SECURED TRANSACTION ESSENTIALS FOR BUSINESS LAWYERS

157

SECURED TRANSACTION ESSENTIALS FOR BUSINESS LAWYERS BUSINESS LAW Tuesday, April 27, 2021 ISBN: 978-1-77060-827-6 Sponsored by:

Transcript of SECURED TRANSACTION ESSENTIALS FOR BUSINESS LAWYERS

SECURED TRANSACTION ESSENTIALS FOR BUSINESS LAWYERS BUSINESS LAW Tuesday, April 27, 2021 ISBN: 978-1-77060-827-6 Sponsored by:

DISCLAIMER This work appears as part of the Ontario Bar Association’s initiatives in continuing legal education. It aims to provide information and opinion which will assist lawyers in maintaining and enhancing their competence. It does not, however, represent or embody any official position of, or statement by, the OBA except where this may be specifically indicated; nor does it attempt to set forth definitive practice standards or to provide legal advice. Precedents and other material contained herein are intended to be used thoughtfully, as nothing in the work relieves readers of their responsibility to consider it in the light of their own professional skill and judgment.

NOTE RE PRECEDENTS

The model precedents are provided for your consideration and use when you draft your own documents. They are NOT meant to be used "as is". Their suitability will depend upon a number of factors, such as the current state of the law and practice in each area of law, your writing style, your needs and the needs and preferences of you and your clients. These documents may need to be modified to correspond to current law and practice.

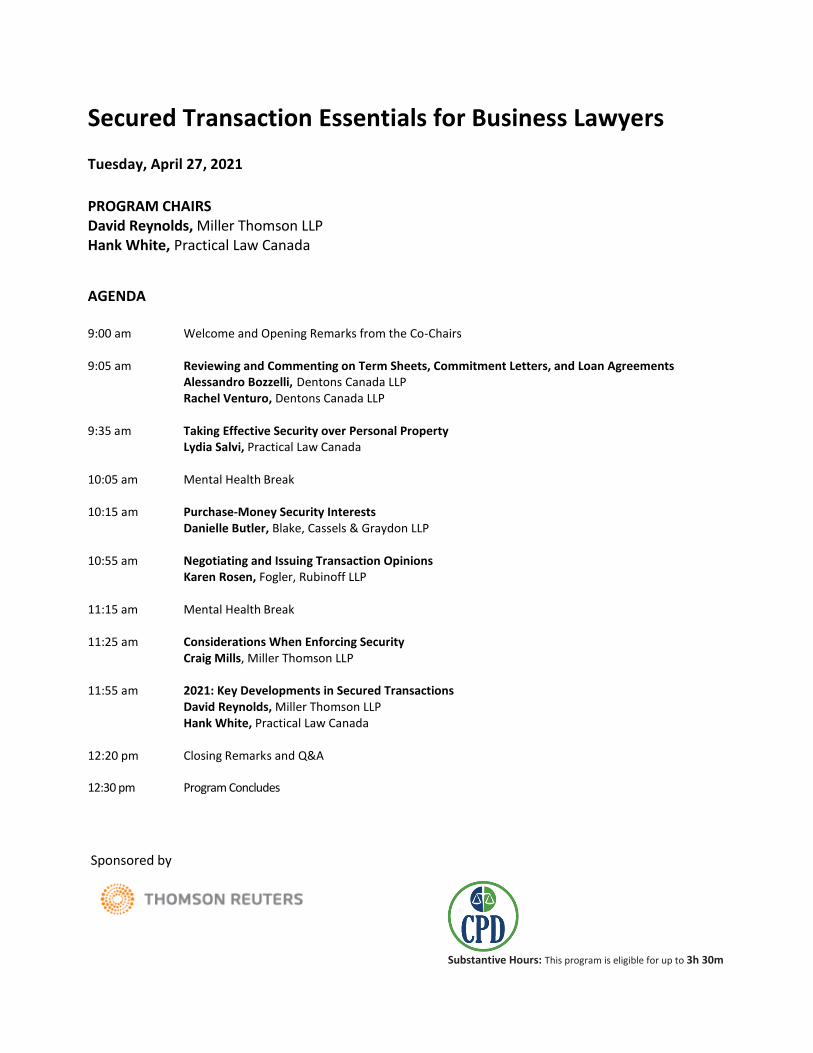

Secured Transaction Essentials for Business Lawyers Tuesday, April 27, 2021

PROGRAM CHAIRS David Reynolds, Miller Thomson LLP Hank White, Practical Law Canada

AGENDA

9:00 am Welcome and Opening Remarks from the Co-Chairs 9:05 am Reviewing and Commenting on Term Sheets, Commitment Letters, and Loan Agreements

Alessandro Bozzelli, Dentons Canada LLP Rachel Venturo, Dentons Canada LLP

9:35 am Taking Effective Security over Personal Property Lydia Salvi, Practical Law Canada 10:05 am Mental Health Break 10:15 am Purchase-Money Security Interests Danielle Butler, Blake, Cassels & Graydon LLP

10:55 am Negotiating and Issuing Transaction Opinions

Karen Rosen, Fogler, Rubinoff LLP 11:15 am Mental Health Break 11:25 am Considerations When Enforcing Security

Craig Mills, Miller Thomson LLP 11:55 am 2021: Key Developments in Secured Transactions

David Reynolds, Miller Thomson LLP Hank White, Practical Law Canada

12:20 pm Closing Remarks and Q&A

12:30 pm Program Concludes

Substantive Hours: This program is eligible for up to 3h 30m

Sponsored by

PROGRAM PARTICIPANTS

DAVID REYNOLDS (PROGRAM CHAIR)

David Reynolds practices commercial lending and private business transactions. David advises banks, other institutional lenders and corporate borrowers in connection with secured and unsecured lending transactions. His expertise also includes syndicated transactions, single-lender transactions, financing of day-to-day operations, acquisition financing, asset-based lending, wholesale automotive financing, domestic and cross-border transactions. In addition to his experience in commercial lending, David also advises and acts for clients in a diverse range of corporate transactions such as asset and share purchases. David graduated from the University of Western Ontario (UWO) in 2010 with a Juris Doctorate. During his time at UWO, he worked as Program Manager of the Sport Solution Legal Clinic where he advised Canadian National Team and Olympic athletes on various legal issues.

HANK WHITE (PROGRAM CHAIR)

Hank White has been a Senior Lawyer Editor for Practical Law Canada's Finance service since 2015. Prior to joining

Practical Law, Hank was Legal Counsel at The Bank of Nova Scotia for eight years. Hank commenced his career in

private practice with Miller Thomson LLP in Toronto, practicing in the Financial Services group for six years. He has

advised financial institutions and borrowers on domestic and international transactions that include syndicated

loans, hospitality finance, asset-based loans, dealer and equipment finance as well as conventional lending. Hank is

the immediate Past-Chair of the Business Law Section of the Ontario Bar Association, a member of the OBA’s

Personal Property Security Legislation Committee and participates in the Toronto Opinions Group.

ALESSANDRO BOZZELLI

Alessandro specializes in the areas of banking and finance, where he regularly provides counsel to international and domestic lenders and borrowers in all areas of debt financing transactions, including syndicated financings, acquisition financings, real estate financings, asset-based lending, project finance and subordinated/mezzanine financings. Prior to attaining his law degree and his MBA, Alessandro was employed with Enbridge Gas Distribution Inc. holding various positions. Throughout his post-secondary education, Alessandro has studied in various countries throughout the world, including Italy.

DANIELLE BUTLER Blake, Cassels & Graydon LLP. Danielle has a broad-based financial services practice that focuses on domestic and cross-border debt financing transactions, structured finance transactions and acquisition financings. She has experience representing lenders and borrowers in both secured and unsecured financing transactions (bilateral and syndicated loan structures). Danielle advises sellers and purchasers on public and private securitization transactions involving various asset classes, including auto loans and leases, residential and commercial mortgage loans, credit cards and trade receivables. She first joined Blakes as a summer law student in 2014 and completed her articles with the Firm in 2015/2016. During her articles, Danielle was seconded to the legal department of one of Canada's leading banks.

CRAIG A. MILLS Craig Mills is a Partner in Miller Thomson LLP’s Restructuring & Insolvency Group. The focus of his practice

is commercial litigation with a focus on commercial disputes, creditors’ remedies, restructuring law and

franchise law. Craig’s litigation background has proven to be a valuable tool in strategically advising clients

on commercial debt enforcement/recovery, restructuring and insolvency matters, commercial litigation,

and claims resolution management. Craig’s clients include lenders, creditors, owner-operators,

borrowers, mortgagees, franchisors, landlords and trustees/receivers/monitors. He has appeared as

counsel before the Ontario Superior Court of Justice, Commercial List, Divisional Court and Court of

Appeal. Craig is a regular author and lecturer on creditors’ remedies and insolvency issues.

KAREN ROSEN

Karen Rosen is the Chair of the Corporate Department and Lead of the Financial Services & Insolvency Group at Fogler, Rubinoff LLP. A significant portion of her practice is devoted to corporate and commercial lending. She works in close partnership with her clients advising on all aspects of commercial/corporate finance, including syndicated lending, subordinate/mezzanine financing, asset-based lending and aircraft financing. Karen is highly regarded for her business minded approach and has significant expertise in advising clients on mergers, acquisitions and divestitures, private equity investments, corporate structuring and restructuring, commercial agreements, corporate reorganizations, shareholder matters and aircraft acquisitions and sales. Public and private companies and financial institutions call upon Karen for her ability to structure innovative financing solutions, both Canadian and cross-border. She regularly acts for lenders and borrowers and provides advice across industries, including, solar energy, food & beverage processing, aviation, e-commerce, natural health products, garment manufacturing and distribution and telecommunications.

LYDIA SALVI

Lydia Salvi is the Past Chair of the Business Law Section for the Ontario Bar Association. She is currently an officer for the Business Law Section of the Canadian Bar Association. She is the team lead for Practical Law Canada Finance at Thomson Reuters. Prior to Thomson Reuters, Lydia was a partner in the Financial Services Groups of Baker & McKenzie LLP and Cassels Brock & Blackwell LLP where she obtained high profile private M&A, corporate and commercial lending and corporate restructuring experience in Canada, the United States and internationally. Lydia represents financial institutions, funds, aviation financiers and corporations on all aspects of traditional and non‐traditional types of financings including acquisition financings, asset based financings, syndicated financings, private equity, equipment leasing and distressed investing and workouts.

RACHEL VENTURO

Rachel Venturo is an associate in the Banking and Finance group, where she represents both borrowers and lenders in various domestic and cross-border banking matters and commercial transactions. Her experience includes matters related to insolvency, restructuring and other associated commercial litigation. Rachel also represents lenders, lessors and operators in aircraft financing and leasing transactions.

Secured Transaction Essentials for Business Lawyers

TABLE OF CONTENTS

TAB 1 Reviewing and Commenting on Term Sheets, Commitment Letters, and Loan Agreements

Alessandro Bozzelli, Dentons Canada LLP Rachel Venturo, Dentons Canada LLP

TAB 2 Taking Effective Security over Personal Property

Lydia Salvi, Practical Law Canada Finance

TAB 3 Purchase-Money Security Interests

Danielle Butler, Blake, Cassels & Graydon LLP

TAB 4 Opinions on Secured Lending Transactions

Karen Rosen, Fogler, Rubinoff LLP

TAB 5 Considerations When Enforcing Security

Craig Mills, Miller Thomson LLP

TAB 6

2021: Key Developments in Secured Transactions David Reynolds, Miller Thomson LLP Hank White, Practical Law Canada

SECURED TRANSACTION ESSENTIALS FOR BUSINESS LAWYERS BUSINESS LAW Term Sheets and Commitment Letters in Financing Transactions Alessandro Bozzelli, Dentons Canada LLP Rachel Venturo, Dentons Canada LLP

Term Sheets and Commitment

Letters in Financing

Transactions

1

Alessandro Bozzelli and Rachel Venturo

April 27, 2021

Overview

27 April 2021 2

• What’s the Difference?

• Basics of Term Sheets

• Basics of Commitment Letters

• Essential Provisions within each

• Concluding Remarks

3

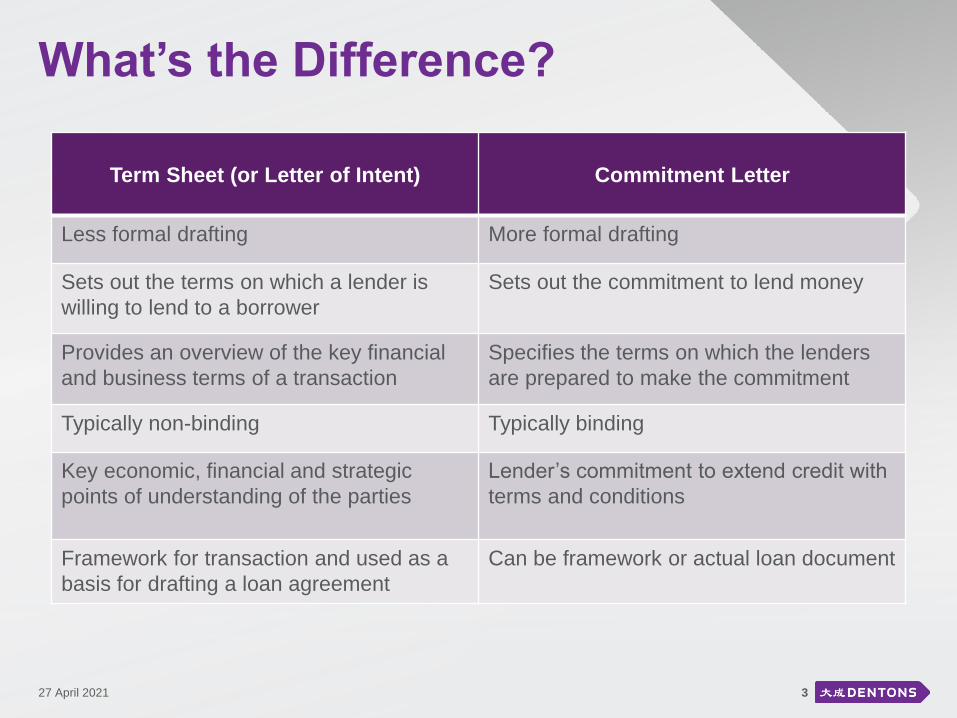

What’s the Difference?

27 April 2021

Term Sheet (or Letter of Intent) Commitment Letter

Less formal drafting More formal drafting

Sets out the terms on which a lender is

willing to lend to a borrower

Sets out the commitment to lend money

Provides an overview of the key financial

and business terms of a transaction

Specifies the terms on which the lenders

are prepared to make the commitment

Typically non-binding Typically binding

Key economic, financial and strategic

points of understanding of the parties

Lender’s commitment to extend credit with

terms and conditions

Framework for transaction and used as a

basis for drafting a loan agreement

Can be framework or actual loan document

4

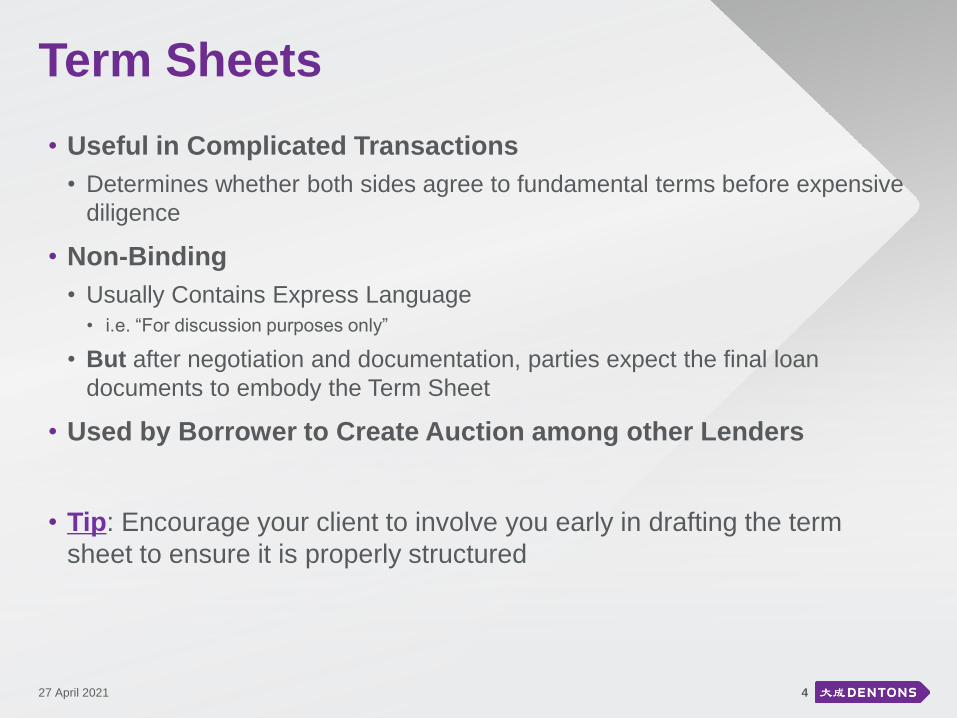

Term Sheets

• Useful in Complicated Transactions

• Determines whether both sides agree to fundamental terms before expensive

diligence

• Non-Binding

• Usually Contains Express Language

• i.e. “For discussion purposes only”

• But after negotiation and documentation, parties expect the final loan

documents to embody the Term Sheet

• Used by Borrower to Create Auction among other Lenders

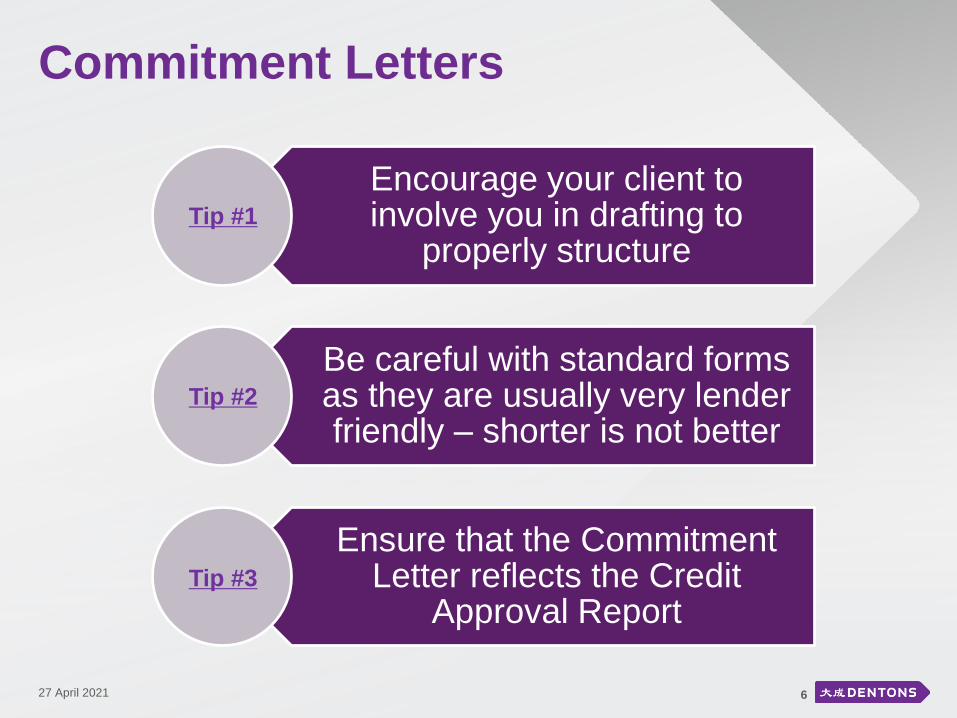

• Tip: Encourage your client to involve you early in drafting the term

sheet to ensure it is properly structured

27 April 2021

Commitment Letters

5

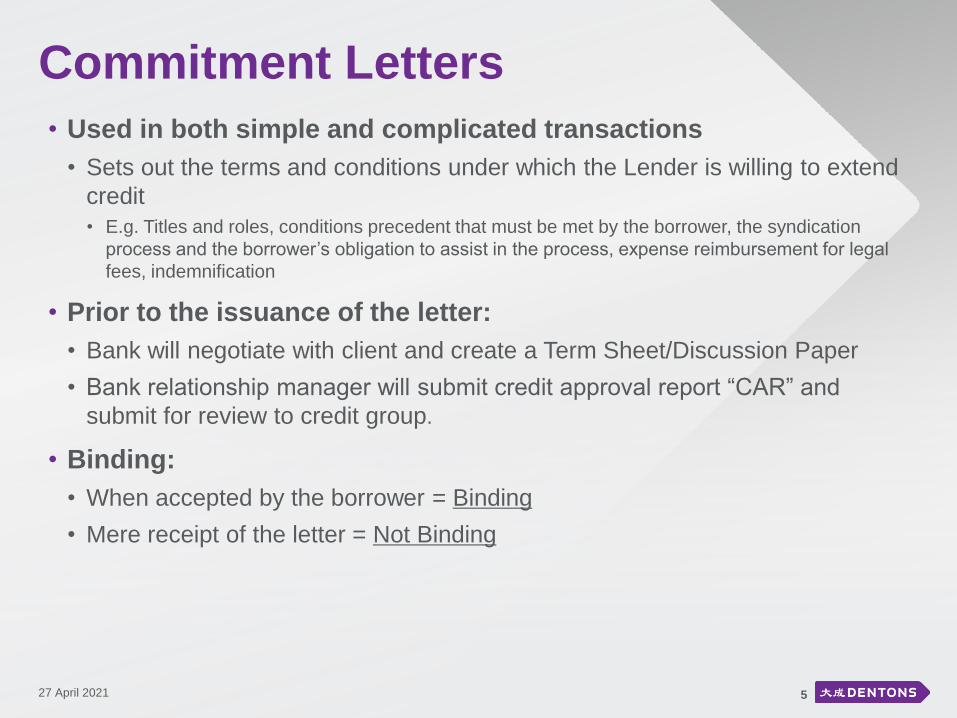

• Used in both simple and complicated transactions

• Sets out the terms and conditions under which the Lender is willing to extend

credit

• E.g. Titles and roles, conditions precedent that must be met by the borrower, the syndication

process and the borrower’s obligation to assist in the process, expense reimbursement for legal

fees, indemnification

• Prior to the issuance of the letter:

• Bank will negotiate with client and create a Term Sheet/Discussion Paper

• Bank relationship manager will submit credit approval report “CAR” and

submit for review to credit group.

