Session 6C Internal audit value Developing metrics to ...

16

Session 6C Internal audit value – Developing metrics to present IA value Lawrence J. Harrington CIA QIAL CRMA, Vice President, Internal Audit, Raytheon Company, USA and Chairman of the Board, IIA-Global

Transcript of Session 6C Internal audit value Developing metrics to ...

Session 6C Internal audit value – Developing

metrics to present IA value

Lawrence J. Harrington CIA QIAL CRMA, Vice President, Internal Audit, Raytheon Company, USA

and Chairman of the Board, IIA-Global

Metrics Help Build Internal Audit’s Brand

• Customers demand value from IA.

• Metrics often fail to communicate IA’s value.

• Most IA metrics are inward facing.

• Few outward metrics resonate with customers.

• Metrics help build the function’s brand, but

they depend on the personal brands of every

member of the audit team.

Demonstrating Value is Crucial

More demanding stakeholders

means little margin for error

and less time to react.

Stakeholder perception is

reality; we must provide more

value to customers.

Meaningful metrics, internal

and external, strengthen and

promote internal audit’s brand.

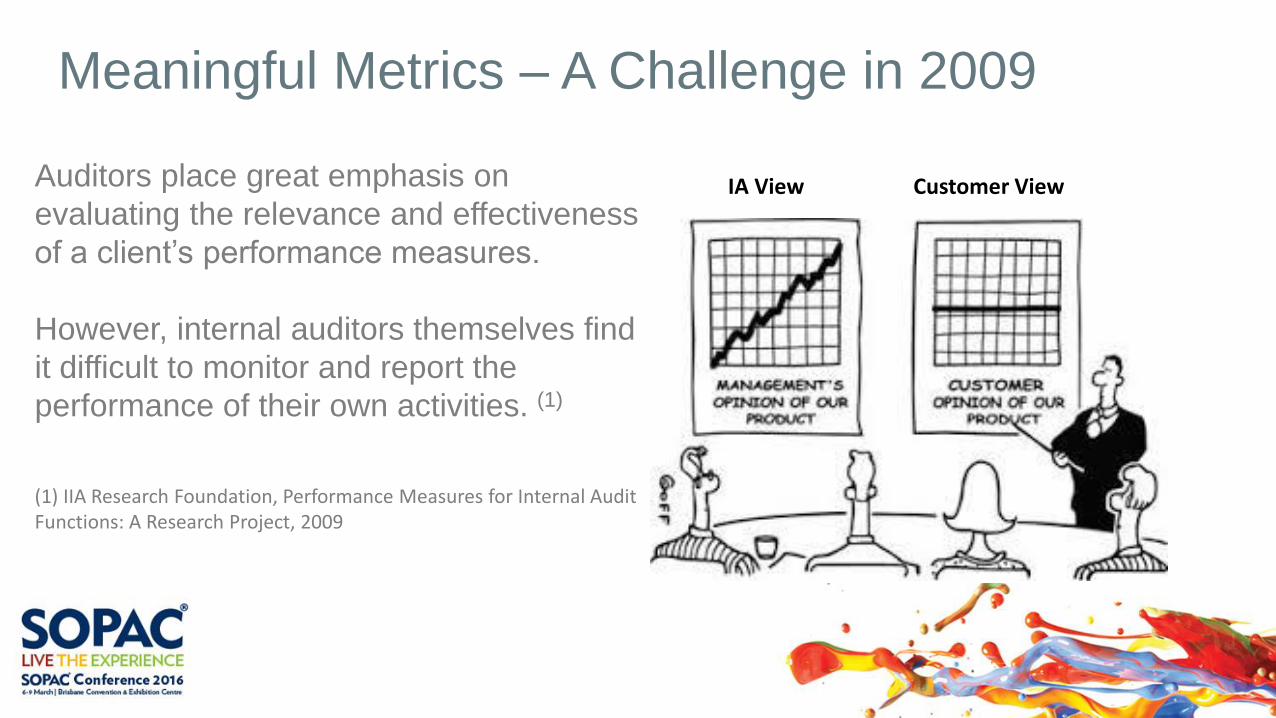

Meaningful Metrics – A Challenge in 2009

Auditors place great emphasis on

evaluating the relevance and effectiveness

of a client’s performance measures.

