Services productivity growth in Australia, Europe and US Robert Inklaar Groningen Growth and...

21

Services productivity growth in Australia, Europe and US Robert Inklaar Groningen Growth and Development Centre, University of Groningen and The Conference Board with Bart van Ark and Marcel Timmer

-

date post

20-Dec-2015 -

Category

Documents

-

view

213 -

download

0

Transcript of Services productivity growth in Australia, Europe and US Robert Inklaar Groningen Growth and...

Services productivity growth in Australia, Europe and US

Robert InklaarGroningen Growth and Development Centre,

University of Groningen andThe Conference Board

with Bart van Ark and Marcel Timmer

Background: analysis

Different growth pattern since 1995 US, Australia faster GDP growth Europe has slowed down

Mainly diverging productivity growth But where is it coming from?

Need industry data Productivity growth and levels Investment in new technology (ICT)

Background: data

Results based on preliminary version of EUKLEMS database

Full industry productivity database; growth & levels; 1970-2004; 30-70 industries; Europe, US, and others

Big EU-funded project 15 institutions, GGDC leading

15 March 2007 first public release See www.euklems.net for details Australia will be added later

Current results prepared for Economic Policy

Main findings

Productivity growth accelerated after 1995 in Anglo-Saxon countries

Market services main source of strength Growth in Europe slowed down, in

particular in services ICT investment & complementary

intangibles explain part Competition and regulation further

candidates

Surge in services productivity growth main post-1995 story

Industry contributions to market economy labour productivity growth, 1987-2004

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1987-1995 1995-2004 1987-1995 1995-2004 1987-1995 1995-2003

US EU-11 Australia

ICT production Goods-producing industries Market services Reallocation of hours

First suspect: ICT investment

Perform industry growth accounting exercise:

Aqvkvkvy LN

KI

K NI

Labour productivity growth

ICT capital deepening

Non-ICT capital deepening

TFP growth

Labour composition change

Labour productivity growth and the contribution of ICT capital in market services, 1995-2004

-1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5 3.0

ESPITA

GERDNKFRAAUTBELNLDSWE

FINUK

EU11US

AUS

ICT contribution Other labour productivity

ICT is part of the story

But ICT may be more important

General purpose technology => complementary investments

For ICT mostly intangible, time-consuming mismeasured in National Accounts?

Firm research & case studies find support So far less from industry-level

Follow method of Brynjolfsson & Hitt (2003, REStat)

Main idea: increase time horizon

11,1, ttIK

tt KvA I

1010,10, ttIK

tt KvA I

Long-term effect of ICT is twice as large as short-term effect

Productive effect of ICT relative to user cost of ICT capital, 1-year to 10-year time horizon

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1 2 3 4 5 6 7 8 9 10

95% Lower bound Point estimate 95% Upper bound

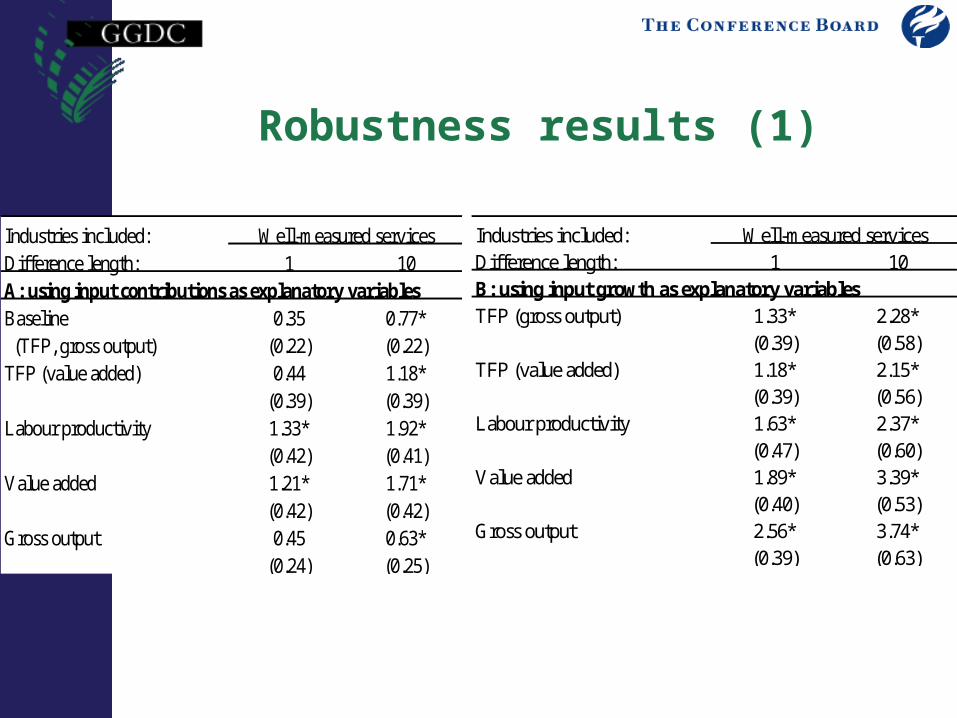

Robustness checks (1)

