American Industrialization I. What Factors Caused the US to Industrialize?

Seeds of American Industrialization: A New ViewFrom Economic Geography

Stephen Sun

November 15, 2016

Abstract

This article examines the degree to which a large preexisting demand en-courages the growth of connected industries using the case of the 19th cen-tury United States’ agricultural implements industry. The agricultural imple-ments industry is distinguished by having linkages with both the agriculturaland manufacturing sectors and by the fact that its output is mostly sold out-side of cities, which creates product-level spatial variation in demand notseen in other manufactures. I study the impact of proximity to demand andof spillovers and find a strongly significant effect for both, with proximityto demand being roughly 1.5 times as important. These results provide evi-dence of a role for agriculture as a foundation for manufacturing growth andfurther implies the existence of positive spillovers which could drive furtherindustrialization. I also find evidence for a role for human capital.

1 Introduction

The traditional story of industrialization emphasizes capital deepening and accessto markets. In this picture, linkages between industries are key: for a location to in-dustrialize, nascent industries must be able to build enough forward and backwardlinkages that firms will be able to overcome the lumpiness inherent to large-scalemanufacturing technology and benefit from economies of scale. This idea led inpart to import-substitution (ISI) and similar development strategies which relied

1

upon government intervention to achieve the necessary scale (Lindauer and Pritch-ett 2002). Many of these considerations can be considered part of one of two maincategories of potential determinants of industrial location: those of comparative ad-vantages or factor endowments, and those which relate to transaction costs, whichare a function of geography. Table 1 lists some hypotheses of each type. In additionto market access in the sense of proximity to consumers, some research has consid-ered other factors such as skilled labor pooling and knowledge sharing to explainindustry location choices. The more recent decline of manufacturing in the UnitedStates and the mixed record of Big Push/ISI strategies in developing countries haveshown that industrial size alone is not enough to assure continued success. Baldwin(2011) highlights one aspect of this problem by arguing that the improvement incommunications technology caused the dissolution of local physical linkages: lowtransport costs make it profitable for industry without local demand to join distantsupply chains on the strength of low factor prices, but when these circumstanceschange (e.g. an exchange rate shock or emergence of still cheaper factors), pro-ducers will quickly find themselves in distress. With this in mind, this paper seeksto assess the importance of linkages to existing economic activity in industrial lo-cation by comparing these two categories of competing explanations for industrylocation in an unusually situated industry: agricultural implements manufacturingin the late 19th century United States. As a test case for industrialization, the agri-cultural implements industry has a number of advantages which allow it to be usedto investigate two dimensions of this question. First, to test hypotheses about whatforces influence industrial location decisions and to estimate their magnitude, andsecond, the importance of existing (non-manufacturing, in this case agriculture)economic activity in directing industrial development.

Table 1: Determinants of Location Choice

NEG Interactions HO interactionsOutput market potential Access to raw materials

Intermediates market potential Labor poolingKnowledge spillovers Local infrastructure

Notes: NEG (new economic geography) interactions measurethe influence of distance-dependent transaction costs and arethus driven by location relative to areas of economic activity.HO (Heckscher-Ohlin) interactions measure the importance ofcomparative advantages which are properties of a region not directlydependent on the properties of other regions.

Economic historians have recognized the potential for trade costs and market ac-cess to influence industry location since at least the time of Marshall, but attempts

2

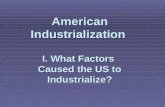

to disentangle which forces are most important run into the problem that both for-ward and backward linkages (e.g. labor supply, consumer markets, intermediatesmanufacturers, financial services) all concentrate in cities and therefore have simi-lar geographical distributions. But due to its position between two major economicsectors, firms in the implements industry face distinct market access patterns forupstream and downstream markets, which must be balanced against each other inlocation choices. Furthermore, the agricultural sector which provides the demandfor their output provides an additional form of geographical variation: exogenousclimate and soil differences between regions result in differences in crop suitabil-ity which in turn require different tools. Figure 1 illustrates this using the clearnorth/south split between corn and cotton planter production. Thus, backward andforward market potentials will be characterized by different spatial distributions,allowing their effects to be distinguished more easily. This article takes advantageof not only the difference between backward and forward spatial distribution butalso the differences among the distributions of target markets for implements in-tended for use on different crops to separate the influence of demand market accessfrom spillover effects related to other manufacturers and from factor endowments.

The United States was a major exporter of agricultural goods long before it be-came a major producer of manufactured goods; exports of non-food manufacturesdid not exceed imports until the final years of the 19th century (Carter et al. 2006).The volume of agricultural trade suggests its importance: in 1878, already well intothe industrialization of the United States, cotton and cereal grains contributed over50 percent of U.S. exports. If manufactured food products are included that sharegrows to near 70 percent (U.S. Census Bureau et al. 1878). At that time, aroundhalf the labor force was still employed in agriculture. The conventional account ofthe emergence of the United States as an industrial power takes the position that theUnited States did so by reallocating factors away from agriculture (e.g. Broadberry1998). However, the size of the agricultural sector suggests that a strong forward orbackward linkage with agriculture could become a powerful lever to encourage thegrowth of an industry. The agricultural sector was by no means stagnant during the19th century, and mechanization had much to do with this. Olmstead and Rhode(2002), who emphasize the role of biological innovations in raising labor produc-tivity in wheat agriculture, still attribute about half to mechanical innovations–anincrease of over 100 percent between 1839 and 1909.1

1In the no-bio innovation counterfactual, Olmstead and Rhode estimate an increase from 0.316bushels per hour to 0.803. Previously it was believed that biological innovations were unimportantbefore the 1930s; in this case one would naturally attribute much more of the total increase, to 1.318bushels per hour, to mechanization.

3

(a)C

orn

plan

ters

mfg

.(b

)Cor

nfa

rmou

tput

(c)C

otto

npl

ante

rsm

fg.

(d)C

otto

nfa

rmou

tput

Figu

re1:

Geo

grap

hica

ldis

trib

utio

nof

man

ufac

ture

ofco

rnan

dco

tton

plan

ters

in18

80.

The

diff

eren

cein

man

ufac

turi

nglo

catio

nsbe

twee

npl

antin

gim

plem

ents

targ

eted

atdi

ffer

entc

rops

isre

adily

appa

rent

inpa

nels

(a)a

nd(c

).Fo

rcom

pari

son,

the

dist

ribu

tion

offa

rmou

tput

corr

espo

ndin

gto

the

impl

emen

tis

show

nin

(b)a

nd(d

).So

urce

:U

.S.C

ensu

sof

Man

ufac

ture

s18

80.

