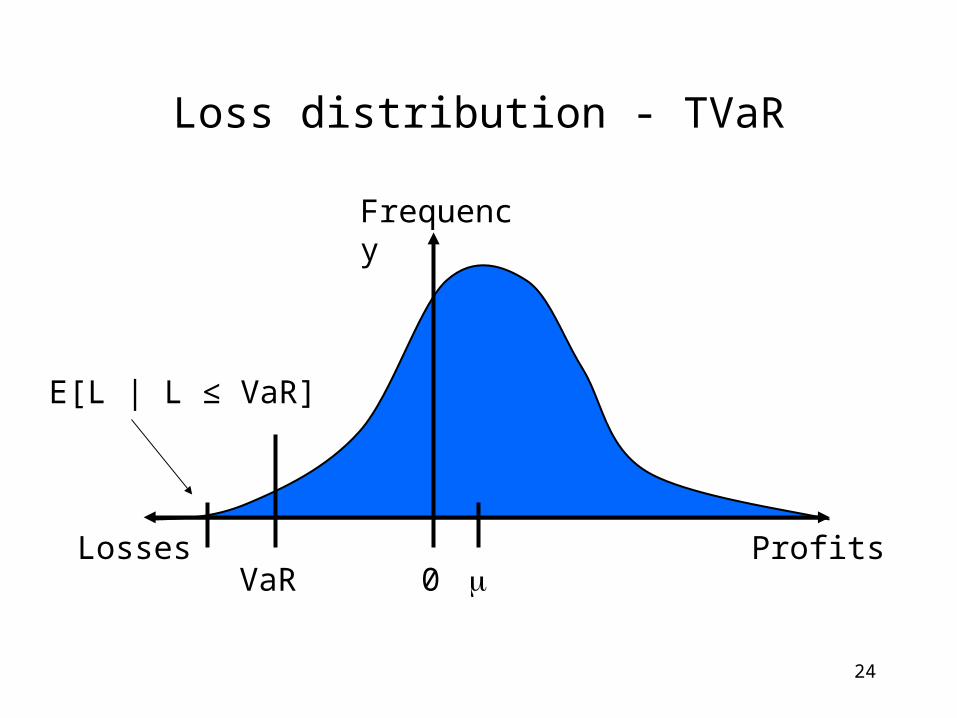

Loss distribution - TVaR

ProfitsLosses0

Frequency

VaR

E[L | L ≤ VaR]

25

Example

• Given the following 30 ordered, simulated percentage returns of an asset, calculate the VaR and the expected shortfall (both expressed in terms of returns) at a 90% confidence level.

• -16, -14, -10, -7, -7, -5, -4, -4, -4, -3, -1, -1, 0, 0, 0, 1, 2, 2, 4, 6, 7, 8, 9, 11, 12, 12, 14, 18, 21, 23

26

Desirable properties for risk measures

• Monotonicity: If losses in portfolio A are larger than losses in portfolio B for all possible risk factor return scenarios, then the risk of portfolio A is higher than the risk in portfolio B

• Translation Invariance: known cash (flows) do not contribute to risk

• Homogeneity: If the size of every position in a portfolio is doubled, the risk of the portfolio will be twice as large

• Subadditivity: The risk of the sum of the portfolios is smaller or equal than the sum of their individual risks

• A risk measure satisfying all above criteria is said to be a coherent risk measure

– VaR fails to satisfy subadditivity property, not a coherent measure

– CVaR is a coherent measure

27

VaR parameters: confidence level

• Confidence Level: Choose appropriate level • If goes up, VaR increases

– But: number of exceptions become very rare

• Choice of largely depends on use of VaR

• Consistency is what really matters!

– Across business units (trading desks), across time

• Capital adequacy: use high confidence level

• For backtesting purposes: use lower (e.g. 95%) to ensure that outcomes “beyond” actually occur during investigation period

28

• Target horizon: Choose appropriate “holding period” T

• If T increases, VaR increases

– Depends on:• Behaviour of risk factor(s)

• Portfolio positions

• Can we establish basic rule?

– Yes, if returns are i.i.d. and normally distributed

• Choose shorter horizon, if positions change quickly and / or exposures change as underlying change (e.g. delta)

• But: Target horizon cannot be less than P&L reporting frequency

NTNdaysVaRTdaysVaR

VaR parameters: horizon

29

Backtesting

• Involves systematically comparing historical VaR measures with subsequent returns

• Returns can be based upon

– „Frozen portfolio“

– Actual return („dirty“ P&L) including intra-day trades and other profit items (actual portfolio changes its composition)

– „Cleaned“ return: actual return minus all non-marked-to-market items (funding costs, fee income, reserves released,...)

