SCDI Future Scotland - Macroeconomic & Fiscal Sustainability

63

Future Scotland Macroeconomic and Fiscal Sustainability April 2013

-

Upload

yvonne-macarthur -

Category

Documents

-

view

215 -

download

0

description

SCDI Future Scotland - Macroeconomic & Fiscal Sustainability

Transcript of SCDI Future Scotland - Macroeconomic & Fiscal Sustainability

Future Scotland

Macroeconomic and Fiscal Sustainability

April 2013

Disclaimer SCDI is an independent, non-aligned organisation, which maintains impartiality in matters of political debate. In this programme of work, SCDI is seeking to inform members on key economic issues relating to the debate on Scotland’s constitutional future. The contents of the Future Scotland reports are not intended to reflect SCDI policy.

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 1

Contents Page Foreword 3 Introduction 4 Executive Summary 5

Closing the Gap Constitutional Debate Key Questions

The Fiscal Gap 11

Scotland Long-term Fiscal Challenges 13

Fiscal Projections Economic – Low Growth Economic – Innovation Economic – Infrastructure Social – Ageing Demographics Social – Inequality Environmental – Climate Change Environmental – Resource Constraints

The Scottish Economy 18

Overview Competitiveness

Options and Opportunities to Address the Fiscal Challenge 20

Increase Revenues o Where Might Economic Growth to Generate Higher Revenues

Come From? o What Changes to Taxes Might Generate Higher Revenues?

Reduce Tax Evasion and Avoidance Taxes Reserved Taxes Institute of Fiscal Studies ‘Mirrlees Review’ of UK Tax

System (2012) Further Proposals Devolved Taxes

How Might Savings Be Made in Government Expenditure? The Constitutional Debate 30

Scotland’s Fiscal Position

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 2

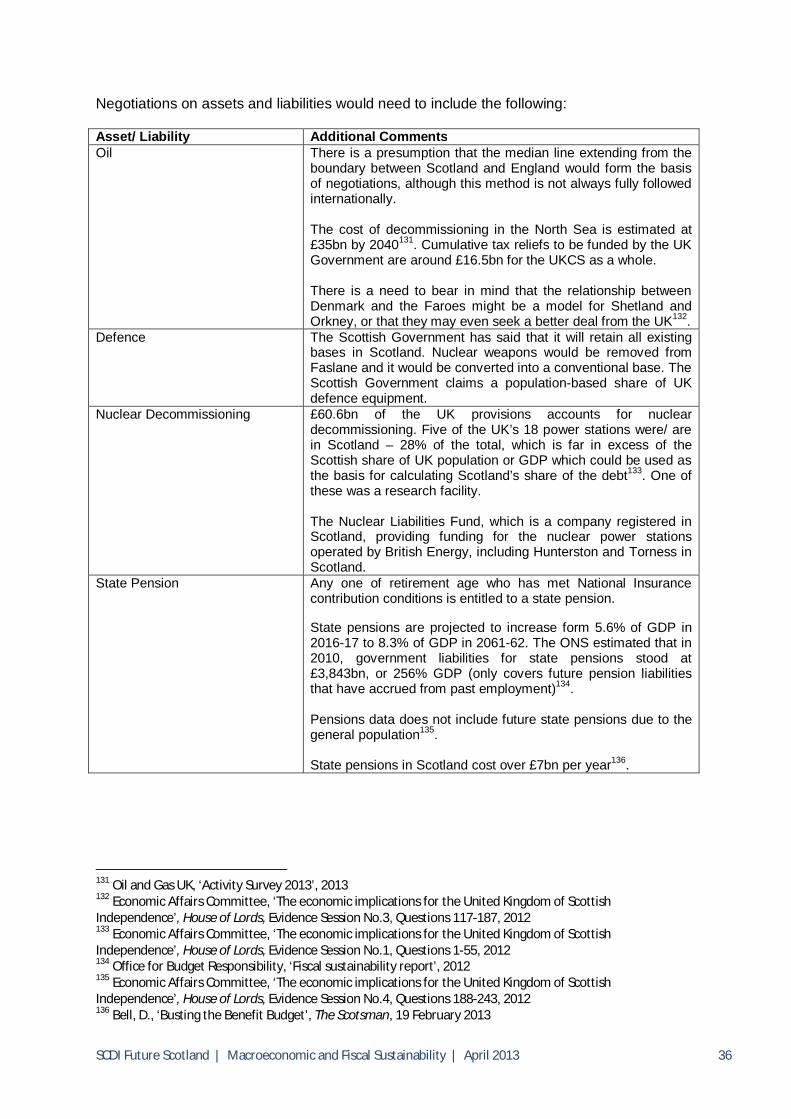

Page Division of Assets and Liabilities 31

International Rules The Role of External Creditors – Paper by Dane Rowlands Negotiations Debt Oil Revenues

Monetary Policy Options 40

Pound Euro Scottish Currency – Pegged Scottish Currency – Unpegged

Financial Stability 42

Financial Regulation Lender of Last Resort

Fiscal Policy 45

Credit Rating/ Borrowing Monetary Policy, Financial Stability and Fiscal Independence

The Fiscal Challenge 50

Revenue Generation and Collection Scottish Government Post-Independence Expenditure Policy Scottish Government Post-Independence Taxation Policy

Enhanced Devolution 52

Scotland Act Northern Ireland and Wales Party Political Proposals

o Federalism – Lib Dem Proposals o Labour Party Commission o Conservatives

Think-tank Proposals o Devo More o Devo Plus o Devo Max

ANNEX A 56 ANNEX B 57 ANNEX C 58 ANNEX D 59

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 3

Foreword Future Scotland: Future Growth In 2010, SCDI articulated in its Blueprint for Scotland the long-term vision and aspirations we maintain for a Scotland which is ambitious, enterprising and outward-looking; and which measures success in its ability to maximise its natural assets, its economic potential and its people. For more than eight decades, SCDI has pioneered thinking on the significant economic challenges of the time, from a perspective which is independent, inclusive and representative across civic Scotland. In 2013 SCDI continues to be a catalyst for debate and thought leadership, as our economy faces the challenges of unprecedented global change and competition. As an independent organisation with a broad membership, SCDI takes no political view on these issues for the Scottish electorate. However, the organisation’s role has always been to examine and consider impartially the industrial, commercial and economic challenges and opportunities facing Scotland. Amidst the current debate about Scotland’s future constitutional options, SCDI has undertaken an enquiry into some of the key issues across the Macroeconomic and Fiscal, Europe and International, and Energy spheres. Through this work, we hope to inform and provide insights to our members and stakeholders, through the identification and analysis of the issues and evidence to be considered. By way of recommendation, my engagement with expert colleagues on the Energy Working Group has been extremely useful in developing my understanding of the major issues for the sector – and the opportunities for our economy. As this body of work has developed, it has become increasingly clear that the issues raised in individual workstreams should not be considered in isolation, and that there is significant interrelation. For example, the implications for skills and employment in Scotland’s economy has been a recurrent theme across all workstreams. Therefore, it is recognised that a change in the responsibilities of governance of Scotland would not result in a series of discrete options, but rather a range of interrelated key choices, each of which would entail opportunities and constraints and many, if not all, of which would be related to others. Ultimately, such arrangements would be determined in negotiation and with agreement of other parties. The work is informed by wide and in-depth consultation across SCDI’s broad membership, including organisations across all sectors of the economy, in the corporate sector, SMEs, public sector agencies, trade unions, local authorities, educational institutions and the third sector. Online and face-to-face interviews have gathered substantial evidence from SCDI members and our work has also been informed by relevant statistics, statements and publications from a range of experts. These reports are not intended to provide comprehensive answers, or to outline SCDI policy. They are, however, intended to provide a framework to inform SCDI members and encourage further discussion, including at the SCDI Forum. I very much hope that this extensive programme of work will prove valuable to all who wish to achieve sustainable economic growth for Scotland. Bill Drummond Chair Scottish Council for Development and Industry

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 4

Introduction In the debate about Scotland’s economic future and the constitutional context, there is a need for impartial and informed analysis, and SCDI has responded to the requests from members to facilitate and inform their thinking and the discussion on key economic factors. Within this report, we present the findings of our Macroeconomic and Fiscal Sustainability Workstream – a high-level steering group of key business and civic leaders. In compiling it, SCDI has aimed to act as a safe forum and conduit for constructive debate and dialogue on the issues. In our 2010 Blueprint for Scotland, we proposed the managed restoration of the public finances (while continuing to support capital investment, research and development and skills) as a key five-year priority for the Scottish economy. It is now clear that this process will take longer and involve more fundamental choices and changes than originally envisaged – and that, looking forward, the main challenge will be to identify a balanced approach that delivers sustainable economic growth while addressing the additional pressures on public finances likely to be imposed by increasing social, economic and environmental demands. Our starting point was the need to address this challenge and forge a new path towards macroeconomic and fiscal sustainability, in any constitutional settlement. However, given SCDI’s overarching remit, consideration of the means by which sustainable economic growth might be achieved has been retained as a central theme. Our investigation has also taken account of another key priority identified in the Blueprint: the need to restore the strength, reputation and competitiveness of Scotland’s financial services sector and its important support for investment in business, manufacturing and infrastructure. We outline the principal economic issues in these areas and suggest a number of Key Questions which politicians, campaigners and stakeholders on all sides of the constitutional debate should consider. These Key Questions are summarised on page 10 below. We would like to thank the Steering Group and the many SCDI members who have contributed their expertise and experience to make this process robust and representative. Brendan Dick Brian Veitch Co-chairs Macroeconomic and Fiscal Sustainability Workstream

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 5

Executive Summary1 The UK recorded a deficit between its tax receipts and its expenditure in 27 of the 33 years between 1979 and 2011. Persistent annual deficits accumulated to build up the UK national debt, and this resulted in increasing interest charges to service the debt. Between 1997 and 2007 the UK Government reduced public sector borrowing slightly, but the majority of other leading industrial countries achieved a greater reduction. When the financial crisis struck, this left the UK in a more vulnerable position relative to comparable countries. The UK’s annual fiscal deficit increased substantially following the financial crisis and recession in 2007-08, as tax revenues slumped. In response, a rolling programme of spending cuts and tax increases has been implemented, but, thus far, these have only reduced the annual fiscal deficit from 11.2% of GDP in 2009-10 to 7.9% of GDP in 2011-12. As a result, the UK national debt has continued to increase, albeit at a slightly reduced rate. With the economy sluggish and the recession significantly reducing its long-term productive potential, debt is forecast to continue growing and to peak at 85.6% of GDP in 2016-17. The UK’s credit rating has been downgraded for the first time since 1978. This has raised questions about the sustainability of the levels of borrowing which prevailed under the pre-2007 economic and fiscal model and whether a new approach is needed to close the fiscal gap. Scotland’s public finances are also in deficit. It is estimated that in 2011-12 Scotland had a deficit of 11.2% of GDP excluding North Sea revenue or a deficit of 2.3% of GDP when a geographical share of North Sea revenue is included. In recent years, Scotland’s deficit has tended to be larger than the UK’s when tax revenues from oil and gas are excluded and similar if not smaller when they are included. If oil and gas tax revenues were to decline, Scotland’s fiscal deficit would increase, unless other revenue sources emerge or spending is reduced. It is also forecast that the UK’s public finances will come under renewed pressure over the longer term, with receipts from oil and gas production taxes, environmental taxes and tobacco duties expected to reduce by up to 2% of GDP over the next 30 years. This report recognises a significant number of long-term challenges which will put pressure on fiscal sustainability:

