Serving on your Church’s finance...

14

1 God’s intent and desire throughout the ages has been for His People to reach the lost. The Church Ministry Budget Guide is a tool to provide the church with the financial support to undergird God’s intent. A ministry made possible by your Cooperative Program gifts. Nate Adams, Executive Director Sylvan Knobloch, Director Church Health & Staff Development Illinois Baptist State Association P.O. Box 19247 Springfield, IL 62794 Phone: 217-391-3133 Fax: 217-391-5126 E-mail: [email protected]

Transcript of Serving on your Church’s finance...

1

God’s intent and desire throughout the ages has been for His People to reach the lost. The Church Ministry Budget Guide is a tool to provide the church with the financial support to undergird

God’s intent.

A ministry made possible by your Cooperative Program gifts. Nate Adams, Executive Director

Sylvan Knobloch, Director Church Health & Staff Development Illinois Baptist State Association P.O. Box 19247 Springfield, IL 62794 Phone: 217-391-3133 Fax: 217-391-5126 E-mail: [email protected]

2

Serving on your Church’s finance team places you at the epicenter of the church’s missional purpose. It is in this room that decisions will be made to fund new ministry and sustain existing ministry. Annual calendar planning, staffing, building needs, debt retirement, mission support and ministry resources can rise quickly like a flash flood at planning time. The goal in this booklet is not just to create a budget, but to fund a budget that will have kingdom impact on your church and community. Consider including these actions as your church develops next year’s missional budget for Kingdom growth: Seek spiritual direction Identify spiritual needs of your community and church—pastor, deacons, or elders will

want to make a presentation regarding the spiritual needs of both Consult with organizational and church leaders and staff Study the church’s mission statement Build congregational acceptance

Step 1 Identifying the church’s purpose calls for a clear understanding of its mission. Study these scriptures for key spiritual insights into the church’s purpose: Matthew 28:16-20, Acts 1:8, I Corinthians 12:20 and 13:13, 2 Corinthians 5:18-19, Ephesians 4:11-16.

Step 2 Analyze Ministries A ministry analysis is an evaluation of church programs in the light of the mission/purpose of the church and the needs of the community and church. The pastor will call a meeting of the church council and other key leaders, including the finance committee chairperson. They will discuss church programs, accomplishments of the last year and ask the question, “What does God desire for this church to become?”

What are the needs of our people? What are the needs of our community?

Outreach ministries Family ministries Youth ministries Senior adult ministries Special ministries Other

3

How well is the church doing its job? 1. Evaluate activities and projects conducted last year. 2. What new ministries are needed? 3. What current programs or projects are no longer needed? 4. Which community needs should the church address? 5. Plan church activities and events for the next year.

Analyze your Annual Church Profile (ACP). Your Church Clerk should have this information or you can contact IBSA Church Health for an ACP report. Calculate the baptism to membership ratio to find out how many members it takes to win a new member. Then divide the total receipts by the Average Worship Attendance. Divide that number by 52 to obtain the weekly giving per capita. This information will help you determine several things such as how well you are reaching others or whether you need a stewardship program. Next analyze your community. Request a Percept report on your church’s zip code or the radius around the church from IBSA Church Health. It will answer many questions about your neighborhood:

1. How many people live in the defined study area? 2. How do racial or ethnic groups contribute to diversity in this area? 3. What major generational groups are represented? 4. Overall, how traditional are family structures? 5. Which household concerns are unusually high in the area? 6. What is the likely faith receptivity? 7. What is the likely giving potential in the area?

Step 3: Ministry Proposals A ministry proposal is a written description of a suggested ministry. Ministry proposals are the most vital instruments in this budgeting approach as they are the means by which leaders and committees plan their work for the coming year. These should be carefully thought out and well defined. The form on page 4 should be given to all directors and persons wishing to make a church budget request. Building Spiritual Direction: Consult with church leaders. Ask for budget proposals from all those responsible for church ministries. Evaluate each current church ministry based on its spiritual impact. Ministry proposals are to include date(s) and funding requested.

4

Step 4 Evaluate Ministry Proposals by asking of each request:

What contribution will this allocation and the ministry it supports make toward fulfilling our church’s purpose?

