Seasoned African Campaigner Initiation of Coverage ... · Canaccord Genuity is the global capital...

30

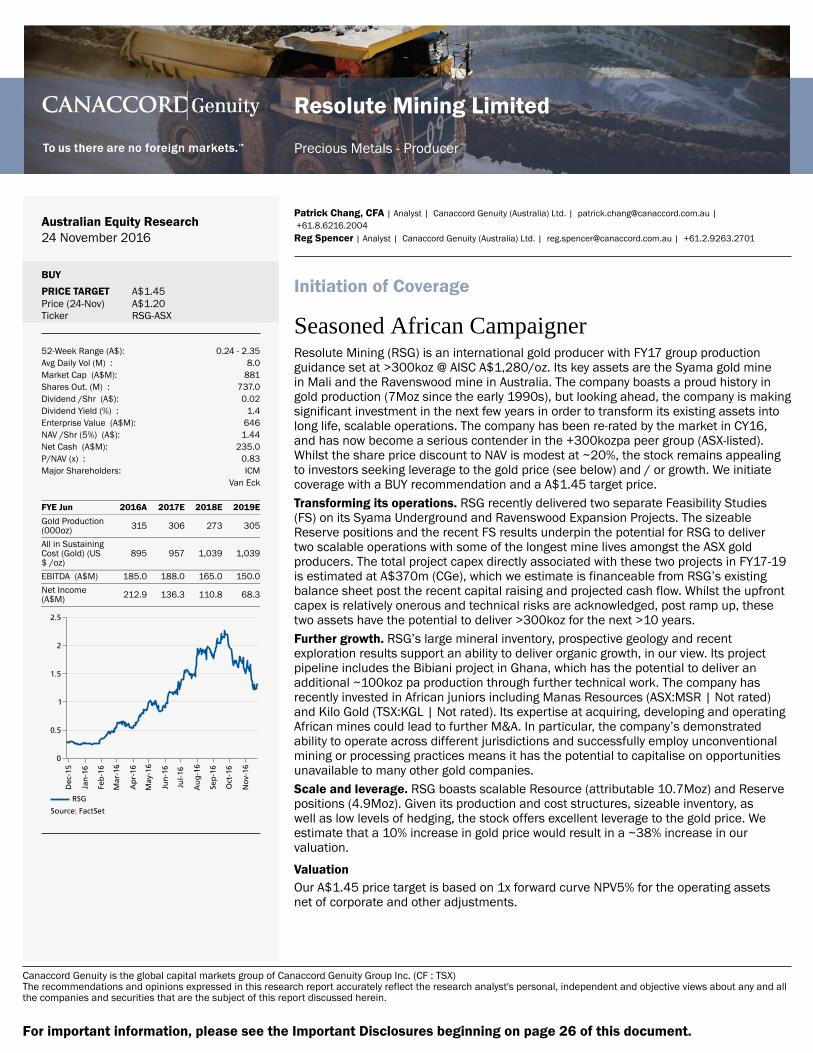

Resolute Mining Limited Precious Metals - Producer Canaccord Genuity is the global capital markets group of Canaccord Genuity Group Inc. (CF : TSX) The recommendations and opinions expressed in this research report accurately reflect the research analyst's personal, independent and objective views about any and all the companies and securities that are the subject of this report discussed herein. Australian Equity Research 24 November 2016 BUY PRICE TARGET A$1.45 Price (24-Nov) Ticker A$1.20 RSG-ASX 52-Week Range (A$): 0.24 - 2.35 Avg Daily Vol (M) : 8.0 Market Cap (A$M): 881 Shares Out. (M) : 737.0 Dividend /Shr (A$): 0.02 Dividend Yield (%) : 1.4 Enterprise Value (A$M): 646 NAV /Shr (5%) (A$): 1.44 Net Cash (A$M): 235.0 P/NAV (x) : 0.83 Major Shareholders: ICM Van Eck FYE Jun 2016A 2017E 2018E 2019E Gold Production (000oz) 315 306 273 305 All in Sustaining Cost (Gold) (US $ /oz) 895 957 1,039 1,039 EBITDA (A$M) 185.0 188.0 165.0 150.0 Net Income (A$M) 212.9 136.3 110.8 68.3 2.5 2 1.5 1 0.5 0 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 RSG Source: FactSet Patrick Chang, CFA | Analyst | Canaccord Genuity (Australia) Ltd. | [email protected] | +61.8.6216.2004 Reg Spencer | Analyst | Canaccord Genuity (Australia) Ltd. | [email protected] | +61.2.9263.2701 Initiation of Coverage Seasoned African Campaigner Resolute Mining (RSG) is an international gold producer with FY17 group production guidance set at >300koz @ AISC A$1,280/oz. Its key assets are the Syama gold mine in Mali and the Ravenswood mine in Australia. The company boasts a proud history in gold production (7Moz since the early 1990s), but looking ahead, the company is making significant investment in the next few years in order to transform its existing assets into long life, scalable operations. The company has been re-rated by the market in CY16, and has now become a serious contender in the +300kozpa peer group (ASX-listed). Whilst the share price discount to NAV is modest at ~20%, the stock remains appealing to investors seeking leverage to the gold price (see below) and / or growth. We initiate coverage with a BUY recommendation and a A$1.45 target price. Transforming its operations. RSG recently delivered two separate Feasibility Studies (FS) on its Syama Underground and Ravenswood Expansion Projects. The sizeable Reserve positions and the recent FS results underpin the potential for RSG to deliver two scalable operations with some of the longest mine lives amongst the ASX gold producers. The total project capex directly associated with these two projects in FY17-19 is estimated at A$370m (CGe), which we estimate is financeable from RSG’s existing balance sheet post the recent capital raising and projected cash flow. Whilst the upfront capex is relatively onerous and technical risks are acknowledged, post ramp up, these two assets have the potential to deliver >300koz for the next >10 years. Further growth. RSG’s large mineral inventory, prospective geology and recent exploration results support an ability to deliver organic growth, in our view. Its project pipeline includes the Bibiani project in Ghana, which has the potential to deliver an additional ~100koz pa production through further technical work. The company has recently invested in African juniors including Manas Resources (ASX:MSR | Not rated) and Kilo Gold (TSX:KGL | Not rated). Its expertise at acquiring, developing and operating African mines could lead to further M&A. In particular, the company’s demonstrated ability to operate across different jurisdictions and successfully employ unconventional mining or processing practices means it has the potential to capitalise on opportunities unavailable to many other gold companies. Scale and leverage. RSG boasts scalable Resource (attributable 10.7Moz) and Reserve positions (4.9Moz). Given its production and cost structures, sizeable inventory, as well as low levels of hedging, the stock offers excellent leverage to the gold price. We estimate that a 10% increase in gold price would result in a ~38% increase in our valuation. Valuation Our A$1.45 price target is based on 1x forward curve NPV5% for the operating assets net of corporate and other adjustments. For important information, please see the Important Disclosures beginning on page 26 of this document.

Transcript of Seasoned African Campaigner Initiation of Coverage ... · Canaccord Genuity is the global capital...

Resolute Mining Limited

Precious Metals - Producer

Canaccord Genuity is the global capital markets group of Canaccord Genuity Group Inc. (CF : TSX)The recommendations and opinions expressed in this research report accurately reflect the research analyst's personal, independent and objective views about any and allthe companies and securities that are the subject of this report discussed herein.

Australian Equity Research24 November 2016

BUYPRICE TARGET A$1.45Price (24-Nov)Ticker

A$1.20RSG-ASX

52-Week Range (A$): 0.24 - 2.35Avg Daily Vol (M) : 8.0Market Cap (A$M): 881Shares Out. (M) : 737.0Dividend /Shr (A$): 0.02Dividend Yield (%) : 1.4Enterprise Value (A$M): 646NAV /Shr (5%) (A$): 1.44Net Cash (A$M): 235.0P/NAV (x) : 0.83Major Shareholders: ICM

Van Eck

FYE Jun 2016A 2017E 2018E 2019EGold Production(000oz) 315 306 273 305

All in SustainingCost (Gold) (US$ /oz)

895 957 1,039 1,039

EBITDA (A$M) 185.0 188.0 165.0 150.0Net Income (A$M) 212.9 136.3 110.8 68.3

2.5

2

1.5

1

0.5

0

Dec-15

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

RSG

Source:�FactSet

Patrick Chang, CFA | Analyst | Canaccord Genuity (Australia) Ltd. | [email protected] | +61.8.6216.2004Reg Spencer | Analyst | Canaccord Genuity (Australia) Ltd. | [email protected] | +61.2.9263.2701

Initiation of Coverage

Seasoned African CampaignerResolute Mining (RSG) is an international gold producer with FY17 group productionguidance set at >300koz @ AISC A$1,280/oz. Its key assets are the Syama gold minein Mali and the Ravenswood mine in Australia. The company boasts a proud history ingold production (7Moz since the early 1990s), but looking ahead, the company is makingsignificant investment in the next few years in order to transform its existing assets intolong life, scalable operations. The company has been re-rated by the market in CY16,and has now become a serious contender in the +300kozpa peer group (ASX-listed).Whilst the share price discount to NAV is modest at ~20%, the stock remains appealingto investors seeking leverage to the gold price (see below) and / or growth. We initiatecoverage with a BUY recommendation and a A$1.45 target price.Transforming its operations. RSG recently delivered two separate Feasibility Studies(FS) on its Syama Underground and Ravenswood Expansion Projects. The sizeableReserve positions and the recent FS results underpin the potential for RSG to delivertwo scalable operations with some of the longest mine lives amongst the ASX goldproducers. The total project capex directly associated with these two projects in FY17-19is estimated at A$370m (CGe), which we estimate is financeable from RSG’s existingbalance sheet post the recent capital raising and projected cash flow. Whilst the upfrontcapex is relatively onerous and technical risks are acknowledged, post ramp up, thesetwo assets have the potential to deliver >300koz for the next >10 years.Further growth. RSG’s large mineral inventory, prospective geology and recentexploration results support an ability to deliver organic growth, in our view. Its projectpipeline includes the Bibiani project in Ghana, which has the potential to deliver anadditional ~100koz pa production through further technical work. The company hasrecently invested in African juniors including Manas Resources (ASX:MSR | Not rated)and Kilo Gold (TSX:KGL | Not rated). Its expertise at acquiring, developing and operatingAfrican mines could lead to further M&A. In particular, the company’s demonstratedability to operate across different jurisdictions and successfully employ unconventionalmining or processing practices means it has the potential to capitalise on opportunitiesunavailable to many other gold companies.Scale and leverage. RSG boasts scalable Resource (attributable 10.7Moz) and Reservepositions (4.9Moz). Given its production and cost structures, sizeable inventory, aswell as low levels of hedging, the stock offers excellent leverage to the gold price. Weestimate that a 10% increase in gold price would result in a ~38% increase in ourvaluation.

ValuationOur A$1.45 price target is based on 1x forward curve NPV5% for the operating assetsnet of corporate and other adjustments.

For important information, please see the Important Disclosures beginning on page 26 of this document.

2

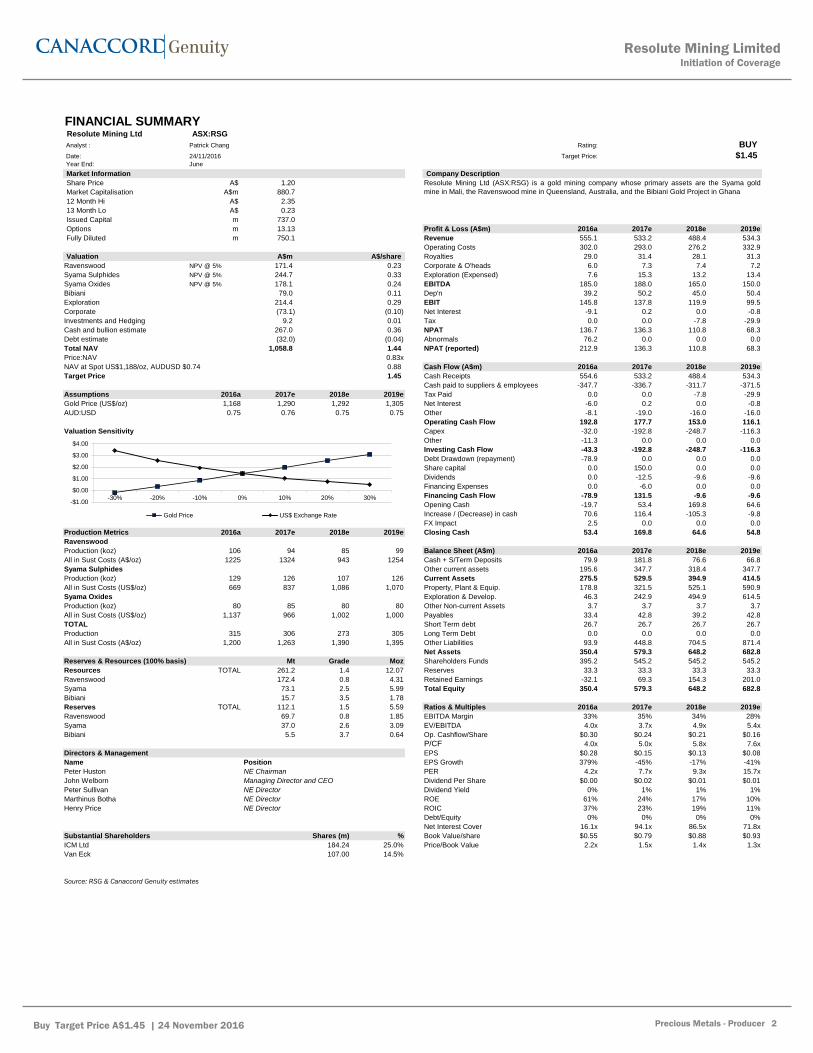

FINANCIAL SUMMARY Resolute Mining Ltd ASX:RSG

Analyst : Patrick Chang Rating:

Date: 24/11/2016 Target Price: $1.45Year End: June

Market Information Company Description

Share Price A$ 1.20

Market Capitalisation A$m 880.7

12 Month Hi A$ 2.35

13 Month Lo A$ 0.23

Issued Capital m 737.0

Options m 13.13 Profit & Loss (A$m) 2016a 2017e 2018e 2019e

Fully Diluted m 750.1 Revenue 555.1 533.2 488.4 534.3

Operating Costs 302.0 293.0 276.2 332.9

Valuation A$m A$/share Royalties 29.0 31.4 28.1 31.3

Ravenswood NPV @ 5% 171.4 0.23 Corporate & O'heads 6.0 7.3 7.4 7.2

Syama Sulphides NPV @ 5% 244.7 0.33 Exploration (Expensed) 7.6 15.3 13.2 13.4

Syama Oxides NPV @ 5% 178.1 0.24 EBITDA 185.0 188.0 165.0 150.0

Bibiani 79.0 0.11 Dep'n 39.2 50.2 45.0 50.4

Exploration 214.4 0.29 EBIT 145.8 137.8 119.9 99.5

Corporate (73.1) (0.10) Net Interest -9.1 0.2 0.0 -0.8

Investments and Hedging 9.2 0.01 Tax 0.0 0.0 -7.8 -29.9

Cash and bullion estimate 267.0 0.36 NPAT 136.7 136.3 110.8 68.3

Debt estimate (32.0) (0.04) Abnormals 76.2 0.0 0.0 0.0

Total NAV 1,058.8 1.44 NPAT (reported) 212.9 136.3 110.8 68.3

Price:NAV 0.83x

NAV at Spot US$1,188/oz, AUDUSD $0.74 0.88 Cash Flow (A$m) 2016a 2017e 2018e 2019e

Target Price 1.45 Cash Receipts 554.6 533.2 488.4 534.3

Cash paid to suppliers & employees -347.7 -336.7 -311.7 -371.5

Assumptions 2016a 2017e 2018e 2019e Tax Paid 0.0 0.0 -7.8 -29.9

Gold Price (US$/oz) 1,168 1,290 1,292 1,305 Net Interest -6.0 0.2 0.0 -0.8

AUD:USD 0.75 0.76 0.75 0.75 Other -8.1 -19.0 -16.0 -16.0

Operating Cash Flow 192.8 177.7 153.0 116.1

Valuation Sensitivity Capex -32.0 -192.8 -248.7 -116.3

Other -11.3 0.0 0.0 0.0

Investing Cash Flow -43.3 -192.8 -248.7 -116.3

Debt Drawdown (repayment) -78.9 0.0 0.0 0.0

Share capital 0.0 150.0 0.0 0.0

Dividends 0.0 -12.5 -9.6 -9.6

Financing Expenses 0.0 -6.0 0.0 0.0

Financing Cash Flow -78.9 131.5 -9.6 -9.6

Opening Cash -19.7 53.4 169.8 64.6

Increase / (Decrease) in cash 70.6 116.4 -105.3 -9.8

FX Impact 2.5 0.0 0.0 0.0

Production Metrics 2016a 2017e 2018e 2019e Closing Cash 53.4 169.8 64.6 54.8

Ravenswood

Production (koz) 106 94 85 99 Balance Sheet (A$m) 2016a 2017e 2018e 2019e

All in Sust Costs (A$/oz) 1225 1324 943 1254 Cash + S/Term Deposits 79.9 181.8 76.6 66.8

