Section 3 – Underwriting Policies Section 3.… · Section 3 – Underwriting Policies ......

29

Section 3 – Underwriting Policies Go to specific points of interest using Bookmark Links on the left Overview General Description This section discusses Nationwide Bank’s Underwriting Policies and Procedures. For specific product underwriting guidelines please refer to that product in Section 2 of the Seller Guide. Underwriting Guidelines Typically all Conventional loans are underwritten by Nationwide prior to close, unless Delegated Underwriting has been approved for the correspondent. Nationwide offers FHA underwriting as well as VA Authorized Agency underwriting. All loans purchased fall into Nationwide’s normal Quality Assurance Review. All loans may be submitted to Nationwide for pre-purchase approval. Please refer to Pre-Approval Program for direction and fees charged. It is the responsibility of the correspondents to assure that the appraisers they use are properly licensed and qualified to appraise for the secondary market. Underwriting Fees ADMINISTRATION FEE: All purchased loans will be assessed an Administration Fee of $221.00. This fee will be netted from the funding at the time of purchase. UNDERWRITING FEE: The fees are as follows: Conventional DO: $210 (Correspondent provides loan file with DO findings) Conventional DU: $210 (Nationwide Bank runs loan application through DU) All Types of VA/FHA: $210 Appraisal Review Only $75 Appraisal Waiver: $75* Condo Approval (CPM) $75 (Delegated Lenders Only) Nationwide Bank 1 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Transcript of Section 3 – Underwriting Policies Section 3.… · Section 3 – Underwriting Policies ......

Section 3 – Underwriting Policies

Go to specific points of interest using Bookmark Links on the left

Overview General Description

This section discusses Nationwide Bank’s Underwriting Policies and Procedures. For specific product underwriting guidelines please refer to that product in Section 2 of the Seller Guide.

Underwriting Guidelines

Typically all Conventional loans are underwritten by Nationwide prior to close, unless Delegated Underwriting has been approved for the correspondent. Nationwide offers FHA underwriting as well as VA Authorized Agency underwriting. All loans purchased fall into Nationwide’s normal Quality Assurance Review. All loans may be submitted to Nationwide for pre-purchase approval. Please refer to Pre-Approval Program for direction and fees charged. It is the responsibility of the correspondents to assure that the appraisers they use are properly licensed and qualified to appraise for the secondary market.

Underwriting Fees

ADMINISTRATION FEE: All purchased loans will be assessed an Administration Fee of $221.00. This fee will be netted from the funding at the time of purchase. UNDERWRITING FEE: The fees are as follows: Conventional DO: $210 (Correspondent provides loan file with DO findings) Conventional DU: $210 (Nationwide Bank runs loan application through DU) All Types of VA/FHA: $210 Appraisal Review Only $75 Appraisal Waiver: $75* Condo Approval (CPM) $75 (Delegated Lenders Only)

Nationwide Bank 1 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Underwriting Fees (cont)

*If a file has been approved through DO/DU and granted an appraisal waiver, an appraisal waiver fee of $75 will be charged if a property appraisal is not ordered. Delegated lenders that do not have access to Fannie Mae's condo project approval system, Condo Project Manager (CPM), may submit the completed Condo Questionnaire, Budget and Master Condo Insurance Policy to Nationwide Bank Underwriting via our website for review before you underwrite the file. We will charge a $75 fee for the review. If the loan funds, the fee will be withheld (net funded) from the funding amount. If the loan cancels or is withdrawn, the lender will be billed the fee. Nationwide Bank will not charge a fee on loan applications which have been denied. Loans underwritten by Nationwide Bank that are subsequently withdrawn will be charged an underwriting fee of $210. Conventional, FHA Direct Endorsement, and VA Authorized Agency loans are to be submitted to Nationwide for underwriting prior to closing. Please put the reference number from the billing on your check and send to the attention of the Accounting Department.

Consumer Financial Protection Bureau Regulated Changes Effective Jan 2014

This section explains Nationwide Bank’s policies with the CFPBs changes effective January 2014. Nationwide Bank will not purchase any mortgage loan originated under a Small Creditor exemption. Ability to Repay (ATR) and Qualified Mortgage (QM) Standards Under the Truth in Lending Act (Regulation Z) Regulation Z currently prohibits a creditor from making a higher-priced mortgage loan without regard to the consumer’s ability to repay the loan. In January 2013, the CFPB finalized new rules implementing sections of the Dodd-Frank Act requiring creditors to make a determination of the borrower’s ability to repay a loan secured by a dwelling (with some exclusions, including HELOCs) and establishes the elements of a “Qualified Mortgage”. In addition to meeting ability to repay requirements, a Qualified Mortgage may not:

Nationwide Bank 2 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Consumer Financial Protection Bureau Regulated Changes Effective Jan 2014 (cont)

• exceed a 30 year term • may not include any unique features (i.e. balloon, teaser rates) • may not exceed a maximum DTI of 43% • points and fees may not exceed 3% of the total loan amount,

as defined by the rule. Nationwide Bank will only purchase Qualified Mortgages. Lenders must confirm that each loan satisfies the requirements of a Qualified Mortgage before closing the loan. Lenders will be required to supply a Rate Lock Agreement and complete Nationwide Bank’s Fee Itemization Form. This form will provide evidence of compliance with the elements of the ATR and QM requirements. Nationwide Bank will review this information prior to purchasing your loan to ensure the CFPB’s guidelines are met. The Fee Itemization Form and Tips for Completing the Fee Itemization Form are found on the Seller Guide Tab of the website under forms. Lenders can use one of the following approved forms in lieu of the Nationwide Bank Fee Itemization Form:

• Wells Fargo’s Fee Details Form • LoanScoreCard QM Assessment (version 4.4), Safe Harbor

results, from the Calyx origination system • Creative Visions form, which includes the Qualified Mortgage

Analysis form and the Home Ownership and Equity Protection Assessment form

• Byte Enterprise System’s CPBP Form • Encompass’ CFPB form the the Ability-to-Repay section (The

Mavent Expanded Fee Form must be provided if the Ability-to-Repay is not included

• Doc Magic CFPB Form • Compliance Eagle CFPB Form

In addition to the Fee Itemization Form, Nationwide Bank will also require Lenders to provide a completed and signed certification attesting that the loan is a Qualified Mortgage and that the disclosed points and fee calculation reflects the actual terms of the loan, including any fees paid to an affiliate of the Lender. This form is found on the Seller Guide Tab of the website under forms. High-Cost Mortgage and Homeownership Counseling Amendments to the Truth in Lending Act (Regulation Z) and Homeownership Counseling Amendments to the Real Estate Settlement Procedures Act (Regulation X)

Nationwide Bank 3 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Consumer Financial Protection Bureau Regulated Changes Effective Jan 2014 (cont)

The final rule amends Regulation Z by expanding the types of mortgage loans that are subject to the protections of the Home Ownership and Equity Protections Act (HOEPA), revises and expands the tests triggering HOEPA, and creates additional restrictions for loans covered by HOEPA. Nationwide Bank will not purchase HOEPA loans. The rule also amends Regulation Z and Regulation X implementing requirements related to homeownership counseling for all transaction. The 2013 Final Rule requires lenders to provide applicants for federally-related mortgages with a written list of HUD-approved housing counseling agencies. The following are examples of documents that Nationwide will accept for this document:

• Vendor or Lender created document which includes borrower acknowledgment and list of 10 approved housing counselors – document must be signed and dated if the form contains signature and date line.

• Printed list of 10 approved counselors provided to the borrower(s) from the CFPB’s “Find a Housing Counselor” from the CFPB link http://www.consumerfinance.gov/find-a-housing-counselor/ or from HUD’s Approved Housing Counseling Agencies link http://www.hud.gov/offices/hsg/sfh/hcc/hcs.cfm. The list must be signed and dated if a signature and date line are present on the list.

Nationwide Bank will require documentation in loan files submitted for purchase that Homeownership Counseling Disclosure was provided to the borrower. Disclosure and Delivery Requirements for Copies of Appraisals and Other Written Valuations Under the Equal Credit Opportunity Act (Regulation B The Bureau of Consumer Financial Protection (Bureau) is amending Regulation B, to implement an amendment to ECOA, concerning appraisals and other valuations, that was enacted as part of the Dodd-Frank Act. Lenders must provide applicants with free copies of all appraisals and other written valuations developed in connection with a mortgage application, no later than three days prior to closing unless the

Nationwide Bank 4 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Consumer Financial Protection Bureau Regulated Changes Effective Jan 2014 (cont)

borrower waives in writing his/her right to receive such reports within the time frame set out in the regulation.

• For loans sold to Nationwide Bank, a “valuation” would be: o The appraisal report required by DU/LP. o An estimation of value provided by DU/LP when the AUS

provides a Property Inspection Waiver (PIW) and no appraisal is to be performed.

o Any and all attachments and exhibits that are an integrated part of any form of valuation must also be provided to the borrower.