Which of the church's objectives and goals does this proposal fulfill? What is the priority position of this request? Is this the best way to achieve this ministry? Is the money being allocated in proportion to available resources?

Building Spiritual Direction Seek God. Ask Him for wisdom as to how best to spend the gifts from His people to impact

His kingdom. Study ministry requests from department and church leaders. Study the Church Giving Profile. Emphasize personal stewardship as a benchmark of a growing disciple of Christ.

1. Write a description of proposed ministry and how it relates to the church’s mission.

2. Which need(s) will this ministry address?

3. What is the cost to the church for this ministry?

4. What will this ministry mean to the church in future years?

5. For whom is this ministry planned?

6. Is there a budget alternative?

7. Estimate expenditures per month (cash flow).

6. What are the results that we expect to accomplish?

Jan. Feb. Mar. Apr. May June July Aug. Sept. Oct. Nov Dec. Total

Joshua 3:5 Joshua told the people, Consecrate yourselves, because the Lord will do wonders among you tomorrow.

5

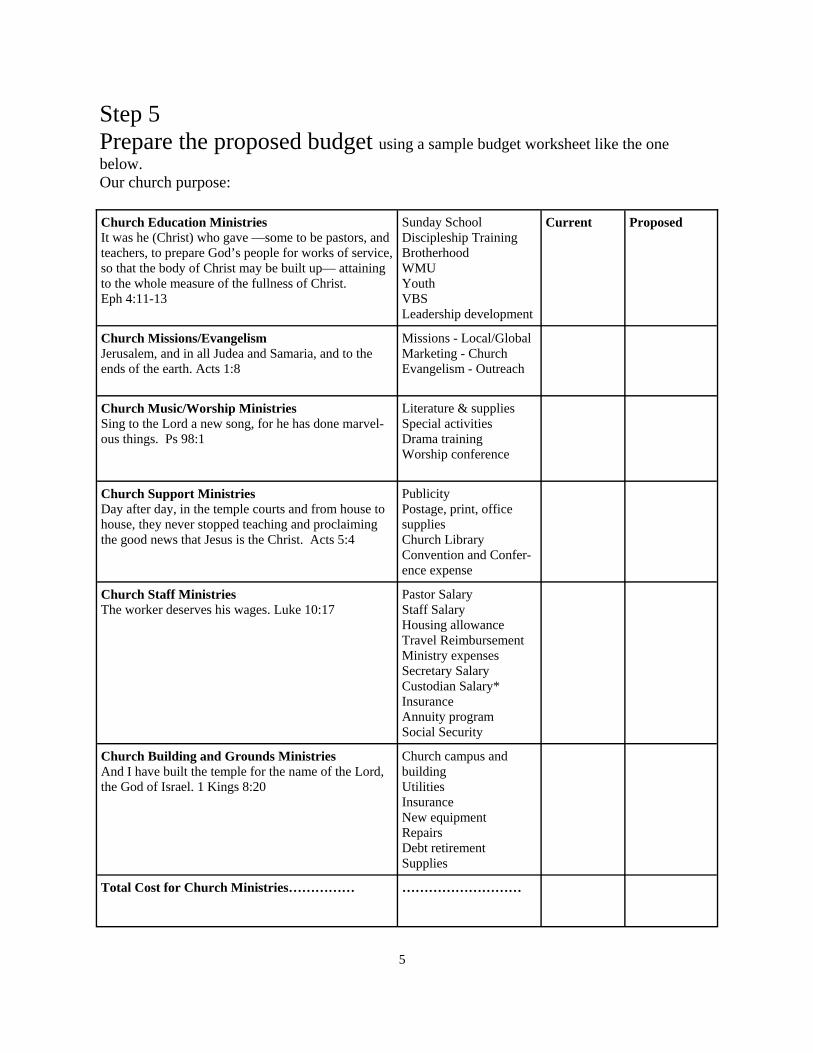

Step 5 Prepare the proposed budget using a sample budget worksheet like the one below. Our church purpose:

Church Education Ministries It was he (Christ) who gave —some to be pastors, and teachers, to prepare God’s people for works of service, so that the body of Christ may be built up— attaining to the whole measure of the fullness of Christ. Eph 4:11-13

