SCM Project

12

March 22nd 201 0 Karthik Regunathan PGP25304 Rahul Tom Joseph PGP25317 “Impact of GST on the Fast Moving Consumer Goods Sector”

-

Upload

rahul-tom-joseph -

Category

Documents

-

view

236 -

download

1

Transcript of SCM Project

March 22nd 2010

Karthik Regunathan PGP25304 Rahul Tom Joseph PGP25317

“Impact of GST on the Fast Moving Consumer Goods Sector”

INTRODUCTION:

Goods and Services Tax:

Of the many fiscal initiatives of the reinstated UPA government, the rolling out of the Goods and Services Tax promises to be the most significant initiative of Independent India. Initially envisaged to be in place by April 1, 2010 the GST would result in a major rationalization and simplification of the consumption tax structure at both the centre and state levels by replacing all central and state level indirect taxes such as value added tax (VAT), excise duty, service tax, entertainment tax among others bring relief to the common man.

GST: An Executive Summary

GST is the most ambitious indirect tax reform in India ever attempted and aims to create one “borderless domestic market”. It will tax consumption as against “production” which is the current norm. A uniform rate will be imposed on a product only once, at the point of its supply, thus reducing the cost for consumers.

Key benefits: If GST is implemented without many exemptions and with a single rate, the following benefits will accrue:

Macro: Successful pan-India implementation will add 1-1.7 % to the GDP and boost the tax/GDP ratio.

Micro: Incidence of tax will come down in case of manufactured goods. However, in case of services the incidence and coverage of tax may rise resulting in higher prices.

Industry: Volume growth will accrue as incidence of taxation is minimized. Also, supply chain efficiencies will accrue as there will be no need for multiple depots and warehouses.

Likely beneficiaries: Auto, FMCG, Logistics sectors

GST is not just VAT + Service tax, but an improvement over the previous VAT and disjointed services tax:

Will remove cascading effect of taxes and include comprehensively more indirect Central taxes and integrate goods and services taxes for set-off relief, but also capture certain value addition in the distributive trade.

A continuous chain of set-off from the original producer’s point and service provider’s point up to the retailers level would be established which would eliminate the burden of all cascading effects, including the burden of CENVAT and service tax.