• Binding:

• When accepted by the borrower = Binding

• Mere receipt of the letter = Not Binding

27 April 2021

Commitment Letters

627 April 2021

Encourage your client to involve you in drafting to

properly structure

Be careful with standard forms as they are usually very lender friendly – shorter is not better

Ensure that the Commitment Letter reflects the Credit

Approval Report

Tip #1

Tip #2

Tip #3

7

When may a Commitment Letter be a Credit Agreement?

27 April 2021

Suitable as the Credit

Agreement

Smaller Credit Facility

Structure of transaction is simple

Parties want to minimize legal fees

*Must contain all necessary elements of a binding

contract

Suitable as the Roadmap:

Larger Credit Facility

More complex transaction

*Transaction will be conditional on the

negotiation of the Credit Agreement

Essential Provisions

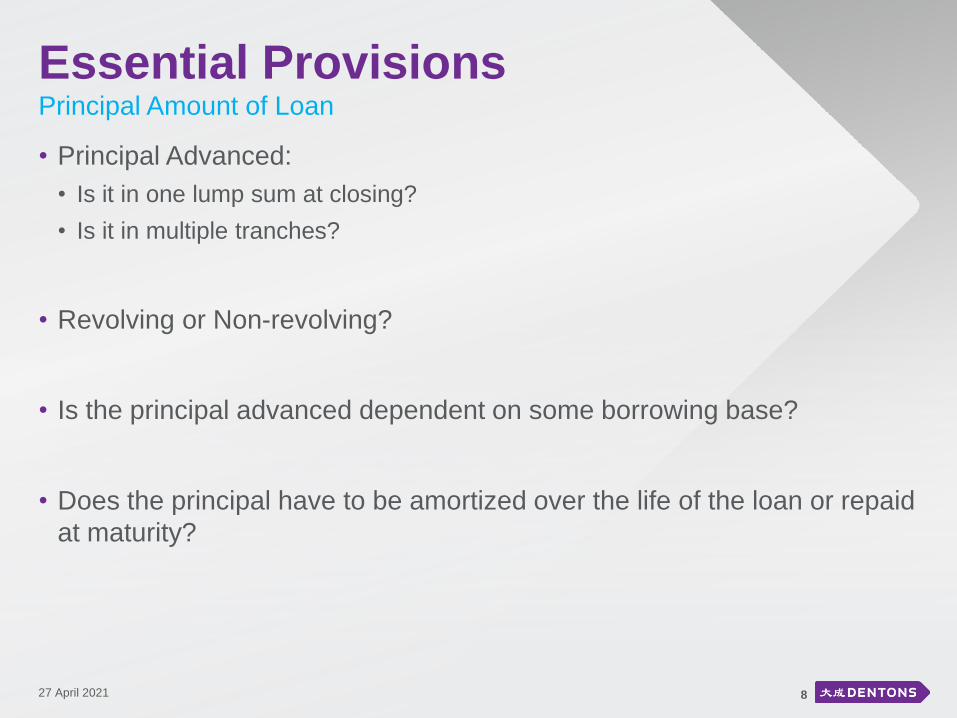

• Principal Advanced:

• Is it in one lump sum at closing?

• Is it in multiple tranches?

• Revolving or Non-revolving?

• Is the principal advanced dependent on some borrowing base?

• Does the principal have to be amortized over the life of the loan or repaid

at maturity?

8

Principal Amount of Loan

27 April 2021

Essential Provisions

9

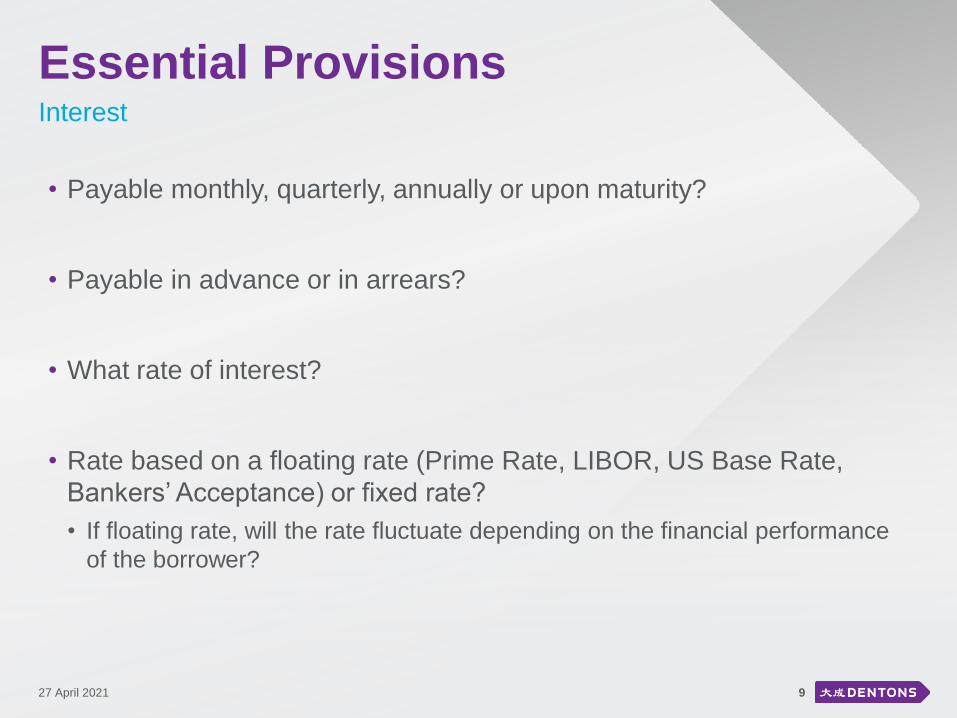

Interest

• Payable monthly, quarterly, annually or upon maturity?

• Payable in advance or in arrears?

• What rate of interest?

• Rate based on a floating rate (Prime Rate, LIBOR, US Base Rate,

Bankers’ Acceptance) or fixed rate?

• If floating rate, will the rate fluctuate depending on the financial performance

of the borrower?

27 April 2021

Essential Provisions

10

Use of Funds

• Can the funds advanced be used at the discretion of the borrower?

- or -

• Must the funds be used for a particular purpose?

27 April 2021

Essential Provisions

11

Representations and Warranties

• Should be tailored for the particular deal, borrower and guarantors

• Why are representations and warranties given?

• Tool for allocating risk between the borrower and the lenders

• Used to provide information to a lender in connection with its due diligence

review and credit assessment

• Term Sheets and Commitment Letters usually include:

• Borrower’s Counsel:

• need to insert thresholds and knowledge qualifiers for borrower’s representations and

warranties (e.g. “material”, “reasonable”, “Material Adverse Effect”, “to the best of its

knowledge”)

• Lender’s Counsel:

• ensure borrower’s representations and warranties are clean and void of any of the

foregoing qualifiers

27 April 2021

Essential Provisions

12

Payment Provisions

• Can all or any portion of the loan be repaid prior to maturity?

• If early prepayment is provided for:

• Will there be an early repayment fee payable by the borrower to the lender?

• If the borrower disposes of certain assets which are collateral under the

loan agreement:

• Do the proceeds of such disposition need to be repaid against the loan?

• What happens to the payment of insurance proceeds?

27 April 2021

• Borrower’s Counsel: will try to

minimize what constitutes an Event

of Default and increase threshold

that must be reached before an

event is deemed and Event of

Default

• Lender’s Counsel: will try to

broaden what constitutes an Event

of Default, limit cure rights, and

minimize any metric that dictates

whether an Event of Default has

occurred.

13

Events of Default

Essential Provisions

• Loan Payable:

On demand?

Only upon occurrence of an Event

of Default?

• Non-demand Loan:

What events permit the lender to

enforce and cause repayment of

the loan?

Will the borrower have the option

to “cure” an Event of Default?

27 April 2021

Essential Provisions

• Secured or unsecured loan?

• If secured:

• Security from borrower only or also a third party in the form of a guarantee?

• Security over real property and/or personal property?

• Where will security need to be obtained?

• Will the security of the lender be first-ranking?

• Do you need to obtain:

• third party estoppels

• subordinations

• postponements

• Is the lender required to share security over the borrowers assets?

• If yes: is an intercreditor agreement required to govern the relationship between multiple secured

parties?

14

Security Documentation

27 April 2021

Essential Provisions

15

Conditions Precedent

• What closing deliverables must be satisfied prior to closing?

• In most cases:

• For the sole benefit of the lender and may be waived in the lender’s sole

discretion

• Borrower’s Counsel: have the lender provide a detailed list up front

• This should prevent the lender from adding further requirements later when

the borrower has less leverage

27 April 2021

Essential Provisions

• These should guide the borrower’s behavior and line up with the credit approvals

• Need to be tailored for the particular deal

• Positive

• Actions which the borrower has a positive obligation to complete

• Negative

• Actions that a borrower is expressly forbidden from taking

• Lender’s Counsel: be wary of providing cure periods for breach

• Financial

• Minimum financial performance

• Usually measured by certain financial ratios that a borrower or other credit

party will need to maintain during the term of the credit facility

16

Covenants

27 April 2021

Essential Provisions

17

Governing Law

• What law will govern the loan documentation?

• Lender’s Counsel:

• Should insist on the jurisdiction that has the greatest connection to the

transaction

• But also: consider where it would want to go litigate where the loan to go into

default

27 April 2021

Essential Provisions

18

Fees

• Who will pay the lender’s fees and disbursements?

• Are these fees capped?

• What fees must the borrower pay the lender?

• Term sheet may be non-binding but it should contain a binding provision

requiring the borrower to reimburse the lender for certain transactional

expenses if the financing does not close

• This protects the lender from making unnecessary expenditures in reliance

on a non-binding document

• The commitment letter and term sheet may be accompanied by a fee

letter

27 April 2021

Closing Remarks

19

• Essential to explicitly state:

• Binding or non-binding

• The role of the document in the transaction

• Counsel should get involved early to ensure:

• An agreement can be reached

• The document contains sufficient details

• The provisions are in the best interests of their client

27 April 2021

20

Rachel specializes in the areas of banking and finance, where she

represents both borrowers and lenders in various domestic and

cross-border banking matters and commercial transactions.

Her experience includes matters related to insolvency, restructuring

and other associated commercial litigation. Rachel also represents

lenders, lessors and operators in aircraft financing and leasing

transactions.

About us

Rachel Venturo

Associate

Financial Services

D +1 416 863 4716

Alessando Bozzelli

Senior Associate

Financial Services

D +1 416 863 4352

Alessandro specializes in the areas of banking and finance, where

he regularly provides counsel to international and domestic lenders

and borrowers in all areas of debt financing transactions, including

syndicated financings, acquisition financings, real estate financings,

asset-based lending, project finance and subordinated/mezzanine

financings.

Prior to attaining his law degree and his MBA, Alessandro was

employed with Enbridge Gas Distribution Inc. holding various

positions. Throughout his post-secondary education, Alessandro

has studied in various countries throughout the world, including

Italy.

27 April 2021

Questions?

2127 April 2021

Thank you

Dentons Canada LLP

77 King Street West

Suite 400

Toronto, Ontario M5K 0A1

Canada

22

Dentons is the world's largest law firm, delivering quality and value to clients around the globe. Dentons is

a leader on the Acritas Global Elite Brand Index, a BTI Client Service 30 Award winner and recognized by

prominent business and legal publications for its innovations in client service, including founding Nextlaw

Labs and the Nextlaw Global Referral Network. Dentons' polycentric approach and world-class talent

challenge the status quo to advance client interests in the communities in which we live and work.

www.dentons.com

© 2017 Dentons. Dentons is a global legal practice providing client services worldwide through its member firms and affiliates. This document is not designed to provide legal or other advice and you should not take, or refrain from taking, action based on its content. We are providing information to you on the basis you agree to keep it confidential. If you give us confidential information but do not instruct or retain us, we may act for another client on any matter to which that confidential information may be relevant. Please see dentons.com for Legal Notices.

SECURED TRANSACTION ESSENTIALS FOR BUSINESS LAWYERS BUSINESS LAW Taking Effective Security over Personal Property Lydia Salvi, Practical Law Canada Finance

Taking Effective Security Over Personal Property

LYDIA SALVIPractical Law Canada Finance

Agenda

• Due Diligence: Objectives and Considerations

• Legislation: The PPSA and the STA

• Perfecting Security Interests

• Third Party Agreements

• Other Considerations:

– Bank Act Security

– Conflict of Laws: Where do I register?

• Wrap up and Questions

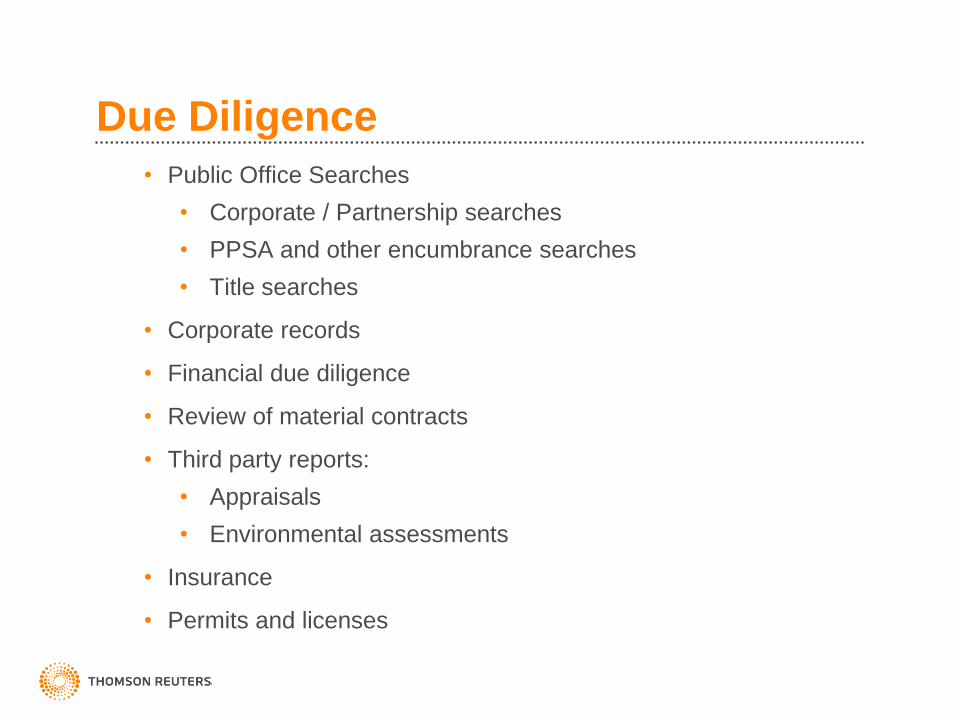

Due Diligence

• Public Office Searches

• Corporate / Partnership searches

• PPSA and other encumbrance searches

• Title searches

• Corporate records

• Financial due diligence

• Review of material contracts

• Third party reports:

• Appraisals

• Environmental assessments

• Insurance

• Permits and licenses

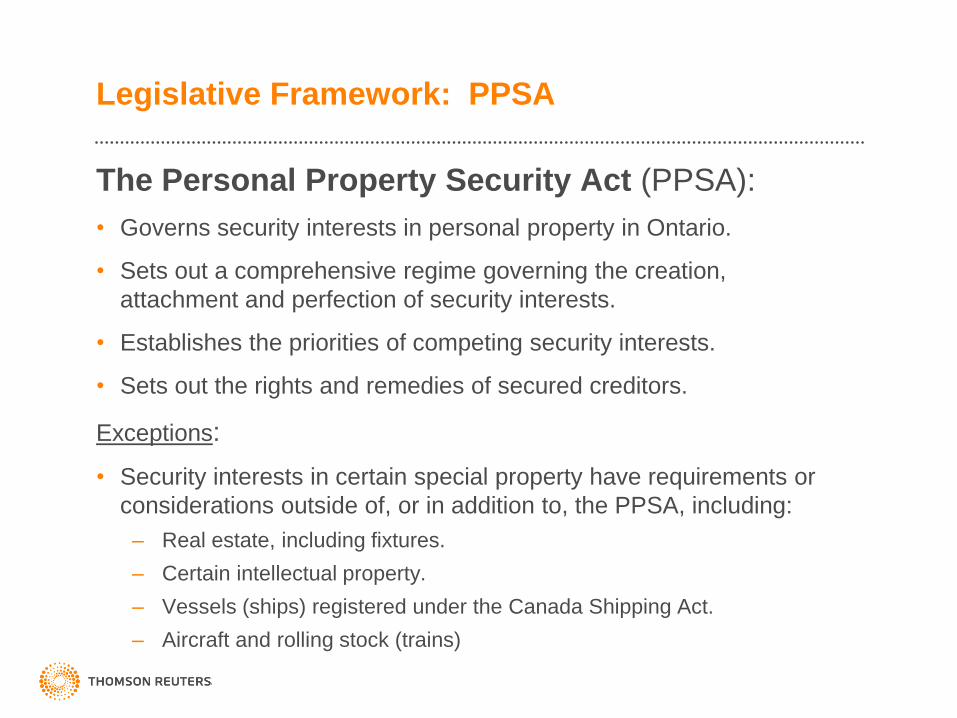

Legislative Framework: PPSA

The Personal Property Security Act (PPSA):

• Governs security interests in personal property in Ontario.

