Scrooge” and our Software Industry

17

“Scrooge” and our Software Industry Keynote for the 10th European Software Conference By David Boventer

Transcript of Scrooge” and our Software Industry

“Scrooge” and our Software Industry

Keynote for the 10th

European Software Conference

By David Boventer

Introduction and why does Scrooge interest us?SCROOGE McDUCK AND MONEY was another little Disney film which both entertained & educated. crooge informs the viewer about the history of the development of convenient currency and gives a brief explanation of inflation, economics and the importance of living on a budget for good household management. He reveals the reason for taxes, explains why money must circulate and advocates the value of making shrewd investments. Throughout, the animation is strictly routine - showing where Disney pinched a few production pennies.

There are parallels between Scrooge and our software industry as we experience them

Scarcity – we are confronted with a limited budget of time, energy and money

Power disproportion – we encounter mega-corporations with a seemingly abundant amount of financial potential- though we are not directly competing with them it takes strength and confidence in your abilities and resource saving abilities

But we are all global players. Starting from our customers to the language options we offer online and the way the income reaches us crossing many tax borders and into our pockets.

Our products are our wealth and currency, translating into hard cash depending on the quality, on the trust we enjoy on our markets and among our users.

The aggregation of capabilities and strength resulting in wealthScrooge is the best example of a successful entrepreneur to its extreme and therefore an extreme picture of automated aggregation of wealth. He demonstrates the absurdity of enormous wealth but stresses the importance of his first penny earned. Wealth evolves around the first success and builds up on it. As software developers we have to do it right from the beginning. But never loose traction with the ground we stand on.

We know that it is important to:

Ascertain our markets and opportunitiesGive time for networking and education (like attending the ESWC!)

Ascertain our markets and opportunities e.g. Broadband access in the EU and the USAWhen we start thinking about the IT-Business in Europe we probably think about the technical conditions that enable E-commerce in general. The broadband-access is a good indirect indicator for the general acceptance of software products.There we can see that the infrastructure in the EU still has many deficits esp. In the rural areas.Austria has a coverage of about 58 percent, Germany is at 65 percent with Iceland leading with 87 percent. The US has a coverage of about 65 percent.

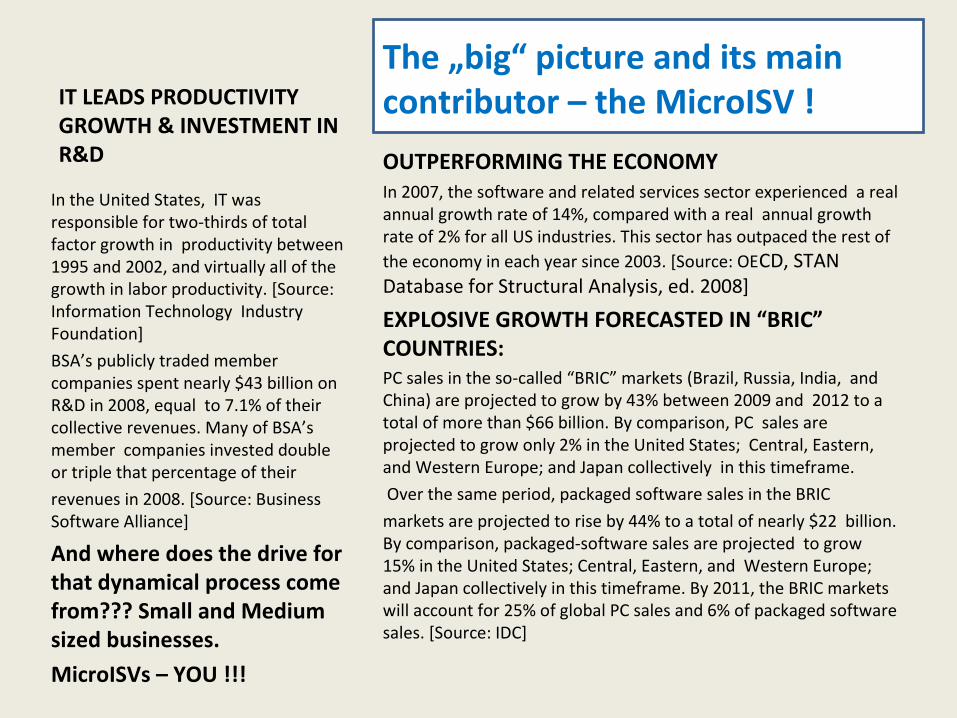

IT LEADS PRODUCTIVITY GROWTH & INVESTMENT IN R&D OUTPERFORMING THE ECONOMY

In 2007, the software and related services sector experienced a real annual growth rate of 14%, compared with a real annual growth rate of 2% for all US industries. This sector has outpaced the rest of the economy in each year since 2003. [Source: OECD, STAN Database for Structural Analysis, ed. 2008]

EXPLOSIVE GROWTH FORECASTED IN “BRIC” COUNTRIES: PC sales in the so-called “BRIC” markets (Brazil, Russia, India, and China) are projected to grow by 43% between 2009 and 2012 to a total of more than $66 billion. By comparison, PC sales are projected to grow only 2% in the United States; Central, Eastern, and Western Europe; and Japan collectively in this timeframe.

