SENIOR ISSUES (B) TASK FORCE - naic.org · Jennifer Hammer Illinois Stephen W ... Doug Ommen Iowa...

112

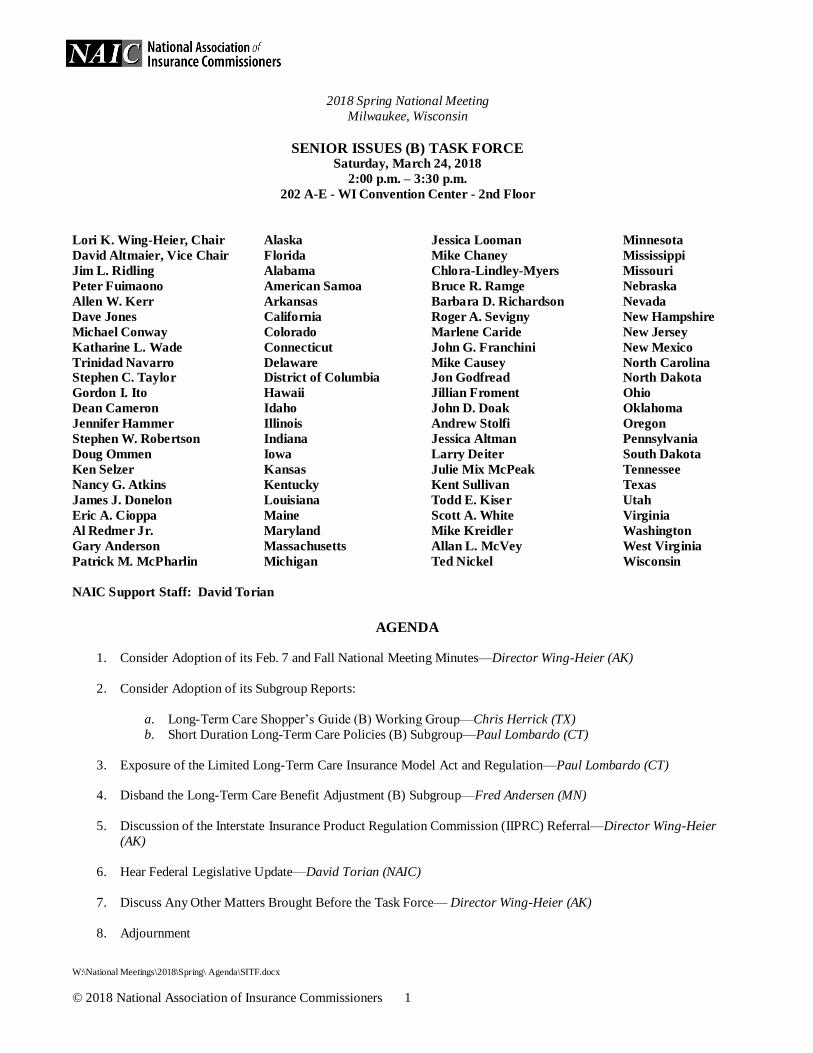

© 2018 National Association of Insurance Commissioners 1 2018 Spring National Meeting Milwaukee, Wisconsin SENIOR ISSUES (B) TASK FORCE Saturday, March 24, 2018 2:00 p.m. – 3:30 p.m. 202 A-E - WI Convention Center - 2nd Floor Lori K. Wing-Heier, Chair Alaska David Altmaier, Vice Chair Florida Jim L. Ridling Alabama Peter Fuimaono American Samoa Allen W. Kerr Arkansas Dave Jones California Michael Conway Colorado Katharine L. Wade Connecticut Trinidad Navarro Delaware Stephen C. Taylor District of Columbia Gordon I. Ito Hawaii Dean Cameron Idaho Jennifer Hammer Illinois Stephen W. Robertson Indiana Doug Ommen Iowa Ken Selzer Kansas Nancy G. Atkins Kentucky James J. Donelon Louisiana Eric A. Cioppa Maine Al Redmer Jr. Maryland Gary Anderson Massachusetts Patrick M. McPharlin Michigan Jessica Looman Minnesota Mike Chaney Mississippi Chlora-Lindley-Myers Missouri Bruce R. Ramge Nebraska Barbara D. Richardson Nevada Roger A. Sevigny New Hampshire Marlene Caride New Jersey John G. Franchini New Mexico Mike Causey North Carolina Jon Godfread North Dakota Jillian Froment Ohio John D. Doak Oklahoma Andrew Stolfi Oregon Jessica Altman Pennsylvania Larry Deiter South Dakota Julie Mix McPeak Tennessee Kent Sullivan Texas Todd E. Kiser Utah Scott A. White Virginia Mike Kreidler Washington Allan L. McVey West Virginia Ted Nickel Wisconsin NAIC Support Staff: David Torian AGENDA 1. Consider Adoption of its Feb. 7 and Fall National Meeting Minutes—Director Wing-Heier (AK) 2. Consider Adoption of its Subgroup Reports: a. Long- Term Care Shopper’s Guide (B) Working Group—Chris Herrick (TX) b. Short Duration Long-Term Care Policies (B) Subgroup—Paul Lombardo (CT) 3. Exposure of the Limited Long-Term Care Insurance Model Act and Regulation—Paul Lombardo (CT) 4. Disband the Long-Term Care Benefit Adjustment (B) Subgroup—Fred Andersen (MN) 5. Discussion of the Interstate Insurance Product Regulation Commission (IIPRC) Referral—Director Wing-Heier (AK) 6. Hear Federal Legislative Update—David Torian (NAIC) 7. Discuss Any Other Matters Brought Before the Task Force— Director Wing-Heier (AK) 8. Adjournment W:\National Meetings\2018\Spring\ Agenda\SITF.docx

Transcript of SENIOR ISSUES (B) TASK FORCE - naic.org · Jennifer Hammer Illinois Stephen W ... Doug Ommen Iowa...

© 2018 National Association of Insurance Commissioners 1

2018 Spring National Meeting

Milwaukee, Wisconsin

SENIOR ISSUES (B) TASK FORCE Saturday, March 24, 2018

2:00 p.m. – 3:30 p.m.

202 A-E - WI Convention Center - 2nd Floor

Lori K. Wing-Heier, Chair Alaska

David Altmaier, Vice Chair Florida

Jim L. Ridling Alabama

Peter Fuimaono American Samoa

Allen W. Kerr Arkansas

Dave Jones California

Michael Conway Colorado

Katharine L. Wade Connecticut

Trinidad Navarro Delaware Stephen C. Taylor District of Columbia

Gordon I. Ito Hawaii

Dean Cameron Idaho

Jennifer Hammer Illinois

Stephen W. Robertson Indiana

Doug Ommen Iowa

Ken Selzer Kansas

Nancy G. Atkins Kentucky

James J. Donelon Louisiana

Eric A. Cioppa Maine

Al Redmer Jr. Maryland

Gary Anderson Massachusetts

Patrick M. McPharlin Michigan

Jessica Looman Minnesota

Mike Chaney Mississippi

Chlora-Lindley-Myers Missouri

Bruce R. Ramge Nebraska

Barbara D. Richardson Nevada

Roger A. Sevigny New Hampshire

Marlene Caride New Jersey

John G. Franchini New Mexico

Mike Causey North Carolina Jon Godfread North Dakota

Jillian Froment Ohio

John D. Doak Oklahoma

Andrew Stolfi Oregon

Jessica Altman Pennsylvania

Larry Deiter South Dakota

Julie Mix McPeak Tennessee

Kent Sullivan Texas

Todd E. Kiser Utah

Scott A. White Virginia

Mike Kreidler Washington

Allan L. McVey West Virginia

Ted Nickel Wisconsin

NAIC Support Staff: David Torian

AGENDA

1. Consider Adoption of its Feb. 7 and Fall National Meeting Minutes—Director Wing-Heier (AK)

2. Consider Adoption of its Subgroup Reports:

a. Long-Term Care Shopper’s Guide (B) Working Group—Chris Herrick (TX)

b. Short Duration Long-Term Care Policies (B) Subgroup—Paul Lombardo (CT)

3. Exposure of the Limited Long-Term Care Insurance Model Act and Regulation—Paul Lombardo (CT)

4. Disband the Long-Term Care Benefit Adjustment (B) Subgroup—Fred Andersen (MN)

5. Discussion of the Interstate Insurance Product Regulation Commission (IIPRC) Referral—Director Wing-Heier

(AK)

6. Hear Federal Legislative Update—David Torian (NAIC)

7. Discuss Any Other Matters Brought Before the Task Force— Director Wing-Heier (AK)

8. Adjournment

W:\National Meetings\2018\Spring\ Agenda\SITF.docx

Agenda Item #1

Consider Adoption of the Feb. 7 and Fall National Meeting

Minutes

Draft 2/14/18

Senior Issues (B) Task Force

Conference Call

February 7, 2018

The Senior Issues (B) Task Force met via conference call Feb. 7, 2018. The following Task Force members participated: Lori

Wing-Heier, Chair (AK); David Altmaier, Vice Chair (FL); Jim L. Ridling represented by Steve Ostlund (AL); Allen W.

Kerr represented by Stephanie Fowler (AR); Dave Jones represented by Tyler McKinney (CA); Katharine L. Wade

represented by Mary Ellen Breault (CT); Trinidad Navarro represented by Susan Jennette (DE); Doug Ommen represented by

Jennifer Lindberg (IA); Dean L. Cameron represented by Kathy McGill (ID); Jennifer Hammer represented by Eric Anderson

(IL); Stephen W. Robertson represented by Karl Knable (IN); Ken Selzer represented by Cindy Hermes (KS); Nancy G.

Atkins represented by Stephanie McGaughey-Bowker (KY); Al Redmer Jr. represented by Joy Hatchette (MD); Eric A.