Syama Sulphides Other current assets 195.6 347.7 318.4 347.7

Production (koz) 129 126 107 126 Current Assets 275.5 529.5 394.9 414.5

All in Sust Costs (US$/oz) 669 837 1,086 1,070 Property, Plant & Equip. 178.8 321.5 525.1 590.9

Syama Oxides Exploration & Develop. 46.3 242.9 494.9 614.5

Production (koz) 80 85 80 80 Other Non-current Assets 3.7 3.7 3.7 3.7

All in Sust Costs (US$/oz) 1,137 966 1,002 1,000 Payables 33.4 42.8 39.2 42.8

TOTAL Short Term debt 26.7 26.7 26.7 26.7

Production 315 306 273 305 Long Term Debt 0.0 0.0 0.0 0.0

All in Sust Costs (A$/oz) 1,200 1,263 1,390 1,395 Other Liabilities 93.9 448.8 704.5 871.4

Net Assets 350.4 579.3 648.2 682.8

Reserves & Resources (100% basis) Mt Grade Moz Shareholders Funds 395.2 545.2 545.2 545.2

Resources TOTAL 261.2 1.4 12.07 Reserves 33.3 33.3 33.3 33.3

Ravenswood 172.4 0.8 4.31 Retained Earnings -32.1 69.3 154.3 201.0

Syama 73.1 2.5 5.99 Total Equity 350.4 579.3 648.2 682.8

Bibiani 15.7 3.5 1.78

Reserves TOTAL 112.1 1.5 5.59 Ratios & Multiples 2016a 2017e 2018e 2019e

Ravenswood 69.7 0.8 1.85 EBITDA Margin 33% 35% 34% 28%

Syama 37.0 2.6 3.09 EV/EBITDA 4.0x 3.7x 4.9x 5.4x

Bibiani 5.5 3.7 0.64 Op. Cashflow/Share $0.30 $0.24 $0.21 $0.16

P/CF 4.0x 5.0x 5.8x 7.6x

Directors & Management EPS $0.28 $0.15 $0.13 $0.08

Name Position EPS Growth 379% -45% -17% -41%

Peter Huston NE Chairman PER 4.2x 7.7x 9.3x 15.7x

John Welborn Managing Director and CEO Dividend Per Share $0.00 $0.02 $0.01 $0.01

Peter Sullivan NE Director Dividend Yield 0% 1% 1% 1%

Marthinus Botha NE Director ROE 61% 24% 17% 10%

Henry Price NE Director ROIC 37% 23% 19% 11%

Debt/Equity 0% 0% 0% 0%

Net Interest Cover 16.1x 94.1x 86.5x 71.8x

Substantial Shareholders Shares (m) % Book Value/share $0.55 $0.79 $0.88 $0.93

ICM Ltd 184.24 25.0% Price/Book Value 2.2x 1.5x 1.4x 1.3x

Van Eck 107.00 14.5%

Source: RSG & Canaccord Genuity estimates

Resolute Mining Ltd (ASX:RSG) is a gold mining company whose primary assets are the Syama gold

mine in Mali, the Ravenswood mine in Queensland, Australia, and the Bibiani Gold Project in Ghana

BUY

-$1.00

$0.00

$1.00

$2.00

$3.00

$4.00

-30% -20% -10% 0% 10% 20% 30%

Gold Price US$ Exchange Rate

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 2

3

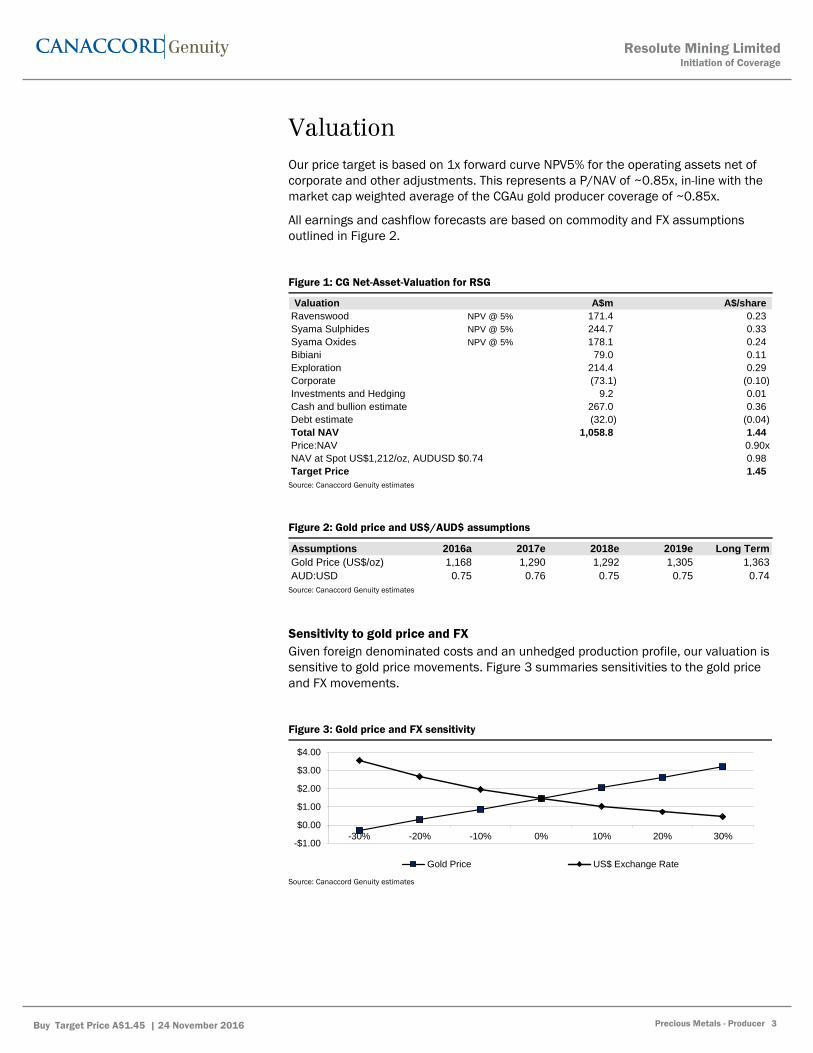

Valuation

Our price target is based on 1x forward curve NPV5% for the operating assets net of

corporate and other adjustments. This represents a P/NAV of ~0.85x, in-line with the

market cap weighted average of the CGAu gold producer coverage of ~0.85x.

All earnings and cashflow forecasts are based on commodity and FX assumptions

outlined in Figure 2.

Figure 1: CG Net-Asset-Valuation for RSG

Source: Canaccord Genuity estimates

Figure 2: Gold price and US$/AUD$ assumptions

Source: Canaccord Genuity estimates

Sensitivity to gold price and FX

Given foreign denominated costs and an unhedged production profile, our valuation is

sensitive to gold price movements. Figure 3 summaries sensitivities to the gold price

and FX movements.

Figure 3: Gold price and FX sensitivity

Source: Canaccord Genuity estimates

Valuation A$m A$/share

Ravenswood NPV @ 5% 171.4 0.23

Syama Sulphides NPV @ 5% 244.7 0.33

Syama Oxides NPV @ 5% 178.1 0.24

Bibiani 79.0 0.11

Exploration 214.4 0.29

Corporate (73.1) (0.10)

Investments and Hedging 9.2 0.01

Cash and bullion estimate 267.0 0.36

Debt estimate (32.0) (0.04)

Total NAV 1,058.8 1.44

Price:NAV 0.90x

NAV at Spot US$1,212/oz, AUDUSD $0.74 0.98

Target Price 1.45

Assumptions 2016a 2017e 2018e 2019e Long Term

Gold Price (US$/oz) 1,168 1,290 1,292 1,305 1,363

AUD:USD 0.75 0.76 0.75 0.75 0.74

-$1.00

$0.00

$1.00

$2.00

$3.00

$4.00

-30% -20% -10% 0% 10% 20% 30%

Gold Price US$ Exchange Rate

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 3

4

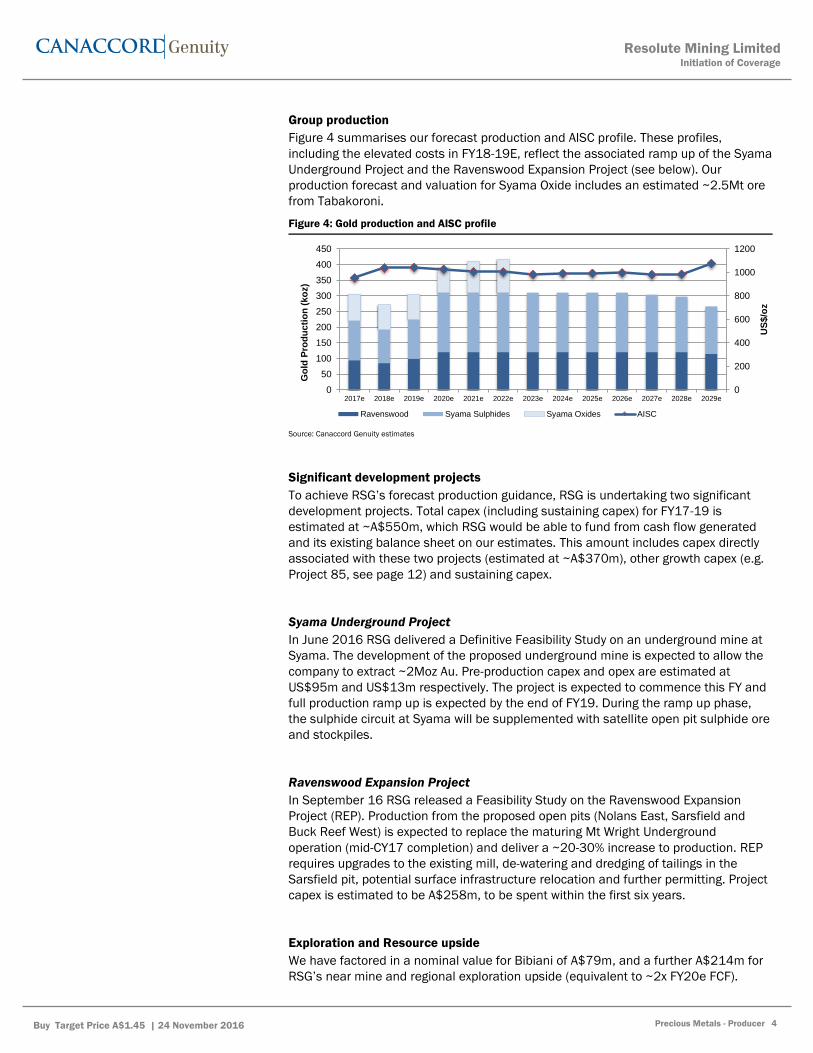

Group production

Figure 4 summarises our forecast production and AISC profile. These profiles,

including the elevated costs in FY18-19E, reflect the associated ramp up of the Syama

Underground Project and the Ravenswood Expansion Project (see below). Our

production forecast and valuation for Syama Oxide includes an estimated ~2.5Mt ore

from Tabakoroni.

Figure 4: Gold production and AISC profile

Source: Canaccord Genuity estimates

Significant development projects

To achieve RSG’s forecast production guidance, RSG is undertaking two significant

development projects. Total capex (including sustaining capex) for FY17-19 is

estimated at ~A$550m, which RSG would be able to fund from cash flow generated

and its existing balance sheet on our estimates. This amount includes capex directly

associated with these two projects (estimated at ~A$370m), other growth capex (e.g.

Project 85, see page 12) and sustaining capex.

Syama Underground Project

In June 2016 RSG delivered a Definitive Feasibility Study on an underground mine at

Syama. The development of the proposed underground mine is expected to allow the

company to extract ~2Moz Au. Pre-production capex and opex are estimated at

US$95m and US$13m respectively. The project is expected to commence this FY and

full production ramp up is expected by the end of FY19. During the ramp up phase,

the sulphide circuit at Syama will be supplemented with satellite open pit sulphide ore

and stockpiles.

Ravenswood Expansion Project

In September 16 RSG released a Feasibility Study on the Ravenswood Expansion

Project (REP). Production from the proposed open pits (Nolans East, Sarsfield and

Buck Reef West) is expected to replace the maturing Mt Wright Underground

operation (mid-CY17 completion) and deliver a ~20-30% increase to production. REP

requires upgrades to the existing mill, de-watering and dredging of tailings in the

Sarsfield pit, potential surface infrastructure relocation and further permitting. Project

capex is estimated to be A$258m, to be spent within the first six years.

Exploration and Resource upside

We have factored in a nominal value for Bibiani of A$79m, and a further A$214m for

RSG’s near mine and regional exploration upside (equivalent to ~2x FY20e FCF).

0

200

400

600

800

1000

1200

0

50

100

150

200

250

300

350

400

450

2017e 2018e 2019e 2020e 2021e 2022e 2023e 2024e 2025e 2026e 2027e 2028e 2029e

US

$/o

z

Go

ld P

rod

uc

tio

n (

ko

z)

Ravenswood Syama Sulphides Syama Oxides AISC

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 4

5

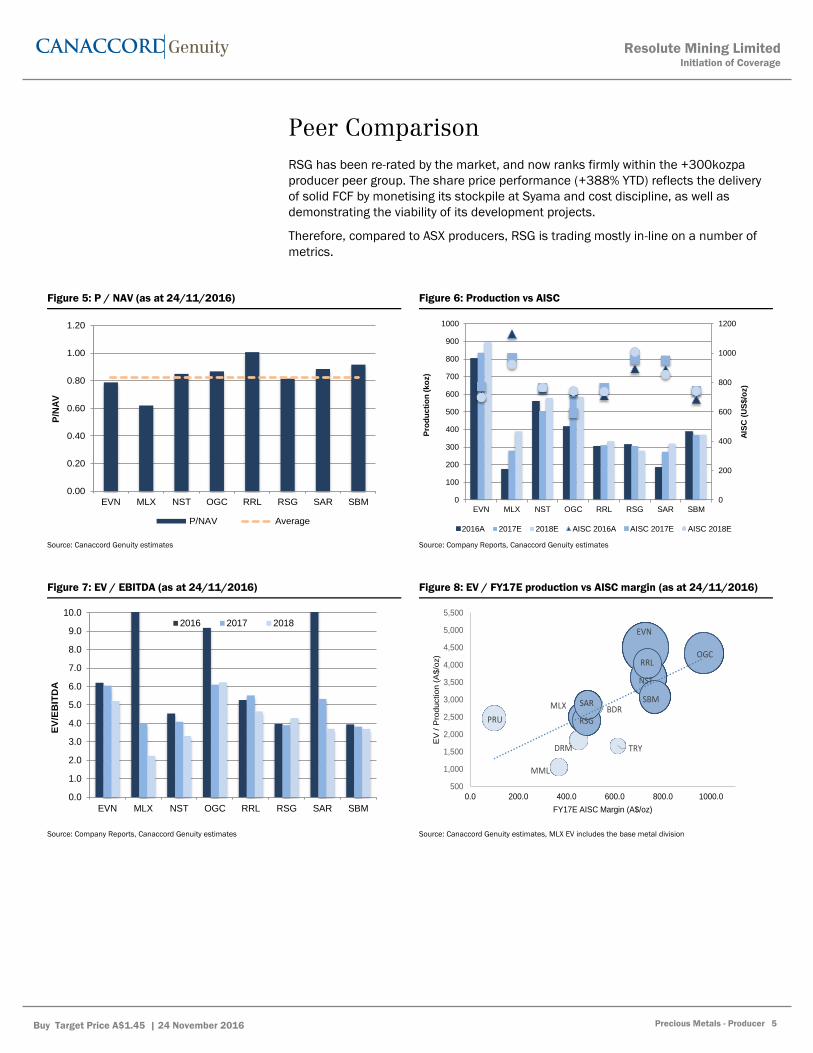

Peer Comparison

RSG has been re-rated by the market, and now ranks firmly within the +300kozpa

producer peer group. The share price performance (+388% YTD) reflects the delivery

of solid FCF by monetising its stockpile at Syama and cost discipline, as well as

demonstrating the viability of its development projects.

Therefore, compared to ASX producers, RSG is trading mostly in-line on a number of

metrics.