• Sets out a comprehensive regime governing the creation,

attachment and perfection of security interests.

• Establishes the priorities of competing security interests.

• Sets out the rights and remedies of secured creditors.

Exceptions:

• Security interests in certain special property have requirements or

considerations outside of, or in addition to, the PPSA, including:

– Real estate, including fixtures.

– Certain intellectual property.

– Vessels (ships) registered under the Canada Shipping Act.

– Aircraft and rolling stock (trains)

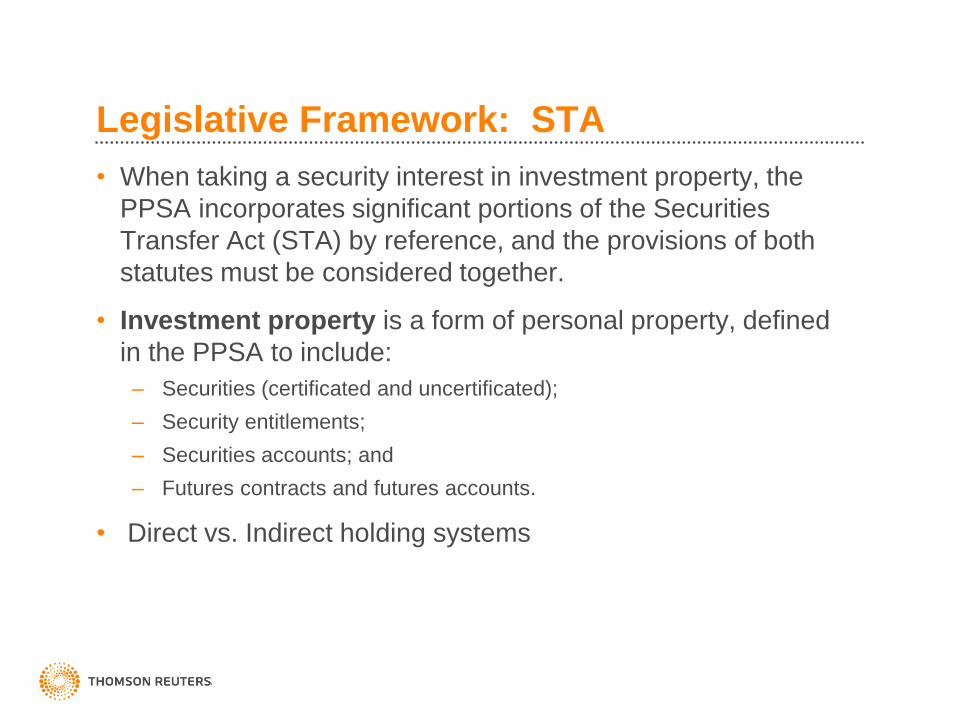

Legislative Framework: STA

• When taking a security interest in investment property, the

PPSA incorporates significant portions of the Securities

Transfer Act (STA) by reference, and the provisions of both

statutes must be considered together.

• Investment property is a form of personal property, defined

in the PPSA to include:

– Securities (certificated and uncertificated);

– Security entitlements;

– Securities accounts; and

– Futures contracts and futures accounts.

• Direct vs. Indirect holding systems

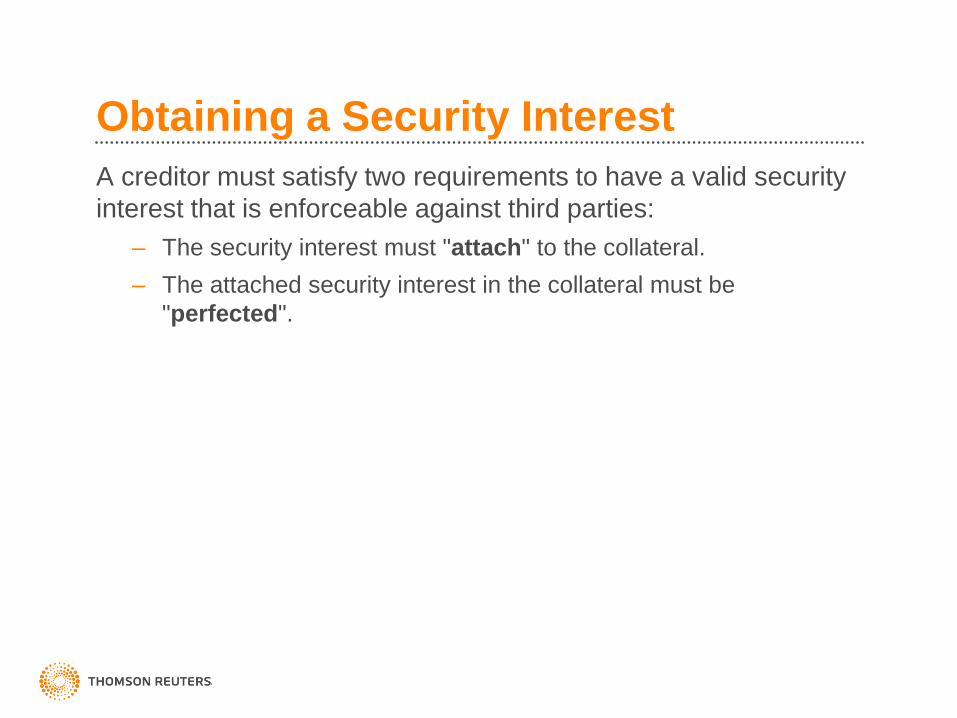

Obtaining a Security Interest

A creditor must satisfy two requirements to have a valid security

interest that is enforceable against third parties:

– The security interest must "attach" to the collateral.

– The attached security interest in the collateral must be

"perfected".

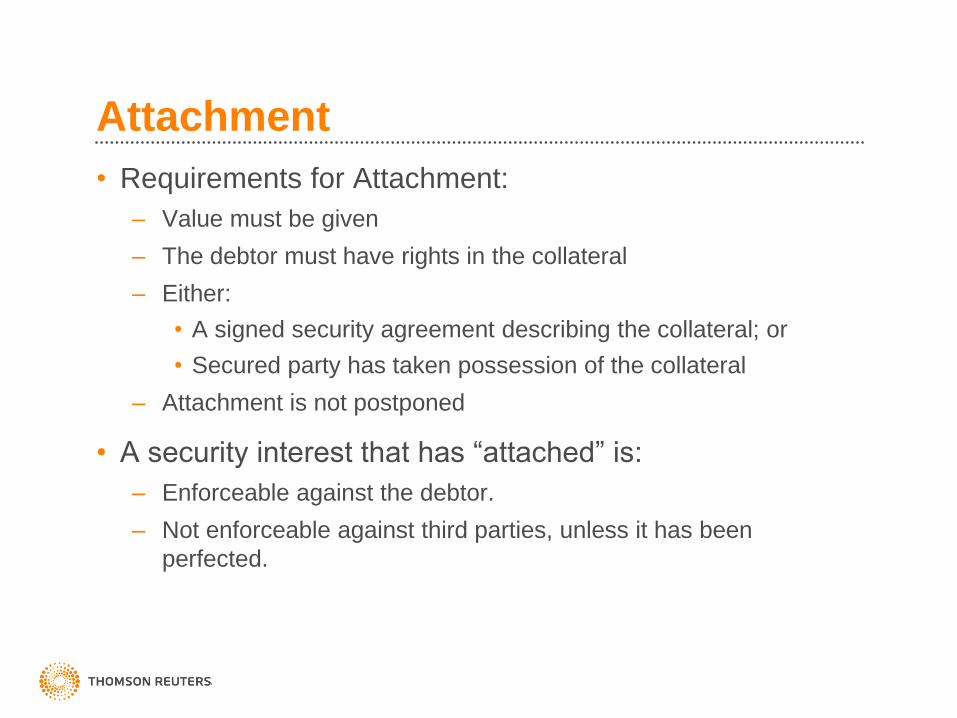

Attachment

• Requirements for Attachment:

– Value must be given

– The debtor must have rights in the collateral

– Either:

• A signed security agreement describing the collateral; or

• Secured party has taken possession of the collateral

– Attachment is not postponed

• A security interest that has “attached” is:

– Enforceable against the debtor.

– Not enforceable against third parties, unless it has been

perfected.

Perfecting a Security Interest

Perfection

Once a security interest is "attached", and can be enforced by

the secured party against the debtor, the secured party then

"perfects" the security interest to make its security interest

effective against third parties.

Four methods to perfect an attached security interest are:

• Registration.

• Possession.

• Control.

• Automatic perfection.

Perfecting a Security Interest (Registration)

Perfection by Registration

• Registering a financing statement under the PPSA will perfect a

security interest in any type of personal property collateral.

• A financing statement can be registered before or after the security

agreement is signed by the debtor, unless the collateral constitutes

consumer goods.

• One financing statement can perfect one or more security interests

provided for in one or more security agreements, even if they are not

part of the same transaction (known as “sheltering”).

• Generally, lenders will register their financing statement well in

advance of the closing of a transaction to:

– establish their priority under the first-to-register rule; and

– identify any earlier registrations that must be dealt with.

Perfecting a Security Interest (Control)

• Only security interests in the following types of collateral may be

perfected by control:

– Investment Property

– Electronic Chattel Paper (ECP)

• Control is the best method of perfection for security interests in

investment property and ECP – ranks ahead of interests perfected

by registration.

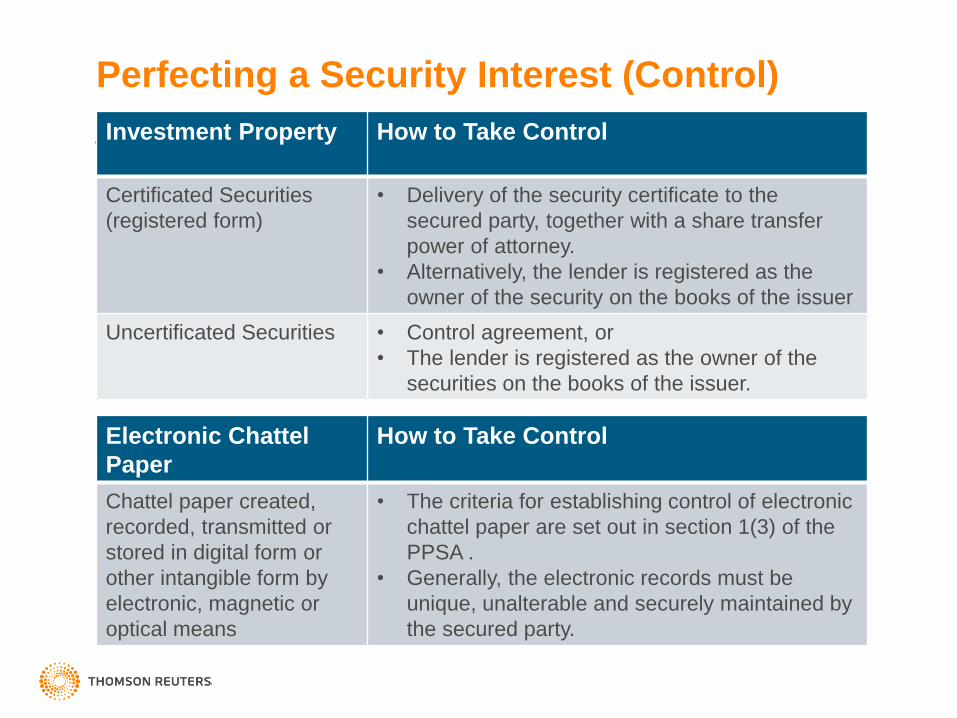

Perfecting a Security Interest (Control)

Investment Property How to Take Control

Certificated Securities

(registered form)

• Delivery of the security certificate to the

secured party, together with a share transfer

power of attorney.

• Alternatively, the lender is registered as the

owner of the security on the books of the issuer

Uncertificated Securities • Control agreement, or

• The lender is registered as the owner of the

securities on the books of the issuer.

Electronic Chattel

Paper

How to Take Control

Chattel paper created,

recorded, transmitted or

stored in digital form or

other intangible form by

electronic, magnetic or

optical means

• The criteria for establishing control of electronic

chattel paper are set out in section 1(3) of the

PPSA .

• Generally, the electronic records must be

unique, unalterable and securely maintained by

the secured party.

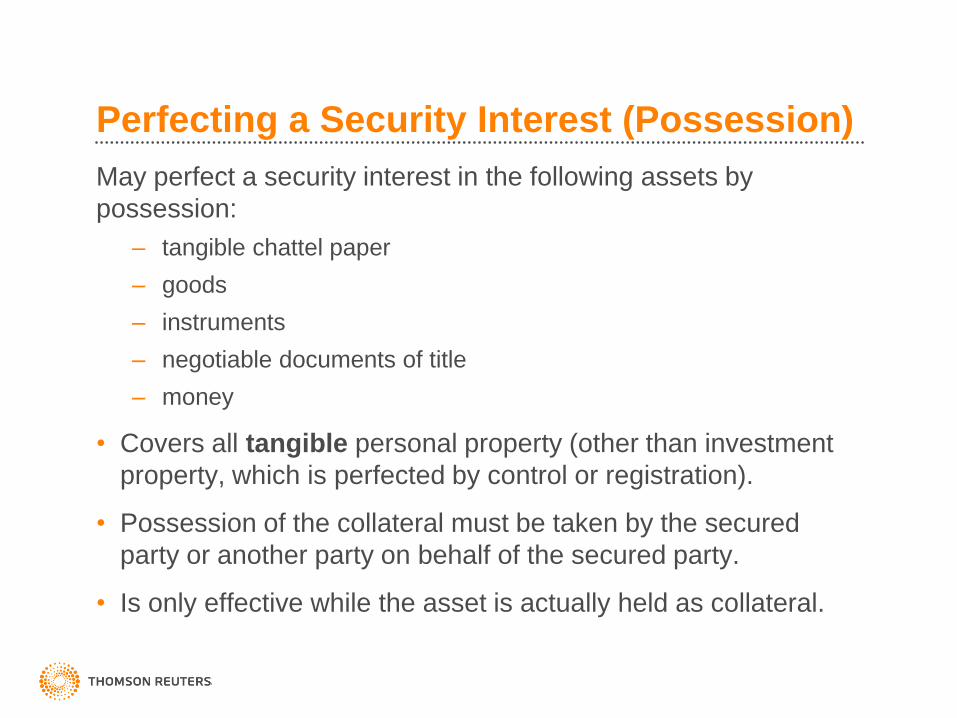

Perfecting a Security Interest (Possession)

May perfect a security interest in the following assets by

possession:

– tangible chattel paper

– goods

– instruments

– negotiable documents of title

– money

• Covers all tangible personal property (other than investment

property, which is perfected by control or registration).

• Possession of the collateral must be taken by the secured

party or another party on behalf of the secured party.

• Is only effective while the asset is actually held as collateral.

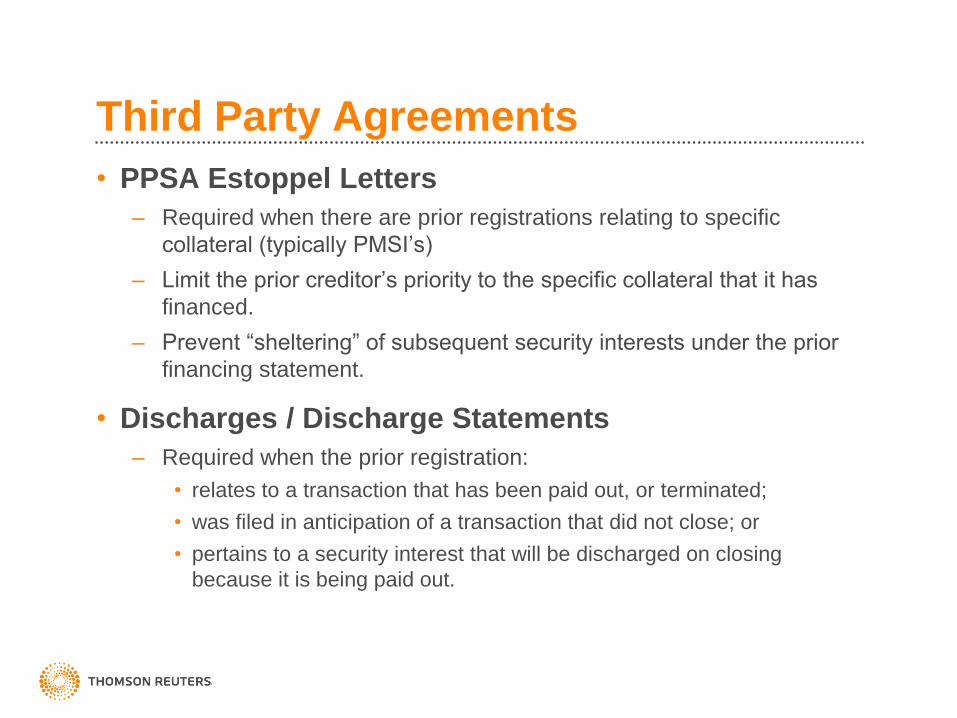

Third Party Agreements

• PPSA Estoppel Letters

– Required when there are prior registrations relating to specific

collateral (typically PMSI’s)

– Limit the prior creditor’s priority to the specific collateral that it has

financed.

– Prevent “sheltering” of subsequent security interests under the prior

financing statement.

• Discharges / Discharge Statements

– Required when the prior registration:

• relates to a transaction that has been paid out, or terminated;

• was filed in anticipation of a transaction that did not close; or

• pertains to a security interest that will be discharged on closing

because it is being paid out.

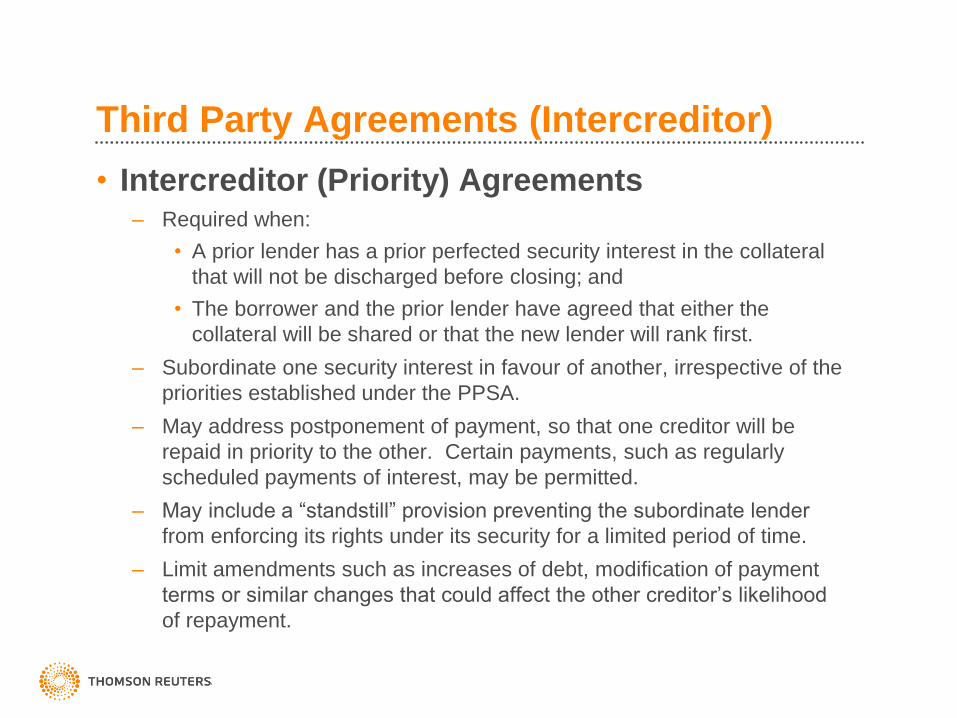

Third Party Agreements (Intercreditor)

• Intercreditor (Priority) Agreements– Required when:

• A prior lender has a prior perfected security interest in the collateral

that will not be discharged before closing; and

• The borrower and the prior lender have agreed that either the

collateral will be shared or that the new lender will rank first.