Sunday School Discipleship Training Brotherhood WMU Youth VBS Leadership development

Current Proposed

Church Missions/Evangelism Jerusalem, and in all Judea and Samaria, and to the ends of the earth. Acts 1:8

Missions - Local/Global Marketing - Church Evangelism - Outreach

Church Music/Worship Ministries Sing to the Lord a new song, for he has done marvel-ous things. Ps 98:1

Literature & supplies Special activities Drama training Worship conference

Church Support Ministries Day after day, in the temple courts and from house to house, they never stopped teaching and proclaiming the good news that Jesus is the Christ. Acts 5:4

Publicity Postage, print, office supplies Church Library Convention and Confer-ence expense

Church Staff Ministries The worker deserves his wages. Luke 10:17

Pastor Salary Staff Salary Housing allowance Travel Reimbursement Ministry expenses Secretary Salary Custodian Salary* Insurance Annuity program Social Security

Church Building and Grounds Ministries And I have built the temple for the name of the Lord, the God of Israel. 1 Kings 8:20

Church campus and building Utilities Insurance New equipment Repairs Debt retirement Supplies

Total Cost for Church Ministries…………… ………………………

6

Step 6 Celebrate the budget with the church finance committee with the church council with the church The finance committee has prepared the budget to highlight church ministries. It is the ministries that are proposed, not just budget items. The interpretation of the budget will communicate the purpose of the ministries and how they will help fulfill the Great Commission. Celebrate highlights from the previous year’s ministries by using various methods to communicate this story: Video taped messages PowerPoint slides Brochures emphasizing current programs and unmet needs Testimonies from members telling the story of a ministry and its results Highlight mission trips, community ministries and people whose lives were touched

personally by the church’s faithfulness

Step 7 Adopt the budget The budget is presented to the members by recommendation of the finance committee. Encourage questions and discussion; this provides for a healthy situation. Everyone who prepared a ministry proposal should be present to discuss that ministry when called on. It would be good for the finance committee to serve as a panel for the presentation and discussion. Demonstrate by using the church’s giving profile how giving has increased. Ask the congregation to pray over the budget; provide time for questions. Ask the congregation to return at a later date to approve the budget.

Step 8 Report on ministry progress Month-by-month financial support is necessary for a healthy ministry program. Therefore, regular communication with church members is essential to report on progress toward ministry goals as well account for expenditures use both innovative as well as traditional approaches to report ministry progress, including testimonies, PowerPoint, video presentations and brochures.

Step 9 Evaluate Ask, “How did the year go?”

7

Building of the church finance team Attributes of finance team members Elected by the church. Understand Biblical stewardship. Practice Biblical stewardship Have a genuine concern for the well-being of the church. Be willing to be trained. Be faithful in completing assignments. Be willing to use effective techniques to communicate church ministries and budget. The church finance team should focus on four important areas. 1. Stewardship education a) Recommend stewardship features on the annual calendar. b) Provide seminars to help church members develop money management skills. c) Provide seminars to teach Biblical stewardship principles. 2. Church budget a) Follow the process outlined in this booklet. b) Promote church ministries and budget as helping the church to be faithful to its purpose/mission. 3. Good accounting practices a) Provide good accounting of all funds. b) Create trust in the church’s handling of its resources. 4. Estate planning a) Promote estate giving to church. b) Plan and conduct an estate planning emphasis. c) Formulate a policy on receiving gifts. d) Become familiar with charitable giving methods. e) Seek to establish an endowment for your church. g) Evaluate capital needs of the church. The team’s purpose is to increase revenue streams into the church budget so that the church can be faithful to its mission and purpose.

2010 Budget Analysis 15% Education Ministries 13% Evangelism Ministries 5% Music & Worship Ministries 2% Support Ministries 40% Pastoral Ministries 10% Building and Grounds Ministries 15% Debt Retirement

8

Suggestions for the Budget and Finance Committee

1. The counting committee chairman should sort out the money - stacks of bills by denomination, coins and checks. Then count the money. Each member should sign the register tapes and deposit slips verifying the deposit. Designate one individual to lock the bag in the presence of at least two or more committee members. Establish a secure location in the church where the keys are kept. Establish a committee –not a single individual to place church offerings in bank deposit bag. (Many churches use the usher committee to handle this responsibility.)

