Second quarter results 2001 16 August, 2001. Broad mix of clients and products proves its value ...

30

Second quarter results 2001 16 August, 2001

-

Upload

primrose-foster -

Category

Documents

-

view

213 -

download

0

Transcript of Second quarter results 2001 16 August, 2001. Broad mix of clients and products proves its value ...

Second quarter results 2001

16 August, 2001

Broad mix of clients and products proves its value

Strategy continuous dynamic process

Overriding objective Top 5;

annual performance targets published at full year results 2001

Changes in Managing Board

Second quarter results 2001

Highlights second quarter 2001

Second quarter reflects quality and sustainability of the income stream

Restructuring programmes in SBUs are beginning to bear fruit

Michigan National Corporation consolidated in BU United States

Excluding consolidation, divestitures and currency translation effects RWA contracted by EUR 4.2 bn

Revenues up 8.1% despite weak market conditions

Operating profit before taxes increased by 3.8%

EUR 962 mln extraordinary gain from the sale of EAB

Interim dividend per share at EUR 0.45

Status report on strategic initiatives:Strategy Wholesale Clients SBU

Revenue enhancement– strong focus on European client base – emphasis on financial institutions and large/medium cap

corporate clients– emphasis on annuity products and selective investment banking

products

Cost control

– decrease in headcount from TOPS, equity business and

disposal of certain international operations

Capital allocated will be reduced

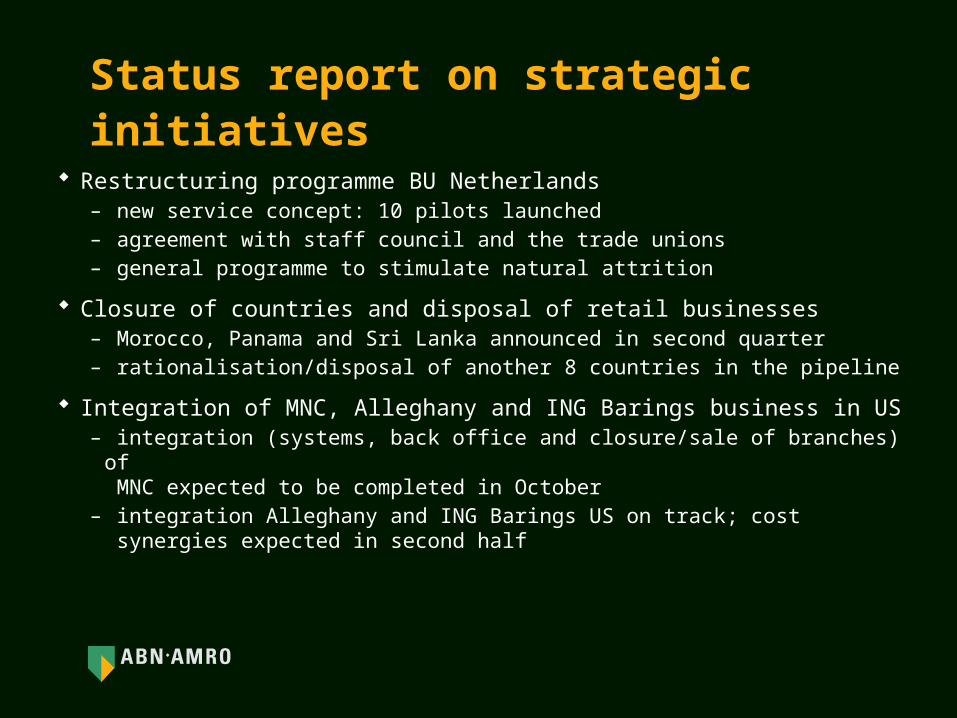

Status report on strategic initiatives

Restructuring programme BU Netherlands– new service concept: 10 pilots launched– agreement with staff council and the trade unions– general programme to stimulate natural attrition

Closure of countries and disposal of retail businesses– Morocco, Panama and Sri Lanka announced in second quarter– rationalisation/disposal of another 8 countries in the pipeline

Integration of MNC, Alleghany and ING Barings business in US– integration (systems, back office and closure/sale of branches) of