– Subordinate one security interest in favour of another, irrespective of the

priorities established under the PPSA.

– May address postponement of payment, so that one creditor will be

repaid in priority to the other. Certain payments, such as regularly

scheduled payments of interest, may be permitted.

– May include a “standstill” provision preventing the subordinate lender

from enforcing its rights under its security for a limited period of time.

– Limit amendments such as increases of debt, modification of payment

terms or similar changes that could affect the other creditor’s likelihood

of repayment.

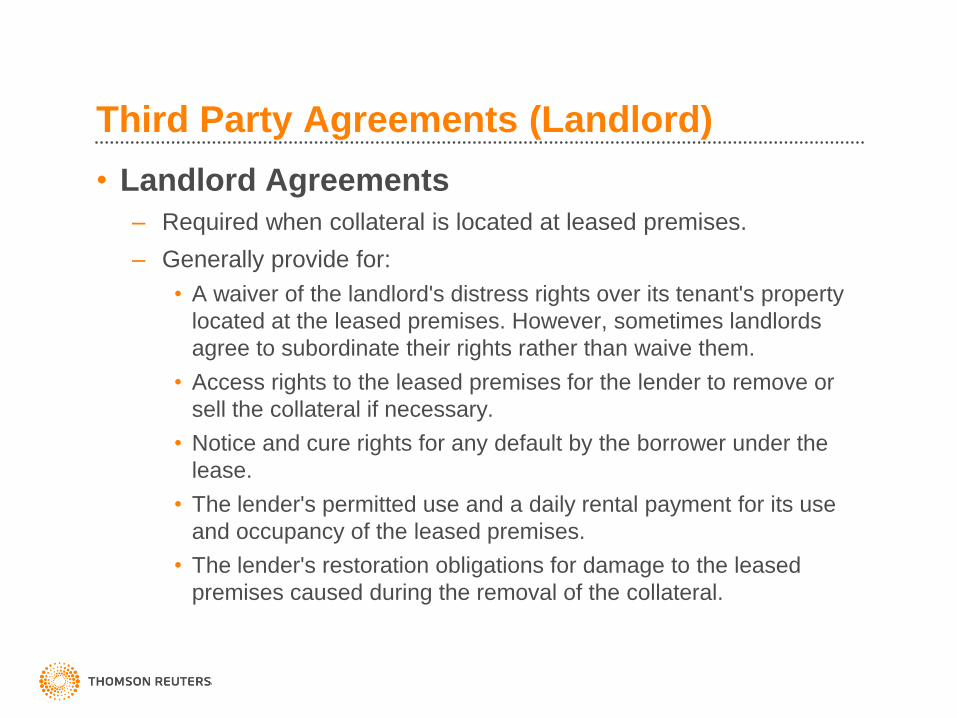

Third Party Agreements (Landlord)

• Landlord Agreements

– Required when collateral is located at leased premises.

– Generally provide for:

• A waiver of the landlord's distress rights over its tenant's property

located at the leased premises. However, sometimes landlords

agree to subordinate their rights rather than waive them.

• Access rights to the leased premises for the lender to remove or

sell the collateral if necessary.

• Notice and cure rights for any default by the borrower under the

lease.

• The lender's permitted use and a daily rental payment for its use

and occupancy of the leased premises.

• The lender's restoration obligations for damage to the leased

premises caused during the removal of the collateral.

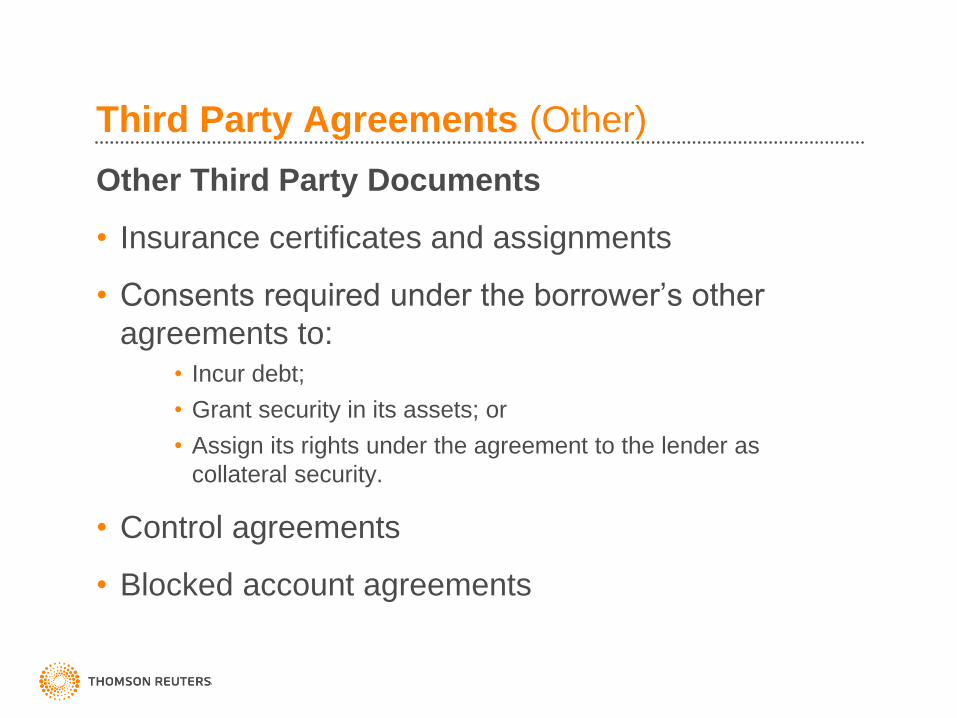

Third Party Agreements (Other)

Other Third Party Documents

• Insurance certificates and assignments

• Consents required under the borrower’s other

agreements to:

• Incur debt;

• Grant security in its assets; or

• Assign its rights under the agreement to the lender as

collateral security.

• Control agreements

• Blocked account agreements

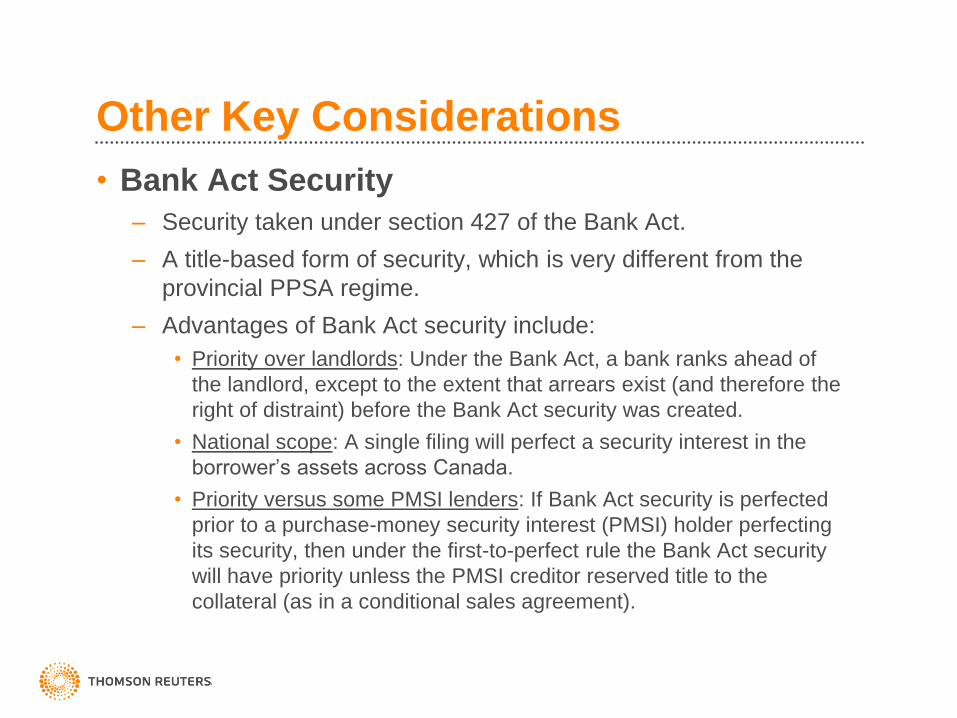

Other Key Considerations

• Bank Act Security

– Security taken under section 427 of the Bank Act.

– A title-based form of security, which is very different from the

provincial PPSA regime.

– Advantages of Bank Act security include:

• Priority over landlords: Under the Bank Act, a bank ranks ahead of

the landlord, except to the extent that arrears exist (and therefore the

right of distraint) before the Bank Act security was created.

• National scope: A single filing will perfect a security interest in the

borrower’s assets across Canada.

• Priority versus some PMSI lenders: If Bank Act security is perfected

prior to a purchase-money security interest (PMSI) holder perfecting

its security, then under the first-to-perfect rule the Bank Act security

will have priority unless the PMSI creditor reserved title to the

collateral (as in a conditional sales agreement).

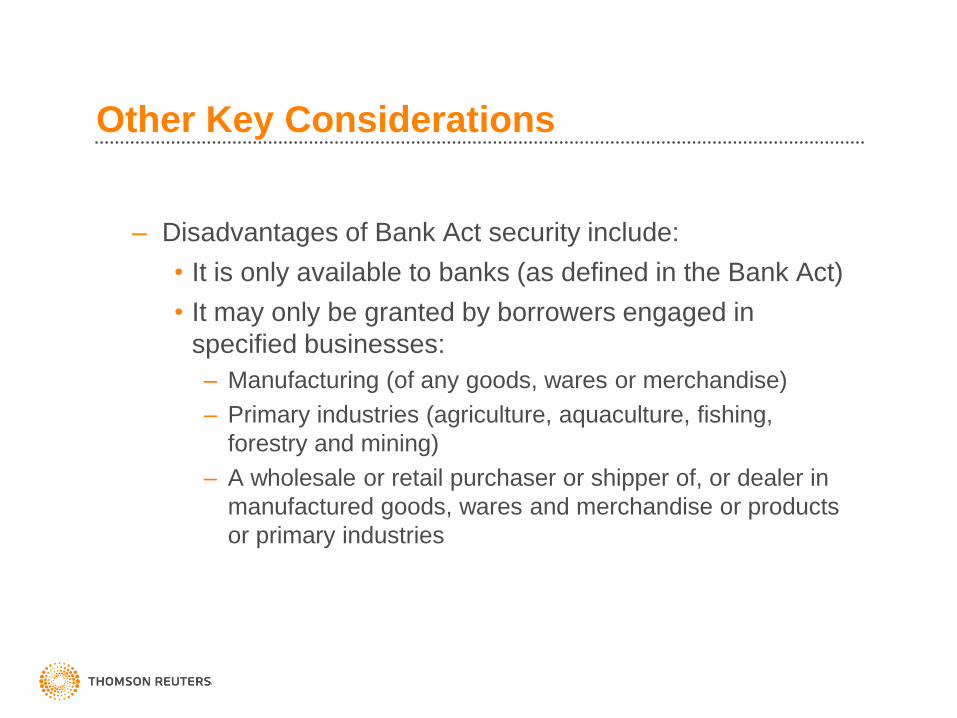

Other Key Considerations

– Disadvantages of Bank Act security include:

• It is only available to banks (as defined in the Bank Act)

• It may only be granted by borrowers engaged in

specified businesses:

– Manufacturing (of any goods, wares or merchandise)

– Primary industries (agriculture, aquaculture, fishing,

forestry and mining)

– A wholesale or retail purchaser or shipper of, or dealer in

manufactured goods, wares and merchandise or products

or primary industries

Other Key Considerations: Jurisdiction

• Jurisdiction & Conflict of Laws:

– An understanding of the conflict of laws provisions in

Ontario’s PPSA and in the equivalent legislation in other

jurisdictions is essential.

– Conflict of laws provisions determine the laws that govern

the creation, perfection and priority of security interests.

– Ontario’s rules are different from the rest of Canada.

– You may be required to register a single security

agreement in multiple jurisdictions to properly perfect the

security interests it creates.

– You may be required to search for prior creditors in

multiple jurisdictions.

Questions?

SECURED TRANSACTION ESSENTIALS FOR BUSINESS LAWYERS BUSINESS LAW Purchase-Money Security Interests Danielle Butler, Blake, Cassels & Graydon LLP

Purchase Money Security Interests

(“PMSI”)

Danielle ButlerBlake, Cassels & Graydon LLP

April 27, 2021

Agenda

• What is a PMSI?

• Eligible Transactions

• Obtaining a PMSI– Registration and Perfection

– Notice

• Priority– Priority under the PPSA

– Priority over Other Interests in Collateral

• Questions

2

What is a Purchase Money Security Interest?

• A security interest in specific goods that a creditor has either:

– provided to a debtor on credit; or

– financed the acquisition of those goods by the debtor.

• Available for all classes of personal property, except investment property.

• Once perfected, PMSI’s rank in priority to other security interests in the same goods, subject to several exceptions.

• PMSIs allow a business to acquire the goods that it needs to operate or expand its business on credit, even when it has already granted general security over its assets to another lender.

3

Example

• Day 1: Debtor grants a general security agreement in

favour of Secured Party 1. There are no prior

registrations against Debtor.

• Day 5: Secured Party 2 lends “purchase moneys” to

Debtor to acquire a widget and takes and registers a

security interest in such widget.

4

What Transactions Are Eligible for a PMSI?

• Three groups of creditors can obtain a PMSI:(a) Seller of goods who take a security interest in the goods sold

as security for all or part of the purchase price.

(b) Lenders who finance the purchase of specific goods are eligible for a PMSI in the goods whose purchase it financed.

(c) Lessors providing goods under a “lease for a term of more than one year”.

• PMSIs are not available for sale-and-lease-back transactions.

5

Obtaining a PMSI Super-Priority

• Meeting the PMSI definition is not enough to get

PMSI super-priority.

• You must satisfy the tests pursuant to Section 33 of

the PPSA.

6

How to Get PMSI Super-Priority

Non-Inventory Collateral

• Perfection of PMSI (attachment, value, registration, etc.) within the specified

time frames.

Inventory Collateral

• Perfection of PMSI (attachment, value, registration, etc.) within the specified

time frame; and

• a PMSI notice is delivered to all prior secured parties with a prior interest in

the inventory or accounts of the debtor prior to the debtor taking

possession.

7

Registration and Other Perfection Steps

• Non-Inventory – For collateral other than intangibles, perfected before or within 15 days after debtor (or

third-party at request of debtor) obtained possession “as a debtor”.

– For intangibles, perfected before or within 15 days after the security interest attached.

• Inventory– Perfected before the goods come into the possession of the debtor.

• When the debtor comes into possession of the collateral is a critical time. All PMSI creditors should maintain records of when their debtor came into possession of the PMSI collateral.

• Possession by the debtor can (and frequently does) arise before the goods are physically delivered to the debtor.

8

PMSI Notices

• If the collateral will become inventory in the hands of the debtor, notice of the security interest must be provided:

– To (and received by) all creditors who have registered a financing statement against the inventory or accounts of the debtor prior in time to the PMSI creditor’s registration.

– Before the debtor receives possession of the inventory.

• Content of Notice:

– a statement that the creditor has or expects to acquire a PMSI in inventory of the debtor; and

– a description of the inventory by item or type.

• Search against the debtor under the PPSA to identify who receives notice afterthe PMSI lender has filed its own financing statement.

9

Summary to get Super Priority

There are the following requirements to get a super priority PMSI:

• Must satisfy the definition of PMSI

• Must satisfy the perfection requirements within the specified time frames (prior to possession for inventory collateral and prior to or within 15 days of possession for most non-inventory collateral)

• Must deliver PMSI notices to prior secured creditors in accounts and inventory prior to possession for inventory collateral

10

Consequences of Not Perfecting

Failure to Perfect by Registration

• If not registered, then the creditor has an unperfected security interest and not a PMSI.

• Late registration will not create a PMSI in already-delivered collateral (subject to 15-day window for non-inventory), but can support a PMSI in as-yet undelivered collateral.

Failure to Provide Notice (Inventory)

• A creditor can still have a perfected security interest, subject to the first to file rule and any intercreditor arrangements.

• Late notice can support a PMSI in any inventory that is delivered after notice is provided.

11

PMSI Priority

• General Rule: – Under the PPSA, PMSI’s rank in priority to other security interests in the

same goods.

– However, there are several exceptions.

• PMSI vs. Other PPSA Security Interests– A PMSI will have priority over all other PPSA security interests in the

same collateral, even if those security interests were registered before the PMSI lender's registration.

• Proceeds– PMSI priority extends to proceeds, so long as the proceeds are identifiable

and traceable.

12

Competing PMSIs in the Same Collateral

• Seller PMSI vs Lender PMSI

– The PPSA gives priority to the seller PMSI over the lender or any other

PMSI.

– General policy reason is that lenders are more sophisticated than

sellers, and are therefore more likely to conduct searches.

• Lender PMSI vs Lender PMSI

– Residual priority rule would apply, i.e. the first to file.

13

Priority over Other Interests in Collateral

Bank Act Security vs. PMSI• If the PMSI holder perfected their PMSI (registered) first, it will have

priority.

• If the Bank Act security was perfected first:– If the PMSI holder is a supplier who reserved or retained title to the collateral (such as

in a true lease of equipment or a conditional sales contract), then the borrower will not be able to assign title to the bank and the PMSI supplier will win.

– If title to the goods financed by the PMSI holder passes to the borrower (for example, the PMSI holder is a lender financing the purchase or a supplier that does not reserve title to the collateral in its security agreement), then the first-in-time rule will apply.

14

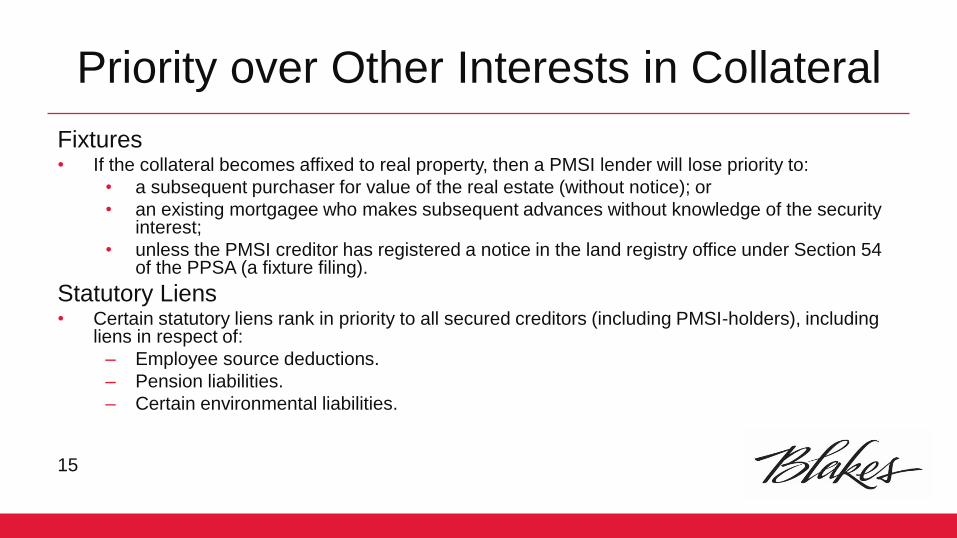

Priority over Other Interests in Collateral

Fixtures• If the collateral becomes affixed to real property, then a PMSI lender will lose priority to:

• a subsequent purchaser for value of the real estate (without notice); or

• an existing mortgagee who makes subsequent advances without knowledge of the security interest;

• unless the PMSI creditor has registered a notice in the land registry office under Section 54 of the PPSA (a fixture filing).

