SEB Retail Banking 2009

17

Mats Torstendahl Head of Retail Banking January – June 2009 Retail Banking presentation

-

Upload

sebgroup -

Category

Devices & Hardware

-

view

7.752 -

download

2

description

Retail Banking Presentation. January - June 2009.

Transcript of SEB Retail Banking 2009

Mats TorstendahlHead

of Retail

Banking

January –

June 2009

Retail Banking presentation

OrganisationPresident &

CEO

Annika Falkengren

Group Credits & Group Risk Control

Johan Andersson

Compliance

Gent Jansson

Wealth ManagementFredrik Boheman

Life

Anders Mossberg

CFO

Jan Erik Back

Group IT

Ulf Thorstensson

Group Operations

Pia Warnerman

Group Staff

Bo Magnusson

Merchant Banking

Magnus Carlsson

Retail Banking

Mats Torstendahl

Group Strategy & Business Dev.Hans Larsson

HR & Org. Dev.

Ingrid Engström

Business Support &

Group Staff

Bo Magnusson,Deputy CEO

* Reports directly to the Board

Internal Audit

Agneta Brevenhag*

Baltic

Martin Johansson

SEB's

retail

operations H1: 2009

945 FTE's

59 branches

#2 position, ~25% market share

883 FTE's

60 branches

#2 position, ~15% market share

1 411 FTE's

75 branches

# 1 position, ~30% market share

1 716 FTE's

174 branches

~1% market share

2 642 FTE's

161 branches

#4 position, 10-15% market share

812 FTE's

3.2m cards

#1 inom charge card

Retail Sweden -

Strong performance

Retail Sweden in short

Attractive customer base–

sustained growth in SME and affluent segment

Proven earnings capacity–

4% income growth H1-09 vs. H1-08–

Mortgage volumes +6% since year start

Competitive profitability–

19% RoE in first half of 2009

Innovative product offerings–

Enkla

firman, SME product of the year

Healthy credit quality–

Credit losses in H1 manageable: SEK 185m

Retail Sweden, H1 2009HighlightsSEK m

Jan –

Jun 2009

2008

Total income

3,231

4%Interest, net

2,344

6%Commission, net 727

-4%Total expenses -2,034

4%

Profit bef. credit losses

1,197

3%Credit losses, net

-185

462%Operating profit 1,012

-10%

RoE, %

19.0

22.0C/I 0.63

0.63

Total lending

322,500

6%Total deposits

155,000

4%

Both the SME and mass affluent segment has continued to develop well during 2009–

2,800 net new SME customers–

1,400 net new mass affluent customers

Importance of lending is growing–

Increasing margins and sustained growth in lending volumes, not least in mortgages

–

Sharply falling margins and limited growth in deposit volumes

Although higher than previous year, credit loss-level is still reflecting good credit quality

Financial performance over time Retail Banking Sweden

-2000

200400600800

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08 Q4-08 Q1-09 Q2-09

Credit losses Profit (after Credit losses)

0

500

1 000

1 500

2 000

Q1 07 Q2 07 Q3 Q4 Q1 08 Q2 08 Q3 Q4 Q1 09 Q2 09

Income Expenses SEK m

Changes in income generation NII Q3 ’08 –

Q2 ’09, Retail Banking, Sweden

Deposits

Other lending

Mortgages

Q3 2008 Q4 2008 Q1 2009 Q2 2009

35%

33%

33%

28%

30%

42%

24%

28%

48%

21%

25%

54%

Mortgages private market Total Sweden, volumes and margins

0

50

100

150

200

250

Q12006

Q2 Q3 Q4 Q12007

Q2 Q3 Q4 Q12008

Q2 Q3 Q4 Q12009

Q20,00%

0,25%

0,50%

0,75%

1,00%

1,25%Outstanding volume, SEK bn Average margin

Mortgages private market Retail Sweden, market share, per cent

* New measurement method from Q4 2007. Lowers the volume market share with approximately 0.2 percentage points

*10

12

14

16

18

20

Q106

Q2 Q3 Q4 Q107

Q2 Q3 Q4 Q108

Q2 Q3 Q4 Q109

Q2

Sales Volume

YTD2007

YTD2008

YTD2009

Q1 2009 Q2 2009

Equities

-17%

Q1 2009 Q2 2009

Q1 2009 Q2 2009

+21%

+26%

+20%

Total commissions, netEquity linked bonds

Mutual funds

Commissions re-bounce Light in the tunnel….?