Nationwide Bank will require lenders to include a disclosure at application that indicates to the borrower that a copy of the appraisal/other written valuation will be provided to them “promptly upon completion”.

• Completion occurs when the last version is received by the lender, or when the lender has reviewed and accepted the appraisal or other written valuation to include any changes or correction required, whichever is later.

Nationwide Bank will also require an appraisal/valuation delivery acknowledgement form signed at closing. Borrowers may indicate on this acknowledgment that they have waived their right to receive the valuation report 3 or more days prior to the closing date and acknowledge that they understand they will receive a copy of the valuation report promptly upon its completion. Both the disclosure signed at application and the Appraisal/Valuation Delivery Acknowledgement are to be in the loan file when submitted for purchase.

Nationwide Bank 5 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Initial Credit Submission Packages

Initial Underwriting packages should be sent to the Nationwide Bank Underwriting Department via the Nationwide Bank website. Please do not email packages. To ensure your loan will be reviewed without delay, please complete the appropriate Credit Package Submission Form and upload the file on the Nationwide Bank website in the proper order. The forms are available on our Correspondent website under Forms on the Seller Guide Tab. Files are kept in the Underwriting Department until the closed loan package arrives in the office.

Re-Subs and Conditions

Re-subs and prior conditions must be uploaded and submitted on our website directly to the Nationwide Bank Underwriting Department.

Underwriting Decisions

After Underwriting has reached a decision on a file, (approve, deny, or incomplete), the originating Lender will receive an Underwriting Transmittal, detailing the decision in writing. Approve – Underwriting will render an “Approve” decision when the file has met Nationwide Bank and Investor guidelines. The Underwriting Transmittal may have “Closing” or “Prior to Close” conditions.

• “Closing” conditions are conditions that the Underwriter does not need to review for a clear to close but will need to be submitted to Nationwide Bank when the loan is sent to be purchased.

• "Prior to Close" conditions are issues the underwriter feels strongly may jeopardize approval of the loan. For your benefit, these conditions will be reviewed generally within 24 to 48 hours of receipt. The Lender will be notified of the Underwriter's disposition regarding these conditions with an amended Underwriting Transmittal.

• If the loan changes prior to closing, the case may need to be re-underwritten. Some items that can cause the re-underwriting of a loan can be:

o Loan amount increases or decreases. o Discount points increase. o Interest rate increases. o Loan term changes.

Nationwide Bank 6 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Underwriting Decisions (cont)

o Source of assets to close changes. o Other material change prior to close

Incomplete - Your loan will be marked as "Incomplete" if required documentation or information is not submitted. The missing information or documentation will need to be submitted before an underwriting decision may be made. (For example, a borrower is self-employed and tax returns with all schedules is not submitted with your underwriting package.) If the file is being resubmitted due to an incomplete status, no priority will be given. File will be date-stamped and subject to same turnaround time as first time submissions. Please submit all incomplete items at the same time. Denied - Your loan will be "Denied" if all documentation has been submitted with the underwriting package and the findings are not satisfied. The Underwriter may give you options to re-work the loan, if possible. (For example, the income is not sufficient and the borrower's DTI is above Nationwide Bank's allowable maximum DTI ratio. An option may be presented to the Lender to document more income in attempt to lower the DTI). A denied loan will only be re-reviewed by an Underwriter if new information or documentation has been submitted.

Desktop Originator (DO) Policies and Procedures

The purpose of this document is to help our Correspondents do business with Nationwide Bank (Nationwide Bank) using Fannie Mae’s Desktop Originator on the Web. Within this document is a discussion of our method of operating with Desktop Originator, submission procedures, Correspondent roles and responsibilities and loan delivery procedures. Also included are Nationwide Bank’s commitments related to loan delivery and loan registration that will be followed when using Desktop Originator. Nationwide Bank will use the same consistent three-in-file merged credit reports that you request at point of sale, from any of the directly connected credit information providers. Correspondent Partners that are presently a Desktop Originator Subscriber and are adding Nationwide Bank as a new lender, will need to complete the MORNETPlus Desktop Originator Lender/Originator Relationship Form. Once you have submitted your online registration to FNMA, Nationwide Bank will be contacted that you are requesting

Nationwide Bank 7 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Desktop Originator (DO) Policies and Procedures (Cont)

Sponsorship. You will receive an overnight package from FNMA with all necessary materials, as well as a User ID and Password.

Desktop Originator Workflow

Our Correspondent Partners are only authorized to access DO via our sponsorship for loans that are committed and

sold to Nationwide Bank.

1. Create an electronic casefile by inputting the borrower information into the FNMA 1003 loan application. This can be done on your LOS and imported into the Desktop Originator or it can be done on the Desktop Originator and exported to your LOS for your future tracking. Order a credit report, choosing one of your credit information providers. The information from the credit report will populate the liability section of the 1003. Reconcile liabilities with the document provided by the borrower.

2. If you have not already done so, register the loan via

Internet/phone/fax. Loans are registered according to procedures set out in the Nationwide Bank Correspondent Lending Manual. A loan number will be assigned for each case file you submit to Desktop Originator.

3. Complete the remainder of the 1003 loan application. 4. Transmit your first “Interim” submission for the underwriting

recommendation.

5. You may submit five (5) Interim submissions for the same loan. If you have already submitted the casefile five times, the sixth submission should be a final submission releasing the electronic data to Nationwide Bank. You can perform only one Final submission.

6. If you have not been successful in getting an “Approve Eligible”

status after submitting the electronic file 5 times, you should call the Nationwide Bank underwriter to discuss the circumstances surrounding the casefile. There may be alternative ways of structuring the loan that will give you an approval.

7. Review the findings report and lender conditions and process

accordingly.

8. The file must now be submitted for “Final” underwriting. All of the documentation that was required in the underwriting

Nationwide Bank 8 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Desktop Originator (DO) Policies and Procedures (Cont)

findings, including the appraisal, should be gathered prior to final submission. Print a copy of the FINAL DU Underwriting Findings and validate all of the electronic data against the paper copy of your documentation. The physical file containing that documentation must arrive in our office no more than 48 hours following a final submission. Failure to ship the physical file in a timely manner may slow down the process on your loan. Package the file according to the Submission Form located in Forms on the website.

9. Upon receipt of the hard copy file, the Nationwide Bank

underwriter checks the file for data integrity, correct documentation for all findings required and reviews the appraisal. Any additional appraisal or missing credit documentation conditions will be added at that time.

Case File Submissions Interim Submission: The Correspondent has the ability to make changes to the loan data until the credit package is submitted as a final submission. As an interim submission the file can be viewed but not changed by Nationwide Bank. Prior to sending the credit package to Nationwide Bank for review the status must be final in DO. Final Submission: A Final submission can be performed only once on each file. As soon as the Final submission is performed, ownership of the casefile is turned over to Nationwide Bank and you can no longer make data changes. In the event you find it necessary to make changes to a case file after it has been submitted for Final underwriting, you will need to request the underwriter make those changes by making a phone call to the Nationwide Bank Underwriter. The changes can be made by the underwriter without releasing the file back to you, and the casefile can be re-submitted by the underwriter for an approved recommendation. Reviewing Underwriting Findings and Casefile Conditions: Once the validation of data and underwriting of the appraisal has been completed on the casefile, the underwriter will transfer the Desktop Underwriter conditions as well as any additional conditions identified by the underwriter to the Nationwide Bank Underwriting Transmittal. All standard closing conditions apply as set forth in the Nationwide Bank Correspondent Lending Manual, along with loan specific conditions noted on your loan approval. It is your responsibility to

Nationwide Bank 9 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

make sure your loans follow Investor guidelines as well as all guidelines stated in the Nationwide Bank Correspondent Lending Manual. Case File Manager: Desktop Originator on the Web maintains a record of all your loans for up to 120 days (180 days for new construction-to-perm loans) from the last submission and provides sort and search capabilities. After that time, the casefile cannot be pulled up any longer. If the loan has not yet been submitted for final underwriting, it must be resubmitted as a new loan at additional fees to Fannie Mae and to Nationwide Bank.

Desktop Underwriter (DU) Policies and Procedures

Automated Underwriting for Conventional, FHA, and VA Loans Desktop Underwriter is an automated underwriting system created by FNMA. It provides an accurate and consistent application of the mortgage eligibility and underwriting “rules” that are in Fannie Mae’s Seller Guide, thus enabling lenders to underwrite mortgages faster and more accurately than ever before. Desktop Underwriter uses a 3-repository merged credit report; a streamlined set of data taken from the loan application for the applicant’s employment, income, and assets; a model-based evaluation of the mortgage applicant’s financial ability and willingness to pay, and a recommendation on alternative processing paths that can reduce the verification documents and appraisal fieldwork that are needed for the final approval of the mortgage. After this risk analysis is completed (within a matter of minutes), Desktop Underwriter will provide a recommendation on whether the applicant is “approved” or “referred” to the lender’s underwriter for further review. This approval assumes the information Desktop Underwriter used to reach its decision was accurate and not fraudulent (and the lender satisfies all conditions of the “approval”). The procedures for using the Desktop Underwriter are as follows:

1. Lender uploads on the website a complete application along with the borrowers signed authorization to the Nationwide

Nationwide Bank 10 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Desktop Underwriter (DU) Policies and Procedures (Cont.)