Statutory Liens• Certain statutory liens rank in priority to all secured creditors (including PMSI-holders), including

liens in respect of:

– Employee source deductions.

– Pension liabilities.

– Certain environmental liabilities.

15

Questions?

16

SECURED TRANSACTION ESSENTIALS FOR BUSINESS LAWYERS BUSINESS LAW Opinions on Secured Lending Transactions Karen Rosen, Fogler, Rubinoff LLP

Secured Financing EssentialsFor Business Lawyers

Opinions on Secured Lending TransactionsKaren Rosen, Fogler, Rubinoff LLP

April 27, 2021

I. Developments in Opinions Practice – What is Customary ?

II. Electronic signatures – Impact on Opinions

III. Formulation of Basic Opinions

IV. Multi-Jurisdictional Opinions

V. Opinions on Non-Corporate Entities

VI. Negotiation

VII. Questions ?

2

I. Developments in Opinion Practice

3

While opinions are rare in M&A transactions, they are “market” in lending transactions.

Customary practice guides the scope and nature of the opinions we give and receive on secured lending transaction.

More common to see a confirmation that the opinion giver has not reviewed the minute books of the opinion party.

Resources: Firm Opinion Committees, Practical Law, Toronto Opinions Group (TOROG) and Wilfred M. Estey – Legal Opinions in Commercial Transactions and SLAW.ca

II. E-Signatures and Opinions Work from home has resulted in an increased use of electronic

signatures.

Electronic signatures don’t necessarily look like signatures.

The Electronic Commerce Act, 2000 (Ontario) provides that a requirement for a signature on a document can be satisfied by an electronic signature.

Does the use of an electronic signature require any additional diligence on the part of the opinion giver?

When was the last time anyone attended a traditional closing?

How does the use of an electronic signature change opinion practices?

4

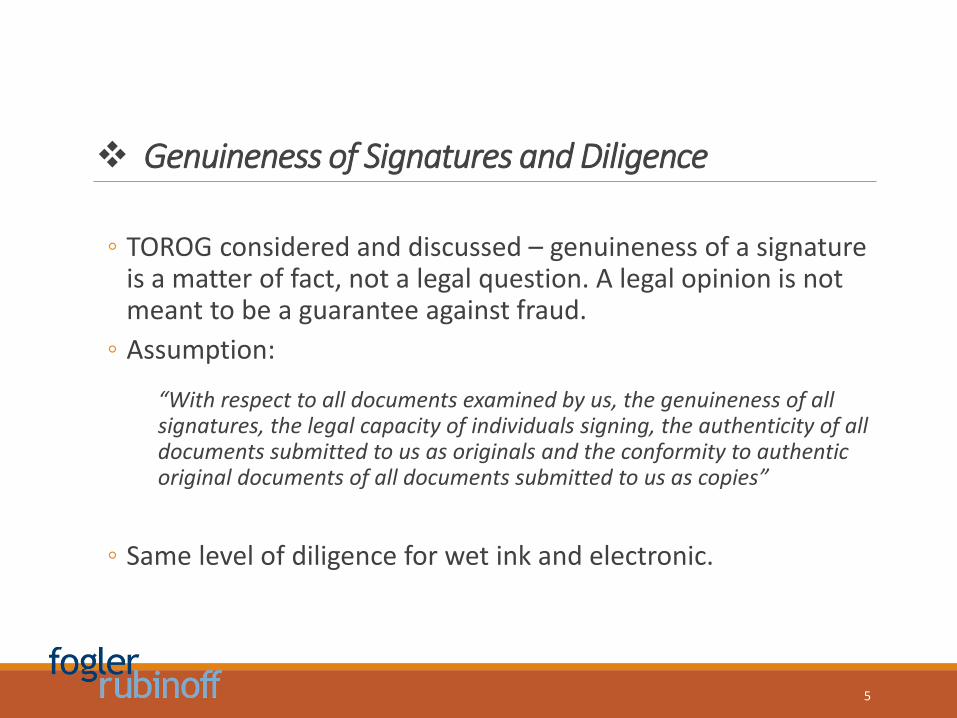

◦ TOROG considered and discussed – genuineness of a signature is a matter of fact, not a legal question. A legal opinion is not meant to be a guarantee against fraud.

◦ Assumption:

“With respect to all documents examined by us, the genuineness of all signatures, the legal capacity of individuals signing, the authenticity of all documents submitted to us as originals and the conformity to authentic original documents of all documents submitted to us as copies”

◦ Same level of diligence for wet ink and electronic.

5

Genuineness of Signatures and Diligence

Incumbency

◦ Officer’s Certificate often includes incumbency certificate which certifies directors and officers of the Corporation, titles and sometimes a specimen signature of the officer(s) signing the transaction documents.

◦ What is the utility of a specimen signature if the signatories are using a digital signature or typewritten electronic signature ?

◦ TOROG discussed ongoing inclusion of specimen signatures as part of an officer’s certificate.

◦ Should opining lawyer be verifying handwriting ? To compare the specimen with the signatures on the signed documents ?

6

III. Formulation of Basic OpinionsWhile each firm usually has its own preferred version, most opinions typically follow a similar structure and format:

Opening paragraph describing the opinion parties

A list of loan and security documents which are the subject of the opinion

A list of examined documents which are necessary in completing due diligence and providing support for opinions

Reliance and assumptions

Law

Opinions

Qualifications and Limitations

7

Opinions

◦ Corporate existence

◦ Power and capacity

◦ Corporate action and authority

◦ Execution and delivery

◦ Enforceability

◦ No conflict with articles; laws or USA

◦ Creation of valid security interest

◦ Registration opinion

◦ No authorization or consent or approval required

8

Opinions

If there are shares being pledged:

◦ Authorized and issued share capital

◦ Perfection by control

◦ All necessary corporate action to authorize the transfer of the pledged shares

9

Qualifications

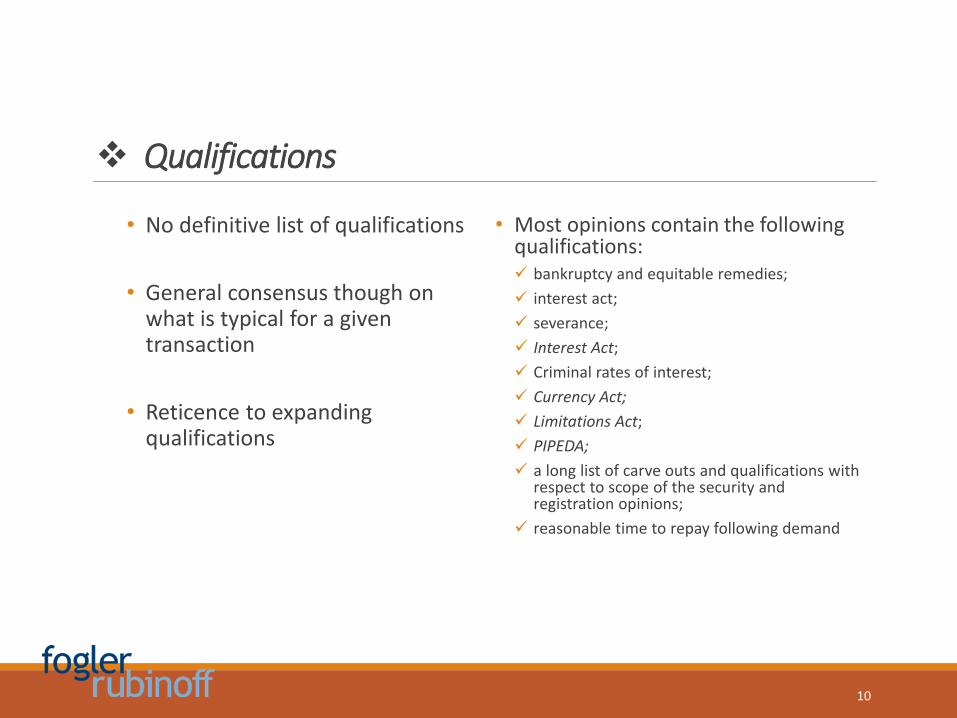

• No definitive list of qualifications

• General consensus though on what is typical for a given transaction

• Reticence to expanding qualifications

• Most opinions contain the following qualifications: bankruptcy and equitable remedies;

interest act;

severance;

Interest Act;

Criminal rates of interest;

Currency Act;

Limitations Act;

PIPEDA;

a long list of carve outs and qualifications with respect to scope of the security and registration opinions;

reasonable time to repay following demand

10

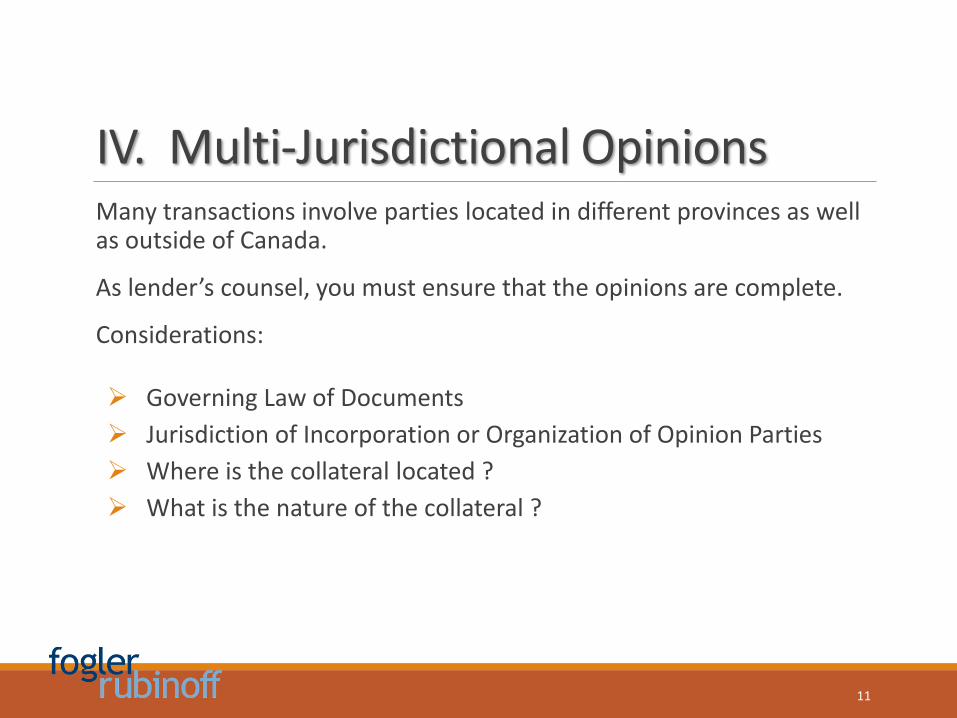

IV. Multi-Jurisdictional OpinionsMany transactions involve parties located in different provinces as well as outside of Canada.

As lender’s counsel, you must ensure that the opinions are complete.

Considerations:

Governing Law of Documents

Jurisdiction of Incorporation or Organization of Opinion Parties

Where is the collateral located ?

What is the nature of the collateral ?

11

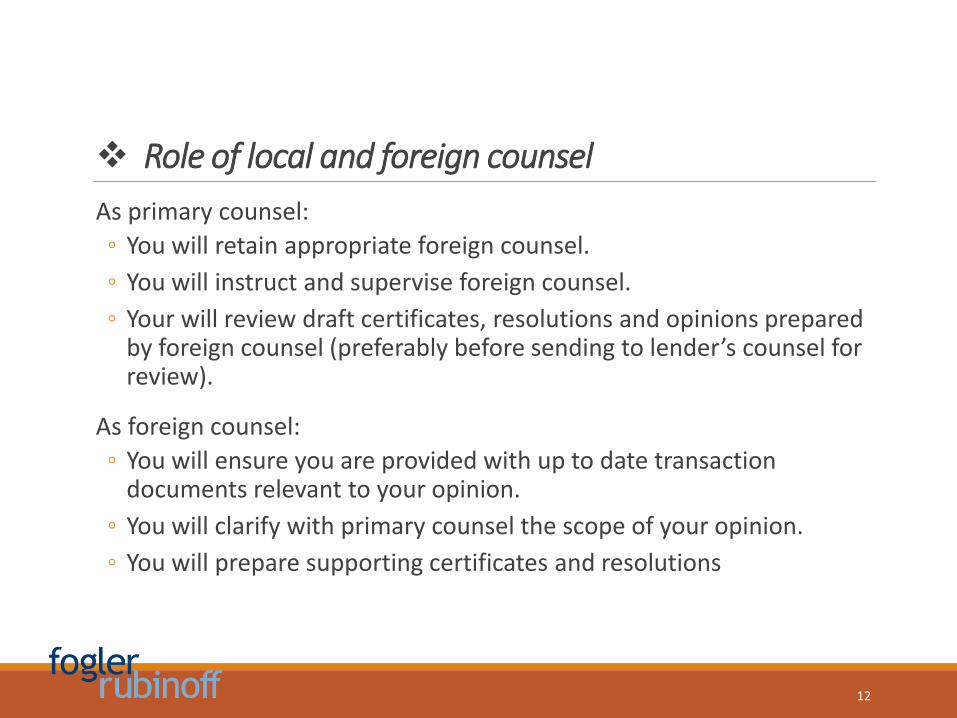

Role of local and foreign counsel

As primary counsel:

◦ You will retain appropriate foreign counsel.

◦ You will instruct and supervise foreign counsel.

◦ Your will review draft certificates, resolutions and opinions prepared by foreign counsel (preferably before sending to lender’s counsel for review).

As foreign counsel:

◦ You will ensure you are provided with up to date transaction documents relevant to your opinion.

◦ You will clarify with primary counsel the scope of your opinion.

◦ You will prepare supporting certificates and resolutions

12

V. Opinions on Non-Corporate Entities

Trusts

Partnerships

Limited Partnerships

Natural Person

13

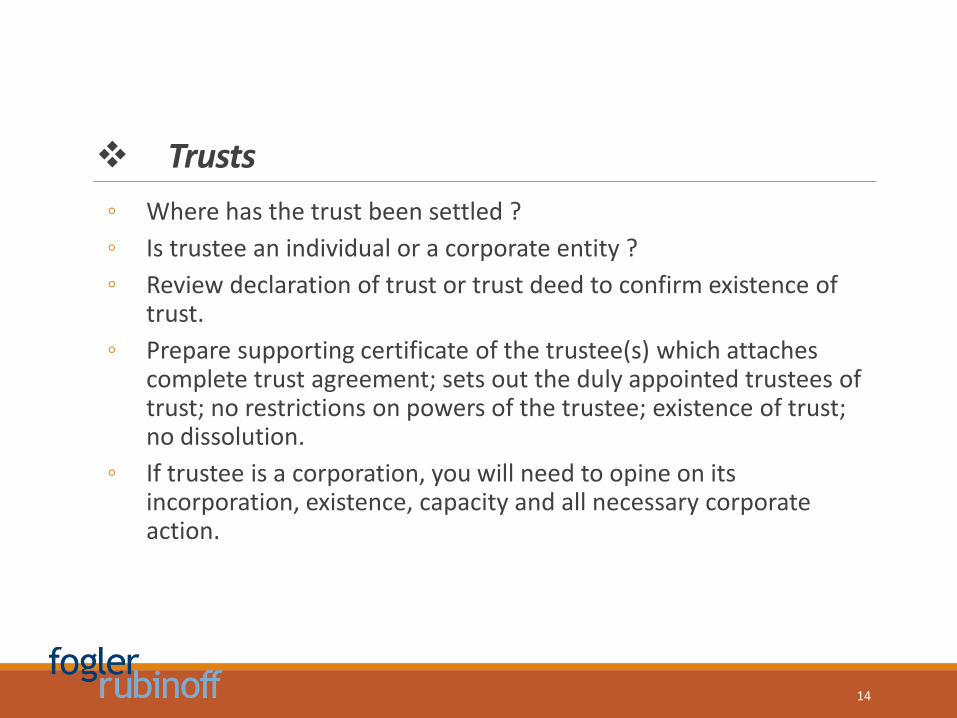

Trusts

◦ Where has the trust been settled ?

◦ Is trustee an individual or a corporate entity ?

◦ Review declaration of trust or trust deed to confirm existence of trust.

◦ Prepare supporting certificate of the trustee(s) which attaches complete trust agreement; sets out the duly appointed trustees of trust; no restrictions on powers of the trustee; existence of trust; no dissolution.

◦ If trustee is a corporation, you will need to opine on its incorporation, existence, capacity and all necessary corporate action.

14

Partnerships

◦ Review the partnership agreement. What is the process for authorizing agreements or transactions ? Do all partners need to sign agreements or can certain partners be appointed to execute agreements ?

◦ Determine if the partnership name registered under the Business Names Act (Ontario).

◦ Obtain a supporting certificate from the partners certifying the completeness of the partnership agreement; all partners; no restrictions; existence; no dissolution.

◦ Are any of partners corporate entities ?

15

Limited Partnerships

◦ Must have filed a declaration with the Registrar appointed under the Business Names Act;

◦ Review current limited partnership report;

◦ Review limited partnership agreement;

◦ Prepare supporting certificate of the general partner on behalf of the limited partnership certifying completeness of the limited partnership agreement; declaration; confirming general partner; existence; solvency of general partner; no liquidation or dissolution; no proceedings; no restrictions on powers and authority of the general partner to carry on and manage the business.

16

Natural Person

◦ We assume power and legal capacity as well as genuineness of signatures of an individual.

◦ If individual is unknown to you, obtain government issued ID. Consider having the documents signed in person.

17

VI. Negotiation It is typical for lender’s counsel to prepare the first draft of a form of

opinion.

Usually counsel for borrower and other opinion parties will customize the opinion and will often add additional assumptions and qualifications. Ensure qualifications are relevant.

In some instances borrower’s counsel will resist giving enforceability on standard form bank documents which cannot be varied or negotiated.

Parties will often negotiate the contents of the officer’s certificate or supporting certificate prepared by borrower’s counsel. Certificates should only address matters of fact and should not contain legal conclusions.