Economic - Low Growth – linked to high indebtedness curtailing public spending and an ageing population reducing worker productivity and entrepreneurship;

Economic – Innovation – weak business investment and R&D spending Economic – Infrastructure – inadequate investment and structures to support the

development of economic infrastructure projects, in particular transport and energy Social – Ageing Demographics – much of the future spending increases projected

can be attributed to the UK’s ageing population profile. In Scotland, the number of ‘dependants’ per 100 people of working age population is expected to rise from 60 per 100 to 64 per 100 in 2035, with an increase of pensionable aged people of 2.9% compared with 1.7% for the UK. An ageing population will incur higher health, care and pension costs. Modelling carried out by COSLA forecast a funding gap for local authority services of almost £3bn by 2016-17, with around half attributed to a rising demand for services driven largely by demographics and future needs. Twenty per cent of people in the UK are doing nothing to save for their retirement

1 For all source references please see full report

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 6

Social – Inequality – income inequality may slow growth, causes credit booms and financial busts and weaken demand. The UK has had the most rapid increase in income inequality of the 34 OECD countries since 1975, with a rising share of national income taken by the top 1%. Inequality of opportunity accounts for over 20% of total inequality in Britain and inhibits social mobility. In 2009, Scotland had the widest gap in educational attainment between the top and bottom 20% in developed Europe

Environmental – Climate Change – The Scottish Government has estimated the cost to the Government of implementing its proposals and policies on climate change could amount to £8bn by 2022. It has been estimated that while this would cost less than 1% of GDP in 2020, the long-term cost of not acting would be 5-20% of GDP

Environmental – Resource Constraints – Over the next 20 years the growth of the resource hungry middle-classes is predicted to be faster than at any other time in history, and to reach 5bn by the end of the period. At the same time, resources will be under pressure from rising extraction costs

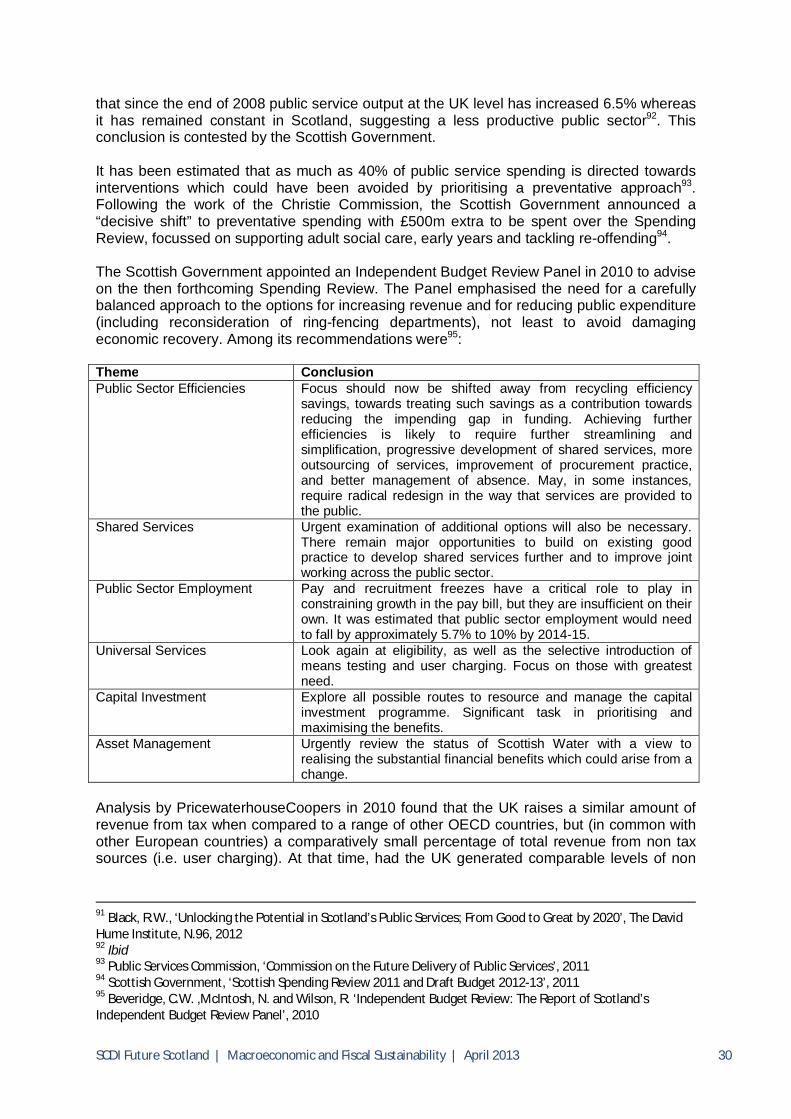

Closing the Gap This report makes an assessment of the ability of the Scottish economy to meet these challenges. In a UK context, the Scottish economy has performed relatively well over the last 30 years, in comparison with some other UK regions such as North East England. The success of the oil and gas and financial services sectors in Scotland were two significant factors. Scotland’s gross value added (GVA) per head at 98.7% of the UK average in 2010 is exceeded only by London and South-East England. Scotland’s average annual growth in GDP over the 30 years to 2006 was 0.5% below the UK average and 0.9% behind the average of comparable EU countries. However, Scotland’s population has not grown as fast as either over the same period. Those industrial sectors which grew fastest in Scotland over the 10 years prior to the 2007/08 financial crisis, such as financial services, property and retail, are unlikely to grow as strongly in the future. While the latest annual survey of Scottish exports showed an increase of 7% to £23.9bn in 2011, there is evidence that at a UK level that exports stalled in 2012. Scotland has particular weaknesses in entrepreneurial activity, business R&D and innovation. The Scottish Government has identified three means by which Scotland’s long-term sustainable rate of economic growth can be increased and its per capita income raised:

Increasing the level of labour productivity and competitiveness; Increasing the participation rate i.e. the number of people actually working; Increasing Scotland's population and the supply of potential workers.

Its economic strategy identifies seven key growth sectors and analysis of the strategies of these sectors suggests that strongest growth is anticipated in oil and gas, renewables and food and drink. The report then considers revenue-raising from key taxes and reducing tax evasion and avoidance. Over the last 35 years the overall tax take in the UK has been relatively stable at around 38% of GDP. Corporation tax in the UK is currently higher than the EU average of 22.6%, but, with the aim of stimulating investment, it is to be reduced in stages to reach 20% in 2015, the lowest rate of any major western economy, with the aim of stimulating investment. We highlight the recommendations of the ‘Mirrlees Review’ on reforming the UK tax system; these include improvement of the work incentives for those around pension age (to increase total earnings by £3bn) and the introduction of road user charging to replace fuel

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 7

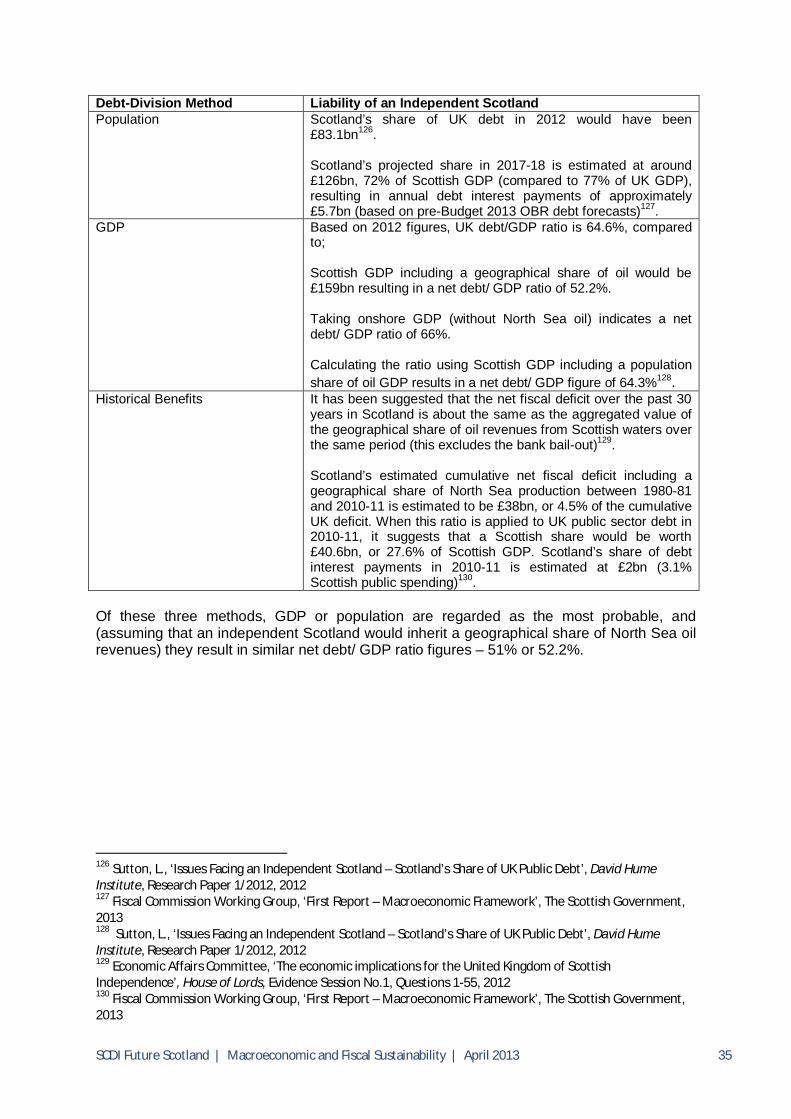

duty and protect revenue of £38bn. The Scottish Government has relatively few revenue-raising powers and has implemented a freeze on council tax. In 2011-12, Scotland accounted for 9.3% of total UK public spending, compared to its 8.4% share of the UK population. In 2010-11 spending was estimated to be higher in all categories with the exception of defence. Following devolution, the Scottish Government Budget grew by an average of 5.5% per annum in real terms, but this growth ended with UK fiscal consolidation. It may take until 2025-26 for the Scottish Government’s total budget to return to its 2009-10 levels in real terms and, in which case, the cumulative loss in the intervening period is estimated at potentially £51bn. The Scottish Government has a target that all public sector bodies should deliver a 3% efficiency target per annum. It has been estimated that as much as 40% of public service spending is directed towards interventions which could have been avoided by adopting a preventative approach. The Scottish Government is spending an estimated £500m over three years until 2014-15, focussed on supporting adult social care, early years and tackling re-offending. It also appointed an Independent Budget Review Panel in 2010 for advice on spending. A number of its recommendations were implemented, but, as identified in this report, some were not. Constitutional Debate This is the fiscal context for the debate on Scotland’s constitutional future. Under current constitutional arrangements, the Scottish Budget is largely determined by a block grant from the UK Government. The size of this grant is defined by the Barnett Formula. The advantages of this approach include its simplicity, stability and the absence of UK ring-fencing of Scottish spending. However, there is a very weak link between expenditure and revenue-raising in Scotland. Arguably, this reduces accountability and efficiency, and does not provide sufficient incentives to improve the economy and deliver value for money. Public spending per capita in Scotland is above the average for England and slightly above for Wales. On the other hand, if the UK deficit is removed from GDP calculations, and the geographic share of North Sea oil and gas revenue that an independent Scotland could expect to receive is included, Scotland currently receives approximately as much public money as it contributes through taxes. The fiscal position of an independent Scotland would not be the same as that of Scotland within the UK. We identify key UK assets and liabilities and consider how these might be divided if Scotland were to separate from the UK. The UK Government’s view is that an independent Scotland would be responsible for a share of the UK’s liabilities, but, legally, the rUK would continue to own the UK’s assets. The Scottish Government’s view is that Scotland would be entitled to a proportionate share of the UK’s assets and that there would be a negotiation on liabilities. It highlights the major and at times overlooked influence of external creditors on the negotiations whose interest is receiving their money back. Three debt-division methods have been proposed:

