SCOTIABANK MINING CONFERENCEs2.q4cdn.com/343762060/files/doc_presentations/2014-12...SCOTIABANK...

28

SCOTIABANK MINING CONFERENCE December 2-3 2014

Transcript of SCOTIABANK MINING CONFERENCEs2.q4cdn.com/343762060/files/doc_presentations/2014-12...SCOTIABANK...

SCOTIABANK MINING CONFERENCE December 2-3 2014

2

This document contains certain forward-looking statements. Forward-looking statements can generally be identified by the use of statements that include such words as “believe”, “expect”, “anticipate”, “intend”, “plan”, “forecast”, “likely”, “may”, “will”, “could”, “should”, “suspect”, “outlook”, “projected”, “continue” or other similar words or phrases. Specifically, forward-looking statements in this document include, but are not limited to, certain expectations about capital costs and expenditures; capital project commissioning and completion dates; sufficiency of working capital and capital project funding; production of nickel, cobalt, oil and gas, and power; production costs and the global market for nickel. Forward-looking statements are not based on historic facts, but rather on current expectations, assumptions and projections about future events, including commodity and product prices and demand; realized prices for production; earnings and revenues; development and exploratory wells and enhanced oil recovery in Cuba; environmental rehabilitation provisions; availability of regulatory approvals; compliance with applicable environmental laws and regulations; the impact of regulations related to greenhouse gas emissions and credits; debt repayments; collection of accounts receivable; and certain corporate objectives, goals and plans for 2014. By their nature, forward-looking statements require the Corporation to make assumptions and are subject to inherent risks and uncertainties. There is significant risk that predictions, forecasts, conclusions or projections will not prove to be accurate, that those assumptions may not be correct and that actual results may differ materially from such predictions, forecasts, conclusions or projections. The Corporation cautions readers of this document not to place undue reliance on any forward-looking statement as a number of factors could cause actual future results, conditions, actions or events to differ materially from the targets, expectations, estimates or intentions expressed in the forward-looking statements. Key factors that may result in material differences between actual results and developments and those contemplated by this document include global economic and market conditions, and business, economic and political conditions in Canada, Cuba, Madagascar, and the principal markets for the Corporation’s products. Other such factors include, but are not limited to, uncertainties in the development, construction, ramp-up and operation of large mining, processing and refining projects; risks related to the availability of capital to undertake capital initiatives; changes in capital cost estimates in respect of the Corporation’s capital initiatives; risks associated with the Corporation’s joint-venture partners; expectations of the timing of financial completion at the Ambatovy Joint Venture; risk of future non-compliance with financial covenants; potential interruptions in transportation; political, economic and other risks of foreign operations; the Corporation’s reliance on key personnel and skilled workers; the possibility of equipment and other unexpected failures; the potential for shortages of equipment and supplies; risks associated with mining, processing and refining activities; uncertainty of gas supply for electrical generation; uncertainties in oil and gas exploration; risks related to foreign exchange controls on Cuban government enterprises to transact in foreign currency; risks associated with the United States embargo on Cuba and the Helms-Burton legislation; risks related to the Cuban government’s and Malagasy government’s ability to make certain payments to the Corporation; risks related to exploration and development programs; uncertainties in reserve estimates; risks associated with access to reserves and resources; uncertainties in environmental rehabilitation provisions estimates; risks related to the Corporation’s reliance on partners and significant customers; risks related to the Corporation’s corporate structure; foreign exchange and pricing risks; uncertainties in commodity pricing; credit risks; competition in product markets; the Corporation’s ability to access markets; risks in obtaining insurance; uncertainties in labour relations; uncertainty in the ability of the Corporation to enforce legal rights in foreign jurisdictions; uncertainty regarding the interpretation and/or application of the applicable laws in foreign jurisdictions; risks associated with future acquisitions; uncertainty in the ability of the Corporation to obtain government permits; risks associated with governmental regulations regarding greenhouse gas emissions; risks associated with government regulations and environmental, health and safety matters; uncertainties in growth management; interest rate risk; risks related to political or social unrest or change and those in respect of indigenous and community relations; risks associated with rights and title claims; and certain corporate objectives, goals and plans for 2014; and the Corporation’s ability to meet other factors listed from time to time in the Corporation’s continuous disclosure documents. Readers are cautioned that the foregoing list of factors is not exhaustive and should be considered in conjunction with the risk factors described in the Corporation’s other documents filed with the Canadian securities authorities. The Corporation may, from time to time, make oral forward-looking statements. The Corporation advises that the above paragraph and the risk factors described in this document and in the Corporation’s other documents filed with the Canadian securities authorities including, but not limited to, the Corporation’s Annual Information Form for the year ended December 31, 2013 should be read for a description of certain factors that could cause the actual results of the Corporation to differ materially from those in the oral forward-looking statements. The forward-looking information and statements contained in this document are made as of the date hereof and the Corporation undertakes no obligation to update publicly or revise any oral or written forward-looking information or statements, whether as a result of new information, future events or otherwise, except as required by applicable securities laws. The forward-looking information and statements contained herein are expressly qualified in their entirety by this cautionary statement.

