Session 7 Types of Life Insurance Modified Endowment Contract Beneficiary Designations

22

©2015, College for Financial Planning, all rights reserved. Session 7 Types of Life Insurance Modified Endowment Contract Beneficiary Designations CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAM Financial Planning Process & Insurance

-

Upload

hayfa-sanders -

Category

Documents

-

view

41 -

download

2

description

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAM Financial Planning Process & Insurance. Session 7 Types of Life Insurance Modified Endowment Contract Beneficiary Designations. Session Details. Life Insurance Diagram: Term. Term life insurance is for - PowerPoint PPT Presentation

Transcript of Session 7 Types of Life Insurance Modified Endowment Contract Beneficiary Designations

©2015, College for Financial Planning, all rights reserved.

Session 7Types of Life Insurance Modified Endowment ContractBeneficiary Designations

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMFinancial Planning Process & Insurance

Session Details

Module 5

Chapter(s)

2 & 3

LOs 5-2 &

5-3

Identify types, uses, and limitations of various types of individual life insurance policies.

Compare the purposes of the general provisions of a life insurance policy.

6-2

Life Insurance Diagram: Term

Term life insurance is for temporary needs:• mortgage costs• dependent education• consumer debts• large coverage, small

premium• cost rises with age 6-3

Life Insurance Diagram: Whole Life

Whole life insurance is for

permanent needs:• lifetime needs• last expenses• estate liquidity• business needs• premiums same for life6-4

Life Insurance Diagram: UL/VUL

Universal life:• unbundles premiums• increased

contributions

Variable life:• policyowner selects

investmentsBoth have separate accounts.

6-5

Taxation of Life Insurance

Death benefits

• Income tax free to beneficiaries

• Accelerated death benefit rules allow some distributions as income tax free – terminal illness, LTC benefits, etc.

• Exception if transfer for value (viatical settlement owner, etc.)

• Included in estate tax if any incidence of ownership

6-6

Taxation of Life Insurance

Tax free build up of cash value

• Accounts grow tax deferred

• Withdrawals up to basis tax free (includes loans)

• Distributions after basis taxed at ordinary income, NOT capital gains rates

• If MEC, gain is taxed each year independent of whether withdrawn

• If policies lapse, any loans taken that were above basis become taxable

• Some creditor protection6-7

1035 Exchanges

Section 1035 allows policies to

transfer without taxation if:

• cash value life insurance to cash value life insurance or annuities or LTC

• annuities to annuities or LTC

Allows flexibility for lifetime planning – cash value to annuity

or LTC when insurance is no longer needed.

6-8

Selected Characteristics of Life Insurance

6-9

Selected Characteristics of Life Insurance continued

6-10

Selected Characteristics of Life Insurance continued

6-11

Modified Endowment Contract (MEC)

A life insurance policy becomes a MEC if:

• it fails seven-pay test

• loans or withdrawals taxed as ordinary income (LIFO)

• 10% penalty on withdrawals taken before age 59½

• death benefits retain normal tax status

6-12

Seven-Pay Test

6-13

Withdrawals from a MEC

• MEC withdrawals prior to 59½ are subject to 10% penalty on taxable gains.

• Once a policy becomes a MEC, it remains a MEC forever.

• In the case of a 1035 exchange, a MEC is still a MEC.

• Policies that avoid MEC status in their first seven years may still be subject to MEC rules in the event of material change, such as a change of age or increase of coverage amount.

• A new seven-year premium limit is instituted.

• All single-premium life policies are MECs.

