Second General Assembly The IEA/NEA Nuclear Energy ...€¦ · NEA Sustainable Nuclear Energy...

19

© OECD/IEA 2010 Steven Lee, IEA Martin Taylor, NEA Sustainable Nuclear Energy Technology Platform Second General Assembly 14 September 2010, Brussels The IEA/NEA Nuclear Energy Technology Roadmap

Transcript of Second General Assembly The IEA/NEA Nuclear Energy ...€¦ · NEA Sustainable Nuclear Energy...

© OECD/IEA 2010

Steven Lee, IEA

Martin Taylor, NEA

Sustainable Nuclear Energy Technology Platform Second General Assembly

14 September 2010, Brussels The IEA/NEA Nuclear Energy Technology Roadmap

© O

ECD

/IEA

& O

ECD

/NEA

20

10

2

0

5

10

15

20

25

30

35

40

45

50

55

60

2010 2015 2020 2025 2030 2035 2040 2045 2050

Gt

CO

2

CCS 19%

Renewables 17%

Nuclear 6%

Power generation efficiency and fuel switching 5%

End-use fuel switching 15%

End-use fuel and electricity efficiency 38%

BLUE Map emissions 14 Gt

Baseline emissions 57 Gt

WEO 2009 450 ppm case ETP2010 analysis

Key Technology Options

© O

ECD

/IEA

& O

ECD

/NEA

20

10

3

Power Sector 2050 CO2 Emissions Reductions in BLUE Map Scenario

Nuclear, 19%

Hydro; 2%

Wind; 11%

Solar PV; 7%

Solar CSP; 9%

Geothermal; 3% Biomass & waste; 2%

Carbon capture & storage; 31%

IGCC coal; 4%

Ultra/supercritical coal; 3%

Gas efficiency; 2%

Coal to gas switching; 7%

Total CO2 emissions reductions from electricity sector: 14 Gt

Emissions reductions compared to Baseline scenario

© O

ECD

/IEA

& O

ECD

/NEA

20

10

4

Based on a scenario to halve CO2 emissions by 2050 Establish a baseline of technology status today Identify and address technology-specific barriers

Create technical, policy, legal, financial, and public acceptance milestones and priority near-term actions

Create a process for stakeholder collaboration Special developing country focus on engagement,

national roadmaps Identify partners for implementation Support technology diffusion, knowledge sharing

among countries

The Role of the IEA Energy Technology Roadmaps

How Do We Get There From Here?

