Seminar in Auctions and Mechanism Design Based on J. Hartline’s book: Approximation in Economic...

52

Seminar in Auctions and Mechanism Design Based on J. Hartline’s book: Approximation in Economic Design Multi-dimensional Approximation Presented by: Miki Dimenshtein & Noga Levy

-

Upload

branden-firkins -

Category

Documents

-

view

220 -

download

1

Transcript of Seminar in Auctions and Mechanism Design Based on J. Hartline’s book: Approximation in Economic...

Seminar in Auctions and Mechanism Design

Based on J. Hartline’s book: Approximation in Economic Design

Multi-dimensional Approximation

Presented by: Miki Dimenshtein & Noga Levy

1. Introduction to multi-dimensional environments.

*Item pricing against m-agents auction.

2. Reduction to single dimensional preferences.

3. Lottery pricing.

Lecture topics

Background

In previous chapters, we’ve consider agents' types as single dimensional - agent’ private preference is given by a single value for receiving a service

We now turn to multi-dimensional environments where the agents’ preferences are given by a multi-dimensional type

Example – multi-dimensional environment• a home buyer may have distinct values for different houses on the market.

•Consider selling m items and n agents

• Each agent has a valuation function that is defined across all bundles. I.e.,

if agent i receives bundle S ⊂ {1, ...,m} then he has value vi(S).

•A generally multi-dimensional auction assigns to agent i , bundle Si and payment pi.•Agent i’s utility is given by vi(Si) − pi. This called quasi-linear.

• The mechanism chooses the outcome that maximizes social surplus and it charges each agent the externality imposed on the remaining agents

generally multi-dimensional

Theorem For agents with (generally multi-dimensional) quasi-linear preferences, the surplus maximization mechanism is dominant strategy incentive compatible and maximizes

the social surplus.

We will show that posted-pricing mechanisms

can approximate the optimal social surplus in some relevant environments (not all of them).

Even though the surplus maximization mechanism is optimal (for social surplus), it issometimes infeasible to run.

Matching market• n agents and m items

•Each agent i has a value vij for item j

V11 = 10,000$

V12 = 20,000$

V13 = 30,000$

Matching market (cont.)

•The agents are unit-demand - each wants at most one item

•The items are unit-supply - each can be sold to at most one agent

•Agent values are drawn independently at random, vij ∼ Fij .

Item Pricing

We start with only one agent, n = 1.

We need to identify revenue optimal pricings

I.e., identify a pricing p = (p1, . . . , pm) such that:

when the agent buys the item that

maximizes vj − pj → revenue is maximized.

How we do that?

Finding an upper bound on the revenue of an

optimal pricings.

if a pricing approximates this upper bound, it also

approximates the optimal pricing.

Finding an upper bound

First, notice that instead of:Single agent, unit-demand preferences, with m items We create an environment of m (single-dimensional) agents, who each want their specific item, but with the constraint that at most one can be served.

single-agent, m-item pricing V1

V4

V3

V5

V2

Vi ~

Fi

single-item, m-agent auction

V1 V4V3 V5

V2

Vi ~ Fi Only one can be

served!