MNC expected to be completed in October– integration Alleghany and ING Barings US on track; cost

synergies expected in second half

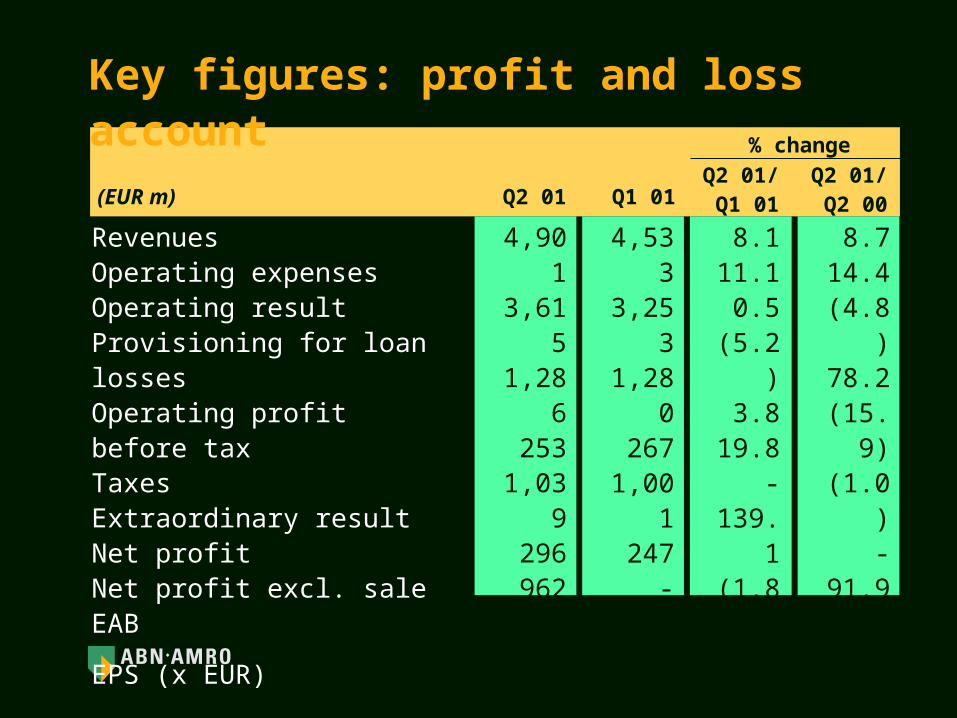

RevenuesOperating expensesOperating resultProvisioning for loan lossesOperating profit before taxTaxesExtraordinary resultNet profitNet profit excl. sale EAB

EPS (x EUR)

(EUR m)

Key figures: profit and loss account

Q2 01

4,9013,6151,286

2531,039

296962

1,633671

0.44

Q1 01

4,5333,2531,280

2671,001

247-

683683

0.45

Q2 01/Q1 01

8.111.1

0.5(5.2)

3.819.8

-139.1(1.8)

(2.2)

8.714.4(4.8)78.2

(15.9)(1.0)

-91.9

(21.2)

(22.8)