4

The literature on American industrialization includes many explanations which arecompatible with this conjecture. If, for example, the expansion of railroads was asignificant factor in American industrialization, it was at least partially driven bywestward movement toward farmland in the Midwest. If it was simply that theMidwest had the demand for manufactures to support such an industry (e.g. Meyer1989), such a demand could only be made possible by a sufficiently large agri-cultural product. And if innovation and technological leadership were significantfactors, then the agricultural implements industry was important in that sense aswell: unlike the textile industry, it was no also-ran, but a clear case of Americantechnological leadership. There was no shortage of research and development inthis industry; the 38,661 patents filed between 18362 and 1900 exceed the numberfiled both in textiles (32,330) and in engines (23,616). Though textiles precededimplements as an important industry, American textile manufacturers were not in-ternational market leaders (Harley 1992). This was not the case for agriculturalimplements, by the admission of British competitors (Clark 1916) and from ob-servation of exports to the Australian market; the province of Victoria went frompurchasing 93 percent of its farm machinery from Britain in 1870 to importing 62percent from the United States and Canada in 1900. This preference for Americanmachinery may have been the result of a greater willingness of American producersto adapt and market their products to the specific market (McLean 1976). Industrytrade numbers reinforce this story: the Census reported 2.58 million dollars in ex-ports but did not bother to enumerate imports in 1878 (U.S. Census Bureau et al.1878). By 1905, exports were 21 million dollars of 113 million produced, or 18.6percent, a higher proportion than any manufactures other than sewing machines(23 percent) and refined mineral oil (56 percent). So to understand the forward andbackward linkages accruing to the agricultural implements industry is to under-stand the way in which changes in agriculture drove American industrialization.

Both categories of explanation in Table 1 have found support in recent work.Though the question of geography is old, much of the quantitative literature onlocation is comparatively recent, having benefited from the development of newmodels. Wright (1990) and Kim (1999) found evidence for factor endowments,focusing in particular on the availability of natural resources, though Wright em-phasizes that differences in resource abundance are a function more of exploitationthan natural endowment. Moretti (2004, 2012) finds a role for human capital inthat increases in plant productivity are correlated with increases in the local shareof college graduates, and compares the rise of “innovation” industries and con-

2The patent office records were destroyed by fire in December of 1936; records from before thencould not be completely reconstructed.

5

(a)C

ultiv

ator

s(b

)See

dso

wer

s

(c)H

arve

ster

s(d

)Thr

eshe

rs

Figu

re2:

Geo

grap

hica

ldis

trib

utio

nof

man

ufac

ture

ofse

lect

edag

ricu

ltura

lim

plem

ents

in18

80.E

ach

ofth

efo

urca

tego

ries

(in

orde

r:cu

ltiva

tor,

seed

er,h

arve

ster

,thr

eshe

r)is

repr

esen

ted.

Man

ufac

ture

ofcu

ltiva

tors

(a)

isw

idel

ydi

stri

bute

d,w

hile

prod

uctio

nof

the

larg

er,m

ore

expe

nsiv

eha

rves

teri

sco

ncen

trat

edw

ithin

the

man

ufac

turi

ngbe

lt(c

).So

urce

:U

.S.C

ensu

sof

Man

ufac

ture

s18

80.

6

comitant decline of manufacturing with the decline of agriculture during the initialrise of manufacturing in the United States. Ellison and Glaeser (1999) find about20 percent of geographic concentration can be explained by selected natural advan-tages in their study and conclude that enough concentration remains unexplainedthat local intraindustry spillovers must play a major role in the more concentratedindustries. Another thread (e.g. Midelfart-Knarvik et al (2001), Head and Mayer(2004), Wolf (2007)) emphasizes market access, using the metric of market po-tential. Market potential can be thought of as potential demand discounted bydistance from the producer’s location; the original formulation was introduced byHarris (1954) and was basically ad hoc, but a version adapted to the Dixit-Stiglitzmodel was derived by Krugman (1992). Klein and Crafts (2011) find that mar-ket potential was key for explaining the rise of the American manufacturing belt,with few other statistically significant elements, challenging the conclusion of Kim(1999). One notable work is that of Greenstone et al. (2010), which finds a 12percent advantage in TFP for plants near a newly opened plant five years after theopening.

For the purpose of comparability, I use a specification inspired by the MKOVmodel described in Midelfart-Knarvik et al (2001), applied to the agricultural im-plements industry for census years from 1870 to 1900 to address the question ofrelative impact of three types of determinants of industrial location: proximity todemand markets, proximity to similar manufacturers (spillovers), and factor en-dowments. For these census years, data is available at the state level for the outputof individual implements, which would correspond approximately to the 5-digitSIC level. Implements can furthermore be categorized according to their intendeduse, which dictates both the location of the demand markets and what types of man-ufacturing activity might provide spillover benefits. The differences in geographicdistribution can be large (see Figure 2). This is an indication of how different thelocation problem of supplying to agriculture is from that of supplying finished con-sumption goods. If it were the case that market potential based on GDP were thekey driver for firm location (as Klein and Crafts find), then we would expect to findthe majority of implements manufacturing in New York and Pennsylvania, as wedo for manufacturing in general. Instead, while New York is still a major player, itis third behind Ohio and Illinois. I will attempt to explain the distribution of manu-facturers in terms of producers’ proximity to crops and other producers of interest,and to their access to labor and capital, up to the end of the 19th century, at theproduct level for 53 implements and 40 states which have non-zero production.

7

2 Empirical Design

My specification is based partly on the model developed by Midelfart-Knarvik etal. (2001) (henceforth, MKOV), and subsequently used by Wolf (2007) and Kleinand Crafts (2011), which derives from the usual CES demand system the followingestimating equation:

skit = c(νi : k, t)1−ηm(uk : i, t)exp[εk

it ] (1)

where c is the unit cost function and m is market potential. Log-linearizing thisaround a reference point captures many of the linkages of interest with the basicform

ln(skit) = α +∑

jβ

j(y jit − y j)(x jk

t − x j)+ εkit (2)

where skit is the share of domestic gross output by value for industry k in state i in

period t and j denotes a pairing of a location characteristic (values y) with an in-dustry characteristic (values x), which are believed to jointly affect the desirabilityof a location for firms in the given industry. In my case, each value of k woulddenote a specific implement. The parameters y j and x j are referred to as referencevalues, since they denote values for which the share of output in a state or indus-try would be independent of the corresponding industry or location characteristic.This model can be written as:

ln(skit) = (α +∑

jy jx j)+∑

j(β jy j

itxjkt −β

jy jx jkt −β

jx jy jit)+ ε

kit (3)

which makes it clear that each linkage can be expressed in the form of an inter-action between a state characteristic and industry characteristic, expanded at thereference point–the coefficients to be estimated in a regression analysis are β j onthe interactions and −β jy j and −β jx j on industry and state characteristics respec-tively.