18

SECURED TRANSACTION ESSENTIALS FOR BUSINESS LAWYERS BUSINESS LAW Considerations When Enforcing Security Craig Mills, Miller Thomson LLP

V A N C O U V E R C A L G A R Y E D M O N T O N S A S K A T O O N R E G I N A L O N D O N K I T C H E N E R - W A T E R L O O G U E L P H T O R O N T O V A U G H A N M A R K H A M M O N T R É A L

Considerations When Enforcing Security: A Practical Guide

Secured Transaction Essentials for Business Lawyers, OBA

Craig Mills, Partner

2

Agenda + Introduction:

1. Initial Considerations

2. Issuing the Demand Letter

3. Enforcing the Security

April 2021

3

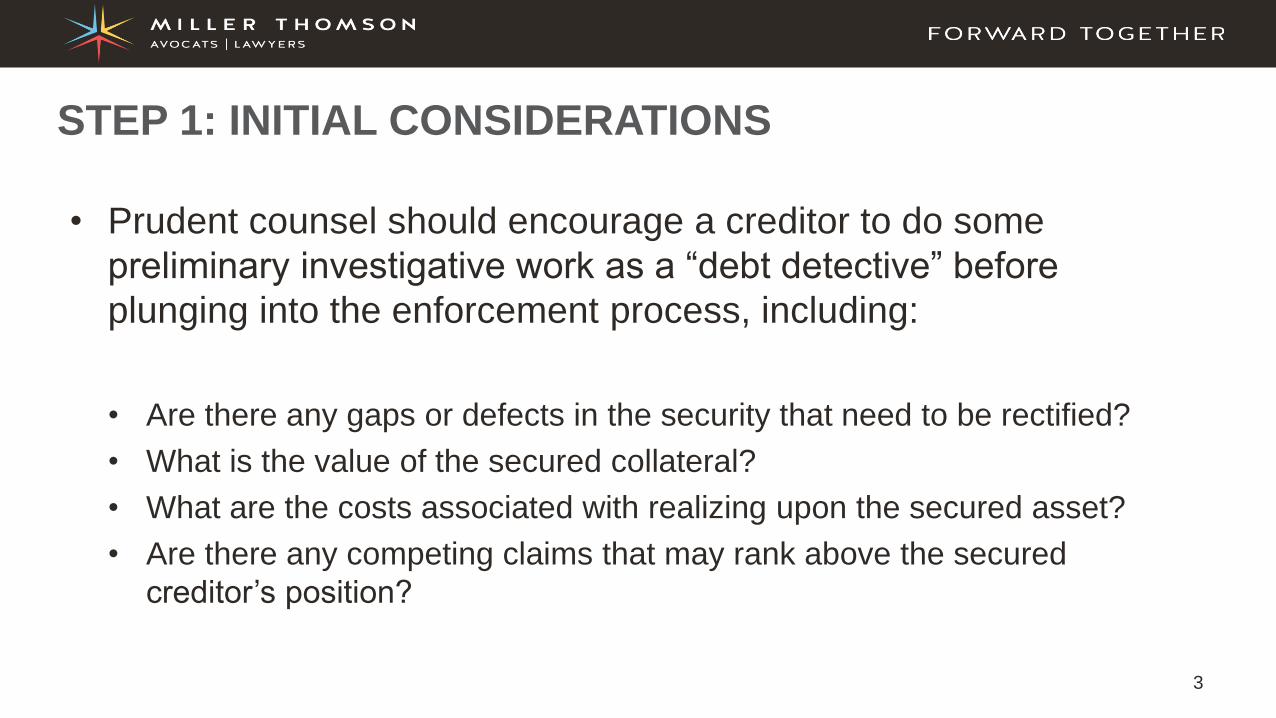

• Prudent counsel should encourage a creditor to do some

preliminary investigative work as a “debt detective” before

plunging into the enforcement process, including:

• Are there any gaps or defects in the security that need to be rectified?

• What is the value of the secured collateral?

• What are the costs associated with realizing upon the secured asset?

• Are there any competing claims that may rank above the secured

creditor’s position?

STEP 1: INITIAL CONSIDERATIONS

4

• Pre-enforcement is the best time to ensure that there are no defects in the

security agreement

• Some of the things a creditor should look for include:

• Executed copies of director’s resolutions authorizing the security interest

being granted

• Evidence of the funds being advanced by creditor

• Can the creditor establish that the security interest has attached to the

collateral in question and that it has been properly perfected?

• Does the file contain estoppel letters (a “no interest letter”) or priority/inter-

creditor agreements signed by other creditors?

• Are there landlord/mortgagee waivers (if appropriate)?

SECURITY REVIEW

5

• The corresponding PPSA registration(s) should be reviewed to

ensure that the debtor names are properly entered (including

English and French versions of the corporate name) and the

collateral description matches the security

• A current corporate profile report should also be obtained

• If a motorized vehicle is the asset, the registration should include

the VIN

• Counsel should suggest that a security review be prepared

SECURITY REVIEW (cont’d)

6

• Most security agreements permit the secured party reasonable access to

inspect the collateral or obtain financial information

• Creditor may consider performing a spot audit to review the books and

records of the debtor to assess financial position and/or collateral

• Alternatively, the creditor might also consider appointing a “monitor” under its

security to put together a snapshot of the debtor’s financial position

• Ensure that the monitoring agreement clearly states that the monitor does not

have any control over the operations, management or affairs of the debtor

• An appraiser can be engaged by your client, as appropriate

ASSESSING THE VALUE OF THE COLLATERAL

7

• Second phase of pre-enforcement analysis is to determine whether any are competing claims that could present issues for your client in maximizing recovery (ex. statutory liens or deemed trusts created under federal and provincial legislation can have priority over perfected security interests)

Other Secured Creditors

• Obvious first step is to review creditor’s security to ensure that it is valid and enforceable

• This includes an assessment of other competing security interests, ex: Is your client the first PPSA registrant against the debtor? Does it rank in priority as a PMSI creditor?

• Alternatively, is there an inter-creditor agreement or postponement/subordination agreement in place with a prior ranking PPSA creditor?

COMPETING CLAIMS

8

Deemed Trusts

• Deemed trust claim is a super-priority claim that ranks ahead of all creditors

• It arises under a number of taxation statutes; ensures that an employer faithfully remits employee

remittances (income tax, employment insurance and Canada Pension Plan) or HST remittances

• Should the employer and/or vendor fail to remit these amounts, the legislation provides that the

provincial or federal government has a “super-priority” claim over the debtor’s assets ahead of

secured creditors

• Unfortunately, a deemed trust claim will not be revealed through a PPSA or other form of search

• Exceptions: Security in the form of a conditional sales agreement or lease agreement falls outside

the net of the deemed trust

• In respect to real property, the super-priority claim is subject to a “prescribed security interest”

– a pre-existing mortgage registered prior to the deemed trust being triggered

COMPETING CLAIMS (Continued)

9

Deemed Trusts (Continued)

• Unless have debtor’s consent authorizing CRA to release information to the creditor, it is difficult

to verify these amounts independently

• Creditor may be left with relying upon debtor or “best guesstimate” when attempting to quantify

deemed trust.

• Priority of some deemed trusts may be reversed by way of a bankruptcy.

• Section 67(2) of the BIA: all statutory deemed trusts are rendered invalid in a bankruptcy except

for the deemed trust for employee source deductions (income tax, CPP and EI) or for provincial

deemed trusts relating to taxes similar in nature to the Income Tax Act or a provincial pension

plan which is of the same nature as the Canada Pension Plan. No protection extended to HST

deemed trust

• If the debtor’s assets are insufficient to pay both the secured creditor’s claims and a Crown claim

for unremitted HST, secured creditor may wish to consider whether a bankruptcy is warranted

COMPETING CLAIMS (Continued)

10

Wage Earner Protection Program Act

• The Wage Earner Protection Program (“WEPP”) ensures payment of outstanding wages to employees whose employer becomes bankrupt or is subject to a receivership within the meaning of subsection 243(2) of the BIA

• Covers eligible wages up to an amount equal to seven (7) times the maximum weekly insurable earnings under the Employment Insurance Act

• Federal government is subrogated to the rights of the wage earner against the bankrupt company/company in receivership

• Employee Charge: Under s. 81.3 and 81.4 of the BIA, employee wage claims are given a "super-priority" charge of $2,000 per employee over the current assets (cash, accounts receivable and inventory) of an employer in the event of a bankruptcy or the appointment of a receiver (including both privately and court appointed receivers)

• Pension Charge: a similar priority extended to unremitted employer pension contributions, although no maximum limit was set

• Secured creditors should take potential WEPPA obligations into account prior to taking steps to enforce their security

COMPETING CLAIMS (Continued)

11

Landlords

• Payment default under a security agreement usually means parallel default under the debtor’s lease

• The landlord’s right of distraint permits a landlord to seize the tenant’s assets and sell them for purposes of recovery

• Landlord is unable to seize assets owned by a third party; however, creditors should be mindful that there is a possibility that the landlord may exercise its right of distraint on the debtor’s assets over which the secured party has security

• Should the landlord seize and sell the collateral prior to the secured party taking any steps to enforce its security, the landlord will prevail: “race of the swiftest”

• Best case scenario: creditor has waiver from the landlord in which it agreed not to distrain against the secured party’s collateral.

• Where the creditor has not obtained a waiver from the landlord, the creditor may consider initiating bankruptcy proceedings to stay landlord’s distraint remedy (if not completed)

COMPETING CLAIMS (Continued)

12

Purchase Money Security Interest

• PMSI: security interest that ranks ahead of all other secured creditors, regardless of the timing of the creditor’s

registration, assuming the secured creditor has satisfied the requirements of s. 33 of the PPSA

• This may not always be clear from PPSA search; creditor can request details of security under s. 18 of PPSA

Bank Act Creditors

• Separate regime from PPSA for banks

• For valid security: (a) the debtor must deliver a security agreement to the bank; and (b) bank must properly register

its security in the Bank of Canada registry: s. 427 of the Bank Act

• Upon registering a valid security interest, bank then obtains priority over all rights subsequently acquired in the same

assets, including the rights of an unpaid vendor

• It effectively vests the right and title of the owner of the goods in the bank, giving bank a first and preferential lien

• Bank Act vs. PPSA: Generally speaking, the ‘first-in-time’ rule applies

COMPETING CLAIMS (Continued)

13

• Letter gives clear notice to the debtor that the debt is due and the consequences that will result should the letter go ignored

• Demand should clearly set out: (i) the amount of the indebtedness; (ii) the nature of the indebtedness; (iii) name of creditor and the per diem interest rate accruing on the overdue accounts

• A clear deadline or cure date should be clearly indicated to the recipient along with the consequences of ignoring the letter (e.g. the commencement of litigation and/or the creditor exercising its enforcement rights)

STEP 2: ISSUING THE DEMAND LETTER

14

• The suitable amount of common law “reasonable notice” is fact

specific and will need to be weighed in light of various factors

which include: (1) the amount of the loan; (2) the length of the

relationship between debtor and creditor; (3) the risk to the

secured creditor of losing its money or the collateral; and (4) the

character and reputation of the debtor

• In practice, most counsel adopt a standard ten day notice period

as it tracks the ten day notice period required under the BIA

How much notice must a secured creditor give?

15

• Under s. 244(1) of the BIA, secured creditors are required to give 10 days’ notice (calendar days) prior to enforcing their security against “all or substantially all” of the debtor’s inventory, accounts receivable or other property

• Prescribed form known as a “Notice of Intention to Enforce Security”

• Must be sent to the debtor in the manner required in the notice provisions in the security agreement

• If the security agreement is silent, then the Section 244 Notice must be sent by registered mail or courier

• Good practice to send copies of the Demand/Notice to any guarantors

• During the mandatory 10 day notice period, the secured creditor cannot take any steps to enforce its security unless the debtor consents to earlier enforcement (obtained after notice sent)

S. 244 of the BIA

16

• If security at risk during 10 day notice period, creditor can apply to the court, without notice to the

debtor, under s. 47 of the BIA, either before or after the notice is delivered, for the appointment of an

interim receiver to take control of the debtor’s assets and preserve them

• Secured creditor must clearly establish that it is necessary for the protection of the debtor’s estate or

the interests of the creditor

• Creditor must also show that there is significant danger that the debtor’s assets will be dissipated

• Application must be made in the “locality of the debtor” – meaning where the debtor carries on business

or resides

• Appointment of an interim receiver terminates upon the earliest of:

1. Court-appointed receiver (s. 243 BIA) taking of possession of the debtor’s property;

2. Trustee taking possession of the debtor’s property; and

3. Expiry of 30 days after the appointment of the interim receiver or any period specified by the court.

• Powers of interim receiver are purposely limited to, subject to the discretion of the court, taking

possession, exercising control over the property and business and taking conservation measures

S. 244 of the BIA (Continued)

17

• Before enforcing any remedy against a farmer's property, or commencing any proceedings, secured

creditor must also serve the farmer with a Notice of Intent to Realize on Security under the Farm Debt

Mediation Act (FDMA) prior to exercising its remedies under its security.

• The Farm Debt Notice can be served at the same time as the demand letter and Section 244 Notice

• The notice must still be given even if the farmer is not insolvent

• The notice period under the FDMA is 15 business days

• During notice period, or at any time afterwards, the farmer can request a stay of proceedings under s.

5(1)(a) of the FDMA, preventing the creditor from beginning or continuing its enforcement efforts

against the farmer's assets or commencing or continuing any action for the recovery of debt

• The initial term of the stay of proceedings is 30 days, but the stay can be extended in 30 day

increments up to a maximum period of 120 days

• If a secured creditor fails to give a Farm Debt Notice, any act done against the farmer by the

creditor will be null and void

Farm Debt Mediation Act

18

• Under a typical loan agreement, a default occurs when there is a

failure to meet the legal obligations of the agreement. Some of

the most common include:

1. Monetary default;

2. Covenant breaches;

3. Failure to pay insurance dues;

4. Endangering the asset; and

5. Ipso Facto clauses.

What constitutes a default?

19

• A creditor will usually allow for a few missed payments before it

considers enforcement in order to allow the debtor to rectify and

bring the contract payments back in line

• However, beyond a reasonable period of time, the creditor will

need to resort to issuing a demand letter as a first step

• A continued default may lead to consideration of recovering the

asset and termination in accordance with the remedies provided

under the terms of the agreement.

Monetary Default

20

• A lease contract or conditional sale agreement generally require the debtor to maintain appropriate insurance over the asset, naming the creditor as a loss payee or named insured, and provide proof of this to the creditor

• Where the policy lapses or the debtor fails to pay the required premiums, this will trigger a default under the agreement

• This can represent a serious risk to the secured creditor, so a creditor will need a well-established “early warning” system in place so that it can take immediate steps to contact the debtor to reinstate insurance coverage or determine the best way to safeguard the collateral (eg. repossession or appointing a receiver)

Failure to Pay Insurance Dues:

21

• Most contracts include stipulations surrounding the assignment, subletting, or transferring the equipment or asset in question; prior written consent of the creditor must be obtained

• Unauthorized transfer to a third party could impact the enforceability of the creditor’s security interest

• In situations where the creditor is concerned that the equipment or asset is at risk, there are civil remedies that can be used

• Secured creditors should contemplate using a Rule 44 order to obtain an interim recovery order of the asset, or making an application under s. 67 of the PPSA

Endangering the Asset:

22

• Ipso facto clauses: provisions that permit the termination of an agreement due to debtor becoming bankrupt or the subject to a receivership proceeding.

• However, Parliament has enacted legislative provisions that explicitly restrict non-defaulting party’s rights when a debtor becomes subject to a formal insolvency proceeding• s. 65.1 of the BIA nullifies ipso facto clauses when a debtor files a proposal or a notice of

intention to do so

• s. 84.2(1) of the BIA provides that no person may terminate or amend any agreement with a bankrupt individual by reason only of the individual’s bankruptcy or insolvency

• Stay of proceedings under a receivership appointment order or an Initial Order under the Companies’ Creditors Arrangement Act will also stop termination of an agreement/ prohibit enforcement of remedies without consent of the court officer or court authorization

Ipso Facto Clauses:

23

• Does the contract contain cross-default provision?

• A default under Contract A would also be considered to be a default under

Contract B

• Does agreement contain cross-collateralization provision?

• allows a lender to look to additional assets or property as collateral outside

of the original loan and security

• Can be important in reducing risk that there may be a shortfall after

realization on one part of the basket of secured assets

Cross-default and cross-collateralization provisions

24

Forbearance Agreement

• Agreement by which secured creditor agrees to hold off on exercising its rights and/or remedies under its security agreement after an event of default for set period of time

• In exchange for forbearance, creditor will want to specific payment terms/forbearance fee and payment deadlines

• expanded security package such as additional guarantees or collateral security

• Creditor will also require acknowledgments from debtor regarding

• amount of the indebtedness due and owing

• Confirmation of default

• Confirmation that security is valid and enforceable

• debtor’s receipt of any statutory notices, including the Section 244 Notice, the Farm Debt Notice and notices of sale under the PPSA

• waiver of defences and release of claims against the creditor by the debtor and guarantors

• regular financial reporting

• consent to the appointment of a receiver.

STEP 3: ENFORCING THE SECURITY

25

• A secured creditor can seize goods under its security and under s. 62 of the PPSA. Seizure can be

accomplished in one of three ways: (1) by the secured creditor directly, (2) by a bailiff or agent

appointed by the creditor or, (3) through a private receiver appointed pursuant to the terms of the

security agreement.

• The purpose of the receiver is not to operate the debtor’s business but to take possession and control

of the secured assets

• secured creditor can also appoint a receiver and manager for the purpose of selling the business as a

going concern

• receiver must still strive to achieve a commercially reasonable and supportable sale

• where debtor is uncooperative and refuses to allow the receiver or agent on its property, the secured

creditor may be required to obtain an order for recovery under s. 104 of the Courts of Justice Act and

Rule 44 of the Rules of Civil Procedure

• Another option is making an application for a recovery order under the broad provisions of s. 67 of the

PPSA

Taking Possession

26

• Upon successfully seizing the collateral, the secured creditor can then take steps to sell the

collateral

• Prior to selling the secured assets, the creditor (or its private receiver) must issue a notice of

sale (“Notice of Sale”) pursuant to s. 63 of the PPSA

• Must provide at least 15 days’ notice to the debtor, guarantors of the debtor, parties with a

registered security interest and anyone else who has an interest in the collateral

• collateral may be disposed of by way of a public sale, private sale, lease or through another

method at any time or place, provided the disposition is on a “commercially reasonable

basis”

• Although the secured party is able to purchase the collateral, it may only do so at a public

sale unless a court orders otherwise

Selling the Collateral

27

• The creditor issues a notice under s. 65 of the PPSA of its proposal to accept the collateral in

lieu of payment of the debtor’s obligations

• Foreclosure Notice must be delivered to those who would be entitled to a Notice of Sale

under the PPSA

• If no objections are made within 15 days after the Foreclosure Notice is served, (or the

secured party has received written consent from all of the parties entitled to notice), then

creditor is deemed to have accepted the secured asset in full satisfaction of the debt

• If objection in writing, creditor must sell or dispose of the collateral in accordance with s. 63

of the PPSA

• Alternatively, creditor can apply to the Court to obtain an order that objection is ineffective

because objection was made for a purpose other than the protection of the party’s interest in

the collateral or the fair market value of the collateral is less than the total amount owing to

the secured creditor

Foreclosure (Alternative to Sale)

28

• Where the creditor determines that it is not appropriate to appoint a private receiver, it may opt to appoint a receiver

under s. 243 of the BIA and s. 101 of the Courts of Justice Act (“CJA”)

• Where the creditor decides that it necessary to apply for an interim receiver during the ten day notice period, it is

able to continue the appointment under s. 243 of the BIA

• Under s. 243 of the BIA and s. 101 of the CJA, Court may appoint a receiver to take possession of the debtor’s

property and exercise control over the debtor’s business where it is “just and convenient” to do so

• The over-arching benefit of a court-appointed receiver is the stay of proceedings contained in the receivership

order

• The creditor’s desire to appoint a receiver may be tempered by the existence of environmental issues

• Another significant advantage of a court-appointed receiver is the ability to sell assets and property through a

court approved sale process

• Counsel acting for creditors seeking to appoint a court-appointed receiver should consult with the Model

Receivership Order approved by the Commercial List Users Committee

Appointment of Receiver

29

• If there is a remaining deficiency after the security creditor has exhausted its realization efforts, it is

open to that secured creditor to commence a claim against the debtor pursuant to the amounts owing

under the agreement

• Creditor should consider applicable limitation period before commencing proceedings

• According to the 2015 Canadian Lawyer Legal Fees survey, the average cost of a civil action resulting

in a 2 day trial was $47,605 (costs will vary depending on variety of factors)

• Unlike asset realization, litigation can be an extremely lengthy process

• In addition, the costs of litigation are often difficult to estimate due to the potentially unpredictable

behaviour of a debtor

• Consider commencing action under Simplified Rules (R. 76) even where debt is in excess of $200,000

Initiating a Law Suit

V A N C O U V E R C A L G A R Y E D M O N T O N S A S K A T O O N R E G I N A L O N D O N K I T C H E N E R - W A T E R L O O G U E L P H T O R O N T O V A U G H A N M A R K H A M M O N T R É A L

Conclusion

M I L L E R T H O M S O N . C O M

© 2018 Miller Thomson LLP. All Rights Reserved. All Intellectual Property Rights including copyright in this presentation are owned by Miller Thomson LLP. This presentation may be reproduced and distributed in its entirety provided no alterations are made to the form or content. Any other

form of reproduction or distribution requires the prior written consent of Miller Thomson LLP which may be requested from the presenter(s).