1. Population – Scotland accounts for 8.4% of the UK’s population. 2. GDP – Scotland accounts for 8.3% of the UK’s GVA 3. Historical benefits – net benefits/ fiscal debts over a period e.g. 30 years?

Of these three methods, debt division based on population or GDP are regarded as the most probable, and would result in similar net debt/ GDP ratio figures for an independent Scotland. Projections of oil and gas production tax revenues and liabilities from decommissioning are central to any debate about the potential fiscal position of an independent Scotland.

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 8

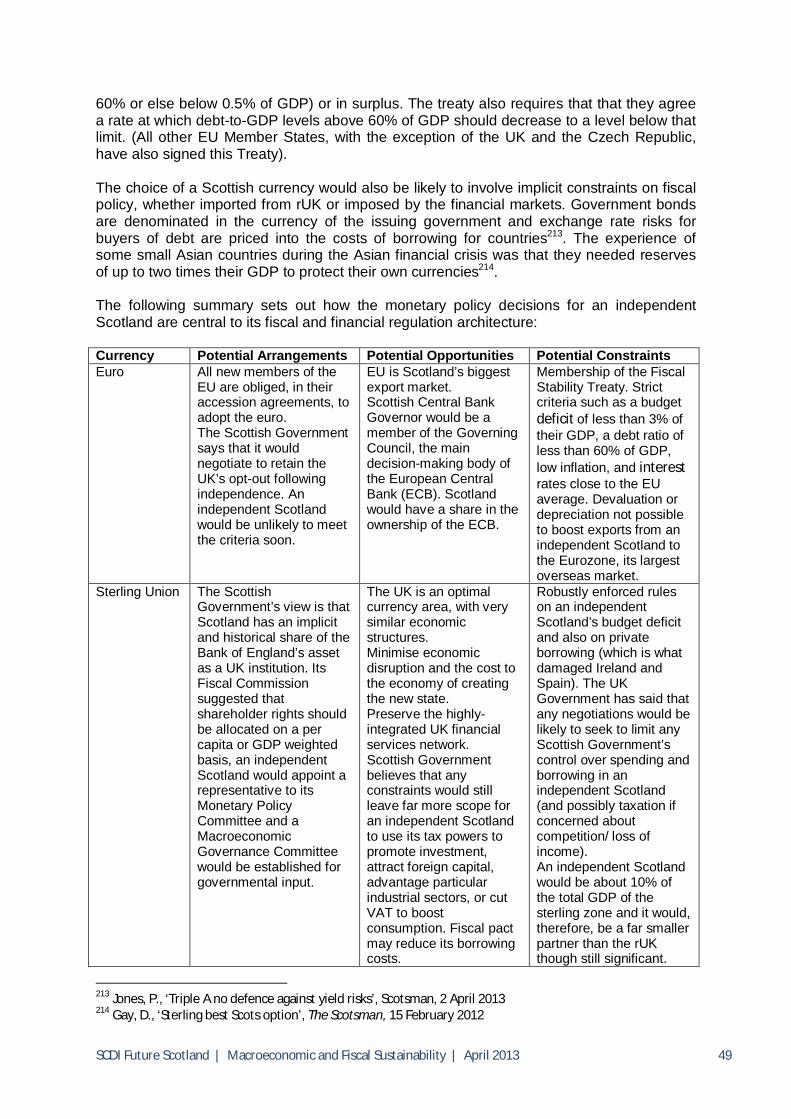

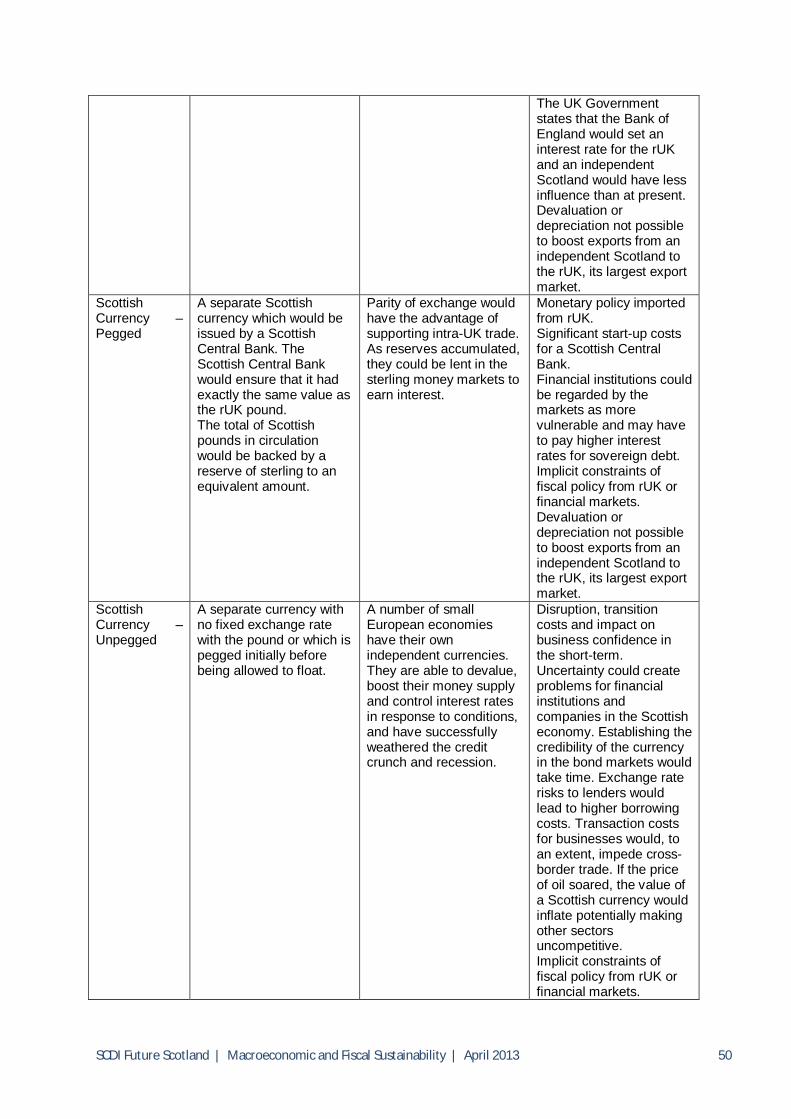

Government revenues from production are a function of (a) oil prices, (b) oil/gas production, (c) new investment and capital allowances allowed against income for tax purposes. In recent years, there have been wide swings in the price of oil and medium-term forecasts vary significantly. North Sea oil and gas production has appeared more erratic and difficult to predict. Increased capital investment totalling £13bn for the year ending 2013 will increase oil and gas production in time but, in the short-term, tax revenues will reduce as the capital allowances associated with planned investment increases. For an independent Scotland, the key issues would be the volatility of this revenue and maximising revenues in the long-term. Over the long-term, estimates prepared by the OBR suggest that tax revenues will fall to the equivalent of 3% of Scottish GDP, compared with 5-10% of GDP during the previous 30 years. Other economists believe that revenues can be sustained at 5%. The costs of providing decommissioning relief to industry for the UK Government are estimated to be around £16.5bn, mostly for installations in Scottish waters. An independent Scotland would need to be able to fund its share or this could lead to premature decommissioning of fields by industry. The monetary policy decisions for an independent Scotland are central to its fiscal and financial regulation arrangements. Four currency options are discussed in this report:

Euro; Sterling Union; Scottish Currency – pegged; and Scottish Currency – unpegged.

The report summarises the potential institutional arrangements for each and the potential opportunities and constraints for economic and fiscal policy which these options entail. The UK has an opt-out from the euro, however all new Member States are obliged in their accession agreements to adopt the euro when they meet the necessary criteria. The Scottish Government has said that it would aim to negotiate retention of an opt-out while the UK Government has said that an independent Scotland would not automatically inherit one. An independent Scotland would be highly unlikely to meet the debt-to-GDP ratio criteria for membership in the near future. Membership of the euro would mean a common currency with Scotland’s largest overseas trade market, but also adherence to the strict rules of the EU’s Fiscal Stability Treaty. A Sterling Union is the strong preference of the Scottish Government. The UK is an optimal currency zone and a sterling union would minimise economic disruption. An independent Scottish Government would have scope to use fiscal levers, but a rUK Government may seek in negotiations on the currency to limit its flexibility over spending and borrowing, while the Bank of England may set an interest rate for the rUK and not for an independent Scotland. A pegged Scottish currency would also support cross-border trade with the rUK and allow for more flexibility on future options, but would import monetary policy from the rUK with implicit fiscal constraints, and involve start-up and, probably, higher borrowing costs. An unpegged Scottish currency would mean that an independent Scotland could devalue, boost its monetary supply and control its interest rates in response to conditions. However, it would be more disruptive for businesses and mean start-up and transition costs, with the probability that uncertainty and the need to build credibility in the bond markets would mean higher borrowing costs. These arrangements are of key concern to the highly-integrated UK financial services sector. Two of the UK’s largest banks, RBS and Lloyds, both part-owned by the UK Government, have their HQs in Scotland. Insurers based in Scotland sell 94% of their products to the rest