Log-linearization as an econometric strategy carries some downsides, however,chiefly the fact that it deals poorly with zeros. At the 5-digit SIC equivalent levelof disaggregation obtained when considering each implement as a separate indus-try, there will be many zeros in the production data. Furthermore, unless ratherstringent criteria on the errors are fulfilled, OLS will not be consistent (SantosSilva and Tenreyro 2006). Both of these problems can be overcome by applyingthe Poisson pseudo-maximum-likelihood (PPML) estimator suggested by Santos

8

Silva and Tenreyro directly to the estimating equation (1); this reduces the neces-sary assumption for consistency to the form of the conditional mean, that is, thatE[sk

it |x] = exp(xiβ ), which should be compatible with the definition given in equa-tion (1).

I express the model as:

skit =β1 (lnSHAREURBANit ×T ECHGROUPk)

+β2 (lnEDUCAT EDPOPit ×T ECHGROUPk)

+β3 (lnKLRAT IOit ×T ECHGROUPk)

+β4 (lnCROPMARKET POT ENT IALikt)

+β5 (lnT ECHMARKET POT ENT IALikt)

+β6 (lnMARKET POT ENT IALit)

+∑i

γiSTAT Eit +∑k

θkIMPLEMENTkt + εikt

where STAT E and IMPLEMENT are dummies for states and implements respec-tively, and T ECHGROUP is a set of dummy variables denoting groups of im-plements arranged roughly by level of sophistication. Since implement-specificmeasures of labor and capital requirements are not available, I substitute for themby categorizing implements into four groups and compare the impact of endow-ments on each category–more complex implements are expected to require moreskilled labor and capital to manufacture. In category 1 are traditional hand toolssuch as hoes and scythes; category 2 consists of early mechanized implements (e.g.the reaper). Category 3 contains implements which are not thought to be excep-tionally complex but were introduced late in the sample period and may thereforebenefit from later technological developments, while category 4 are those complex“second generation” mechanized implements (e.g. binding harvesters, an advanceddevelopment of the mechanical reaper). The first three terms in this specification,which feature the technology group dummy, are interactions intended to representthe effect of factor endowments on location by group, these being labor pooling,availability of skilled labor, and capital endowment respectively. I also look at al-ternative measures–mean level of schooling and experience in place of educatedpopulation and wage level in place of urban population.

Unlike the first three terms, the fourth and fifth terms in the specification are not ex-plicitly interactions between a state characteristic and an implement characteristic,but the market potential term can be thought of as that part of the whole market po-tential which influences location for the implement at hand (e.g. for cotton planters,the crop market potential would be equivalent to the total market potential for all

9

crops interacted with a function that multiplied the contribution of each region bythe fraction of the crop which is cotton). The fourth term is a measure of theimpact of downstream market potential. Implements manufacturers will naturallylocate nearer to large concentrations of farms producing crops that the implementsin question are useful for (see Figure 2) because of the direct impact on transportcosts, but this term will also absorb any other effect stemming from close proximityto customers, e.g. better feedback leading to reduced development costs. The fifthterm, “technology market potential,” addresses the issue of spillovers by measuringthe effect of proximity to manufacturers producing implements with similar func-tionality; the underlying mechanism would be that implements designed to performsimilar tasks (even if on different crops) will share features that can be copied oradapted between manufacturers. For example, a mower is a tool for harvestinghay. Developments in reapers or binding harvesters might be transferable to mow-ers, since they have some common mechanisms: both are machines for cutting tallplants, they can be horse-drawn and seat the operator. The final term covers theimpact of a “general” market potential of the type used in previous articles; this iscalculated from regional GDP and is included to account for proximity to generaleconomic activity which may be attractive to manufacturers. If it were the case thatthe agricultural implements industry has no special connection to either farmers orrelated manufacturers but only to manufacturing activity in general, this interactionwould have high explanatory power.

The market potentials used here follow the form introduced by Harris (1954):

MPi = ∑j

Yj/di j

with di j being the distance between regions i and j. When using such a measureit is necessary to address the issue of how distance is to be assessed, particularlyas regards the impact of transportation infrastructure. A variety of approaches tothis problem have been used, ranging from arguing that transportation networksare more or less complete and making no adjustments to great circle distances (e.g.Klein and Crafts 2011) to exhaustively calculating minimum route lengths withGIS (Donaldson and Hornbeck 2015). While the GIS method is very accurate inprinciple, it requires two assumptions about route efficiency that may not hold true:first, that the estimate of wagon route distance (which cannot be found using GIS)is correct, and second, that the shortest route is also the cheapest route. Certainly,farmers in several states were sufficiently upset about perceived rate discriminationto pass the Granger laws in an attempt to force railroads to charge more favorablerates. In the present situation, manufacturing output data is at the state level, so lackof geographical disaggregation precludes making full use of the GIS method in any

10

event. However, because relevant market potentials for agricultural implements canbe driven by locations with low population and poor railroad access to a greaterdegree than most final consumer goods, I elect to adjust the distance over the inter-state distance estimates based on the cost of road wagon transportation. Effectivedistance between two states is therefore the interstate distance between centers ofstates by railroad (assuming states are roughly circular, the mean distance to points

within a state will be d =23

√Aπ

.3), plus an estimate of the average distance traveled

within the destination state by wagon. This wagon distance is estimated based onthe density of track in miles of track per square mile of land area; the distance isthen added to the railroad at a penalty rate based on the ratio of cost per ton-mileto the railroad freight cost. This ratio ranges from a low of 4.84 in 1870 to 20.5 in1900, reflecting a steep decline in railroad freight rates; wagon costs per ton-mileare largely stagnant over the period (Carter et al 2006). More details can be foundin the appendix.

3 Data

The majority of the underlying data comes either directly or indirectly from the USCensus. Data on the scale of agricultural implements manufacturing come fromthe Census of Manufactures industry special reports at the state-implement levelgathered as part of the decennial Census from 1870 to 1900. Variables includenumber of establishments, total workers, capital, total wages, and value of inputsand outputs. Worker counts are broken into men, women and children; however,adult men comprise over 96 percent of the industry workforce in all periods, sosignificant heterogeneity stemming from worker demographics is unlikely. I there-fore refer only to the total number of hands in each period. The outstanding featureof the special reports is the tabulation of output of each implement. Studies of late19th century industrial location typically have industry data disaggregated only to alevel comparable to 2-digit SIC, but the individual product tabulations in the specialreports are comparable to a 5-digit level of disaggregation. The Census of Agricul-ture (also decennial 1870-1900) provides data on the crop output for the purposeof calculating market potential for the backward linkages. Data on harvests are de-tailed and include the yields of several dozen farm products, and their acreage. For

3States are typically not actually circular, but the difference in estimated distance between a circleand a square is only about 2 percent, which is unlikely to be a greater source of inaccuracy than theassumption of uniformly distributed activity within the state, unless the state is very oblong.