Underwriting Department. A Directory is posted on the Correspondent website. A cover sheet should accompany the upload that is directed to the Underwriter. An incomplete application will be suspended for completion.

a. FHA loans need the additional information: i. Form 92900-A, signed original should be

submitted with the file ii. Loan Estimate iii. HUD-92900-LT – complete Loan Underwriting and

Transmittal Summary b. VA loans need the additional information:

i. Form 92900-A, signed original should be submitted with the file

ii. Completed VA Loan Analysis

2. Application is input into the FNMA Desktop Underwriting system. The system will pull a credit report and perform an analysis of the information provided. Nationwide will fax a copy of the credit report to the lender with the approval only if there are discrepancies that need to be cleared up. If there is a need for an item to be updated, that will be taken care of by Nationwide when possible.

3. An initial underwriting approval will be uploaded to the website

to the lender, showing the required documentation and level of appraisal required. The approval will recommend alternative processing documents, such as pay stubs, bank statement, W-2s, to substantiate the loan. Send only the documentation required by the Desktop Underwriter. You must thoroughly review any alternative documentation submitted to make sure it satisfies conditions and is properly identified as belonging to your borrower.

4. After receipt of the initial approval, lender may order the

Uniform Residential Appraisal Report as determined by Desktop Underwriter. Other documentation as required on the approval is gathered and, along with the original application and authorization, ACCO fastened in a manila folder and forwarded to the Underwriting Department.

5. Typically, the approval will include a telephone certification by

the lender, verifying certain information from the employer. The verbal verification must state that the information was independently obtained and did not utilize the information provided on the loan application.

Nationwide Bank 11 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

6. Conditions, along with documents and the appraisal will be

reviewed and a final approval will be uploaded to the website.

Resubmissions to DU after closing: Effective immediately, Fannie Mae is establishing the following policies with regard to DU submissions:

• The same casefile ID may not be used to underwrite more than one mortgage loan with DU.

• The first submission to DU must occur before closing of the mortgage loan.

• New requirements apply when the loan casefile is resubmitted to DU after closing but prior to delivery to Fannie Mae.

• Certain requirements apply if the lender orders a new credit report after closing.

In instances when the lender is not able to access the original DU loan casefile for resubmission purposes after closing, the lender may create a new loan casefile in DU subject to certain criteria.

Disaster Area Policy

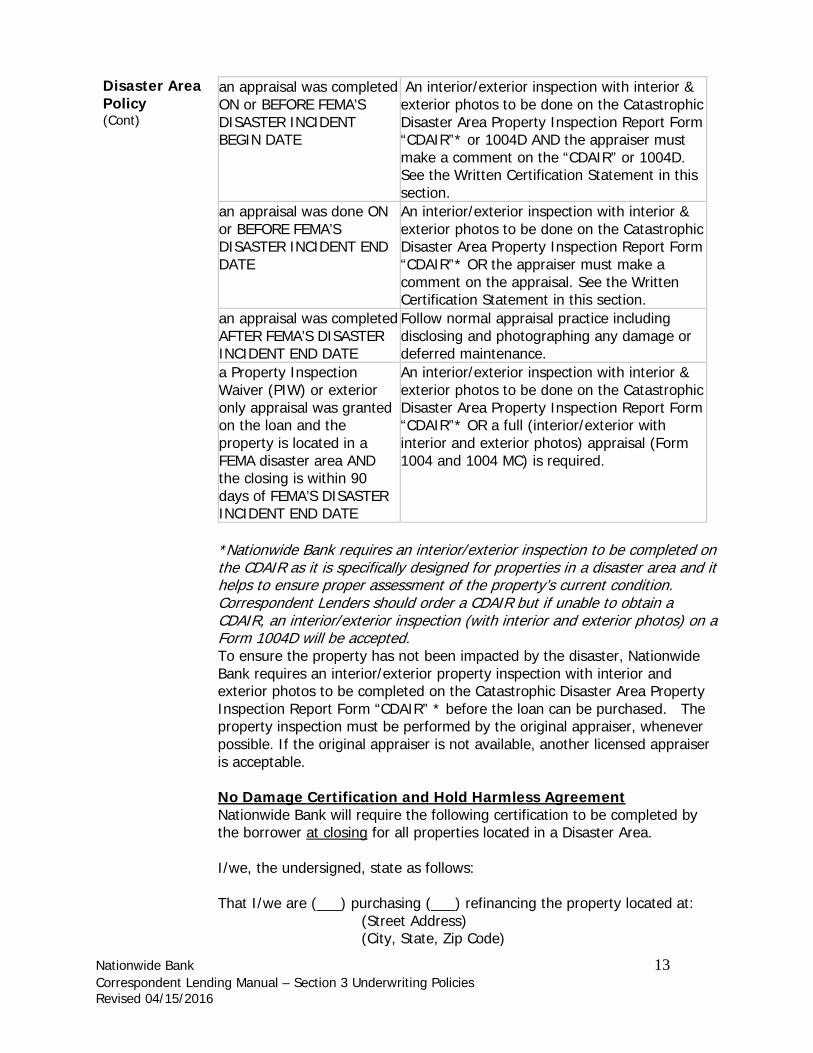

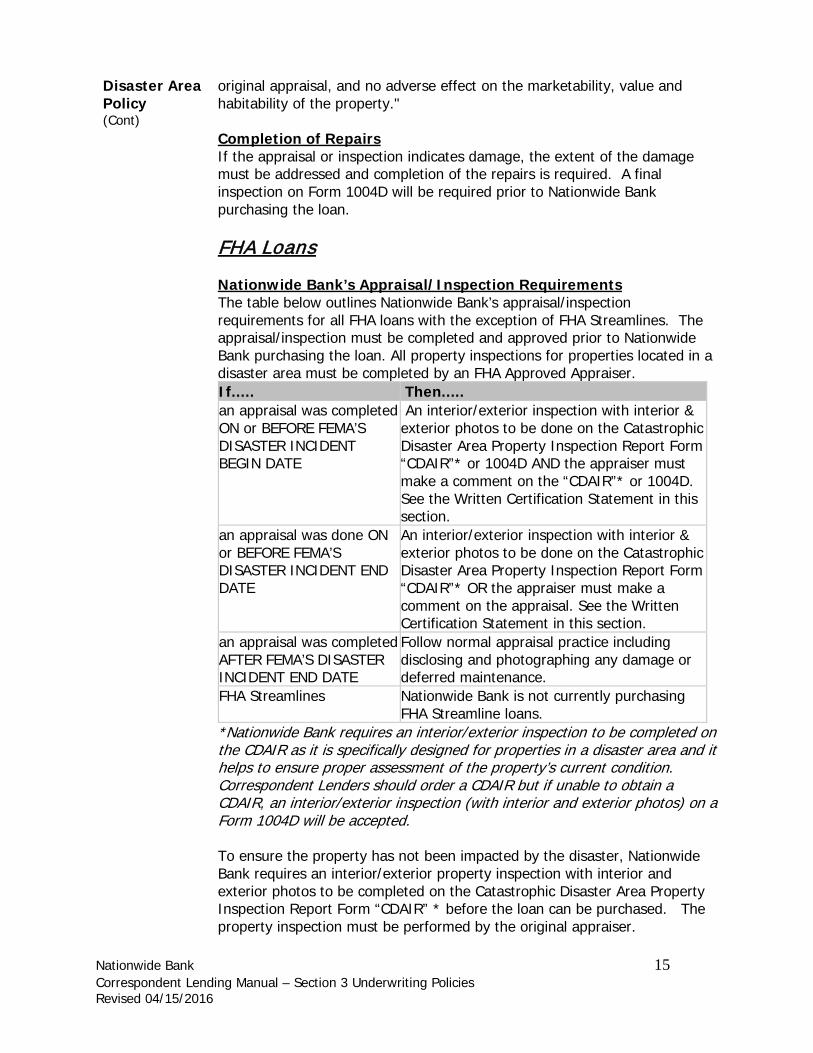

Introduction When a natural disaster occurs, the Federal Emergency Management Agency (FEMA) publishes the list of counties that have been declared eligible for federal assistance. This procedure details Nationwide Bank’s appraisal and re-inspection policies and procedures for loans secured by properties located in a declared disaster area. Seller’s Responsibilities Nationwide Bank (Nationwide Bank) requires Correspondent Lenders to initiate the re-inspection requirements outlined within this policy if the property is located in a FEMA Declared Disaster area. Nationwide Bank will suspend any loan during the purchase process that does not adhere to these requirements. Properties located in a disaster area are subject to all re-inspection requirements until Nationwide Bank advises otherwise. Areas Subject to Disaster Policy Nationwide Bank’s Disaster Area appraisal and re-inspection policy applies to areas that have been declared eligible for Individual Assistance according to FEMA. Conventional Loans Nationwide Bank’s Appraisal/Inspection Requirements The table below outlines Nationwide Bank’s appraisal/inspection requirements for all conventional loans. The appraisal/inspection must be completed and approved prior to Nationwide Bank purchasing the loan. If..... Then.....