Current tax structure consists of a plethora of central and state levies…

The proposed structure wherein a host of taxes will be subsumed in GST…

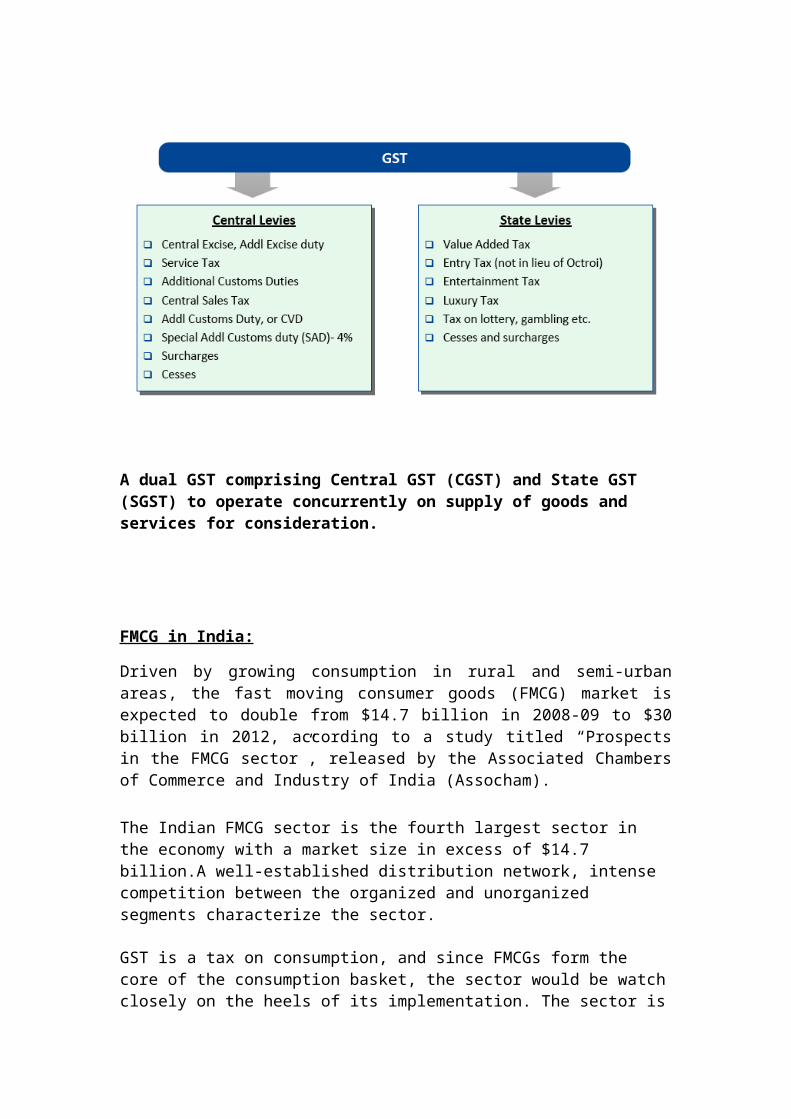

A dual GST comprising Central GST (CGST) and State GST (SGST) to operate concurrently on supply of goods and services for consideration.

FMCG in India:

Driven by growing consumption in rural and semi-urban areas, the fast moving consumer goods (FMCG) market is expected to double from $14.7 billion in 2008-09 to $30 billion in 2012, according to a study titled “Prospects in the FMCG sector”, released by the Associated Chambers of Commerce and Industry of India (Assocham).

The Indian FMCG sector is the fourth largest sector in the economy with a market size in excess of $14.7 billion.A well-established distribution network, intense competition between the organized and unorganized segments characterize the sector.

GST is a tax on consumption, and since FMCGs form the core of the consumption basket, the sector would be watch closely on the heels of its implementation. The sector is bound to witness many gainers and closers, depending crucially on the base and rates of the GST.