Cioppa represented by Marti Hooper (ME); Jessica Looman represented by Fred Andersen (MN); Chlora Lindley-Myers

represented by Mary Mealer (MO); Mike Causey represented by Ted Hamby (NC); Jon Godfread represented by Yuri

Venjohn (ND); Bruce R. Ramge represented by Martin Swanson (NE); Roger A. Sevigny represented by Jennifer Patterson

(NH); John G. Franchini represented by Anna Krylova (NM); Barbara D. Richardson represented by Jack Childress (NV);

Jillian Froment represented by Laura Miller (OH); John D. Doak represented by Frank Stone (OK); Julie Mix McPeak

represented by Michael Humphreys (TN); Todd E. Kiser represented by Tanji Northrup (UT); Mike Kreidler represented by

Michael Bryant (WA); and Ted Nickel represented by Jennifer Stegall (WI). Also participating were: Vincent Gosz (AZ);

Debra Peirce (GA); and Andrew Dvorine (SC).

1. Discussed the Task Force’s 2018 Agenda

Director Wing-Heier asked each of the Task Force’s subgroups and working group to explain their plans for 2018.

Ms. Breault, Short Duration Long-Term Care Policies (B) Subgroup chair, said the Subgroup hopes to have the new model

completed shortly.

Mr. Andersen, Long-Term Care Benefit Adjustment (B) Subgroup chair, said no meeting has yet been scheduled for the

Subgroup. Director Wing-Heier said she would work with Mr. Andersen on the Subgroup’s agenda. The Long-Term Care

Shopper’s Guide (B) Working Group chair was not able to be on the call, but Ms. Mealer said the Working Group just began

its work on revising A Shopper’s Guide to Long-Term Care Insurance and plans to complete its work by the Fall National

Meeting.

Director Wing-Heier said she plans to speak with Acting Commissioner Jessica Altman (PA), the former chair of the Long-

Term Care Innovation (B) Subgroup, about the work completed by the Subgroup and the third workstream the Subgroup

planned to examine—studying regulatory barriers to innovation.

The Long-Term Care Innovation (B) Subgroup has also been instructed to review and consider the referral from the Interstate

Insurance Product Regulation Commission (IIPRC) to the Task Force whether the Long-Term Care Insurance Model

Regulation (#641) needs to be revised to facilitate a uniform interpretation and/or to clarify the scope and intent of Section

6B(6). Karen Schutter (IIPRC) briefly explained the history of the topic and referral. Ms. Northrup and Bonnie Burns

(California Health Advocates—CHA) both expressed their opposition to the IIPRC provision.

Director Wing-Heier said she that would continue to study the matter further and that the Task Force will discuss it in more

detail on a future call. She said she would speak with Superintendent Elizabeth Kelleher Dwyer (RI) about chairing the Long-Term Care Innovation (B) Subgroup.

Having no further business, the Senior Issues (B) Task Force adjourned.

G:\Health and Life\Long Term Care Insurance\SITF\SITF Minutes 02-07-2018.docx

Senior Issues (B) Task Force

Honolulu, Hawaii

December 2, 2017

The Senior Issues (B) Task Force met in Honolulu, HI, and via conference call Dec. 2, 2017. The following Task Force

members participated: Jessica Altman, Chair, and Alison Beam (PA); David Altmaier, Vice Chair, and Craig Wright (FL);

Lori K. Wing-Heier represented by Jacob Lauten (AK); Jim L. Ridling represented by Steve Ostlund (AL); Allen W. Kerr

represented by Kenneth Ryan James (AR); Leslie R. Hess (AZ); Dave Jones represented by Perry Kupferman (CA);

Marguerite Salazar (CO); Katharine L. Wade represented by Mary Ellen Breault (CT); Stephen C. Taylor represented by

Howard Liebers (DC); Trinidad Navarro represented by Colleen Pawluczyk (DE); Gordon I. Ito represented by Kathleen

Nakasone (HI); Doug Ommen (IA); Dean L. Cameron represented by Elaine Mellon and Wes Trexler (ID); Jennifer Hammer

represented by Michael Chrysler (IL); Stephen W. Robertson represented by Karl Knable (IN); Ken Selzer represented by

Cindy Hermes, Julie Holmes and Craig Van Aalst (KS); Nancy G. Atkins (KY); James J. Donelon represented by Ron

Henderson (LA); Al Redmer Jr. represented by Joy Hatchette (MD); Eric A. Cioppa represented by Robert Wake (ME);

Patrick M. McPharlin represented by Kathy Kirby (MI); Jessica Looman represented by Fred Andersen and Candace Gergin

(MN); Mike Chaney represented by Bob Williams (MI); Chlora Lindley-Myers, Mary Mealer, Angela Nelson and Molly

White (MO); Mike Causey represented by Ted Hamby (NC); Jon Godfread represented by Ed Moody (ND); Bruce R. Ramge

represented by Matt Holman and Martin Swanson (NE); Roger A Sevigny represented by Mike Wilkey (NH); Jillian Froment

represented by Tynesia Dorsey and Laura Miller (OH); John D. Doak represented by Mike Rhoads and Frank Stone (OK);

Larry Deiter represented by Melissa Klemann (SD); Julie Mix McPeak represented by Brian Hoffmeister (TN); Kevin Brady

represented by Doug Danzeiser, Jan Graeber and Carol Lo (TX); Todd E. Kiser represented by Nancy Askerlund and Tomasz

Serbinowski (UT); Jacqueline K. Cunningham represented by Jackie Myers (VA); Mike Kreidler represented by Molly Nollette (WA); and Ted Nickel represented by Jennifer Stegall, Diane Dambach and Sue Ezalarab (WI).

Commissioner Redmer chaired the meeting on behalf of Commissioner Altman, since she was participating via conference

call.

1. Adopted its Nov. 7, Sept. 28 and Summer National Meeting Minutes

The Task Force met Nov. 7, Sept. 28 and Aug. 6. During its Nov. 7 meeting, the Task Force took the following action:

1) appointed the Long-Term Care Shopper’s Guide (B) Working Group; and 2) adopted the Long-Term Care Shopper’s

Guide (B) Working Group’s charge. During its Sept. 28 meeting, the Task Force adopted its 2018 proposed charges.

Mr. Kupferman made a motion, seconded by Mr. Ostlund, to adopt the Task Force’s Nov. 7 (Attachment One), Sept. 28

(Attachment Two) and Aug. 6 minutes (see NAIC Proceedings – Summer 2017, Senior Issues (B) Task Force). The motion

passed.

2. Adopted the Report of the Short Duration Long-Term Care Policies (B) Subgroup

Ms. Breault reported that the Short Duration Long-Term Care Policies (B) Subgroup met Nov. 15, Oct. 25, Oct. 4, Sept. 13

and Aug. 16. She said the Subgroup, during these calls, completed a section-by-section review of the Long-Term Care

Insurance Model Act (#640) and continued a section-by-section review of the Long-Term Care Insurance Model Regulation

(#641) as it moves forward to developing a model to address short duration long-term care (LTC) policies. The Subgroup is

charged with creating a model to address short-term duration policies that are excluded from Model #640 and Model #641

but do not quite fit under the Accident and Sickness Insurance Minimum Standards Model Act (#170) and the Model Regulation to Implement the Accident and Sickness Insurance Minimum Standards Model Act (#171).

Ms. Breault made a motion, seconded by Mr. Henderson, to adopt the report of the Short Duration Long-Term Care Policies

(B) Subgroup, including its Nov. 15 (Attachment Three), Oct. 25 (Attachment Four), Oct. 4 (Attachment Five), Sept. 13

(Attachment Six) and Aug. 16 (Attachment Seven) minutes. The motion passed.

3. Adopted the Actuarial Analysis Report

Mr. Kupferman explained that at the Summer National Meeting, the Senior Issues (B) Task Force agreed to accept a referral

from the Interstate Insurance Product Regulation Commission (IIPRC) to consider whether Model #641 may need revisions

to facilitate a uniform interpretation and/or to clarify the scope and intent of Section 6B(6), a provision for a limitation or

exclusion for “expenses for services or items available or paid under another long-term care insurance or health insurance

policy.” Mr. Kupferman explained that the Long-Term Care Actuarial (B) Working Group and the Long-Term Care Pricing

(B) Subgroup agreed to develop an actuarial analysis report prior to the referral going to the Long-Term Care Innovation (B) Subgroup for a full review.

Mr. Kupferman said the actuarial report concluded that Section 6B(6) does allow a long-term care (LTC) policy form to

include a non-duplication of benefit provision (NDBP) language. However, there are policy and actuarial issues that should

be considered when determining whether to include NDBP language in an LTC policy form and the impact of such a

provision, if any, on pricing. He said there was not one position regarding the impact of an NDBP on pricing a LTC policy

form that will apply in all situations. He said the report acknowledges that there are a number of factors affecting the actuarial

analysis of an NDBP subject to multiple variables and demographic considerations, including: 1) impact on consumer

behavior and insurer sales practices; 2) lifetime limits relative to the expected claim continuance; 3) the relationship between

the cost of LTC services or an LTC facility and the maximum benefits available under the policy form; and 4) inflation

protection level, if any, and its impact on the probability that the LTC benefits exceed the cost of care under the policy form.

Mr. Kupferman made a motion, seconded by Mr. Ostlund, to adopt the actuarial analysis report of the Long-Term Care

Actuarial (B) Working Group and the Long-Term Care Pricing (B) Subgroup on the IIPRC referral (Attachment Eight)

4. Adopted a Motion to Refer to the Long-Term Care Innovation (B) Subgroup the Actuarial Analysis Report

Mr. Kupferman said that the actuarial analysis report also included the following recommendation: that the Task Force

recommend to the IIPRC that the sale of any additional policies containing NDBP language should never result in the total

amount of coverage under all policies issued to the individual to exceed the highest level of coverage (daily, monthly,

lifetime) approved for sale on currently approved policy forms, since such rates and benefit levels never received approval.