11

categorizable implements, I organize these into 13 crops or groups of crops4 whichI use to construct the demand or crop market potentials5. Rounding out the censusdata is the population Census containing tables of reported occupations at the statelevel. I use these to obtain the share of the workforce who are professionals. I alsorefer to Haines’s (2004) digitization of the Census data, which includes number offarms by size, acreage of improved and unimproved land, farm capital divided intocategories (including value of farm implements and machinery), and output.

Table 2 summarizes the size and output of the industry in the period covered bythe study. While growing considerably in size, the industry experiences its maingrowth in labor productivity during the decade between 1880 and 1890. By 1900,the industry has undergone a great deal of consolidation and can be consideredlargely established. Additionally, the interval of data collection changes for theCensus of Manufactures so that the data sources are no longer concurrent; thereforeI choose 1900 as the end date for the sample.

Table 2: Industry Size and Output

Establishments Hands Output (1900 dollars)

1870 2076 25249 $52,066,875

1880 1943 39580 $68,640,486

1890 910 42544 $81,271,651

1900 715 56628 $98,010,506Source: Census of Manufactures 1870-1900.

There are three groups of market potentials to be constructed: crop market poten-tial, technological potential, and general (or GDP) market potential, which func-tions as a control. As noted by Klein and Crafts (2011), internal trade flows dataare unavailable before 1949, so I follow them in constructing market potential us-ing Harris’s (1954) method of inverse distance-weighted sums. A separate marketpotential is calculated for each crop and implement category (of which there arefour: seeders, cultivators, harvesters, and separators). If an implement is capable

4Wheat, rye, barley and oats are grouped together as “small grains” because they can use thesame equipment; likewise, potatoes and sweet potatoes are grouped.

5It is in some cases necessary to calculate the values of crops themselves; the appendix containsfurther details.

12

of serving more than one crop type, the market potential will be the sum of indi-vidual crops’ market potentials. State level income estimates are drawn from Klein(2009); average education and experience figures for alternate specifications arebased on estimates by Turner et al (2006). As mentioned briefly above, I handledistances by estimating interstate distances as being on a railroad with distancebetween the centers of each state in a pair, and the intrastate distance as the ap-proximate distance from a railroad based on railroad density. Therefore, a railroadmap is necessary to correctly estimate the transport costs needed to find market po-tential. For this purpose, I use U.S. state maps for 1870 to 1900 (Siczewicz 2011)to calculate the distances between states and area of states. The length of track instate is drawn from the Statistical Abstract of the United States; this number andthe land area of the state are used to estimate the track density and the distancetraveled.

The combination of the above data sources yields a dataset on 53 implements infour categories in 40 states and four years, with five state characteristics and twoindustry-state characteristics (the crop and technology market potentials)6.

4 Results

In this section I discuss the results of Poisson estimation on the specification de-fined in the Empirical Design section above. As previously discussed, due to thedisaggregation of the implements and the geographical concentration of many ex-amples thereof, there will be many zeros in the data, so the log-linear model usedin some of the prior art is contraindicated. A similar problem is frequently facedin gravity estimation; the Poisson pseudo-maximum likelihood estimator (SantosSilva and Tenreyro 2006) is able to retain most of these observations while cor-recting for certain biases. The downside is that the possible endogeneity of marketpotentials must still be addressed and the use of a non-linear model will complicatethe use of instruments.

Tables 3 and 4 report the results of estimation on the previously-defined specifica-tion, with standard errors clustered by state. Here, the values of the market poten-tials are scaled so that the mean for each implement is equal to 1; under the PPMLmodel the estimated coefficients can be interpreted as elasticities. The key results

6Market potentials are normalized to a mean of 1. Different implements vary widely in size ofmarket; this allows state shares in their production to be compared to each other.

13

are first, that both downstream market access (Crop MP) and proximity to similarmanufacturers (Tech MP) are statistically significant at the 0.1 percent level, withthe effect of downstream market access being in the range of 1.5 times as strong asproximity to manufacturers. Second, after accounting for proximity to implement-specific geographical influences, I find no further impact of general market poten-tial. If the agricultural implements industry were not particularly influenced by thelocation of growing regions, we should expect to find that it would behave simi-larly to other manufactures and be positively associated with the general marketpotential (GDP MP). Since this is not observed, the key downstream influence isshown to be the location of agriculture. I also find no statistically significant in-fluence for the interaction on capital-labor ratio. For basic tools the proportion ofprofessional workers is significant at the 5 percent level in some specifications;one possible reason is the prevalence of smaller farms in the Eastern states whichpreviously held a larger share of hand tool manufacturing and which also have ahigher share of professionals. The third HO interaction, on urban share or industrywage, is marginally significant, and in the case of industry wages on larger im-plements such as reapers and its more advanced developments (categories 2 and4), it can be strongly significant. Industry wages are likely to reflect productivity,so this provides some support for the idea that a large supply of skilled workerswas an inducement to locate in a state, at least for manufacturers of heavier andmore complex equipment. Specifications 2 to 4 also include interactions betweenthe market potentials and year fixed effects, shown in Table 4, with significanceat the 5 percent level suggesting that the value of proximity to demand may havebeen weaker in the decade before 1890. If so, this change coincides with a periodof strong consolidation in the industry with number of operating manufacturers de-clining by more than half, from 1943 plants to just 910, between the 1880 and 1890censuses.

Due to the danger of endogeneity in market potential measures, I use two instru-ments: the first, 10-year lagged values of crop market potential. Both crop andtechnology market potential measures are strongly correlated over time–crop mar-ket potential extremely so, with correlations of over 0.9 between decades. Whileit is in principle possible that past market potentials could directly influence thecurrent location of industry, this risk is reduced by the decade-long gap betweenobservations. Though direct data on firm lifetimes is hard to find, the combinationof continuous industry consolidation over the period of interest, the lack of a sig-nificance on a capital channel in the preceding estimates, and some later experiencewith the auto industry indicate that non-leading firms are unlikely to be long-lived.Therefore, past crop market potential should only affect industry location throughits impact on current market potential. As a check on this assumption, I also run

14

Table 3: Clustered Poisson regression for manufacturing share, market potential and factorendowment-tech interactions.