2. Make arrangements with your bank to place the locked bag in the bank night depository on Sunday for safekeeping. (Never send money home with an individual.) Rotate among committee members the responsibility for taking the bag to the bank weekly. The next business day a member of the counting committee goes to the bank to verify the deposit.

3. Establish a policy to ensure that people who handle the church’s money are different from the ones charged with spending and writing checks.

4. Establish a policy requiring at least two signatures on checks. Make it a practice to give this responsibility to people who are thoroughly familiar with the budget and church spending policies. Never assign this responsibility to an individual who would be inclined to sign without questioning. Who can sign checks:

One church staff member Two or three other individuals who are members of the budget or finance

committee. This procedure, allows the church to have at least two signatures even if some persons are unavailable at the time the checks are written.

Consider establishing on-line banking. It will save time and have less errors. The bank will help you securely set up this account.

5. Minimize the number of discretionary and designated funds or accounts. Too many such accounts discourage people from giving to a unified budget and may result in needed areas of budget being underfunded. Establish a policy requiring all accounts to be church-approved (http://www.lifeway.com/lwc/files/lwcF_PDF_Hamilton_DesignatedFundManagement.pdf ) this website will give you excellent resources for establishing these funds.

6. At the beginning of the budget year, set up a clearly-stated policy of what is to be done with surplus funds (money given above the budget, or budgeted funds not spent). This policy reaffirms there is accountability and ethical spending habits, leading church members to know the excess funds will be used wisely.

7. Special program offerings (concert, guest speakers) should come through the church account, and a single check cut to the individual or group by the church. Thus the church is aware of the total gifts and givers receive proper credit for their contributions.

8. The IRS now requires certification that none of the funds reported as “contributions” are for services rendered. Stamps denoting “restricted account—not for contribution credit” can be used for checks received by the church where there is value received; such as church supper. If the church is to keep the contribution credit now allowed by IRS, we must conform strictly to IRS regulations. Canceled checks, according to IRS are no longer proof of contributions; the giver must have statement from the church.

9

Designated Funds It is important for a church to have clear policies and procedures for handling designated funds. http://www.lifeway.com/Article/Handling-benevolence-gifts-according-to-IRS-guidelines Maximizing Tax Benefits for Ministers Housing allowance is considered a part of the minister’s salary, and this part is given special tax consideration. The minister must be duly ordained, licensed or commissioned. Other criteria include: Does he administer church ordinances? Does he conduct religious services? Does he have management responsibilities in the church? Is he perceived to be a religious leader by the congregation? Once it is determined he is a minister: The Church must adopt a procedure to identify who will receive the minister’s housing allowance request and who will respond on behalf of the church. Receive a written request from the minister. It is strongly encouraged that the minister submit an annual written housing request. (The minister will identify the amount of the housing allowance and it should be approved by the church.) Provide written response that the request has been accepted and designated. This includes church approval of the request. Non-Taxable Employer Paid Fringe Benefits The church can assist an employee through non-taxable fringe benefits that are usually paid on their behalf to a third party. These benefits must be approved in advance of salary payment. (2010 Church & Clergy Tax Guide pages 200-203) This type of payment includes: Medical insurance Flexible spending arrangement Health reimbursement arrangement Health saving account These amounts should be established in advance by the personnel/ budget committee and if paid correctly can be treated as non-taxable employer provided fringe benefits. (See: IRS Publication 969 Health Saving Accounts or IRS publication 15-B Employer’s Tax Guide to Fringe Benefits.) Accountable Reimbursement Plans An accountable reimbursement plan provides advances or reimbursements of an employee’s ministry expenditures incurred in the performance of their duties. (See: IRS Publication 1828 also see Publication 463.) Requirements that must be followed are: Involves a business connection Requires employee to substantiate expenses incurred (type, place, amount, time & date, ministry

propose-[why] and ministry relationship-[who]) Requires the employee to return any excess amounts within 120 days and all expenses must be

substantiated within 60 days Any plans that meet the above requirements are: Excluded from an employee’s gross income Not required to be reported on the employee’s IRS Form W2 Wage and Tax Statement Exempt from the withholding and payment of wages subject to FICA taxes and income tax

withholdings.