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 9

of the UK while 84% of mortgages sold by Scottish firms are to the rest of the UK. Scottish Financial Enterprise believes that, implicitly under the EU’s regulatory framework, Scotland would need its own financial regulator. The Scottish Government’s Fiscal Commission has proposed that systemically important banking institutions should be supervised either by the Bank of England, under an agency agreement with the Scottish Government, or by a Scottish Monetary Institute in partnership with the Bank. A Scottish regulator would undertake microprudential regulation of financial services companies. The challenges of establishing a separate financial regulator should not be underestimated. Lender of last resort facilities were provided to RBS at a cost of about 3% of UK GDP – comparable figures for an independent Scotland have been estimated at 37% of GDP. The Scottish Government’s Fiscal Commission has proposed that such interventions in the future could be undertaken jointly and co-ordinated through its proposed Macroeconomic Governance Committee. The UK Government has also said that the rUK would be unlikely to intervene until there was an impact on the rUK’s financial position and, if it did agree to the arrangements, it would probably negotiate tight rules to govern the finances of the Scottish Government and Scotland’s banks. Financial markets and overseas customers would want as much assurance as possible. This may influence the banks on their future corporate locations and structures. Monetary and financial regulation arrangements would influence the rate at which an independent Scotland could borrow. Credit ratings are usually but not always reflected in a government’s cost of borrowing. Moodys has recently downgraded the UK’s credit rating. There is some evidence of a small country risk premium for borrowing, though small countries are among the few remaining with AAA ratings. Scotland’s debt inheritance, lack of a track record, volatile revenues and large banks, may result, initially, in a higher borrowing rate and, therefore, extra outlays from the budget of an independent Scottish Government. The Scottish Government’s Fiscal Commission has recommended that an independent Scotland should plan budgets on a “cautious estimate” for North Sea oil revenues and invest any upside revenue volatility in a stabilisation fund. How an independent Scotland would address the fiscal sustainability challenge would not be clear until the completion of negotiations with the rUK and the formation of the first independent Scottish Government. Our report does identify some of the expenditure and taxation proposals of the present administration. In particular, Scottish Ministers would like to reduce corporation tax. However, in negotiations on the continuance of a sterling union and common financial regulation, it is possible that the rUK may seek to limit an independent Scottish Government’s flexibility in fiscal policy, particularly if it was concerned about the fiscal stability of a sterling zone, and about cross-border competition for investment and the potential reduction of its tax revenues. This report concludes with a description of the Scotland Bill and opposition party policies and/ or processes for enhanced devolution. This has not been a focus for SCDI’s work, but we are interested in how all constitutional arrangements – independence, the status quo, and enhanced devolution - would address the Key Questions that follow.

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 10

Key Questions How could best use be made of fiscal and other levers to deliver sustainable economic growth while addressing the pressures on public finances likely to be imposed by increasing social, economic and environmental demands? How could different constitutional arrangements, including the Union and Scottish Independence, and their associated opportunities and constraints, impact on the challenge above and the following questions?

1. How can the current and projected gaps between Scotland’s revenues and expenditure be closed? What can we learn from countries which have successfully tackled fiscal challenges and have greater fiscal sustainability?

2. What can be done to stimulate sustainable economic growth, particularly in those areas where Scotland’s performance has been at its weakest, such as the rates of entrepreneurial activity, business R&D and innovation activity?

3. What are the fiscal levers which could most improve business growth in Scotland? What would be the likely trade-offs between tax competiveness, public investment and the costs of doing business across the UK market?

4. What can be done to address fiscal challenges from economic competition, an

ageing population, climate change, inequality, infrastructural renewal and declining revenues from oil and gas production and environmental taxes?

5. What can be done - in terms of key criteria such as economic growth and structure,

budgetary performance and stability, debt burdens and management, political stability, wealth and demographics – to ensure that Scotland benefits from competitive rates of borrowing from financial markets?

6. How could possible currency arrangements affect Scotland’s ability to deliver on this agenda and what opportunities and constraints could these entail?

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 11

The Fiscal Gap All governments borrow money. Governments may run a deficit between their revenues and their expenditures which requires borrowing from the financial markets for a variety of sound reasons e.g. to cover for an unexpected shortfall in revenues, to stimulate demand in the economy, to invest in infrastructure which will enable economic growth in the long-term or to finance war. Successive UK Governments have needed to borrow to make up the difference between receipts and expenditure. In the 33 years between 1979 and 2011, the UK has had a deficit in 27 of these. Persistent annual deficits lead to the build up of national debt and interest payments, Following large-scale wars, the UK has had a level of debt which is far higher than today. However, by running budget surpluses, it managed to reduce these debts over time. Between 1997 and 2007 the UK Government reduced public sector borrowing slightly and was using a greater proportion of borrowing to finance investment rather than current spending. Public sector debt was also reduced over this period. However, the vast majority of other leading industrial countries achieved a greater reduction in borrowing and debt over this decade, leaving the UK in a worse-off position when the financial crisis struck, relative to comparable countries2. The deficit substantially increased following the financial crisis and recession in 2007-08, as tax revenues slumped. In response, a rolling programme of tax increases and spending cuts has been implemented under successive Governments. The new Coalition Government committed to two fiscal targets - a fiscal mandate which states that the structural current budget must be forecast to be in balance or surplus by the end of the five year forecast horizon, and a supplementary target that states Public Sector Net Debt (PSND) as a share of national income must be falling at a fixed date of 2015-16. The Institute of Fiscal Studies (IFS) reported that by the end of 2012-13, 79% of the planned tax increases, 67% of the investment spending cuts, 32% of the benefit spending cuts and 21% of the public service cuts will have been implemented3. When it is completed, the austerity programme will be the longest in the UK’s history. The Scottish Government has estimated that, on current forecasts, it could take until 2025-26 for the Scottish Budget to return to the level of 2009-10 in real terms, which would result in a cumulative amount foregone over that period of close to £51bn4. Arguments will continue as to whether the cuts were unavoidable and necessary to heal the economy and public finances, or have resulted in higher deficits by reducing growth, thereby decreasing tax revenues and leading to higher welfare spending5. Either way, the deficit is now forecast by the independent Office of Budgetary Responsibility to be 5.6% of GDP in 2012-13, and is expected to peak at 6.8% next year before declining to 2.2% of GDP by 2017-18. Debt is forecast to continue growing and peak at 85.6% of GDP in 2016-17, before falling only slightly to 84.8% in 2017-18. As a result, the Government’s target for PSND looks highly likely to be missed6. Debt interest is making up a growing proportion of the UK Government’s expenditure, and in turn restricts governments’ ability to respond to future challenges. Reflecting this deteriorating outlook, agencies have started to downgrade the credit rating of the UK for borrowing for the first time since 1978. 2 Chote, R. et al, 'The Public Finances: 1997 to 2010', Institute of Fiscal Studies, IFS BN93, 2010 3 Institute of Fiscal Studies, ‘The IFS Green Budget: February 2013’, 2013 4 Gillespie, G., ‘State of the Economy – November 2012’, Scottish Government, 2012 5 International Monetary Fund, ‘World Economic Outlook: Coping with High Debt and Sluggish Growth’, 2012 6 Office for Budget Responsibility, ‘Economic and Fiscal Outlook’, 2013

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 12

As has previously been noted, the UK has successfully reduced far larger debts in its history. Even following the recession in the early 1990s, there were fears about the sustainability of the UK’s public debt which economic growth subsequently dispelled. However, there is a concern among SCDI members and some economists that the long-term fiscal position of the UK is weaker than at that time. Reasons for this include:

The UK’s structural budget deficit was already growing before the recession; The large proportion of tax revenues which were generated from the UK’s financial

services sector will not return due to reforms to the banking sector; The UK, with Japan, is the most indebted of all big, rich economies. The aggregate

indebtedness of the UK – the sum of household debts, company debts, government debts and bank debts – was estimated to have risen to 507% of GDP by 2012. By way of comparison, US indebtedness fell to 279% of GDP and Germany’s was 278% (and even Spain’s was far lower at 363%)7;

The UK faces substantial long-term expenditure challenges, particularly due to fundamental demographic changes increasing health and social care costs;

According to the OBR’s analysis, the recession has significantly reduced the long-term productive potential of the UK economy and there is little scope for above-trend rates of economic growth. In 2008, the Treasury’s “cautious” projection was that potential national income would grow by 2.5% per year. However, the OBR estimates that the potential capacity of the economy increased by an average of 0.4% a year between 2007−08 and 2012−13 and from 2013-14 onwards the long-term growth rate is just 2.25%. As such, potential national income is now estimated to be 13% lower in 2016−17 than was projected by the Treasury in 20088;

The economic axis of the world is shifting decisively to emerging markets. One possible way of reducing debt is through inflation reducing the debt to GDP ratio. The IMF, however, considered 26 episodes since 1875 when debt has topped 100% of GDP and how that ratio was then reduced, concluding that the relationship between inflation and debt reduction is ambiguous, and while hyperinflation clearly correlates with sharp debt reduction, if these extreme episodes are excluded, there is no clear association between the average inflation rate and the change in debt9. Higher inflation can boost tax revenues. However, it can also increase spending on benefits and public sector wages. It can result in investors demanding higher interest rates to compensate for inflation risks. UK debt is high, its debt maturity is around 13 years, and a fifth of this debt is inflation linked. It has therefore been ranked as one of the worst placed G7 countries to reduce debt through inflation (Germany was ranked best placed due to its small deficit, little inflation linked debt and average debt maturity of six years). Private sector debt is also much higher that it was in the 1970s, and in Britain 66% of outstanding mortgages are variable rate10. Inflation in the UK has been and is expected to remain above the Bank of England’s 2% target. While some of these challenges may be particularly acute for the UK, on-going debates in the US and Eurozone have illustrated that the broader issue of fiscal sustainability is common to many developed countries. For example, the German Chancellor Angela Merkel

7 McKinsey Global Institute, ‘Debt and deleveraging: Uneven progress on the path to growth’, 2012 8 Johnson, P. and Phillips, D., ‘Scottish independence: the fiscal context’, Institute for Fiscal Studies, 2012 9 International Monetary Fund, ‘World Economic Outlook: Coping with High Debt and Sluggish Growth’, 2012 10 The Economist, ‘Escaping the debt crisis: the inflation option’, The Economist, 14 June 2011

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 13

has pointed out that, while Europe accounts for 8% of the world’s population and 25% of its GDP, it accounts for 50% of its social spending11. Scotland The Government Expenditure and Revenue Scotland (GERS) is the official analysis of the current budget balance for the public sector in Scotland. It estimated that in 2011-12 there was a deficit of £14bn (11.2% of GDP) excluding North Sea revenue or a deficit of £3.4bn (2.3% of GDP) including an illustrative geographical share of North Sea revenue. In 2011-12, the UK as a whole ran a current budget deficit, including 100% of North Sea revenue, of £92.3bn (6% of GDP). In the year 2009-10, Scotland’s fiscal deficit would have been 18.1% of GDP excluding oil revenues and 10.7% of GDP including a geographical share of oil revenues. Between 1980-81 and 2011-12 Scotland’s average annual net fiscal deficit is estimated at 9.2% of GDP excluding North Sea revenue. Including a geographical share of North Sea revenue, this becomes an average 0.2% surplus. The UK in the same period is estimated to have run an average annual net fiscal deficit of 3.2%12.