The Task Force agreed that the Long Term Care Innovation (B) Subgroup should consider this recommendation in particular when it considers the IIPRC referral.

Ms. Stegall made a motion, seconded by Mr. Ostlund, to refer to the Long Term Care Innovations Subgroup for its

consideration the actuarial analysis report, including in particular, the recommendation contained in the report that the sale of

any additional policies containing NDBP language should never result in the total amount of coverage under all policies

issued to the individual to exceed the highest level of coverage (daily, monthly, lifetime) approved for sale on currently

approved policy forms, since such rates and benefit levels never received approval. The motion passed.

5. Heard a Federal Legislative Update

Jennifer Cook (NAIC) gave an update on federal legislative matters. She said the U.S. Congress is close to passing legislation

to reform the U.S. tax code. She said the U.S. House of Representatives and U.S. Senate have passed separate versions of the

bill. The House is set to vote on a motion to go to conference on the tax bills on Dec. 4. The Senate is expected to vote on a

similar measure soon after.

According to the Congressional Budget Office (CBO), the legislation will increase the federal deficit by $1.5 trillion. Per the

Statutory Pay-As-You-Go Act of 2010, which was intended to enforce a rule of budget neutrality on new revenue and direct

spending legislation, the tax bill could trigger $136 billion in automatic cuts to mandatory spending in 2018, including

$25 billion in cuts to the Medicare program.

The deadline to fund the government for 2018 is rapidly approaching. The status of the State Health Insurance Program

(SHIP), and all other federal programs, is unknown. The NAIC is communicating with relevant appropriations staffers in

Congress to track the funding levels for SHIPs. It is unlikely that the SHIPs would be eliminated, but it is unclear where federal spending cuts will occur to offset the projected increases in the federal deficit that would result from the passage of

the tax bill.

Having no further business, the Senior Issues (B) Task Force adjourned.

W:\National Meetings\2017\Fall\TF\SR\SITF Minutes draft.docx

Agenda Item #2

Consider Adoption of the Senior Issues (B) Task Force’s

Subgroups and Working Group Reports

Agenda Item #2a

Consider Adoption of the Long-Term Care Shopper’s

Guide (B) Working Group Report

The Long-Term Care Shopper’s Guide (B) Working Group met via open conference call

on March 12, Feb. 26, Feb. 12 and Jan. 30.

Draft: 3/14/18

Long-Term Care Shopper’s Guide (B) Working Group Conference Call

March 12, 2018

The Long-Term Care Shopper’s Guide (B) Working Group of the Senior Issues (B) Task Force met via conference call

March 12, 2018. The following Working Group members participated: Chris Herrick, Chair (TX); Cindy Hermes, Vice Chair

(KS); Perry Kupferman (CA); Jen Lindberg (IA); Mary Mealer (MO); Anna Krylova (NM); and Tracy Bixler (PA). Also

participating were: Sarah Bailey (AK); Susan Jennette (DE); Allison Variwyk (FL); Stephanie McGaughey-Bowker (KY);

Jan Ludwigson (MN); Ted Hamby (NC); Martin Swanson (NE); Charles Uhl (NJ); Jack Childress (NV); Martin Wojcik

(NY); Tynesia Dorsey (OH); Frank Stone (OK); Jan Graeber (TX); Jaakob Sundberg (UT); and Joylyn Fix (WV).

1. Discussed Revision of the Guide

Mr. Herrick reminded the Working Group of its charge, noting that the A Shopper’s Guide to Long-Term Care Insurance

(Guide) is an educational document and is not meant to endorse or disapprove any service or product. He asked if the

Working Group had any objections to the changes made on its Feb. 26 call. No objections were heard. He asked that

comments be submitted no later than March 28.

The Working Group continued to revise the Guide beginning with the section titled “Do I Need To Buy Long-Term Care

Insurance?” The Working Group agreed with the some of the edits suggested by Bonnie Burns (California Health

Advocates—CHA). The Working Group agreed to delete the sentence referencing the premium of the policy.

The Working Group discussed revising the sentence referencing trusted family members. Wayne Mehlman (American Council of Life Insurers—ACLI) suggested “financial professional” be included along with “family and friends.” Ms. Burns

suggested trusted financial advisor. Ms. Mealer recommended “knowledgeable” instead of “trusted.” Mr. Mehlman agreed.

The Working group continued to discuss different variations and agreed to “family members, a friend, and a trusted and

knowledgeable financial professional.” Ms. Swalwell suggested removing the last sentence in parenthesis. The Working

Group agreed.

The Working Group discussed the boxed entry in the Guide and the suggested edits by Ms. Bixler. Ms. Burns, Ms. Mealer

and Mr. Herrick said they liked the edits. Ms. Burns suggested changing the word “exhaust” back to the original word of

“use.” The Working Group agreed. The Working Group discussed the bullet point: “You don’t want to depend on support

from others.” The Working Group agreed to change that sentence to: “You don’t want to burden family or friends.”

Having no further business, the Long-Term Care Shopper’s Guide (B) Working Group adjourned.

G:\Health and Life\Long Term Care Insurance\Shoppers Guide (B) Working Group\Minutes 03-12-2018.docx

Draft: 3/7/18

Long-Term Care Shopper’s Guide (B) Working Group Conference Call

February 26, 2018

The Long-Term Care Shopper’s Guide (B) Working Group of the Senior Issues (B) Task Force met via conference call

Feb. 26, 2018. The following Working Group members participated: Chris Herrick, Chair (TX); Cindy Hermes, Vice Chair

(KS); Tyler McKinney (CA); Tracy Swalwell (IA); Anna Krylova (NM); and Tracy Bixler (PA). Also participating were:

Mayumi Gabor (AK); Vincent Gosz (AZ); Susan Jennette (DE); Kathy McGill (ID); Eric Anderson (IL); Karl Knable (IN);

Stephanie McGaughey-Bowker (KY); Joy Hatchette (MD); Jan Ludwigson (MN); Mary Wegenast (NC); Yuri Venjohn

(ND); Martin Swanson (NE); Karen McCallister (NH); Charles Uhl (NJ); Martin Wojcak (NY); Tynesia Dorsey (OH); Frank

Stone (OK); Matthew Gendron (RI); Andrew Dvorine (SC); Vickie Trice (TN); Jan Graeber (TX); Jaakob Sundberg (UT);

Katie C. Johnson (VA); Linda Low (WI); and Allan L. McVey (WV).

1. Discussed Revision of the Guide

Mr. Herrick reminded the Working Group of its charge, noting that the A Shopper’s Guide to Long-Term Care Insurance

(Guide) is an educational document and is not meant to endorse or disapprove any service or product. He asked if the

Working Group had any objections to the changes made on its last call. No objections were heard. He asked that comments

be submitted no later than March 7.

The Working Group continued to revise the Guide beginning with the renamed section, “How Might You Pay For Long-

Term Care?” The Working Group agreed to retain suggested edits made by Pennsylvania and Bonnie Burns (California

Health Advocates—CHA), Brenda J. Cude (University of Georgia) and Karrol Kitt (University of Texas at Austin). The Working Group did not edit the Personal Resources language.

The Working Group agreed to delete a large portion of the Medicare section and the Medicare Supplement Insurance section

and include a hyperlink for each term. The Working Group agreed to retain the Medicaid section. The Working Group edited

the title of “Will I Need Long-Term Care?” to “Will I Need or Use Long-Term Care?” The Working Group debated whether

the statistics should remain in bullet form or include an infographic in its place. Mr. Herrick mentioned a web page created

by the Texas Health and Human Service Commission that uses infographics and asked that the link be shared with the

Working Group so it can view the web page. The Working Group agreed to discuss the statistics portion on its next call.

The Working Group agreed to edit the section titled “Do I Need To Buy Long-Term Care Insurance?” by deleting a few

sentences and inserting language to refer the reader to the Personal Assessment language and document.

Having no further business, the Long-Term Care Shopper’s Guide (B) Working Group adjourned.

G:\Health and Life\Long Term Care Insurance\Shoppers Guide (B) Working Group\Minutes 02-26-2018.docx

Draft: 2/27/18

Long-Term Care Shopper’s Guide (B) Working Group Conference Call

February 12, 2018

The Long-Term Care Shopper’s Guide (B) Working Group of the Senior Issues (B) Task Force met via conference call Feb.

12, 2018. The following Working Group members participated: Chris Herrick, Chair (TX); Cindy Hermes, Vice Chair (KS);

Tyler McKinney (CA); Tracy Swalwell (IA); Anna Krylova (NM); Tracy Bixler (PA); and Michael Bryant (WA). Also

participating were: Sarah Bailey (AK); William Lacy (AR); Susan Jennette (DE); Martha Im (HI); Eric Anderson (IL); Joy

Hachette (MD); Jan Ludwigson (MN); Pam Koenig (MT); Martin Swanson (NE); Karen McCallister (NH); Charles Uhl

(NJ); Jack Childress (NV); Martin Wojcik (NY); Tynesia Dorsey (OH); Melissa Klemann (SD); Brian Hoffmeister (TN);

Misty Highnote (TX); Jaakob Sundberg (UT); and Dena Wildman (WI).

1. Discussed Revision of the Guide

Mr. Herrick reminded the Working Group of its charge, noting that the Guide is an educational document and is not meant to

endorse or disapprove any service or product. He asked if the Working Group had any objections to the changes made on its

last call. No objections were heard. The Working Group agreed to postpone edits to the Table of Contents until completion of

the revisions to A Shopper’s Guide to Long-Term Care Insurance (Guide).

The Working Group agreed to edit the section titled “What is Long-Term Care?” The Working Group shortened and

simplified the section and edited the Medicare language. The Working Group debated whether the listing of services

provided and the types of services in this section should be explained in more detail or done later in the Guide. The Working

group agreed to the latter. The Working Group also agreed to change the phrase “home health care” to “home care.”