Nationwide Bank 12 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Disaster Area Policy (Cont)

an appraisal was completed ON or BEFORE FEMA’S DISASTER INCIDENT BEGIN DATE

An interior/exterior inspection with interior & exterior photos to be done on the Catastrophic Disaster Area Property Inspection Report Form “CDAIR”* or 1004D AND the appraiser must make a comment on the “CDAIR” or 1004D. See the Written Certification Statement in this section.

an appraisal was done ON or BEFORE FEMA’S DISASTER INCIDENT END DATE

An interior/exterior inspection with interior & exterior photos to be done on the Catastrophic Disaster Area Property Inspection Report Form “CDAIR”* OR the appraiser must make a comment on the appraisal. See the Written Certification Statement in this section.

an appraisal was completed AFTER FEMA’S DISASTER INCIDENT END DATE

Follow normal appraisal practice including disclosing and photographing any damage or deferred maintenance.

a Property Inspection Waiver (PIW) or exterior only appraisal was granted on the loan and the property is located in a FEMA disaster area AND the closing is within 90 days of FEMA’S DISASTER INCIDENT END DATE

An interior/exterior inspection with interior & exterior photos to be done on the Catastrophic Disaster Area Property Inspection Report Form “CDAIR”* OR a full (interior/exterior with interior and exterior photos) appraisal (Form 1004 and 1004 MC) is required.

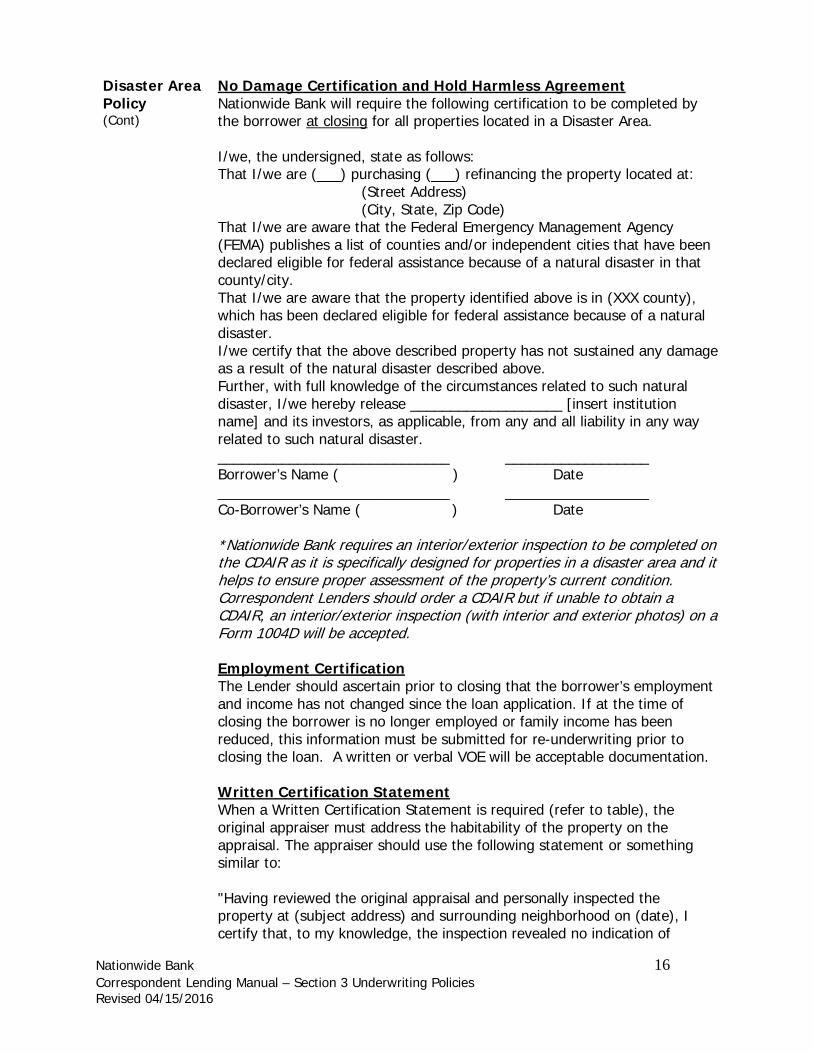

*Nationwide Bank requires an interior/exterior inspection to be completed on the CDAIR as it is specifically designed for properties in a disaster area and it helps to ensure proper assessment of the property’s current condition. Correspondent Lenders should order a CDAIR but if unable to obtain a CDAIR, an interior/exterior inspection (with interior and exterior photos) on a Form 1004D will be accepted. To ensure the property has not been impacted by the disaster, Nationwide Bank requires an interior/exterior property inspection with interior and exterior photos to be completed on the Catastrophic Disaster Area Property Inspection Report Form “CDAIR” * before the loan can be purchased. The property inspection must be performed by the original appraiser, whenever possible. If the original appraiser is not available, another licensed appraiser is acceptable. No Damage Certification and Hold Harmless Agreement Nationwide Bank will require the following certification to be completed by the borrower at closing for all properties located in a Disaster Area. I/we, the undersigned, state as follows: That I/we are (___) purchasing (___) refinancing the property located at: (Street Address) (City, State, Zip Code)

Nationwide Bank 13 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Disaster Area Policy (Cont)