% change

Q2 01/Q2 00

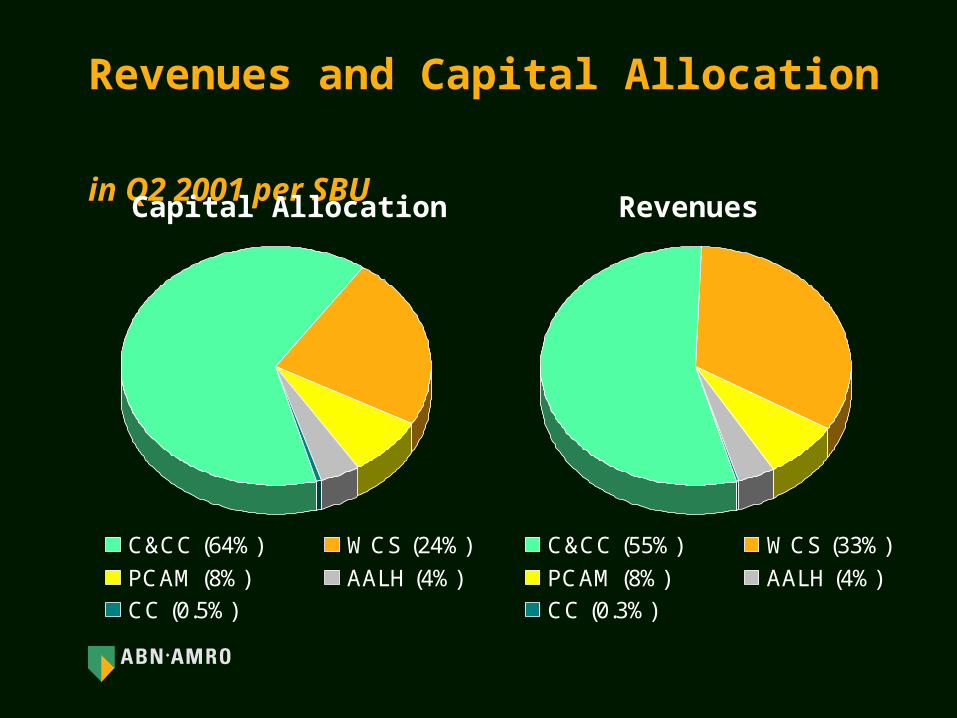

C&CC (64%) WCS (24%)

PCAM (8%) AALH (4%)

CC (0.5%)

Revenues and Capital Allocation in Q2 2001 per SBU

C&CC (55%) WCS (33%)

PCAM (8%) AALH (4%)

CC (0.3%)

Capital Allocation Revenues

C&CC (58%)

WCS (17%)

PCAM (10%)

AA Lease Holding (5%)

Corporate Centre (10%)

EUR 1,039 mln (+3.8%)

Operating profit before tax Q2 2001in %

Provisioning second quarter 2001

- specific bad debt provisioning- cross-border risks provisioning

Provisioning for loan lossesAddition to FARTotal

262(9)

253-

253

160(36)

12418

142

Q2 01(EUR m)

280(13)

267-

267

Q1 01 Q2 00

Consumer & Commercial ClientsWholesale ClientsPrivate Clients & Asset ManagementAA Lease HoldingCorporate Centre

22040(1)

5(11)

809010

4(42)

Q2 01(EUR m)

17692

34

(8)

Q1 01 Q2 00

0

50

100

150

200

250

300

92 93 94 95 96 97 98 99 '00 01*

0

10

20

30

40

50

60EUR bn

Risk provisioning (2001: excl. changes in FAR)as a % of RWA (right hand scale)

Risk provisioning as a % of RWA

RWA

26bp

39bp35bp

BASISPOINTS

* 2001 annualised

23bp

36bp

Key figures: balance sheet

* -1.5% adjusted for impact of acquisitions and exchange rates

Total assetsShareholders’ EquityGroup capitalRisk-weighted assets*

Total capital ratioTier 1 ratio

(EUR bn) 30 06 01

614.611.634.7

286.1

10.19%6.55%

31 03 01

601.712.233.7

278.4

10.19%6.82%

30 06 01/ 31 03 01

2.1(5.1)

2.92.8

13.2(7.6)

6.68.4

% change

30 06 01/31 12 00

Operating result

Provisioning

Pre-tax profit

RWA* (EUR bn)

Revenues Q2 2001

Interest

Other

Commissions

Diversified, stable and consistent income stream

Costs are strictly monitored and under control

Higher provisioning levels, but overall quality of the portfolio remains strong

Performance BU Netherlands stabilising, US and Brazil perform well

Trading

(EUR m) Q2 01 Q1 01

Consumer & Commercial Clients

* RWA June 2001 compared to March 2001

% change

818

220

598

166.4

847

176

671

163.3

(3.4)

25.0

(10.9)

1.9

10.4

175.0

(9.5)

Q2 01/Q1 01

Q2 01/Q2 00

The Netherlands (10%)

United States (69%)

Brazil (20%)

Rest of the world (1%)

EUR 598 mln (-10.9%)

C&CC operating profit before tax split-up by market

Aligning clients with products has led to the choice of high margin products and better allocation of capital

Negative impact of depressed equity markets is partly offset by broad mix of clients and products in general and the performance of GFM in particular

Strong increase in interest income and lowering of provisioning drive profitability

Wholesale Clients

Operating result

Provisioning

Pre-tax profit

RWA* (EUR bn)

Revenues Q2 2001

Interest

Other

Commissions

Trading

(EUR m) Q2 01 Q1 01

* RWA June 2001 compared to March 2001

% change

229

40

178

100.5

213

92

113

96.9

7.5

(56.5)

57.5

3.7

(38.8)

(55.6)

(42.6)