The Working Group agreed to insert a “Personal Assessment” section in the Guide. The Working Group also agreed to make

minor edits to the section titled “How Much Does Long-Term Care Cost?” The Working Group agreed to rename the section

titled “Who Pays For It?” to “How Might You Pay For Long-Term Care?”

Having no further business, the Long-Term Care Shopper’s Guide (B) Working Group adjourned.

G:\Health and Life\Long Term Care Insurance\Shoppers Guide (B) Working Group\Minutes 02-12-2018.docx

Draft: 2/1/18

Long-Term Care Shopper’s Guide (B) Working Group Conference Call

January 30, 2018

The Long-Term Care Shopper’s Guide (B) Working Group of the Senior Issues (B) Task Force met via conference call

Jan. 30, 2018. The following Working Group members participated: Chris Herrick, Chair (TX); Tyler McKinney (CA);

Jennifer Lindberg (IA); Mary Mealer (MO); Anna Krylova (NM); Tracy Bixler (PA); and Michael Bryant (WA). Also

participating were: Sarah Bailey (AK); William Lacy (AR); Susan Jennette (DE); Howard Matsuura (HI); Eric Anderson

(IL); Tate Flott (KS); Stephanie McGaughey-Bowker (KY); Ron Henderson (LA); Jan Ludwigson (MN); Pam Koenig (MT);

Garlinda Taylor (NC); Yuri Venjohn (ND); Martin Swanson (NE); Karen McCallister (NH); Charles Uhl (NJ); Jack

Childress (NV); Martin Wojcak (NY); Frank Stone (OK); Tracy Bixler (PA); Sarah Neil (RI); Vickie Trice (TN); Jaakob

Sundberg (UT); and Linda Low (WI).

1. Reviewed its Charge

Mr. Herrick informed the Working Group that the goal is to revise A Shopper’s Guide to Long-Term Care Insurance (Guide).

He reminded the Working Group that the Guide is an educational document and is not meant to endorse or disapprove any

service or product. Mr. Herrick said the Working Group plans to meet every other week with the goal of completing the

revision of the Guide by the Fall National Meeting.

2. Discussed Revision of the Guide

Ms. Mealer asked about the guide prepared by the State of Iowa that was distributed to the Working Group. Mr. Herrick said the Iowa guide is simply an example of a type of guide recently distributed by Iowa and illustrates a more interactive type of

guide than the current NAIC Guide. Ms. Mealer, Bonnie Burns (California Health Advocates—CHA) and Karrol Kitt

(University of Texas at Austin) said they liked the simplicity and clarity of the language in the Iowa guide.

Ms. Lindberg asked Mr. Herrick if he had a vision of how the Guide should look. Mr. Herrick said the Guide should have

graphs, hyperlinks and charts where necessary among the textual portions. Mr. Henderson asked about the intended target

audience for the new revised Guide. Mr. Herrick said the Guide targets all parties, from 30-year olds thinking about the

future to older consumers interested in purchasing long-term care insurance (LTCI).

Ms. Burns said the opening paragraph on page 2 of the Guide should be moved before the Table of Contents. Ms. Mealer

agreed but said that the order of the sentences should be moved and that some sentences are not necessary, such as references

to state laws. Ms. Jennette agreed. Ms. Burns said the sentence referencing that states produce their own guides should be

retained. Ms. Lindberg agreed. Ms. Burns suggested a survey of which states produce guides may be helpful. Ms. Koenig

said Montana has put together a spreadsheet of states that produce either LTC shopper’s or rate guides, or both. She said the

spreadsheet was created because Montana is in the process of deciding whether to produce its own guide. The Working

Group agreed to move the section entitled “About This Shopper’s Guide” on page 2 to before the Table of Contents, to delete

redundant sentences and reword certain sentences.

Mr. Herrick said a redline version of the changes made by the Working Group will be available prior to the Working Group’s

next call.

Having no further business, the Long-Term Care Shopper’s Guide (B) Subgroup adjourned. G:\Health and Life\Long Term Care Insurance\LTC Shopper’s Guide (B) Subgroup\Minutes 01-30-2018.docx

Agenda Item #2d

Consider Adoption of the Short Duration Long-Term Care

Policies (B) Subgroup Report

The Short Duration Long-Term Care Policies (B) Subgroup met via open conference call

on March 7, Feb. 14, Jan. 24 and Dec. 13.

Draft: 3/15/18

Short Duration Long-Term Care Policies (B) Subgroup

Conference Call

March 7, 2018

The Short Duration Long-Term Care Policies (B) Subgroup of the Senior Issues (B) Task Force met via conference call

March 7, 2018. The following Subgroup members participated: Mary Ellen Breault, Chair (CT); Tyler McKinney, Vice Chair

(CA); Rebecca Vaughan (IN); Cindy Hermes (KS); Stephanie McGaughey-Bowker (KY); Laura Arp (NE); Anna Krylova

(NM); Mike Rhoads and Frank Stone (OK); Rachel Bowden (TX); Tomasz Serbinowski and Jaakob Sundberg (UT); and

Jennifer Stegall (WI). Also participating were: William Lacy (AR); Jen Lindberg (IA); Jennifer Hammer (IL); Fern Thomas

(MD); Jan Ludwigson (MN); Ted Hamby (NC); Jack Childress (NV); Jeremy Bowllam (NY); Tynesia Dorsey (OH); Andrew

Dvorine (SC); Lorrie Brouse (TN); Yolanda Tennyson (VA); and Dena Wildman (WV).

1. Completed Revisions of Sections of Model #641

a. Section 4—Definitions

Ms. Breault said she had reviewed Section 4 and said all could remain for the new model except for Subsection 4B,

Subsection 4C and Subsection 4D. She asked if the Subgroup had any objection to removing those three subsections. Bonnie

Burns (California Health Advocates—CHA) said she has concerns with removing Subsection 4C and its impact in incidental

benefits. Ms. Breault said the subsection pertains to pricing and not benefits. Ms. Burns asked if states require prior approval

before a company may sell. Ms. Breault and Mr. Stone said their respective state require prior approval before anything can

be sold. The Subgroup agreed to delete Subsection 4B, Subsection 4C and Subsection 4D.

b. Section 5—Policy Definitions

Ms. Breault said the entire section could remain for the new model. The Subgroup agreed.

2. Discussed Outstanding Issues

Ms. Breault said the issues raised regarding Section 6B(4)(c) and Section 30 could be handled in the future if a problem were

to arise. She said these sections have been part of the Long-Term Care Insurance Model Regulation (#641) for quite some

time and there have not been any problems. The Subgroup agreed.

3. Discussed Definitions and Industry Concerns

Ms. Breault said the charge of the Subgroup was to develop a new model act and model regulation to address those

alternative products that do not fit fully within the purview of long-term care insurance (LTCI). She said the point is that the

benefit period, and not the duration, is less than a year and this is totally different from short duration health care. She said

she had reviewed many company websites, broker information and documentation about these short-term or recovery plans.

She said she found they do not fit within a short duration medical care definition but do fit within a type of long-term care.

She said many of the marketing materials and websites compared these products to long-term care and defined long-term care

to be coverage for services for individuals who can no longer perform some or all of the basic activities of daily living

(ADLs) or who have cognitive impairment. These short-term and recovery plans offered use ADLs as a factor, which is not

the case within short duration medical plans. She said “short-term care” is predominately used in the websites and

documentation she had reviewed and that if the benefits are comparable it cannot really be called something different.

Michael Colliflower (Aetna) said Aetna does not sell its recovery plans without filings or approval. He said 30 states have

approved this product; the product he gave to the Subgroup is an example. He said their product is not legally defined as

LTC. He said he has concerns with the new model in terms of unintended consequences and increased price for consumers

due to the increased compliance requirements. Ms. Breault asked what the increased costs are and how they are different than

the requirements in the LTC model regulation. Mr. Colliflower said the training costs due to the additional hours required and

the physical examination and medical records provisions are a couple examples. Ms. Arp said the physical examination and

medical records provisions are in Section 11C(3). Ms. Burns asked how often these policies are sold to those 80 years of age

and older. Richard Waggoner (Aetna) said Aetna sells its policies up to age 89. Ms. Breault asked if the Subgroup objected to

deleting Section 11C(3). Ms. Stegall and Mr. Stone said they support deletion. The Subgroup agreed to delete Section

11C(3).

Ms. Burns raised the issue of agent training and said agents must have good training, especially since they pay for their own training. Ms. Hermes agreed that agents must have good training, and Ms. Breault said the training requirements do not seem

onerous and are comparable to the requirements in Section 9 of the Long-Term Care Insurance Model Act (#640). Mr.

Waggoner said companies bear the burden of training costs for captive agents and other agents bear the cost themselves. Mr.

Colliflower said he does not understand the need for the extra training. He said the current rules, regulations and laws on the

books can stop inappropriate practices and new regulations and rules are not necessary. He said he did not support a

mandated specific time period. Ms. Burns said if agents have the proper training, then state insurance regulators will not need

to exercise those rules and regulations.

Ms. Breault asked how the Subgroup felt about making the training requirements dependent on the state insurance regulator’s

discretion and including a drafting note to Section 9. Ms. Burns opposed it and said the training requirements are not

excessive. Ms. Hermes and Mr. Serbinowski did not oppose it. Mr. Sundberg asked Mr. Colliflower about the agents that sell

LTCI. Mr. Colliflower said their brokers sell a wide variety of products but do not sell LTCI. Ms. Breault asked if there was

any objection from Subgroup members to making Section 9 optional and including a drafting note. The Subgroup agreed to

make Section 9 optional and to include a drafting note.

Ms. Breault said she reviewed the suggestions from industry about the title of the model. She said she found the suggestions

potentially confusing and said the title was not that important. Ms. Arp suggested “limited duration.” Mr. Rhoads said that

may trip up some people and suggested “limited benefit long-term care” or use “recovery” in parenthesis after short-term

care. Ms. Breault said the products in question are not limited to medical care and “recovery” would be confusing. Ms. Burns

and Ms. Vaughan said “short-term care (recovery care)” implies that a consumer gets better and that is not the case most

times. Ms. Breault said “short-term care” is rather prevalent and should be retained.