(1) (2) (3) (4)Output share Year*MP Wages Urban+wages

Crop MP 2.800∗∗∗ 3.286∗∗∗ 3.277∗∗∗ 3.283∗∗∗

(8.72) (9.85) (9.11) (9.37)Tech MP 2.046∗∗∗ 2.229∗∗∗ 2.147∗∗∗ 2.163∗∗∗

(5.36) (5.32) (5.02) (5.30)GDP MP -5.012 -9.870 -9.364 -9.690

(-1.20) (-1.58) (-1.49) (-1.56)

Tech Group 2 × Share Pro -1.106 -1.090 -0.716 -1.180(-1.34) (-1.39) (-1.03) (-1.58)

Tech Group 3 × Share Pro -1.812 -1.384 -0.935 -2.118(-1.10) (-0.90) (-0.86) (-1.08)

Tech Group 4 × Share Pro 1.533 1.425 1.811 1.377(1.06) (1.02) (1.29) (1.00)

Tech Group 2 × K/L -0.0909 -0.0638 -0.382 -0.367(-0.17) (-0.12) (-0.82) (-0.79)

Tech Group 3 × K/L -0.237 0.241 -0.0361 -0.268(-0.17) (0.19) (-0.03) (-0.21)

Tech Group 4 × K/L -0.734 -0.686 -1.240 -1.221(-1.00) (-0.93) (-1.62) (-1.66)

Tech Group 2 × Urban share 0.758∗ 0.773∗ 0.622(2.51) (2.34) (1.90)

Tech Group 3 × Urban share 1.559∗ 1.325∗ 1.157(2.08) (2.02) (1.65)

Tech Group 4 × Urban share 0.969 0.968 0.766(1.88) (1.83) (1.39)

Tech Group 2 × State industry wage 1.835∗∗ 1.100∗

(2.63) (2.04)Tech Group 3 × State industry wage 3.614∗ 2.795

(2.29) (1.45)Tech Group 4 × State industry wage 2.745∗∗ 1.855∗∗∗

(3.15) (3.56)

Constant 2.235 2.247 -12.31 -10.42(0.18) (0.18) (-0.86) (-0.60)

Time Interactions NO YES YES YESObservations 4951 4951 4951 4951

Notes: t statistics in parentheses, ∗ p < 0.05, ∗∗ p < 0.01, ∗∗∗ p < 0.001. Columns: (1) No year interactions (2)Year interaction with main market potentials (3)-(4) Year interaction and alternative labor measures; using stateindustry average wage costs a small number of observations due to no within-industry wage being availablefor states that have zero production. State and product fixed effects are included in all specifications; marketpotentials are scaled to a mean of 1.

15

Table 4: Clustered Poisson regression for manufacturing share, year on marketpotential effects.

(1) (2) (3) (4)Output share Year*MP Wages Urban+wages

Crop MP 2.800∗∗∗ 3.286∗∗∗ 3.277∗∗∗ 3.283∗∗∗

(8.72) (9.85) (9.11) (9.37)Tech MP 2.046∗∗∗ 2.229∗∗∗ 2.147∗∗∗ 2.163∗∗∗

(5.36) (5.32) (5.02) (5.30)GDP MP -5.012 -9.870 -9.364 -9.690

(-1.20) (-1.58) (-1.49) (-1.56)

Share Pro 1.515 2.439∗ 2.239∗ 2.483∗

(1.32) (2.19) (1.97) (2.36)K/L -0.307 0.0425 0.373 0.251

(-0.51) (0.07) (0.62) (0.39)Share Urban -0.564 -0.327 -0.126

(-0.58) (-0.37) (-0.14)State Industry Wage -1.375∗ -0.763

(-1.97) (-1.35)

1870 × Crop MP -0.523 -0.498 -0.458(-1.01) (-0.97) (-0.86)

1880 × Crop MP -0.998 -1.062 -1.031(-1.83) (-1.88) (-1.89)

1890 × Crop MP -0.0282 -0.0390 -0.0484(-0.07) (-0.09) (-0.13)

1870 × Tech MP -0.537 -0.573∗ -0.500(-1.18) (-2.01) (-1.09)

1880 × Tech MP 0.254 0.351 0.345(0.50) (0.76) (0.68)

1890 × Tech MP -0.762∗ -0.737∗ -0.675(-2.16) (-2.31) (-1.89)

Time Interactions NO YES YES YESObservations 4951 4951 4951 4951

Notes: t statistics in parentheses, ∗ p < 0.05, ∗∗ p < 0.01, ∗∗∗ p < 0.001. Columns: (1) Noyear interactions (2) Year interaction with main market potentials (3)-(4) Year interactionand wage measures; using state industry average wage costs a small number of observationsdue to no within-industry wage being available for states that have zero production. Hereare shown time effects on the market potential coefficients; GDP MP time effects are allinsignificant and dropped for length.

16

the analysis with 20-year lags (see Table 6). The second set instruments for the ge-ographical distribution of implement manufacturing by relating each state to fixedgeographical locations. For each of the four years in the sample I construct in-struments which are the inverse distance from the center point of the implementsindustry in those years. Alternatively, I instrument with distance from three cities:Chicago, New York, and Dayton, Ohio, which is chosen because it is close to thecenter point of the manufacturing belt and is strongly correlated with technologymarket potential for each of the four implement categories over the period 1870-1900.

IV estimation is performed using two-step GMM on the Poisson model, however,including fixed effects in an instrumental variables regression on the Poisson modelmay not yield a consistent estimator. In order to address this issue I also provide theresult of Poisson estimates without instruments, dropping the fixed effects. Theseresults are shown in Table 5. The key comparison is between columns 2 and 3,which are the non-IV Poisson without fixed effects, and the Poisson estimate withIV. Losing the fixed effects on state and implement from column 1 to column 2produced a moderate change in regression coefficients, but the coefficient magni-tudes are largely unchanged between columns 2 and 3, though the standard errorsin the IV regression are naturally much larger. The very similar appearance ofthe instrumented coefficients suggests that any endogeneity in the market poten-tials as regressors for share of manufacturing output is mild. The outcomes of thealternative instrument specifications are shown in Table 6; columns 1 and 2 com-pare the base IV specification with the alternate fixed distance instruments, andcolumns 3 and 4 compare the base IV specification for years 1880-1900 with al-ternate 20-year lagged crop market potentials. In each comparison, the coefficientsare qualitatively similar.