The IFS has found that this has been generally true of recent years. Excluding oil and gas revenues, or assigning them on a population basis, results in a larger spending gap in Scotland than in the UK as a whole. However, assigning oil and gas revenues geographically results in a similar if not smaller spending gap in Scotland13. The Centre for Public Policy for Region’s (CPPR) forecasts of Scotland’s fiscal balance have predicted that by the year 2016-17 (excluding North Sea revenue) Scotland would have a deficit of £13.7bn (9.3% of GDP). When North Sea revenue is taken into account, the deficit closes to £9.2bn (5.1% of GDP)14. So there is a similar large deficit between revenues and expenditure in Scotland to the UK as a whole. How to return to long-term fiscal sustainability is, therefore, a challenge which Scotland would and must face under any constitutional settlement. Long-term Fiscal Challenges Fiscal Projections The long-term outlook for public spending and revenues is subject to huge uncertainties. When projected forward, relatively minor changes to GDP growth or demographics in the short-term compound into far greater differences. Central to the projections made by the OBR is an assumption that economic productivity will grow at an average 2.2% per year, in line with the average rate over the last 50 years. The OBR suggests that public finances will come under pressure over the longer term. Spending other than on debt interest will rise from 35.6% of GDP forecast for 2016-17 to 40.8% of GDP by 2061-62. Meanwhile, declining receipts from oil and gas production taxes, environmental taxes and tobacco duties are expected to reduce revenue by up to 2% of GDP over the next 30 years. Corporation tax and VAT receipts may also come under downward pressure due to international competition. This would result in the primary budget balance moving from a projected surplus of 1.7% of GDP in 2016-17 to a deficit of 2.6% of

11 Peel, Q., 'Merkel warns on cost of welfare', Financial Times, 16 December 2012 12 Scottish Government, ‘Government Expenditure and Revenue Scotland 2011-12’, 2013 13 Johnson, P. and Phillips, D., ‘Scottish independence: the fiscal context’, Institute for Fiscal Studies, 2012 14 Centre for Public Policy for Regions, ‘Analysis of Scotland’s Past and Future Fiscal Position: Reflections on GERS 2013, the Scottish Government’s Oil and Gas Analytical Bulletin, and the 2013 UK Budget’, March 2013

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 14

GDP in 2061-62. Debt is projected to fall from 74% of GDP in 2016-17 to 57% in the mid-2020s, before rising at an increasingly faster rate to reach 89% of GDP in 2061-6215. The sustainability of public sector debt can be measured through consideration of the ‘fiscal gap’ i.e. how large a permanent spending cut or tax increase is necessary to move public sector net debt to a particular target level at a particular target date. The OBR illustrates that to return UK debt to a pre-crisis level of 40% of GDP in 2061-62, the government would need to introduce, probably incrementally, a permanent tax increase or spending cut of 1.1% of GDP (£17bn in today’s terms)16. The Scottish Government expects real terms increases in the costs of providing public services for two reasons: in the long run wages rise in real terms to ensure that appropriate staff can be recruited and retained, and demographic pressures will increase demand for public services, particularly but not only in health, requiring real terms increases in budgets, and the costs of state pensions and public sector pensions17. Economic – Low Growth High debt/GDP levels (90% and above) are associated with lower growth. Between 1830 and 2009 average real GDP growth during periods of UK government debt of over 90% was only 1.8% per year, compared to 2.15% with debt between 60-90% of GDP, 2.2% for debt between 30-60% of GDP and 2.5% for debt below 30%18. Academics have modelled financial collapses from the last 200 years and found that, on average, it took countries with similar levels of modern debt 23 years to recover19. By the 2020s and 2030s the working age population of ageing European countries and Japan is expected to contract between 0.5% and 1.5% per year. Household savings rates will decline as a larger share of the population moves into retirement years, potentially dampening economic growth and worker productivity, and entrepreneurship will fall. It has been suggested that “unless labour-force participation rates surge or economic performance improves dramatically, some developed countries could face a future of secular economic stagnation—in other words, of zero real GDP growth from peak to peak of the business cycle”20. It is expected that small-population, ageing European countries will have the slowest growth. While the UK will perform better, its growth rates over the next few decades are still expected to be significantly lower than over the previous decades. HSBC has suggested annual GDP growth rates for the UK of 1.6% (2010-20), 1.7% (2020-30), 1.9% (2030-40) and 2.2% (2040-50), compared to 2.4% over the last 30 years21.

15 Office for Budget Responsibility, ‘Financial Sustainability Report’, 2012 16 Ibid 17 Swinney, J., Scottish Government Cabinet Paper, 2012 18 Reinhart, C.M., Rogoff, K.S., ‘Growth in a Time of Debt’, The National Bureau of Economic Research, Working paper No.15639, 2010 19 Reinhart, C.M., Reinhart, V.R, and Rogoff, K.S., ‘Debt Overhangs: Past and Present’, The National Bureau of Economic Research, Working paper No.18015, 2012 20 Jackson, R., ‘How demography is reshaping the economic and social landscape of the 21st century’, The Geneva Association, 2012 21 Ward, K., ‘The World in 2050: From the Top 30 to the Top100’, HSBC Global Research, 2012

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 15

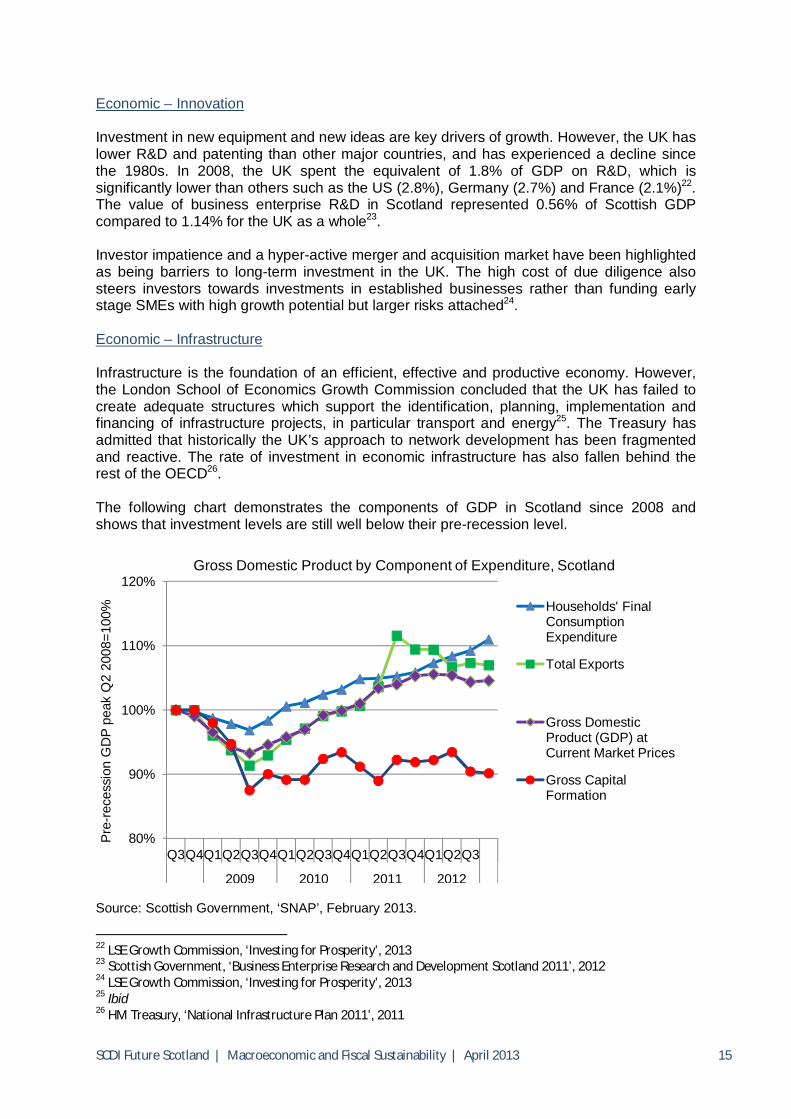

Economic – Innovation Investment in new equipment and new ideas are key drivers of growth. However, the UK has lower R&D and patenting than other major countries, and has experienced a decline since the 1980s. In 2008, the UK spent the equivalent of 1.8% of GDP on R&D, which is significantly lower than others such as the US (2.8%), Germany (2.7%) and France (2.1%)22. The value of business enterprise R&D in Scotland represented 0.56% of Scottish GDP compared to 1.14% for the UK as a whole23. Investor impatience and a hyper-active merger and acquisition market have been highlighted as being barriers to long-term investment in the UK. The high cost of due diligence also steers investors towards investments in established businesses rather than funding early stage SMEs with high growth potential but larger risks attached24. Economic – Infrastructure Infrastructure is the foundation of an efficient, effective and productive economy. However, the London School of Economics Growth Commission concluded that the UK has failed to create adequate structures which support the identification, planning, implementation and financing of infrastructure projects, in particular transport and energy25. The Treasury has admitted that historically the UK’s approach to network development has been fragmented and reactive. The rate of investment in economic infrastructure has also fallen behind the rest of the OECD26. The following chart demonstrates the components of GDP in Scotland since 2008 and shows that investment levels are still well below their pre-recession level.

Source: Scottish Government, ‘SNAP’, February 2013.

22 LSE Growth Commission, ‘Investing for Prosperity’, 2013 23 Scottish Government, ‘Business Enterprise Research and Development Scotland 2011’, 2012 24 LSE Growth Commission, ‘Investing for Prosperity’, 2013 25 Ibid 26 HM Treasury, ‘National Infrastructure Plan 2011’, 2011

80%

90%

100%

110%

120%

Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3

2009 2010 2011 2012

Pre

-rec

essi

on G

DP

pea

k Q

2 20

08=1

00%

Gross Domestic Product by Component of Expenditure, Scotland

Households' Final Consumption Expenditure

Total Exports

Gross Domestic Product (GDP) at Current Market Prices

Gross Capital Formation

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 16

According to the Institution of Civil Engineers only ‘Water and Waste Water’ infrastructure in Scotland is adequate. ‘Energy’, ‘Transport’, ‘Waste’, and ‘Flood Risk Management’ infrastructure, on the other hand, all require attention27. The backlog in maintenance of the physical estate in Scotland has been estimated to stand in excess of £4bn. In addition, local authorities will need to increase waste management spending by £580m per year in order to meet waste management targets28. At a time when the Scottish population has grown to record high figures, the level of all housing completions last year was the lowest since World War Two29. Where possible, housing adaptations represent a cost-effective alternative to residential care for the elderly and can reduce hospital admissions. It is estimated that the number of pensioner households requiring adaptations to make them more suitable for old age will increase from 66,300 in 2008 to over 106,000 in 203330. The UK’s National Infrastructure Investment Plan identifies a pipeline of projects valued at around £310bn to 2015 and beyond31. The Scottish Government’s Infrastructure Investment Plan identifies its plans for investment in the next 20 years. The total cost has of this Plan been, independently, estimated to be around £60bn32. Social - Ageing Demographics Much of the future spending increases projected by the OBR can be attributed to the UK’s ageing population profile. The proportion of the population aged over 65 will rise from 17% in 2012 to an estimated 26% in 206133. In Scotland, the proportion of older people aged 85+ is expected to double in 2010-30 from 1.9% to 3.8%. Between 1951 and 2009 life expectancy increased from 64.4 to 75.8 for males and from 68.7 to 80.3 years for females, 10 to 20 years after the default retirement ages34. The dependency ratio (number of ‘dependants’ per 100 people of working age population) is expected to rise from 60 per 100 to 64 per 100 in 2035, with an increase of pensionable aged people of 2.9% compared with 1.7% for the UK35. Although healthy life expectancy is increasing, it is not improving at the same rate36. An ageing population will incur higher health, care and pension costs. For example, the amount of money spent by Scottish local authorities on providing personal care services to older people in their own homes has more than doubled in the last 7 years, increasing from £133m in 2003-04 to £342m in 2010-1137. Modelling carried out by COSLA forecast a funding gap for local authority services of almost £3bn by 2016-17, with around half attributed to a rising