© O

ECD

/IEA

& O

ECD

/NEA

20

10

5

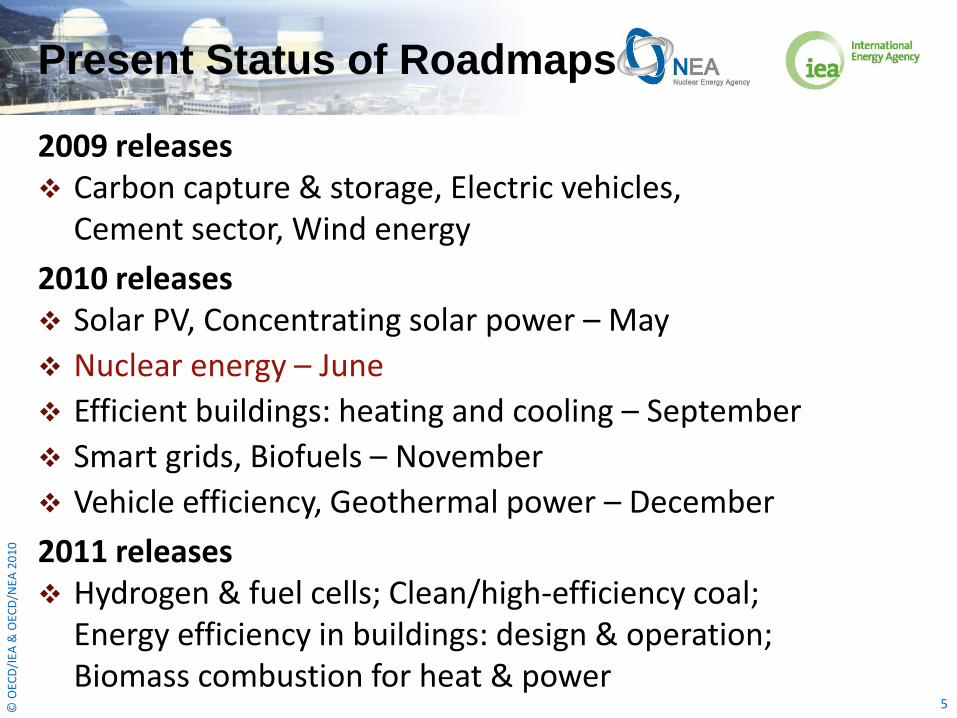

Present Status of Roadmaps

2009 releases Carbon capture & storage, Electric vehicles,

Cement sector, Wind energy

2010 releases Solar PV, Concentrating solar power – May

Nuclear energy – June

Efficient buildings: heating and cooling – September

Smart grids, Biofuels – November

Vehicle efficiency, Geothermal power – December

2011 releases Hydrogen & fuel cells; Clean/high-efficiency coal;

Energy efficiency in buildings: design & operation; Biomass combustion for heat & power

© O

ECD

/IEA

& O

ECD

/NEA

20

10

6

Nuclear is Already a Widely Used Low-Carbon Technology

Natural gas,

21,7%

Wind, 1,4%

Nuclear, 21.4%

Other, 0,4%

Hydro, 11,8%

Biomass & waste, 2,0%

Oil, 4,1%

Coal, 37.2%

OECD Total: 10 642 TWh

Natural gas;

20,9%

Wind; 0,9%

Nuclear, 13.8%

Other; 0,3%

Hydro; 15,6% Biomass

& waste; 1,3%

Oil; 5,7%

Coal, 41.6%

World Total: 19 756 TWh

Data for 2007. Source: World Energy Outlook, IEA 2009

© O

ECD

/IEA

& O

ECD

/NEA

20

10

7

0

50

100

150

200

250

Nuclear Coal Gas WindOnshore

Nuclear Coal Gas WindOnshore

Nuclear Coal Gas WindOnshore

N. America Europe Asia Pacific

USD

/MW

h

Median Line

Nuclear is already a very cost competitive technology

Levelised Electricity Generation Cost by Region (5% Discount Rate)

Source: Projected Costs of Generating Electricity, IEA/NEA 2010

© O

ECD

/IEA

& O

ECD

/NEA

20

10

8

Levelised Electricity Generation Cost by Region (10% Discount Rate)

0

50

100

150

200

250

Nuclear Coal Gas WindOnshore

Nuclear Coal Gas WindOnshore

Nuclear Coal Gas WindOnshore

N. America Europe Asia Pacific

USD

/MW

h

Median Line

But nuclear costs depend strongly on the discount rate Source: Projected Costs of Generating Electricity, IEA/NEA 2010

© O

ECD

/IEA

& O

ECD

/NEA

20

10

9

A New Age of Electrification

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

50 000

2007 Baseline 2050 BLUE Map 2050 BLUE HighNuclear 2050

Ele

ctr

icit

y g

en

era

tio

n (

TW

h)