• Model testing is faced with two types of errors:

– Type I: Reject a correct model

– Type II: Accept an incorrect model

• Reduced to classical statistical decision problem: errors of type I and II must be balanced against each other

30

Model verification: example

• Failure rates: Fix confidence level (p*=1-) and record VaR figure for a number of T days. Count number of days where actual loss (profit) exceeds previous day‘s VaR. This number is N, and the failure rate N/T

• Outline of a test: Null (H0) is p=p*; Number of exceptions N follows binomial probability distribution:

• If T is large, use CTL and approximate by standard normal

• Under the null, z is standard normally distributed

• Basel framework uses such a type of model verification

NTN ppN

TNf

1)( with E(N)=pT, V(N) = p(1-p)T

Tpp

pTNz

)1(

31

Introduction to Insurance Risk• Insurance risk:

– Risk that policyholder claims may prove to be in excess of what was expected

• Risk metric: – Volume measure (technical provisions, written premium)– Requires consistent valuation of Liabilities

• Risk measure: – “VaR” of volume measure– Confidence level: 99.5 %– Holding period: 1 year

32

Reserve risk• Reserve risk: non-life underwriting risk that technical provisions, held to cover

incurred claims for coverage already provided, may prove inadequate

• Principle:

– Use simple factors differentiated by • Line of Business (different risk characteristics)• Size of portfolio (Reserve fluctuation of large portfolios tend to be less volatile

because of greater diversification)

– Allow for reinsurance by using net reserves as volume measure

– Factor can be conceptually considered as a multiple of the standard deviation of the distribution of the technical claim provision. The multiple is determined such that the required capital plus the MV of claim provisions combined, are 99.5% sufficient to cover incurred claims for coverage already provided

33

Reserve risk (2)

• Implementation:

– Required Capital Reserve Risk (LOB) = MV net claims provisions (LOB) * factor (LOB) * size factor (LOB)

• Example:

– Reserve risk factor• Accident and health: 28%

• Motor, third party liability: 12%

– Size factor• Between 0.7 and 10 (e.g. 2 for net reserves = 25 m CHF)

– CRres (A&H) = 25m CHF * 28% * 2 = 14 m CHFCRres (M)= 25m CHF * 12% * 2 = 6 m CHF

34

Premium risk

• Defined as risk that volume of ultimate losses for future claims occurred or still to occur at the valuation date (losses paid during time horizon of the cover and provisions made at its end) is higher than the premiums received for the cover period

• Principle:

– Use simple factors differentiated by lines of business and size of portfolio

– New business and renewals arising over the next year create additional source of risk

– Business written over upcoming year is uncertain and a proxy for the written premium of the previous year ca be used

– Use net premiums as volume measure to take Reinsurance into account

35

Premium risk (2)

• Implementation:

– Required capital premium Risk (LOB) =(Net written premium (LOB) + Net unearned premiums(LOB)) * factor (LOB) * size factor (LOB)

• Example:

– Premium risk factor• Accident & Health 18%

• Motor, third-party liability 12%

– Size factor• Between 0.7 and 10 (e.g. 2 for net written premium= 25 m CHF)

– CRprem(A&H) = 25m CHF * 18% * 2 = 9m CHFCRprem(M) = 25m CHF * 12% * 2 = 6m CHF

36

Catastrophe risk

• Principle:

– Include impact of catastrophe events taking into account reinsurance structure of the company

– Specify certain catastrophe scenarios for the entire market (e.g. flooding)

– Exposure to catastrophe will be measured by the gross market share of the insurance undertaking

– Take Reinsurance into account• Excess of Loss more effective than proportional for

catastrophe events

• Reinsurance limits and retentions should be applied

37

Mortality risk

• Defined as unexpected deviation on the mortality experience for products providing death coverage

• Risk components are:

– Volatility

– Uncertainty (level risk and trend risk)

– Extreme event (catastrophe)

• Principle:

– Use simple factors

– Volatility risk can be reduced by increasing size of portfolio

– Uncertainty and catastrophe risk are not diversifiable by increasing portfolio size

38

Mortality risk (2)• Implementation:

– Required capital mortality risk = (Factorvol + Factorterm)* Net sum at risk

– Net sum at risk = sum assured less technical provisions less reinsurance cover

39

Longevity risk• Defined as unexpected deviation on the mortality

experience for products providing coverage in case of life

• Implementation:

– CR Longevity Risk = Net Technical Provision * Longevity factor

40

Lapse risk• Defined as unexpected deviation on the expected lapse rate

• Implementation:

– CR Lapse Risk = Net Technical Provision * Lapse factor

41

Univariate distribution functions

• Random variable X is entirely characterized by its probability distribution function (cumulative distribution function)

which gives probability that X ends up below x

• If X takes discrete values

where f(x) is the probability density function (pdf)

)()( xXPxF

xx

j

j

xfxF )()(

Appendix

42

Moments

• Are used to describe characteristics of distributions (in fact, a distribution is uniquely defined by all of its moments)

• First order moment: mean (expected value, average)

• Second order moment: variance

N

iii xfxXE

1

)()(

22 )()( xEXV

Appendix

43

Variance and standard deviation

• The variance measures dispersion (uncertainty) of a random variable

• Standard deviation used as measure in the same units as random variable X

• In finance, the standard deviation, measured in relative terms, is often called „volatility“

)()( XVXSD

Appendix

44

Quantiles

• Quantile: given probability c, which cutoff point x is associated with it?