Figure 5: P / NAV (as at 24/11/2016) Figure 6: Production vs AISC

Source: Canaccord Genuity estimates Source: Company Reports, Canaccord Genuity estimates

Figure 7: EV / EBITDA (as at 24/11/2016) Figure 8: EV / FY17E production vs AISC margin (as at 24/11/2016)

Source: Company Reports, Canaccord Genuity estimates Source: Canaccord Genuity estimates, MLX EV includes the base metal division

0.00

0.20

0.40

0.60

0.80

1.00

1.20

EVN MLX NST OGC RRL RSG SAR SBM

P/N

AV

P/NAV Average

0

200

400

600

800

1000

1200

0

100

200

300

400

500

600

700

800

900

1000

EVN MLX NST OGC RRL RSG SAR SBM

AIS

C (

US

$/o

z)

Pro

du

cti

on

(ko

z)

2016A 2017E 2018E AISC 2016A AISC 2017E AISC 2018E

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

EVN MLX NST OGC RRL RSG SAR SBM

EV

/EB

ITD

A

2016 2017 2018

BDR

DRM

EVN

MLX

MML

NST

OGC

PRU

RRL

RSG

SAR SBM

TRY

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

0.0 200.0 400.0 600.0 800.0 1000.0

EV

/ P

roductio

n (

A$/o

z)

FY17E AISC Margin (A$/oz)

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 5

6

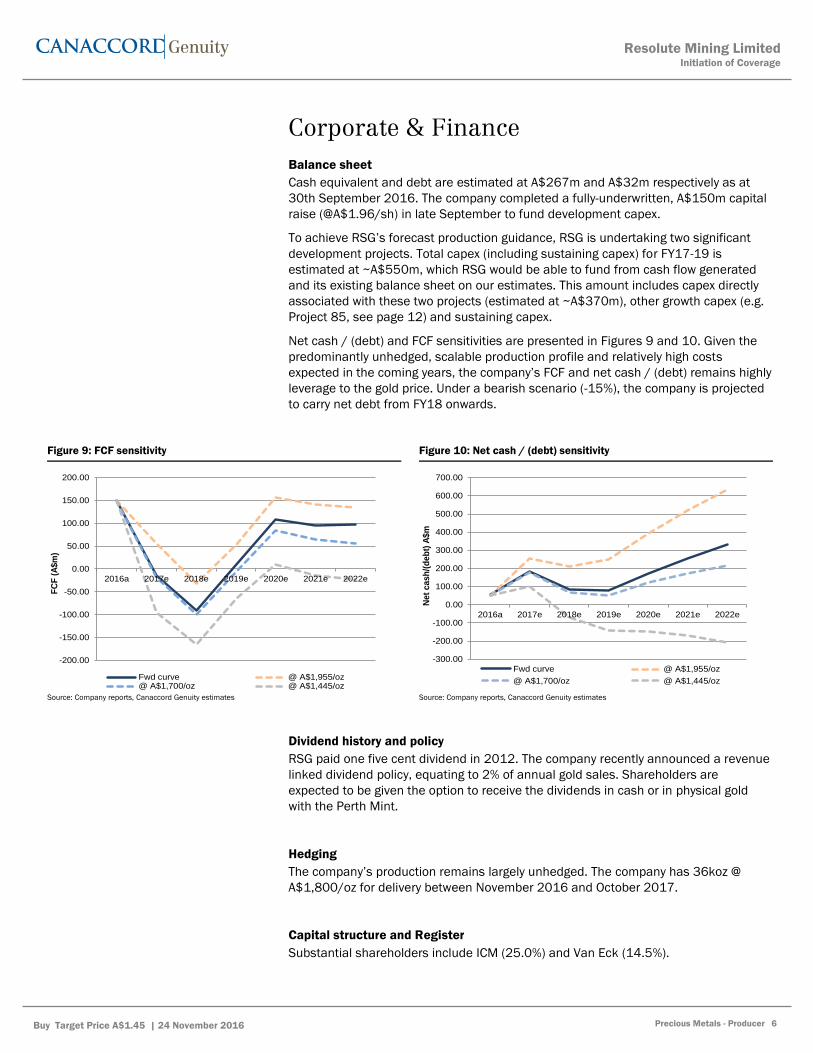

Corporate & Finance

Balance sheet

Cash equivalent and debt are estimated at A$267m and A$32m respectively as at

30th September 2016. The company completed a fully-underwritten, A$150m capital

raise (@A$1.96/sh) in late September to fund development capex.

To achieve RSG’s forecast production guidance, RSG is undertaking two significant

development projects. Total capex (including sustaining capex) for FY17-19 is

estimated at ~A$550m, which RSG would be able to fund from cash flow generated

and its existing balance sheet on our estimates. This amount includes capex directly

associated with these two projects (estimated at ~A$370m), other growth capex (e.g.

Project 85, see page 12) and sustaining capex.

Net cash / (debt) and FCF sensitivities are presented in Figures 9 and 10. Given the

predominantly unhedged, scalable production profile and relatively high costs

expected in the coming years, the company’s FCF and net cash / (debt) remains highly

leverage to the gold price. Under a bearish scenario (-15%), the company is projected

to carry net debt from FY18 onwards.

Figure 9: FCF sensitivity Figure 10: Net cash / (debt) sensitivity

Source: Company reports, Canaccord Genuity estimates Source: Company reports, Canaccord Genuity estimates

Dividend history and policy

RSG paid one five cent dividend in 2012. The company recently announced a revenue

linked dividend policy, equating to 2% of annual gold sales. Shareholders are

expected to be given the option to receive the dividends in cash or in physical gold

with the Perth Mint.

Hedging

The company’s production remains largely unhedged. The company has 36koz @

A$1,800/oz for delivery between November 2016 and October 2017.

Capital structure and Register

Substantial shareholders include ICM (25.0%) and Van Eck (14.5%).

-200.00

-150.00

-100.00

-50.00

0.00

50.00

100.00

150.00

200.00

2016a 2017e 2018e 2019e 2020e 2021e 2022e

FC

F (

A$m

)

Fwd curve @ A$1,955/oz@ A$1,700/oz @ A$1,445/oz

-300.00

-200.00

-100.00

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

2016a 2017e 2018e 2019e 2020e 2021e 2022e

Net

cash

/(d

eb

t) A

$m

Fwd curve @ A$1,955/oz

@ A$1,700/oz @ A$1,445/oz

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 6

7

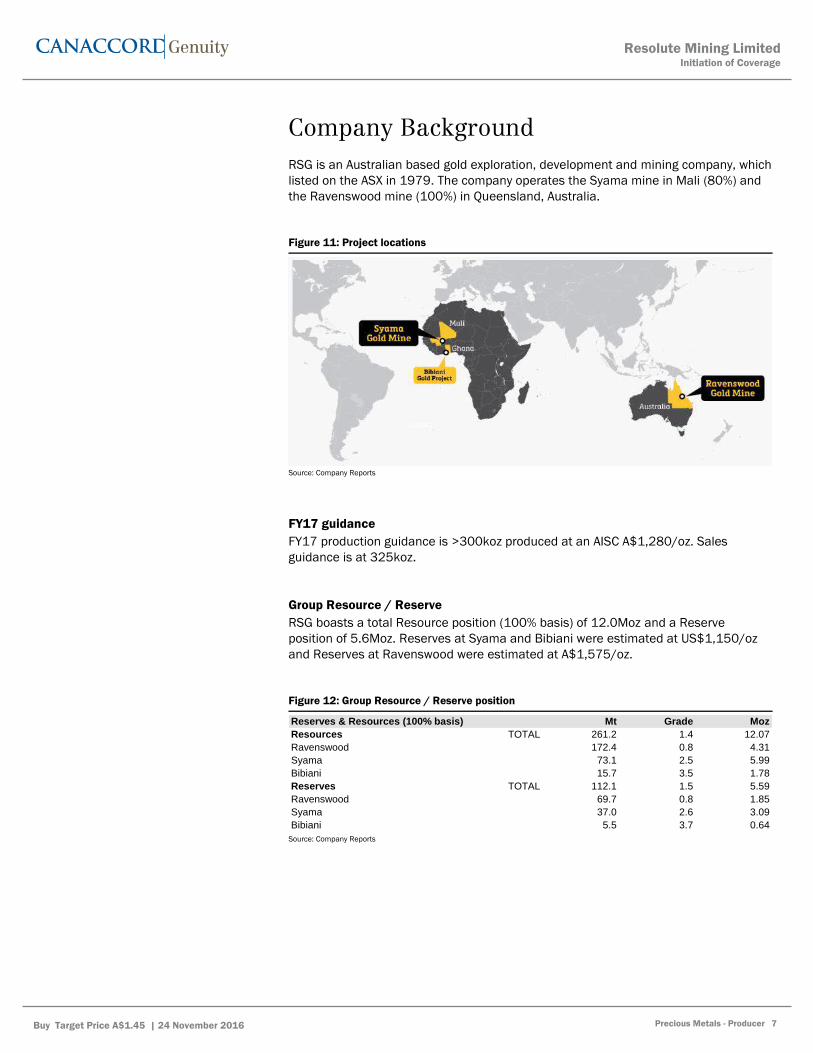

Company Background

RSG is an Australian based gold exploration, development and mining company, which

listed on the ASX in 1979. The company operates the Syama mine in Mali (80%) and

the Ravenswood mine (100%) in Queensland, Australia.

Figure 11: Project locations

Source: Company Reports

FY17 guidance

FY17 production guidance is >300koz produced at an AISC A$1,280/oz. Sales

guidance is at 325koz.

Group Resource / Reserve

RSG boasts a total Resource position (100% basis) of 12.0Moz and a Reserve

position of 5.6Moz. Reserves at Syama and Bibiani were estimated at US$1,150/oz

and Reserves at Ravenswood were estimated at A$1,575/oz.

Figure 12: Group Resource / Reserve position

Source: Company Reports

Reserves & Resources (100% basis) Mt Grade Moz

Resources TOTAL 261.2 1.4 12.07

Ravenswood 172.4 0.8 4.31

Syama 73.1 2.5 5.99

Bibiani 15.7 3.5 1.78

Reserves TOTAL 112.1 1.5 5.59

Ravenswood 69.7 0.8 1.85

Syama 37.0 2.6 3.09

Bibiani 5.5 3.7 0.64

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 7

8

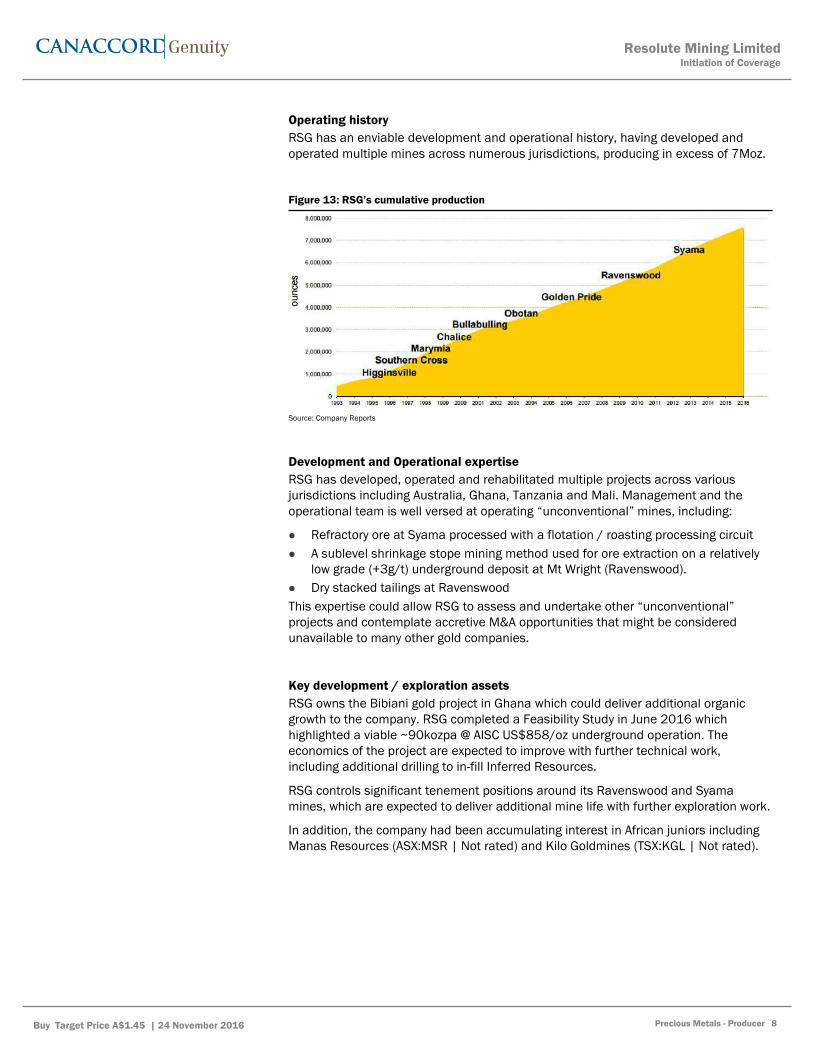

Operating history

RSG has an enviable development and operational history, having developed and

operated multiple mines across numerous jurisdictions, producing in excess of 7Moz.

Figure 13: RSG’s cumulative production

Source: Company Reports

Development and Operational expertise

RSG has developed, operated and rehabilitated multiple projects across various

jurisdictions including Australia, Ghana, Tanzania and Mali. Management and the

operational team is well versed at operating “unconventional” mines, including:

Refractory ore at Syama processed with a flotation / roasting processing circuit

A sublevel shrinkage stope mining method used for ore extraction on a relatively

low grade (+3g/t) underground deposit at Mt Wright (Ravenswood).

Dry stacked tailings at Ravenswood

This expertise could allow RSG to assess and undertake other “unconventional”

projects and contemplate accretive M&A opportunities that might be considered

unavailable to many other gold companies.

Key development / exploration assets

RSG owns the Bibiani gold project in Ghana which could deliver additional organic

growth to the company. RSG completed a Feasibility Study in June 2016 which

highlighted a viable ~90kozpa @ AISC US$858/oz underground operation. The

economics of the project are expected to improve with further technical work,

including additional drilling to in-fill Inferred Resources.

RSG controls significant tenement positions around its Ravenswood and Syama

mines, which are expected to deliver additional mine life with further exploration work.

In addition, the company had been accumulating interest in African juniors including

Manas Resources (ASX:MSR | Not rated) and Kilo Goldmines (TSX:KGL | Not rated).

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 8

9

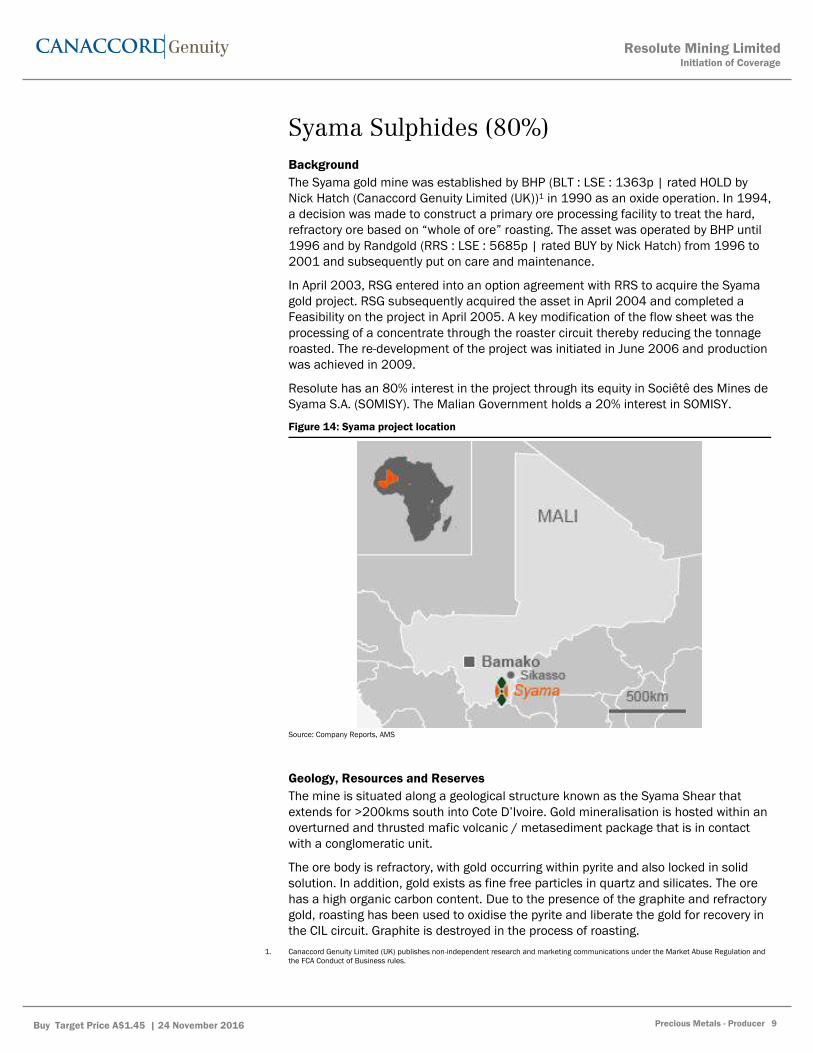

Syama Sulphides (80%)

Background

The Syama gold mine was established by BHP (BLT : LSE : 1363p | rated HOLD by

Nick Hatch (Canaccord Genuity Limited (UK))1 in 1990 as an oxide operation. In 1994,

a decision was made to construct a primary ore processing facility to treat the hard,

refractory ore based on “whole of ore” roasting. The asset was operated by BHP until

1996 and by Randgold (RRS : LSE : 5685p | rated BUY by Nick Hatch) from 1996 to

2001 and subsequently put on care and maintenance.