Other

Solar

Wind

Biomass + CCS

Biomass/waste

Hydro

Nuclear

Natural gas + CCS

Natural gas

Oil

Coal + CCS

Coal

© O

ECD

/IEA

& O

ECD

/NEA

20

10

10

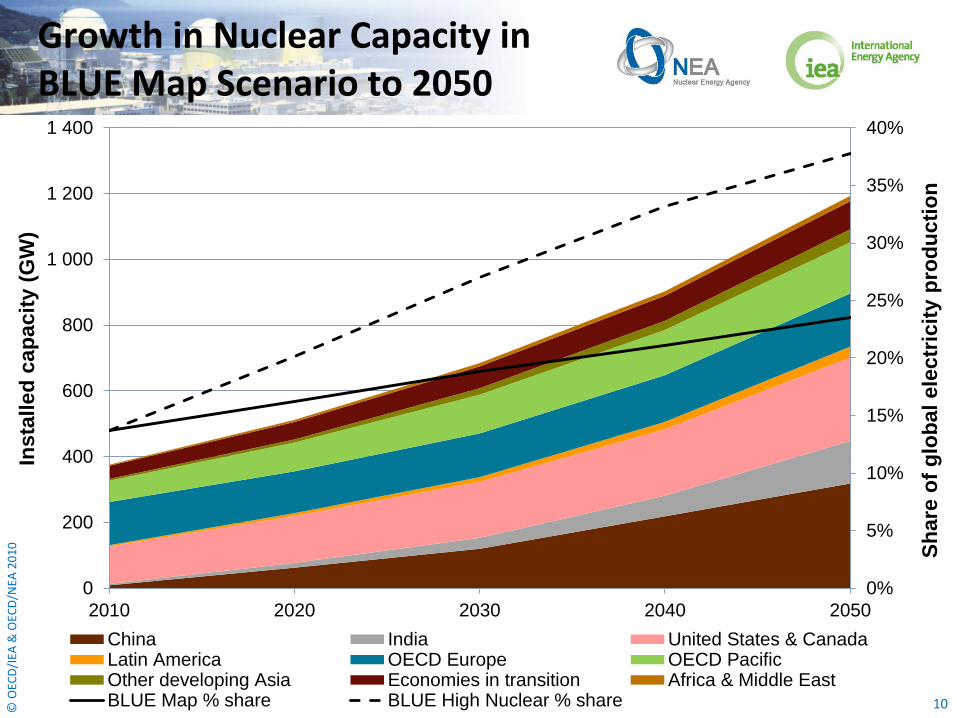

Growth in Nuclear Capacity in BLUE Map Scenario to 2050

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

200

400

600

800

1 000

1 200

1 400

2010 2020 2030 2040 2050

Sh

are

of

glo

bal

ele

ctr

icit

y p

rod

ucti

on

Insta

lled

cap

acit

y (

GW

)

China India United States & CanadaLatin America OECD Europe OECD PacificOther developing Asia Economies in transition Africa & Middle EastBLUE Map % share BLUE High Nuclear % share