Q2 01/Q1 01

Q2 01/Q2 00

Healthy increase in revenues despite difficult market conditions

Integration of businesses within Private Clients and integration of Alleghany within Asset Management well under way

Assets under Management rose 4.5% to EUR 175.8 bn

Assets under Administration remained stable at EUR 110 bn

Private Clients & Asset Management

Operating result

Provisioning

Pre-tax profit

RWA* (EUR bn)

Revenues Q2 2001

Interest

Other

Commissions

Trading

(EUR m) Q2 01 Q1 01

* RWA June 2001 compared to March 2001

% change

97

(1)

99

6.0

70

3

66

6.1

38.6

-

50.0

(1.6)

(41.6)

-

(36.5)

Q2 01/Q1 01

Q2 01/Q2 00

Wholesale limits by regionas per June 2001

Asia Pacific Advanced8% (8%)

North America27% (26%)

Africa1% (1%)

Europe 48% (50%)

Eastern Europe1% (2%)

Middle East

1% (1%)

Asia7% (6%)

Latin America6% (5%)

( ) December

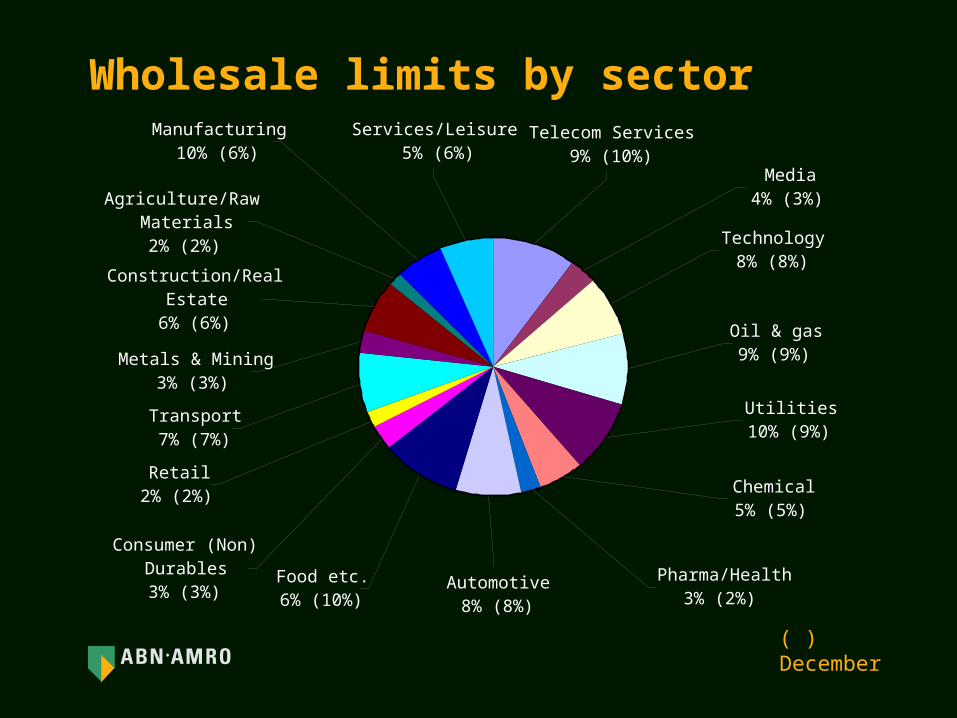

Wholesale limits by sectorTelecom Services

9% (10%)Media

4% (3%)

Technology8% (8%)

Oil & gas9% (9%)

Utilities10% (9%)

Pharma/Health3% (2%)

Chemical5% (5%)

Automotive8% (8%)

Food etc.6% (10%)

Services/Leisure 5% (6%)

Manufacturing10% (6%)

Agriculture/Raw Materials2% (2%)

Construction/Real Estate

6% (6%)

Retail2% (2%)

Consumer (Non) Durables3% (3%)

Transport7% (7%)

Metals & Mining3% (3%)

( ) December

Outlook full year 2001

The much hoped for improvements, in the economic and

market conditions, have not materialised in the first half

of the year and it is unlikely that there will be a significant

improvement in the remainder of the year.

Consequently, we expect our full year results to be

broadly in line with our performance in the first half of

this year.