In April 2003, RSG entered into an option agreement with RRS to acquire the Syama

gold project. RSG subsequently acquired the asset in April 2004 and completed a

Feasibility on the project in April 2005. A key modification of the flow sheet was the

processing of a concentrate through the roaster circuit thereby reducing the tonnage

roasted. The re-development of the project was initiated in June 2006 and production

was achieved in 2009.

Resolute has an 80% interest in the project through its equity in Sociêtê des Mines de

Syama S.A. (SOMISY). The Malian Government holds a 20% interest in SOMISY.

Figure 14: Syama project location

Source: Company Reports, AMS

Geology, Resources and Reserves

The mine is situated along a geological structure known as the Syama Shear that

extends for >200kms south into Cote D’Ivoire. Gold mineralisation is hosted within an

overturned and thrusted mafic volcanic / metasediment package that is in contact

with a conglomeratic unit.

The ore body is refractory, with gold occurring within pyrite and also locked in solid

solution. In addition, gold exists as fine free particles in quartz and silicates. The ore

has a high organic carbon content. Due to the presence of the graphite and refractory

gold, roasting has been used to oxidise the pyrite and liberate the gold for recovery in

the CIL circuit. Graphite is destroyed in the process of roasting.

1. Canaccord Genuity Limited (UK) publishes non-independent research and marketing communications under the Market Abuse Regulation and

the FCA Conduct of Business rules.

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 9

10

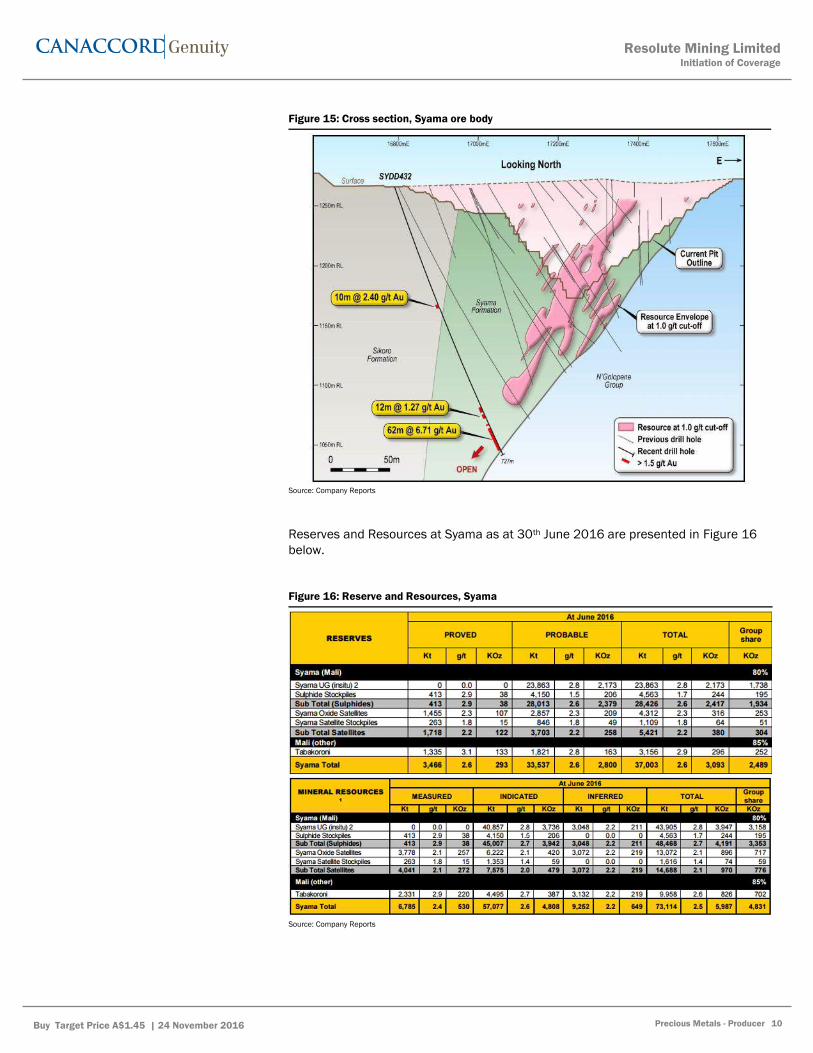

Figure 15: Cross section, Syama ore body

Source: Company Reports

Reserves and Resources at Syama as at 30th June 2016 are presented in Figure 16

below.

Figure 16: Reserve and Resources, Syama

Source: Company Reports

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 10

11

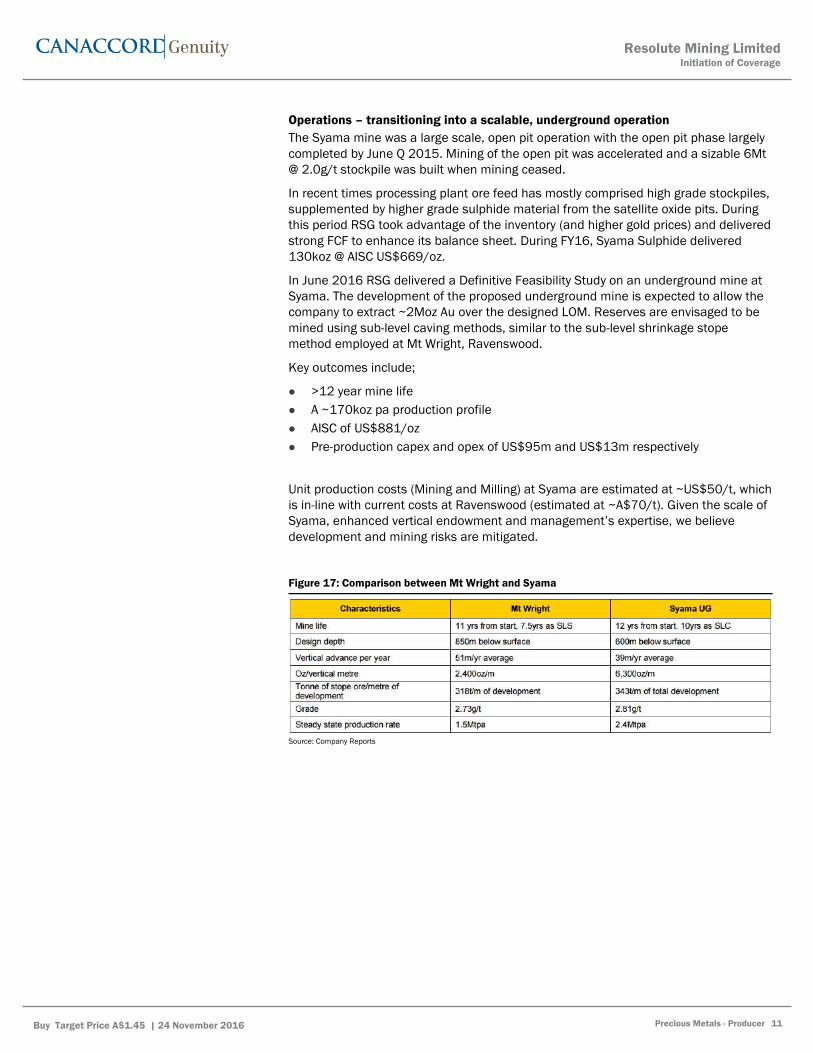

Operations – transitioning into a scalable, underground operation

The Syama mine was a large scale, open pit operation with the open pit phase largely

completed by June Q 2015. Mining of the open pit was accelerated and a sizable 6Mt

@ 2.0g/t stockpile was built when mining ceased.

In recent times processing plant ore feed has mostly comprised high grade stockpiles,

supplemented by higher grade sulphide material from the satellite oxide pits. During

this period RSG took advantage of the inventory (and higher gold prices) and delivered

strong FCF to enhance its balance sheet. During FY16, Syama Sulphide delivered

130koz @ AISC US$669/oz.

In June 2016 RSG delivered a Definitive Feasibility Study on an underground mine at

Syama. The development of the proposed underground mine is expected to allow the

company to extract ~2Moz Au over the designed LOM. Reserves are envisaged to be

mined using sub-level caving methods, similar to the sub-level shrinkage stope

method employed at Mt Wright, Ravenswood.

Key outcomes include;

>12 year mine life

A ~170koz pa production profile

AISC of US$881/oz

Pre-production capex and opex of US$95m and US$13m respectively

Unit production costs (Mining and Milling) at Syama are estimated at ~US$50/t, which

is in-line with current costs at Ravenswood (estimated at ~A$70/t). Given the scale of

Syama, enhanced vertical endowment and management’s expertise, we believe

development and mining risks are mitigated.

Figure 17: Comparison between Mt Wright and Syama

Source: Company Reports

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 11

12

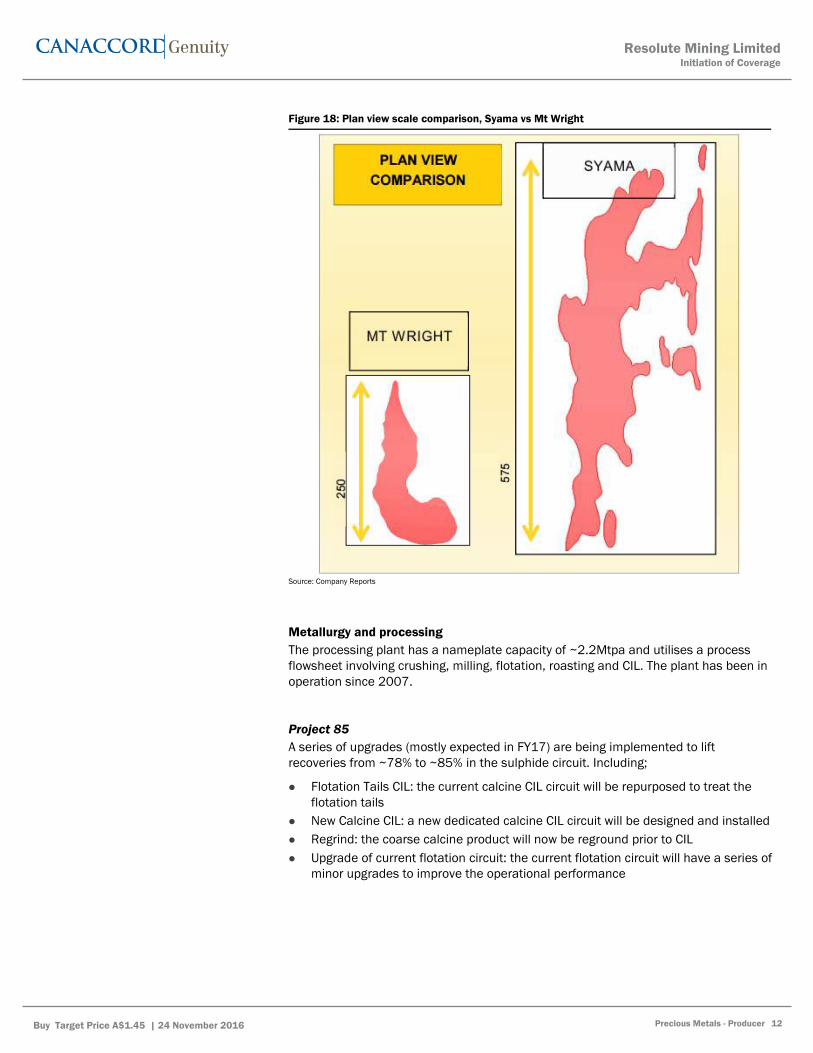

Figure 18: Plan view scale comparison, Syama vs Mt Wright

Source: Company Reports

Metallurgy and processing

The processing plant has a nameplate capacity of ~2.2Mtpa and utilises a process

flowsheet involving crushing, milling, flotation, roasting and CIL. The plant has been in

operation since 2007.

Project 85

A series of upgrades (mostly expected in FY17) are being implemented to lift

recoveries from ~78% to ~85% in the sulphide circuit. Including;

Flotation Tails CIL: the current calcine CIL circuit will be repurposed to treat the

flotation tails

New Calcine CIL: a new dedicated calcine CIL circuit will be designed and installed

Regrind: the coarse calcine product will now be reground prior to CIL

Upgrade of current flotation circuit: the current flotation circuit will have a series of

minor upgrades to improve the operational performance

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 12

13

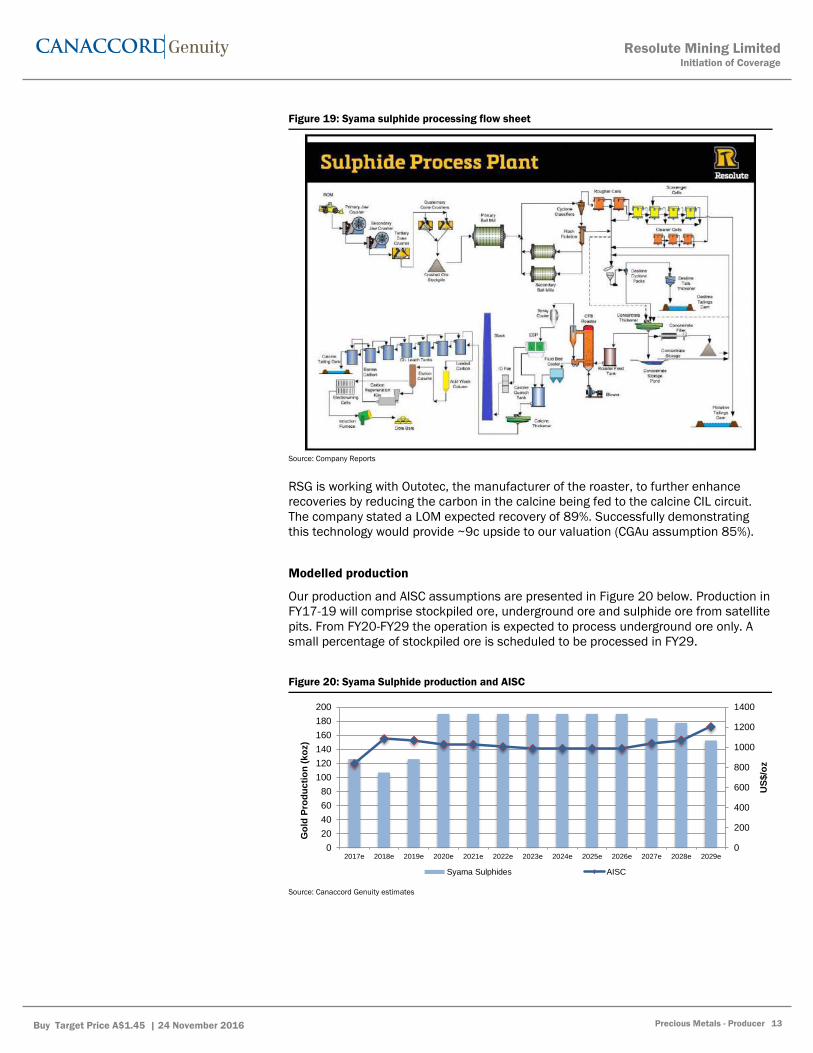

Figure 19: Syama sulphide processing flow sheet

Source: Company Reports

RSG is working with Outotec, the manufacturer of the roaster, to further enhance

recoveries by reducing the carbon in the calcine being fed to the calcine CIL circuit.

The company stated a LOM expected recovery of 89%. Successfully demonstrating

this technology would provide ~9c upside to our valuation (CGAu assumption 85%).

Modelled production

Our production and AISC assumptions are presented in Figure 20 below. Production in

FY17-19 will comprise stockpiled ore, underground ore and sulphide ore from satellite

pits. From FY20-FY29 the operation is expected to process underground ore only. A

small percentage of stockpiled ore is scheduled to be processed in FY29.