Over the same period, packaged software sales in the BRIC

markets are projected to rise by 44% to a total of nearly $22 billion. By comparison, packaged-software sales are projected to grow 15% in the United States; Central, Eastern, and Western Europe; and Japan collectively in this timeframe. By 2011, the BRIC markets will account for 25% of global PC sales and 6% of packaged software sales. [Source: IDC]

In the United States, IT was responsible for two-thirds of total factor growth in productivity between 1995 and 2002, and virtually all of the growth in labor productivity. [Source: Information Technology Industry Foundation]

BSA’s publicly traded member companies spent nearly $43 billion on R&D in 2008, equal to 7.1% of their collective revenues. Many of BSA’s member companies invested double or triple that percentage of their

revenues in 2008. [Source: Business Software Alliance]

And where does the drive for that dynamical process come from??? Small and Medium sized businesses.

MicroISVs – YOU !!!

The „big“ picture and its main contributor – the MicroISV !

Companies and the end consumer- writing software for who`s infrastructure?

The broadband access of companies is very high in all of Europe so there definitely is a gap between the potential suppliers of software and their customers. The individual programmer will have to decide to which market he is willing and able to serve. For that he has to undergo intensive training and testing…

IT-Productivity in the EUThe few and … chosen?...among us who actually produce software. How many are they?

The Software industry is still based on few persons that actually have the skills to write software (or even to create own content on web portals etc) and to fulfill the tasks necessary. We can see that from the second (and don`t worry last) statistic from the EU. The degree of productivity is very different with Estonia leading the stats – partially parallel to the built- up infrastructure we have seen in the stats before, but it seems that there are other elements playing a role such as the level of education; priority by the local European governments, and awareness of modern technology. Factors that are not exactly related to the economic numbers of one country.

Some voices on the software industryBig and small

A short zoological excursion:Which big and small combination describes you best:

Or

“Security software vendors that have a balanced mix of channel, new license and maintenance revenue streams and flexibility in contractual terms, such as software as a service (SaaS), open source and outsourcing, have the strongest options for continued growth and to even out the risk”

… The consumer security software market remains the largest security software segment, with 2010 revenue projected to reach $4.2 billion in 2010, up from $3.9 billion in 2009. The endpoint protection platform (enterprise) market is the No. 2 security software segment, with revenue on pace to reach $3 billion in 2010, up from $2.9 billion in 2009.

Credit: Gartner/Contu

“As a professional engineer, designing with steel beams, am I going to trust *anything* to do my calculations that only costs $2? If my beam collapses, do I blame the $2 program in court?”

Credit Gary Elring – Elfringsoft.com

Software Industry – Zoology Part II

or

or

Or ???

Think broad, stay agile, act bigJust think what made this computer great and what enabled its victory building up new industries and enourmous wealth ...well the answer is SOFTWARE. And grasping the potential that the „technology“ of our times is offering is an extremely important here. Networking your ideas and getting inspired within a group of creative people that understand your visions and ideas, sharing knowledge to step ahead – that is where we come in. And I am sure that this 10th European Software Conference will contribute to this effort for not only foreseeing future (income) but also for actually building it!

Some trend speculations for our Software Industry 1. Development of a Common communications infrastructure – which can be accessed through different devices and technologies, removing sources of exclusion and discrimination, allowing the supporting technologies to ‘draw in’ new people and uses and put them in greater touch with one another.

2. Evolution towards Computing as a ubiquitous utility - putting computing on the same footing as water, power and telecommunications.

3. The emergence of the Intelligent Web: - describing the deployment of existing technologies providing ‘intelligence’ to the protocols, structures and internal functions of the Internet itself, rebalances responsibilities and contributions of different stakeholders to overall socioeconomic impacts and creates a powerful ‘pull’ factor for further technological, economic, financial and social innovation..

Credit:Rand for EU Comm TR776

Scenarios for our Software Industry1. Scattered World (closed, private,

competition); reflect a future of cutthroat monopolistic competition, unrestrained by active and effective antitrust and other regulation.

2. Connected World (open, public, collaboration) paints a future where companies collaborate both domestically and internationally, facilitated by governments who take a cooperative lead in setting rules to optimise global public value creation.

3. Borderless World (open, private, competition) depicts a world in which systems connect. It is basically a world where global standards emerged from a shake-out of less favoured standards, and are self-enforcing by virtue of strong customer and user preferences for products that connect to the enormous global investment represented by the Internet.

Credit:Rand for EU Comm TR776

And so all the scary data and insights point to the MicroISV … to us and that REALLY is scary!!!

Enjoy and learn – Opening all senses!The 10th European SoftwareConference