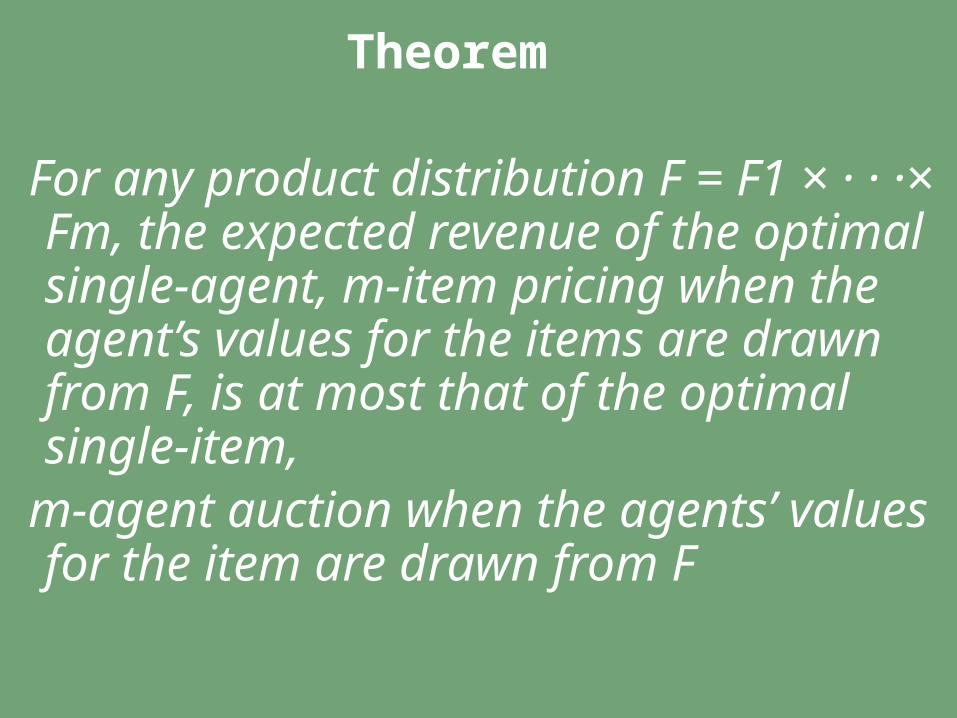

Theorem

For any product distribution F = F1 × · · ·× Fm, the expected revenue of the optimal single-agent, m-item pricing when the agent’s values for the items are drawn from F, is at most that of the optimal single-item,

m-agent auction when the agents’ values for the item are drawn from F

Expected revenue of the optimal single-item, m-agent auction

V1V4

V3

V5

V2

Expected revenue of the optimal

single-agent, m-item pricing

≥

Pricing problem : seller can only post a

price on each item.Auction problem: the competition between agents can drive the price up.

Revenue in the (single-dimensional) auction

environment is an upper bound on the revenue in the single buyer (multi-dimensional) pricing environment.

Proof• Any item pricing p can be converted into a

single-item auction Ap such that the expected revenue from the item pricing is at

most that of the auction.• The auction Ap assigns the item to the agent j that maximizes vj − pj .• For any fixed values of the other agents, v−j , this allocation rule is monotone in agent j’s value and therefore ex post incentive compatible. It is also deterministic.• Our auction is deterministic, DSIC Mechanism

• So according to 2.18: there is a critical value j for agent j which is the infimum of values for which the agent wins the auction; the agent pays exactly this critical value on winning. Of course j ≥ pj

Proof (cont.)Also, notice that the allocation rule of the auction Ap is identical to the allocation rule of the pricing p:

*For the pricing the agent chooses the item that maximizes vj − pj

*For the auction the winner is selected to maximize vj −pj .

*The revenue for the pricing is exactly the pj that corresponds to this j whereas in

the auction it is τj which, is at least pj .

Therefore,

the auction Ap obtains at least revenue of the pricing p.

Now we can say.

Revenue in the (single-dimensional) auction environment is an upper bound on the revenue in the (multi-dimensional) pricing environment.

Reminder:Theorem 4.7. There exists a threshold strategy such that the expected prize of the gambler is at least half the expected value of the maximum prize. Moreover, one such threshold strategy is the one where the probability that the gambler receives no prize is exactly 1/2. Moreover, this bound is invariant to the tie-breaking rule.

Theorem 4.9. For any independent, single-item environment the second-price auction witha uniform ironed virtual reserve price is a 2-approximation to the optimal auction revenue.Theorem 4.10. For any independent, single-item environment a sequential posted pricingof uniform ironed virtual prices is a 2-approximation to the optimal auction revenue.

7.2 Reduction: Unit-demand to Single-dimensional Preferences

Goal: Show a reduction from multi-dimensional unit-demand preferences to single-dimensional preferences from the perspective of approximation.

We assume independence of the agents values.

Define a general unit-demand environment:

n agents, m services.Agent i has value for service j.

Indicator x with

C() – cost function for the implicit constraint that each agent can only receive one service:

𝑣𝑖𝑗

𝑥𝑖𝑗 = ቄ1 𝑖𝑓 𝑖 𝑟𝑒𝑐𝑖𝑣𝑒𝑠 𝑠𝑒𝑟𝑣𝑖𝑐𝑒 𝑗0 𝑜𝑡ℎ𝑒𝑟𝑤𝑖𝑠𝑒

𝑥𝑖𝑗 = 𝑥𝑖′𝑗 = 1 𝑓𝑜𝑟 𝑖′ ≠ 𝑖 ℎ𝑎𝑣𝑒 𝑐ሺ𝑥ሻ= ∞

7.2.1 Single-dimensional Analogy

•Definition 7.4 the representative environment for the n agent, m services unit demand environment given by F and c() is the single-dimensional environment given by F and c() with nm single-dimensional agents indexed by coordinates ij.