Figure 20: Syama Sulphide production and AISC

Source: Canaccord Genuity estimates

0

200

400

600

800

1000

1200

1400

0

20

40

60

80

100

120

140

160

180

200

2017e 2018e 2019e 2020e 2021e 2022e 2023e 2024e 2025e 2026e 2027e 2028e 2029e

US

$/o

z

Go

ld P

rod

uc

tio

n (

ko

z)

Syama Sulphides AISC

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 13

14

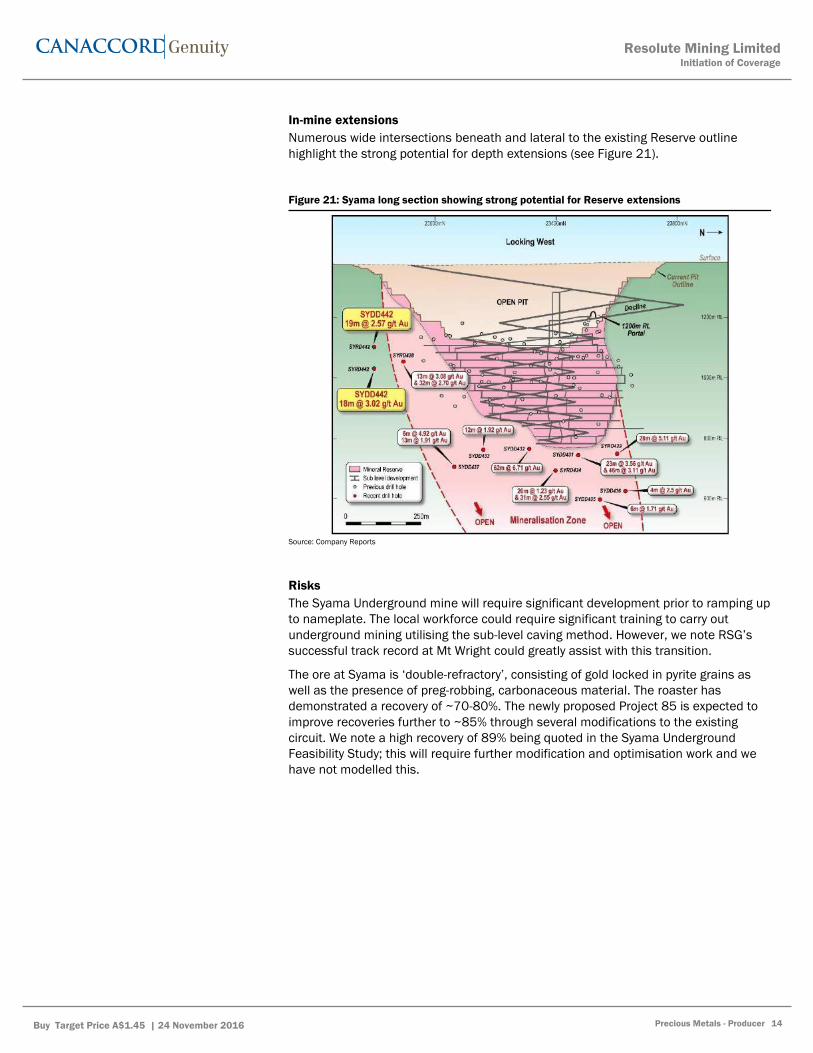

In-mine extensions

Numerous wide intersections beneath and lateral to the existing Reserve outline

highlight the strong potential for depth extensions (see Figure 21).

Figure 21: Syama long section showing strong potential for Reserve extensions

Source: Company Reports

Risks

The Syama Underground mine will require significant development prior to ramping up

to nameplate. The local workforce could require significant training to carry out

underground mining utilising the sub-level caving method. However, we note RSG’s

successful track record at Mt Wright could greatly assist with this transition.

The ore at Syama is ‘double-refractory’, consisting of gold locked in pyrite grains as

well as the presence of preg-robbing, carbonaceous material. The roaster has

demonstrated a recovery of ~70-80%. The newly proposed Project 85 is expected to

improve recoveries further to ~85% through several modifications to the existing

circuit. We note a high recovery of 89% being quoted in the Syama Underground

Feasibility Study; this will require further modification and optimisation work and we

have not modelled this.

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 14

15

Syama Oxides

Background

In mid-2012, RSG completed a Definitive Feasibility Study on the multifaceted

expansion of the Syama operation, which included an independent, parallel, ~1Mtpa

oxide circuit. This circuit would be utilised to process the substantial oxide Resource

at Syama and satellite deposits and increase site output by ~70koz pa.

Start-up capex of the project was estimated by the company at US$123m. The circuit

was completed on budget and ahead of schedule. It is currently operating at

~1.3Mtpa vs the initial nameplate capacity of 1.0Mtpa.

Operation

The operation utilises conventional open pit mining methods. Load and haul, drill and

blast, grade control drilling are contracted to Ausdrill (ASX:ASL | Not rated) until

August 2018.

After a period of elevated waste material movement, CGAu is modelling a modest

average stripping ratio of ~5:1 for the next twelve Qs.

The oxide processing circuit is expected to be suitable for a large percentage of oxide

material at Tabakoroni, which features Reserves of 296koz @ 2.9g/t. Our modelling

reflects the expected processing of this material through the oxide circuit.

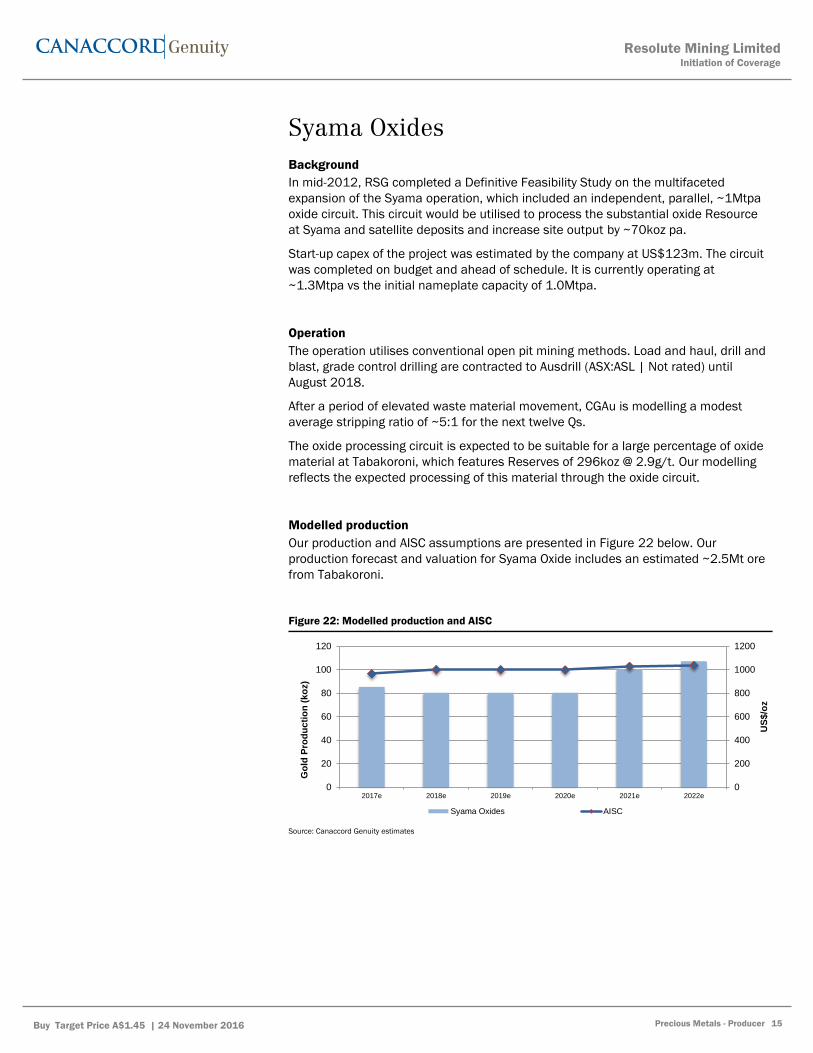

Modelled production

Our production and AISC assumptions are presented in Figure 22 below. Our

production forecast and valuation for Syama Oxide includes an estimated ~2.5Mt ore

from Tabakoroni.

Figure 22: Modelled production and AISC

Source: Canaccord Genuity estimates

0

200

400

600

800

1000

1200

0

20

40

60

80

100

120

2017e 2018e 2019e 2020e 2021e 2022e

US

$/o

z

Go

ld P

rod

uc

tio

n (

ko

z)

Syama Oxides AISC

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 15

16

Ravenswood

Background and operational history

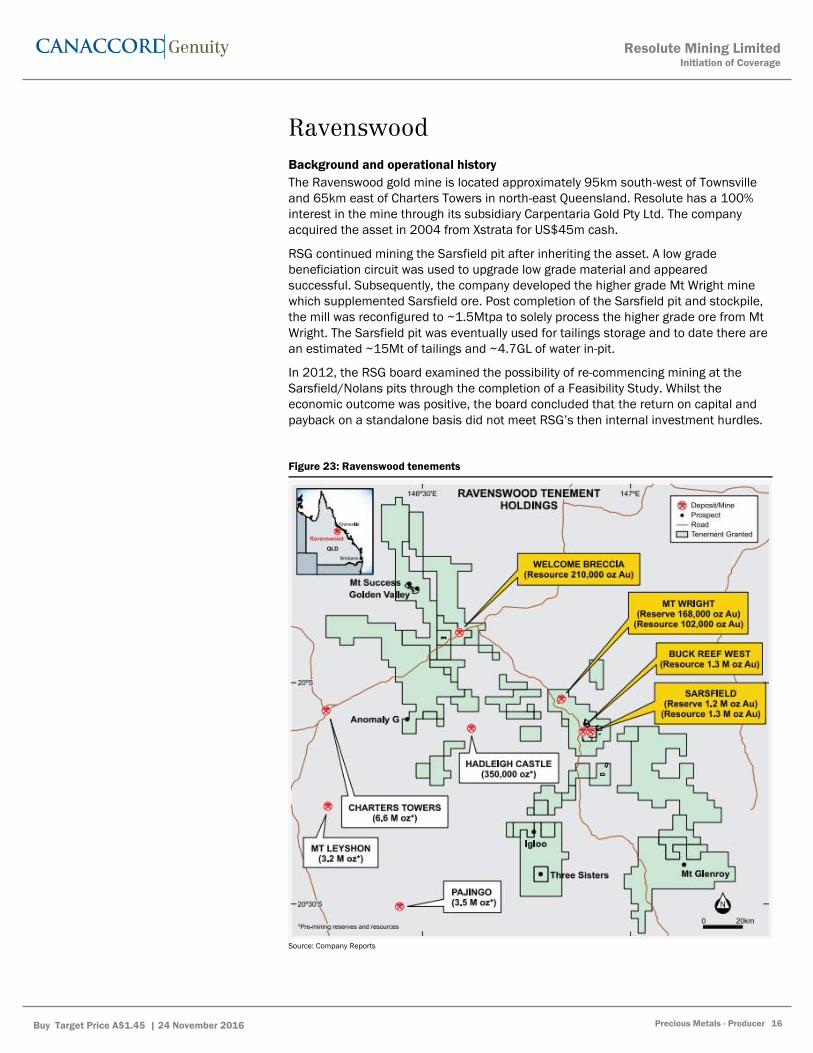

The Ravenswood gold mine is located approximately 95km south-west of Townsville

and 65km east of Charters Towers in north-east Queensland. Resolute has a 100%

interest in the mine through its subsidiary Carpentaria Gold Pty Ltd. The company

acquired the asset in 2004 from Xstrata for US$45m cash.

RSG continued mining the Sarsfield pit after inheriting the asset. A low grade

beneficiation circuit was used to upgrade low grade material and appeared

successful. Subsequently, the company developed the higher grade Mt Wright mine

which supplemented Sarsfield ore. Post completion of the Sarsfield pit and stockpile,

the mill was reconfigured to ~1.5Mtpa to solely process the higher grade ore from Mt

Wright. The Sarsfield pit was eventually used for tailings storage and to date there are

an estimated ~15Mt of tailings and ~4.7GL of water in-pit.

In 2012, the RSG board examined the possibility of re-commencing mining at the

Sarsfield/Nolans pits through the completion of a Feasibility Study. Whilst the

economic outcome was positive, the board concluded that the return on capital and

payback on a standalone basis did not meet RSG’s then internal investment hurdles.

Figure 23: Ravenswood tenements

Source: Company Reports

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 16

17

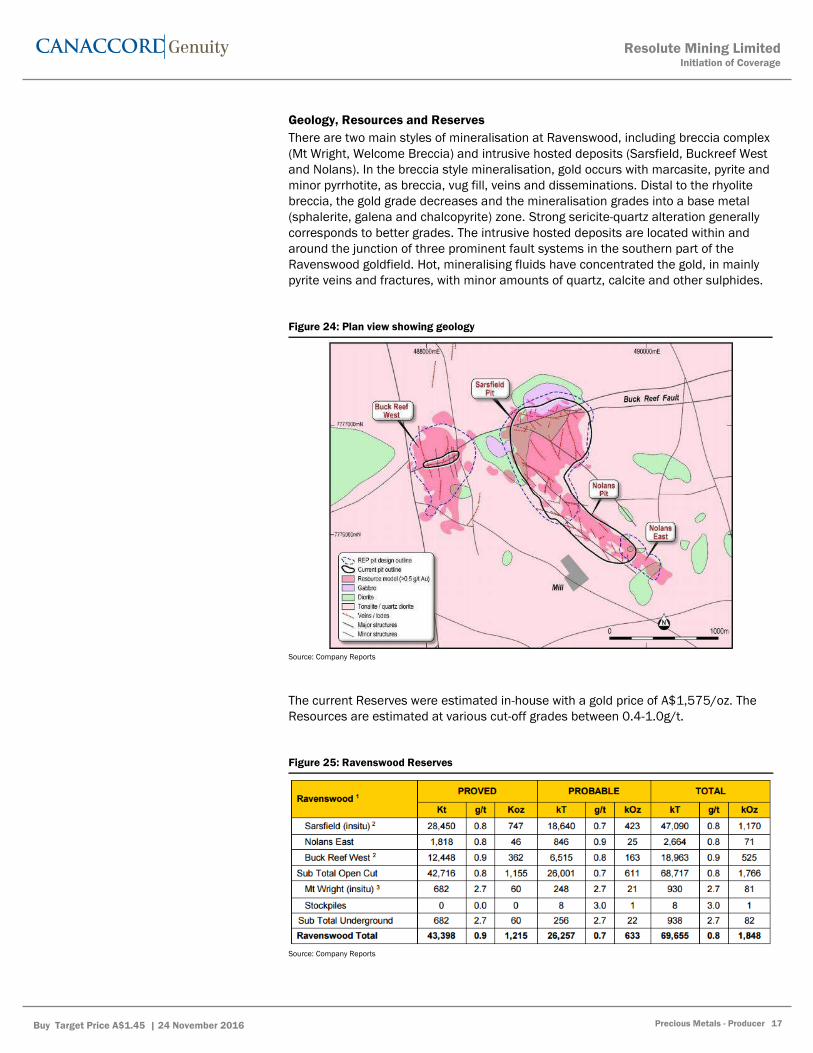

Geology, Resources and Reserves

There are two main styles of mineralisation at Ravenswood, including breccia complex

(Mt Wright, Welcome Breccia) and intrusive hosted deposits (Sarsfield, Buckreef West

and Nolans). In the breccia style mineralisation, gold occurs with marcasite, pyrite and

minor pyrrhotite, as breccia, vug fill, veins and disseminations. Distal to the rhyolite

breccia, the gold grade decreases and the mineralisation grades into a base metal

(sphalerite, galena and chalcopyrite) zone. Strong sericite-quartz alteration generally

corresponds to better grades. The intrusive hosted deposits are located within and

around the junction of three prominent fault systems in the southern part of the

Ravenswood goldfield. Hot, mineralising fluids have concentrated the gold, in mainly

pyrite veins and fractures, with minor amounts of quartz, calcite and other sulphides.

Figure 24: Plan view showing geology

Source: Company Reports

The current Reserves were estimated in-house with a gold price of A$1,575/oz. The

Resources are estimated at various cut-off grades between 0.4-1.0g/t.

Figure 25: Ravenswood Reserves

Source: Company Reports

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 17

18

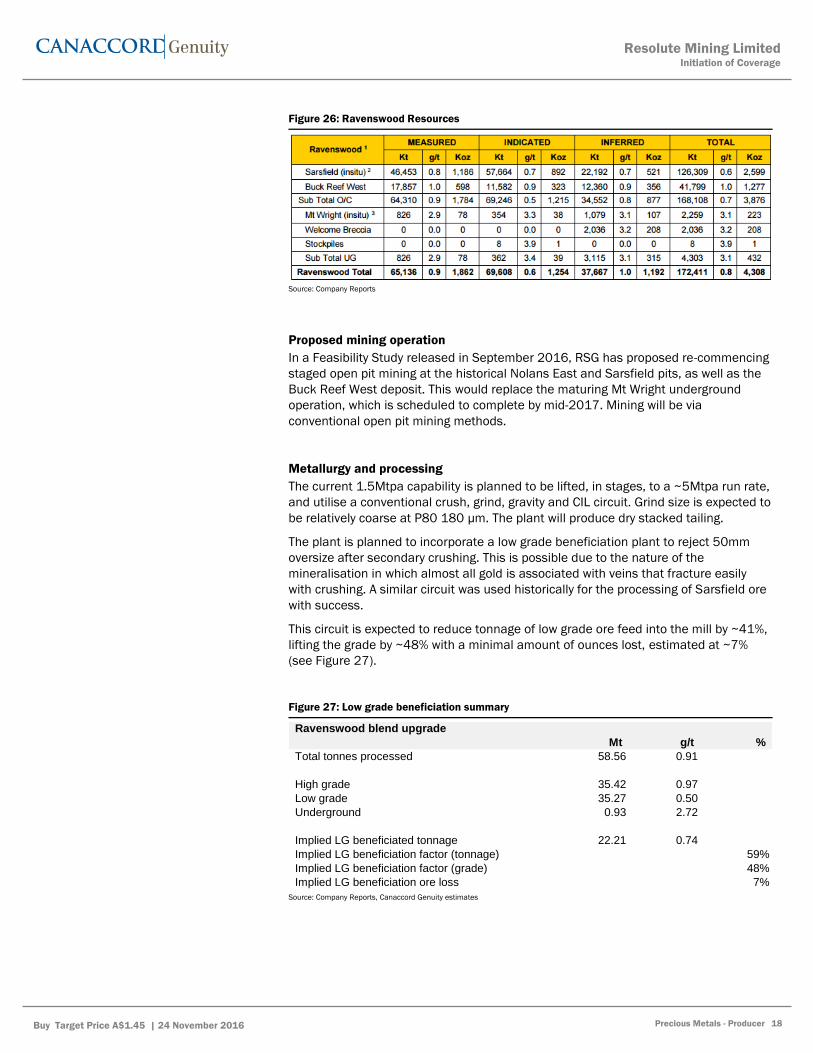

Figure 26: Ravenswood Resources

Source: Company Reports

Proposed mining operation

In a Feasibility Study released in September 2016, RSG has proposed re-commencing

staged open pit mining at the historical Nolans East and Sarsfield pits, as well as the

Buck Reef West deposit. This would replace the maturing Mt Wright underground

operation, which is scheduled to complete by mid-2017. Mining will be via

conventional open pit mining methods.