© O

ECD

/IEA

& O

ECD

/NEA

20

10

11

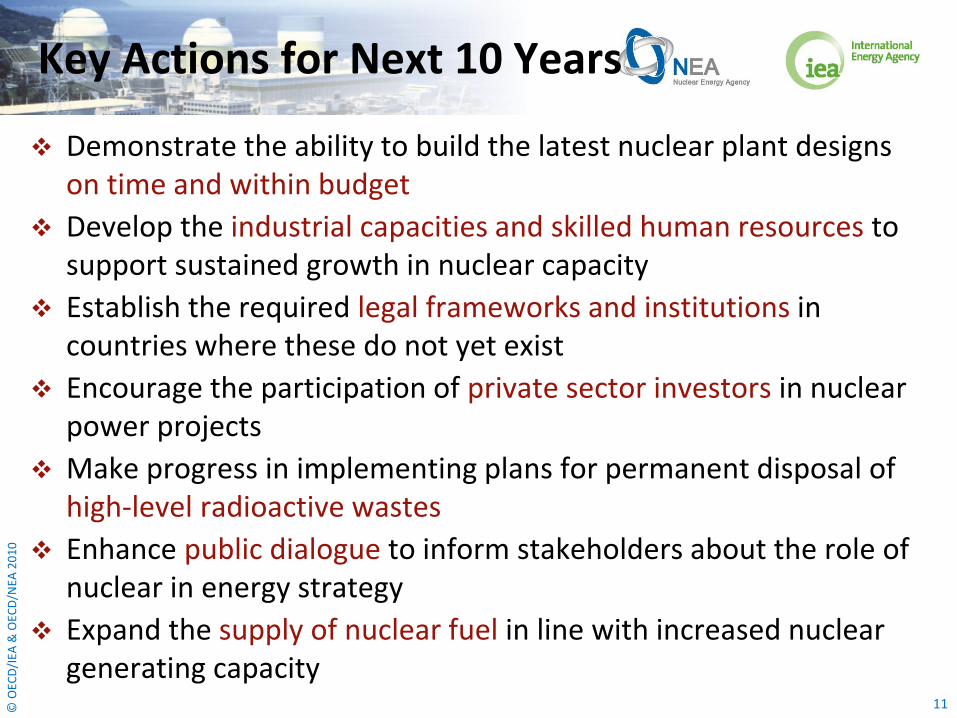

Demonstrate the ability to build the latest nuclear plant designs on time and within budget

Develop the industrial capacities and skilled human resources to support sustained growth in nuclear capacity

Establish the required legal frameworks and institutions in countries where these do not yet exist

Encourage the participation of private sector investors in nuclear power projects

Make progress in implementing plans for permanent disposal of high-level radioactive wastes

Enhance public dialogue to inform stakeholders about the role of nuclear in energy strategy

Expand the supply of nuclear fuel in line with increased nuclear generating capacity

