SCHOOL OF LAW LAW413 BANKING LAW A. GENERAL …

50

1 SCHOOL OF LAW Year 2013/14 Term 2 LAW413 BANKING LAW Instructor: Professor John Phillips Visiting Professor Tel: 6828 0xxx (to be confirmed) Email: [email protected] Office: School of Law, Level x, Room xxxx (to be confirmed) A. GENERAL SCOPE OF THE MODULE The law of banking is a topic of fundamental importance in market economies. Banks as providers of deposit and savings accounts, payment mechanisms, and finance are crucial to all sectors of commerce. A significant sector of the legal profession provides advice to the banking industry and this course will be helpful to those seeking to work in that sector. The initial part of the course will focus upon the duties and obligations of banks and their customers, in particular, in respect of payment methods. In this context there will be an analysis of those legal principles which enable a bank (or its customer) to recover mistaken payments, as well as an examination of the bank's liability for the fraudulent activities of third parties. More generally, there will be a consideration of the bank’s responsibility as a fiduciary and its duty of confidentiality to its customer. The second part of the course will then be devoted to the pivotal role of the bank as a finance provider. There will be a consideration of different types of loan, together with legal mechanisms that are available, or may be utilised, to secure their repayment (for example, guarantees, set–offs, security over receivables and liens). Particular emphasis will be placed on problems of drafting. Attention will also be given to the bank's role in financing international trade through performance bonds and letters of credit. B. SPECIFIC TOPICS (SEE HANDOUTS, SECTION I – VI FOR DETAILS) I. Introductory matters – functions, definitions and the banker–customer relationship. II. The Bank and payment mechanisms. III. Recover of mistaken payments.

Transcript of SCHOOL OF LAW LAW413 BANKING LAW A. GENERAL …

1

SCHOOL OF LAW Year 2013/14 Term 2 LAW413 BANKING LAW Instructor: Professor John Phillips Visiting Professor Tel: 6828 0xxx (to be confirmed) Email: [email protected] Office: School of Law, Level x, Room xxxx (to be confirmed) A. GENERAL SCOPE OF THE MODULE The law of banking is a topic of fundamental importance in market economies. Banks as providers of deposit and savings accounts, payment mechanisms, and finance are crucial to all sectors of commerce. A significant sector of the legal profession provides advice to the banking industry and this course will be helpful to those seeking to work in that sector. The initial part of the course will focus upon the duties and obligations of banks and their customers, in particular, in respect of payment methods. In this context there will be an analysis of those legal principles which enable a bank (or its customer) to recover mistaken payments, as well as an examination of the bank's liability for the fraudulent activities of third parties. More generally, there will be a consideration of the bank’s responsibility as a fiduciary and its duty of confidentiality to its customer. The second part of the course will then be devoted to the pivotal role of the bank as a finance provider. There will be a consideration of different types of loan, together with legal mechanisms that are available, or may be utilised, to secure their repayment (for example, guarantees, set–offs, security over receivables and liens). Particular emphasis will be placed on problems of drafting. Attention will also be given to the bank's role in financing international trade through performance bonds and letters of credit. B. SPECIFIC TOPICS (SEE HANDOUTS, SECTION I – VI FOR DETAILS)

I. Introductory matters – functions, definitions and the banker–customer relationship.

II. The Bank and payment mechanisms. III. Recover of mistaken payments.

2

IV. The Bank’s duty of confidentiality. V. The Bank in an advisory role. VI. The Bank as a finance provider.

a. Different types of facility (including the impact and drafting of important clauses).

b. Mechanisms for protecting the lender’s position. c. Guarantees and mortgages: case studies in the execution, maintenance and

enforcement of securities. d. The Bank and trade finance.

Some topics will be covered in more detail than others. It is anticipated that about half the hours will be devoted to Section VI (The Bank as Finance Provider). C. READING MATERIAL Selected pages from: Ellinger’s Modern Banking Law (E.P. Ellinger, E Lomnicka, C.V.M. Hare) OUP, 5th ed 2011 (hereafter, Ellinger). Banking Law (Po Chu Chai) LexisNexis, 2nd ed 2011 (hereafter Po Chu Chai). The Modern Contract of Guarantee (J Phillips) Sweet and Maxwell, 2nd English ed 2010 (hereafter Phillips). For occasional references: Principles of Banking Law (R Cranston) 2002, reprinted 2006 (hereafter Cranston). Articles and Cases as set out on the Handouts Copies of Ellinger and Poh Chu Chai will be made available in the library and the bookshop. If purchasing the books, it might be sensible for several students to club together to purchase a single copy since it is not necessary to read the whole book. The reading is directed to specific pages only in each work. Copies of the relevant pages in Phillips will be photocopied for students. D. ASSESSMENT Assessment will take the following form:

1. 10% for general class participation 2. 10% for leading discussion on hypothetical case study or a specific topic. (These will

be group projects). 3. 30% for writing a legal opinion on a hypothetical case study, or writing an essay on a

specific topic( to be written and assessed individually) 4. 50% for an examination.

3

Academic Integrity All acts of academic dishonesty (including, but not limited to, plagiarism, cheating, fabrication, facilitation of acts of academic dishonesty by others, unauthorized possession of exam questions, or tampering with the academic work of other students) are serious offences. All work presented in class must be the student’s own work. Any student caught violating this policy may result in the student receiving zero marks for the component assessment or a fail grade for the course. This policy applies to all works (whether oral or written) submitted for purposes of assessment. Where in doubt, students are encouraged to consult the instructors of the course. Details on the SMU Code of Academic Integrity may be accessed at http://www.smuscd.org/resources.html.

4

I. Introductory matters: Functions, Definitions and the Banker– Customer

relationship

A. FUNCTIONS AND DEFINITION OF A BANK

Cranston pp 1 – 12 and Poh Chu Chai pp 11 – 25

Banking Act (Statutes of the Republic of Singapore Cap 19, Rev Ed 2008), s 2.

“bank” means any company which holds a valid licence under section 7 or 79; “banking business” means the business of receiving money on current or deposit account, paying and collecting cheques drawn by or paid in by customers, the making of advances to customers, and includes such other business as the Authority may prescribe for the purposes of this Act;”

s 4(1) “No banking business shall be transacted in Singapore except by a company which is in possession of a valid licence granted under this Act by the Authority authorising it to conduct banking business in Singapore.”

Note also the use of term “banking business’ in other Statutes in Singapore Bills of Exchange Act (Statutes of the Republic of Singapore, Cap 23, Rev Ed 1999), s 2.

“‘banker’ includes a body of persons, whether incorporated or not, who carry on the business of banking.”

See generally on the meaning of “banking business”: *Vernes Asia Ltd v Trendale Investment Pte Ltd [1988] 1 MLJ 357. *United Dominions Trust Ltd v Kirkwood [1966] 2 QB 431. Re Roes’ Legal Charge [1982] 2 Lloyds Rep 370. Consequential definitions arising from the definition of “banking business”

Current account.

Deposit account.

Cheques (and payment and collection of cheques).

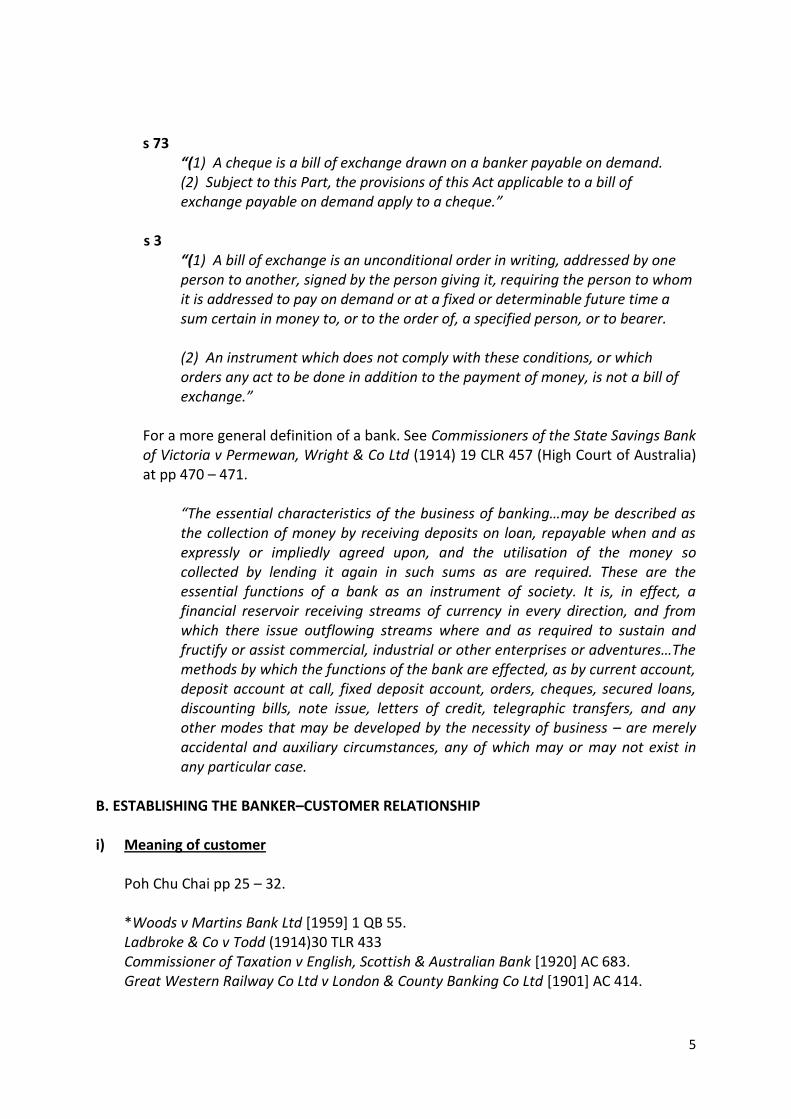

See the definition of a cheque in the Bills of Exchange Act (Statutes of the Republic of Singapore, Cap 23, Rev Ed 1999), ss 73, s 3 and see also Ellinger pp 386 – 389.

5

s 73

“(1) A cheque is a bill of exchange drawn on a banker payable on demand. (2) Subject to this Part, the provisions of this Act applicable to a bill of exchange payable on demand apply to a cheque.”

s 3

“(1) A bill of exchange is an unconditional order in writing, addressed by one person to another, signed by the person giving it, requiring the person to whom it is addressed to pay on demand or at a fixed or determinable future time a sum certain in money to, or to the order of, a specified person, or to bearer. (2) An instrument which does not comply with these conditions, or which orders any act to be done in addition to the payment of money, is not a bill of exchange.”

For a more general definition of a bank. See Commissioners of the State Savings Bank of Victoria v Permewan, Wright & Co Ltd (1914) 19 CLR 457 (High Court of Australia) at pp 470 – 471.