5 Conclusion

I have estimated the relative impact of three channels that may influence indus-trial location for the US agricultural implements industry. The estimate on generalmarket potential rule out the possibility that agricultural implements manufactur-ing location is primarily associated with general consumer demand. Rather, thelocation of the industry is clearly driven by access to agricultural demand. Cropmarket potential, which includes the direct effect on shipping costs of proximity toconsumers as well as other potential benefits such as access to feedback, is a strong

17

Table 5: Instrumental variables Poisson regression for manufacturing share.

(1) (2) (3) (4)FE Poisson, no FE IV IV alternate

Crop MP 2.800∗∗∗ 2.165∗∗∗ 2.156∗∗∗ 2.217∗∗∗

(8.72) (5.75) (3.78) (3.74)Tech MP 2.046∗∗∗ 1.806∗∗∗ 1.917∗∗ 1.801∗

(5.36) (4.94) (2.59) (2.19)GDP MP -5.012 -0.841 -1.564 -1.518

(-1.20) (-0.94) (-1.54) (-1.41)

Share Pro 1.515 0.910 0.480 0.350(1.32) (0.97) (0.47) (0.34)

Tech Group 2 × Share Pro -1.106 -0.965 -1.178∗ -1.217∗

(-1.34) (-1.63) (-2.02) (-2.15)Tech Group 3 × Share Pro -1.812 -2.061 -1.843 -1.738

(-1.10) (-1.40) (-1.68) (-1.57)Tech Group 4 × Share Pro 1.533 0.0710 0.101 0.743

(1.06) (0.09) (0.16) (1.09)

K/L -0.307 0.198 0.125 0.156(-0.51) (0.45) (0.28) (0.27)

Tech Group 2 × K/L -0.0909 -0.327 -0.427 -0.436(-0.17) (-1.40) (-1.86) (-1.14)

Tech Group 3 × K/L -0.237 -0.657 -0.645 -0.850(-0.17) (-1.14) (-1.59) (-0.98)

Tech Group 4 × K/L -0.734 0.183 0.143 -0.982(-1.00) (0.53) (0.54) (-1.77)

Urban share -0.564 0.275 0.618 0.586(-0.58) (0.51) (0.98) (0.91)

Tech Group 2 × Urban share 0.758∗ 0.605 0.542 0.547(2.51) (1.62) (1.22) (1.24)

Tech Group 3 × Urban share 1.559∗ 1.679∗∗ 0.972 0.930(2.08) (2.89) (1.90) (1.80)

Tech Group 4 × Urban share 0.969 1.155 0.710 0.670(1.88) (1.96) (1.36) (1.20)

State industry wage 0.296(0.58)

Tech Group 2 × State industry wage -0.00640(-0.02)

Tech Group 3 × State industry wage 0.286(0.37)

Tech Group 4 × State industry wage 1.633∗

(2.40)Observations 4951 4951 4951 4951

Notes: t statistics in parentheses, ∗ p < 0.05, ∗∗ p < 0.01, ∗∗∗ p < 0.001. Columns: (1) Non-IV Poisson (asTable 4 col. 1) (2) Non-IV Poisson without fixed effects (3)-(4) Poisson with IV and two labor measures. TheIV regressions cannot be run with fixed effects, but note the similarity in coefficients between (2) and (3).

18

Table 6: Comparison of alternative IV specifications.

(1) (2) (3) (4)IV Alt. Tech IV IV, no 1870 Alt. Crop IV

Crop MP 2.156∗∗∗ 2.209∗∗∗ 2.026∗∗∗ 2.398∗∗∗

(3.78) (4.07) (3.64) (3.83)Tech MP 1.917∗∗ 1.578∗∗ 1.921∗∗ 1.714∗

(2.59) (2.58) (2.90) (2.47)GDP MP -1.564 -0.734 -1.667 -1.617

(-1.54) (-0.90) (-1.64) (-1.62)

Share Pro 0.480 0.908 0.641 0.625(0.47) (1.03) (0.61) (0.61)

Tech Group 2 × Share Pro -1.178∗ -0.934 -1.029 -1.038(-2.02) (-1.72) (-1.41) (-1.46)

Tech Group 3 × Share Pro -1.843 -1.612 -1.937∗ -1.869∗

(-1.68) (-1.41) (-2.11) (-2.11)Tech Group 4 × Share Pro 0.101 0.0643 0.357 0.374

(0.16) (0.09) (0.47) (0.50)

K/L 0.125 0.213 -0.135 -0.109(0.28) (0.52) (-0.27) (-0.22)

Tech Group 2 × K/L -0.427 -0.314 -0.345 -0.350(-1.86) (-1.47) (-1.23) (-1.29)

Tech Group 3 × K/L -0.645 -0.502 -0.655 -0.624(-1.59) (-1.14) (-1.83) (-1.81)

Tech Group 4 × K/L 0.143 0.166 0.296 0.315(0.54) (0.56) (0.94) (1.01)

Urban share 0.618 0.264 0.636 0.649(0.98) (0.54) (0.93) (0.95)

Tech Group 2 × Urban share 0.542 0.588 0.670 0.666(1.22) (1.70) (1.36) (1.39)

Tech Group 3 × Urban share 0.972 1.388∗∗ 1.108∗∗ 1.119∗∗

(1.90) (3.07) (2.81) (2.87)Tech Group 4 × Urban share 0.710 1.052∗ 1.090∗ 1.170∗

(1.36) (2.06) (2.48) (2.53)Observations 4951 4951 4076 4076t statistics in parentheses∗ p < 0.05, ∗∗ p < 0.01, ∗∗∗ p < 0.001

Notes: t statistics in parentheses, ∗ p < 0.05, ∗∗ p < 0.01, ∗∗∗ p < 0.001. Columns: (1) IV Poisson (asTable 5 col. 3) (2) IV Poisson with alternate (3-city) IV (3) IV Poisson as col. 1, from 1880-1900 (4)IV Poisson with 20-year lagged crop market potentials.

19

driver of location choices, with an elasticity of around 3. This interaction is esti-mated to be roughly 1.5 times as strong in determining manufacturing location asproximity to manufacturers of similar implements. That second channel of proxim-ity to similar manufacturers may include benefits such as shared infrastructure butalso technological spillovers. For HO-type interactions, which measure the influ-ence of factor endowments, I find that capital-related channels are not statisticallysignificant, but that industry wages and availability of professionals have an impacton concentration of larger, more complex implements. This could be consideredtentative evidence for an effect of unobserved skills in the workforce. This channelappears to be of comparable strength to that of the market potential terms.