Metallurgy and processing

The current 1.5Mtpa capability is planned to be lifted, in stages, to a ~5Mtpa run rate,

and utilise a conventional crush, grind, gravity and CIL circuit. Grind size is expected to

be relatively coarse at P80 180 µm. The plant will produce dry stacked tailing.

The plant is planned to incorporate a low grade beneficiation plant to reject 50mm

oversize after secondary crushing. This is possible due to the nature of the

mineralisation in which almost all gold is associated with veins that fracture easily

with crushing. A similar circuit was used historically for the processing of Sarsfield ore

with success.

This circuit is expected to reduce tonnage of low grade ore feed into the mill by ~41%,

lifting the grade by ~48% with a minimal amount of ounces lost, estimated at ~7%

(see Figure 27).

Figure 27: Low grade beneficiation summary

Source: Company Reports, Canaccord Genuity estimates

Ravenswood blend upgrade

Mt g/t %

Total tonnes processed 58.56 0.91

High grade 35.42 0.97

Low grade 35.27 0.50

Underground 0.93 2.72

Implied LG beneficiated tonnage 22.21 0.74

Implied LG beneficiation factor (tonnage) 59%

Implied LG beneficiation factor (grade) 48%

Implied LG beneficiation ore loss 7%

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 18

19

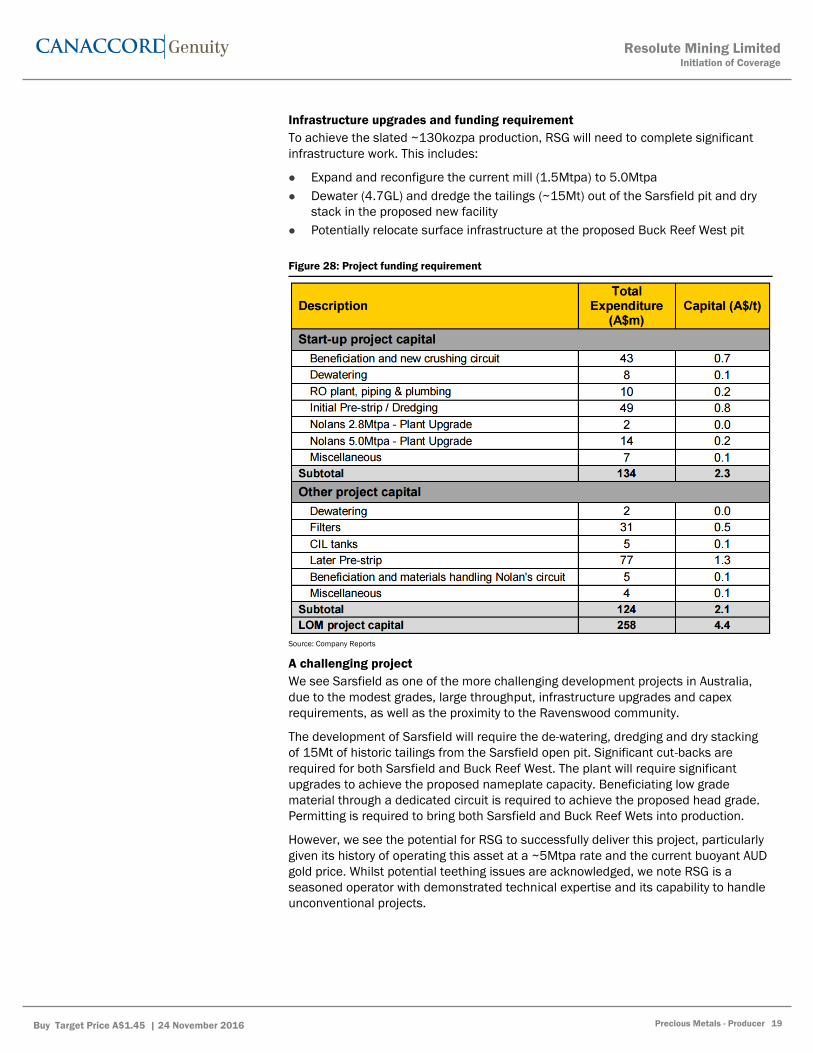

Infrastructure upgrades and funding requirement

To achieve the slated ~130kozpa production, RSG will need to complete significant

infrastructure work. This includes:

Expand and reconfigure the current mill (1.5Mtpa) to 5.0Mtpa

Dewater (4.7GL) and dredge the tailings (~15Mt) out of the Sarsfield pit and dry

stack in the proposed new facility

Potentially relocate surface infrastructure at the proposed Buck Reef West pit

Figure 28: Project funding requirement

Source: Company Reports

A challenging project

We see Sarsfield as one of the more challenging development projects in Australia,

due to the modest grades, large throughput, infrastructure upgrades and capex

requirements, as well as the proximity to the Ravenswood community.

The development of Sarsfield will require the de-watering, dredging and dry stacking

of 15Mt of historic tailings from the Sarsfield open pit. Significant cut-backs are

required for both Sarsfield and Buck Reef West. The plant will require significant

upgrades to achieve the proposed nameplate capacity. Beneficiating low grade

material through a dedicated circuit is required to achieve the proposed head grade.

Permitting is required to bring both Sarsfield and Buck Reef Wets into production.

However, we see the potential for RSG to successfully deliver this project, particularly

given its history of operating this asset at a ~5Mtpa rate and the current buoyant AUD

gold price. Whilst potential teething issues are acknowledged, we note RSG is a

seasoned operator with demonstrated technical expertise and its capability to handle

unconventional projects.

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 19

20

Potential upside

Upside at Ravenswood includes the potential incorporation of Welcome Breccia

(208koz @ 3.2g/t) and a potential underground operation at Buck Reef Deeps (drilling

results include 19m @ 4.4g/t and 26m @ 2.8g/t).

Furthermore, subject to permitting, bringing forward Buck Reef could potentially

reduce upfront capex and deliver higher grades to the mill.

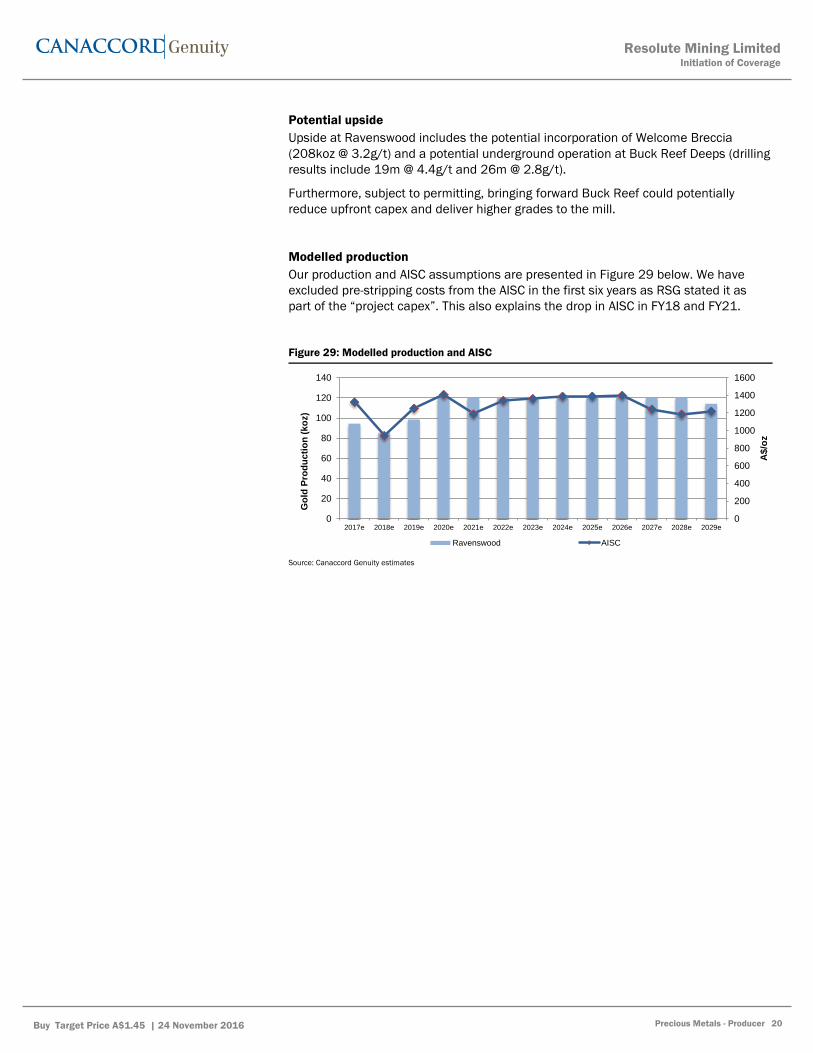

Modelled production

Our production and AISC assumptions are presented in Figure 29 below. We have

excluded pre-stripping costs from the AISC in the first six years as RSG stated it as

part of the “project capex”. This also explains the drop in AISC in FY18 and FY21.

Figure 29: Modelled production and AISC

Source: Canaccord Genuity estimates

0

200

400

600

800

1000

1200

1400

1600

0

20

40

60

80

100

120

140

2017e 2018e 2019e 2020e 2021e 2022e 2023e 2024e 2025e 2026e 2027e 2028e 2029e

A$

/oz

Go

ld P

rod

uc

tio

n (

ko

z)

Ravenswood AISC

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 20

21

Bibiani (90%)

Background

Bibiani is located in the western region of Ghana, near the town of Bibiani. Historically,

the mine was in production from 1902-1913 and 1927-1973, predominantly as an

underground mine and produced ~2Moz. Modern mining followed the acquisition by

AngloGold Ashanti (SJ:ANG | Not rated) in mid-1990s. ANG produced ~1.8Moz from

the main and satellite pits until 2006.

RSG assumed 90% ownership of the project through the approval of its proposed

Deed of Company Arrangement (DOCA) by Noble Mineral’s creditors in 2013 and

following governmental approvals in 2014. RSG was Noble’s 20% shareholder and the

largest external creditor and held just under 100% of Noble’s listed unsecured

convertible notes. The government of Ghana owns 10% project interest (free carried).

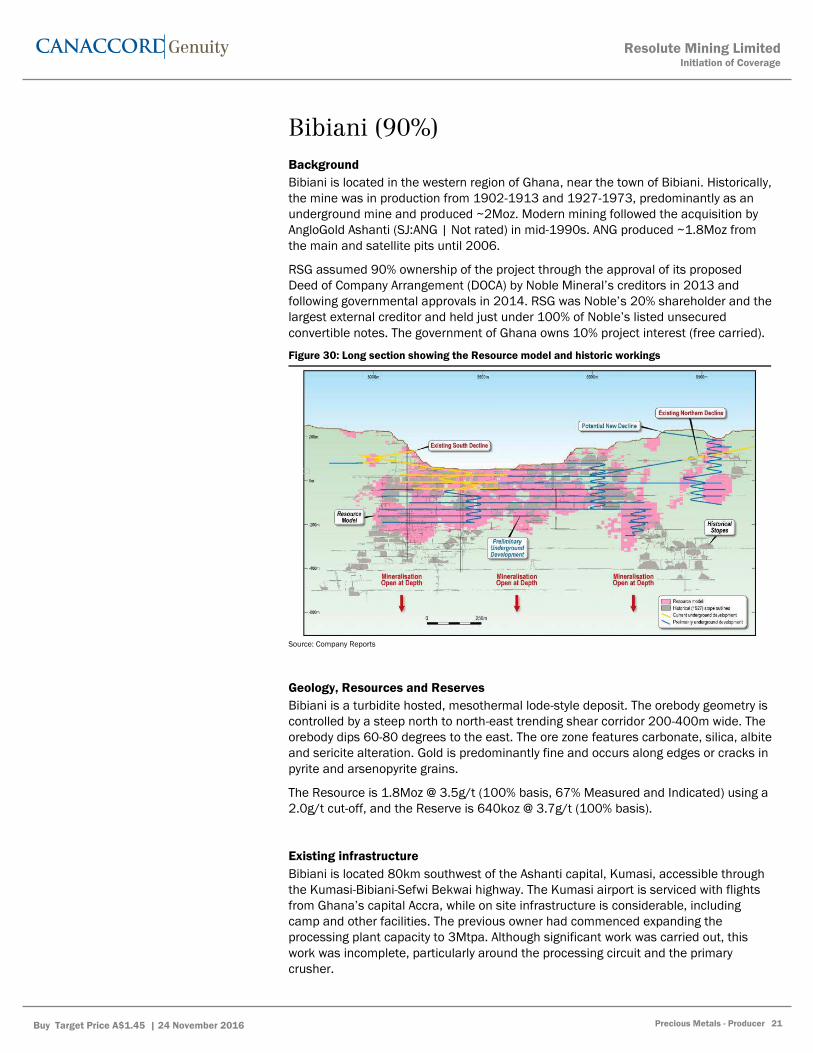

Figure 30: Long section showing the Resource model and historic workings

Source: Company Reports

Geology, Resources and Reserves

Bibiani is a turbidite hosted, mesothermal lode-style deposit. The orebody geometry is

controlled by a steep north to north-east trending shear corridor 200-400m wide. The

orebody dips 60-80 degrees to the east. The ore zone features carbonate, silica, albite

and sericite alteration. Gold is predominantly fine and occurs along edges or cracks in

pyrite and arsenopyrite grains.

The Resource is 1.8Moz @ 3.5g/t (100% basis, 67% Measured and Indicated) using a

2.0g/t cut-off, and the Reserve is 640koz @ 3.7g/t (100% basis).

Existing infrastructure

Bibiani is located 80km southwest of the Ashanti capital, Kumasi, accessible through

the Kumasi-Bibiani-Sefwi Bekwai highway. The Kumasi airport is serviced with flights

from Ghana’s capital Accra, while on site infrastructure is considerable, including

camp and other facilities. The previous owner had commenced expanding the

processing plant capacity to 3Mtpa. Although significant work was carried out, this

work was incomplete, particularly around the processing circuit and the primary

crusher.

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 21

22

Proposed mining operation

The project was previously envisaged to be an open pit operation by its previous

owner, requiring significant cut-backs and population relocation, as the local

communities hosts ~7,500 people. RSG proposed to mine the ore using underground

methods (Long Hole Open Stoping).

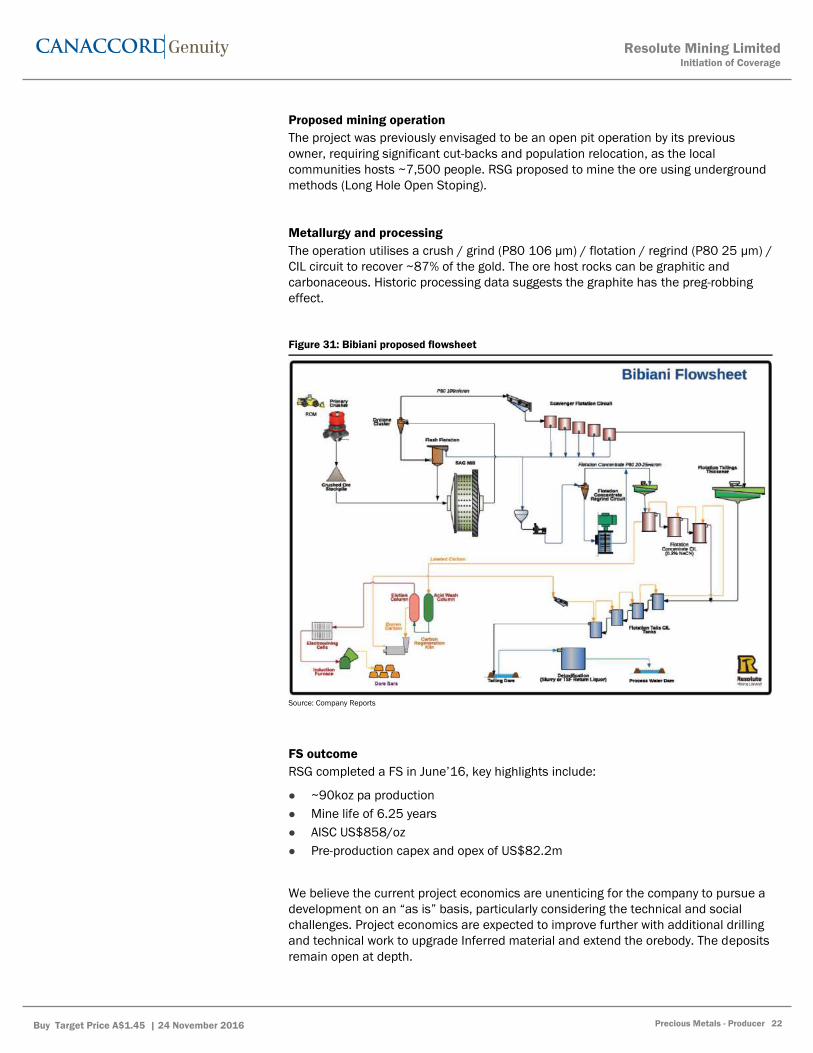

Metallurgy and processing

The operation utilises a crush / grind (P80 106 µm) / flotation / regrind (P80 25 μm) /

CIL circuit to recover ~87% of the gold. The ore host rocks can be graphitic and

carbonaceous. Historic processing data suggests the graphite has the preg-robbing

effect.