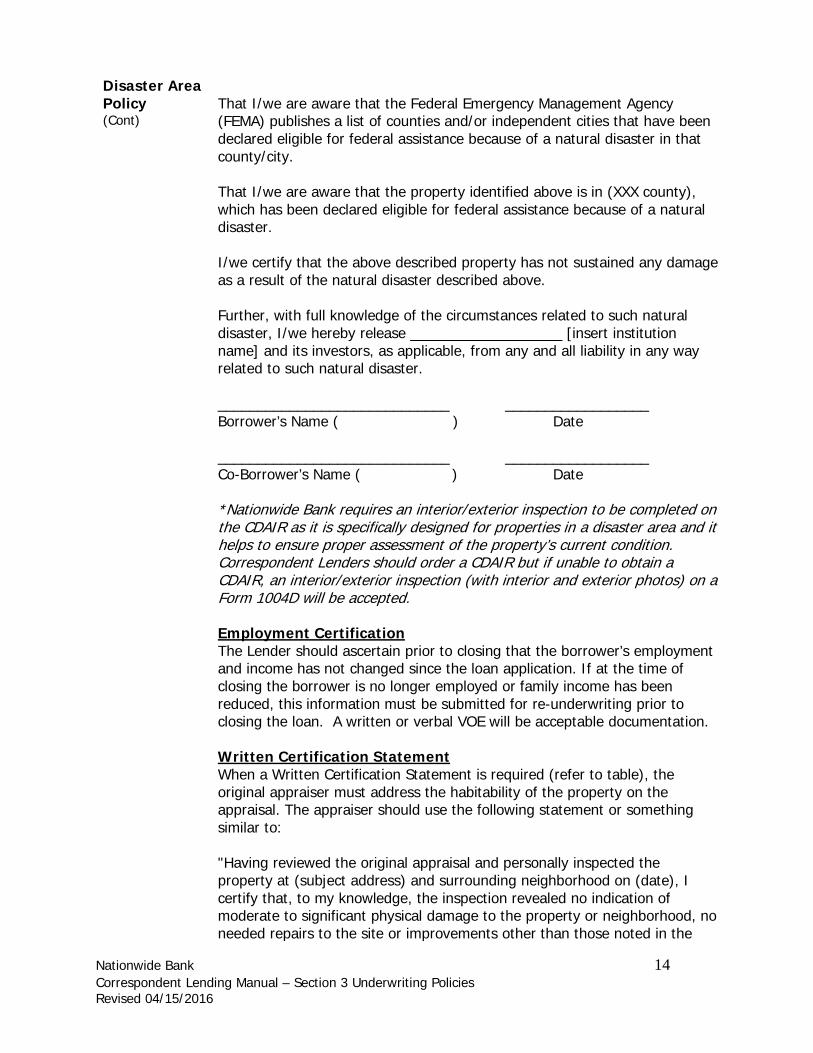

That I/we are aware that the Federal Emergency Management Agency (FEMA) publishes a list of counties and/or independent cities that have been declared eligible for federal assistance because of a natural disaster in that county/city. That I/we are aware that the property identified above is in (XXX county), which has been declared eligible for federal assistance because of a natural disaster. I/we certify that the above described property has not sustained any damage as a result of the natural disaster described above. Further, with full knowledge of the circumstances related to such natural disaster, I/we hereby release ___________________ [insert institution name] and its investors, as applicable, from any and all liability in any way related to such natural disaster. _____________________________ __________________ Borrower’s Name ( ) Date _____________________________ __________________ Co-Borrower’s Name ( ) Date *Nationwide Bank requires an interior/exterior inspection to be completed on the CDAIR as it is specifically designed for properties in a disaster area and it helps to ensure proper assessment of the property’s current condition. Correspondent Lenders should order a CDAIR but if unable to obtain a CDAIR, an interior/exterior inspection (with interior and exterior photos) on a Form 1004D will be accepted. Employment Certification The Lender should ascertain prior to closing that the borrower’s employment and income has not changed since the loan application. If at the time of closing the borrower is no longer employed or family income has been reduced, this information must be submitted for re-underwriting prior to closing the loan. A written or verbal VOE will be acceptable documentation. Written Certification Statement When a Written Certification Statement is required (refer to table), the original appraiser must address the habitability of the property on the appraisal. The appraiser should use the following statement or something similar to: "Having reviewed the original appraisal and personally inspected the property at (subject address) and surrounding neighborhood on (date), I certify that, to my knowledge, the inspection revealed no indication of moderate to significant physical damage to the property or neighborhood, no needed repairs to the site or improvements other than those noted in the

Nationwide Bank 14 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

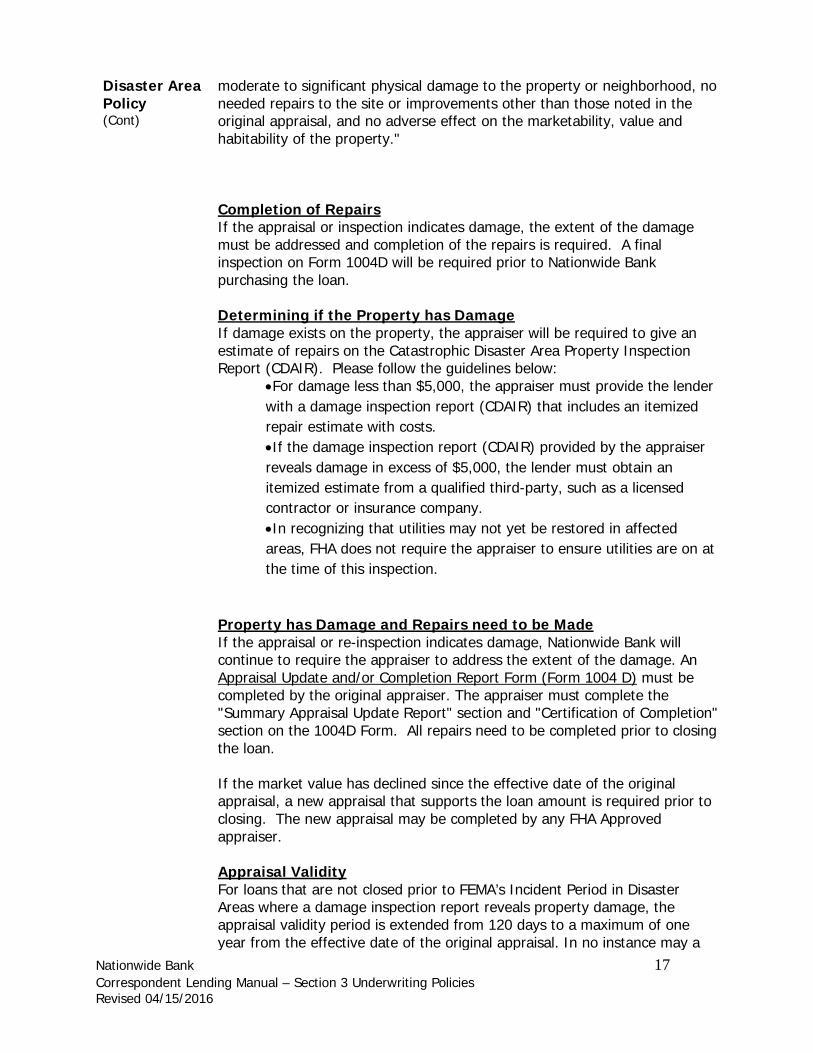

Disaster Area Policy (Cont)

original appraisal, and no adverse effect on the marketability, value and habitability of the property." Completion of Repairs If the appraisal or inspection indicates damage, the extent of the damage must be addressed and completion of the repairs is required. A final inspection on Form 1004D will be required prior to Nationwide Bank purchasing the loan. FHA Loans Nationwide Bank’s Appraisal/Inspection Requirements The table below outlines Nationwide Bank’s appraisal/inspection requirements for all FHA loans with the exception of FHA Streamlines. The appraisal/inspection must be completed and approved prior to Nationwide Bank purchasing the loan. All property inspections for properties located in a disaster area must be completed by an FHA Approved Appraiser. If..... Then..... an appraisal was completed ON or BEFORE FEMA’S DISASTER INCIDENT BEGIN DATE

An interior/exterior inspection with interior & exterior photos to be done on the Catastrophic Disaster Area Property Inspection Report Form “CDAIR”* or 1004D AND the appraiser must make a comment on the “CDAIR”* or 1004D. See the Written Certification Statement in this section.

an appraisal was done ON or BEFORE FEMA’S DISASTER INCIDENT END DATE

An interior/exterior inspection with interior & exterior photos to be done on the Catastrophic Disaster Area Property Inspection Report Form “CDAIR”* OR the appraiser must make a comment on the appraisal. See the Written Certification Statement in this section.

an appraisal was completed AFTER FEMA’S DISASTER INCIDENT END DATE

Follow normal appraisal practice including disclosing and photographing any damage or deferred maintenance.

FHA Streamlines Nationwide Bank is not currently purchasing FHA Streamline loans.

*Nationwide Bank requires an interior/exterior inspection to be completed on the CDAIR as it is specifically designed for properties in a disaster area and it helps to ensure proper assessment of the property’s current condition. Correspondent Lenders should order a CDAIR but if unable to obtain a CDAIR, an interior/exterior inspection (with interior and exterior photos) on a Form 1004D will be accepted. To ensure the property has not been impacted by the disaster, Nationwide Bank requires an interior/exterior property inspection with interior and exterior photos to be completed on the Catastrophic Disaster Area Property Inspection Report Form “CDAIR” * before the loan can be purchased. The property inspection must be performed by the original appraiser.

Nationwide Bank 15 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Disaster Area Policy (Cont)

No Damage Certification and Hold Harmless Agreement Nationwide Bank will require the following certification to be completed by the borrower at closing for all properties located in a Disaster Area. I/we, the undersigned, state as follows: That I/we are (___) purchasing (___) refinancing the property located at: (Street Address) (City, State, Zip Code) That I/we are aware that the Federal Emergency Management Agency (FEMA) publishes a list of counties and/or independent cities that have been declared eligible for federal assistance because of a natural disaster in that county/city. That I/we are aware that the property identified above is in (XXX county), which has been declared eligible for federal assistance because of a natural disaster. I/we certify that the above described property has not sustained any damage as a result of the natural disaster described above. Further, with full knowledge of the circumstances related to such natural disaster, I/we hereby release ___________________ [insert institution name] and its investors, as applicable, from any and all liability in any way related to such natural disaster. _____________________________ __________________ Borrower’s Name ( ) Date _____________________________ __________________ Co-Borrower’s Name ( ) Date *Nationwide Bank requires an interior/exterior inspection to be completed on the CDAIR as it is specifically designed for properties in a disaster area and it helps to ensure proper assessment of the property’s current condition. Correspondent Lenders should order a CDAIR but if unable to obtain a CDAIR, an interior/exterior inspection (with interior and exterior photos) on a Form 1004D will be accepted. Employment Certification The Lender should ascertain prior to closing that the borrower’s employment and income has not changed since the loan application. If at the time of closing the borrower is no longer employed or family income has been reduced, this information must be submitted for re-underwriting prior to closing the loan. A written or verbal VOE will be acceptable documentation. Written Certification Statement When a Written Certification Statement is required (refer to table), the original appraiser must address the habitability of the property on the appraisal. The appraiser should use the following statement or something similar to: "Having reviewed the original appraisal and personally inspected the property at (subject address) and surrounding neighborhood on (date), I certify that, to my knowledge, the inspection revealed no indication of

Nationwide Bank 16 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Disaster Area Policy (Cont)

moderate to significant physical damage to the property or neighborhood, no needed repairs to the site or improvements other than those noted in the original appraisal, and no adverse effect on the marketability, value and habitability of the property." Completion of Repairs If the appraisal or inspection indicates damage, the extent of the damage must be addressed and completion of the repairs is required. A final inspection on Form 1004D will be required prior to Nationwide Bank purchasing the loan. Determining if the Property has Damage If damage exists on the property, the appraiser will be required to give an estimate of repairs on the Catastrophic Disaster Area Property Inspection Report (CDAIR). Please follow the guidelines below:

•For damage less than $5,000, the appraiser must provide the lender with a damage inspection report (CDAIR) that includes an itemized repair estimate with costs. •If the damage inspection report (CDAIR) provided by the appraiser reveals damage in excess of $5,000, the lender must obtain an itemized estimate from a qualified third-party, such as a licensed contractor or insurance company. •In recognizing that utilities may not yet be restored in affected areas, FHA does not require the appraiser to ensure utilities are on at the time of this inspection.