Strong linkage effects put this article in agreement with much of the post-2000work in the area of location effects on industrialization. Particularly, the strongimpact of proximity to agricultural customers on the production of technologicallyadvanced capital goods indicates that, for the United States, a large and commer-cialized agricultural sector may have been a boon to industrializing entrepreneursand accelerated the transition to a manufacturing economy. The positive estimatesconnecting implements manufacturers to those working on similar equipment im-ply that existing manufacturers have the potential to attract new manufacturing ac-tivity to the states they are located in. Subsequent export behavior in the early 20thcentury indicates that further work on the development of technologies relating tothe location of agriculture may also bear fruit, as American manufacturers appearto lead where implement mechanisms (e.g. plow and reaper blades) are concernedbut lag behind in implements such as traction engines (Dennis 1909) where thewide range of experience in soil and climate conditions cannot provide benefits tothe product designer. Further examination of the related question of whether pro-duction of technologies that served the agricultural market impacted the growth ofmanufacturing in general is needed to decide the importance of this channel, butthe combination of the results is suggestive: the possibility that certain “trailbreak-ing” industries might have had an impact on the location of American industry inexcess of their size cannot be ruled out.

20

6 References

Baldwin, R. 2011, Trade and industrialization after globalisation’s 2nd unbundling:How building and joining a supply chain are different and why it matters. NationalBureau of Economic Research Working Paper No. 17716, Cambridge, MA.

Broadberry, S. N. 1998, How Did the United States and Germany Overtake Britain?A Sectoral Analysis of Comparative Productivity Levels, 1870-1990. The Journalof Economic History, 58(2): 375-407.

Carter, S., Gartner, S., Haines, M., Olmstead, A., Sutch, R., Wright, G. 2006,Historical Statistics of the United States. Cambridge: Cambridge University Press.

Clark, V. S. 1916, History of Manufactures in the United States 1607-1860. Wash-ington, D.C.: Carnegie Institution of Washington Publication No. 215B.

Ellison, G., Glaeser, E. L. 1999, The Geographic Concentration of Industry: DoesNatural Advantage Explain Agglomeration? American Economic Review, 89(2):311316.

Haines, M. R. 2004, Historical, Demographic, Economic, and Social Data: TheUnited States, 1790-2002. ICPSR02896-v3. Ann Arbor, MI: Inter-university Con-sortium for Political and Social Research [distributor], 2010-05-21. http://doi.org/10.3886/ICPSR02896.v3

Harley, C. K. 1992, International Competitiveness of the Antebellum AmericanCotton Textile Industry. The Journal of Economic History, 52(3): 559584.

Harris, C. 1954, The market as a factor in the localization of industry in the UnitedStates. Annals of the Association of American Geographers, 64: 315348.

Head, K., Mayer, T. 2004, Market Potential and the Location of Japanese Firms inthe European Union. The Review of Economics and Statistics, 86(4): 959-972.

Kim, S. 1999, Regions, resources, and economic geography: sources of U.S.regional comparative advantage, 18801987. Regional Science and Urban Eco-nomics, 29: 132.

Klein, A., Crafts, N. 2011, Making sense of the manufacturing belt: determinantsof US industrial location, 18801920. Journal of Economic Geography, 12: 775807.

21

Krugman, P. 1992, A Dynamic Spatial Model. National Bureau of Economic Re-search Working Paper No. 4219, Cambridge, MA.

Lindauer, D. L., Pritchett, L. 2002, What’s the Big Idea? The Third Generation ofPolicies for Economic Growth. Economia, 3(1): 1-39.

McLean, I. W. 1976, Anglo-American Engineering Competition, 1870-1914: SomeThird-Market Evidence. The Economic History Review, 29(3): 452-464.

Meyer, D. R. 1989, Midwestern Industrialization and the American ManufacturingBelt in the Nineteenth Century. The Journal of Economic History, 49(4): 921937.

Midelfart-Knarvik, K. H., Overman, H. G., Venables, A. J. 2001, Comparativeadvantage and economic geography: estimating the determinants of industrial lo-cation in the EU. London: CEPR at London School of Economics.

Moretti, E. 2004, Estimating the social return to higher education: evidence fromlongitudinal and repeated cross-sectional data. Journal of Econometrics, 121:175212.

Moretti, E. 2012, The New Geography of Jobs. New York, NY: Houghton MifflinHarcourt Publishing Company.

Olmstead, A. L., Rhode, P. W. 2002, The Red Queen and the Hard Reds: Produc-tivity Growth in American Wheat, 18001940. The Journal of Economic History,62(4): 929-966.

Perloff, H. S., Dunn Jr, E. S., Lampard, E. E., Keith, R. 1960, Regions, resources,and economic growth. Regions, resources, and economic growth.

Santos Silva, J. M. C., Tenreyro, S. 2006, The Log of Gravity. Review of Economicsand Statistics, 88(4): 641658.

Wolf, N. 2007, Endowments vs. market potential: What explains the relocation ofindustry after the Polish reunification in 1918? Explorations in Economic History,44: 2242.

22

7 Data

Dennis, Roland R. 1909, American Agricultural Implements in Europe, Asia, andAfrica. Washington, D.C.: Government printing office.

Siczewicz, Peter. 2011, U.S. Historical Counties. Dataset. Emily Kelley, digitalcomp. Atlas of Historical County Boundaries, ed. by John H. Long. Chicago: TheNewberry Library. Available online from http://publications.newberry.org/ahcbp.

U.S. Bureau of Foreign and Domestic Commerce. 1918, Department of Com-merce. Statistical Abstract of the United States, vol. 41, 1918. Washington, D.C.:Government printing office.

U.S. Census Bureau. 1864, Manufactures of the United States in 1860; compiledfrom the original returns of the eighth census, under the direction of the Secretaryof the Interior. Washington, D.C.

U.S. Census Bureau. 1865, Agriculture of the United States in 1860; compiledfrom the original returns of the Eighth Census, under the direction of the Secretaryof the Interior. By Joseph C.G. Kennedy, Superintendent of Census. Washington,D.C.

U.S. Census Bureau. 1872, Ninth Census – Volume III. The statistics of the wealthand industry of the United States, embracing the tables of wealth, taxation, andpublic indebtedness; of agriculture; manufactures; mining; and the fisheries, withwhich are reproduced, from the volume of population, the major tables of occupa-tions, compiled from the original returns of the ninth census (June 1, 1870) underthe direction of the Secretary of the Interior, by Francis A. Walker, Superintendentof Census. Washington, D.C.