CAUTIONARY STATEMENT ON FORWARD-LOOKING INFORMATION

3

EXECUTING ON OUR STRATEGY

4

WHO WE ARE

• A leader in the mining and refining of low cost nickel production with operations in Canada, Cuba and Madagascar

• Largest independent

energy producer in Cuba

• Licenses proprietary technologies and provides metallurgical services to commercial metals operations worldwide

5

FINANCIAL DISCIPLINE

• Maintaining liquidity, and strengthening the balance sheet

• Reducing debt • Restructuring and selling non-core assets

• Any investment case, whether brownfield or

acquisition, will be compared to paying down debt • Enhancing disclosure and communications

CUBAN ENERGY BUSINESS

• Extending long-term oil production profile

FOCUS ON WHAT WE DO BEST: NICKEL

• Building a low-cost, global nickel company • Ramping up at Ambatovy

INVESTOR FOCUS

EXECUTING ON OUR STRATEGY

6

WE ARE FOCUSED ON

COST MANAGEMENT

• Rationalized administration costs • Sale of non-operating assets (Toronto and Fort Saskatchewan real estate)

CAPITAL DISCIPLINE

• Enhanced focus on risk adjusted full cycle economics • Sustaining capital decisions based on investment case • Sulawesi withdrawal

GROUNDWORK FOR GROWTH IN THE LONG-TERM

• Pursuit of low risk optimization projects • Focus on nickel • Long-term diversification into other political jurisdictions will be compared to nickel

opportunities in Cuba

7

FINANCIAL PERFORMANCE IMPROVING

Adjusted EBITDA Contribution by Business Unit

43 60

172 166

2 19

-42 -23

-100

-50

0

50

100

150

200

250

300

($ m

illio

ns)

Metals Oil & Gas Power Corporate

YTD 2013 YTD 20141

$222M $174M

Notes: (1) Includes $12.8 million gain on arbitration settlement in Q3 2014

CORPORATE GOVERNANCE

8

• 5 new Directors appointed since 2012

• 8 Independent Directors, total number of Directors 9

• Helms-Burton Act - meetings with governmental bodies to heighten awareness and encourage involvement

9

WHERE NICKEL IS HEADED

10

LONG-TERM FUNDAMENTALS REMAIN STRONG FOR NICKEL

• Nickel market remains in surplus position with significant LME inventories Strong demand for nickel continues

• Nickel market anticipated to move from surplus to deficit in near term due to:

o Growing impact of Indonesian export ban on nickel supply

o future supply growth of major projects is inadequate to meet continental demand growth