“The essential characteristics of the business of banking…may be described as the collection of money by receiving deposits on loan, repayable when and as expressly or impliedly agreed upon, and the utilisation of the money so collected by lending it again in such sums as are required. These are the essential functions of a bank as an instrument of society. It is, in effect, a financial reservoir receiving streams of currency in every direction, and from which there issue outflowing streams where and as required to sustain and fructify or assist commercial, industrial or other enterprises or adventures…The methods by which the functions of the bank are effected, as by current account, deposit account at call, fixed deposit account, orders, cheques, secured loans, discounting bills, note issue, letters of credit, telegraphic transfers, and any other modes that may be developed by the necessity of business – are merely accidental and auxiliary circumstances, any of which may or may not exist in any particular case.

B. ESTABLISHING THE BANKER–CUSTOMER RELATIONSHIP i) Meaning of customer

Poh Chu Chai pp 25 – 32. *Woods v Martins Bank Ltd [1959] 1 QB 55. Ladbroke & Co v Todd (1914)30 TLR 433

Commissioner of Taxation v English, Scottish & Australian Bank [1920] AC 683. Great Western Railway Co Ltd v London & County Banking Co Ltd [1901] AC 414.

6

ii) Some incidents of the relationship to be analysed later in the course in specific contexts

Bank’s obligation to comply strictly with its mandate.

Customer’s contractual duties.

Bank’s/customer’s duty of care.

Bank’s fiduciary obligations.

Bank’s duty of confidence.

Bank’s rights to combine account and take advantage of statutory defences. C. NATURE OF BANKER – CUSTOMER RELATIONSHIP

Ellinger pp 115 – 119. Poh Chu Chai pp 466 – 476. *Foley v Hill (1848) HL Cases 28 at 36. Joachimson v Swiss Bank Corp [1921] 3 KB 110. Woodland v Fear (1857) 7 El & Bl 519. *Damayanti Kontilal Doshi v Indian Bank [1999] 4 SLR 1, esp at 11 (discussed Poh Chu Chai pp 472 – 473). Vroegop “The status of bank branches” *1990+ JIBL 445. Arab Bank Ltd v Barclays Bank plc [1954] AC 495. Note, however, the impact of the principal – agent relationship in relation to payment instructions (see Handout II below).

D. TERMS OF THE BANKER – CUSTOMER RELATIONSHIP i) Express Terms: problems of incorporation

Burnett v Westminster Bank [1966] 1 QB 742. ii) Implied terms

Common law rules AG of Belize v Belsize Telecom Ltd [2009] UKPC 11.

Banking usage as a source of implied terms Hare v Henty (1861) 10 CBNS 65 at 67 “a man who employs a banker is bound by the usage of bankers”. Requirement of customer’s knowledge? *Turner v Royal Bank of Scotland [2001] 1 All ER (Comm) 664.

7

*Emerald Meats (London) Ltd v AIB Group (UK) Ltd [2002] EWCA Civ 460. Lloyds Bank plc v Voller [2002] 2 All ER (Comm) 978.

iv) Application of Unfair Contract Terms Act (Statutes of the Republic of Singapore Cap

396, Rev Ed 1977) (Considered later in relation to specific clauses and drafting problems) Proctor “International Banking & Unfair Contract Terms” *1999+ JIBFL 230.

8

II. The bank and payment mechanisms

A. GENERAL i) Nature of Funds Transfer

Ellinger pp 599 (2nd para) – 560. *R v Preddy [1996] AC 815 (Adjustment of balances on bank accounts of payor and payee).

ii) Clearing + Settlement

Ellinger pp 362 – 367. Barclay’s Bank plc v Bank of England [1985] 1 All ER 385 at paras 7 – 12.

B. TRANSFERS BY CHEQUE i) Definition and function of a cheque

See Handout I, section A

ii) Cheque clearing systems

Barclays Bank plc v Bank of England [1985] 1 All ER 385 at paras 1 – 14. Ellinger pp 392 (last para) – 394. Vroegop [1990] LMCLQ 244. Bills of Exchange Act (Cap 23 Rev. ed 2004) ss 89 –90 (Cheque truncation). City Hardware Pte Ltd Goh v Boon Chye [2005] 1 SLR 754 (Discussed Poh Chu Chai pp 802– 804).

iii) Position and liability of paying bank

Ellinger [1985] OXJLS 293.

a) Requirement of Compliance with Mandate

Strict Compliance

Poh Chu Chai pp 463– 466.

9

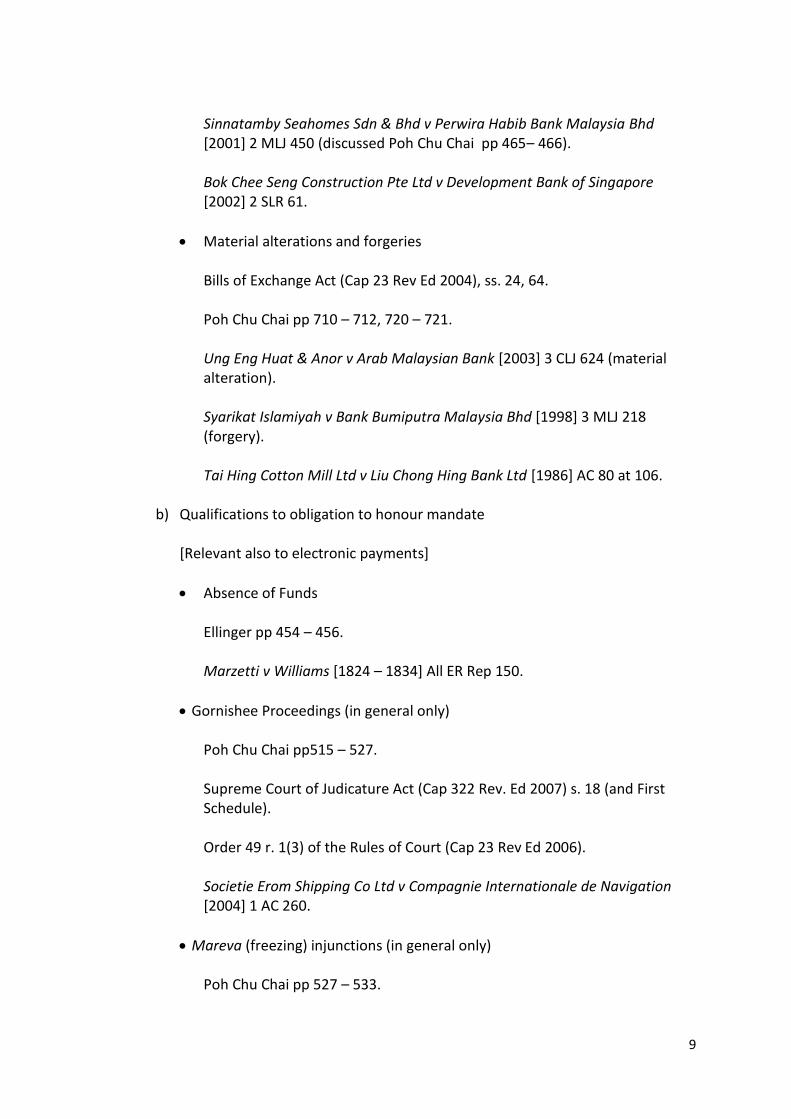

Sinnatamby Seahomes Sdn & Bhd v Perwira Habib Bank Malaysia Bhd [2001] 2 MLJ 450 (discussed Poh Chu Chai pp 465– 466).

Bok Chee Seng Construction Pte Ltd v Development Bank of Singapore [2002] 2 SLR 61.

Material alterations and forgeries

Bills of Exchange Act (Cap 23 Rev Ed 2004), ss. 24, 64. Poh Chu Chai pp 710 – 712, 720 – 721. Ung Eng Huat & Anor v Arab Malaysian Bank [2003] 3 CLJ 624 (material alteration). Syarikat Islamiyah v Bank Bumiputra Malaysia Bhd [1998] 3 MLJ 218 (forgery).

Tai Hing Cotton Mill Ltd v Liu Chong Hing Bank Ltd [1986] AC 80 at 106.

b) Qualifications to obligation to honour mandate

[Relevant also to electronic payments]

Absence of Funds Ellinger pp 454 – 456. Marzetti v Williams [1824 – 1834] All ER Rep 150.

Gornishee Proceedings (in general only)

Poh Chu Chai pp515 – 527. Supreme Court of Judicature Act (Cap 322 Rev. Ed 2007) s. 18 (and First Schedule). Order 49 r. 1(3) of the Rules of Court (Cap 23 Rev Ed 2006). Societie Erom Shipping Co Ltd v Compagnie Internationale de Navigation [2004] 1 AC 260.

Mareva (freezing) injunctions (in general only)

Poh Chu Chai pp 527 – 533.

10

Civil Law Act (Cap 43 Rev. Ed 1999) s. 4(10).

Facilitating Criminal Activity

Poh Chu Chai pp 601 – 610. Corruption, Drug Trafficking and Other Serious Crime (Confiscation of Benefits) Act (Cap 65A Rev Ed 2000) ss 39, 48. Terrorism (Suppression of Financing) Act (Cap 325 Rev Ed 2003) s 8.

Dilemmas for the banks Tayeb v HSBC Bank Plc [2004] 2 All ER (Comm) 880. C v S [1999] 2 All ER 343. [These cases will be considered under electronic payments]

Insolvency

Poh Chu Chai pp 508 – 513 (only in general terms).

Death/ Mental Disorder (only in general terms)

Poh Chu Chai pp 502 – 505.

Countermand

Poh Chu Chai pp 493 – 500. Westminster Bank v Hilton (1926) 43 TLR 124. Curtice v London & City Midland Bank [1908] 2 KB 293.