Works only for relatively measured industries Excludes finance, business services

Other production function specifications (more general) Show even higher returns (even short-term

excess returns) All show upward trend in coefficients All show excess returns in the long-run

Industries included:Difference length: 1 10A: using input contributions as explanatory variablesBaseline 0.35 0.77* (TFP, gross output) (0.22) (0.22)TFP (value added) 0.44 1.18*

(0.39) (0.39)Labour productivity 1.33* 1.92*

(0.42) (0.41)Value added 1.21* 1.71*

(0.42) (0.42)Gross output 0.45 0.63*

(0.24) (0.25)

Well-measured services Industries included:Difference length: 1 10B: using input growth as explanatory variablesTFP (gross output) 1.33* 2.28*

(0.39) (0.58)TFP (value added) 1.18* 2.15*

(0.39) (0.56)Labour productivity 1.63* 2.37*

(0.47) (0.60)Value added 1.89* 3.39*

(0.40) (0.53)Gross output 2.56* 3.74*

(0.39) (0.63)

Well-measured services

Robustness results (1)

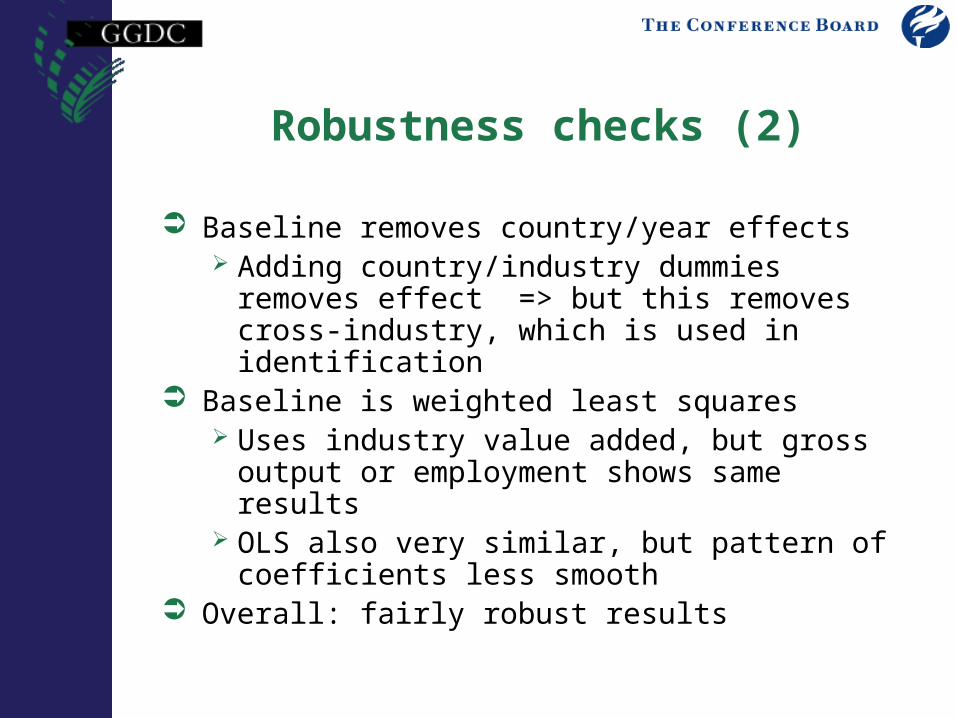

Robustness checks (2)

Baseline removes country/year effects Adding country/industry dummies removes

effect => but this removes cross-industry, which is used in identification

Baseline is weighted least squares Uses industry value added, but gross

output or employment shows same results OLS also very similar, but pattern of

coefficients less smooth Overall: fairly robust results

Robustness results (2)Industries included:Difference length: 1 10Panel A: country, industry and year controlsBaseline 0.35 0.77* (WLS, value added weights, country/year dummies) (0.22) (0.22)WLS, country dummies -0.22 0.28