Key Actions for Next 10 Years

© O

ECD

/IEA

& O

ECD

/NEA

20

10

12

Milestones: Policy Support

2010 2020 2030 2040 2050

Clear & stable

commitment to

nuclear power in

energy policy Harmonise regulatory requirements to

facilitate the use of standardised designs

Strengthen non-proliferation regimes,

while providing security of fuel supply

Ensure legal &

regulatory

systems work

effectively

Ensure institutions & funding are in place

for waste disposal & decommissioning

Develop legal & institutional frameworks

for wider use of advanced fuel cycles

© O

ECD

/IEA

& O

ECD

/NEA

20

10

13

Milestones: Capacity Building & Industry

2010 2020 2030 2040 2050

Increase capacity

to supply nuclear

plant components

& systems

Strengthen & broaden global supply chains as more countries

launch nuclear programmes

Increase uranium production & nuclear fuel cycle capacities to

meet rapid demand growth

Develop the

qualified & skilled

human resources

needed

Achieve nuclear

construction rates

from 2020 double

present levels

Continue to

increase nuclear

construction rates

Develop industrial

capacities to

support advanced

fuel cycles

© O

ECD

/IEA

& O

ECD

/NEA

20

10

14

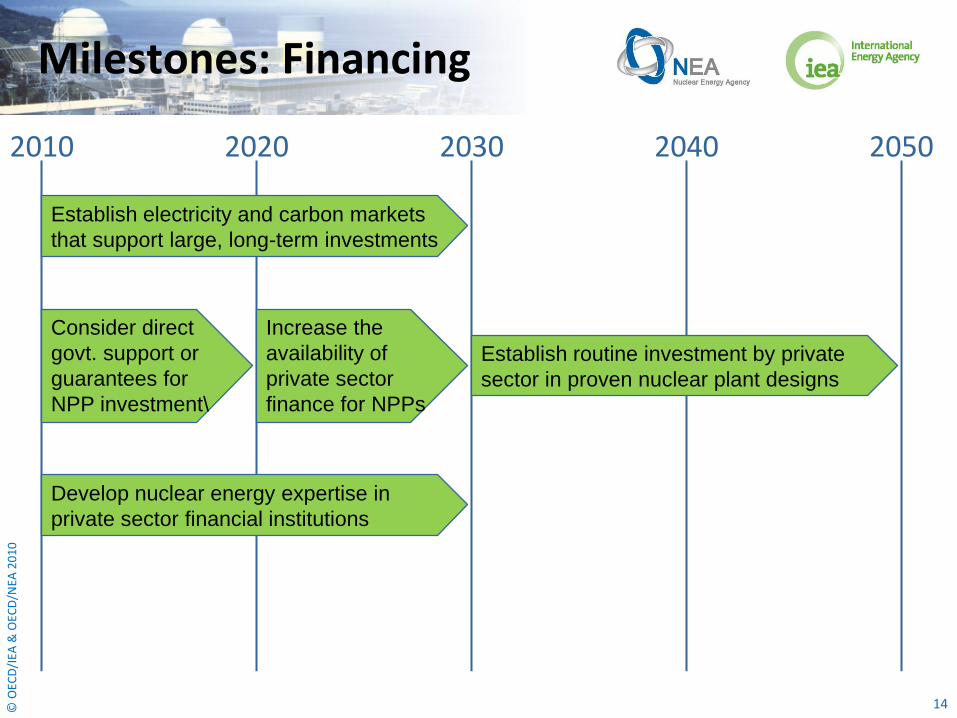

Milestones: Financing

2010 2020 2030 2040 2050

Consider direct

govt. support or

guarantees for

NPP investment\

Establish electricity and carbon markets

that support large, long-term investments

Develop nuclear energy expertise in

private sector financial institutions

Establish routine investment by private

sector in proven nuclear plant designs

Increase the

availability of

private sector

finance for NPPs

© O

ECD

/IEA

& O

ECD

/NEA

20

10

15

Regional Investment Needs for Nuclear in BLUE Map Scenario

China 893 USD bn

India 389 USD bn

Latin America 116 USD bn

United States & Canada

883 USD bn

OECD Europe 586 USD bn

OECD Pacific 615 USD bn

Other Developing Asia

107 USD bn

Economies in Transition

330 USD bn

Africa & Middle East

56 USD bn

© O

ECD

/IEA

& O

ECD

/NEA

20

10

16

Milestones: Technology Development & Deployment

2010 2020 2030 2040 2050

Fully

establish

Gen III+

designs,

bring

FOAK

plants

on-line

Implement plans to build & operate

geological repositories for waste disposal

Show

on-time

& on-

budget

completion

of further

Gen III+

plants Complete demonstration of the most

promising Gen IV nuclear plants

Increase use of nuclear energy for non-

electricity applications (e.g. heat)

Strengthen RD&D

in advanced fuel

cycles

Build & operate

commercial-scale

Gen IV plants

© O

ECD

/IEA

& O

ECD

/NEA

20

10

17

Key Findings (1)

Nuclear is a mature low-carbon energy technology that is already available for wider deployment

In the ETP BLUE Map scenario, nuclear capacity grows to 1 200 GWe by 2050, providing 24% of global electricity

Obstacles to this expansion are mainly policy-related, industrial and financial, rather than technological

But in the longer term, technological development will be needed for nuclear to remain competitive

A clear and stable commitment to nuclear as part of national energy strategy is a prerequisite

Financing will be a major challenge, and government support may be needed for private-sector investment

© O

ECD

/IEA

& O

ECD

/NEA

20

10

18

Key Findings (2)

Industrial capacity to build nuclear plants will need to double by 2020 for expansion in line with the scenario; fuel cycle capacities will also need to increase

A great increase in highly qualified and skilled human resources will also be needed

Progress needs to be made in building and operating facilities for the disposal of spent fuel & high-level waste

Safeguards and physical protection measures must be maintained and strengthened where necessary

Generation IV reactor and fuel cycle technologies may offer improved sustainability, economics, proliferation-resistance, safety and reliability, starting before 2050

© O

ECD

/IEA

& O

ECD

/NEA

20

10

19

The Nuclear Energy Roadmap was released on 16 June

All roadmaps are

available at:

www.iea.org/roadmaps