Liggett defence [See below: mistaken payments]

Bank as Constructive Trustee [See below: mistaken payments]

c) Payor’s bank liability for failing to pay cheque in accordance with the mandate

Ellinger pp 509 – 513. Kpohraror v Woolwich Building Society [1996] 4 All ER 119 (Noted Hooley [1996] CLJ 189; Enonchong (1997) 60 MLR 412).

d) Duty of care and its relationship to requirement to obey mandate

11

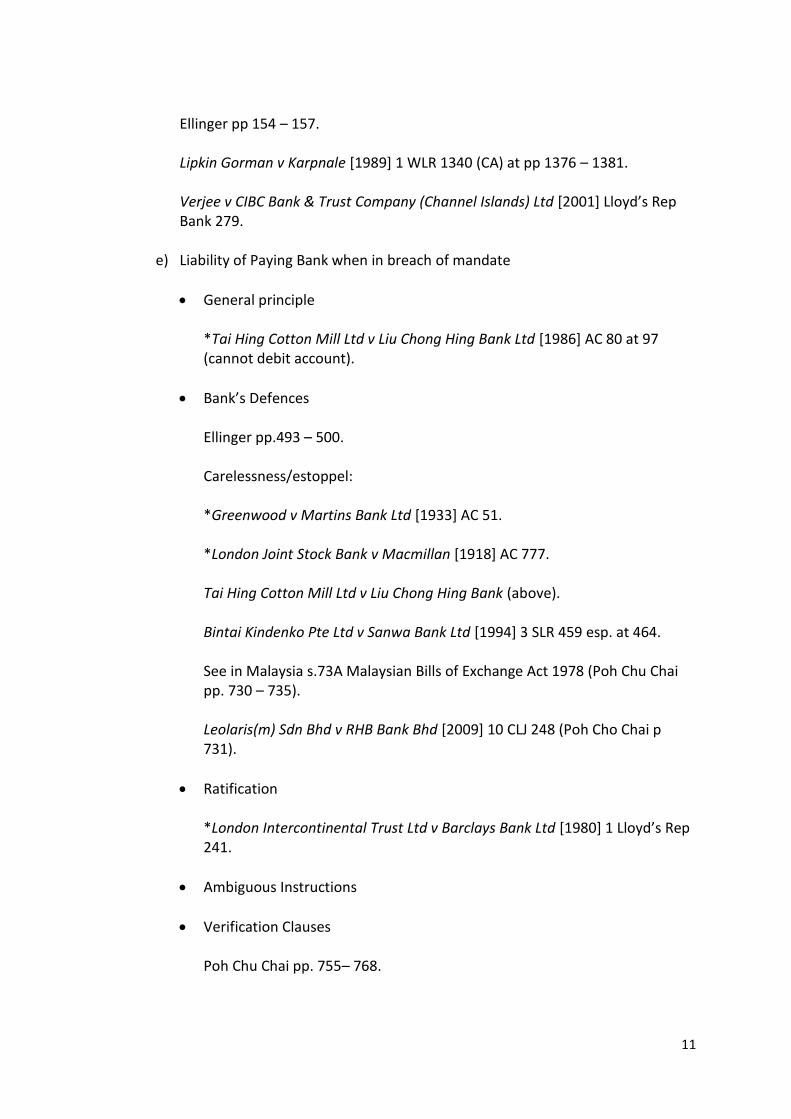

Ellinger pp 154 – 157. Lipkin Gorman v Karpnale [1989] 1 WLR 1340 (CA) at pp 1376 – 1381. Verjee v CIBC Bank & Trust Company (Channel Islands) Ltd *2001+ Lloyd’s Rep Bank 279.

e) Liability of Paying Bank when in breach of mandate

General principle

*Tai Hing Cotton Mill Ltd v Liu Chong Hing Bank Ltd [1986] AC 80 at 97 (cannot debit account).

Bank’s Defences

Ellinger pp.493 – 500.

Carelessness/estoppel:

*Greenwood v Martins Bank Ltd [1933] AC 51. *London Joint Stock Bank v Macmillan [1918] AC 777. Tai Hing Cotton Mill Ltd v Liu Chong Hing Bank (above). Bintai Kindenko Pte Ltd v Sanwa Bank Ltd [1994] 3 SLR 459 esp. at 464.

See in Malaysia s.73A Malaysian Bills of Exchange Act 1978 (Poh Chu Chai pp. 730 – 735). Leolaris(m) Sdn Bhd v RHB Bank Bhd [2009] 10 CLJ 248 (Poh Cho Chai p 731).

Ratification *London Intercontinental Trust Ltd v Barclays Bank Ltd *1980+ 1 Lloyd’s Rep 241.

Ambiguous Instructions

Verification Clauses

Poh Chu Chai pp. 755– 768.

12

*Consmat Singapore (Pte) Ltd v Bank of America National Trust & Saving Association [1992] 2 SLR 828. *Pertamina Energy Trading Ltd v Credit Suisse [2006] 4 SLR 273.

iv) Position and Liability of Collecting Bank

a) General duties to customer

Ellinger pp 715 – 716. Barclays Bank v Bank of England (above). Redmond v Allied Irish Bank [1987] FLR 307.

b) Liability in Conversion

General

Ellinger pp 680 – 683. [As to an alternate restitutionary claim see mistaken payments: Handout III]

Proper Claimant – True owner (right to immediate possession) *Bute (Marquess of) v Barclays Bank Ltd [1955] 1 QB 502. Dextra Bank & Trust Co v Bank of Jamaica [2002] 1 All ER (Comm) 193 at paras 22 – 23. Poh Chu Chai pp 831 – 834.

c) Forgeries and Material Alterations

Poh Chu Chai pp 814 – 818. Bills of Exchange Act (Cap 23 Rev Ed 2004), ss. 24 and 64. Smith v Lloyd’s TSB Group Plc [2001] QB 541. Cf. Bintai Kindenko Pte Ltd v Sanwa Bank Ltd [1994] 3 SLR 459.

d) Defences open to Converting Bank

Bills of Exchanges Act (Cap 23 Rev Ed 2004) s 86.

Poh Chu Chai pp. 844 – 851; 853 – 862; 882 – 884.

13

*Architects of Wine Ltd v Barclays Bank [2007] 2 All ER (Comm) 285 (General standard of care and payment into wrong account). *Marfani &Co Ltd v Midland Bank Ltd [1968] 1 WLR 956 (Opening of account – references). Rubber Industry (Re planting) Board v Hong Kong and Shanghai Banking Corp [1957] MLJ 103 (opening of account – discussed Poh Chu Chai pp. 855 – 856). Lloyds Bank v Chartered Bank of India, Australia & China [1929] 1 KB 40 (Unusual circumstances). Yap Moi v Hong Kong Bank Bhd [2002] 3 CJJ 562 (Account/payee cheques – Poh Chu Chai p 882).

*Honourable Society of Middle Temple v Lloyd’s Bank Plc [1999] 1 All ER (Comm) 193, noted by Hooley [1999] CLJ 278.

Bank claiming as holder in due course

Poh Chu Chai pp. 824 – 825.

e) Liability of Other banks

Ellinger pp 708 – 711.

Processing Banks

Collecting Banks as agent for foreign banks [See also electronic payment] *Honourable Society of Middle Temple v Lloyd’s Bank Plc [1999] 1 All ER (Comm) 193, noted by Hooley [1999] CLJ 278.

Paying Bank

Bills of Exchange Act (Cap 23 Rev Ed 2004), s 80. C. ELECTRONIC FUNDS TRANSFERS i) General

Credit/Debit transfer

Domestic/International Payment

14

Different Clearing systems

Settlement ii) Position and Liability of Paying Bank

Ellinger pp 610 – 616.

a) Relationship to payor

Mandate

Royal Products Ltd v Midland Bank Ltd *1981+ 2 Lloyd’s Rep 194. Dovey v Bank of New Zealand *2000+ 3 NZLR 641 (Under heading “Steps taken to effect–transfer”). [See also above exceptions to mandate under heading B(iii) (b) above]

Duty of care and skill

Royal Products Ltd (above). Patel v Standard Chartered Bank *2001+ Lloyd’s Rep Bank 229. *Barclays Bank Plc v Quincecare [1992] 4 ALL ER 363. *See also above heading B (iii) (d) ‘Duty of care and its relationship to requirement to obey mandate’+

b) Relationship to payee

Contract Right of Third Parties Act 1999 (Cap 53B Rev Ed 2002). Wells v First National Commercial Bank [1998] PNLR 552 (CA). Grosvenor Casinos Ltd v National Bank of Abu Dhabi [2008] EWHC 511 (Comm).

iii) Position and Liability of Payee’s Bank

a) Authority to accept funds

Dovey (above under heading “first cause of action”).

b) Duty of care and skill to payee (but not payor) Ellinger pp 627 – 628.

15

Abu–Rahma v Abacha [2005] EWHC 2662 (QB). So v HSBC Bank plc [2009] EWCA 296 at para 95 – 102.

iv) Position and Liability of Correspondent Bank

J.Vroegop “Role of Correspondent Banks in Money Transfers” *1990+ LMCLQ 547. Ellinger pp 619 – 621. Royal Products Ltd (above). Calico Printers Association v Barclays Bank Ltd (1936) 36 Com Cas 71.

v) Countermand of Payment

Barclays Bank plc v Bank of England [1985] 1 ALL ER 385 at 394 D. vi) Completion

a) Differentiate Completion/Countermand b) Commercial Significance of completion meaning

The Brimnes [1973] 1 WLR 386 at 400 B – C interpreted in The Chikuma [1981] 1 WLR 314 at 319 H.

c) Time of Completion

Poh Chu Chai pp 360 – 371.

J.Vroegop “The time of Payment in paper–based and Electronic funds transfer systems” *1990+ LMCLQ 64. *Rekstin v Severo Sibirsko [1933] 1 KB 47 (Discussed Poh Chu Chai pp 361 – 362). *Momm v Barclays Bank International Ltd [1977] Q.B 790 (Discussed Poh Chu Chai pp 362 – 363). *Mardorf Peach &Co Ltd v Anica Sea Carriers Corp of Libya, The Laconia [1977] AC 580.

d) Acceptance by payee bank of late payments

16

The Laconia (above). vii) Private electronic banking

Poh Chu Chai pp 377 – 383.

D. CARD PAYMENTS (BASIC STRUCTURE) Ellinger pp 649 – 656; 660 – 664. i) Credit Cards/Charge Cards

a) Process and relevant Contractual relationships Lancore Services Ltd v Barclays Bank plc [2009] EWCA Civ 752 at paras 4 – 10. Re Charge Card Services Ltd [1987] Ch 150. Do–Buy 925 Ltd v National Westminster Bank [2010] EWHC 2862 (QB) except paras 39 – 54. Code of Practice for Banks (a sub–code of the Code of Consumer Banking Practice) by the Association of Banks of Singapore.

b) Absolute or Conditional Payment?

Re Charge Card Services Ltd (above).

ii) Debit cards/Cash Cards

a) Process and Relevant Contractual Relationship

Do–Buy 925 Ltd v National Westminster Bank [2010] EWHC 2862 (QB) except paras 39 – 54.

b) Absolute or Conditional Payment?

Re Charge Card Services Ltd (above).

iii) Digital Cash Cards

R. Hooley, “Payment in a cashless society” in BAK Rider (ed), The Realm of Company Law – A Collection of Papers in Honour of Professor Leonard Sealy (1998) p 245. D Kreitszhein (2003) 14 JBFLP 161 and 261.

17

Questions and Case Studies

1. What is the legal nature of a fund’s transfer?

[Reading: Section A i)] 2. East North Bank (with its headquarters located in Singapore) has a number of foreign

branches. One of them is based in Cyprus. During the financial crisis in Europe, all Cyprus banks are closed. John Phillips, a customer of the Orchard Road branch of the East North Bank in Singapore presents a cheque (payable to cash) withdrawing the balance of his funds (of 10,000 Dollars) from the Cyprus branch.