However, internal auditors themselves find

it difficult to monitor and report the

performance of their own activities. (1)

(1) IIA Research Foundation, Performance Measures for Internal Audit Functions: A Research Project, 2009

IA View Customer View

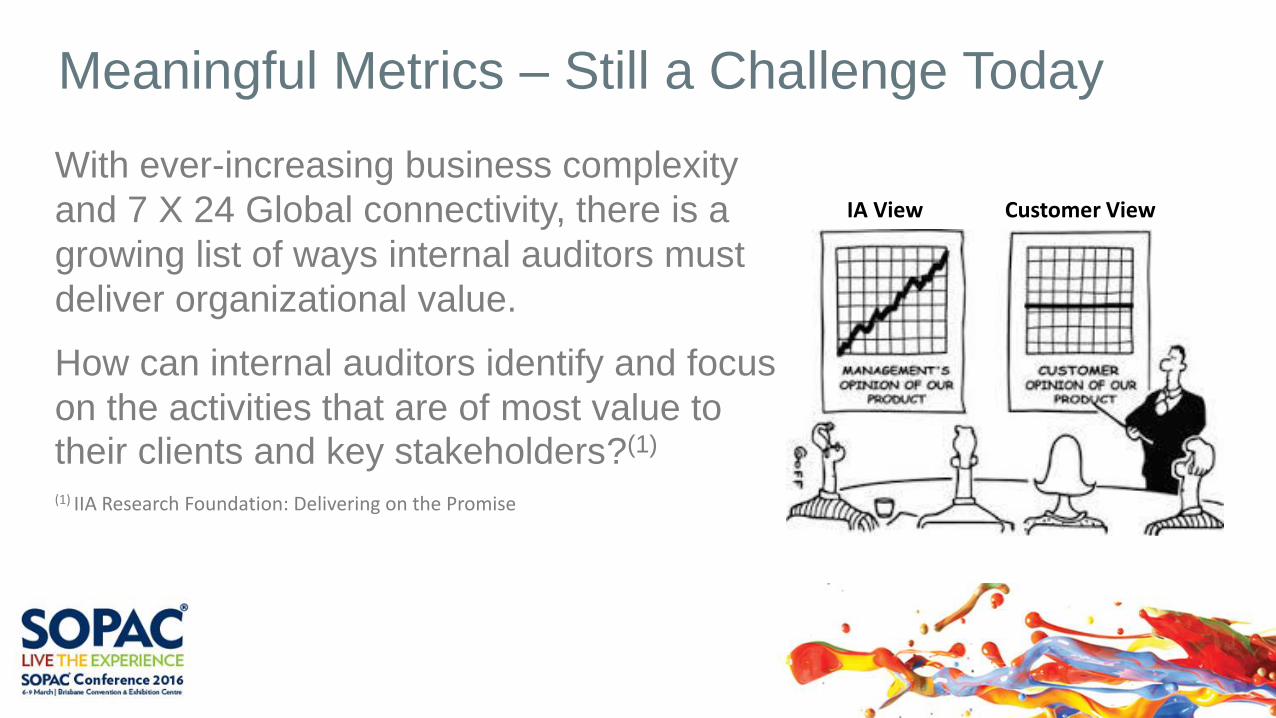

Meaningful Metrics – Still a Challenge Today

With ever-increasing business complexity

and 7 X 24 Global connectivity, there is a

growing list of ways internal auditors must

deliver organizational value.

How can internal auditors identify and focus

on the activities that are of most value to their clients and key stakeholders?(1)

(1) IIA Research Foundation: Delivering on the Promise

IA View Customer View

Today’s Challenge – Customer Satisfaction

How satisfied are you that your

company’s internal audit function

delivers the value to the

Company that it should? (1)

Sixty percent of audit committees

are less than fully satisfied that

the internal audit function

delivers the value that it should.