William Schiffbauer (Schiffbauer Law Office) said that the original purpose of the Subgroup was to create model to address

those products that look like LTC but for a benefit period of less than a year. He said that there were court cases, specifically

a U.S. Supreme Court case, where the title or naming of a law or regulation provides the indication of intent of the drafters.

Ms. Breault suggested placing in the Outline of Coverage Section (Section 31) language that this is limited LTCI and make it

clear this is not traditional LTCI and does not meet the minimum requirement of traditional LTCI. Ms. Arp and Mr. Rhoads

said they liked the term “limited long-term care.” The Subgroup agreed to change “short-term care” in the model act and

model regulation to “limited long-term care” and to include new language in Section 31E(6).

4. Adopted Model Act and Model Regulation

Ms. Breault made a motion, seconded by Mr. Stone, to adopt the new model act and new model regulation and refer the

model to the Senior Issues (B) Task Force for exposure. The motion passed.

Having no further business, the Short Duration Long-Term Care Policies (B) Subgroup adjourned.

G:\Health and Life\Long Term Care Insurance\Short Duration LTC Policies (B) Subgroup\Minutes 03-07-2018.docx

Draft: 3/1/18

Short Duration Long-Term Care Policies (B) Subgroup

Conference Call

February 14, 2018

The Short Duration Long-Term Care Policies (B) Subgroup of the Senior Issues (B) Task Force met via conference call

Feb. 14, 2018. The following Subgroup members participated: Mary Ellen Breault, Chair (CT); Tyler McKinney, Vice Chair

(CA); Karl Knable (IN); Craig VanAalst (KS); Stephanie McGaughey-Bowker (KY); Mary Mealer (MO); Laura Arp (NE);

Karen McAllister (NH); Anna Krylova (NM); Mike Rhoads and Frank Stone (OK); Tracy Bixler (PA); Philip Reyna (TX);

Tomasz Serbinowski and Jaakob Sundberg (UT); and Jennifer Stegall (WI). Also participating were: Mayumi Gabor (AK);

William Lacy (AR); Martha Im (HI); Jennifer Lindberg (IA); Kathy McGill (ID); Mike Chrysler (IL); Rebecca DeLaSalle

(LA); Fern Thomas (MD); Kristi Bohn (MN); Garlinda Taylor (NC); Yuri Venjohn (ND); Charles Uhl (NJ); Barbara D.

Richardson (NV); Jerry Stamoulis (NY); Tynesia Dorsey (OH); Andrew Dvorine (SC); Jeff Smith (SD); Vicki Trice (TN);

and Mike Bryant (WA).

1. Discussed Definitions

The Subgroup discussed the letter submitted by Reserve National Insurance (RNI). Ms. Breault said the Subgroup could

address RNI’s concerns when the Subgroup addresses Section 4—Definitions, stating that the issues raised have been

discussed on previous calls. Mr. Rhoads said it is important to revisit this matter because of the concern of commingling

long-term care (LTC) and health insurance products. He also said the title of the new model should be revised. Ms. Breault

said the title is a lesser issue and can be addressed later. She said she is struggling with the issues raised in the letter and reminded the Subgroup members that they have asked the industry repeatedly to explain the benefit differences, but the

Subgroup has not received any response. Ms. Mealer expressed concerns with the way the new model is being drafted and

that it seems to fall under the Accident and Sickness Insurance Minimum Standards Model Act (#170) and the Model

Regulation to Implement the Accident and Sickness Insurance Minimum Standards Model Act (#171).

Kyle Conrad (RNI) expressed concern with the definition of “short-term care insurance,” stating that it is overly broad and

encroaches on health insurance within the purview of Model #170 and Model #171. Ms. Breault asked Mr. Conrad how it

encroaches on health insurance. Mr. Conrad said benefits that fall under health coverage are subject to specific requirements

and that broad definition could encompass policies not intended. He said he welcomes full disclosure in marketing, the

outline of coverage and other areas. Ms. Mealer said these products really do not fall under the Long-Term Care Insurance

Model Act (#640) or the Long-Term Care Insurance Model Regulation (#641). Ms. Breault said they also really do not fall

under Model #170 and Model #171, either, which is why the Subgroup was appointed and charged with creating a

new model.

William Schiffbauer (Schiffbauer Law Office) said the work on the new model seems to only clarify what is currently in the

marketplace. He said the language in the RNI letter makes the definition of these products clearer. Ms. Arp said the debate

seems to be centered on whether an insurer can or should make people buy a complete benefit package, when they only need

or want recovery coverage. Ms. Breault asked if the Subgroup wants to scrap the work done to date, or to continue and revisit

this when Section 4 is reviewed. Ms. Arp, Ms. Mealer and Mr. Sundberg all said that to scrap the work completed to date

would not be productive. Mr. Schiffbauer agreed to not scrap the work done to date.

Michael Colliflower (Aetna) said Aetna’s recovery care policies are filed as hospital indemnity. Mr. Sundberg said that if the

main component of the policy is hospital indemnity with a small nursing home component, it would fall under this new model. Ms. Mealer said there needs to be clear disclosure of what is and is not included. Ms. Bohn said that if presented with

a product that looks like LTC but called something else, Minnesota would still review it under the LTC parameters.

Mr. Reyna said the discussion seems to be about labels and what something looks like versus what something is called,

noting that the Subgroup must view substance over labels. Bonnie Burns (California Health Advocates—CHA) and Susan

Voss (American Enterprise Group—AEG) agreed with that point of view.

Mr. Serbinowski said the industry must provide examples of the contracts that may or may not be subject to this regulation.

He asked how the Subgroup can work on Section 4 without the requisite knowledge. He said if the industry does not respond,

then the Subgroup should not entertain changing the definition. Ms. Breault agreed and suggested the Subgroup move on to

Section 30—Prompt Payment of Clean Claims.

2. Continued Revisions of Sections of Model #641

a. Section 30—Prompt Payment of Clean Claims

Ms. Breault said she did not see any need for changes to Section 30. The Subgroup agreed.

b. Section 31—Standard Format Outline of Coverage

Ms. Breault said language should be placed in the Outline of Coverage stating that this is not LTC coverage. Ms. Burns

agreed. Mr. Colliflower asked if #11 in the Outline of Coverage is needed. Ms. Breault and Ms. Burns said there is no harm

in retaining the language and having it spelled out. The Subgroup agreed. Ms. Burns said “other organic brain disorders”

should be changed to “other cognitive impairments,” as was done in Section 6B(2). The Subgroup agreed. The Subgroup

agreed to add “State Department of Insurance” to #14 in the Outline of Coverage.

c. Section 32—Penalties

Ms. Breault said this is standard language and did not see any need for changes. The Subgroup agreed.

d. Optional Provision

Ms. Voss said the first two paragraphs of the drafting note are not necessary. The Subgroup agreed. Ms. Breault reminded the

Subgroup of the letter from the National Association of Insurance and Financial Advisors (NAIFA) recommending that the

proposed model not include language addressing the issue of producer compensation arrangements. Ms. Burns expressed

concern with not including such language. Ms. Breault asked the Subgroup whether this provision should remain optional. Ms. Mealer and Mr. Rhoads said the optional provision could be removed. The Subgroup agreed to insert language in the

drafting note indicating the states may refer to Model #641 if the state observes considerable abuses in the marketplace.