1 950

176

1 000

1 200

1 400

1 600

1 800

2 000

2 200

Total expenses H1-08 Total expenses H1-09

Cost base Increased pension cost

Number of FTEs:

2 865

2 642

Change in expense level –

driven by pensions

Swedish Retail, H12009 vs. H12008, SEK m

Credit losses Retail Sweden Q1 ’07 –

Q2 ’09, SEK m

-20

0

20

40

60

80

100

120

Q1'07

Q2'07

Q3'07

Q4'07

Q1'08

Q2'08

Q3'08

Q4'08

Q1'09

Q2'09

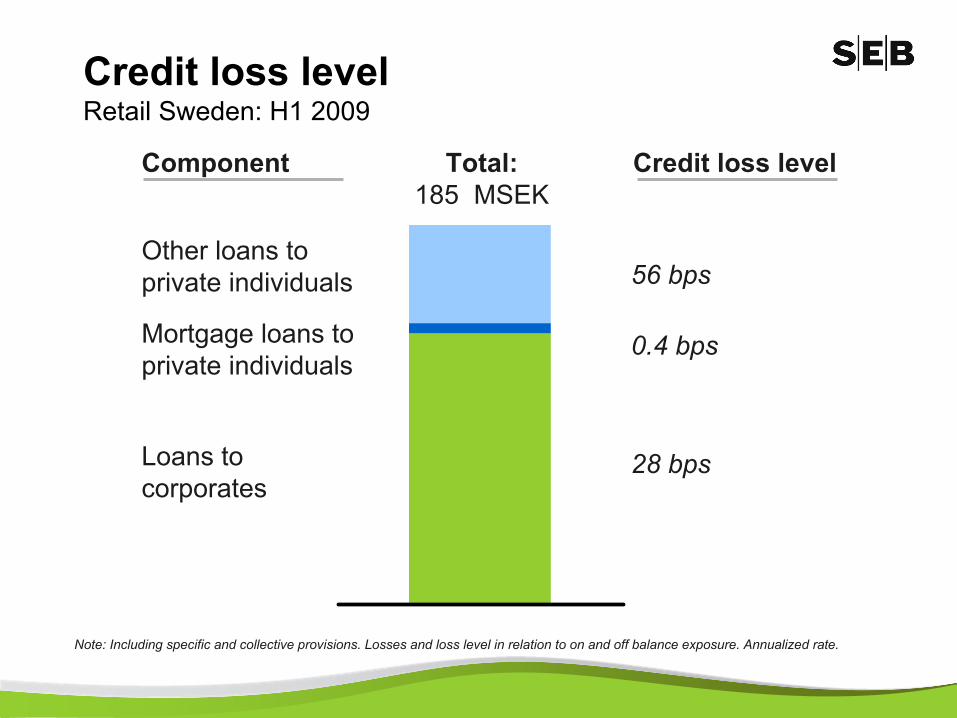

Total:185 MSEK

Other loans to private individuals

Mortgage loans to private individuals

Loans to corporates

Component

Note: Including specific and collective provisions. Losses and loss level in relation to on and off balance exposure. Annualized rate.

28 bps

0.4 bps

56 bps

Credit loss level

Credit loss level Retail Sweden: H1 2009

Stabilising economy but long and winding road to recovery

SEB well positioned to support our customers and develop the business in core areas

Swedish Retail is one of these core areas

Improve customer experience & satisfaction

Grow SME –

not only the micro segment

Strengthen remote channels (e.g. OITR)

Leadership & employee development

Appendix

Business volume development Retail Sweden, SEK bn

Mortgages

0

50

100

150

200

250

Q206

Q4 Q207

Q4 Q208

Q4 Q209

CorporatePrivate

Other lending*

0

50

100

150

200

250

Q206

Q4 Q207

Q4 Q208

Q4 Q209

Deposits

0

50

100

150

200

250

Q206

Q4 Q207

Q4 Q208

Q4 Q209

*

Excluding leasing