10

Sample Accountable Reimbursement Policy In accordance with IRS regulations 1.162-17 and 1.274-5T(f) the __________________ Baptist Church hereby establishes an accountable reimbursement policy for all ministers and employees with the following terms and conditions: 1. The minister or employee will be reimbursed by the church for ordinary, necessary,

reasonable, substantiated, authorized, and ministry-related expenses incurred on behalf of the church. Subject to budget limitations, such expenses will include:

Travel Expense: Ministry travel away from home including travel, lodging and

meals on overnight ministry trips. Entertainment/Hospitality Expense: Reimbursed only if ministry connection

requirement is met. Transportation Expense: Mileage reimbursement for local ministry use of personal

automobile, up to the current IRS standard mileage rate. Training Expense: Convention, conference and ministry related workshop fees. Educational Expense: Reimbursed only if otherwise qualified as an itemized

deduction and in accordance with IRS guidelines. Subscriptions Expense: Periodicals, books and tapes will be reimbursed if ministry

or employment related and ownership does not transfer to employee. Cell Phone Expense: Reimbursed only if required for the convenience of the church

and as a condition of employment. In accordance with IRS guidelines, any personal call should be identified and reimbursed to the church.

2. The minister or employee will substantiate each allowable expense in writing within 60

days including the following documentation with the original receipt: What: Itemized amount requested for reimbursement When: Time/Date of expense Where: Place/Location of expense Why: Ministry purpose/description of expense Who: Name and ministry relationship (meals and entertainment expense)

3. The minister of employee will return to the church any amount received (advances) in

excess of the substantiated expenses within 120 days of receipt. Under this accountable reimbursement plan, the church will not report any properly substantiated reimbursement payments as income on any Form W-2. Additionally, any employee should not report properly reimbursed amounts as income on Form 1040. (Refer to IRS Publication 463, Travel, Entertainment, Gift, and Car Expenses, for more information.)

11

Southern Baptist Annual Compensation Study This biennial compensation study is a joint project of state Baptist Conventions, GuideStone Financial Resources and LifeWay Christian Resources. Compensation and congregational data is collected anonymously from ministers and office/custodial personnel of Southern Baptist churches and church-type missions. Comparison reports are based on compensation for nearly 13,000 respondents from all 50 states. While this data is made available with respect for the autonomy of each local church, the information can help a church be objective in considering appropriate staff compensation. Advantages of using this salary comparison study:

It is uniquely Southern Baptist. All responses included in the survey are for ministers and employees of SBC churches.

It is free. The participating state conventions, LifeWay Christian Resources and GuideStone Financial Resources pay all costs.

All reports are available on the internet.

Most compensation studies provide reports based on attendance, budget, etc. The customized report option is unique to the SBC study. This makes it possible to get compensation data based on churches most like your own by combining criteria.

Every survey form received is evaluated for valid, usable data and over 20 data integrity filters are used on the data before study results are compiled.

Information on this survey can be obtained by contacting your local state convention office or

obtained directly at http://compstudy.lifeway.com.

12

Financial Support Worksheet A. Ministry Related Expenses (not compensation)

1. Automobile $ ______________________________

2. Conventions/conferences $ ______________________________

3. Books, periodicals, CDs $ ______________________________

4. Continuing education $ ______________________________

5. Hospitality $ ______________________________

Total Reimbursement Funds $ ______________________________

B. Employee Benefits (not Compensation)

1. Life and Health Coverage $ ______________________________

Medical $ ______________________________

Disability $ ______________________________

Term Life $ ______________________________

Personal Accident $ ______________________________

2. 403 (b) (9) Retirement contribution $ ______________________________

3. Social Security offset $ ______________________________

Total Benefits $ ______________________________

C. Personal Income

1. Cash Pay $ ______________________________

2. Housing Allowance $ ______________________________

Total Personal Income $ ______________________________

Worksheet taken from GuideStone Financial Services book, “Planning Financial Support Workbook”