Figure 31: Bibiani proposed flowsheet

Source: Company Reports

FS outcome

RSG completed a FS in June’16, key highlights include:

~90koz pa production

Mine life of 6.25 years

AISC US$858/oz

Pre-production capex and opex of US$82.2m

We believe the current project economics are unenticing for the company to pursue a

development on an “as is” basis, particularly considering the technical and social

challenges. Project economics are expected to improve further with additional drilling

and technical work to upgrade Inferred material and extend the orebody. The deposits

remain open at depth.

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 22

23

Exploration upside

Near mine Syama

The Syama deposit remains open at depth, with recent robust results suggesting

further orebody extensions (see Figure 21). Hits include: 62m @ 6.7g/t, 28m @ 5.1g/t

and 46m @ 3.1g/t. Additionally, RSG recently discovered a southern zone ~250m

south of the current Reserve, with encouraging results including 19m @ 2.6g/t from

273m and 18m @ 3.0g/t from 372m.

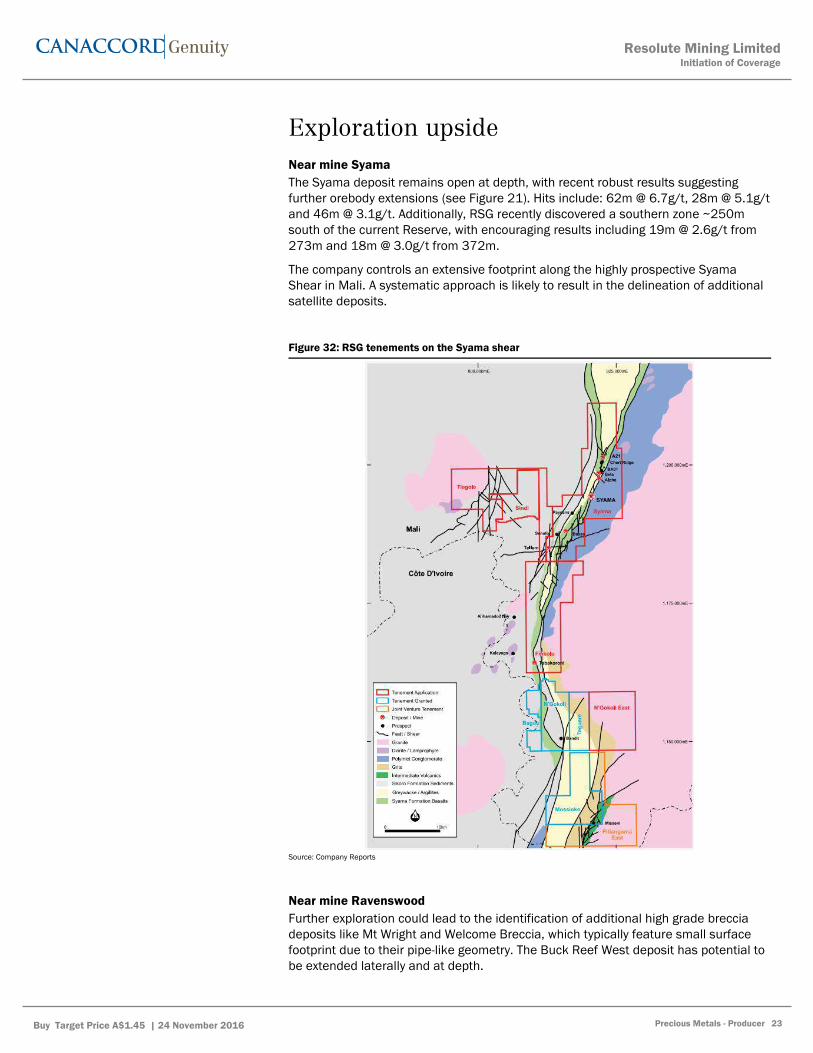

The company controls an extensive footprint along the highly prospective Syama

Shear in Mali. A systematic approach is likely to result in the delineation of additional

satellite deposits.

Figure 32: RSG tenements on the Syama shear

Source: Company Reports

Near mine Ravenswood

Further exploration could lead to the identification of additional high grade breccia

deposits like Mt Wright and Welcome Breccia, which typically feature small surface

footprint due to their pipe-like geometry. The Buck Reef West deposit has potential to

be extended laterally and at depth.

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 23

24

Investment risks

Sovereign risks

RSG operates in several West African countries including Mali and Ghana, and has

interest in exploration and development companies located in Tanzania and the DRC.

As such, it is subject to sovereign risks. We note the company’s enviable track record

of successfully operating and rehabilitating mines across numerous jurisdictions

including Ghana, Tanzania and Mali.

Operating risks

Companies in production will be subject to risks such as plant/equipment

breakdowns, metallurgical (meeting design recoveries within a complex flowsheet),

materials handling and other technical issues. An increase in operating costs could

reduce the profitability and free cash generation from the operating assets

considerably and negatively impact valuation. Further, the actual characteristics of an

ore deposit may differ significantly from initial interpretations which can also

materially impact forecast production from original expectations.

Exploration risks

Exploration is subject to a number of risks and can require a high rate of capital

expenditure. Risks can also be associated with exploration techniques and lack of

accuracy in interpretation of geochemical, geophysical, drilling and other data. No

assurance can be given that exploration will delineate further minable Reserves.

Commodity price and currency fluctuation

The company as a gold producer is exposed to commodity price and currency

fluctuations, often driven by macro-economic forces including inflationary pressure,

interest rates and supply and demand of commodities. These factors are external and

could reduce the profitability, costing and prospective outlook for the business.

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 24

25

Directors and management

Peter Ernest Huston – Non-Executive Chairman (retiring at AGM)

Mr Peter Huston was appointed Chairman in 2000. After gaining admission in

Western Australia as a Barrister and Solicitor, Mr Huston initially practised in the area

of corporate and revenue law. Subsequently, he moved into the area of public listings,

reconstructions, equity raisings, mergers and acquisitions and advised on a number of

major public company floats, takeovers and reconstructions. Mr Huston is admitted to

appear before the Supreme Court, Federal Court and High Court of Australia. Mr

Huston was a partner of the international law firm now known as "Deacons" until

1993 when he retired to establish the boutique investment bank and corporate

advisory firm known as "Troika Securities Limited".

John Paul Welborn – Managing Director and CEO

Mr John Welborn was appointed to the board on 27 February 2015 as a non‐executive director and became the Managing Director and Chief Executive Officer on 1

July 2015. Mr Welborn is a Chartered Accountant with a Bachelor of Commerce

degree from the University of Western Australia and is a Fellow of the Institute of

Chartered Accountants in Australia, a Fellow of the Australian Institute of

Management and is a member of the Australian Institute of Mining and Metallurgy,

the Financial Services Institute of Australasia, and the Australian Institute of Company

Directors. Mr Welborn has extensive experience in the resources sector as a senior

executive and in corporate management, finance and investment banking. He was

most recently the Managing Director of Equatorial Resources Limited and was

previously the Head of Specialised Lending in Western Australia for Investec Bank

(Australia) Ltd.

Peter Ross Sullivan – Non-Executive Director

Mr Peter Sullivan was appointed Managing Director and Chief Executive Officer of the

Company in 2001 and retired as Chief Executive Officer on 30 June 2015. Mr Sullivan

is an engineer and has been involved in the management and strategic development

of resource companies and projects for over 20 years. Mr Sullivan is also a director of

GME Resources Limited (appointed 1996), Zeta Resources Limited (appointed 2013),

Pan Pacific Petroleum NL (appointed 2014) and Panoramic Resources Limited

(appointed 2015).

Marthinus Johan Botha – Non -Executive Director

Mr Martin Botha is a non-executive director and was appointed to the board in

February 2014. Mr Botha is an Engineering Surveyor by training who has 30 years’

experience in banking, with 24 years spent in leadership roles building Standard Bank

Plc’s international operations. Mr Botha’s primary responsibilities at Standard Bank

included establishing and leading the development of the core global natural

resources trading and financing franchises, as well as various geographic strategies,

including those in the Russian Commonwealth of Independent States, Turkey and the

Middle East. Mr Botha graduated with first class honours from the University of Cape

Town and is based in London.

Mr Henry Thomas Stuary Price - Non-Executive Director

Mr Bill Price is a non-executive director and was appointed to the board in 2003. Mr

Price is a Fellow Chartered Accountant with over 35 years of experience in the

accounting profession. Mr Price has extensive taxation and accounting experience in

the corporate and mining sector. In addition to his professional qualifications, Mr Price

is a member of the Australian Institute of Company Directors, a registered tax agent

and registered company auditor. Mr Price is also a director of Tennis West.

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 25

Appendix: Important DisclosuresAnalyst CertificationEach authoring analyst of Canaccord Genuity whose name appears on the front page of this research hereby certifies that (i) therecommendations and opinions expressed in this research accurately reflect the authoring analyst’s personal, independent andobjective views about any and all of the designated investments or relevant issuers discussed herein that are within such authoringanalyst’s coverage universe and (ii) no part of the authoring analyst’s compensation was, is, or will be, directly or indirectly, related to thespecific recommendations or views expressed by the authoring analyst in the research.Analysts employed outside the US are not registered as research analysts with FINRA. These analysts may not be associated persons ofCanaccord Genuity Inc. and therefore may not be subject to the FINRA Rule 2241 and NYSE Rule 472 restrictions on communicationswith a subject company, public appearances and trading securities held by a research analyst account.Sector CoverageIndividuals identified as “Sector Coverage” cover a subject company’s industry in the identified jurisdiction, but are not authoringanalysts of the report.

Investment RecommendationDate and time of first dissemination: November 24, 2016, 14:30 ETDate and time of production: November 24, 2016, 14:31 ETTarget Price / Valuation Methodology:Resolute Mining Limited - RSGOur price target is based on 1x forward curve NPV5% for the operating assets net of corporate and other adjustments.BHP Billiton plc - BLTOur target price comprises 3 components. We value the shares on the basis of the rounded average of EV/EBITDA (relative to thecompany's historical performance), rolling P/E relative to the FTSE All Share Index, and our NPV.Randgold Resources - RRSOur target price is based on a 1.50x target NAV multiple (5% discount rate) using Canaccord Genuity's forward Au/Ag price curve.Risks to achieving Target Price / Valuation:Resolute Mining Limited - RSG

Sovereign risksRSG operates in several West African countries including Mali and Ghana, and has interest in exploration and development companieslocated in Tanzania and the DRC. As such, it is subject to sovereign risks. We note the company’s enviable track record of successfullyoperating and rehabilitating mines across numerous jurisdictions including Ghana, Tanzania and Mali.

Operating risksCompanies in production will be subject to risks such as plant/equipment breakdowns, metallurgical (meeting design recoveries withina complex flowsheet), materials handling and other technical issues. An increase in operating costs could reduce the profitability andfree cash generation from the operating assets considerably and negatively impact valuation. Further, the actual characteristics ofan ore deposit may differ significantly from initial interpretations which can also materially impact forecast production from originalexpectations.

Exploration risksExploration is subject to a number of risks and can require a high rate of capital expenditure. Risks can also be associated withexploration techniques and lack of accuracy in interpretation of geochemical, geophysical, drilling and other data. No assurance can begiven that exploration will delineate further minable Reserves.

Commodity price and currency fluctuationThe company as a gold producer is exposed to commodity price and currency fluctuations, often driven by macro-economic forcesincluding inflationary pressure, interest rates and supply and demand of commodities. These factors are external and could reduce theprofitability, costing and prospective outlook for the business.BHP Billiton plc - BLTThe main risks to our view are different commodity prices vs our current forecasts. The company is also exposed to the potentially open-ended liability from the Samarco disaster and the risk of "lower-for-longer" oil prices if we fail to see supply restraint - the onshore USbusiness may be particularly at risk.Randgold Resources - RRS

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 26

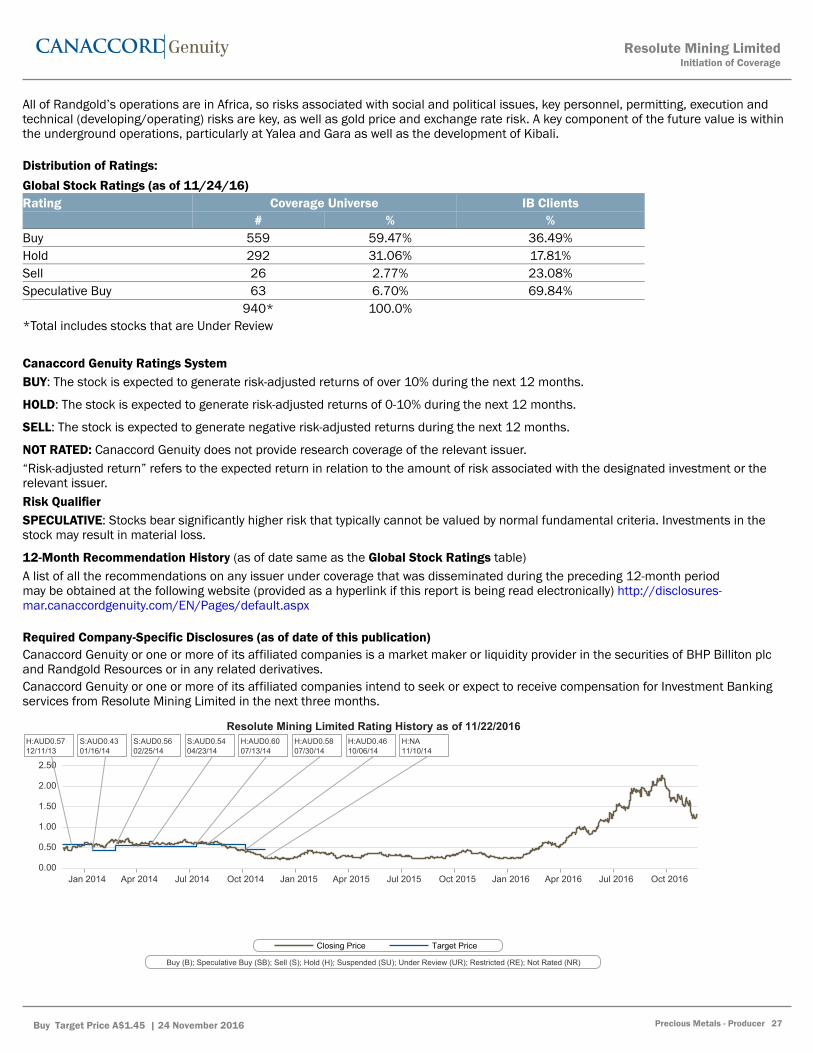

All of Randgold’s operations are in Africa, so risks associated with social and political issues, key personnel, permitting, execution andtechnical (developing/operating) risks are key, as well as gold price and exchange rate risk. A key component of the future value is withinthe underground operations, particularly at Yalea and Gara as well as the development of Kibali.

Distribution of Ratings:Global Stock Ratings (as of 11/24/16)Rating Coverage Universe IB Clients

# % %Buy 559 59.47% 36.49%Hold 292 31.06% 17.81%Sell 26 2.77% 23.08%Speculative Buy 63 6.70% 69.84%

940* 100.0%*Total includes stocks that are Under Review

Canaccord Genuity Ratings SystemBUY: The stock is expected to generate risk-adjusted returns of over 10% during the next 12 months.

HOLD: The stock is expected to generate risk-adjusted returns of 0-10% during the next 12 months.

SELL: The stock is expected to generate negative risk-adjusted returns during the next 12 months.

NOT RATED: Canaccord Genuity does not provide research coverage of the relevant issuer.“Risk-adjusted return” refers to the expected return in relation to the amount of risk associated with the designated investment or therelevant issuer.Risk QualifierSPECULATIVE: Stocks bear significantly higher risk that typically cannot be valued by normal fundamental criteria. Investments in thestock may result in material loss.