27 Institution of Civil Engineers, ‘The State of the Nation Briefing, Scotland: Infrastructure Special 2011’, 2011 28 Black, R.W., ‘Unlocking the Potential in Scotland’s Public Services; From Good to Great by 2020’, The David Hume Institute, N.96, 2012 29 Homes for Scotland, ‘Activity Report, 2012’, 2012 30 Scottish Government, ‘Age, home and community: a strategy for housing for Scotland’s Older People: 2012-2021’, 2011 31 HM Treasury and Infrastructure UK, ‘National Infrastructure Plan: update 2012’, 2012 32 Scottish Government, ‘Capital Spending Plans’, 6 December 2012 33 Office for Budget Responsibility, ‘Financial Sustainability Report’, 2012 34 Bell, D., ‘Fiscal Sustainability: Issues for the Finance Committee Work Programme 2012’, 2012 35 Finance Committee, ‘Demographic change and aging population inquiry; submission from The National Records of Scotland’, Scottish Parliament, 2012 36 Scottish Government, ‘Demographic change in Scotland’, 2010 37 Scottish Government, ‘Free Personal and Nursing Care, Scotland, 2010-11’, A National Statistics Publication for Scotland, 2012

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 17

demand for services driven largely by demographics and their needs in the future38. State pensions in Scotland cost over £7bn per year39. Across the UK, it has been estimated that an additional 6% of GDP will be required by 2030 to meet the social costs of ageing and other commitments40. According to a study of 15 developed and developing countries, people in the UK are the worst prepared for retirement, with savings which will run out after a third of the way through the average retirement, leaving a further 12 years with no savings41. Another study suggested that, in 2011, 20% of people were doing nothing at all to prepare for their retirement. Two-thirds of those who could reasonably be expected to save for retirement (i.e. excluding under 30’s and those earning less than £10,000 per year) were preparing adequately, while the remaining third either did not save or made only a ‘token effort’42. Social – Inequality Research by economists at the International Monetary Fund suggests that income inequality slows growth, causes financial crises and weakens demand. A survey for the World Economic Forum pointed to inequality (alongside fiscal imbalances) as the most pressing problem of the coming decade. Bigger income gaps can reduce social mobility and, therefore, future prosperity. Some economists have said that rising income gaps have led to credit booms as those falling behind try to keep up, causing macroeconomic instability, although others have disputed this evidence. The Gini co-efficient aggregates the gaps between people’s incomes into a single measure. The UK has had the most rapid increase in income inequality of the 34 OECD countries since 1975, with a rising share of national income taken by the top 1%43. According to the World Bank, inequality of opportunity accounts for over 20% of total inequality in Britain. This is higher than the US and any European country except Italy. Over half of income differences persist between generations in the UK, reflecting a low level of social mobility44. In 2009 Scotland had the widest gap in educational attainment between the top 20% and bottom 20% in developed Europe. At the age of 15 the bottom 20% performs as if they have received 5 years less schooling than the top 20%45. “Skill-biased technological change” is one of the main determinants of inequality. The London School of Economics Growth Commission stated that improving human capital is arguably the most effective way of encouraging inclusive growth and reversing these trends in rising inequality46. Environmental – Climate Change The Climate Change (Scotland) Act 2009 established a statutory commitment to reduce emissions by 42% by 2020 compared to 1990 levels, and by 80% by 2050. The Scottish

38 Finance Committee, ‘Demographic change and aging population inquiry; submission from COSLA’, Scottish Parliament, 2012 39 Bell, D., ‘Busting the Benefit Budget’, The Scotsman, 19 February 2013 40 2020 Public Services Trust, ‘From social security to social productivity: a vision for 2020 Public Services: The final report of the Commission on 2020 Public Services’, The RSA, 2010 41 HSBC, ‘The Future of Retirement: A new reality - Global report’, 2013 42 Scottish Widows, ‘The Scottish Widows UK Pensions Report; Seventh annual report on the state of retirement savings across the nation’, 2011 43 OECD, ‘Divided We Stand: Why Inequality Keeps Rising’, 2011 44 The Economist, ‘Special Report: For Richer, For Poorer’, 13 October 2012 45 Mair, C., Zdeb, K. and Markie, K., ‘Making Better Places: Making Places Better; the distribution of positive and negative outcomes in Scotland’, The Improvement Service, 2011 46 LSE Growth Commission, ‘Investing for Prosperity’, 2013

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 18

Government has estimated the cost to the Government of implementing its proposals and policies on climate change could amount to £8bn by 202247. However, due to the potential of climate change to disrupt the economy the costs of inaction could be much higher. The UK Government’s Committee on Climate Change has advised that while the 42% reduction target is likely to cost less than 1% of GDP in 2020, the cost of not acting is estimated at 5-20% of GDP48. The Stern Review concluded that tackling climate change is a long-term pro-growth strategy49. Environmental – Resource Constraints Over the last 30 years there has been a large expansion in the global population and the number of people globally who can be defined as ‘middle class’ in terms of consumption has also grown from around 1.1bn to 1.8bn. Over the next 20 years the growth of this resource hungry portion of population is predicted to continue rising to nearly 5bn people, an expansion far faster than at any other time in history50. Resources are also under pressure from rising extraction costs. Forecasts indicate that demand could triple for a series of critical materials by 2030 compared with 2006 levels. The price of copper has already increased 400% between 2000-10. The shortage and instability of supply of these materials is already impacting business. The Scottish Economy Overview In a UK context, the Scottish economy has performed relatively well over the last 30 years, diverging from regions such as North East England. The success of the oil and gas and financial services sectors were two major reasons. GDP per head is now above nearly every English region. Scotland’s gross value added (GVA) per head at 98.7% of the UK average in 2010 is only exceeded by London and the south-east of England. In the 1960s Scotland’s GDP per head was 12% below the UK’s average, making it one of the poorest regions51. Scotland’s average annual growth in GDP over the 30 years to 2006 was 1.9%, well below the UK average of 2.4%, resulting in an underlying GDP growth gap of around 0.5%, but its population has not grown as fast as the rest of the UK either52. The gap in the unemployment rates of England and Scotland fell from almost 4% in the mid-1980s to virtually zero since 200053. In terms of annual average growth of GDP over the last 30 years, Scotland has performed worse than EU countries of a comparable size (i.e. Austria, Denmark, Finland, Ireland, Luxembourg, Portugal and Sweden). Their average was 2.7%, resulting in an underlying GDP growth gap of around 0.9%54. However, the Scottish Government argues that Eurostat GDP per capita figures have shown Scotland would be fifth richest country in the EU while

47 Beveridge, C.W. ,McIntosh, N. and Wilson, R. ‘Independent Budget Review: The Report of Scotland’s Independent Budget Review Panel’, 2010 48 Scottish Government, ‘Low Carbon Scotland: Meeting the Emissions Reduction Targets 2010-2022’, 2011 49 Stern, N, ‘Stern Review: The Economics of Climate Change’, HM Treasury, 2006 50 McKinsey, ‘Mobilizing for a resource revolution’, McKinsey Quarterly, 2012 51 McCrone, G., ‘The Scope for Economic Policy After Independence’, 2012 52 Economic Affairs Committee, ‘The economic implications for the United Kingdom of Scottish Independence’, House of Lords, Evidence Session No.3, Questions 117-187, 2012 53 Economic Affairs Committee, ‘The economic implications for the United Kingdom of Scottish Independence: Oral and Written Evidence’, House of Lords, p.21-30, 2012 54 ‘Technical Notes for Scotland Performs Indicators and Targets – Purpose Target 1’ http://www.scotland.gov.uk/Topics/Statistics/About/NotesSP/TechnicalNotesSPPT1

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 19

the UK would rank 11th55. On the other hand, the Centre for Public Policy for Regions (CPPR) says if the Scottish Government used GNP rather than GDP figures, Scotland’s position would not be as high. It estimates that Scotland would be about the 15th richest country in the world56. According to the CPPR, the fastest growing industrial sectors since 1998 were:

Financial Services; Transport, Storage & Communications; Real Estate and Business Services; Retail & Wholesale (for Scotland); Health & Social Work (for the UK)57.