7.2.2 Upper boundThe restriction that only one representative of each unit demand agent can be served at once induces competition between representatives.

Intuitively this competition should resultin an increased revenue in the optimal mechanism for the representative environment overthe original unit-demand environment.

Theorem 7.5. For any independent, unit-demand environment, the optimal deterministic mechanism’s revenue is at most that of the optimal mechanism for the single-dimensional representative environment.

single-item, nm-agent auction

Vi1Vi4Vi3 Vi5Vi2

Vi j ~ Fij

V1j

V2j

V3j

V4j

V5j

Reminder

Theorem 4.10. For any independent, single-item environment a sequential posted pricingof uniform ironed virtual prices is a 2-approximation to the optimal auction revenue.

Sequential posted pricings, i.e., where the agents arrive in any order, approximate the optimal multi-agent single-item auction.

7.2.3 Reduction

We will now show a lower bound:

In unit-demand pricing, item is allocated that

In sequential posted pricing ties are broken in worst-case order to

I.e. worst case is that the first agent arrives and pays the lowest price.

𝑀𝑎𝑥(𝑣𝑗 − 𝑃𝑗)

𝑀𝑎𝑥(−𝑃𝑗)

Definition 7.6. A sequential posted pricing is an pricing of services (specialized) for each agent with the semantics that agents arrive in any order and take their favorite service that remains feasible. The revenue of such a pricing is given by the worst-case ordering.

A sequential posted pricing is given by prices p with the price offered to agent i for item j.

After the valuations are realized, the agents arrive in sequence and take their utility maximizing item that is still feasible.

𝑝𝑖𝑗

Example

We assume worst case

Theorem 7.7. The expected revenue of a sequential posted pricing for unit-demand environments is at least the expected revenue of the same pricing in the representative single-dimensional environment.

Proof

When comparing the two environments, in the representative environment the nm agents can arrive in any order.

In the original environment, an agent arrives an considers the prices on services ordered by utility.

The set of orders in the representative environment contains the set of orders in the original.

For worst-case the representative is worse.

Corollary 7.8. If a sequential posted pricing is approximately optimal in the representative(single-dimensional) environment it is approximately optimal in the original (unit-demand) environment.

7.2.4 Instantiationwe need to show that there are good sequential posted pricing mechanisms for single-dimensional environments.

Here we will give such an instantiation for independent, regular, matching markets, i.e., wherethe services are items, and each item has only one unit of supply.

The representative environment for matching markets:•nm agents.•Agent ij with value desires item j.• For item j and original agent i, at most one representative ij can win.•VSM is the optimal mechanism. • - the probability that VSM serves ij.• .•

𝑣𝑖𝑗 ~𝐹𝑖𝑗

𝑞𝑖𝑗𝑉𝑆𝑀 𝑝𝑖𝑗𝑉𝑆𝑀= 𝐹𝑖𝑗−1(1− 𝑞𝑖𝑗𝑉𝑆𝑀) 𝑝𝑖𝑗 = 𝐹𝑖𝑗−1൫1− 𝑞𝑖𝑗൯ 𝑓𝑜𝑟 𝑞𝑖𝑗 = 𝑞𝑖𝑗𝑉𝑆𝑀2

Definition 7.9. For the representative matching market environments, the simulation prices, p, satisfy 𝑝𝑖𝑗 = 𝐹𝑖𝑗−1ቀ1− 12Prሾ𝑡ℎ𝑒 𝑜𝑝𝑡𝑖𝑚𝑎𝑙 𝑚𝑎𝑐ℎ𝑎𝑛𝑖𝑠𝑚 𝑠𝑒𝑟𝑣𝑒𝑠 𝑖𝑗ሿቁ 𝑓𝑜𝑟 𝑎𝑙𝑙 𝑖,𝑗

Theorem 7.10. For regular distributions in the representative matching market environment, the sequential posted pricing with the simulation prices p is an 8-approximation to the revenue of the optimal mechanism.

Lemma 7.11. For regular distributions in the representative matching market environment, the expected revenue of the optimal mechanism, VSM, is at most .