East North Bank refuses to allow the withdrawal. Is it entitled to do so? [See Handout I: Introductory matters – functions, definitions and the Banker

Customer relationship – Part C] 3.

(a) What reasons may justify a bank refusing to comply with the customer’s instructions? [Reading Section B iii) a)- b)]

(b) East North Bank makes a mistake in not paying a cheque drawn by its customer, Clothing Manufacturing Pte Ltd, in favour of one of its suppliers of cotton fabric. This is because a cashier has misread the instructions, erroneously thinking that the signatures of two directors were required rather than one. The cheque is returned to the drawer with the words ‘Refer to Drawer’. Advise Clothing Manufacturing Ltd.

[Reading Section B iii) c)]

4. Fred Smith an employee of Clothing Manufacturing Pte Ltd (a customer of East North

Bank) has been defrauding the company. Fred is a senior accountant and has authority to draw cheques on behalf of the company. Over a period of 2 years he draws twenty cheques payable to himself and paid them into his own account at West South Bank. No cheque was drawn for an amount greater than S$5,000, and the total amount credited was S$50,000. Fred also drew cheques in favour of David Tan Enterprises Pte Ltd (a supplier of cotton material). Fred opened an account in the name of David Tan Enterprises, at the West South Bank, using a forged registration certificate. No further checks were made by West South Bank, and he was not asked to provide references as to the creditworthiness of the company. Fred is the only signatory on the account. The cheques drawn in favour of David Tan Enterprises Pte Ltd are paid into the account in that name at West South Bank and subsequently withdrawn by Fred. The total amount credited (and withdrawn) from

18

this account is S$6 million. The evidence shows that Fred has been allowed to work without supervision and there has never been a thorough auditing reconciling the company’s books with the bank statements provided by East North Bank. The bank rules (which are part of the contract between East North Bank and Clothing Manufacturing Pte Ltd) state, inter alia: “A statement of the customer’s account will be rendered once a month. Customers must: (1) examine all entries in the statement of account and report at once to the bank any error found therein, (2) return the confirmation slip duly signed. In the absence of any objection to the statement within seven days after its receipt by the customer, the account shall be deemed to have been confirmed.”

(a) East North Bank refuse to reimburse Clothing Manufacturing Pte Ltd with the

amount debited to its account and tells the company it should reach a remedy elsewhere.

(b) The position is as in (a), except Fred does not have authority to draw cheques and

forges the signature of a director of Clothing Manufacturing Pte Ltd (Albert Jones)

(c) Albert Jones draws a cheque for S$4000 in favour of the lawyers (T. Smith,

partners) used by Clothing Manufacturing Pte Ltd. The cheque is handed to a courier (Tom Smith), ordered and paid for by Clothing Manufacturing Pte Ltd. Tom Smith (which has a gambling problem) steals the cheque and pays it into his account at West South Bank. He is also able to add a ‘0’ after 4000 and change ‘four’ to ‘forty’ so that Clothing Manufacturing Pte Ltd’s account is debited with the amount of S$40,000. Tom absconds after withdrawing the money from account. You are asked to advise in respect of Clothing Manufacturing Pte Ltd’s legal position? [Reading Sections B iii) d) – e) and B iv) a) – e)]

5. East North Bank Ltd is in the process of engaging a correspondent bank (Best Bank

Ltd) in the United Kingdom. The correspondent Bank will be involved in the processing of payments both in respect cheques and electronic funds transfer. As East North Bank’s legal adviser you have been invited to a meeting to address the executives of both banks on the following:

a) The potential liability of both East North Bank Ltd and Best Bank Ltd to a

customer of East North Bank who is remitting money (either by cheque or electronic funds transfer) to a beneficiary payee in the United Kingdom.

b) The potential liability of both East North Bank Ltd and Best Bank Ltd to the

beneficiary payee in the United Kingdom.

19

c) The legal relationship, liabilities and obligations between the two banks.

The executives have read the material and cases (on the Handout at C ii) to C iii) (inclusive) but still are confused.

6. Brian Tan is a customer of East North Bank at the Orchard Street branch. He is the

owner of a fleet of luxury yachts and charters (i.e. leases) them out to his billionaire clients. The period of the charter party is usually three years, payment to be made at six monthly intervals. John charters a yacht, with the second rental payment to be made on 31st July. A clause in the contract states that “payment of hire to be made in pounds sterling – without discount, half–monthly in advance. In default of payment the owners have the right of withdrawing the vessel from the service of the charterers” on or before July 31st. Brian is keen to terminate the charter party since he has an opportunity to charter the yacht to another client at a substantially increased rental.

You are asked to advise Brian Tan in the following alternative circumstances?

(a) An electronic funds transfer sent by John’s bank for the full amount of the six

months payment is received by International Division of East North Bank on July 31st. Nothing further is done that day.

(b) An electronic transfer of funds is received by the International Division of East

North Bank on July 31st, and the bank’s computers are programmed by staff to credit the funds to Brian’s account but they do not appear on his on–line account statement until August 2nd.

(c) The funds are credited to Brian’s account at 3pm on July 31st, but East North Bank

are suspicious of the origin of the funds and put a temporary stop on the operation of the account.

(d) Brian gave instructions to East North Bank to return any payment received from

John Phillip (or his bank) after July 31st. East North Bank receive an electronic funds transfer from John on August 1st and credit Brian’s account. On six or seven previous occasions, Brian has given similar instructions to East North Bank. On these occasions the Bank has nevertheless accepted the payment, and Brian has not objected.

In a) could John countermand payment at that stage?

[Reading Sections C v) and vi)]

7. East North Bank, Orchard Street Branch, has received a substantial payment into the account of a new customer. The Manager is concerned that the money is the product of criminal activities and wants to return the money. He seeks your advice. What should he do?

20

Reading Section B iii) b) under the headings ‘facilitating criminal activity’ and ‘dilemmas for the banks’

8. (a) What contractual relationship governs the use of a credit/debit card?

(b) Read Do–Buy Ltd v National Westminster Bank [2010] EWHC 2862 (QB) (except

paras 39 – 54). Do you agree with the court’s analysis of the contractual terms discussed in that case?

[Reading Sections D i) ii)]

21

III. Recovery of mistaken payments

A. COMMERCIAL REASONS FOR WRONGFUL PAYMENTS, INCLUDE

Fraud (*Agip Africa Ltd v Jackson [1991] Ch 657).

Error by using wrong beneficiary or account details (*Jones v Churcher [2009] EWHC 772 (QB), *2009+ 2 Lloyd’s Rep 94).

Bank acting contrary to customer’s mandate: (Barclays Bank Ltd v W.J. Simms [1980] QB 677).

Mistake by Bank believing customer is in funds (Lloyd’s Bank plc v Independent Insurance Co Ltd *1999+ 1 Lloyd’s Rep 1).

B. LEGAL MECHANISMS FOR RECOVERY i) Restitutionary Claim

a) General nature of Action

Jones v Churcher (above) at paras 41–42, citing Barclays Bank Ltd v WJ Simms (above) at p.695 C – W.

“(1) If a person pays money to another under a mistake of fact of which causes him to make the payment, he is prima facie entitled to recover it as money paid under a mistake of fact,(2) his claim may however fail if (a) the payer intend that the payee shall have the money at all events, whether the fact be true or false, or is deemed in law so to intend; or (b) the payment is made for good consideration, in particular if the money is paid to discharge, and does discharge , a debt owed to the payee –––––– by the payer or by a third party by whom he is authorised to discharge the debt; or (c) the payee has changed his position in good faith, or is deemed in law to have done so.”

Dextra Bank Trust co v Bank of Jamaica [2002] 1 All ER (Comm) 193 (PC). See also the common law rules as to tracing Agip (Africa) Ltd v Jackson [1991] Ch 547, esp. at 563 – 566. Operational Guidelines regarding refund of payments In the Bye–Laws and Regulations of the Association of Banks in Singapore.

b) Who can make the claim?

Agip (Africa) Ltd v Jackson [1991] Ch 550 at pp 561 – 562. Barclays Bank Ltd v WJ Simms [1980] QB 679 at pp 699 – 700 only.

22

Note, however *B Ligget (Liverpool) Ltd v Barclay’s Bank Ltd [1928] 1 KB 48.

c) Defences

Change of position:

Ellinger pp 527 – 534 *Jones v Churcher (above) at paras 43 – 46, 56 – 65, 79 – 97. Niru Battery Manufacturing v Milestone TradingLtd [2002] 2 All ER (Comm) 705) *Scottish Equitable Plc v Derby [2001] 3 All ER 818.

Good consideration:

Ellinger pp534 – 538. Jones v Churcher (above) paras 48 – 55. Lloyd’s Bank plc v Independent Insurance Co Ltd *1999+ 1 Lloyd’s Rep 1

Ministerial Receipt:

Ellinger pp 539 – 545. Jones v Churcher (above) at paras 66 – 78. Continental Caoutchouc & Gutta Percha Co v Kleinwort & Sons (1904) LT 474.

Estoppel

Ellinger pp 538 – 539. Scottish Equitable Plc v Derby (above).

Liggett Defence

B. Ligget (Liverpool) Ltd v Barclay’s Bank Ltd [1928] 1 KB 48. Cleadon Trust Co [1939] Ch 286.

ii) Tracing/Following in Equity

23

Ellinger pp 306 – 312. *Agip (Africa) Ltd v Jackson [1991] Ch 547. Foskett v McKeown [1998] Ch 265, at pp 277 G – 278 H only. On mistaken payments (other than fraud) see: Chase Manhattan Bank N.A v Israel British Bank (London) Ltd [1981] Ch 105 (Ellinger p.311). but cf. Westdeutsche Landesbank Girozentrale v Islington Borough Council [1996] AC 669 at pp 714C – 715C only. P.J. Millet “Restitution and Constructive Trusts” (1998) 114 LQR 399 at 412 – 413.

iii) Constructive Trust Actions Barnes v Addy (1874) 9Ch App 244 at 251 per Lord Selbourne:

“–––– strangers are not to be made constructive trustees merely because they act as the agents of trustees in transactions within their legal powers, transactions perhaps of which a Court of Equity may disapprove, unless (i) those agents receive and become chargeable with some part of the trust property, or ii) unless they assist with knowledge in a dishonest and fraudulent design on the part of the trustees.”

a) ‘Knowing Receipt’

Ellinger pp 291 – 298.

Elements of action:

a) Disposal of assets in breach of fiduciary duty; b) The beneficial receipt of assets which are traceable as representing the assets of

the claimant; and c) Knowledge on the part of the defendant that the asset(s) he received are

traceable to a breach of fiduciary duty.

(Hoffman LJ in El Ajou v Dollar Land Holdings [1994] 2 All ER 685 at 700)

See also Agip (Africa) Ltd v Jackson [1990] 1 Ch 265 at 291.