6-14

Beneficiary Designations/Provisions

6-15

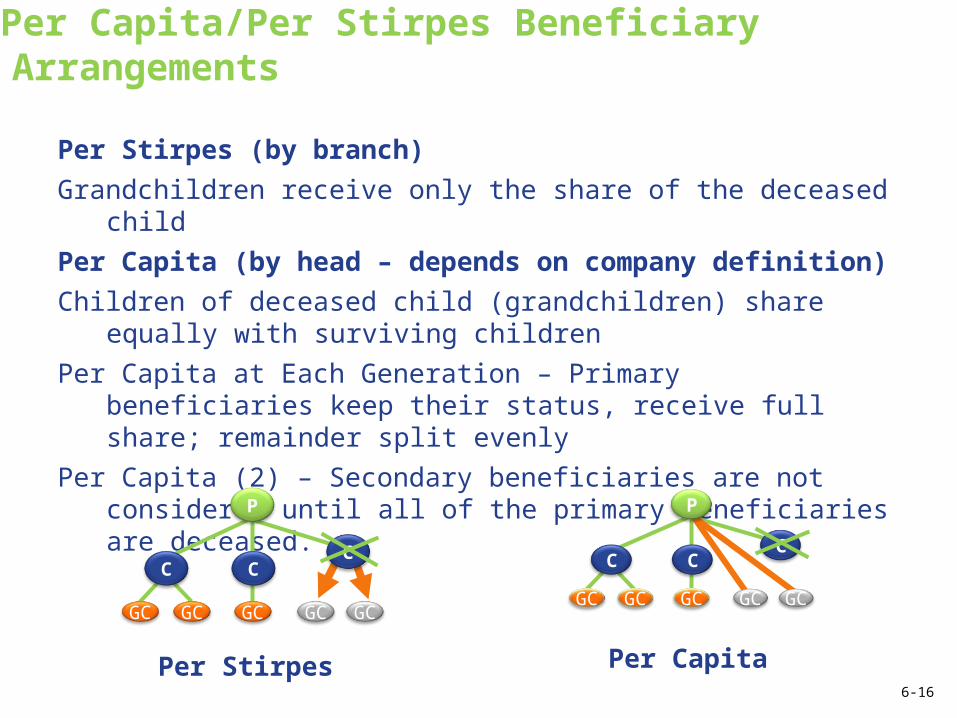

Per Capita/Per Stirpes Beneficiary Arrangements

Per Stirpes (by branch)

Grandchildren receive only the share of the deceased child

Per Capita (by head – depends on company definition)

Children of deceased child (grandchildren) share equally with surviving children

Per Capita at Each Generation – Primary beneficiaries keep their status, receive full share; remainder split evenly

Per Capita (2) – Secondary beneficiaries are not considered until all of the primary beneficiaries are deceased.

C

GC GC

CC

P

GC GC GC

C

GC GC

CC

P

GC GC GC

Per CapitaPer Stirpes6-16

Question 1

Which one of the following correctly identifies an acceptable 1035(a) exchange?a. an endowment contract for a term life

policyb. an annuity contract for a whole life

policyc. an annuity contract for an endowment

contractd. an endowment for an annuity contract

6-17

Question 2

Which one of the following is not an advantage of universal life (UL) insurance?a. It has flexible premium payments.b. It lends itself to a compulsory savings

program.c. It has an adjustable death benefit.d. It has an unbundled structure.

6-18

Question 3

Modified endowment contracts can only be created in which of the following types of life insurance policies?

I. term life policiesII. whole life policiesIII. universal life policiesIV. variable universal life policies

a. I and II onlyb. III and IV onlyc. II, III, and IV onlyd. I, II, III, and IV

6-19

Question 4

All of the following are true regarding life insurance beneficiaries, except a. primary beneficiaries are paid before

secondary beneficiaries.b. there is no limit to the number of

beneficiaries in any one class.c. spouses are the most commonly

named primary beneficiaries.d. most beneficiary designations are

irrevocable.

6-20

Question 5

Which one of the following is not true regarding second to die policies? a. The policy pays when the last person

dies.b. Premiums are generally lower than the

cost for two separate policies.c. They are generally not a very useful

tool for estate planning purposes.d. They may be generally advantageous

when one of the two insureds is older and highly rated.

6-21

©2015, College for Financial Planning, all rights reserved.

Session 7End of Slides

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMFinancial Planning Process & Insurance