(0.23) (0.29)WLS, country/industry dummies -0.84* -1.01*

(0.32) (0.30)WLS, country/industry/year dummies -1.32* -1.71*

(0.36) (0.36)Panel B: weightingOLS, country/year dummies 0.32 0.77*

(0.18) (0.18)WLS, hours weights, country/year dummies 0.40 1.00*

(0.30) (0.23)WLS, gross output weights, country/year dummies 0.46 0.88*

(0.24) (0.26)

Well-measured industries

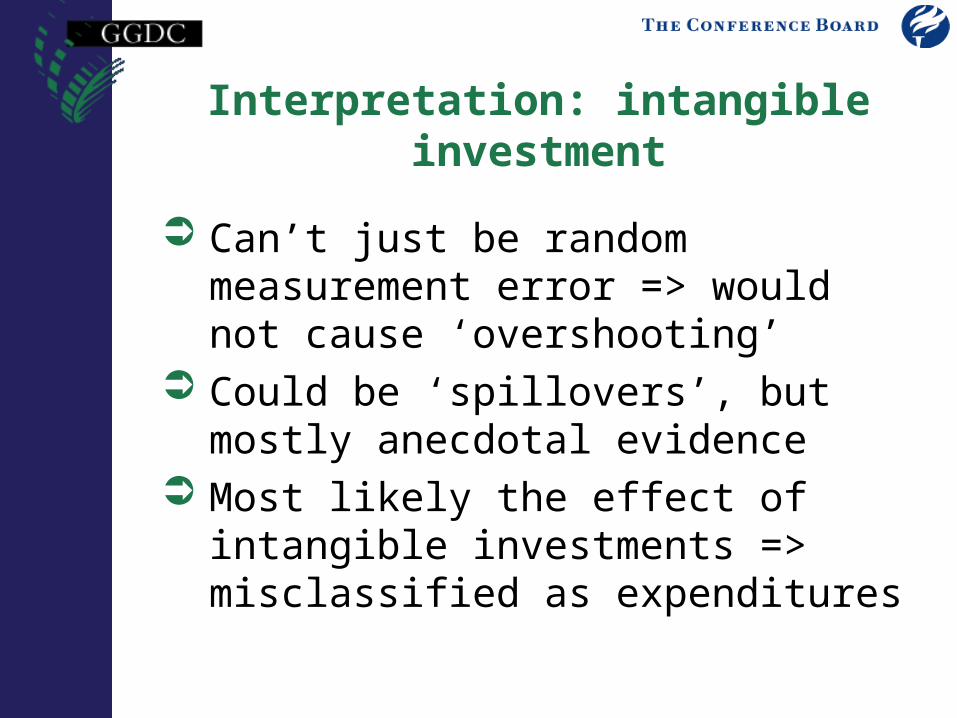

Interpretation: intangible investment

Can’t just be random measurement error => would not cause ‘overshooting’

Could be ‘spillovers’, but mostly anecdotal evidence

Most likely the effect of intangible investments => misclassified as expenditures

However: this does not close the gap

Larger long-term effect of ICT is found in all countries* Even effect in US is the same ICT-related intangible investment

then explains only part (0.4%)

So what about convergence to frontier?

* This does not yet include Australia: need the KLEMS data for that

Convergence in only the minority of countries for total services

TFP level in market services in 1995 and 2004, US=100

60

70

80

90

100

110

120

DNK BEL NLD AUS FIN GBR AUT SWE ITA ESP FRA GER

1995 2004

Convergence

Divergence

But convergence is an industry story

Figure 9, Number of market services industries where productivity was at the frontier or converged to the frontier between 1995 and 2004

0

1

2

3

4

5

6

7

8

9

FIN US UK NLD SWE AUT DNK DEU BEL FRA ESP ITA

So what does this mean?

Convergence is happening, even in services But not everywhere

Nicoletti & Scarpetta (’03): convergence depends on regulation Confirmed here: more regulation =>

less convergence (correlation -0.6)

Competition is key (probably)

Regulation story is complex Regulatory burden can be very

industry-specific (retail case study) Competition is about more than

regulation e.g. need robust competition authority

But still the most plausible explanation for productivity growth differences

Erwin’s Enquiries

Does not include land and inventories Uses an internal rate of return Assumes equal av. wage of self-

employed as employees Has a zero floor of user cost and capital

share