This presentation is provided as an information service and is a summary of current legal issues. This information is not meant as legal opinion and viewers are cautioned not to act on information provided in this publication without seeking specific legal advice with respect to their unique

circumstances.

V A N C O U V E R C A L G A R Y E D M O N T O N S A S K A T O O N R E G I N A L O N D O N K I T C H E N E R - W A T E R L O O G U E L P H T O R O N T O V A U G H A N M A R K H A M M O N T R É A L

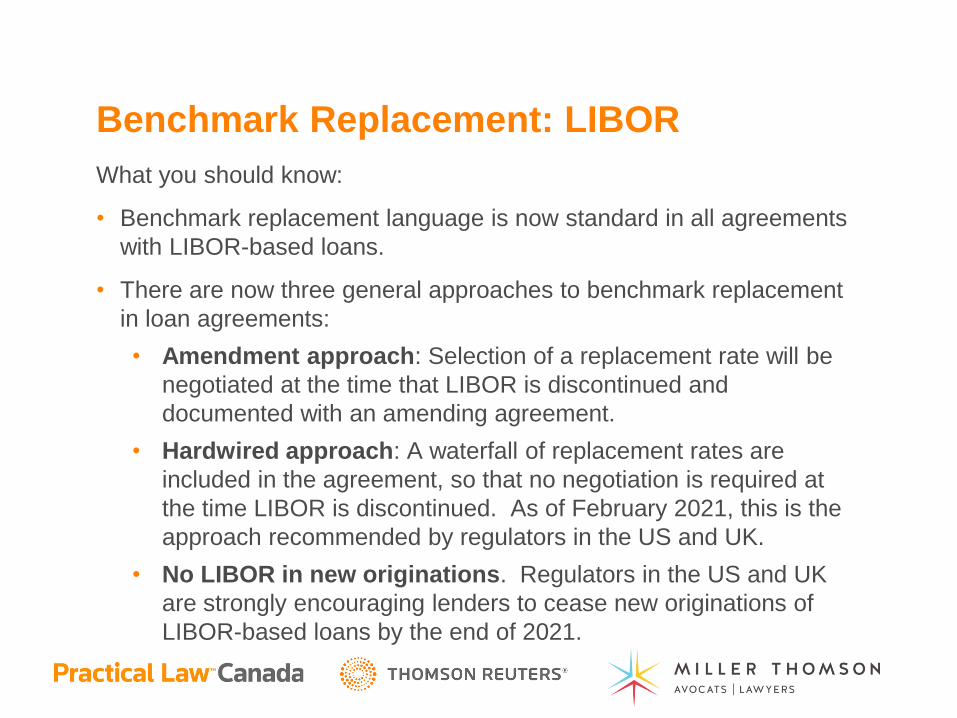

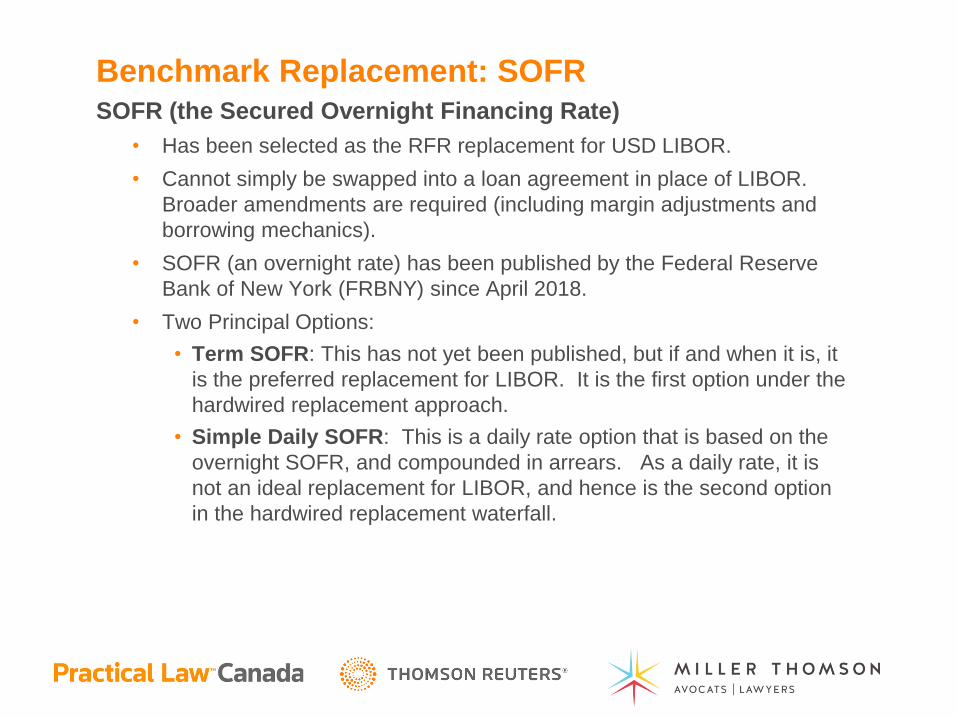

SECURED TRANSACTION ESSENTIALS FOR BUSINESS LAWYERS BUSINESS LAW 2021: Key Developments in Secured Transactions David Reynolds, Miller Thomson LLP Hank White, Practical Law Canada

Key Developments in Secured TransactionsDavid Reynolds, Miller Thomson LLPHank White, Practical Law Canada

Agenda

• Electronic Chattel Paper

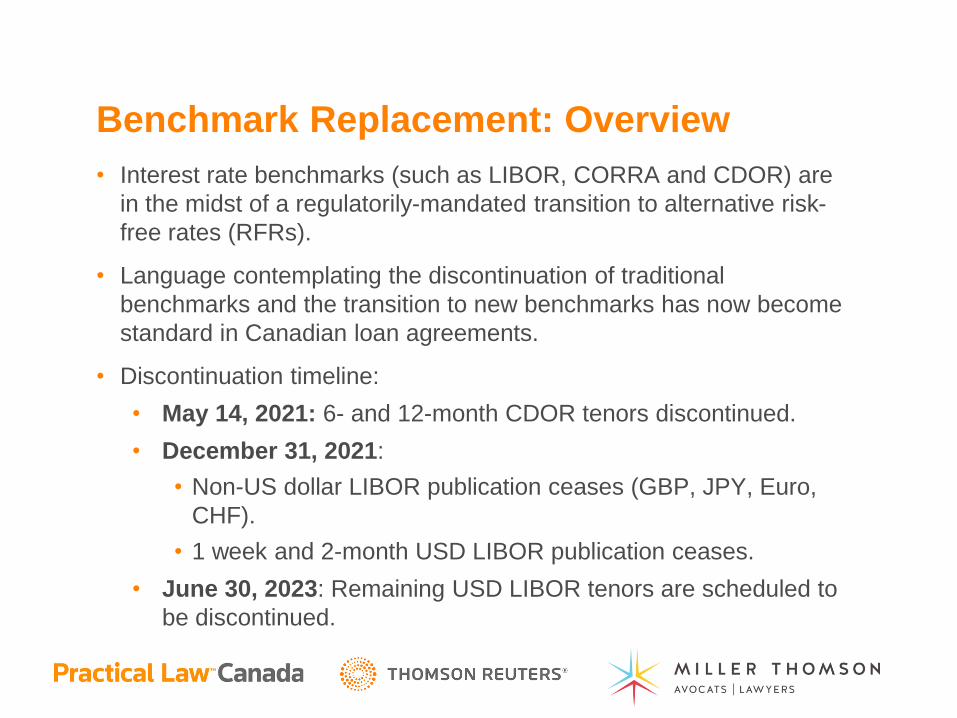

• Benchmark Replacement:

– LIBOR

– CDOR

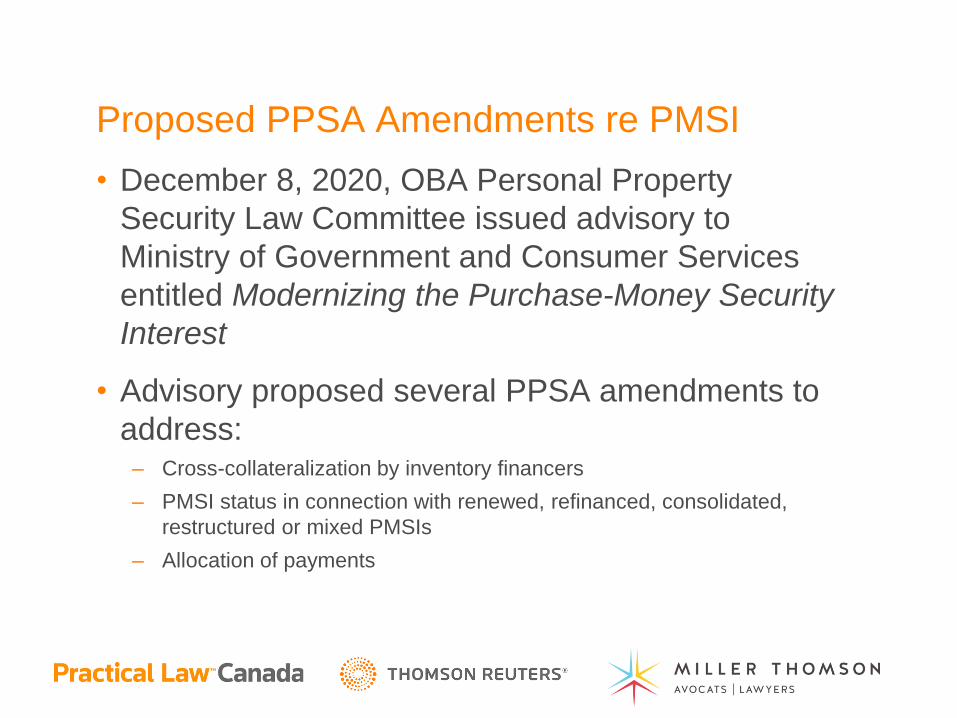

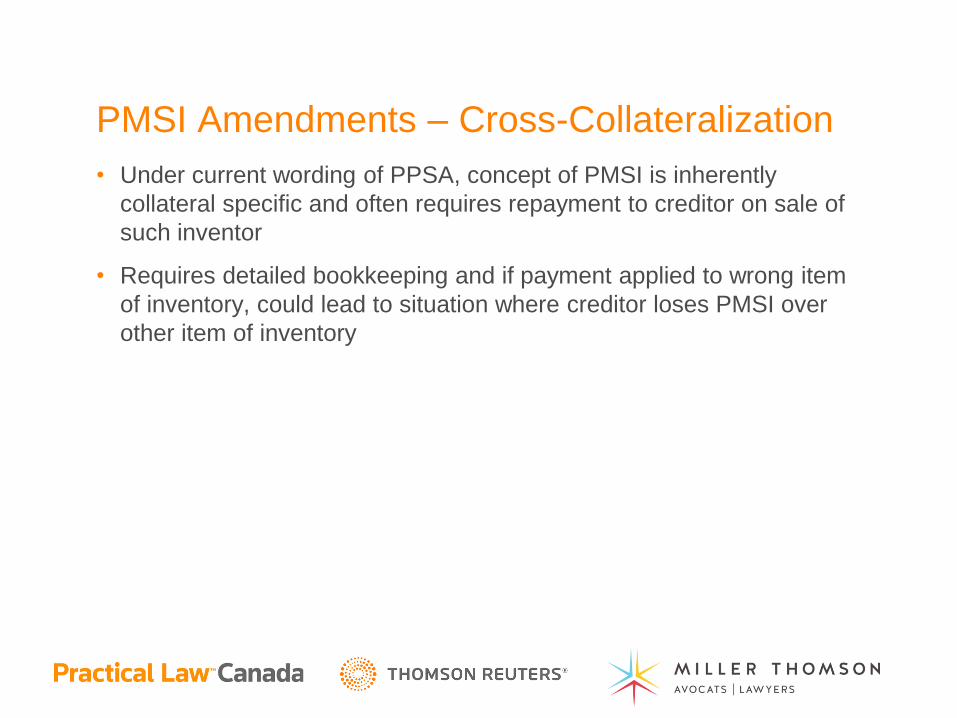

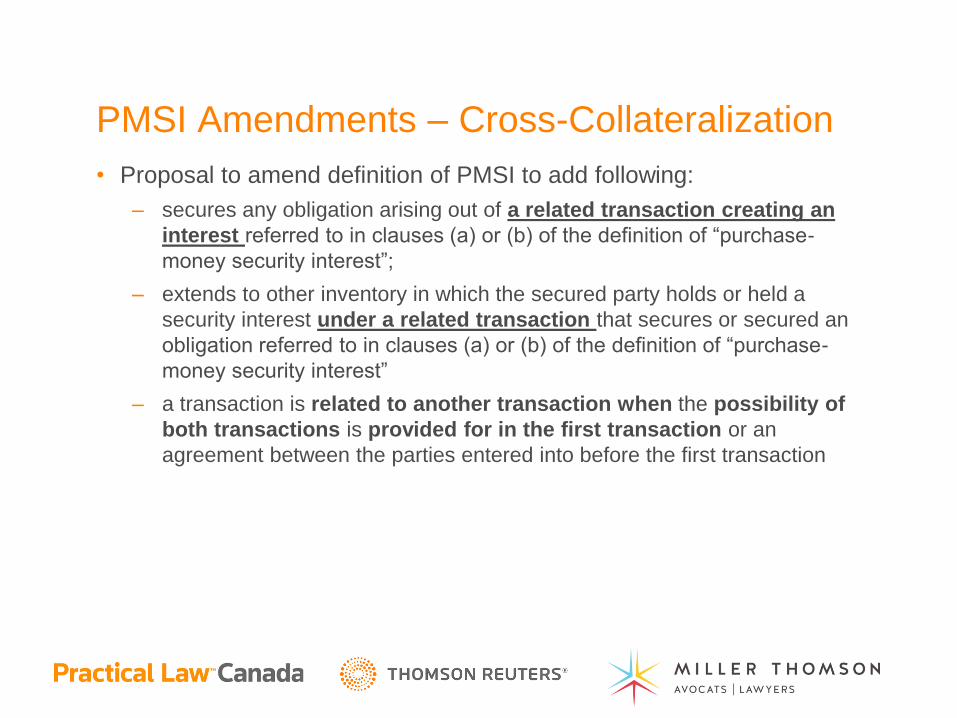

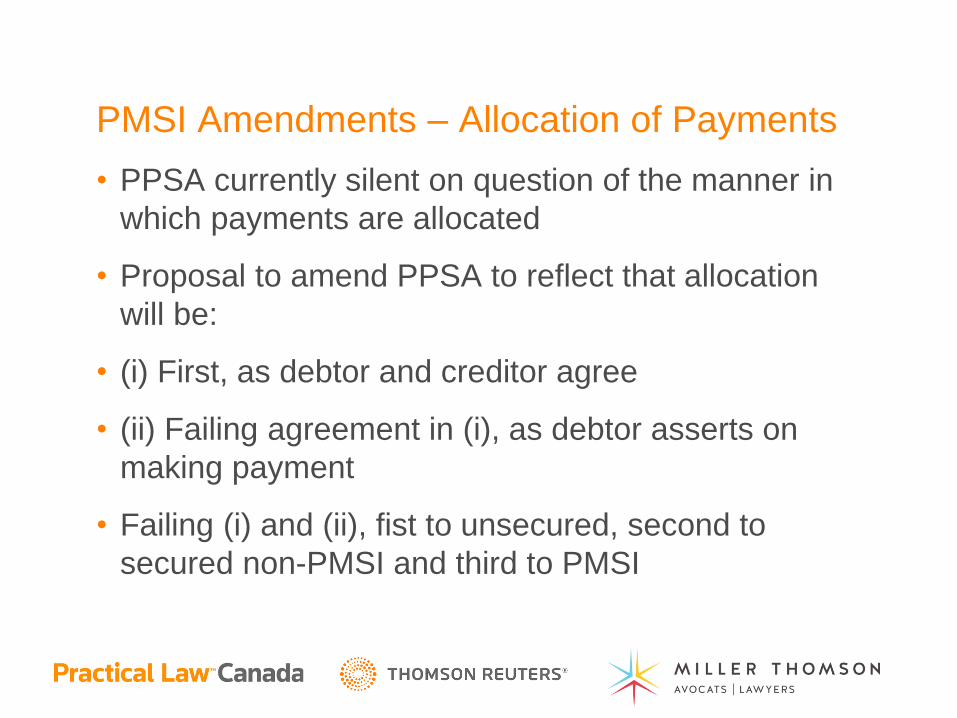

• PPSA Amendments affecting PMSI

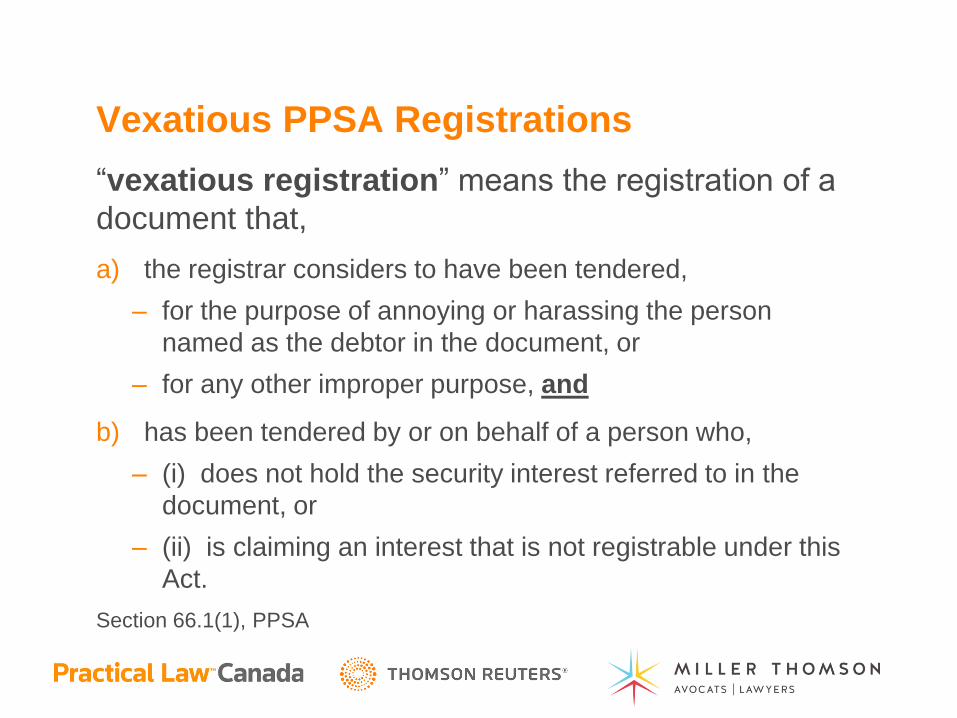

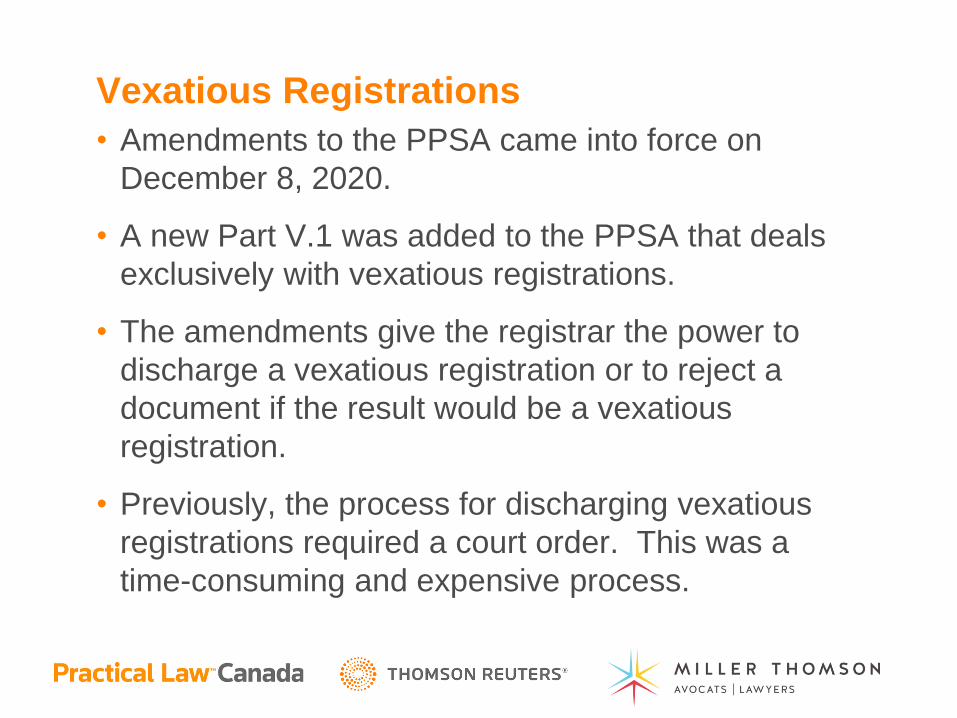

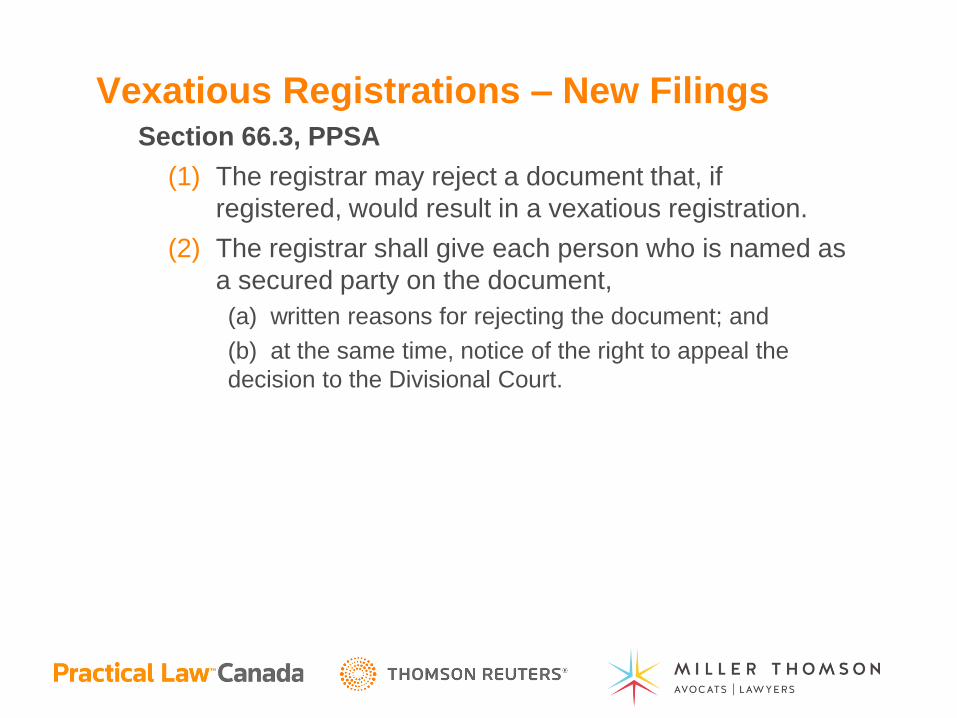

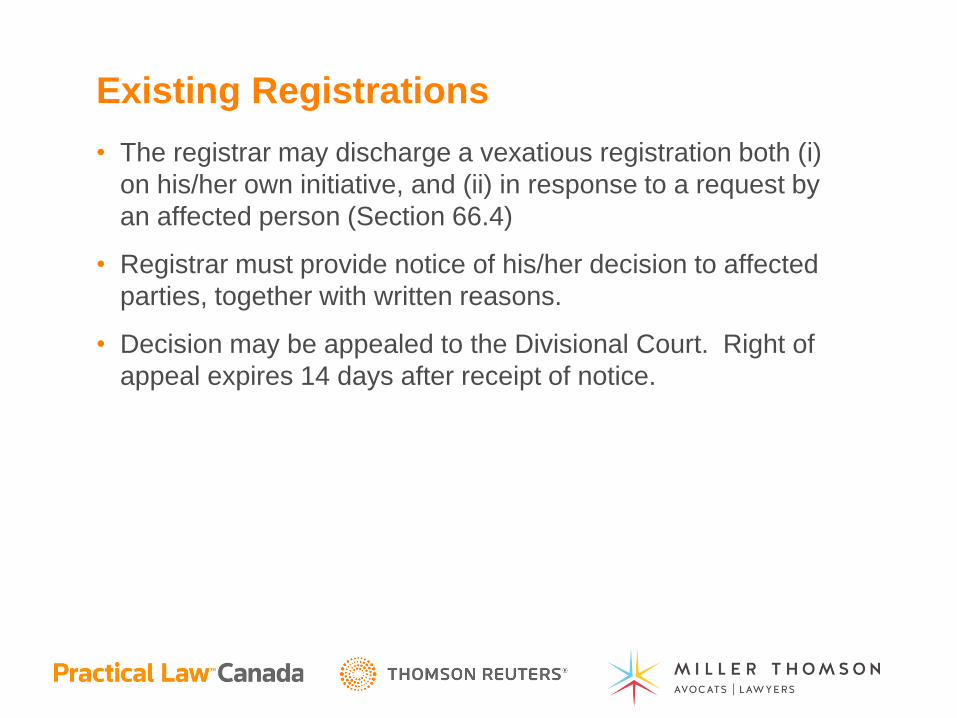

• Vexatious Registrations (PPSA)

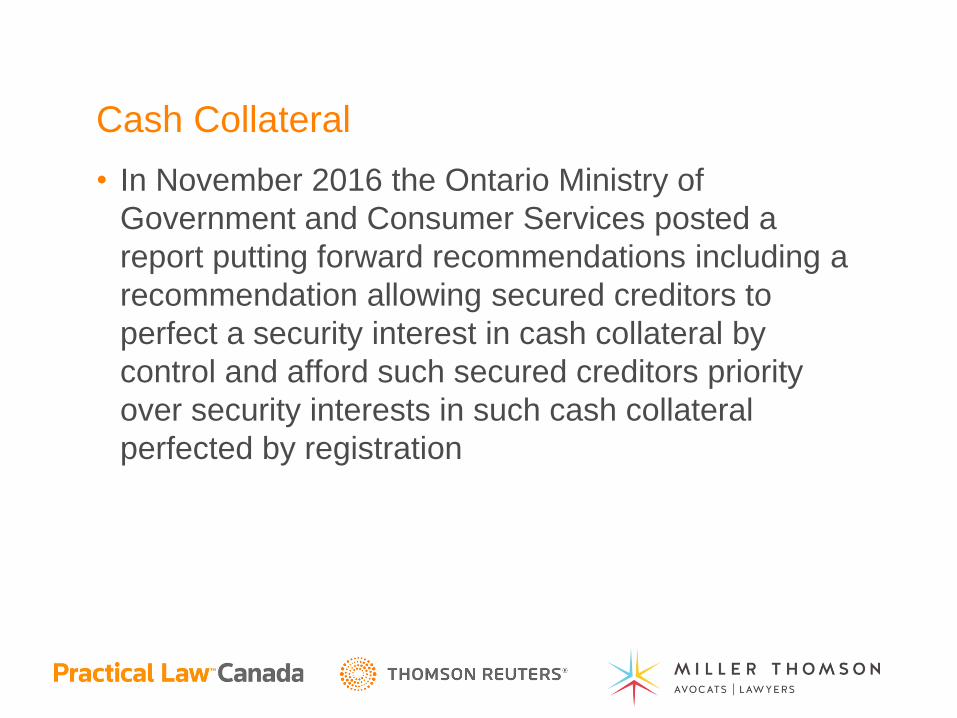

• Cash Collateral

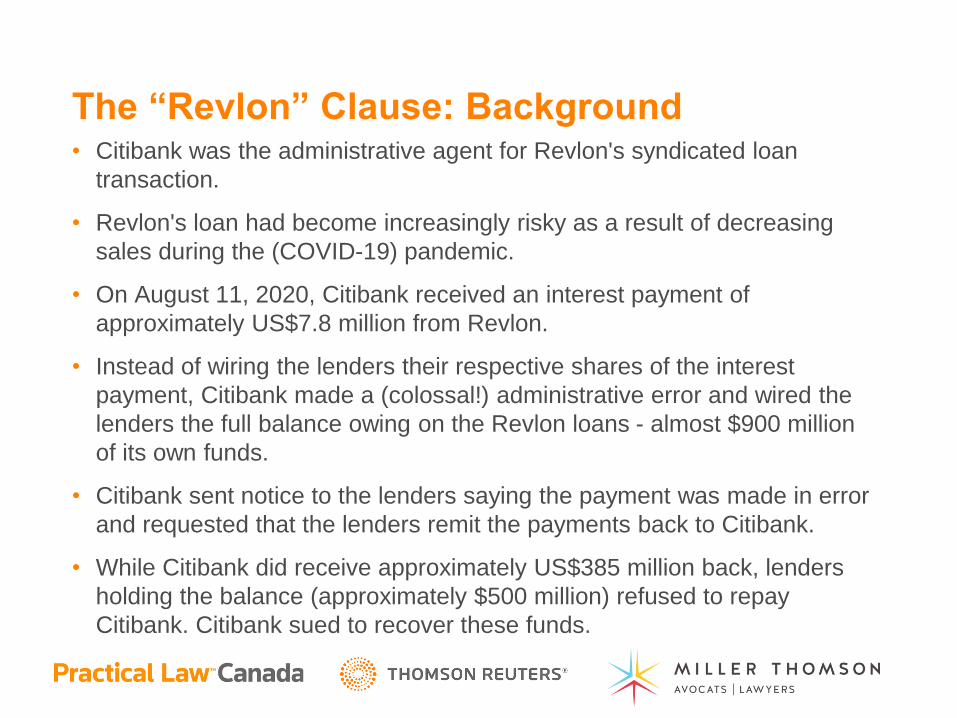

• The “Revlon” Clause

• Questions & Answers

Electronic Chattel Paper – What is Chattel Paper and Current Approach

• What is Chattel Paper

– Record that evidences both a monetary obligation and a

security interest in or a lease of specific goods

• Current Perfection of a Security Interest in Chattel

Paper

– Interest can be perfected by registration or possession

Electronic Chattel Paper – Issues with Current Approach

• Issues with current Approach

– Practically possession is preferred in most cases because

of potential priority afforded against a purchaser of chattel

paper in the ordinary course of business under s. 28 of the

PPSA

– Important for entities that will sell their chattel paper or

assign a security interest in that chattel paper to the

seller’s lender as lenders will typically require assurance

they have first priority

– With a move away from hard copies of documents

towards electronic versions, questions have arisen with

respect to “possession” of chattel paper that exists only in

electronic format

Electronic Chattel Paper – New Definition of Electronic Chattel Paper

• Definition for “Electronic Chattel Paper” and

“Tangible Chattel Paper”

– “electronic chattel paper” means chattel paper created,

recorded, transmitted or stored in digital form or other

intangible form by electronic, magnetic or optical means;

– “tangible chattel paper” means chattel paper evidenced by

a record or records consisting of information inscribed on

a tangible medium;

Electronic Chattel Paper – Control of Electronic Chattel Paper

• Section 1(3) of the PPSA now allows for perfection by control

of Electronic Chattel Paper

– a secured party has control of electronic chattel paper if the record

comprising the chattel paper is created, stored and transferred in a

manner so that,

• (a) a single authoritative record of the electronic chattel paper exists that is unique,

identifiable and, except as otherwise provided in clauses (d), (e), and (f), unalterable;

• (b) the authoritative record identifies the secured party as the transferee of the record;

• (c) the authoritative record is communicated to and securely maintained by the

secured party or the party’s designated custodian;

• (d) copies of or amendments to the authoritative record that add or change an identified

transferee of the authoritative record can be made only with the consent of the secured

party;

• (e) each copy of the authoritative record and any copy of a copy is readily identifiable

as a copy that is not the authoritative record; and

• (f) any amendment of the authoritative record is readily identifiable as to whether it is

authorized or unauthorized.

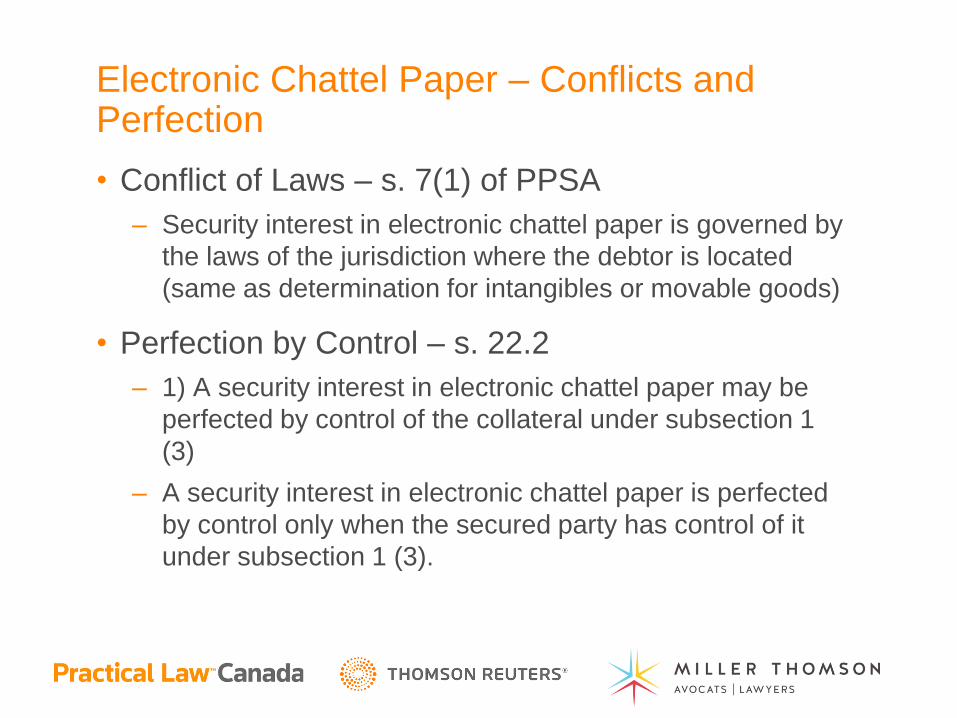

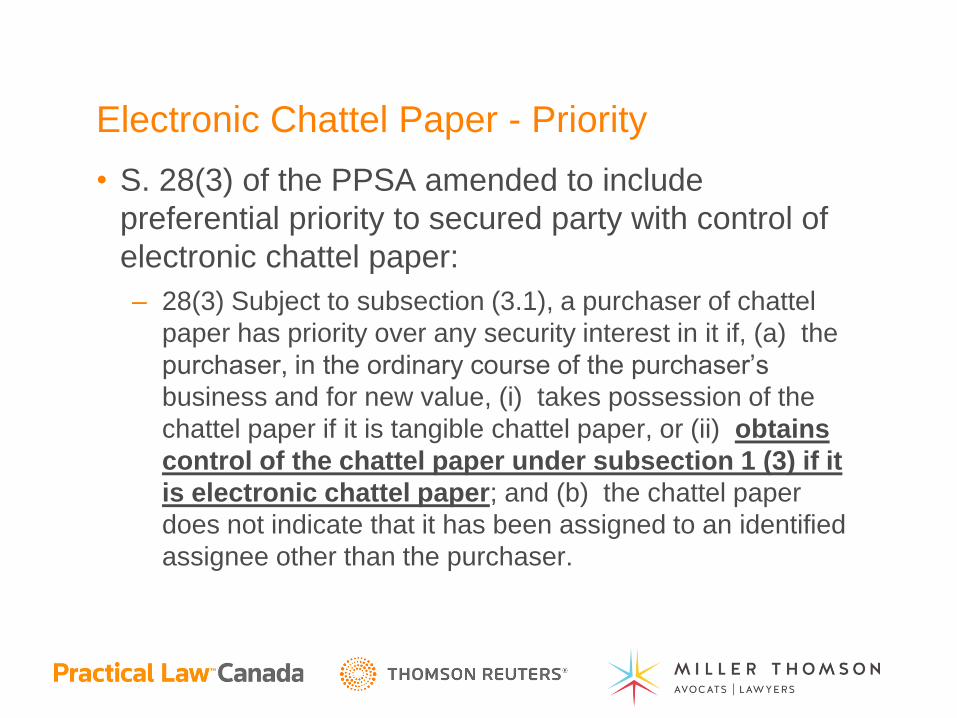

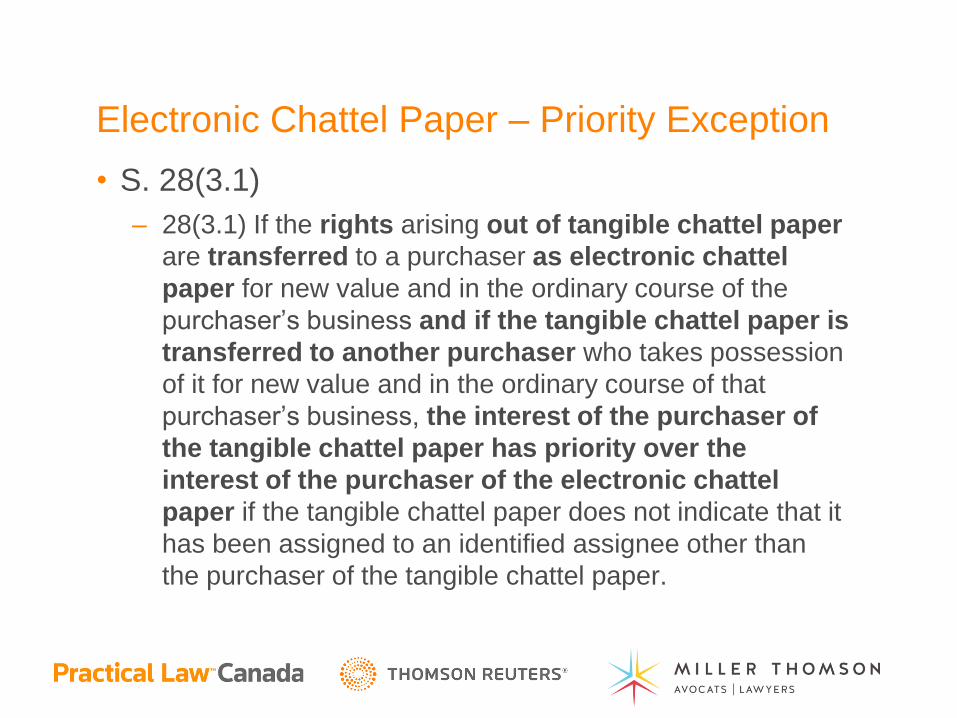

Electronic Chattel Paper – Conflicts and Perfection

• Conflict of Laws – s. 7(1) of PPSA

– Security interest in electronic chattel paper is governed by

the laws of the jurisdiction where the debtor is located

(same as determination for intangibles or movable goods)

• Perfection by Control – s. 22.2

– 1) A security interest in electronic chattel paper may be