12-Month Recommendation History (as of date same as the Global Stock Ratings table)A list of all the recommendations on any issuer under coverage that was disseminated during the preceding 12-month periodmay be obtained at the following website (provided as a hyperlink if this report is being read electronically) http://disclosures-mar.canaccordgenuity.com/EN/Pages/default.aspx

Required Company-Specific Disclosures (as of date of this publication)Canaccord Genuity or one or more of its affiliated companies is a market maker or liquidity provider in the securities of BHP Billiton plcand Randgold Resources or in any related derivatives.Canaccord Genuity or one or more of its affiliated companies intend to seek or expect to receive compensation for Investment Bankingservices from Resolute Mining Limited in the next three months.

Jan 2014 Apr 2014 Jul 2014 Oct 2014 Jan 2015 Apr 2015 Jul 2015 Oct 2015 Jan 2016 Apr 2016 Jul 2016 Oct 2016

2.50

2.00

1.50

1.00

0.50

0.00

Resolute Mining Limited Rating History as of 11/22/2016

Closing Price Target Price

Buy (B); Speculative Buy (SB); Sell (S); Hold (H); Suspended (SU); Under Review (UR); Restricted (RE); Not Rated (NR)

H:AUD0.5712/11/13

S:AUD0.4301/16/14

S:AUD0.5602/25/14

S:AUD0.5404/23/14

H:AUD0.6007/13/14

H:AUD0.5807/30/14

H:AUD0.4610/06/14

H:NA11/10/14

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 27

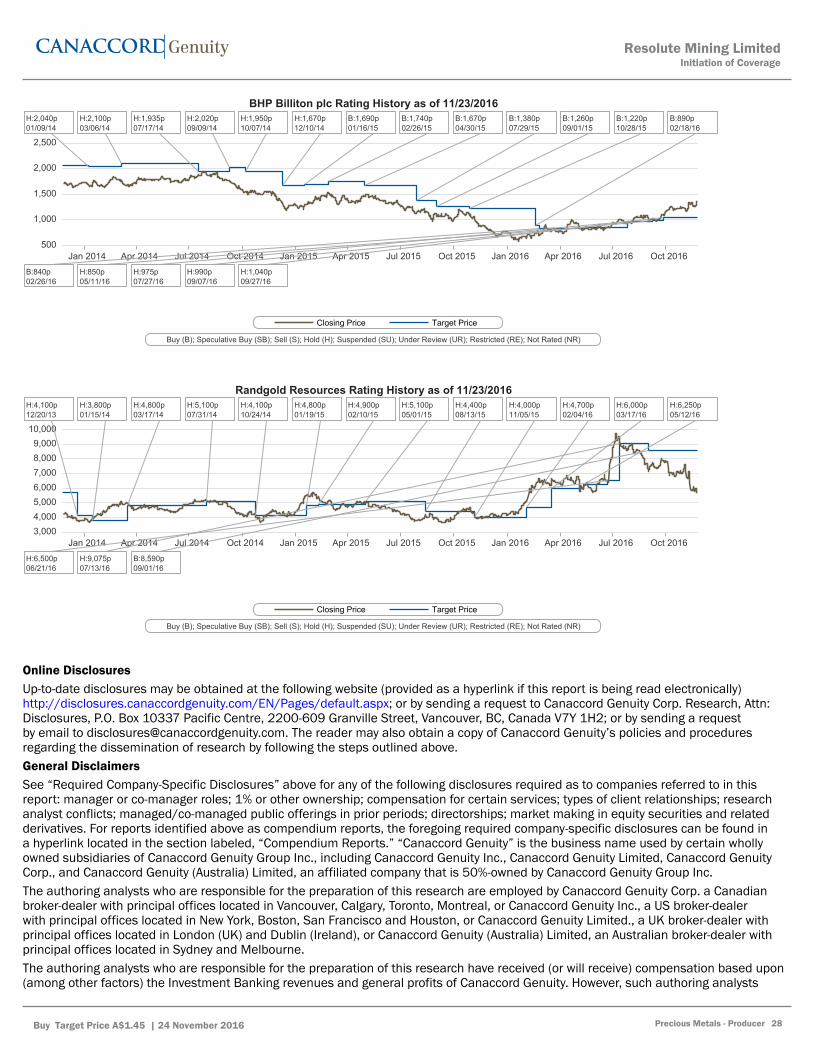

Jan 2014 Apr 2014 Jul 2014 Oct 2014 Jan 2015 Apr 2015 Jul 2015 Oct 2015 Jan 2016 Apr 2016 Jul 2016 Oct 2016

2,500

2,000

1,500

1,000

500

BHP Billiton plc Rating History as of 11/23/2016

Closing Price Target Price

Buy (B); Speculative Buy (SB); Sell (S); Hold (H); Suspended (SU); Under Review (UR); Restricted (RE); Not Rated (NR)

H:2,040p01/09/14

H:2,100p03/06/14

H:1,935p07/17/14

H:2,020p09/09/14

H:1,950p10/07/14

H:1,670p12/10/14

B:1,690p01/16/15

B:1,740p02/26/15

B:1,670p04/30/15

B:1,380p07/29/15

B:1,260p09/01/15

B:1,220p10/28/15

B:890p02/18/16

B:840p02/26/16

H:850p05/11/16

H:975p07/27/16

H:990p09/07/16

H:1,040p09/27/16

Jan 2014 Apr 2014 Jul 2014 Oct 2014 Jan 2015 Apr 2015 Jul 2015 Oct 2015 Jan 2016 Apr 2016 Jul 2016 Oct 2016

10,0009,0008,0007,0006,0005,0004,0003,000

Randgold Resources Rating History as of 11/23/2016

Closing Price Target Price

Buy (B); Speculative Buy (SB); Sell (S); Hold (H); Suspended (SU); Under Review (UR); Restricted (RE); Not Rated (NR)

H:4,100p12/20/13

H:3,800p01/15/14

H:4,800p03/17/14

H:5,100p07/31/14

H:4,100p10/24/14

H:4,800p01/19/15

H:4,900p02/10/15

H:5,100p05/01/15

H:4,400p08/13/15

H:4,000p11/05/15

H:4,700p02/04/16

H:6,000p03/17/16

H:6,250p05/12/16

H:6,500p06/21/16

H:9,075p07/13/16

B:8,590p09/01/16

Online DisclosuresUp-to-date disclosures may be obtained at the following website (provided as a hyperlink if this report is being read electronically)http://disclosures.canaccordgenuity.com/EN/Pages/default.aspx; or by sending a request to Canaccord Genuity Corp. Research, Attn:Disclosures, P.O. Box 10337 Pacific Centre, 2200-609 Granville Street, Vancouver, BC, Canada V7Y 1H2; or by sending a requestby email to [email protected]. The reader may also obtain a copy of Canaccord Genuity’s policies and proceduresregarding the dissemination of research by following the steps outlined above.General DisclaimersSee “Required Company-Specific Disclosures” above for any of the following disclosures required as to companies referred to in thisreport: manager or co-manager roles; 1% or other ownership; compensation for certain services; types of client relationships; researchanalyst conflicts; managed/co-managed public offerings in prior periods; directorships; market making in equity securities and relatedderivatives. For reports identified above as compendium reports, the foregoing required company-specific disclosures can be found ina hyperlink located in the section labeled, “Compendium Reports.” “Canaccord Genuity” is the business name used by certain whollyowned subsidiaries of Canaccord Genuity Group Inc., including Canaccord Genuity Inc., Canaccord Genuity Limited, Canaccord GenuityCorp., and Canaccord Genuity (Australia) Limited, an affiliated company that is 50%-owned by Canaccord Genuity Group Inc.The authoring analysts who are responsible for the preparation of this research are employed by Canaccord Genuity Corp. a Canadianbroker-dealer with principal offices located in Vancouver, Calgary, Toronto, Montreal, or Canaccord Genuity Inc., a US broker-dealerwith principal offices located in New York, Boston, San Francisco and Houston, or Canaccord Genuity Limited., a UK broker-dealer withprincipal offices located in London (UK) and Dublin (Ireland), or Canaccord Genuity (Australia) Limited, an Australian broker-dealer withprincipal offices located in Sydney and Melbourne.The authoring analysts who are responsible for the preparation of this research have received (or will receive) compensation based upon(among other factors) the Investment Banking revenues and general profits of Canaccord Genuity. However, such authoring analysts

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 28

have not received, and will not receive, compensation that is directly based upon or linked to one or more specific Investment Bankingactivities, or to recommendations contained in the research.Some regulators require that a firm must establish, implement and make available a policy for managing conflicts of interest arising asa result of publication or distribution of research. This research has been prepared in accordance with Canaccord Genuity’s policy onmanaging conflicts of interest, and information barriers or firewalls have been used where appropriate. Canaccord Genuity’s policy isavailable upon request.The information contained in this research has been compiled by Canaccord Genuity from sources believed to be reliable, but (with theexception of the information about Canaccord Genuity) no representation or warranty, express or implied, is made by Canaccord Genuity,its affiliated companies or any other person as to its fairness, accuracy, completeness or correctness. Canaccord Genuity has notindependently verified the facts, assumptions, and estimates contained herein. All estimates, opinions and other information containedin this research constitute Canaccord Genuity’s judgement as of the date of this research, are subject to change without notice and areprovided in good faith but without legal responsibility or liability.From time to time, Canaccord Genuity salespeople, traders, and other professionals provide oral or written market commentary ortrading strategies to our clients and our principal trading desk that reflect opinions that are contrary to the opinions expressed in thisresearch. Canaccord Genuity’s affiliates, principal trading desk, and investing businesses also from time to time make investmentdecisions that are inconsistent with the recommendations or views expressed in this research.This research is provided for information purposes only and does not constitute an offer or solicitation to buy or sell any designatedinvestments discussed herein in any jurisdiction where such offer or solicitation would be prohibited. As a result, the designatedinvestments discussed in this research may not be eligible for sale in some jurisdictions. This research is not, and under nocircumstances should be construed as, a solicitation to act as a securities broker or dealer in any jurisdiction by any person or companythat is not legally permitted to carry on the business of a securities broker or dealer in that jurisdiction. This material is prepared forgeneral circulation to clients and does not have regard to the investment objectives, financial situation or particular needs of anyparticular person. Investors should obtain advice based on their own individual circumstances before making an investment decision.To the fullest extent permitted by law, none of Canaccord Genuity, its affiliated companies or any other person accepts any liabilitywhatsoever for any direct or consequential loss arising from or relating to any use of the information contained in this research.Research Distribution PolicyCanaccord Genuity research is posted on the Canaccord Genuity Research Portal and will be available simultaneously for access by allof Canaccord Genuity’s customers who are entitled to receive the firm's research. In addition research may be distributed by the firm’ssales and trading personnel via email, instant message or other electronic means. Customers entitled to receive research may alsoreceive it via third party vendors. Until such time as research is made available to Canaccord Genuity’s customers as described above,Authoring Analysts will not discuss the contents of their research with Sales and Trading or Investment Banking employees without priorcompliance consent.For further information about the proprietary model(s) associated with the covered issuer(s) in this research report, clients shouldcontact their local sales representative.Short-Term Trade IdeasResearch Analysts may, from time to time, discuss “short-term trade ideas” in research reports. A short-term trade idea offers a near-term view on how a security may trade, based on market and trading events or catalysts, and the resulting trading opportunity that maybe available. Any such trading strategies are distinct from and do not affect the analysts' fundamental equity rating for such stocks. Ashort-term trade idea may differ from the price targets and recommendations in our published research reports that reflect the researchanalyst's views of the longer-term (i.e. one-year or greater) prospects of the subject company, as a result of the differing time horizons,methodologies and/or other factors. It is possible, for example, that a subject company's common equity that is considered a long-term ‘Hold' or 'Sell' might present a short-term buying opportunity as a result of temporary selling pressure in the market or for otherreasons described in the research report; conversely, a subject company's stock rated a long-term 'Buy' or “Speculative Buy’ could beconsidered susceptible to a downward price correction, or other factors may exist that lead the research analyst to suggest a sale overthe short-term. Short-term trade ideas are not ratings, nor are they part of any ratings system, and the firm does not intend, and does notundertake any obligation, to maintain or update short-term trade ideas. Short-term trade ideas are not suitable for all investors and arenot tailored to individual investor circumstances and objectives, and investors should make their own independent decisions regardingany securities or strategies discussed herein. Please contact your salesperson for more information regarding Canaccord Genuity’sresearch.For Canadian Residents:This research has been approved by Canaccord Genuity Corp., which accepts sole responsibility for this research and its disseminationin Canada. Canaccord Genuity Corp. is registered and regulated by the Investment Industry Regulatory Organization of Canada (IIROC)and is a Member of the Canadian Investor Protection Fund. Canadian clients wishing to effect transactions in any designated investmentdiscussed should do so through a qualified salesperson of Canaccord Genuity Corp. in their particular province or territory.For United States Persons:Canaccord Genuity Inc., a US registered broker-dealer, accepts responsibility for this research and its dissemination in the United States.This research is intended for distribution in the United States only to certain US institutional investors. US clients wishing to effecttransactions in any designated investment discussed should do so through a qualified salesperson of Canaccord Genuity Inc. Analysts

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 29

employed outside the US, as specifically indicated elsewhere in this report, are not registered as research analysts with FINRA. Theseanalysts may not be associated persons of Canaccord Genuity Inc. and therefore may not be subject to the FINRA Rule 2241 and NYSERule 472 restrictions on communications with a subject company, public appearances and trading securities held by a research analystaccount.For United Kingdom and European Residents:This research is distributed in the United Kingdom and elsewhere Europe, as third party research by Canaccord Genuity Limited,which is authorized and regulated by the Financial Conduct Authority. This research is for distribution only to persons who are EligibleCounterparties or Professional Clients only and is exempt from the general restrictions in section 21 of the Financial Services andMarkets Act 2000 on the communication of invitations or inducements to engage in investment activity on the grounds that it is beingdistributed in the United Kingdom only to persons of a kind described in Article 19(5) (Investment Professionals) and 49(2) (High NetWorth companies, unincorporated associations etc) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005(as amended). It is not intended to be distributed or passed on, directly or indirectly, to any other class of persons. This material is not fordistribution in the United Kingdom or elsewhere in Europe to retail clients, as defined under the rules of the Financial Conduct Authority.For Jersey, Guernsey and Isle of Man Residents:This research is sent to you by Canaccord Genuity Wealth (International) Limited (CGWI) for information purposes and is not to beconstrued as a solicitation or an offer to purchase or sell investments or related financial instruments. This research has been producedby an affiliate of CGWI for circulation to its institutional clients and also CGWI. Its contents have been approved by CGWI and we areproviding it to you on the basis that we believe it to be of interest to you. This statement should be read in conjunction with your clientagreement, CGWI's current terms of business and the other disclosures and disclaimers contained within this research. If you are in anydoubt, you should consult your financial adviser.CGWI is licensed and regulated by the Guernsey Financial Services Commission, the Jersey Financial Services Commission and the Isleof Man Financial Supervision Commission. CGWI is registered in Guernsey and is a wholly owned subsidiary of Canaccord Genuity GroupInc.For Australian Residents:This research is distributed in Australia by Canaccord Genuity (Australia) Limited ABN 19 075 071 466 holder of AFS Licence No234666. To the extent that this research contains any advice, this is limited to general advice only. Recipients should take into accounttheir own personal circumstances before making an investment decision. Clients wishing to effect any transactions in any financialproducts discussed in the research should do so through a qualified representative of Canaccord Genuity (Australia) Limited. CanaccordGenuity Wealth Management is a division of Canaccord Genuity (Australia) Limited.For Hong Kong Residents:This research is distributed in Hong Kong by Canaccord Genuity (Hong Kong) Limited which is licensed by the Securities and FuturesCommission. This research is only intended for persons who fall within the definition of professional investor as defined in the Securitiesand Futures Ordinance. It is not intended to be distributed or passed on, directly or indirectly, to any other class of persons. Recipients ofthis report can contact Canaccord Genuity (Hong Kong) Limited. (Contact Tel: +852 3919 2561) in respect of any matters arising from, orin connection with, this research.Additional information is available on request.Copyright © Canaccord Genuity Corp. 2016 – Member IIROC/Canadian Investor Protection Fund

Copyright © Canaccord Genuity Limited. 2016 – Member LSE, authorized and regulated by the Financial Conduct Authority.

Copyright © Canaccord Genuity Inc. 2016 – Member FINRA/SIPC

Copyright © Canaccord Genuity (Australia) Limited. 2016 – Participant of ASX Group, Chi-x Australia and of the NSX. Authorized andregulated by ASIC.

All rights reserved. All material presented in this document, unless specifically indicated otherwise, is under copyright to CanaccordGenuity Corp., Canaccord Genuity Limited, Canaccord Genuity Inc or Canaccord Genuity Group Inc. None of the material, nor its content,nor any copy of it, may be altered in any way, or transmitted to or distributed to any other party, without the prior express writtenpermission of the entities listed above.None of the material, nor its content, nor any copy of it, may be altered in any way, reproduced, or distributed to any other partyincluding by way of any form of social media, without the prior express written permission of the entities listed above.

Resolute Mining LimitedInitiation of Coverage

Buy Target Price A$1.45 | 24 November 2016 Precious Metals - Producer 30