U.S. Census Bureau, U.S. Bureau of Foreign and Domestic Commerce, U.S. Dept.of Commerce and Labor Bureau of Statistics, U.S. Dept. of the Treasury Bureauof Statistics. 1878, Foreign commerce and navigation of the United States. Wash-ington, D.C.: Government printing office.

U.S. Census Bureau. 1883, Department of the Interior, Census Office. Statistics ofthe population of the United States at the tenth census (June 1, 1880), embracingextended tables of the population of states, counties, and minor civil divisions,with distinction of race, sex, age, nativity, and occupations; together with summary

23

tables, derived from other census reports, relating to newspapers and periodicals;public schools and illiteracy; the dependent, defective, and delinquent classes, etc.

U.S. Census Bureau. 1883, Department of the Interior, Census Office. Report onthe manufactures of the United States at the tenth census (June 1, 1880), embracinggeneral statistics and monographs on power used in manufactures; the factory sys-tem; interchangeable mechanism; hardware cutlery, etc.; iron and steel; silk man-ufacture; cotton manufacture; woolen manufacture; chemical products and salt;glass manufacture. Washington, D.C.

U.S. Congress, Senate Select Committee on wages and prices of commodities,Henry Cabot Lodge. Investigation relative to wages and prices of commodities,vol. 1, 1911. Washington, D.C.: Government printing office.

8 Appendix

8.1 Railroads and Distance Estimates

The construction of the distance variable consists of two main parts. The first isthe distance either between the geographical centers of the two states in question,obtained using the GIS maps made by Siczewicz (2011). The distances themselvesare calculated using Vincenty’s formulae, which account for the oblate spheroidshape of the Earth. The second part of the distance variable is an estimate of thedistance that must be traveled off the railroad by wagon once arriving in the desti-nation state (defined to be the state to be summed over). I obtain my estimate fromthe railroad track density by finding the minimum average distance from the rail-road within the state: effectively, if the state’s area were a rectangle the length ofall the track in the state, this would be one-quarter the width of that rectangle. Forsome states and territories with very poor railroad networks, this estimate exceedsthe estimate of average distance between points within the state; in this case I usethe smaller number. Note that both of these distances are sure to be underestimatesof the real distance traveled, but in the market potential calculation, distances arerelative. Since both estimates are done on the same map, the degree of underes-timation of the distances should be similar and should be equivalent to a scalingfactor which drops out when the market potential figures are normalized.

In the base specification the effective distance is the sum of these two parts, with

24

Table 7: Comparison of alternative distance specifications.

(1) (2) (3)Base Spec Vincenty Alt Distance

Crop MP 3.286∗∗∗ 2.864∗∗∗ 2.586∗∗∗

(9.85) (10.06) (12.52)Tech MP 2.229∗∗∗ 2.086∗∗∗ 1.980∗∗∗

(5.32) (6.17) (7.14)GDP MP -9.870 -10.81∗ -5.391∗

(-1.58) (-2.13) (-1.98)

Share Pro 2.439∗ 2.255∗ 2.276∗

(2.19) (2.06) (2.13)K/L 0.0425 0.220 0.0662

(0.07) (0.33) (0.12)Urban share -0.327 -0.384 -0.412

(-0.37) (-0.48) (-0.50)

1870 × Crop MP -0.552 -0.482 -0.374(-1.00) (-0.92) (-1.03)

1880 × Crop MP -0.997 -0.887 -0.754∗

(-1.83) (-1.81) (-2.34)1890 × Crop MP -0.00797 -0.0570 0.0757

(-0.02) (-0.14) (0.35)

1870 × Tech MP -0.555 -0.360 -0.566(-1.22) (-0.81) (-1.63)

1880 × Tech MP 0.215 0.160 0.149(0.43) (0.42) (0.43)

1890 × Tech MP -0.798∗ -0.736∗ -0.515∗

(-2.29) (-2.44) (-2.31)

Tech Group 2 × Urban share 0.773∗ 0.783∗ 0.734∗

(2.34) (2.46) (2.17)Tech Group 3 × Urban share 1.325∗ 1.434∗ 1.277∗

(2.02) (2.18) (2.04)Tech Group 4 × Urban share 0.968 0.942 0.971

(1.83) (1.80) (1.86)Observations 4951 4951 4951

Notes: t statistics in parentheses, ∗ p < 0.05, ∗∗ p < 0.01, ∗∗∗ p < 0.001. Columns:(1) Poisson with base (additive) distance specification (2) Poisson using onlyVincenty inter-state distances (3) Poisson with alternate, multiplicative distancecalculation. Column (1) likely underestimates the impact of low-infrastructurestates, whereas column (2) overestimates.

25

the second adjusted by the ratio between wagon freight rates and railroad freightrates:

di j = vincentyi j +wagon j ∗ (wagon f reightt/rr f reightt)

This measure of distance is asymmetrical, an unusual choice for distance calcu-lations. The decision to use this measure was made based on the fact that therelevant distances are between farm and factory; factories are assumed to be es-tablished considering access to railroads. As the data are at state level, I cannotknow the distribution of activity within the state, but because whatever railroad ac-cess a state has is likely to be located near areas of major economic activity, thismeasure almost certainly overestimates the wagon travel distance for states withpoorer railroad networks. For comparison purposes I also perform the analysis onmarket potentials calculated on the first (Vincenty) part alone. Since this measureunderestimates the penalty associated with poor railroad networks (by ignoring it),it should serve as an opposite bound for the results of the analysis. As shown inthe first two columns of the table below, the changes in estimates are not partic-ularly dramatic. The third column contains another alternate specification foundby including the wagon distance adjustment multiplicatively (as if the two legsof the journey were separate transactions). This would overstate the adjustmentagainst poor-infrastructure statements by still further and is thus not preferred, it isincluded for completeness.

8.2 Crop Prices

In earlier years in the sample, the Census reports quantities of crops grown and notvalues. In order to combine crop outputs for use with implements that can servemultiple categories, it is necessary to transform these quantities into values. Pricedata is obtained from several sources, notably Investigation Relative to Wages andPrices of Commodities, vol. 1, 1911 and the Historical Statistics of the UnitedStates (Carter et al 2006). Different sources may have different methods of ob-taining the prices (e.g. time averaging of prices due to seasonality, different cityof observation) which can introduce inaccuracy. However, this is mitigated bytwo features of the analysis. Since market potentials are normalized, if two cropsdo not share any implements in common, then they can be from different sourceswithout issue, as crop prices are only relevant for estimating the relative impactof their growing distribution on the same implement; and the crops that have theleast reliable price data are also the crops with the smallest values, so that even alarge discrepancy in the price involved will not induce a big change in the marketpotential calculation.

26