Property has Damage and Repairs need to be Made If the appraisal or re-inspection indicates damage, Nationwide Bank will continue to require the appraiser to address the extent of the damage. An Appraisal Update and/or Completion Report Form (Form 1004 D) must be completed by the original appraiser. The appraiser must complete the "Summary Appraisal Update Report" section and "Certification of Completion" section on the 1004D Form. All repairs need to be completed prior to closing the loan. If the market value has declined since the effective date of the original appraisal, a new appraisal that supports the loan amount is required prior to closing. The new appraisal may be completed by any FHA Approved appraiser. Appraisal Validity For loans that are not closed prior to FEMA’s Incident Period in Disaster Areas where a damage inspection report reveals property damage, the appraisal validity period is extended from 120 days to a maximum of one year from the effective date of the original appraisal. In no instance may a

Nationwide Bank 17 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

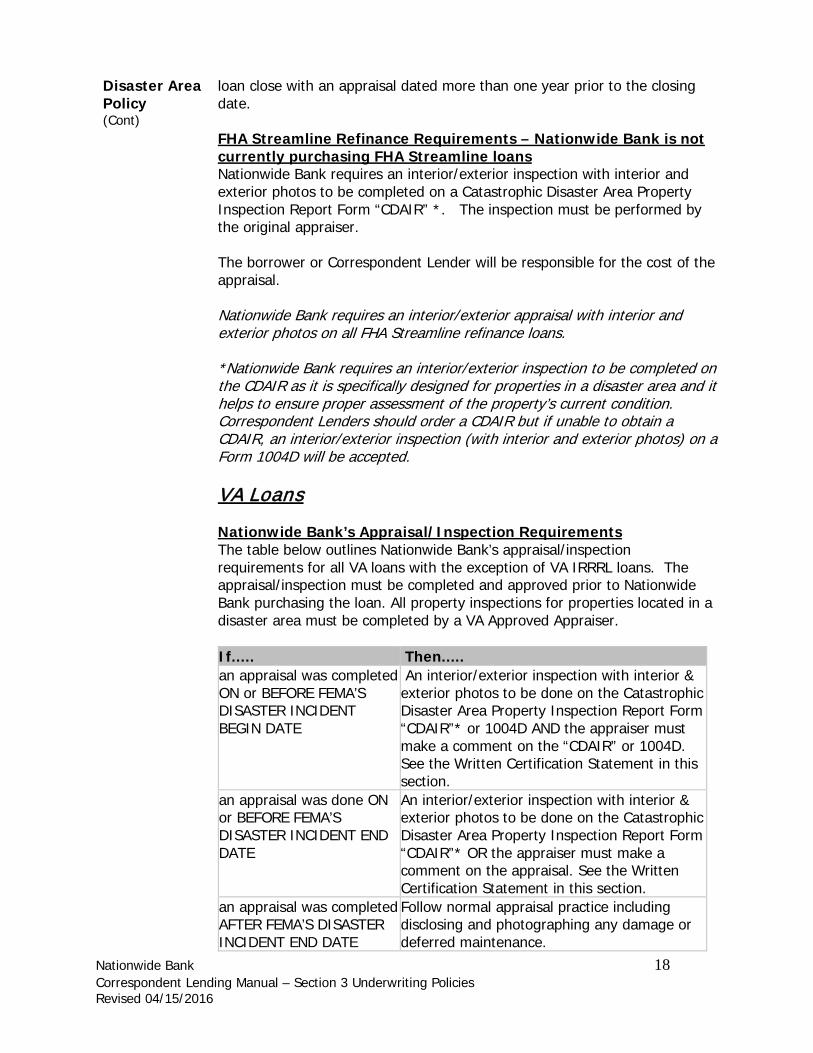

Disaster Area Policy (Cont)

loan close with an appraisal dated more than one year prior to the closing date. FHA Streamline Refinance Requirements – Nationwide Bank is not currently purchasing FHA Streamline loans Nationwide Bank requires an interior/exterior inspection with interior and exterior photos to be completed on a Catastrophic Disaster Area Property Inspection Report Form “CDAIR” *. The inspection must be performed by the original appraiser. The borrower or Correspondent Lender will be responsible for the cost of the appraisal. Nationwide Bank requires an interior/exterior appraisal with interior and exterior photos on all FHA Streamline refinance loans. *Nationwide Bank requires an interior/exterior inspection to be completed on the CDAIR as it is specifically designed for properties in a disaster area and it helps to ensure proper assessment of the property’s current condition. Correspondent Lenders should order a CDAIR but if unable to obtain a CDAIR, an interior/exterior inspection (with interior and exterior photos) on a Form 1004D will be accepted. VA Loans Nationwide Bank’s Appraisal/Inspection Requirements The table below outlines Nationwide Bank’s appraisal/inspection requirements for all VA loans with the exception of VA IRRRL loans. The appraisal/inspection must be completed and approved prior to Nationwide Bank purchasing the loan. All property inspections for properties located in a disaster area must be completed by a VA Approved Appraiser. If..... Then..... an appraisal was completed ON or BEFORE FEMA’S DISASTER INCIDENT BEGIN DATE

An interior/exterior inspection with interior & exterior photos to be done on the Catastrophic Disaster Area Property Inspection Report Form “CDAIR”* or 1004D AND the appraiser must make a comment on the “CDAIR” or 1004D. See the Written Certification Statement in this section.

an appraisal was done ON or BEFORE FEMA’S DISASTER INCIDENT END DATE

An interior/exterior inspection with interior & exterior photos to be done on the Catastrophic Disaster Area Property Inspection Report Form “CDAIR”* OR the appraiser must make a comment on the appraisal. See the Written Certification Statement in this section.

an appraisal was completed AFTER FEMA’S DISASTER INCIDENT END DATE

Follow normal appraisal practice including disclosing and photographing any damage or deferred maintenance.

Nationwide Bank 18 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Disaster Area Policy (Cont)

VA IRRRL – If the property is located in a FEMA disaster area and the closing is within 90 days of FEMA’s DISASTER INCIDENT END DATE

An interior/exterior inspection with interior & exterior photos to be done on the Catastrophic Disaster Area Property Inspection Report Form “CDAIR”*. Refer to page 11 for IRRRL information.

*Nationwide Bank requires an interior/exterior inspection to be completed on the CDAIR as it is specifically designed for properties in a disaster area and it helps to ensure proper assessment of the property’s current condition. Correspondent Lenders should order a CDAIR but if unable to obtain a CDAIR, an interior/exterior inspection (with interior and exterior photos) on a Form 1004D will be accepted. Loan Origination Issues a. Loan Closed Prior to Disaster - Any loan closed prior to FEMA’s Incident Begin Date is eligible for VA Guaranty without regard to the disaster. b. Property Appraised Prior to Disaster - To be eligible for VA Guaranty, a loan with a property appraised on or before, but not closed prior to FEMA’s Incident End Date must meet the following requirements: 1) Certifications - Nationwide Bank will require the following certifications

to be completed before the loan can be purchased. Written Certification Statement When a Written Certification Statement is required (refer to table), the original appraiser must address the habitability of the property on the appraisal. The appraiser should use the following statement or something similar to: "Having reviewed the original appraisal and personally inspected the property at (subject address) and surrounding neighborhood on (date), I certify that, to my knowledge, the inspection revealed no indication of moderate to significant physical damage to the property or neighborhood, no needed repairs to the site or improvements other than those noted in the original appraisal, and no adverse effect on the marketability, value and habitability of the property." Lender Certification An interior/exterior inspection with interior and exterior photos on a Catastrophic Disaster Area Property Inspection Report Form “CDAIR” * will be required to be submitted with the loan package. The appraiser should use the following written certification statement or something similar to it. *Nationwide Bank requires an interior/exterior inspection to be completed on the CDAIR as it is specifically designed for properties in a disaster area and it helps to ensure proper assessment of the property’s current condition.