ANNEXES

Internal credit risk ratingsTelecom Service Industry

UCR 51.6 %

UCR 420.1%

UCR 17.4%

UCR 214.7%

UCR 356.2%

UCR 1 >AA UCR 2 >A- UCR 3 >BBB UCR 4 >BB- UCR 5 >B- UCR 6 >CC UCR 7 <C

Investment grade 78% 81%Non-investment grade 22% 19%

Jun Dec

Internal credit risk ratingsAutomotive Industry

UCR 62%

UCR 51%

UCR 412%

UCR 16%

UCR 228%

UCR 351%

UCR 1 >AA UCR 2 >A- UCR 3 >BBB UCR 4 >BB- UCR 5 >B- UCR 6 >CC UCR 7 <C

Investment grade 85% 89%Non-investment grade 15% 11%

Jun Dec

UCR 61% (0%)

UCR 51% (1%)

UCR 4 12% (10%)

UCR 122% (22%)

UCR 226% (31%)

UCR 339% (36%)

Internal credit risk ratingsWholesale Clients

UCR 1 >AA UCR 2 >A- UCR 3 >BBB UCR 4 >BB- UCR 5 >B- UCR 6 >CC UCR 7 <C

( ) December

Investment grade 86% 89%Non-investment grade 14% 11%

Jun Dec

UCR 1-384% (86%)

UCR 412% (10%)

UCR 5-74% (4%)

( ) December

UCR 1 >AA UCR 2 >A- UCR 3 >BBB UCR 4 >BB- UCR 5 >B- UCR 6 >CC UCR 7 <C

Investment grade 84% 86%Non-investment grade 16% 14%

Jun Dec

Internal credit risk ratings Wholesale United States

UCR 1-364% (66%)

UCR 425% (27%)

UCR 5-711% (7%)

( ) December

UCR 1 >AA UCR 2 >A- UCR 3 >BBB UCR 4 >BB- UCR 5 >B- UCR 6 >CC UCR 7 <C

Investment grade 64% 66%Non-investment grade 36% 34%

Jun Dec

Internal credit risk ratings C&CC BU United States

Loan portfolio C&CC BU United States

45%

8%

54%

37%

47%

35%

56%

8%

11%

7%

0% 20% 40% 60% 80% 100%

MNC

StanFed

LaSalle

BU US

Commercial Real Estate Individuals/Other

2%

Internal credit risk ratings C&CC BU United States

59%

98%

51%

26%

37%

15%

12%

0% 20% 40% 60% 80% 100%

MNC

StanFed

LaSalle

UCR 1-3 UCR 4 UCR 5-7

2%

0%

25%

50%

75%

100%

97-1 97-2 98-1 98-2 99-1 99-2 00-1 00-2 01-1

Other

Trading

Commissions

Interest

Composition of revenue(EUR m)

Trading break down 1996 - 2001(EUR m)

-200

0

200

400

600

800

1000

1200

Other

Derivatives

Securities

Forex

97-1 97-2 98-1 98-2 99-1 99-2 00-1 00-2 01-1

Cautionary Statement regarding Forward-Looking Statements

This announcement contains forward-looking statements. Forward-looking statements arestatements that are not historical facts, including statements about our beliefs and expectations.Any statement in this announcement that expresses or implies our intentions, beliefs,expectations or predictions (and the assumptions underlying them) is a forward-lookingstatement. These statements are based on plans, estimates and projections, as they are currentlyavailable to the management of ABN AMRO. Forward-looking statements therefore speak only asof the date they are made, and we take no obligation to update publicly any of them in light ofnew information or future events.

Forward-looking statements involve inherent risks and uncertainties. A number of importantfactors could therefore cause actual future results to differ materially from those expressed orimplied in any forward-looking statement. Such factors include, without limitation, the conditions inthe financial markets in Europe, the United States, Brazil and elsewhere from which we derive asubstantial portion of our trading revenues; potential defaults of borrowers or tradingcounterparties; the implementation of our restructuring including the envisaged reduction inheadcount; the reliability of our risk management policies, procedures and methods; and otherrisks referenced in our filings with the U.S. Securities and Exchange Commission. For moreinformation on these and other factors, please refer to our Annual Report on Form 20-F filed withthe U.S. Securities and Exchange Commission and to any subsequent reports furnished or filedby us with the U.S. Securities and Exchange Commission.

The forward-looking statements contained in this announcement are made as of the date hereof,and the companies assume no obligation to update any of the forward-looking statementscontained in this announcement.