Nickel Market Synopsis

Nickel Supply and Demand Outlook

Nickel Supply and Demand Outlook

Source: Wood Mackenzie

11

LOW COST NICKEL PRODUCER

FOCUS ON NICKEL GROWTH

13

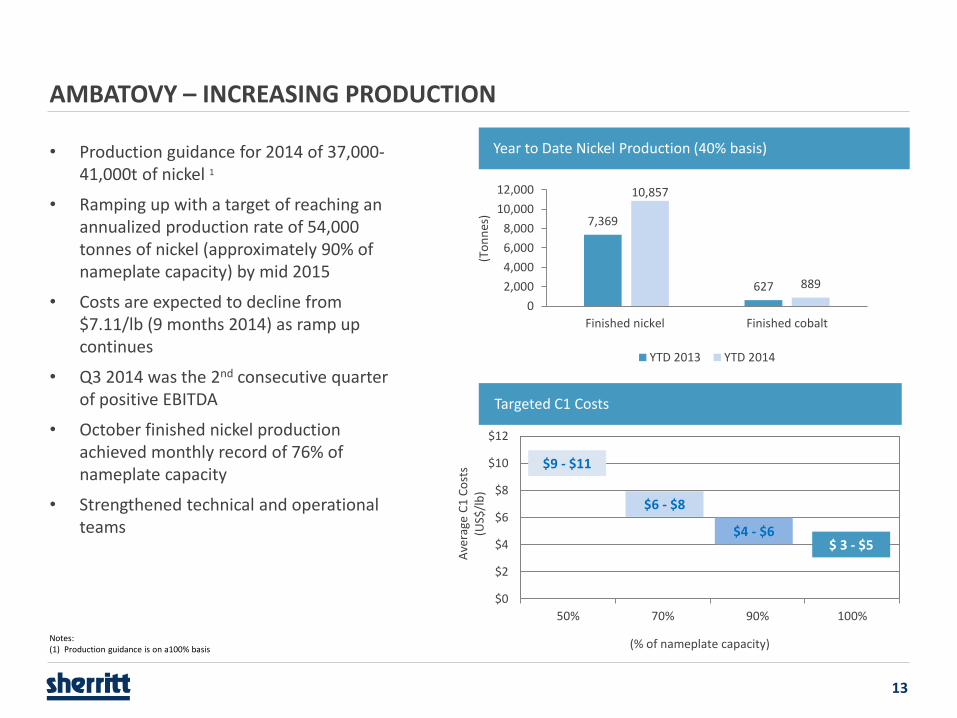

AMBATOVY – INCREASING PRODUCTION

$0

$2

$4

$6

$8

$10

$12

50% 70% 90% 100%

Ave

rage

C1

Co

sts

(U

S$/l

b)

$9 - $11

$ 3 - $5 $4 - $6

$6 - $8

Year to Date Nickel Production (40% basis)

(To

nn

es) 7,369

627

10,857

889

0

2,000

4,000

6,000

8,000

10,000

12,000

Finished nickel Finished cobalt

YTD 2013 YTD 2014

Targeted C1 Costs

(% of nameplate capacity)

• Production guidance for 2014 of 37,000-41,000t of nickel 1

• Ramping up with a target of reaching an annualized production rate of 54,000 tonnes of nickel (approximately 90% of nameplate capacity) by mid 2015

• Costs are expected to decline from $7.11/lb (9 months 2014) as ramp up continues

• Q3 2014 was the 2nd consecutive quarter of positive EBITDA

• October finished nickel production achieved monthly record of 76% of nameplate capacity

• Strengthened technical and operational teams

Notes: (1) Production guidance is on a100% basis

14

AMBATOVY: RAMPING UP THE WORLD’S LARGEST LATERITIC FINISHED NICKEL OPERATION

Counter Current Decantation

B

A

Raw Liquor Neutralization

15

AMBATOVY: ALL RESOURCES FOCUSED ON THE PAL SYSTEM

Mining

Port & Rail

Utilities Systems

Refinery

PAL Systems Work focused

on CCD

Production Component

Q4 2014

• Commission second ore thickener

• Install forced dilution system in CCD#2

• Significant planned maintenance

2015

• No major maintenance planned for H1 2015 (1 autoclave planned)

• Target 90% production for 90 days by end of second quarter

Road Map to Increasing PAL Production Throughput and Achieving Financial Completion

Status

Area of focus Solid-liquid separation carried out by counter-current decantation (CCD)