As to knowledge see BCCI v Akindele [2001] Ch 437 (discussed in Ellinger pp 296 – 298) and Lord Nicholls in W. Cornish et al ‘Restitution – Past, Present & Future’ (1998) p 231.

24

b) ‘Dishonest Assistance’

Ellinger pp 270 – 291 (For general background) and the elements of the cause of action: a) Trust or fiduciary relationship; b) Breach of Trust or other misfeasance; c) Defendant must as a matter of fact have been accessory to or assisted in, the

misfeasance or breach of Trust; and d) The defendant must have been dishonest. See also Agip (Africa) Ltd v Jackson [1991] Ch 547. On dishonesty, see Abou–Rahmah v Abacha [2006] EWCA CIV 1492 at para 64 – 69 (and specially the interpretation of Twinsectra Ltd v Yardley [2002] 2 AC 164 and Barlow Clowes International Ltd v Eurotrust International Ltd [2005] UKPC 37, [2006] 1 ALL ER (Comm) 478). For the potential liability of the Banks, see Abou–Ramah v Abacha (above). For the potential remedies see S. Elliot v C. Mitchell “Remedies for Dishonest Assistance” Vol 67 (2004) Vol 67(1) MLR 16 esp. at 36 – 47.

iii) Conversion (in the case of cheques)

See Handout II– payment by cheques

Questions and Case Studies 1) Read Jones v Churcher *2009+ EWHC 722 (QB), *2009+ 2 Lloyd’s Rep 94.

(A story of greed, mistakes and inefficiency!), mastering the essential facts. Then consider the following: a) What was the principal cause of the action by Mr Jones against Miss Churcher and

Abbey National? What are the elements of that cause of action? b) What defences were raised by Miss Churcher and Abbey National? c) Why were there unsuccessful? d) Does this case suggest that there should be any changes to banking practices?

2) What would have been the position in Jones v Churcher if Miss Churcher had received the initial mistaken payment of £14,300 into her account, which (let us assume) has an existing credit of £5,000 and Miss Churcher then transferred £19,300 to her mother’s account at another bank?

25

Is the £14,300 recoverable by Jones from the mother in an action for restitution?

3) Read Agip (Africa) Ltd v Jackson [1991] Ch 547 and Abou–Rahmah v Abacha [2006] EWCA Civ 1492 (cases of startling fraud) isolating the relevant facts. (Note that in Agip (Africa) Ltd v Jackson, although £518,000 had been paid into Jackson & Co’s account at Lloyds Bank in the Isle of Man to the various fraudsters, approximately £45,000 sill remained in the account). a) What were the causes of action pleaded by Agip (Africa) Ltd against Jackson & Co? b) Which of those actions were successful and why?

c) If Jackson & Co had purchased a vintage car with the £45,000, which had then risen

to value to £90,000, what would have been Agip (Africa) Ltd’s legal position? d) As in c) but Jackson & Co had then sold the car to the Governor of the Isle of Man for

£90,000 e) On the facts of Agip (Africa) Ltd v Jackson would any liability have been incurred by

Lloyd’s Bank at Holborn if the employees of Lloyd’s (Mr Bendon & Miss Freeman) had been suspicious that the Baker Oil account had been established for money laundering, purposes? And on what basis? If not, what evidence would be required to establish the Bank’s liability?

4) East North Bank Ltd in Singapore received instructions to transfer electronically, the sum

of £10,000 to a beneficiary at West South Finance Ltd in the UK. An official of East North Bank Ltd makes a mistake and inserts the wrong account number, which is in fact the account of another customer of West South Finance (Fred Smith). West South Finance Ltd then becomes insolvent.

Can East North Bank Ltd recover the £100000?

5) Does the law as it relates to mistaken payments as applied in the context of the banking

system strike a reasonable balance between the interests of the banks, their customers and third parties?

26

IV. The Bank’s Duty of Confidentiality

Reading: Poh Chu Chai pp. 543 – 573

A. AT COMMON LAW

i) General Duty

*Tournier v National Provincial Union Bank of England [1924] 1 KB 461. A more general approach: R. Spearman “Disclosure of Confidential Information: Tournier and “disclosure in the interests of the bank” re–appraised (2012) 2 JIBFL 78.

ii) Exceptions

a) Compulsion of Law

Bankers Trust Co v Shapira [1980] 1 WLR 1274. C v S [1999] 1 WLR 1551.

b) Duty to the Public

Price Waterhouse v BCCI Holdings (Luxembourg) SA [1992] BCLC 583.

c) Bank’s own Interest

Sunderland v Barclays Bank Ltd (1938) LDAB 163.

d) Customer’s Authority

*Turner v Royal Bank of Scotland [2001] 1 All ER Comm 1057.

iii) Remedy

*Jackson v Royal Bank of Scotland [2005] UKHL 3; [2005] 1 WLR 377. Tan Eng Seong v Malayan Banking Bhd [1997] 2 CLJ Supp 552 (Poh Chu Chai p 553).

B. STATUTORY SCHEME

i) General scheme

ss 40A, 47 Banking Act (Cap 19 Rev Ed 2008).

27

Susilalawati v American Express Bank Ltd [2009] 2 SLR 737. PSA Corp Ltd v Korea Exchange Bank [2002] 3 SLR 37.

ii) Exceptions

See Part I and Part II Banking Act (Rev Ed 2008) esp. Clause I (Part I) and clauses 7, 8, 9 (Part II).

iii) Remedy?

Tan Eng Seong v Malayan Banking Bhd [1997] 2 CLJ Supp 552.

Questions and Case Studies 1 Why does the Law impose a duty of confidentiality?

2 East North Bank has disclosed, or intends to disclose, information in the following

circumstances a) Mr and Mrs Tan are both customers of the bank. Mrs Tan is starting a new

clothing business. As the business is partly founded by her husband, she tells her business manager that she does not object to her husband having access to the statement of her new business account (which she has opened in her own name). Subsequently the business manager notices that substantial amounts have been debited from Mrs Tan’s account and sends a statement of her account to her husband. It transpires that the debits represent amounts spent by Mrs Tan on expensive items of jewellery. Mr Tan is not pleased and begins divorce proceedings. Mrs Tan is forced to close her business.

b) Mr So is a (highly valued) customer of East North Bank and approaches the

Manager of his local branch with a view to investing substantial sums of money in various deposit accounts. It transpires that the investment most suited to Mr So are those offered by a subsidiary of East North Bank (Asset Trust Management). The manager of the local branch sends Mr So’s account details to Asset Trust Management with a note recommending him as a suitable investor.

c) Mr Smith, a customer of East North Bank, has supplied his name to another

financial institution in connection with an application to a credit card facility. East North bank (without seeking Mr Smith’s consent) respond to an enquiry about the financial status of Mr Smith in negative terms, because he has previously defaulted on payment of a loan. Previously East North Bank has informed a credit rating bureau of Mr Smith’s default.

28

d) The Singapore Government sets up an Inquiry to investigate the effectiveness of education in Singapore. The Chairman of the Inquiry considers it necessary to examine the bank account details of various educational institutions, although it has no power to do so by its terms of reference. East North Bank indicates it will supply the information.

Please advise In these four cases: i. If East North Bank is justified in disclosing the relevant information:

a) At Common Law, or b) Pursuant to s.47 Banking Act (Cap 19 Rev Ed 2008)?

ii. If, in any of these circumstances, East North Bank is in breach of its duty of confidentiality, what remedy is available (for example, Mrs Tan in 2(a))?

iii. Generally, what are the advantages and disadvantages to a bank of the regime established pursuant to s.47 Banking Act (Cap19 Rev Ed 2008)?

29

V. The Bank in an Advisory Role Reading: Poh Chu Chai 53 – 57, 616 – 624; Ellinger 154 – 169, 134 – 139, 727 – 736; G. McMeel [2001] LMCLQ 185.

A. BASIS OF DUTY

Tort/Contract Relationship between these liabilities: Go Dante Yap v Bank Austria Creditanstalt AG [2011] 4 SLR 559. Tai Hing Cotton Mill Ltd v Liu Chong Hing Bank Ltd [1986] AC 80. [ Previously considered in relation to payment mechanisms]

B. NO GENERAL DUTY TO ADVISE

i) Tax matters Shioler v Westminster Bank [1970] 2 QB 719.

ii) Lending

Williams & Glyn’s Bank Ltd v Barnes [1981] Com LR 205.

iii) Taking Securities O’Hara v Allied Irish Banks Ltd [1985] BCLC 52. But see Royal Bank of Scotland plc v Etridge (No 2) [2001] UKHL 44 and Lloyd’s Bank Ltd v Bundy [1975] QB 326 (Discussed below – Case studies on Guarantees).

iv) Investments

Titan Steel Wheels Ltd v Royal Bank of Scotland [2010] EWHC 211 esp. paras 77 – 108.

C. ASSUMING RESPONSIBILITY AS ADVISOR

i) ‘Crossing the line’ Titan Wheels Ltd (above) *Deutsche Bank AG v Chang Tse Wen [2013} SGCA 49 Cf *Go Dante Yap v Bank Austria Creditanstalt (above) *Verity & Spendler v Lloyd’s Bank plc [1995] CLC 1157 *Woods v Martins Bank Ltd [1959] 1 QB 55 (discussed Poh Chu Chai (pp. 629–630))

30

ii) Passing on Information:

Royal Bank Trust Co Trinidad Ltd v Pampellone (1986) 35 WIR 392 at p395 (where the advice set out) and p.405 (discussed Lomnicka p 738). Cf. Malaysian International Merchant Bankers Bhd v Lembaga Bersekutu Amanah Pengajian Tinggi Islam Malaysia [2001] 1MLJ 375 (discussed Poh Chu Chai pp 630–631).

D. EFFECT OF CLAUSE PURPORTING TO NEGATE ASSUMPTION OF LIABILITY OR EXCLUDE

LIABILITY, (INCLUDING THE IMPACT OF UNFAIR CONTRACT TERMS ACT (CAP 396 REV ED 1994)).

Generally McMeel (above), especially pp 202 – 205.

Springwell Navigation Corp v J P Morgan Chase Bank [2010] EWCA 1212, per Aikens LJ at paras 143 – 144. Titan Steel Wheels Ltd (above), paras 77 – 92. Deutsche Bank AG v Chang Tse Wen [2013] SGCA 49 at paras 58-68. Orient Centre Investments v Societe General [2007] 3 SLR 566 at paras 42 to 45 (discussed Poh Chu Chai p 624). Raiffersen Zentral Bank Osterreich AG v The Royal Bank of Scotland [2010] EWHC 1392 (Comm) (paras 313–315 only).

E. IMPACT OF FINANCIAL ADVISERS ACT (CAP 97 REV. ED. 2007) See ss 25 – 27, set out below. (Discussed Poh Chu Chai pp 619 – 20).

F. LIABILITY TO THIRD PARTIES

So v HSBC Bank plc [2009] EWCA Civ 296 Noted [2010] LQR 39.