Nationwide Bank 19 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Disaster Area Policy (Cont)

Correspondent Lenders should order a CDAIR but if unable to obtain a CDAIR, an interior/exterior inspection (with interior and exterior photos) on a Form 1004D will be accepted. An underwriter will review the inspection and complete the Lender Certification as shown below if approved. This is to affirm that the property which is security for VA Loan number ______________ has been inspected to ensure that it was either not damaged in the recently declared disaster or has been restored to its pre-disaster condition or better. ________________ _______________________________ Lender Signature Lender Title Date Completion of Repairs If repairs need to be made, a final inspection must be completed on Form 1004D by a VA approved appraiser. An underwriter must review and approve the final inspection and Veteran Certification prior to purchase. Veteran Certification The following certification needs to be completed by the Veteran for a purchase transaction. The seller will be responsible for the inspection costs. I have inspected the property located at __________________________ and find its condition now to be acceptable to me. I understand that I will not be charged for any disaster-related expenses and now wish to close the loan. _________________ ____________________ Veteran Signature Date No Damage Certification and Hold Harmless Agreement Nationwide Bank recommends the following certification to be completed by the Veteran at closing for all properties located in a Disaster Area. I/we, the undersigned, state as follows: That I/we are (___) purchasing (___) refinancing the property located at: (Street Address) (City, State, Zip Code) That I/we are aware that the Federal Emergency Management Agency (FEMA) publishes a list of counties and/or independent cities that have been declared eligible for federal assistance because of a natural disaster in that county/city. That I/we are aware that the property identified above is in (XXX county), which has been declared eligible for federal assistance because of a natural disaster. I/we certify that the above described property has not sustained any damage as a result of the natural disaster described above.

Nationwide Bank 20 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Disaster Area Policy (Cont)

Further, with full knowledge of the circumstances related to such natural disaster, I/we hereby release ___________________ [insert institution name] and its investors, as applicable, from any and all liability in any way related to such natural disaster. _____________________________ __________________ Borrower’s Name ( ) Date _____________________________ __________________ Co-Borrower’s Name ( ) Date 2) VA Loan Summary Sheet - The “Remarks” section of VA Form 26-0286, VA Loan Summary Sheet must be annotated “Lender and Veteran Disaster Certifications Enclosed.” Additionally, if local law requires the property to be inspected and approved by the local building inspection authority, a copy of the appropriate local report(s) must be provided. Neither VA nor the veteran purchaser shall bear the expense of any disaster-related inspection or repairs. 3) Decline in Value - If there is an indication that the property, despite repairs, will be worth less at the time of loan closing than it was at the time of appraisal, the lender must have the VA-approved appraiser update the original value estimate. The payment of the appraiser’s fee for that service will be the responsibility of the borrower on a refinance and will be a contractual matter between the buyer and seller on a purchase. If the property value has decreased, the loan amount must be reduced accordingly. 4) Employment/Income Certification - The Lender should ascertain no sooner than 3 days prior to closing that the veteran’s employment and income have not changed since the loan application. If at the time of closing the veteran is no longer employed or family income has been reduced, this information should be reported to VA or the underwriter, as appropriate, for evaluation prior to closing the loan. A written or verbal VOE will be acceptable documentation. VA Interest Rate Reduction Refinancing Loans (IRRRLs) To ensure the property has not been impacted by the disaster, Nationwide Bank requires an interior/exterior inspection with interior and exterior photos to be completed on the Catastrophic Disaster Area Property Inspection Report Form “CDAIR” *. The CDAIR does not need to be completed by a VA-Approved Appraiser. The Correspondent Lender will be responsible for the cost of the appraisal. *Nationwide Bank requires an interior/exterior inspection to be completed on the CDAIR as it is specifically designed for properties in a disaster area and it helps to ensure proper assessment of the property’s current condition. Correspondent Lenders should order a CDAIR but if unable to obtain a

Nationwide Bank 21 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

CDAIR, an interior/exterior inspection (with interior and exterior photos) on a Form 1004D will be accepted.

Pre-Approvals

Nationwide offers credit approval for certain loans. It may be used for all conventional loans as well as FHA or VA loans for which Nationwide is performing the underwriting under the Direct Endorsement or Authorized Agency programs. A full credit package may be submitted for credit approval, followed by submission of an appraisal with a signed Offer to Purchase. Fees will be net funded for loans that are purchased by Nationwide Bank or billed for loans that are not purchased. Billing will take place shortly after the first of the month following underwriting. Following are the instructions for requesting pre-approval:

o Make sure the borrower has decided on a program and an approximate mortgage amount. Underwriting will be unable to perform a credit approval if any of these issues are unclear.

o The loan must be registered with the reservation desk, and

assigned a loan number prior to submitting the file to underwriting. If there is no property, no rate or points will be locked and no expiration date will be given. This is considered a float status. The same loan number should be used for the loan when locking the rate and points. Please specify that you have a loan at float that you would like to lock in. If a property has been chosen, the rate and points may be locked at registration or may be registered at float.

o Process the loan according to the appropriate guidelines. All

credit documents should be complete and verified prior to submission. Include all disclosures, RESPA notices, etc. in the credit package.

o Submit all original credit documents (according to the

transmittal you typically use) for approval before the borrower obtains a purchase agreement and appraisal. Underwriting cannot give a credit approval if any of the credit information is unverified or omitted.

Contact Correspondent Lending or Underwriting with any questions.

Nationwide Bank 22 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Prepurchase Review Process (Delegated Lenders)

Nationwide Bank conducts a pre-purchase review on a 10% sampling of all loans submitted by delegated lenders to validate compliance with investor guidelines, to mitigate material defects and to ensure underwriting quality, as well as credit quality. We run all loans through a risk mitigation/fraud detection tool as part of this review. The On Hold Report is provided to the lender for any loan with issues that prevent its purchase. If a lender disagrees with the file review conclusions the lender may submit a Rebuttal Form for reconsideration. It is important to use the Rebuttal Process for reconsideration for an expedited response and to assure the lender’s pre-purchase review results (used to monitor quality) reflect successfully rebutted findings. We will review and respond within 48 hours of receipt of the rebuttal. The Hold Dispute Form is attached with this memo and also found on the Correspondent website under Forms on the Seller Guide Tab. An Underwriting Audits for Delegated Lender Report is also shared periodically with the lender; this report identifies critical, training and unsalable issues and should be used by the lender to identify trends in errors and root causes, such as training, performance, processes or systems. If the 10% sampling file review results are not satisfactory (generally, more than 2 of 10 consecutive loan reviews result in findings), the Nationwide Bank Account Executive will work with the lender on a plan to improve file quality and an increased number of files (up to 100%) will be reviewed pre-purchase. Pre-purchase review results for the subsequent month will be monitored and if the review results improve to a level at which Nationwide Bank feels adequate the lender will be returned to a normal 10% sample review. If upon the review of the subsequent month’s pre-purchase review results, due to the frequency and/or severity of the issues discovered, Nationwide Bank determines it necessary to continue with an increased level of pre-purchase file reviews, you will be notified by your account executive that $200 will be charged for each file reviewed, effective immediately. Nationwide Bank will continue to review monthly results of pre-purchase reviews and assess the frequency and severity of issues that

Nationwide Bank 23 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Prepurchase Review Process (Delegated Lenders) (Cont)

prevent purchase of the loans. When the lender has documented the measures taken to improve deficiencies and has achieved a satisfactory result on at least 8 of 10 consecutive loan reviews the $200 charge will be removed, effective immediately; Nationwide Bank, at its discretion, may continue with an increased level of pre-purchase reviews but without additional charge to the lender. Nationwide Bank will continue to monitor results. If quality subsequently deteriorates the $200 charge will be immediately reinstated. The Pre-Purchase Review is solely for the purpose of quality control; as such, this review does not waive the lender’s responsibilities on any loan reviewed or on any other loan delivered to Nationwide Bank and all representations and warrants under the Correspondent Lending Agreement will apply regardless of any outcome of any Pre-Purchase Review.

Uniform Mortgage Data Program

The Uniform Mortgage Data Program (UMDP) includes the following three components: Uniform Appraisal Dataset, Uniform Loan Data Delivery and Uniform Collateral Data Portal. Below is an explanation and Nationwide Bank requirements for each. Uniform Appraisal Dataset (UAD) Nationwide Bank requires all applicable conventional appraisals to comply with the Uniform Appraisal Dataset (UAD) to be eligible for purchase. Fannie Mae and Freddie Mac have announced their property eligibility and appraisal requirements resulting from the UAD Condition and Quality of Construction Ratings. Outlined below are additional agency and Nationwide Bank-specific (in bold face) requirements regarding UAD. UAD Condition and Quality of Construction Ratings All applicable appraisal report forms must be completed using the UAD standards, and must incorporate the UAD Condition and Quality of Construction Ratings that best describes the overall condition of the subject property. Correspondent Lenders should refer to the UAD Field-Specific Standardization Requirements for the definitions for each of the Condition and Quality of Construction Ratings. Correspondent Lenders must ensure all conventional loans submitted for purchase comply with all Nationwide Bank and Agency property eligibility requirements. Regardless of Condition or Quality of Construction Ratings, as before, properties which are not deemed to be safe, habitable or in structurally sound condition are not eligible for purchase.