Lemma 7.12. For regular distributions in the representative matching market environment, the expected revenue from the sequential posted pricing of the simulation prices is at least

σ 𝑝𝑖𝑗𝑉𝑆𝑀𝑞𝑖𝑗𝑉𝑆𝑀𝑖𝑗

18σ 𝑝𝑖𝑗𝑉𝑆𝑀𝑞𝑖𝑗𝑉𝑆𝑀𝑖𝑗

Upper Bound

Lower Bound

Upper BoundConsider an un-constrained mechanism that allocates to representative ij with probability at most

Because if regularity the un-constrained mechanism posts priceto each representative ij and the expected revenue is

VSM is the optimal mechanism for the constrained environment and a valid solution to the un-constrained environment.

𝑞𝑖𝑗𝑉𝑆𝑀

𝑝𝑖𝑗𝑉𝑆𝑀 σ 𝑝𝑖𝑗𝑉𝑆𝑀𝑞𝑖𝑗𝑉𝑆𝑀𝑖𝑗

Lower Bound

• .• since prices increase with a lower selling probability.

• The expected revenue from agent ij is

𝑞𝑖𝑗 = 𝑞𝑖𝑗𝑉𝑆𝑀2 𝑝𝑖𝑗 ≥ 𝑝𝑖𝑗𝑉𝑆𝑀 𝑞𝑖𝑗𝑝𝑖𝑗 ≥ 𝑞𝑖𝑗𝑉𝑆𝑀𝑝𝑖𝑗𝑉𝑆𝑀 2൘

Lower BoundWe need to show that the probability that it is feasible to offer service to representative ij is at least ¼.

Representative ij is last and can be served if none of the other representatives has be served yet, and no one been served item j.

𝑣𝑖′𝑗 < 𝑝𝑖𝑗 𝑓𝑜𝑟 𝑎𝑙𝑙 𝑖′ ≠ 𝑖

Lower BoundShow that each of the events happens with probability at least 1/2, since the events are independent, the probability for both is ¼ .

Consider the event .The possibility that is a bad event happens with probability

The of all the bad events is bounded byTherefore, probability that none of them happen is at least ½.

𝑣𝑖′𝑗 < 𝑝𝑖𝑗 𝑓𝑜𝑟 𝑎𝑙𝑙 𝑖′ ≠ 𝑖 𝑣𝑖′𝑗 ≥ 𝑝𝑖𝑗 𝑞𝑖′ 𝑗 σ 𝑞𝑖′𝑗𝑉𝑆𝑀𝑖′ ≤ 1 →σ 𝑞𝑖′𝑗𝑖′ ≤ 12

Lottery Pricing and Randomized MechanismsOptimal mechanism may not be a deterministic

pricing of items. We now show another mechanism using pricing of items including pricing randomized outcome.

Lotteries – Giving a price to randomized outcomes.

A lottery is a probability distribution over outcomes. For instance, for the m = 2 item case, a lottery could assign

either item 1 or item 2 with probability 1/2 each.

A lottery pricing is then a set of lotteries and prices for each.

For such a lottery pricing, the agent then chooses the lottery and price that give

the highest utility for his given valuations for the items.

Lottery pricings can give

higher revenue than item pricings

• There are 2 items (m=2), 1 agent (n=1)• The agent’s value for each item is distributed independently and uniformly from the interval [5,6].• Set a uniform price of 5.097 for each item. Agent is offered to buy an item at the price of 5.097 • The agent buys the item he values the most, and also at least 5.097

Example

V1 V2

Min price: 5.097

Allocation rule without lottery

• We now provide another option to agent - buying at price 5.057 a lottery with probability ½ to get an item.

Without the lottery option if the agent had average value bigger than 5.057 but no individual value over 5.097, the agent would buy nothing.

Adding the lottery option

V1 V2

Min price: 5.097 or lottery (price: 5.057)

Lottery – 5.057

Allocation rule with lottery with price p’=5.057

There are examples where the optimal lottery pricing obtains more

revenue than the optimal single-item auction for the representative environment.

Unlike representative environment that increased competition to obtain more revenue than that of the original unit-demand environment. It is not entirely correct when randomized mechanisms are allowed.

Optimal lottery pricing

Homework - Exercise 7.2

Prove Theorem 7.5:

For any independent, unit-demand environment, the optimal deterministic mechanism’s revenue is at most that of the optimalmechanism for the single-dimensional representative environment.

תודה