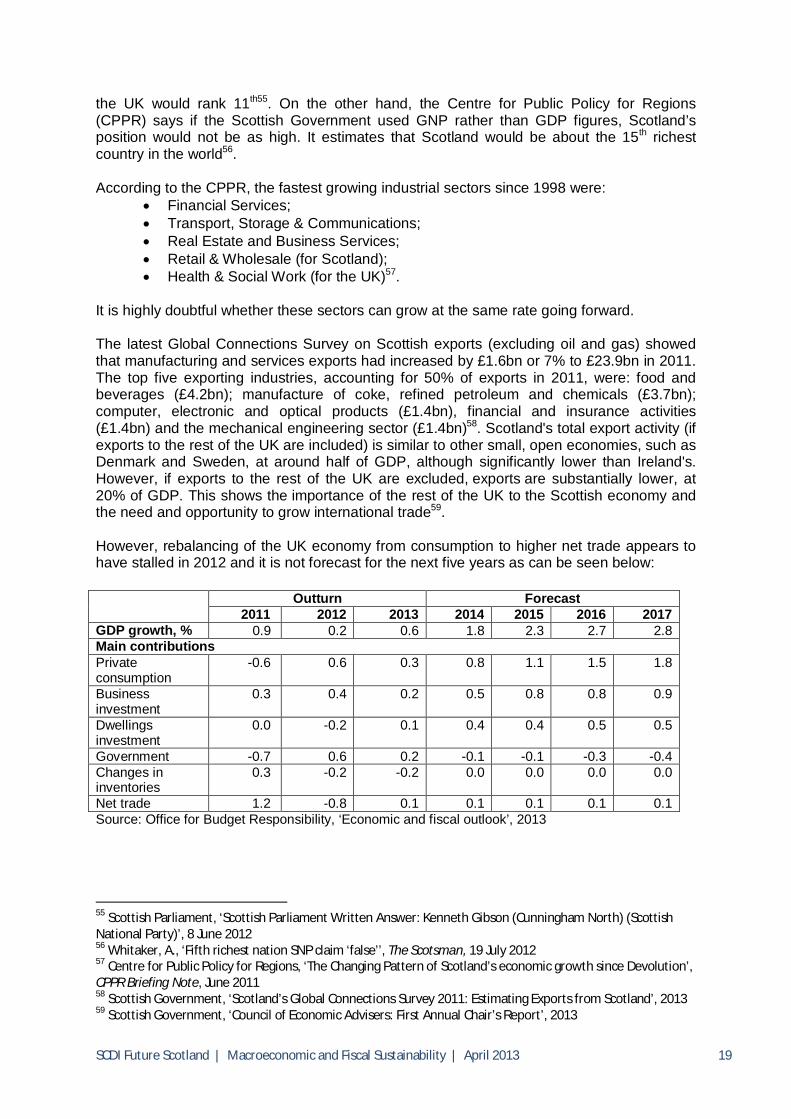

It is highly doubtful whether these sectors can grow at the same rate going forward. The latest Global Connections Survey on Scottish exports (excluding oil and gas) showed that manufacturing and services exports had increased by £1.6bn or 7% to £23.9bn in 2011. The top five exporting industries, accounting for 50% of exports in 2011, were: food and beverages (£4.2bn); manufacture of coke, refined petroleum and chemicals (£3.7bn); computer, electronic and optical products (£1.4bn), financial and insurance activities (£1.4bn) and the mechanical engineering sector (£1.4bn)58. Scotland's total export activity (if exports to the rest of the UK are included) is similar to other small, open economies, such as Denmark and Sweden, at around half of GDP, although significantly lower than Ireland's. However, if exports to the rest of the UK are excluded, exports are substantially lower, at 20% of GDP. This shows the importance of the rest of the UK to the Scottish economy and the need and opportunity to grow international trade59. However, rebalancing of the UK economy from consumption to higher net trade appears to have stalled in 2012 and it is not forecast for the next five years as can be seen below: Outturn Forecast

2011 2012 2013 2014 2015 2016 2017 GDP growth, % 0.9 0.2 0.6 1.8 2.3 2.7 2.8 Main contributions Private consumption

-0.6 0.6 0.3 0.8 1.1 1.5 1.8

Business investment

0.3 0.4 0.2 0.5 0.8 0.8 0.9

Dwellings investment

0.0 -0.2 0.1 0.4 0.4 0.5 0.5

Government -0.7 0.6 0.2 -0.1 -0.1 -0.3 -0.4 Changes in inventories

0.3 -0.2 -0.2 0.0 0.0 0.0 0.0

Net trade 1.2 -0.8 0.1 0.1 0.1 0.1 0.1 Source: Office for Budget Responsibility, ‘Economic and fiscal outlook’, 2013

55 Scottish Parliament, ‘Scottish Parliament Written Answer: Kenneth Gibson (Cunningham North) (Scottish National Party)’, 8 June 2012 56 Whitaker, A., ‘Fifth richest nation SNP claim ‘false’’, The Scotsman, 19 July 2012 57 Centre for Public Policy for Regions, ‘The Changing Pattern of Scotland’s economic growth since Devolution’, CPPR Briefing Note, June 2011 58 Scottish Government, ‘Scotland’s Global Connections Survey 2011: Estimating Exports from Scotland’, 2013 59 Scottish Government, ‘Council of Economic Advisers: First Annual Chair’s Report’, 2013

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 20

In terms of inward investment, Ernst and Young’s UK Attractiveness Survey showed that Scotland topped the UK league in terms of job creation from FDI in 2011 for the second year running and secured 33.3% of all R&D projects investments into UK60.

60 Ernst & Young, ‘UK Attractiveness Survey’, 2011

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 21

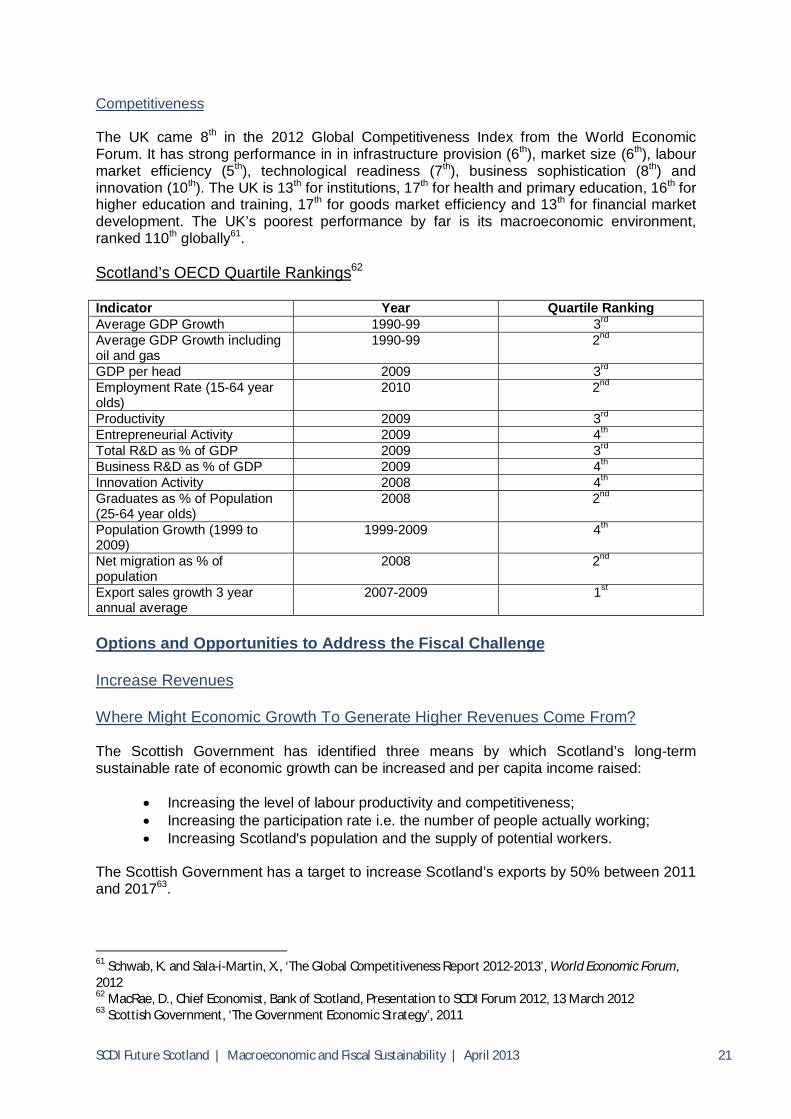

Competitiveness The UK came 8th in the 2012 Global Competitiveness Index from the World Economic Forum. It has strong performance in in infrastructure provision (6th), market size (6th), labour market efficiency (5th), technological readiness (7th), business sophistication (8th) and innovation (10th). The UK is 13th for institutions, 17th for health and primary education, 16th for higher education and training, 17th for goods market efficiency and 13th for financial market development. The UK’s poorest performance by far is its macroeconomic environment, ranked 110th globally61. Scotland’s OECD Quartile Rankings62 Indicator Year Quartile Ranking Average GDP Growth 1990-99 3rd Average GDP Growth including oil and gas

1990-99 2nd

GDP per head 2009 3rd Employment Rate (15-64 year olds)

2010 2nd

Productivity 2009 3rd Entrepreneurial Activity 2009 4th Total R&D as % of GDP 2009 3rd Business R&D as % of GDP 2009 4th Innovation Activity 2008 4th Graduates as % of Population (25-64 year olds)

2008 2nd

Population Growth (1999 to 2009)

1999-2009 4th

Net migration as % of population

2008 2nd

Export sales growth 3 year annual average

2007-2009 1st

Options and Opportunities to Address the Fiscal Challenge Increase Revenues Where Might Economic Growth To Generate Higher Revenues Come From? The Scottish Government has identified three means by which Scotland’s long-term sustainable rate of economic growth can be increased and per capita income raised:

Increasing the level of labour productivity and competitiveness; Increasing the participation rate i.e. the number of people actually working; Increasing Scotland's population and the supply of potential workers.

The Scottish Government has a target to increase Scotland’s exports by 50% between 2011 and 201763.

61 Schwab, K. and Sala-i-Martin, X., ‘The Global Competitiveness Report 2012-2013’, World Economic Forum, 2012 62 MacRae, D., Chief Economist, Bank of Scotland, Presentation to SCDI Forum 2012, 13 March 2012 63 Scottish Government, ‘The Government Economic Strategy’, 2011

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 22

To guide and track progress, the Scottish Government’s Economic Strategy has outlined a number of long term targets.

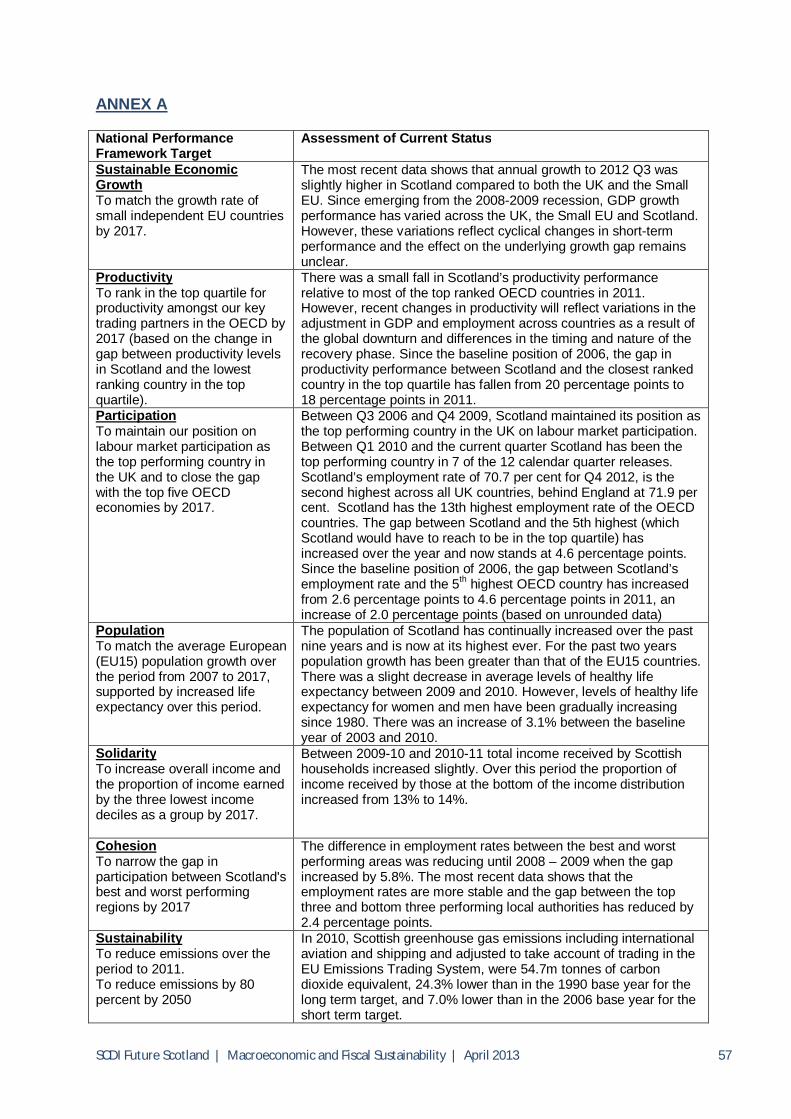

1. Sustainable Economic Growth –To match the growth rate of small independent EU countries by 2017.

2. Productivity – To rank in the top quartile for productivity amongst our key trading partners in the OECD by 2017 (based on the change in gap between productivity levels in Scotland and the lowest ranking country in the top quartile).