References: James Mc Moughten Group Ltd v Hicks Anderson & Co [1991] 2 QB 113 (See Ellinger p 730).

Case Studies

1. Arthur Smith, who has been working as a maintenance builder for the last five years (Undertaking minor repairs to houses) and (with an income of S$60.000 per year) decides he wants to develop his business by buying houses, renovating them and selling them for a profit. He identifies his first suitable property to buy at a price of S$600,000 and approaches his business manager (Tim Smith) at East North Bank for a loan to purchase it. Arthur has seen a pamphlet issued by East North Bank which promotes the activities of its business managers and states “Business Managers – We can advise and guide you at every stage and help you to succeed” . When they met, Tim tells Arthur that they will work together to make a success of the venture.

31

At the time of the meeting, Arthur signs a contract which contains the following clauses:

2.13 – Except where agreed to by the Bank, the Bank is under no obligation to give

any general investment or advice in relation to a specific or proposed transaction

2.14 – Except to the extent that the same resulted from gross negligence, wilful

default, or fraud, the bank is not liable for any loss resulting from any act or omission, representations or conduct of its employees.

Arthur does not have a detailed business plan for his new venture, but is concerned that the economic outlook is buoyant. Tim provides him with an analysis by the Institute of Bank Economists which is often used by East North Bank to provide economic and other forecasts to its client. Their analysis states that in the next five years the economy will be buoyant, with increasingly strong growth. Tim, however, does not know of another separate report of the Institute which predicts a fall in house prices. East North Bank provides a loan for Arthur to buy the property but neither Tim nor any other bank official inspect the property internally, simply giving it a cursory external visual inspection. In the event Arthur’s property venture is a disaster because the house has a structural fault, (making the costs of renovations more extensive than expected) and because house prices fall significantly soon after its purchase. Arthur is forced to sell the property for S$400,000 and the costs of his repairs are S$40,000. You are asked to advise

a) Whether Arthur will succeed in his action against North East Bank?

b) Whether, for the future, the Bank could improve its legal position by including additional, or alternative, clauses in the contract? Are there defects of substance and drafting in the present clauses?

2. Read So v HSBC Bank plc [2009] EWCA Civ 296. How can the bank protect itself adequately against potential liability to third parties?

32

VI. The Bank and the Provision of Finance

A. DIFFERENT TYPES OF FACILITY

i) Overdrafts/Revolving facilities

Poh Chu Chai pp 150 – 151, Ellinger pp 756 – 765, 794 – 797.

a) Commercial reasons for having an overdraft facility.

b) Legal nature of an overdraft

*Office of Fair Trading v Abbey National plc [2008] EWHC 875 (Comm) at paras 64 – 80 (only).

c) Termination (generally “on demand” facilities)

*Sheppard & Cooper Ltd v TSB Bank plc [1996] BCC 965 at 969. Overseas Chinese Banking Corporation v Infocommcentre Pty Ltd [2005] 4 SLR 30. *Lloyds Bank plc v Lambert [1999] 1 All ER (Comm) 161. *Chapman v Barclays Bank Ptc [1997] 6 Bank LR 315. Titford Properties Co Ltd v Cannon Street Acceptances (unreported QBD 22nd May 1975). Bank of Ireland v AMCD Property (Holdings) Ltd [2001] 2 All ER (Comm) 89.

d) Remedy Crimpfil Ltd v Barclays Bank plc [1993] CLC 385.

e) Interest National Bank of Greexe SA v Pincos Shipping Co [1990] 1 AC 637.

ii) Term Loans

a) General

Poh Chu Chai pp 132 – 137

33

Authority to contract First Energy UK Ltd v Hungarian International Bank Ltd [1993] 2 Lloyds Rep 194.

Statements by bank

Box v Midland Bank [1979] 2 Lloyds Rep 391.

Consequences of execution – potential breach of contract by bank

Kluang Wood Products Sdn Bhd v Hong Leong Finance Bhd [1999] 1 MLJ 193 (see Poh Chu Chai pp 136 – 137). P Rawlings “Avoiding the obligation to lend” *2012+ JBL 89, esp. 100 – 110. Essentially Different Ltd v Bank of Scotland Plc [2011] EWHC 475 (Comm).

b) Scheme and Central Provisions (including efficiency and drafting of relevant clauses)

Facilitation and drawdown clauses

Purpose clause Usually for general purposes but cf. *Barclays Bank v Quistclose [1970] AC 567, esp at 578 – 580. Twinsectra Ltd v Yardley [2002] 2 AC 164 at paras 68 – 74 (Lord Millet dissenting but not on this issue).

Repayment clauses

Interest clauses

Limits on lenders discretion as to interest rates. *Paragon Finance Plc v Staunton [2001] 1 WLR 685, esp at para 37 – 48 (as applied to commercial agreements in Socimer International Bank London Ltd [2008] EWCA Civ 116). Sterling Credit Ltd v Rahman [2002] EWHC 3008 (Ch) at paras 3 – 5. Mayban Finance Bhd v Wong Gieng Suk [2003] 1 CLJ 27 (Poh Chu Chai pp 161 – 162).

34

Conditions precedent

Representations and warranties

Covenants

- Pari passu clauses

P R Word “Pari Passu clauses – what do they mean?” *2003+ JIBFL 371.

- Negative pledge clauses R Cranston, Principles of Banking Law (2nd Edn 2002 – reprinted 2009), pp 315 – 321.

Default clauses See generally R Youard “Default in International Loan Agreement I and II” [1986] JBL 276 at 378.

- Events of default (including cross–default clauses and MAC clauses,

cancellation of commitments) As to MAC clauses see R Hooley, “Material Adverse Change clauses after 9/11) in S Worthington (ed) Commercial Law and Commercial Practice (Hart 2003). Zakrewski, “Material adverse change and material adverse effect provisions: construction and application [2011] LFMR 344. *Cukurova Finance International Ltd v Alfa Telecome Turkey Ltd [2013] UKPC 2 at paras 43 – 51. Groupa Hotelera v Carey Value Added [2013](Comm) paras 321 – 365.

c) Restrictions on exercise of rights?

Penalty

Wallingford v Mutual Society (1880) 5 App Cas 685 at 696, per Lord Selbourne.

Relief against forfeiture Cukurova Finance International Ltd (above) at paras 77 – 78.

Statutory control in some jurisdictions

35

Rahman v HSBC Bank plc [2012] EWHC 11 (Ch).

Estoppel Bank of Ireland v AMCD (Property Holdings) Ltd [2001] 3 All ER (Comm) 894.

Incorrect declaration of event of default *Concord Trust v Law Debenture Trust Corp plc [2005] UKHL 27, esp at 30 – 38. (Noted E Peel “No liability for service of an invalid notice of default” (2006) 122 LQR 179).

iii) Syndicated loans

Ellinger pp 781 – 787. M Hughes “Loan Agreements – Single Bank and Syndicated” *2000+ JIBFL 115. a) Structure

Term sheet

When legally binding Maple Leaf Micro Volatility Master Fund v Rouvroy [2009] EWHC 257 (Comm), [2009] 1 Lloyds Rep 475.

Nature of obligations

Decision making

Redwood Master Fund Ltd v TD Bank Europe Ltd [2002] EWHC 2703 (Ch) (See P Wood [2003] CLJ 261).

b) Role of Arranging Bank

Ellinger pp 784 – 787. UBAF Ltd v European American Banking Corp [1984] QB 713.

c) Role of Agent Banks

iv) Loan Participation Schemes (in outline)

36

Ellinger pp 787 – 789.

B. MECHANISMS FOR PROTECTING THE LENDER’S POSITION

(With emphasis on commercial advantages and disadvantages)

i) Commercial purpose, range and nature of securities. Ellinger pp 808 – 811.

ii) Guarantees and mortgages

See Section C – case studies in the execution, maintenance and enforcement of the securities (including the bank’s duty as fiduciary)

iii) Chattel mortgages/hypothecation

Ellinger pp 838 – 841.

iv) Floating charges

Companies Act (Cap 50 Statutes of the Republic of Singapore, Rev Ed 2006) s.13

Ellinger pp 842 – 855. a) Distinction between fixed and floating

Re Yorkshire Wollcombers Association [1903] 2 Ch 284 at pp 293 –296 (only). Re Spectrum Plus [2003] 2 AC 680 at paras 53 – 61, per Lord Hope.

b) Floating charges – crystallisation – “automatic crystallisation” clause – priorities

*Re Brightlife [1986] 1 Ch 200 at pp 214H – 215. Re Manurewa Transport [1971] NZLR 909.

v) Pledges/Trust Receipts

Ellinger pp 856 – 863, esp. 859 – 861. Sale Continuation Ltd v Austin Taylor & Co Ltd [1968] 2 QB 849. The Delfini [1990] 1 Lloyds Rep 252 at p 268. Northwestern Bank Ltd v Poyntee [1895] AC 56 (trust receipts).

37

[See also letters of credit, below]

vi) Banker’s Lien

Ellinger pp 864 – 867. Re Bowes (1866) 33 Ch D 586.

vii) Receivables Financing

Ellinger pp 871 – 879.

a) Various techniques

Factoring/Block discounting Notification factoring (“invoice discounting”).

Charge over book receivables Re Spectrum Plus (above).

Commercial and legal advantages of these techniques

An introduction to some issues of priorities Ellinger pp 879 – 882.

viii) Rights in relation to Bank deposits

a) Combination of accounts

Poh Chu Chai pp 669 – 695.

Re Spectrum Plus (above) at para 60, per Lord Hope.

Requirement of mutuality.

*Good Property Land Development Pte Ltd v Societie General [1996] 2 SLR 239.

Customers’ contingent future or unmatured liabilities not within rule Jeffryes v Agra & Mastermans’ Bank (1866) LR 2 Eq 674 at 680 – 681. *Bradford Old Bank Ltd v Sutcliffe [1918] 2 KB 833.

Requirement of notice?

38

*National Westminster Bank v Halesown Presswork and Assemblies Ltd

[1972] AC 785 at 810, per Lord Cross. *Good Property Land Development v Societie General above.

Accounts in foreign branches Re Firm of TSN [1935] MLJ 139 (Poh Chu Chai p 668 –689).

Insolvency Bankruptcy Act (Rev Ed. 2009), s 88(1) (Poh Chu Chai p.690). National Westminster Bank Ltd v Halesowen Pressweek and Assemblies

Ltd (above) b) Contractual Right of Set–Off Ellinger pp 884 – 889. c) Securities over bank balances (charge backs) Ellinger pp 889 – 891. W Blair “Charges over cash deposits” IFL Rev Nov 1983 14 Re Charge Card Services Ltd [1987] Ch 150 Cf. Re Bank of Credit and Commercial International SA (No 8) [1998] AC 214,

per Lord Hoffman.