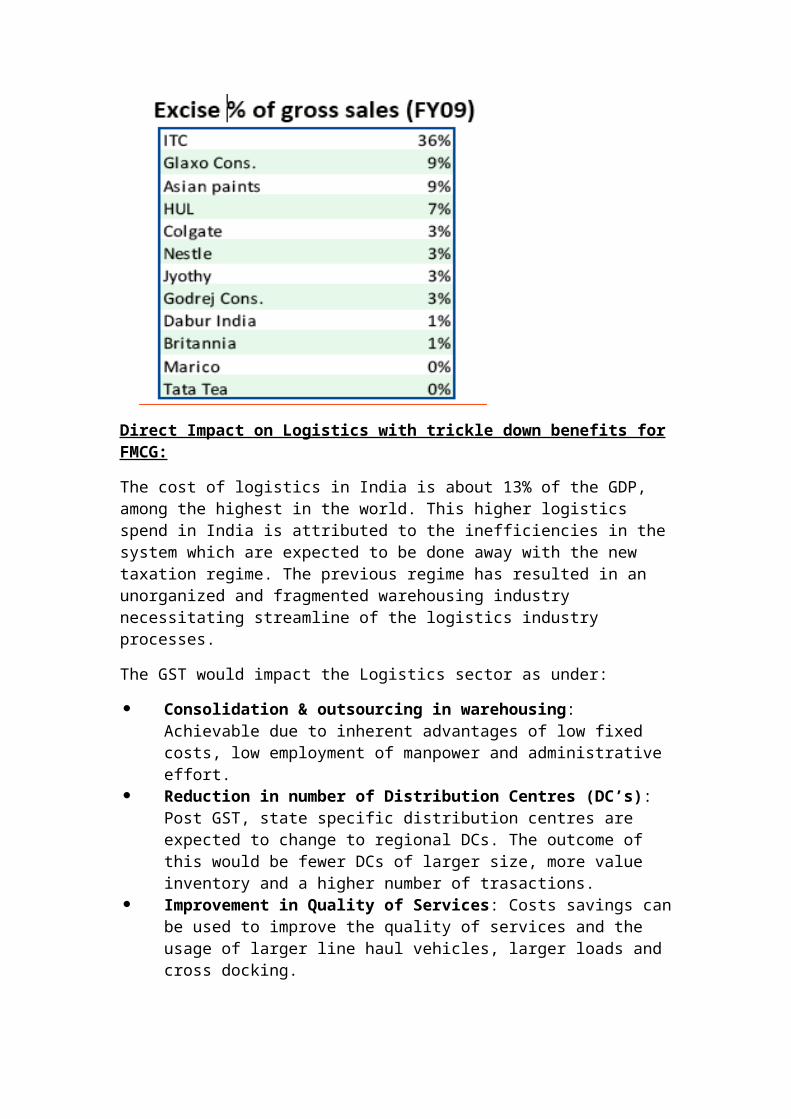

Currently both centre and state tax rates vary- central value added tax (CENVAT) duty varies from 0-14 % (reduced to 8% under the fiscal stimulus package) and the state VAT varies between 0% and 12.5%. Indications are that the combined centre and state GST on FMCGs could range between 12% and 14%, if applied at a single rate. At this rate, the total burden on FMCG’s should remain approximately the same as under the current structure. However, it would lead to simplication in the tax structure and would mitigate the disputes relating to classification of goods into various tax rate categories and determination of factory price for application of CENVAT.

However, if food and other basic necessities were to be exempted or made taxable at a lower rate, then the standard rate for other goods and services could be pushed up to 18% or more. This could lead to disputes on classification of goods to the two rate categories. Leaving aside the issue of rates, many benefits are to be realized with respect to simplification of the supply chain which are summarized thus:

Impact of GST on the FMCG Supply Chain:

The introduction of GST is expected to build best-in-class capability in supply chain as well as people capability and enhance India’s cost leadership position by eliminating inefficiencies in supply chain and taxation:

Multiple Route-to-market models: Upto 35% reduction possible in time-to-market.

Simplification of Supply Chain: With the elimination of central sales tax, manufacturers could implement a centralized warehousing and distribution centre and need not set up distribution depots in individual states and make inter-state sales via consignment agents.

Elimination of Tax Cascading: Currently, FMCG dealers cannot claim a credit for the service tax paid on their inputs. Restrictions also apply on claiming credits for VAT on inputs other than goods for resale.

Reduction in Inventory Costs: Currently, the CENVAT is included in inventory costs, because of which the dealers costs increase. Under the new

structure, the GST paid on inventory would be fully recoverable as input tax credit, reducing the inventory financing costs.

Cash Flow benefit from tax: The dealers would be collecting GST from their customers as they make sales, but would be required to remit it to the government only at the end of the month or the quarter, when they file their returns. This extra cash float would be like a recurring interest-free loan from the government each quarter.