e. Appendices

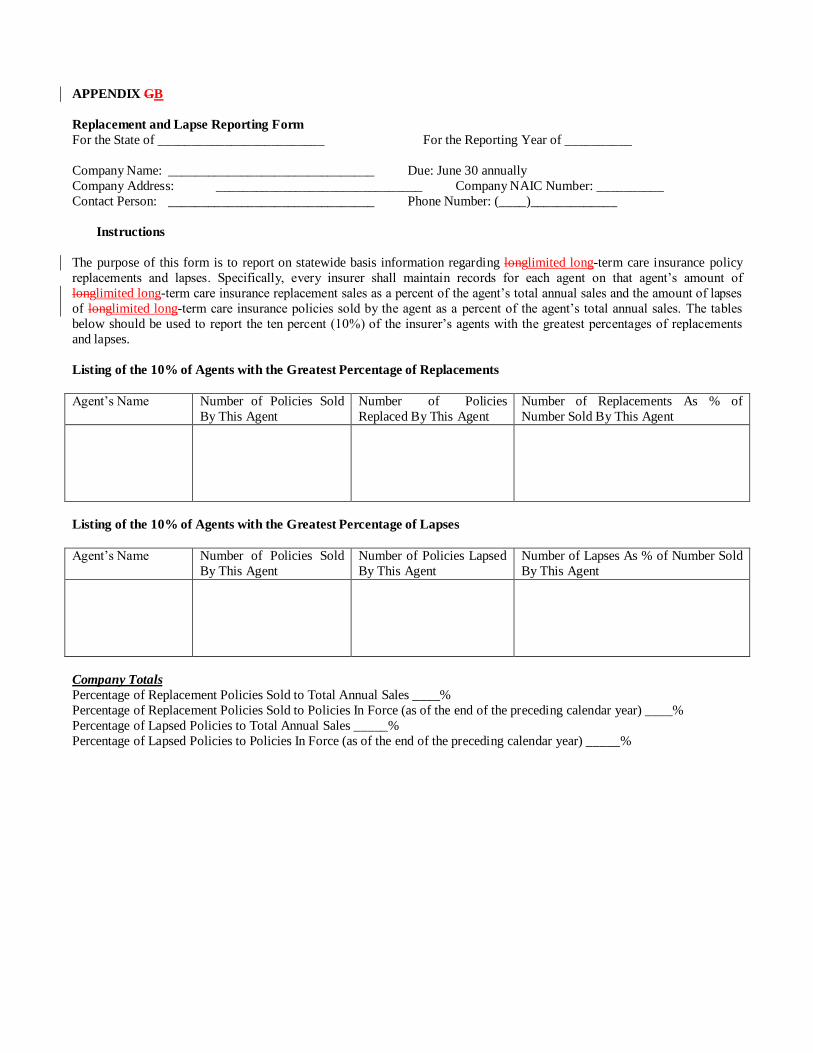

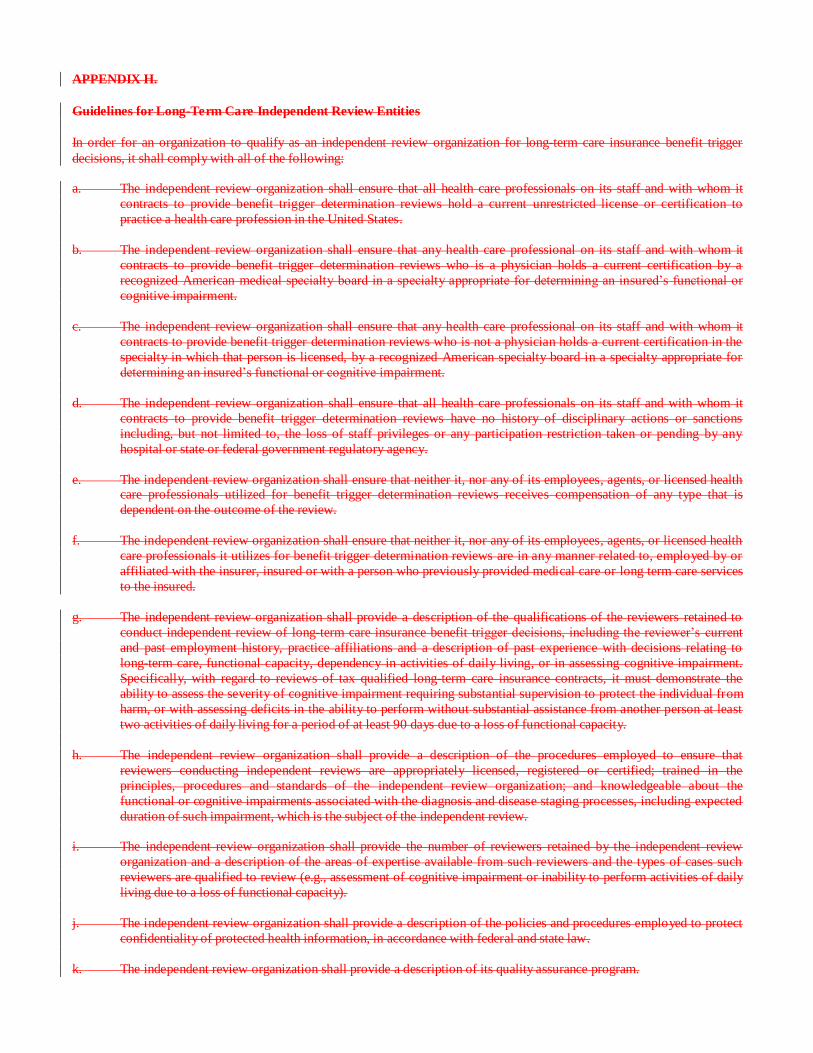

The Subgroup agreed to delete appendices A, B, C, D, E and H. The Subgroup modified Appendix F to remove all language

on contingent nonforfeiture and agreed to retain Appendix G on lapse reporting.

Ms. Breault said the Subgroup will address Section 4 on its next call.

Having no further business, the Short Duration Long-Term Care Policies (B) Subgroup adjourned.

G:\Health and Life\Long Term Care Insurance\Short Duration LTC Policies (B) Subgroup\Minutes 02-14-2018.docx

Draft: 1/30/18

Short Duration Long-Term Care Policies (B) Subgroup

Conference Call

January 24, 2018

The Short Duration Long-Term Care Policies (B) Subgroup of the Senior Issues (B) Task Force met via conference call

Jan. 24, 2018. The following Subgroup members participated: Mary Ellen Breault, Chair (CT); Tyler McKinney, Vice Chair

(CA); John Reilly (FL); Karl Knable (IN); Tate Flott (KS); Stephanie McGaughey-Bowker (KY); Mary Mealer (MO); Laura

Arp (NE); Maureen Belanger (NH); Anna Krylova (NM); Mike Rhoads (OK); Tracy Bixler (PA); Jan Graeber (TX); Jaakob

Sundberg (UT); and Julie Walsh (WI). Also participating were: Sarah Bailey (AK); William Lacy (AR); Martha Im (HI);

Jennifer Lindberg (IA); Kathy McGill (ID); Eric Anderson (IL); Fern Thomas (MD); Jan Ludwigson (MN); Ted Hamby

(NC); Yuri Venjohn (ND); Charles Uhl (NJ); Jack Childress (NV); Jerry Stamoulis (NY); Tynesia Dorsey (OH); Andrew

Dvorine (SC); Brian Hoffmeister (TN); and Mike Bryant (WA).

1. Discussed Changes to Section 10, Section 19 and Section 20 of Model #641

Ms. Breault reminded the Subgroup that on its Dec. 13, 2017 call, the Subgroup agreed to restructure Section 10 and remove

Section 19 of the Long-Term Care Insurance Model Regulation (#641). Ms. Breault asked if there were any comments to the

changes. Michael Colliflower (Aetna) asked about the references to the appendices in the latter part of Section 9. He said he

understood that the Subgroup would address the appendices after completion of the Model Regulation but pointed out that the

Subgroup did agree to remove Appendix B and said that should be reflected in Section 9. The Subgroup agreed.

2. Revisited Sections of Model #641

b. Section 27—Nonforfeiture Benefit Requirement

The Subgroup began with Section 27D. Ms. Breault questioned the need for attained age in the section. Bonnie Burns

(California Health Advocates—CHA) agreed. Mr. Sundberg suggested that it may have been used for graded premiums

where premiums rise until the insured is age 65 and then the premiums level off. The Subgroup agreed to delete Section

27D(1). The Subgroup discussed at length the topics of exhaustion and restoration and agreed to delete the third sentence in

Section 27D(3) and Section 27D(4)(b).

The Subgroup agreed to retain Section 27E and Section 27F. The Subgroup discussed the phrase “become effective twelve

(12) months after adoption” and whether it is relevant to these short duration policies. The Subgroup agreed to delete Section

27G, Section 27H and Section 27J, as well as retain Section 27I (redesignated Section 27G).

Mr. Sundberg asked about Section 27C(3) and whether it would be better to eliminate the chart and revise the language in

that subsection to simply state 50%. The Subgroup agreed.

b. Section 28—Standards for Benefit Triggers

Ms. Breault said that the section looks reasonable and that she does not see any need for changes. Richard Waggoner (Aetna)

asked if medical necessity can be used in lieu of activities of daily living (ADLs). Mr. Serbinowski did not think it could be

used in that manner. Ms. Arp said that ADLs must be the focus but medical necessity could be added. William Schiffbauer

(Schiffbauer Law Group) said the use of medical necessity risks the Subgroup drifting into the realm of healthcare. Ms.

Graeber pointed out that long-term care (LTC) triggers used medical necessity prior to ADLs, but over time, medical necessity was replaced by ADLs because ADLs are more objective criteria. The Subgroup continued to discuss this at length

and agreed to delete Section 28G.

c. Section 29—Appealing an Insurer’s Determination that the Benefit Trigger is not Met

The Subgroup deleted the entire section entitled “Additional Standards for Benefit Triggers for Qualified Long-Term Care

Insurance Contacts” and moved to the renumbered Section 29 (formerly Section 31). The Subgroup deleted the drafting note.

Ms. Breault said Connecticut does not have an external appeal process and asked the Subgroup whether an external appeal

process is needed for these short duration policies. Ms. Waggoner said an external review process is probably going

overboard. Mr. Reilly said there is not much controversy involving these policies. Susan Voss (American Enterprise Group—

AEG) said that there is a cost benefit that companies would examine and that companies would probably rather pay a

disputed issue than hire a doctor to challenge another doctor. Ms. Arp said that an independent review is not necessary for

these short duration policies. Ms. Burns said there should be as many appeal rights as possible and suggested that language be

inserted to include a right for the insured to contact their state department of insurance and state health insurance program (SHIP) office. The Subgroup agreed.

The Subgroup agreed to revise Section 29C(1) to include language suggested by Ms. Burns, to delete Section 29B(3), Section

29C(2), Section 29C(3), Section 29C(4) and Section 29C(5). The Subgroup also agreed to delete Section 29D and the

remainder of the section after. The Subgroup agreed to begin its next call with Section 30—Prompt Payment of Clean

Claims.

Having no further business, the Short Duration Long-Term Care Policies (B) Subgroup adjourned.

G:\Health and Life\Long Term Care Insurance\Short Duration LTC Policies (B) Subgroup\Minutes 01-24-2018.docx

Draft: 12/18/17

Short Duration Long-Term Care Policies (B) Subgroup

Conference Call

December 13, 2017

The Short Duration Long-Term Care Policies (B) Subgroup of the Senior Issues (B) Task Force met via conference call

Dec. 13, 2017. The following Subgroup members participated: Mary Ellen Breault, Chair (CT); Tyler McKinney, Vice Chair

(CA); Rebecca Vaughan (IN); Stephanie McGaughey-Bowker (KY); Chlora Lindley-Myers (MO); Martin Swanson (NE);

Maureen Belanger (NH); Terry Seaton (NM); Frank Stone (OK); Tracy Bixler (PA); Phillip Reyna (TX); Jaakob Sundberg

(UT); and Jennifer Stegall (WI). Also participating were: Mayumi Gabor (AK); William Lacy (AR); Martha Im (HI);

Jennifer Lindberg (IA); Eric Anderson (IL); Fern Thomas (MD); Kristi Bohn (MN); Ted Hamby (NC); Yuri Venjohn (ND);

Andrew Dvorine (SC); Brian Hoffmeister (TN); and Amy Peach (WA).