Nationwide Bank 24 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Uniform Mortgage Data Program (Cont)

Appraisal Expectations based on Agency and Nationwide Bank UAD appraisal requirements:

•The appraisal report must identify and describe physical deficiencies that could affect a property’s safety, soundness, or structural integrity. If the appraiser has identified any of these deficiencies, the property must be appraised subject to completion of the specific repairs or alterations. In these instances, the property Condition and Quality of Construction Ratings must reflect the condition and quality of the property based on the hypothetical condition that the repairs or alterations have been completed. •The appraisal report must contain an accurate description of the improvements and any factors that may affect the market value of marketability of the subject property. •In order to obtain fungible, investment quality loans, properties with Condition Ratings of C5 or C6 are not eligible for delivery to Nationwide Bank in ‘as is’ condition; all deficiencies that caused the rating and/or hypothetical condition must be completed prior to loan purchase. •Correspondent Lenders must provide an Appraisal Update and/or Completion Report (Fannie Mae Form 1004D/Freddie Mac Form 442) in the underwriting package if Non-delegated Lender or closed loan file if a Delegated Lender to evidence satisfactory completion of repairs, when applicable. •Nationwide Bank will purchase mortgage loans secured by properties with a quality of construction rating of Q6 provided any items in relation to the quality of construction that impact the safety, soundness, or structural integrity of the property are repaired prior to the delivery of the mortgage loan to Nationwide Bank. (Note: The final submission to the UCDP should include the property condition and quality of construction ratings after any necessary repairs are made.)

Uniform Loan Delivery Dataset (ULDD) The ULDD includes all of the loan data points that will be required at loan delivery. Lenders must collect the new ULDD data points required for the first phase of implementation, as well as the UAD standardized appraisal data for new loan applications.

•Currently, when reserving loans, lenders enter an Application Date on the website. ULDD requires the Application Date to be the date of the initial application. We recommend you review your procedures to assure you are entering this date correctly.

Uniform Collateral Data Portal (UCDP) Fannie Mae and Freddie Mac have developed the Uniform Collateral Data Portal (UCDP), a single portal for the electronic submission of

Nationwide Bank 25 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Uniform Mortgage Data Program (Cont)

appraisal data files. Lenders will be required to use UCDP to submit electronic appraisal data files that conform to all GSE requirements, including Uniform Appraisal Dataset (UAD) when applicable before Nationwide Bank will purchase the loan. Below is more information on UCDP and Nationwide Bank-specific (in bold face) requirements.

•Correspondent Lenders are required to upload conventional appraisals to both GSE's through UCDP and must resolve any edit issues prior to sending the underwriting package to Underwriting or closed loan file for purchase. A Submission Summary Report (SSR) for each GSE must be submitted with the appraisal to Nationwide Bank.

UCDP Access The UCDP provides a common pathway for the electronic submission of appraisal data files to the GSEs. Correspondent Lenders and/or their lender agents must submit the appraisal to both GSEs (Fannie Mae and Freddie Mac) when selling loans to Nationwide Bank. A "Lender Agent" is an entity that a correspondent lender authorizes to perform functions within the UCDP, such as uploading appraisals and evaluating results on their behalf. Correspondent Lenders and their lender agents may access the UCDP through:

•An easy-to-use Web-based interface that allows users to browse and upload XML or Portable Document Format (PDF) files to the portal. Lenders should evaluate their processes and requirements and should request that appraisers send them the appraisal file in XML format, in addition to obtaining the appraisal in a PDF format as necessary. •Vendor-provided solutions that offer an integrated system interface to the UCDP. Both GSEs have published a list of technology vendors who plan to provide a vendor solution that offers an integrated system interface to the UCDP. If you are interested in having an interface to UCDP from your loan origination system, please review the vendor lists on both GSEs' websites.

Fannie Mae - https://www.efanniemae.com/sf/technology/commitloandel/ucdp/pdf/ucdpvendorlist.pdf Freddie Mac - http://www.freddiemac.com/sell/secmktg/ucdp_vendors.html UCDP Formats

Nationwide Bank 26 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Uniform Mortgage Data Program (Cont)

Either an XML data stream (output from appraisal forms software) with an embedded first-generation .PDF file or first-generation PDF file without the corresponding XML data must be submitted to the UCDP. The following list includes the XML formats that will be supported in the UCDP for the UAD appraisal forms: •MISMO 2.6 Errata 1 GSE Extended form (preferred format) •ACI format •AI Ready format All XML files must include an embedded PDF file that includes all appraisal exhibits, addenda, photographs, and the Market Conditions Addendum to the Appraisal Report. Appraisal software and loan origination system (LOS) vendors directly integrating to the UCDP are working to provide solutions that offer one or more of the UCDP-supported XML file formats. You can save time, reduce potential cost, and increase data reliability by obtaining the XML file from the appraiser for submission to UCDP. Note: The XML format will contain the full PDF as an embedded data point within the XML file. Please work with your appraiser or AMC to ensure they have the appropriate software to meet the UCDP XML format requirements. •If the electronic data is not available, a first-generation .PDF can be converted to an acceptable XML format, however, there are multiple considerations including a per conversion fee and significantly increased time for the actual conversion to occur. •In the future, only electronic appraisal data will be accepted (i.e. .PDF will no longer be accepted). UCDP Functionality Users can submit electronic appraisal data files, receive status and findings, correct and modify appraisal file submissions, and request overrides in the event an appraisal is not accepted by the UCDP. Appraisals that are submitted to the UCDP go through a series of checks, including a UAD Compliance Check. Appraisals that pass all checks receive a "Successful" status from the UCDP. Initially, the UAD Compliance Check results in warning messages only and does not affect the successful submission of appraisals to the UCDP. In the future, the UAD Compliance Check may result in errors that require appraisals to be corrected by the appraiser and re-submitted to the UCDP. For some appraisal submission errors, the user may request an exception or override in the system when the lender believes the submitted data is correct. All appraisals successfully uploaded to the UCDP receive a Submission Summary Report (SSR) for each GSE submission. The SSR contains a summary of the appraisal submission(s) for each loan, the status of

Nationwide Bank 27 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

Uniform Mortgage Data Program (Cont)

the submission(s) and a Document File Identifier (Doc File ID), which is the unique appraisal identifier generated by the UCDP. One Doc File ID is assigned per loan and is the same for delivery to either GSE. The appraisal must be submitted to the UCDP and receive a "Successful" status on the SSR for each GSE before the loan can be submitted to Nationwide Bank. •UCDP supports up to three appraisals per loan. •If a file submission is not accepted, a Doc File ID will not be generated. •Lenders will need to develop processes and system controls to ensure that a "Successful" status is received on each GSE's SSR before submitting to Nationwide Bank. Registering for UCDP In order to use UCDP, each Correspondent Lender must set up an account profile. The steps below outline the process for completing the registration process for portal access and each organization's set up within the UCDP for both GSEs: I. Designate a Primary Lender Administrator: Designate an

individual to serve as primary lender administrator (lender admin). The primary lender admin and any additional lender admins are the only individuals who will be registering directly with both GSEs. The lender admin is responsible for:

•Establishing access to the UCDP for the lender, confirming a relationship to both GSEs, setting up their organization's profile, and adding additional users. •Initiating the setup of other lender administrators in the organization for the ongoing maintenance of UCDP access. •Authorizing lender agents to submit appraisals on behalf of their organization to the UCDP.

II. Register with each GSE: Complete each GSE's unique registration process for lender admin(s) using the appropriate forms on each GSE's website. Refer to links below for each GSE's registration process.

III. Register Lender Agents: Determine if your organization will work with a lender agent. Lender agents are third-party entities (such as Appraisal Management Companies (AMC) or Outsource Providers) that can upload appraisals on the Correspondent lender's behalf to the UCDP. If a Correspondent lender chooses to work with a lender agent, the lender agent must complete the UCDP lender agent registration process to request a UCDP account and to appear on the lender agent list in the UCDP. The lender agent list allows lenders to identify

Nationwide Bank 28 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016

and authorize lender agents to upload appraisals to UCDP on their behalf.

Fannie Mae – https://www.efanniemae.com/sf/technology/accountmanage/ucdp.jsp Freddie Mac - http://www.freddiemac.com/sell/secmktg/uniform_collateral_data_portal.html?tab=2#register

Nationwide Bank 29 Correspondent Lending Manual – Section 3 Underwriting Policies Revised 04/15/2016