See Singapore Civil Law Act (Cap 43 Rev Ed. 1999), s 13 (Poh Chu Chai pp 659 – 660).

ix) Security over shares

Ellinger pp 894 – 900

x) Security over intellectual property A Tosato “Security Interests over intellectual property” JIPLP *2011+ Vol 6(2) 93.

xi) Asset securitisation

Lomnicka pp 882 – 883.

39

C. GUARANTEES: CASE STUDIES IN THE EXECUTION, MAINTENANCE AND ENFORCEMENT

Case study 1: nature and execution (including the negotiating process and the bank’s duty as fiduciary).

Case study 2: extent of liability and maintenance. Case study 3: enforcement. See the case studies and associated reading below (under case studies and questions – section C).

D. THE BANK AND TRADE FINANCE – SOME LEGAL MECHANISMS.

i) Acceptance credits

Ellinger pp 918 – 919.

ii) Letters of credit R Cranston, Principles of Banking Law (2nd Ed 2002, reprinted 2009) pp 384 – 390.

iii) Performance Bonds Phillips, Ch 15. *Master Marine Labroy Offshore Ltd [2012] SGCA 27 * Samwoh Asphalt Premix Pte Ltd v Sum Cheong Piling Pte Ltd [2002] 1 SLR 1. *BS Mount Sophia Pte Ltd v Join-Aim Pte Ltd [2012] SGCA 28

Questions and Case Studies

A. DIFFERENT TYPES OF FACILITY

1. Arthur Tan, a property developer is sole director of Arthur Tan Enterprises Pte Ltd. He has an arranged overdraft with East North Bank with a limit of S$100,000. The terms of the letter of facility states:

Limit The facility permits drawing on the account to a maximum of S$100,000. Purpose The purpose of the facility is the development of 2 residential homes at the development site for sale on the open market. Repayment

40

Payment is “on demand”. The facility will be repaid from the sale of the development.

No time limit is expressed for the duration of the facility. When the company’s account is overdrawn by S$90,000, Arthur draws a cheque in favour of a supplier of modular kitchens for S$30,000. East North Bank pays the cheque without consulting Arthur and debits the Company’s account a fee of S$6,000 for exceeding the overdraft limit. There are no express terms of Arthur’s contract with East North Bank governing requests for an overdraft. At the time East North Bank decides to pay the cheque the relevant branch manager has received a report from East North Bank’s business division showing that a number of its business customers (including Arthur Tan) have severe cash flow problems. One month later, East North Bank demand that the whole balance of the overdraft is to be repaid immediately. Within three hours East North Bank had appointed administrative receivers to the company’s assets. The demand is made despite Arthur telling the bank at a meeting the day before the demand is served that he has funds in overseas accounts that are sufficient to pay off the company’s overdraft. Arthur now complains that the actions of East North bank have ruined his business. Arthur seeks your advice. Reading Section A i)–different types of facility

2. What is: a. A negative pledge clause? b. A material change of circumstances clause? c. A cross default provision?

Consider difficulties in drafting and whether, if properly drafted, they are efficacious from the point of view of the lender? [Reading Section A ii) b)]

3. What is the legal nature of a syndicated loan and loan participation agreements? How

do they differ? [Reading Sections A iii) – iv)]

B. MECHANISMS FOR PROTECTING THE LENDER’S POSITION

1. Equipe Ltd is a private company which hires out second–hand plant (cranes, forklift trucks and the like) to the construction industry and also provides a general repair and maintenance division (for both its own equipment and generally). The company has a well–established reputation in the market place and a good cash flow. Invoices are payable sixty days after receipt. Equipe Ltd is a customer of FastBank ltd, which is

41

giving serious consideration to providing a fixed–term loan of S$5 million which the company requires for the purpose of expansion (which will involve buying additional stock from their overseas suppliers) and the building of a new depot. Previously FastBank Ltd has assisted Equipe Ltd in the purchase of overseas stock through the provision of letters of credit to its overseas suppliers. Additionally it wishes to develop a new technique (now patented) which was devised by one of the company’s maintenance engineers for servicing (much more cheaply than existing methods) the hydraulic system of cranes.

Equipe Ltd has two deposit accounts held with FastBank Ltd, one payable on demand for the amount of S$50,000 and the other (in the same amount) to mature in 2015. It also has a current account with an overdraft facility up to a limit of S$100,000. Currently the overdraft is S$50,000. Equipe Ltd also has an account at an overseas branch of FastBank Ltd located in Frankfurt, Germany (where one of its suppliers is located) with a credit of €50,000. Equipe Ltd also has a shareholding in a number of construction companies with which it deals. The Directors of Equipe Ltd own substantial properties (owned jointly with their wives). As FastBank Ltd’s lawyer, you have been asked to advise them on what legal mechanisms are available to the bank to protect its position in the case of Equipe Ltd’s insolvency. What advice do you give? [See Reading in sections B i) – x)]

C. GUARANTEES: CASE STUDIES IN THE MAINTENANCE EXECUTION AND ENFORCEMENT OF GUARANTEES

Case Study 1: Nature and execution

(including the negotiating process and the bank’s duty as fiduciary)

1. What is the legal arrangement in the following cases:

a) A document headed “Guarantee” in these terms, which has been executed in respect of a loan made by a bank to a customer:

i) I will upon demand pay to the bank sums of money as at any time or from time to time have become payable by the customer but is unpaid by him/her.

ii) I will indemnify and keep indemnified the bank, its successors and assigns from all loss and damage suffered and all claims costs and expenses made against or incurred by the bank having entered into such agreement,

42

whether arising out of a breach by the customer of any of the terms and conditions thereof or otherwise including such loss or damage, etc, as aforesaid as may arise from the said agreement being (for whatever reason) unenforceable against the customer.

iii) The bank shall be entitled to treat you at all material times as if you were a principal debtor.

iv) Your liability shall not be affected by a release given by the bank to the customer or by the bank giving time or other indulgence to the customer.

*Phillips, paras 1–91 to 1–110. *Stadium Finance Co v Helm (1965) 109 SJ 471.

b) A document executed by a parent company in respect of an advance which a bank is considering making to one of the parent company’s subsidiaries: “We take this opportunity to confirm that it is our practice to ensure that our subsidiary (named) will not default on its obligations and will be in a position to meet its financial obligations as they fall due. These financial obligations include repayment of any loss made by your bank under the arrangements mentioned in your letter.” *Phillips, paras 1–78 to 1.83; paras 2–11 to 2–15. *Banque Brussels Lambert SA v Australian National Industries Ltd [1989] 21 NSWLR 502. *Associated British Ports v Ferryways NV [2009] EWCA Civ 189.

2. Fast Bank Ltd agree to advance S$500,000 (dollars) to English Training Enterprises

Ltd for the expansion of its business operations (which is teaching English to overseas students), on condition that guarantees are given by the following persons:

i) Jim Smith, the Managing Director and principal shareholder of English Training Enterprises Ltd, together with a guarantee from his wife Evelyn;

ii) Arthur Jones, a wealthy uncle of Jim Smith. Jim Smith executes a joint and several guarantee which is described as given “in consideration of the bank [that is FastBank Ltd] having agreed to advance S$500,000 to English Training Enterprises Ltd”. Jim Smith signs the guarantee adding these words “on behalf and in my capacity as Trustee of the Jim Smith Family Trust”. Instead of advancing S$500,000, FastBank Ltd eventually advances S$600,000 after representations from Jim Smith. It transpires that the Jim Smith Family Trust has few assets. Evelyn signs a separate guarantee, but her liability is expressed as “joint and several” with that of her husband. Her guarantee is eventually set aside on the basis of common mistake (with the court relying on the principle in Associated Japanese Bank (International) Ltd v Credit de Nord SA [1989] 1 WLR 255).

43

The guarantees given by Jim Smith and Evelyn contain the following clause: “This guarantee shall bind the signatory hereof notwithstanding that another co–guarantor shall never execute any instrument of guarantee” FastBank Ltd regard the guarantee given by Arthur Jones as crucial to the loan, since he is a person of considerable assets. Arthur Jones sends an e–mail to FastBank Ltd saying that he “would take responsibility for any loan made to his nephew”. Due to an error in the bank’s securities department the advance is made without a formal guarantee being signed. You are asked to advise FastBank Ltd whether any of these guarantees/undertakings enforceable and to what extent? Phillips paras 2–76 to 2–85; paras 3–79 to 3–97; paras 3–159 to 3–167; paras 5–102 to 5–106; paras 8–01 to 8–19. John Phillips “Protecting the bankers”*2013+ Vol 3 JBL 248. *Classic Maritime Inc v Lion Diversified Holdings [2009] EWHC 1142 (Comm). Rainforest Trading Ltd v State Bank of India Singapore [2012] SGCA 21 Overseas Union Bank v Lew Keh Lam [1999] 3 SLR 393. Capital Bank CashFlow Finance Ltd v Ian Southall [2004] EWCA Civ 817. Helvetic Investment Corp v Knight (1984) 9 ACLR 773. Perrylease Ltd v Imecar [1987] 2 All ER 373. Holmes v Mitchell (1858) 7 CBNS 361, 141 ER 856. Civil Law Act (Rev Ed 1999), s 6. *J Pereira Fernandes SA v Mehta [2006] 1 WLR 1543 (see also S M Integrated Transware Pte Ltd v Schenker Singapore Pte Ltd [2005] 2 SLR 651 in respect of a lease). *Actionstrength Ltd v International Glass Engineering IN Gl. EN. SpA. [2003] AC 541.

3. Craftwood Furniture Ltd is a joinery business making hand–crafted furniture of a high quality. FastBank Ltd agree to provide a loan of S$750,000 to the company so that the company can expand its operations and manufacture kitchens in modular units. This is a highly competitive market and one other bank had already refused Craftwood Furniture a loan for this purpose. As a condition of the loan FastBank Ltd require guarantees from Phil Green, the Managing Director of Craftwood Furniture Ltd, Sarah (his partner of five years), and the firm’s employed production manager (John). John and Sarah’s guarantees are executed in the following circumstances: i) Sarah’s guarantee

Sarah is a director of the company and takes an active part in the management of the company, in particular, as financial controller. FastBank know of these facts since Sarah is a longstanding customer. Prior to the execution of the guarantee the bank manager interviews Sarah and Phil, explaining in general terms the nature of the guarantee and that if the guarantees were enforced (as a last resort), their home, which they jointly own, would be at risk. Subsequently, FastBank Ltd send both guarantees to the Green’s home address, addressing the

44

letter to Mr Green and requesting that the guarantees be signed. Sarah, who has become worried about the whole venture, is hesitant to sign the guarantee, but does so after Phil informs her that her liability under the guarantee was limited to S$50,000 (which was untrue).

ii) John’s guarantee FastBank Ltd are keen for John to become guarantor (secured by a third party mortgage) since he owns a substantial family house, inherited from his parents. John, like Sarah, is concerned about the commitment but wants to avoid confrontation with his employer and, in particular, is worried about finding another position if made redundant. The bank manager interviews John, whom he has known for many years as a customer of the bank and in the past has given him financial advice. However, he refused to answer a specific question from John as to whether Craftwood Furniture had always re–paid previous loans promptly, because that was a matter of “bank confidentiality”. In fact, Craftwood Furniture Ltd, to the knowledge of the bank, had defaulted on previous loans, although they were eventually repaid. FastBank Ltd also fails to disclose to John that: a) Phil Green had operated a previous business which had become insolvent; b) Craftwood Furniture Ltd had a poor credit–rating; c) FastBank Ltd, on a number of occasions had refused to honour cheques

drawn by Craftwood Furniture Ltd.