1. Discussed Rate Stability Versus Loss Ratio in Section 10, Section 19 and Section 20 of Model #641

Ms. Breault reminded the Subgroup that on its Nov. 15 call, the Subgroup agreed to have an ad hoc group address changes to

the loss ratio language in Section 10, Section 19 and Section 20 of the Long-Term Care Insurance Model Regulation (#641).

Ms. Breault asked if there were any comments to the general changes made by the ad hoc group. Ms. Mealer asked about the

impact on rates and the coding to be used. Ms. Breault said that would be left to the individual states. Ms. Breault asked if the

60% figure in the edited Section 10B(3)(b), which was a placeholder figure used by the ad hoc group, is agreeable to the

Subgroup. She said in Connecticut, the figure is 55% and some in industry had remarked in prior calls that it could be as

close to 50%. Ms. Mealer said the figure should not be below 55%. Richard Waggoner (Aetna) said 60% would be difficult,

and 55% to 50% is reasonable in light of the fixed costs associated with these policies.

Bonnie Burns (California Health Advocates—CHA) asked why the fixed costs warrant the loss ratios to be different and that

it was not appropriate to allow a higher profit margin. Ms. Breault explained that there are fixed costs that would be the same

for both short term care and long term care products. Since short term care products would have lower premiums to reflect a

lower level of benefits, the fixed costs are a greater percentage of the premium as compared to long term care products. Ms.

Burns said that the costs of selling these products seems to be easier than traditional long-term care insurance (LTCI) and

since the duration is of a smaller period how would the fixed costs be greater? Ms. Breault replied that is the fixed costs are

not greater but rather are a higher percentage of the premiums. Upon further discussion, the Subgroup agreed to 55 %.

Ms. Breault asked about Section 10C(2) and whether “a lifetime loss ratio not less than 80%” is agreeable to the Subgroup.

She said the 80% figure would be used in circumstances where documentation is lost or there is no complete record.

Mr. Sundberg said that it is a prospective provision and intended to address past issues. The Subgroup agreed to the 80%

figure.

The Subgroup agreed to delete Section 19, Premium Rate Schedule Increases, and to renumber Section 20. Ms. Breault asked

if the “plus 2%” figure in the new Section 19B is agreeable to the Subgroup. Mr. Waggoner said it is reasonable. The

Subgroup agreed to retain the “plus 2%” figure in Section 19B. Ms. Breault said the language “without margins for adverse

deviations” should be deleted. Mr. Sundberg said he thinks it should be retained but perhaps could be replaced with “best

estimate assumptions.” The Subgroup agreed to that language change in Section 19B.

2. Revisited Sections of Model #641

a. Section 24—Suitability

Doug Danzeiser (TX) proposed new language for Section 24A on the Subgroup’s Nov. 15 call. Ms. Breault asked if the

Subgroup was agreeable to the offered language. The Subgroup agreed to the new language.

b. Section 26—Availability of New Services or Providers

Ms. Breault reminded the Subgroup that on its Nov. 15 call, the Subgroup discussed whether Section 26 should be retained.

Ms. Burns said that this section informs policyholders of new products or changes and saw no harm in retaining the section.

The Subgroup agreed to retain Section 26.

c. Section 27—Right to Reduce Coverage and Lower Premiums

Michael Colliflower (Aetna) suggested language to be added to Section 27 to state that reductions provided are not less than the minimum offered. Robert Glowacki (RPGLTC Services LLC) said Section 27C(2) addresses that issue.

d. Section 28—Nonforfeiture Benefit Requirement

Ms. Breault said Section 28A and Section 28B would need to be revised to reflect the changes made to Section 8 in Model

#641. Ms. Breault asked the Subgroup whether the current table in the Model #641 should be retained as is or modified. Mr.

Sundberg suggested keeping the same contingent nonforfeiture benefit, but not on an age-based basis but rather on a single

percentage basis so all are eligible. He suggested a 50% figure. Ms. Breault, Ms. Mealer and Ms. Bohn supported the

suggestion. The Subgroup agreed to the change.

Mr. Waggoner asked for clarification on the contingent nonforfeiture benefit. Ms. Breault said it is intended for those

consumers who do not purchase a nonforfeiture benefit. She said if an insurance carrier raises rates and an insured cannot

afford the increase, the contingent nonforfeiture allows the insured to receive partial benefits.

The Subgroup agreed to delete Section 28C(4), Section 28C(6) and Section 28C(7). It agreed to retain Section 28C(5). The

Subgroup agreed to remove reference to subsection C(4) in Section 28D. The Subgroup began discussion on Section 28D(1)

and decided to resume further discussion on its next call.

Having no further business, the Short Duration Long-Term Care Policies (B) Subgroup adjourned. G:\Health and Life\Long Term Care Insurance\Short Duration LTC Policies (B) Subgroup\Minutes 12-13-2017.docx

Agenda Item #3

Exposure of the Limited Long-Term Care Insurance Model

Act and Limited Long-Term Care Insurance Model

Regulation

The Short Duration Long-Term Care Policies (B) Subgroup adopted the

Limited Long-Term Care Insurance Model Act and Limited Long-Term Care

Insurance Model Regulation on March 7, 2018.

SHORT-TERMLIMITED LONG-TERM CARE INSURANCE MODEL ACT

Table of Contents

Section 1. Purpose

Section 2. Scope

Section 3. Short Title

Section 4. Definitions

Section 5. Extraterritorial Jurisdiction—Group Short-TermLimited Long-Term Care Insurance

Section 6. Disclosure and Performance Standards for Short-TermLimited Long-Term Care Insurance

Section 7. Incontestability Period

Section 8. Nonforfeiture Benefits

Section 9. Producer Training Requirements [OPTIONAL]

Section 10. Authority to Promulgate Regulations

Section 11. Administrative Procedures

Section 12. Severability

Section 13. Penalties

Section 14. Effective Date

Section 1. Purpose

The purpose of this Act is to promote the public interest, to promote the availability of short-termlimited long-term care insurance policies, to protect applicants for short-termlimited long-term care insurance, as defined, from unfair or deceptive

sales or enrollment practices, to establish standards for short-termlimited long-term care insurance, to facilitate public

understanding and comparison of short-termlimited long-term care insurance policies, and to facilitate flexibility and

innovation in the development of short-termlimited long-term care insurance coverage.

Drafting Note: The purpose clause evidences legislative intent to protect the public while recognizing the need to permit flexibility and innovation with respect to short-termlimited long-term care insurance coverage. Section 2. Scope

The requirements of this Act shall apply to policies delivered or issued for delivery in this state on or after the effective date

of this Act. This Act is not intended to supersede the obligations of entities subject to this Act to comply with the substance

of other applicable insurance laws insofar as they do not conflict with this Act, except that laws and regulations designed and

intended to apply to Medicare supplement insurance policies shall not be applied to short-termlimited long-term care

insurance.

Drafting Note: This section makes clear that entities subject to the Act must continue to comply with other applicable insurance legislation not in conflict with this Act.

Section 3. Short Title

This Act may be known and cited as the “Short-TermLimited Long-Term Care Insurance Act.”

Section 4. Definitions

Unless the context requires otherwise, the definitions in this section apply throughout this Act.

A. “Short-termLimited long-term care insurance” means any insurance policy or rider advertised, marketed,

offered or designed to provide coverage for less than twelve (12) consecutive months for each covered

person on an expense incurred, indemnity, prepaid or other basis; for one or more necessary or medically

necessary diagnostic, preventive, therapeutic, rehabilitative, maintenance or personal care services,

provided in a setting other than an acute care unit of a hospital. The term also includes a policy or rider that

provides for payment of benefits based upon cognitive impairment or the loss of functional capacity. Short-

term Limited long-term care insurance may be issued by insurers; fraternal benefit societies; nonprofit

health, hospital, and medical service corporations; prepaid health plans; health maintenance organizations

or any similar organization to the extent they are otherwise authorized to issue life or health insurance.

Short-termLimited long-term care insurance shall not include any insurance policy that is offered primarily

to provide basic Medicare supplement coverage, basic hospital expense coverage, basic medical-surgical expense coverage, hospital confinement indemnity coverage, major medical expense coverage, disability

income or related asset-protection coverage, accident only coverage, specified disease or specified accident

coverage, or limited benefit health coverage. Notwithstanding any other provision of this Act, any product

advertised, marketed or offered as short-termlimited long-term care insurance shall be subject to the

provisions of this Act.

B. “Applicant” means:

(1) In the case of an individual short-termlimited long-term care insurance policy, the person who

seeks to contract for benefits; and

(2) In the case of a group short-termlimited long-term care insurance policy, the proposed certificate

holder.

C. “Certificate” means, for the purposes of this Act, any certificate issued under a group short-termlimited

long-term care insurance policy, which policy has been delivered or issued for delivery in this state.

D. “Commissioner” means the Insurance Commissioner of this state.

Drafting Note: Where the word “commissioner” appears in this Act, the appropriate designation for the chief insurance supervisory official of the state should be substituted.

E. “Group short-termlimited long-term care insurance” means a short-termlimited long-term care insurance

policy that is delivered or issued for delivery in this state and issued to:

(1) One or more employers or labor organizations, or to a trust or to the trustees of a fund established

by one or more employers or labor organizations, or a combination thereof, for employees or

former employees or a combination thereof or for members or former members or a combination

thereof, of the labor organizations; or

(2) Any professional, trade or occupational association for its members or former or retired members,

or combination thereof, if the association:

(a) Is composed of individuals all of whom are or were actively engaged in the same

profession, trade or occupation; and

(b) Has been maintained in good faith for purposes other than obtaining insurance; or

(3) An association or a trust or the trustees of a fund established, created or maintained for the benefit

of members of one or more associations. Prior to advertising, marketing or offering the policy

within this state, the association or associations, or the insurer of the association or associations,

shall file evidence with the commissioner that the association or associations have at the outset a

minimum of 100 persons and have been organized and maintained in good faith for purposes other

than that of obtaining insurance; have been in active existence for at least one year; and have a

constitution and bylaws that provide that:

(a) The association or associations hold regular meetings not less than annually to further

purposes of the members;

(b) Except for credit unions, the association or associations collect dues or solicit

contributions from members; and

(c) The members have voting privileges and representation on the governing board and

committees.