• The 50%-quantile is called median

• Example:

VaR for confidence level p=95%:

Loss, which will not be exceeded in (1-p) of all cases

cxXP i )(

Appendix

45

Linear Transformations

• Let X be a random variable and consider Y=aX+b

• Expectation of Y

• Variance of Y

• Example:

Portfolio with amount a of cash and b units of shares

)()( XbEabXaE

)()( 2 XVbbXaV

Appendix

46

Normal Distribution

• The normal distribution is characterized by its first two parameters:

– mean (location)

– variance 2 (dispersion)

• The density is given by

• There is no analytic expression (involving elementary functions) for the distribution function (use of tables, approximations)

])(2

1exp[

2

1)()( 2

22

xxxf

Appendix

Gerold Studer

Kein phi

47

Standard Normal Distribution

• Standardization of distribution X~N(, 2) by

• Then, Y~N(0,1): standard normal distribution

• Percentiles of normal distribution

– 66% of distribution between [-, ]

– 95% of distribution between [-2, 2 ]

– 95% of distribution below 1.65– 99% of distribution below 2.33

X

Y

Appendix

48

Illustration: Normal Distribution

-4 -3 -2 -1 0 1 2 3 4

Fre

quen

cy

0.4

0.3

0.2

0.1

0

66%

95%

±1 SD

±2 SD

Appendix

49

Stock Prices: Lognormal Distribution

• The normal distribution is often used for modeling because of its attractive mathematical properties

• The infinite tail on both sides however causes problems in finance: interest rates, stock prices, ... cannot become negative (i.e. returns smaller than –1 are not possible)

• X has lognormal distribution if Y=ln(X) is normally distributed

• The variable X=exp(Y) will always be positive

Appendix

50

0],))(ln(2

1exp[

2

1)( 2

22 xx

xxf

• Y normally distributed with parameters =E[Y] and 2 =V[Y]

• The density of the lognormal variable X is

• The mean of the lognormal is

• The variance of the lognormal is

Lognormal Distribution (cont´d)