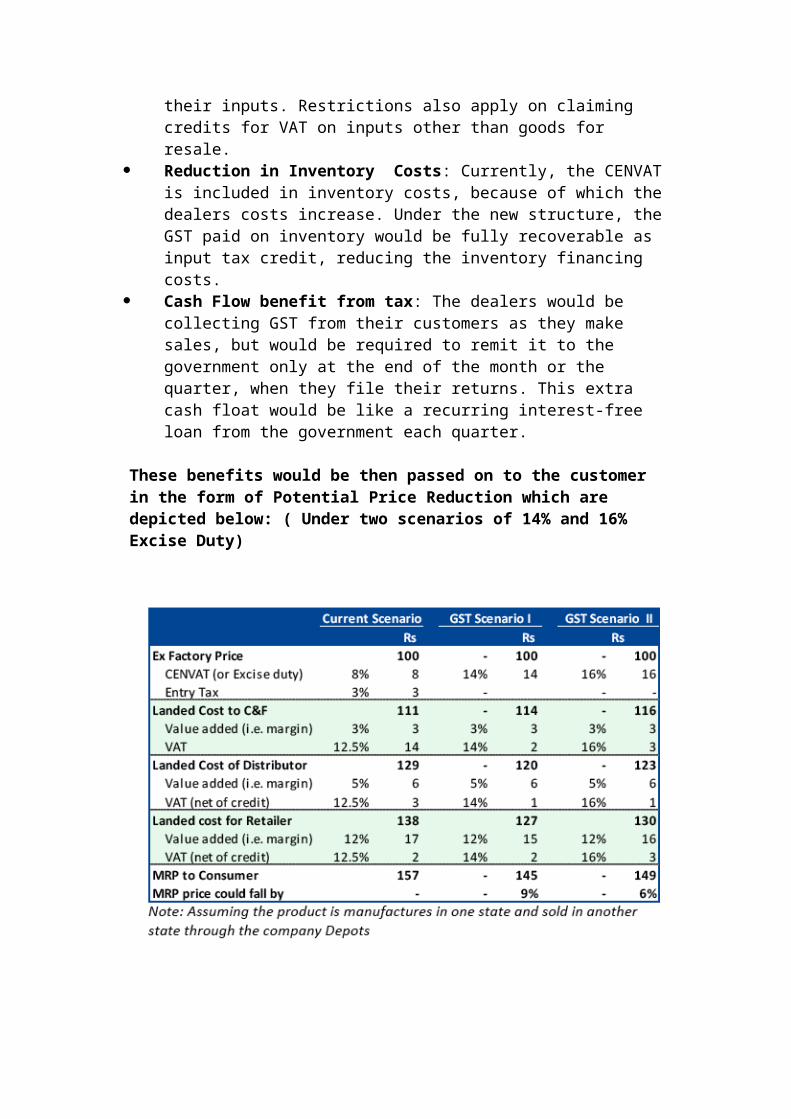

These benefits would be then passed on to the customer in the form of Potential Price Reduction which are depicted below: ( Under two scenarios of 14% and 16% Excise Duty)

Direct Impact on Logistics with trickle down benefits for FMCG:

The cost of logistics in India is about 13% of the GDP, among the highest in the world. This higher logistics spend in India is attributed to the inefficiencies in the system which are expected to be done away with the new taxation regime. The previous regime has resulted in an unorganized and fragmented warehousing industry necessitating streamline of the logistics industry processes.

The GST would impact the Logistics sector as under:

Consolidation & outsourcing in warehousing: Achievable due to inherent advantages of low fixed costs, low employment of manpower and administrative effort.

Reduction in number of Distribution Centres (DC’s): Post GST, state specific distribution centres are expected to change to regional DCs. The outcome of this would be fewer DCs of larger size, more value inventory and a higher number of trasactions.

Improvement in Quality of Services: Costs savings can be used to improve the quality of services and the usage of larger line haul vehicles, larger loads and cross docking.

Alleviation of complexities in documentation and inter State barriers: Through a uniform and seamless application of CGST & SGST irrecoverable taxes such as Central Sales Tax (CST), complex documentation of inter State movement of goods, entry barriers at state borders resulting in long transportation times and imposition of local levies such as entry taxes and octroi upon physical entry of goods into designated areas can be done away with.

Analysis:

In order to satisfy the set of customer needs through its products and services, the firms operating in the FMCG space need to achieve a consistency between their Business Strategy, Product Development Strategy, Marketing & Sales Strategy and Supply Chain Strategy.

As identified earlier, the supply chain strategy which revolves around Operations, Distribution and Service is geared towards cost leadership by the implementation of GST, all while improving quality of service.