Thirty (30) days after the filing the association or associations will be deemed to satisfy the

organizational requirements, unless the commissioner makes a finding that the association or

associations do not satisfy those organizational requirements.

(4) A group other than as described in Subsections E(1), E(2) and E(3), subject to a finding by the

commissioner that:

(a) The issuance of the group policy is not contrary to the best interest of the public;

(b) The issuance of the group policy would result in economies of acquisition or

administration; and

(c) The benefits are reasonable in relation to the premiums charged.

F. “Policy” means, for the purposes of this Act, any policy, contract, subscriber agreement, rider or

endorsement delivered or issued for delivery in this state by an insurer; fraternal benefit society; nonprofit

health, hospital, or medical service corporation; prepaid health plan; health maintenance organization or

any similar organization.

Drafting Note: This Act is intended to apply to the specified group and individual policies, contracts, and certificates whether issued by insurers; fraternal benefit societies; nonprofit health, hospital, and medical service corporations; prepaid health plans; health maintenance organizations or any similar organization. In order to include such organizations, each state should identify them in accordance with its statutory terminology or by specific statutory citation. Depending upon state law, insurance department jurisdiction and other factors, separate legislation may be required. In any event, the legislation should provide that the particular terminology used by these plans and organizations may be substituted for, or added to, the corresponding terms used in this Act. The term “regulations” should be replaced by the terms “rules and regulations” or “rules” as may be appropriate under state law. The definition of “short-termlimited long-term care insurance” under this Act is designed to allow maximum flexibility in benefit scope, intensity and level, while assuring that the purchaser’s reasonable expectations for a short-termlimited long-term care insurance policy are met. The Act is intended to permit short-termlimited long-term care insurance policies to cover diagnostic, preventive, therapeutic, rehabilitative, maintenance or personal care services, or any combination thereof, and not to mandate coverage for each of these types of services. The language in the definition concerning “other than an acute care unit of a hospital” is intended to allow payment of benefits when a portion of a hospital has been designated for, and duly licensed or certified as a long-term care provider or swing bed.

G. “Waiting Period” means, for the purposes of this Act, the time an insured must wait before some or all of

their coverage comes into effect. “Elimination Period” means, for purposes of this Act, the length of time

between meeting the eligibility for benefit payment and receiving benefit payments from an insurer.

Section 5. Extraterritorial Jurisdiction—Group Short-TermLimited Long-Term Care Insurance

No group short-termlimited long-term care insurance coverage may be offered to a resident of this state under a group policy

issued in another state to a group described in Section 4E(4), unless this state or another state having statutory and regulatory

short-termlimited long-term care insurance requirements substantially similar to those adopted in this state has made a

determination that such requirements have been met.

Drafting Note: By limiting extraterritorial jurisdiction to “discretionary groups,” it is not the drafters’ intention that

jurisdiction over other health policies should be limited in this manner.

Drafting Note: States should consider deletion of this section if they already have statutes or rules governing extraterritorial

jurisdition that would automatically encompass short-termlimited long-term care policies.

Section 6. Disclosure and Performance Standards for Short-TermLimited Long-Term Care Insurance

A. No short-termlimited long-term care insurance policy may:

(1) Be cancelled, non-renewed or otherwise terminated on the grounds of the age, gender or the

deterioration of the mental or physical health of the insured individual or certificate holder;

(2) Contain a provision establishing a new waiting period in the event existing coverage is converted

to or replaced by a new or other form within the same company, except with respect to an increase

in benefits voluntarily selected by the insured individual or group policyholder; or

(3) Provide coverage for skilled nursing care only or provide significantly more coverage for skilled care in a facility than coverage for lower levels of care.

B. Preexisting condition.

(1) No short-termlimited long-term care insurance policy or certificate other than a policy or

certificate thereunder issued to a group as defined in Section 4E(1) shall use a definition of

“preexisting condition” that is more restrictive than the following: Preexisting condition means a

condition for which medical advice or treatment was recommended by, or received from a

provider of health care services, within six (6) months preceding the effective date of coverage of

an insured person.

(2) No short-termlimited long-term care insurance policy or certificate other than a policy or

certificate thereunder issued to a group as defined in Section 4E(1) may exclude coverage for a

loss or confinement that is the result of a preexisting condition unless the loss or confinement

begins within six (6) months following the effective date of coverage of an insured person.

(3) The commissioner may extend the limitation periods set forth in Sections 6C(1) and (2) above as

to specific age group categories in specific policy forms upon findings that the extension is in the

best interest of the public.

(4) The definition of “preexisting condition” does not prohibit an insurer from using an application

form designed to elicit the complete health history of an applicant, and, on the basis of the answers on that application, from underwriting in accordance with that insurer’s established underwriting

standards. Unless otherwise provided in the policy or certificate, a preexisting condition,

regardless of whether it is disclosed on the application, need not be covered until the waiting

period described in Section 6C(2) expires. No short-termlimited long-term care insurance policy

or certificate may exclude or use waivers or riders of any kind to exclude, limit or reduce coverage

or benefits for specifically named or described preexisting diseases or physical conditions beyond

the waiting period described in Section 6C(2).

C. Prior hospitalization/institutionalization.

(1) No short-termlimited long-term care insurance policy may be delivered or issued for delivery in

this state if the policy:

(a) Conditions eligibility for any benefits on a prior hospitalization requirement;

(b) Conditions eligibility for benefits provided in an institutional care setting on the receipt

of a higher level of institutional care; or

(c) Conditions eligibility for any benefits other than waiver of premium, post-confinement,

post-acute care or recuperative benefits on a prior institutionalization requirement.

(2) A short-termlimited long-term care insurance policy or rider shall not condition eligibility for non-

institutional benefits on the prior or continuing receipt of skilled care services.

D. The commissioner may adopt regulations establishing loss ratio standards for short-termlimited long-term

care insurance policies provided that a specific reference to short-termlimited long-term care insurance

policies is contained in the regulation.

E. Right of Return

(1) Short-termLimited long-term care insurance applicants shall have the right to return the policy,

certificate or rider to the company or an agent/insurance producer of the company within thirty

(30) days of its receipt and to have the premium refunded if, after examination of the policy,

certificate or rider, the applicant is not satisfied for any reason.

(2) Short-termLimited long-term care insurance policies, certificates and riders shall have a notice prominently printed on the first page or attached thereto including specific instructions to

accomplish a return. This requirement shall not apply to certificates issued pursuant to a policy

issued to a group defined in Section 4E(1) of this Act. The following free look statement or

language substantially similar shall be included:

“You have 30 days from the day you receive this policy, certificate or rider to review it and return

it to the company if you decide not to keep it. You do not have to tell the company why you are

returning it. If you decide not to keep it, simply return it to the company at its administrative

office. Or you may return it to the agent/insurance producer that you bought it from. You must

return it within 30 days of the day you first received it. The company will refund the full amount

of any premium paid within 30 days after it receives the returned policy, certificate or rider. The

premium refund will be sent directly to the person who paid it. The policy, certificate or rider will

be void as if it had never been issued.”

F. Outline of Coverage

(1) An outline of coverage shall be delivered to a prospective applicant for short-termlimited long-

term care insurance at the time of initial solicitation through means that prominently direct the

attention of the recipient to the document and its purpose.

(a) The commissioner shall prescribe a standard format, including style, arrangement and

overall appearance, and the content of an outline of coverage.

(b) In the case of agent solicitations, an agent shall deliver the outline of coverage prior to

the presentation of an application or enrollment form.

(c) In the case of direct response solicitations, the outline of coverage shall be presented in

conjunction with any application or enrollment form.

(d) In the case of a policy issued to a group defined in Section 4E(1) of this Act, an outline of

coverage shall not be required to be delivered, provided that the information described in

Section 6F(2)(a) through (h) is contained in other materials relating to enrollment. Upon

request, these other materials shall be made available to the commissioner.

Drafting Note: States may wish to review specific filing requirements as they pertain to the outline of coverage and these

other materials.

(2) The outline of coverage shall include:

(a) A description of the principal benefits and coverage provided in the policy;

(b) A description of the eligibility triggers for benefits and how those triggers are met;

(c) A statement of the principal exclusions, reductions and limitations contained in the

policy;

(d) A statement of the terms under which the policy or certificate, or both, may be continued

in force or discontinued, including any reservation in the policy of a right to change

premium. Continuation or conversion provisions of group coverage shall be specifically

described;

(e) A statement that the outline of coverage is a summary only, not a contract of insurance,

and that the policy or group master policy contains governing contractual provisions;

(f) A description of the terms under which the policy or certificate may be returned and

premium refunded;

(g) A brief description of the relationship of cost of care and benefits; and

(h) A statement that discloses to the policyholder or certficateholder that the policy is not

long-term care insurance.

G. A certificate issued pursuant to a group short-termlimited long-term care insurance policy that is delivered

or issued for delivery in this state shall include:

(1) A description of the principal benefits and coverage provided in the policy;

(2) A statement of the principal exclusions, reductions and limitations contained in the policy; and

(3) A statement that the group master policy determines governing contractual provisions.

H. If an application for a short-termlimited long-term care insurance contract or certificate is approved, the

issuer shall deliver the contract or certificate of insurance to the applicant no later than thirty (30) days after

the date of approval.

I. If a claim under a short-termlimited long-term care insurance contract is denied, the issuer shall, within