13

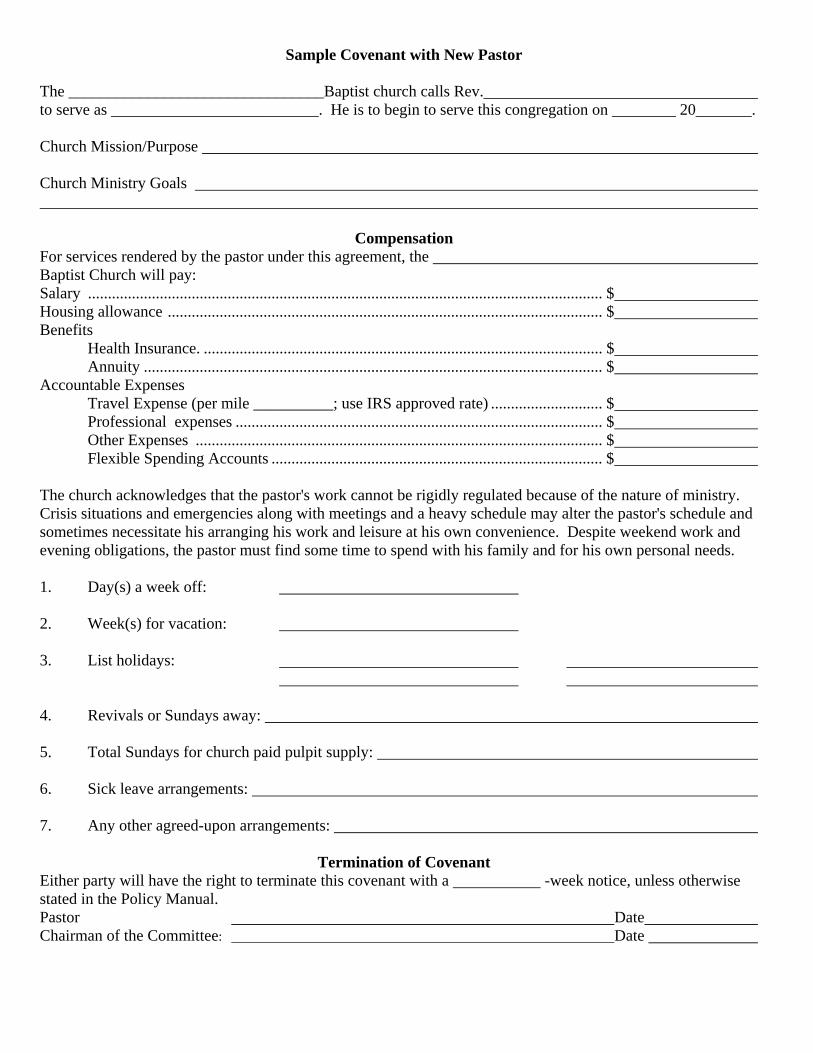

Sample Covenant with New Pastor

The ________________________________Baptist church calls Rev. to serve as __________________________. He is to begin to serve this congregation on ________ 20_______. Church Mission/Purpose Church Ministry Goals

Compensation For services rendered by the pastor under this agreement, the Baptist Church will pay: Salary ................................................................................................................................. $ Housing allowance ............................................................................................................. $ Benefits Health Insurance. .................................................................................................... $ Annuity ................................................................................................................... $ Accountable Expenses Travel Expense (per mile __________; use IRS approved rate) ............................ $ Professional expenses ............................................................................................ $ Other Expenses ...................................................................................................... $ Flexible Spending Accounts ................................................................................... $ The church acknowledges that the pastor's work cannot be rigidly regulated because of the nature of ministry. Crisis situations and emergencies along with meetings and a heavy schedule may alter the pastor's schedule and sometimes necessitate his arranging his work and leisure at his own convenience. Despite weekend work and evening obligations, the pastor must find some time to spend with his family and for his own personal needs. 1. Day(s) a week off: 2. Week(s) for vacation: 3. List holidays:

4. Revivals or Sundays away: 5. Total Sundays for church paid pulpit supply: 6. Sick leave arrangements: 7. Any other agreed-upon arrangements:

Termination of Covenant

Either party will have the right to terminate this covenant with a -week notice, unless otherwise stated in the Policy Manual. Pastor Date Chairman of the Committee: Date

14