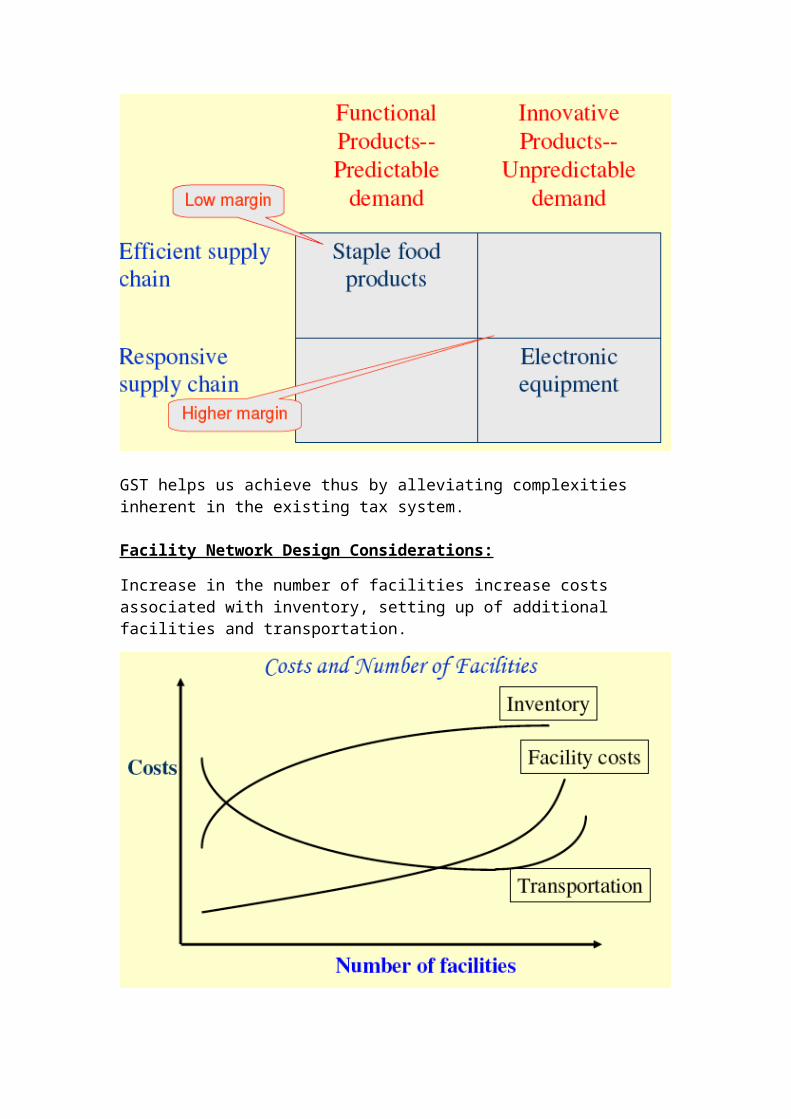

In the FMCG sector, there is a need for an efficient supply chain as consumer goods typically depict predictable demand, explaining their low margins.

GST helps us achieve thus by alleviating complexities inherent in the existing tax system.

Facility Network Design Considerations:

Increase in the number of facilities increase costs associated with inventory, setting up of additional facilities and transportation.

As discussed earlier, the elimination of the Central Sales Tax can help the industry work towards consolidation of warehouses and distribution centres, reducing the number of facilities and thereby the overall logistics costs.

Same has a direct impact on response time, and the savings realized by facility reduction along with the multiple route-to-market models that have opened up, could lead to a 35% reduction in time-to-market.

Recommendations:

Based on the secondary data collected, and the subsequent analysis of the FMCG sector the following recommendations have been tabulated for the benefit of the policy makers:

Extended date of implementation: Setting of the deadline as October, 2010 as opposed to April 1, 2010 would help the Centre solve any and all disputes related to its implementation with the States leading to a flawless roll-out.

Removal of classification between goods and services: To ensure there are no classification disputes, leading to more complications and delays.

Removal of existing area based exemptions: the existing area based exemptions in respect of CENVAT should be discontinued and if need be a direct investment linked cash subsidy may be provided to support the industry, for balanced regional development. The idea is to not break the GST chain with regard to both CGST & SGST.

Recommendations to impacted firms:

Counter increased compliance costs with compressed supply chains: The challenge and the opportunity is to compress supply chains for GST efficiency while ensuring that the business objectives in and around supply chains are also met. The dual GST consequently affords companies significant opportunities for realignment of procurement, manufacturing and distribution / sales patterns and to engineer their supply chains on purely economic considerations as opposed to fiscal considerations. For this purpose, a comprehensive GST impact assessment would need to be carried out.

Re-engineering of supply chains: Based on the information available around the structure of dual GST, the potential issues and areas of impact for a particular company could be identified and a detailed mapping of the ‘as is’ supply chain and the associated current tax costs would be done. Thereafter, the impact of the dual GST on this 'as is' model could be worked out and alternatives/options could be developed for changes in the supply chain business model in order to ensure that both the supply chain as well as the business model are GST efficient. Some of the options around re-engineering the supply chain would relate to decisions on indigenous supplies vis-à-vis imports; Intra-State vis-à-vis Inter-State procurement manufacturing service/warehousing & stocking locations, in-house v/s contract manufacturing, direct sales v/s stock transfers etc.

Bibliography:

“Prospects in the FMCG Sector” a study by ASSOCHAM (Associated Chambers of Commerce and Industry of India)

“A primer on GST” by Sachchidanand Shukla- Sr VP & Economist, Enam Securities

“GST Thought leadership series” by Satya Poddar, Tax Partner, Ernst & Young published in the Financial Express.

“India after GST- Logistics and beyond” by Indian Supply Chain Council

“Impact of Dual GST on supply chains” by S Madhavan, Leader, Indirect Tax Practice, PricewaterhouseCoopers

“White paper on implementation of GST in India”- 13th Empowered Committee of Finance Ministers, 11th November 2009

“Recommendations of GST Task Force”- Finance Commision, 17th December 2009

Sunil Chopra and Peter Meindl, Supply Chain Management: Strategy, Planning & Operation, 3rd Edition, Pearson Education India, 2008.