}

16

AMBATOVY: 5 CERTIFICATES AWAY FROM FINANCIAL COMPLETION

Physical Facilities

Certificate

Mining Certificate

Production Certificate

Port Capacity Certificate

Pipeline Capacity

Certificate

Environmental Certificate

Marketing Certificate

Efficiency Certificate

Legal and Other Conditions Certificate

Financial Certificate

FINANCIAL COMPLETION

17

MOA: CONTINUES TO CONTRIBUTE SIGNIFICANTLY

9 months 2014 Highlights

• Record quarterly production in latest quarter

• Average realized metal prices increased +20% year over year

• Adjusted EBITDA grew by 36% ($15 million) versus YTD 2013

• Executed technology supply contract for the acid plant project

Production Volume (Sherritt’s attributable share)

12,343

1,225

12,123

1,169

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Finished nickel Finished cobalt

(To

nn

es)

YTD 2013 YTD 2014

Nickel Reference Price vs C1 (NDCC) Costs

$7.81

$5.18

0

2

4

6

8

10

12

2011 2012 2013 YTD 2014

US

$/l

b

Nickel Reference Price vs C1 (NDCC) Costs

Cash Cost Reference Price

18

OUR ENERGY BUSINESS

19

OIL AND GAS – EXTENDING PRODUCTION PROFILE IN CUBA

• Produces approximately 20,000 bpd (gross)

o Focused on extending production over the long-term given existing production sharing contracts set to expire in 2017/2018

o Extended a production sharing contract in Cuba for an additional 10 year term to 2028 on new wells

• Waiting for approvals on four exploration blocks from the Cuban Government

• Exploring alternatives for non-core international assets

Production Volumes Operating Costs (Cuba)

20,144

11,255

19,710

11,160

0

5,000

10,000

15,000

20,000

25,000

Gross working-interest -Cuba

Total net working interest

(bo

epd

)

YTD 2013 YTD 2014

$6.58

$8.12

$0

$2

$4

$6

$8

$10

YTD 2013 YTD 2014

($ p

er b

arre

l)

20

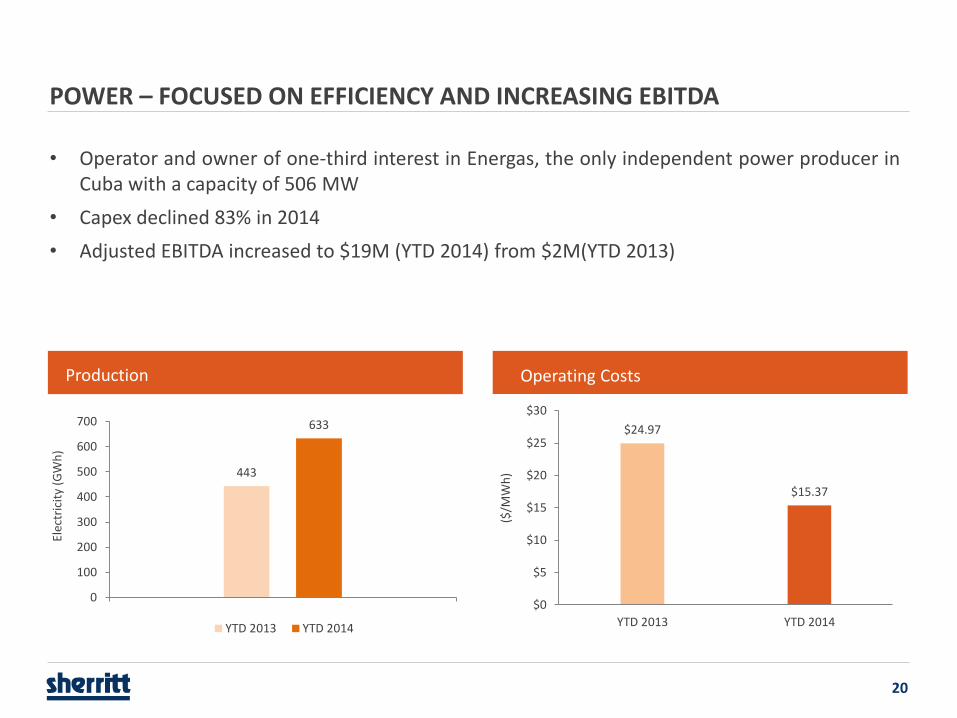

POWER – FOCUSED ON EFFICIENCY AND INCREASING EBITDA

• Operator and owner of one-third interest in Energas, the only independent power producer in Cuba with a capacity of 506 MW