]2

1exp[)( 2 XE

]1exp[][ 22 XV

Appendix

51

Illustration: Lognormal Density Function

0.00 2 4 6 8 10

Fre

quen

cy

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Sigma=1

Sigma=1.2

Sigma=0.6

Appendix

52

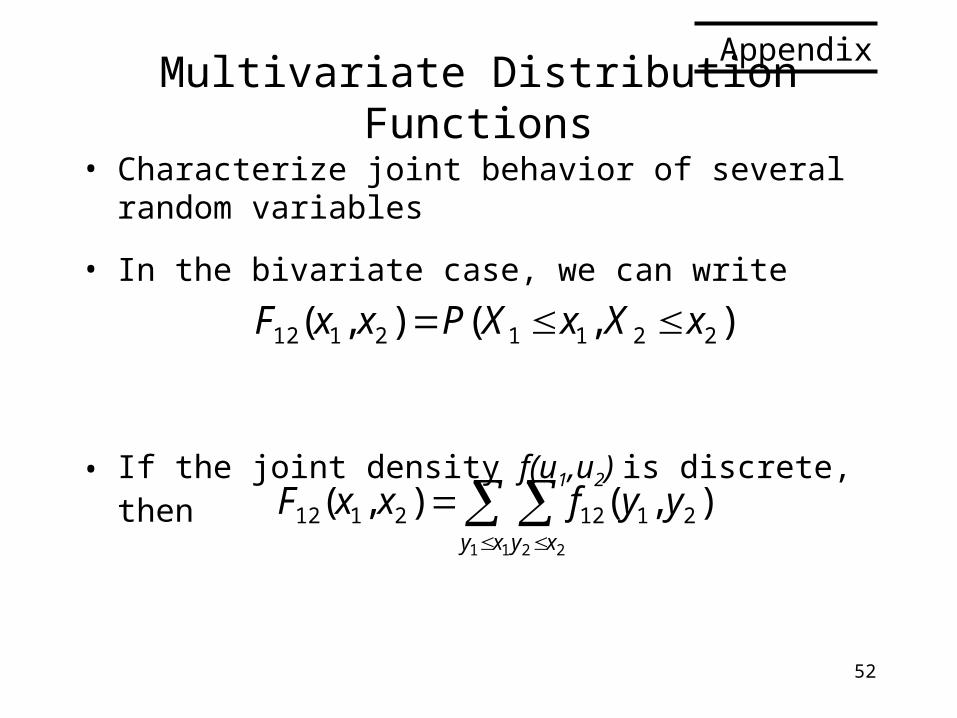

Multivariate Distribution Functions

• Characterize joint behavior of several random variables

• In the bivariate case, we can write

• If the joint density f(u1,u2) is discrete, then

),(),( 22112112 xXxXPxxF

11 22

),(),( 21122112xy xy

yyfxxF

Appendix

53

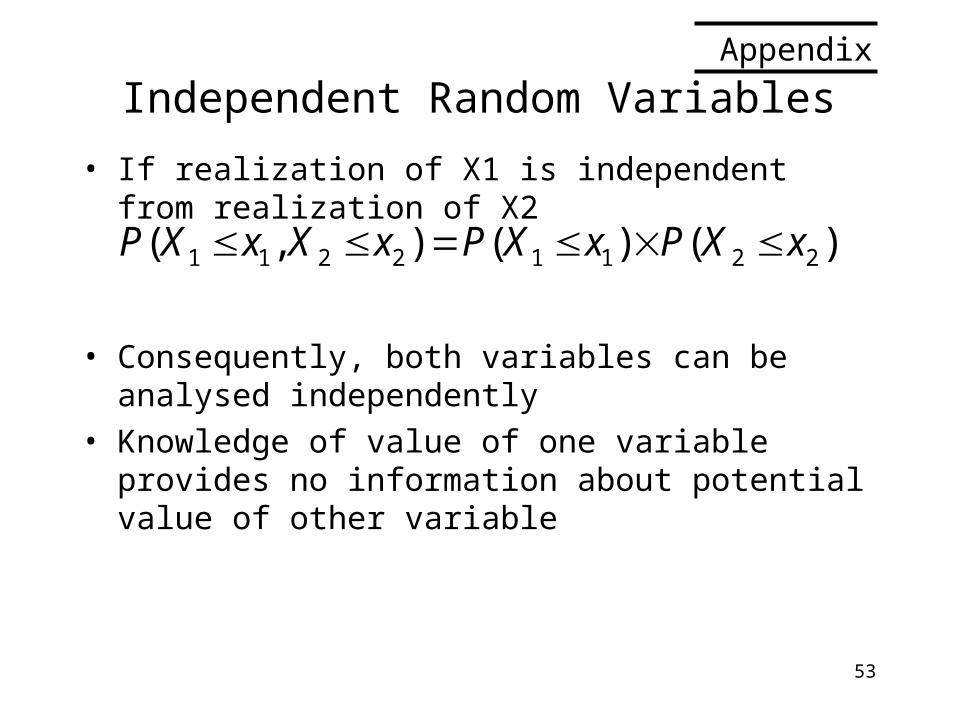

Independent Random Variables

• If realization of X1 is independent from realization of X2

• Consequently, both variables can be analysed independently

• Knowledge of value of one variable provides no information about potential value of other variable

)()(),( 22112211 xXPxXPxXxXP

Appendix

54

Conditional Density

• Conditional density: density of X1, given X2

• If variables are independent:

• The marginal and conditional distributions of multivariate normal distributions are always normal

)(

),()(

22

22112211 xXP

xXxXPxXxXP

)()( 11211 xXPxxXP

Appendix

55

Covariance & Correlation

• Measure of co-movement of 2 random variables

• Correlation as unitless measure

• Correlation lies always in interval [-1,1]

)])([(),( 221121 xxEXXCov

21

2121

),(),(

XXCov

XX

Independence implies correlation of 0, but not vice versa (exception: normal distribution)

Appendix

56

Sum of Random Variables

• Expectation of 2 random variables

• Variance of 2 random variables

• If the variables are uncorrelated, the variance of the sum is equal to the sum of variances

• Formulas generalize easily to n random variables

)()()( 2121 XEXEXXE

),(2)()()( 212121 XXCovXVXVXXV

),(2)()()( 212121 XXCovXVXVXXV

Appendix

57

Portfolios of Random Variables• Linear combinations with fixed weights wi

are a generalization of linear transformations and sums

• Example: Xi: asset returns, wi: portfolio weights („position size“)

N

iii XwY

1

)(11

N

iii

N

iii XEwXwE

),(2)(1

2

1

jijiji

N

iii

N

iii XXCovwwXVwXwV

Appendix