The bank manager advises John to seek independent legal advice and gives him the name of a solicitor who also sometimes acts for the bank, but not in relation to this matter. John takes advice from the solicitor, who sends a certificate of independent advice to the bank. John then signs the guarantee and third party mortgage, although he subsequently complains that the advice was inadequate because the solicitor merely read out the document word for word.

You have been asked to advise FastBank Ltd whether the guarantees (and the third party mortgage) are enforceable? Non–disclosure Phillips, paras 4–02 to 4–31. Commercial Bank of Australia Ltd v Amadio (1983) 151 CLR 184. Royal Bank of Scotland v Bennet (in Royal Bank of Scotland v Etridge [2002] 2 AC 773 at 871 – 878; paras 310 – 351). Susilawti v American Express Bank [2008] 1 SLR 237. Misrepresentation Phillips, paras 4–38 to 4–59. Vadasz v Pioneer Concrete CSA Pty Ltd (1995) 130 ALR 570. TSB Bank plc v Comfield [1995] 1 WLR 430.

45

Undue Influence Phillips, paras 4–130 to 4–167. *Royal Bank of Scotland v Etridge [2002] 2 AC 773. *Credit Lyonnais Bank Nederland NV v Burch [1997] 1 All ER 144. Unconscionable bargains *Phillips, paras 4–168 to 4–172. Commonwealth Bank of Australia v Amadio (above). Credit Lyonnais Bank Nederland NV v Burch (above). Lender’s liability for the conduct of the principal debtor or other third parties Phillips, paras 4–194 to 4–244. *Barclays Bank v O’Brien [1994] 1 AC 180. Bank of East Asia v Mody Sonal M [2004] 4 SLR 113. Royal Bank of Scotland v Etridge (above). Shepard v Midland Bank plc [1987] 2 FLR 175. Yerkey v Jones (1939) 63 CLR 212. Overseas–Chinese Banking Corp Ltd v Tan Teck Khong [2005] 2 SLR 694.

Guarantees: Case Study 2

Extent of liability and maintenance

1) Arthur Tan has entered into a guarantee (supported by a third party mortgage)

guaranteeing a loan facility of S$2,000,000 by FastBank Ltd to AB Construction Ltd. The guarantor’s liability is limited to S$250,000 and is given in respect of “all monies due and owing to the bank under or pursuant to ‘the specified loan agreement”. The purpose of the loan (as stated in the conditions of the loan) is to fund a construction project, the details of which are annexed to the loan agreement.

“This guarantee shall not be avoided or affected in any way by the bank making any

variation or alteration to the terms of the loan facility”. Subsequently FastBank Ltd agree with AB Construction that the amount of the loan

should be increased to S$4,000,000, with significant changes to the terms of the repayment (including interest charges). The scope of works of the construction project is also substantially increased.

FastBank Ltd are naturally keen to preserve its existing securities, in particular, the

guarantee given by Arthur Tan and seek your advice.

46

Phillips, para 5–61 to 5–74, paras 7–39 to 7–51, paras 7–56 to 7–63. *Triodos Bank NV v Dobbs [2005] EWCA Civ 630.

2) Discount Electronics agree to guarantee the indebtedness of its subsidiary ( Discount

Software Ltd) to FastBank Ltd. The guarantee (dated 01/01/2012) is in these terms:

“In consideration of FastBank Ltd *the Bank+ affording future banking facilities to Discount Software Ltd [the customer], we hereby guarantee to pay and satisfy to the bank on demand all and every sum which at any time shall be owing to the bank anywhere on any account whatsoever to a limit of S$2 million.” The guarantee is further secured by a third party mortgage over assets owned by Discount Electronics Ltd. The guarantee also contains, inter alia, a clause stating that “a certificate by an authorised officer of FastBank Ltd shall be conclusive evidence of the amount and legal existence of all and every sum which shall be owing to the bank on any account whatsoever” Discount Software Ltd becomes insolvent. FastBank Ltd seek to recover the following amounts from Discount Electronics Ltd upon the guarantee: a) A loan advanced by FastBank Ltd to Discount Software on 30/01/2011; b) Sums owing to FastBank Ltd by Discount Software Ltd arising from a failure to

meet payments on forward exchange contracts; c) A loan which had not been made directly to Discount Software Ltd , but had been

made through a subsidiary of FastBank Ltd based in Bermuda. This had been done at the request of Discount Software Ltd for tax minimisation purposes;

d) Amounts representing the liabilities of Discount Software Ltd as guarantor of another subsidiary company in the same group (Computer Software Ltd), to which FastBank Ltd has made another loan as principal debtor. This subsidiary company has now defaulted on repayment of the loan;

e) A debt owed by Discount Software Ltd to one of its suppliers, which has now been assigned to FastBank Ltd.

The authorised bank officer has certified “the amount and legal existence” of the total amount owning to the bank under head a) to e) is S$2 million and has detailed the liability under each head. FastBank Ltd demand S$2 million from Discount Electronics Ltd. You are asked to advise Discount Electronics Ltd to what extent it is liable under its guarantee? Phillips, paras 5–01 to 5–29, paras 5–55 to 5–60, paras 5–94 to 5–99, paras 5–112 to 5–123,paras 5–129 to 5–135, paras 5–146 to 5–151. Bank of India v Trans Continental Commodity Merchants and Patel [1982] 1 Lloyds Rep 506 (on appeal *1983+ 2 Lloyd’s Rep 298).

47

*Amalgamated Investment Property Co Ltd (in liquidation) v Texas Commerce International Bank Ltd [1982] QB 84. Bank of Scotland v Wright (1990) BCC 663. Chip Hua Poly– Construction Pte Ltd v Housing and Development Board [1997] 2 SLR 345. Standard Chartered Bank Ltd v Neocorp International Ltd [2005] 2 SLR 345.

3. International Development Ltd and Energy Construction Ltd enter into a building

contract for the construction of a residential complex by Energy Construction Ltd on land owned by International Development Ltd. The contract price is S$3.5 million and the date of completion is 1st January 2012. It is a condition of the contract that International Development will secure access to the site through adjoining council land during working hours (9–5pm each day). The obligations of Energy Construction Ltd are secured by a guarantee (called a bond) given by an insurance company. The bond states, inter alia, that this guarantee is given as security against the failure of Energy Construction to perform in accordance with the terms and conditions of the building contract”.

Two other clauses in the contract state:

a) The obligee shall at all times be entitled to treat the guarantor’s position and liabilities as those of the principal debtor.

b) The guarantor shall remain liable hereunder notwithstanding any other act or thing whereby, but for this provision the guarantor would not have been released.

International Development Ltd are only able to secure access to the site through adjoining council land from 12–5pm each day, which considerably impedes the progress of the work. As a result, International Development Ltd and Energy Construction Ltd agree to extend the time for completion for six months. At a later date it becomes necessary to change the building plans resulting in an increase in the contract price of S$5,000, which International Development Ltd agree to pay. Subsequently, Energy Construction Ltd become insolvent and fail to complete the work by 31st July 2012. International Development Ltd issue a demand upon the guarantor, but agree with the Receiver of Energy Construction Ltd to postpone further proceedings against the guarantor, as the receiver hopes to obtain additional funds to complete the work. Is the guarantor liable? Phillips, paras 7–01 to 7–19, paras 7–33 to 7–65, paras 7–71 to 7–79, paras 7–96 to 7–100, paras 7–105 to 7–117, paras 8–01 to 8–20. Holme v Brunskill (1878) 3 QBD 495. Corumo Holdings Pty Ltd v C Itoh Ltd (1991) 5 ACSR 720. Moat Financial Services Ltd v Wilkinson [2005] EWCA Civ 1253. National Westminster Bank Plc v Riley [1986] FLR 213.

48

Jurong Readymix Concrete Pte Ltd v Kaki Bukit Industrial Park Pte Ltd [2000] 4 SLR 723.

4. FastBank Ltd agrees to grant a S$2 million loan to Waste Disposal Ltd in order that it

can upgrade its ageing technology. It requires, as a security, a guarantee from Fred Smith, who has previously provided financial backing to Waste Disposal Ltd and is a non–executive director. Fred is somewhat concerned about increasing his financial exposure, but agrees to act as a guarantor to a limit of S$1 million after meeting with the bank in which he is informed that “the bank intends to take a mortgage over land owned by Waste Disposals Ltd, and a floating charge over its stock and other assets, and another guarantee from the managing director Arthur Brown”. Both Fred Smith and the bank assume that the land has a market value of over S$2 million.

It transpires that FastBank do not take a floating charge over Waste Disposal Ltd’s assets, and that the land value (over which the mortgage) is secured was (and is) worth only S$1 million because it has been contaminated by pollutants. FastBank Ltd takes a guarantee from Arthur Brown (with a limit of liability of S$500,000), but subsequently renegotiate that guarantee, reducing Arthur Brown’s liability to S$250,000, in the context of a subsequent restructuring of Waste Disposal Ltd’s financial accommodation. As regards Fred Smith’s guarantee, it has been executed hurriedly without Fred Smith’s name above his signature (although Fred Smith is clearly stated as guarantor in the heading to the guarantee). The manager of FastBank Ltd prints in the name and as a precaution adds his own name as a witness. Waste Disposal Ltd defaults on the loan and FastBank serves a demand on Fred Smith. Fred Smith denies liability and specifically requests FastBank to enforce the mortgage and sell the land because he believes the value of the land will fall even further. You are asked to advise FastBank Ltd as to the enforceability of the guarantees? Phillips, paras 4–64 to 4–68, paras 8–21 to 8–28, paras 8–36 to 8–61, paras 8–75 to 8–81. Greer v Keetle [1938] AC 156. Bank Industri Malaysia v Toplace Sdn Bhd [1997] 3 CLJ 389. Raiffeisen Zentralbank Osterreich AG v Crossseas Shipping [2000] 1 WLR 1135. Associated Japanese Bank (Int) Ltd v Credit du Nord SA [1989] 1 WLR 255. Palk v Mortgage Services Funding Plc [1993] 2 All ER 481.

Guarantees: Case Study 3

Enforcement

1. Jim Smith is the principal director of a wholesale electrical distributor called Fair Deal