• Capex declined 83% in 2014

• Adjusted EBITDA increased to $19M (YTD 2014) from $2M(YTD 2013)

Production Operating Costs

$24.97

$15.37

$0

$5

$10

$15

$20

$25

$30

YTD 2013 YTD 2014

($/M

Wh

) 443

633

0

100

200

300

400

500

600

700

1

Elec

tric

ity

(GW

h)

YTD 2013 YTD 2014

FINANCIAL HIGHLIGHTS

22

STRENGTHENING THE BALANCE SHEET

$250 $250 $250

$275

0

100

200

300

400

500

600

2014 2015 2016 2017 2018 2019 2020 2021 2022

($ m

illio

ns)

Pre refinancing Post refinancing

$400

$500

Notes

(1) Amounts at September 30, 2014 have been adjusted to reflect the purchase of $275 million of 7.75% debentures due October 15, 2015, $150 million of 8.00% debentures due November 15, 2018, and $250 million 7.50% debentures due September 24, 2020, issuance of $250 million of 7.875% Senior Unsecured Notes due October 11, 2022, and related fees. These transactions will be completed in the fourth quarter.

Cash & short term investments Total debt Long-term debt to total assets

980.3 2,214.0

39%

• Recently reduced debt by $425 million, extended maturities and reduced principal amounts outstanding • Total debt repaid in 2014 of $790 million

504.0 1,785.0

34%

($ millions, except as noted, as at) September 30, 2014 September 30, 2014

Adjusted (1)

Debenture/Notes Maturity Profile

23

YEAR TO DATE 2014 FINANCIAL HIGHLIGHTS

$78.9

YTD 2013 YTD 2014

Adjusted Revenue 1 ($ millions)

$174

$222

YTD 2013 YTD 2014

Adjusted EBITDA 1($ millions) Adjusted Continuing Operating

Cash Flow 1($ Per Share)

YTD 2013 YTD 2014

$858

$0.25

$0.31

$594

Notes: (1) Refers to a non-GAAP measure. Please see additional information in the MD&A and Financial Statements for Q3, 2014 on the Company’s website or on www.sedar.com

24

INVESTMENT SUMMARY

Our strategic focus and execution is producing results

• Nickel production growth and leverage to nickel prices to contribute to increasing cash flow

• Extending life of oil business and optimizing operations (Moa acid plant)

• Continued focus on cost reductions and sale of non-core assets

• Renewed capital allocation process with a focus on risk adjusted returns

• Laying the groundwork for future growth opportunities

25

APPENDIX

A LEADER IN SUSTAINABILITY

26

• Strong safety performance - 35 per cent reduction in

lost-time injury incident rate and no fatalities during 2013

• Wins prestigious Nedbank Capital Sustainable Business

Award for Ambatovy Nickel Operation

• Recognized by UN and Government of Madagascar as

one of the country's best private sector providers of

humanitarian aid

27

Revenue Generated by Ambatovy (100%)

Payment of Operating Expenses (100%)

Payment of Debt Service (2 parts) (100%)

Funding of Maintenance Capital (100%)

1. Interest @ LIBOR + 140 bps 2. Principal repayments made semi-annually (June, Dec)

Distributable Cash Flow (100%)

Sherritt Sumitomo KORES

40% 27.5%

30% x 40% (1) 70% x 40% Partner Loan Repayment

subtract

subtract

subtract

equals

AMBATOVY DISTRIBUTABLE CASH FLOW

SNC-Lavalin

27.5% 5%

(1) Distributable cash flow to Sherritt until partner loans repaid.

28

Sherritt International Corporation 1133 Yonge Street, Toronto, Ontario, Canada M4T 2Y7

Telephone: 416-935-2451

Toll-Free: 1-800-704-6698

Email: [email protected] Website: www.sherritt.com