(1) KPMG -- 2015 Global Audit Committee Survey

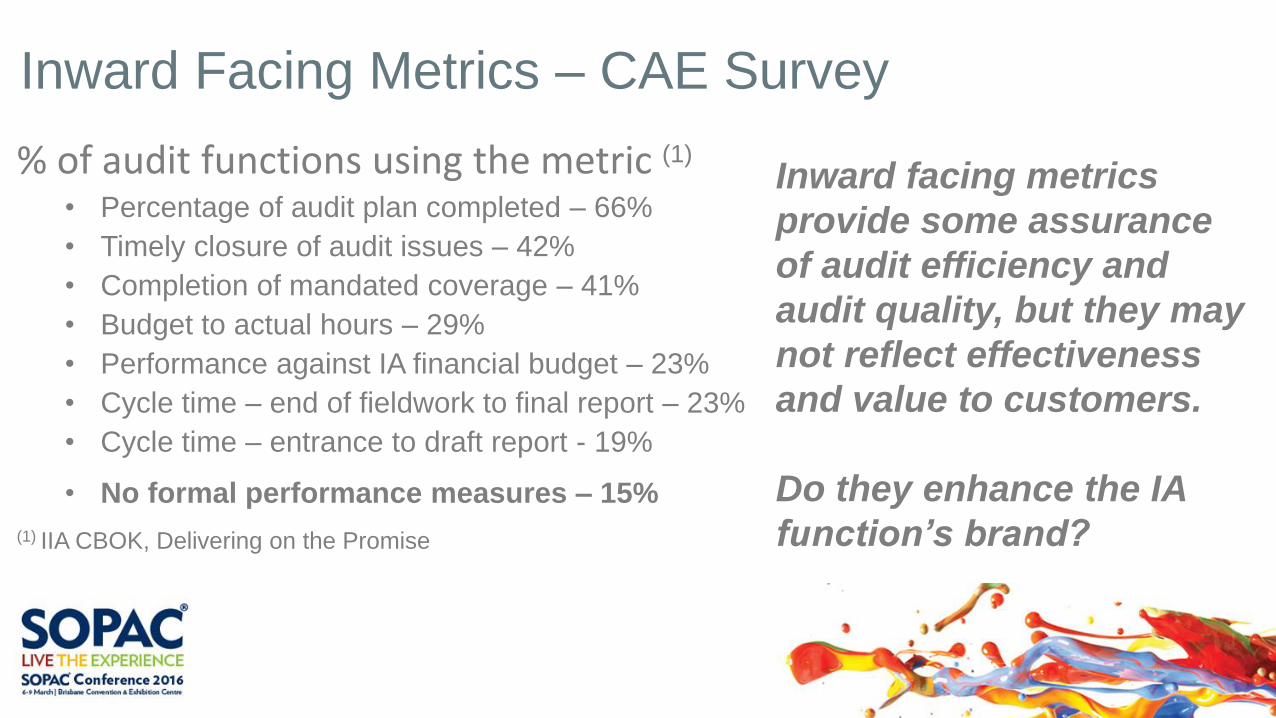

Inward Facing Metrics – CAE Survey

% of audit functions using the metric (1)

• Percentage of audit plan completed – 66%

• Timely closure of audit issues – 42%

• Completion of mandated coverage – 41%

• Budget to actual hours – 29%

• Performance against IA financial budget – 23%

• Cycle time – end of fieldwork to final report – 23%

• Cycle time – entrance to draft report - 19%

• No formal performance measures – 15%

(1) IIA CBOK, Delivering on the Promise

Inward facing metrics

provide some assurance

of audit efficiency and

audit quality, but they may

not reflect effectiveness

and value to customers.

Do they enhance the IA

function’s brand?

Outward Facing Metrics

2 of the top 10 metrics face outward. • Client satisfaction goals (38%)

• Fulfillment of specific expectations agreed to

with key stakeholders (32%)

How can an internal audit function demonstrate and

communicate its value added brand?

Metrics Should Reinforce Your Brand

“Simply put, your brand is your promise to your customer.

It tells them what they can expect from your products and

services; it differentiates your offering. Your brand is

derived from who you are, who you want to be and who

people perceive you to be. Defining your brand is like a

journey of business self-discovery. It can be difficult, time-

consuming and uncomfortable.” (1)

An effective brand resonates with customers. Use metrics

that reflect and reinforce your brand.

(1) John Williams, The Basics of Branding, Entrepreneur

Align Performance Measures and Value Add Activities (1)

1.Learn the customer’s expectations

2.Validate understanding with stakeholders

3.Develop outward facing and inward

facing performance measures

4.Start measuring

5.Report back to stakeholders

6.Repeat the cycle periodically

(1) IIA CBOK, Delivering on the Promise

Measuring Value: Customer Feedback

• Audit objectives were clearly communicated to customer.

• Opportunity to give input to objectives, due dates, deliverables.

• Customer received timely updates.

• Audit timeline/duration was reasonable and minimized disruption.

• Internal Audit took time to understand the business.

• Internal Audit effectively addressed key business risks.

• Internal Audit conducted activities in a professional manner.

• Audit report was accurate, relevant, clear, concise, and timely.

• I would recommend Internal Audit as a value-added service.

Building the Brand: Teaming with CustomersBe inclusive to increase knowledge of the business

Create a GRC council with other functions

Recruit non-auditors from the business

Have customers provide functional overviews

Utilize guest auditors / SMRs from the business

Invite customers to co-present with you

Publicly praise your peers for their successes

Align individual incentives to collaboration goals

٠ Performance measurement based on overall audit satisfaction

٠ Create team value-add deliverables – leave behinds

Use Metrics That Build Your Brand• A strong, effective brand builds trust and creates a

positive emotional response from the customer -

Apple, McDonalds, Nike, Starbucks.

• Metrics must be meaningful and support the brand.

• Inward facing metrics can help promote quality but

must ultimately support outward facing metrics.

• Lesser used metrics may be impactful.

• Internal auditors hired from the business

• Internal auditors placed back into the business

• Performance ratings of auditors hired into the business

• Retention of auditors hired into the business

Strong Function and Personal Brands

• Metrics for building the brand of an audit function

depend on the brands of your team members.

• Brand building metrics for team members include:

• Professional certifications

• Continuing personal and professional

development including company provided

training and investments in yourself

• Involvement in company initiatives or councils

• Networking, exposure to leadership

• Performance on special projects

Metrics and Branding – Self Analysis

• What is your function’s brand?

• What do you want it to be?

• How do your customers perceive your brand?

• What are your outward facing metrics?

• What should the metrics be?

• What are the personal brands of your team?

• Do their brands support the function brand?

• How are you measuring and managing them?

• How can you manage metrics to build the brand?

• Will your brand be stronger tomorrow?