3. Participation – To maintain our position on labour market participation as the top performing country in the UK and to close the gap with the top five OECD economies by 2017.

4. Population – To match the average European population growth over the period from 2007 to 2017, supported by increased life expectancy over this period.

5. Solidarity – To increase overall income and the proportion of income earned by the three lowest income deciles as a group by 2017.

6. Cohesion – To narrow the gap in participation between Scotland's best and worst performing regions by 2017.

7. Sustainability – To reduce emissions over the period to 2011. To reduce emissions by 80 per cent by 2050.

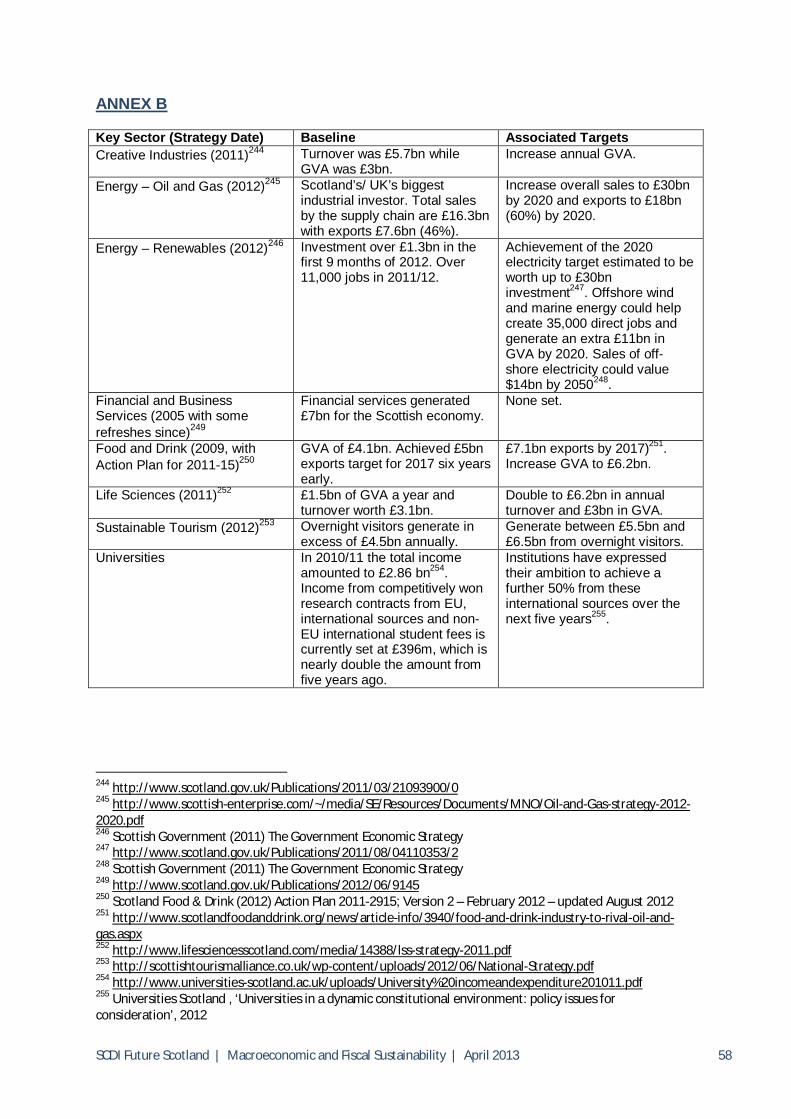

(Further information on progress with each target can be found in Annex A). The Scottish Government’s Economic Strategy identifies seven key sectors in which the Scottish economy has comparative advantages: energy, financial services, life sciences, creative industries, universities, tourism and food and drink. Industry Leadership Groups have prepared growth strategies and associated targets for most of these sectors. Further information on the associated targets can be found in Annex B. Particularly strong growth appears to be anticipated in the following:

1. Oil and gas – £44bn investment in North Sea 2012-16; increase total supply chain sales from £16.3bn to £30bn and exports from £7.6bn to £18bn by 2020.

2. Renewables – 2020 electricity target estimated to be worth up to £30bn investment; offshore wind and marine could generate an extra £11bn GVA.

3. Food and drink – increase exports from £3.7bn to £7.1bn between 2007-17. The wider Low Carbon Economic Strategy64 suggests that the worth of the Scottish sector could increase from £8.5bn to £12bn between 2007-08 and 2015-16, with the number of jobs growing 4% a year to 2020, rising by 130,000 (5% of the workforce). The Cities Strategy65 recognises Scotland’s city-regions as key economic drivers. Scottish Development International expects that there will be a strong increase in demand for Scottish goods and services in the following international markets66:

China: the second largest energy consumer after the USA, and by 2017 the largest importer of food, offering significant opportunities for the energy and food and drink sectors.

The Middle East: significant investment in the energy sector is expected over the next decade.

Norway: high demand for Scottish premium food and drink supported by high disposable incomes, as well as opportunities in oil and gas.

64 Scottish Government, ‘A Low Carbon Economic Strategy for Scotland’, 2011 65 Scottish Government, ‘Scotland’s Cities: Delivering for Scotland’, 2011 66 Scottish Development International, ‘SDI to open seven new international offices’, 27 July 2012

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 23

Brazil: the world’s ninth largest oil producer, offering significant opportunities for Scotland’s oil and gas sector.

West Africa: significant opportunities for the oil and gas sector, including supply chain development and technology collaboration.

South Africa: the 5th largest export market for Scotch Whisky. Canada: rated as the top place to do business in the G7 over the next 3 years by the

Economist Intelligence Unit. South East Asia: the world’s fastest growing student market, expected to account

for 70% of the demand for international higher education by 2025. What Changes to Taxes Might Generate Higher Revenues? Reduce Tax Evasion and Avoidance In 2010-11 the tax gap was estimated to be around £32bn, or 6.7% of tax liabilities. This includes the following: criminal activity (£5bn), undeclared economic activity (£5bn), avoidance (£5bn), evasion (£4bn), legal interpretation (£4bn), non-payment i.e. because of business insolvency (£4bn), failure to take reasonable care i.e. careless/negligent recording and preparation of tax returns (£3bn), and error (£2bn). The largest proportion of the tax gap (45%) arises from Income Tax, National Insurance Contributions and Capital Gains Tax, followed by VAT (30%), Corporation Tax (13%), Excise duties and indirect taxes (10%), and other direct taxes (2%)67. In the 2012 Budget the UK Government announced additional measures to close tax loopholes and bring around £1bn of extra revenue and protect around £10bn over the next five years. It is also planning to introduce a General Anti-Abuse Rule which is aimed at deterring and tackling artificial and abusive tax avoidance schemes68. It has estimated that globally over $21tr has been invested in offshore tax havens. The UK will prioritise the issue of offshoring profits in its G8 Presidency in 201369.

67 HMRC, ‘Measuring tax gaps 2012: tax gap estimates for 2010-11’, 2012 68 HMRC, ‘Issue Briefing: tackling tax avoidance’, 2012 69 Osborne, G, ‘Autumn Statement 2012 to the House of Commons by the Rt Hon George Osborne, MP, Chancellor of the Executive’, 2012

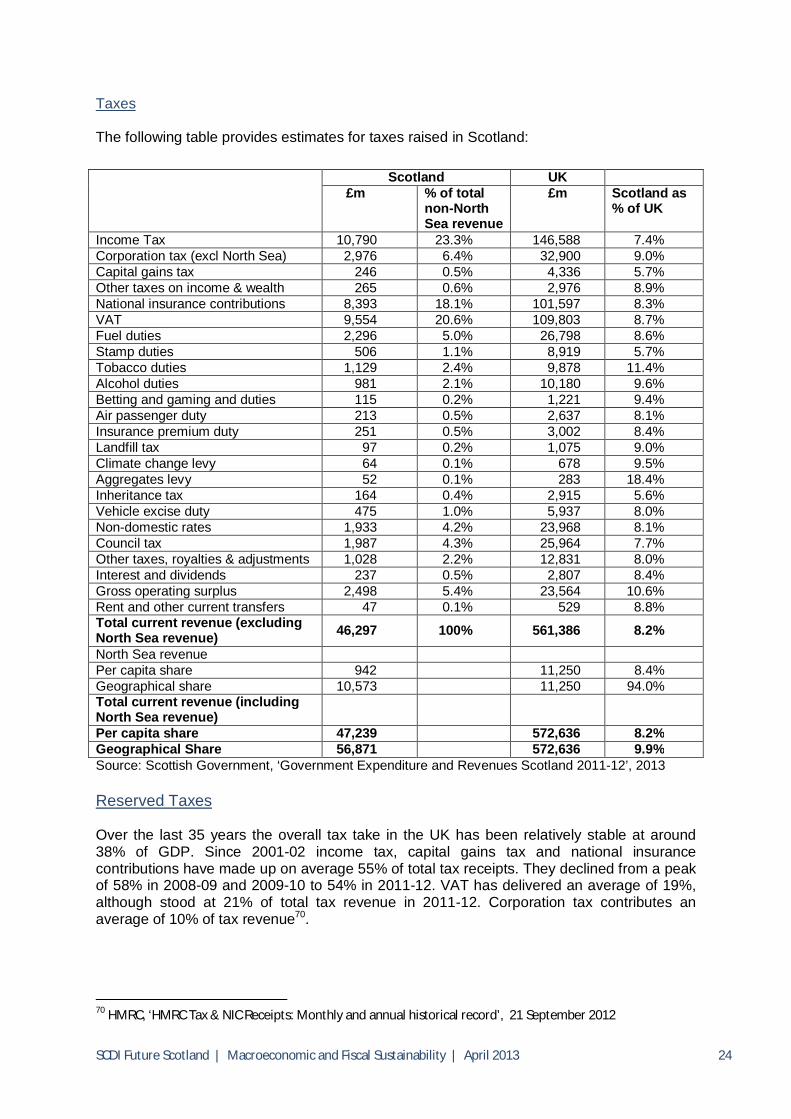

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 24

Taxes The following table provides estimates for taxes raised in Scotland: Scotland UK

£m % of total non-North Sea revenue

£m Scotland as % of UK

Income Tax 10,790 23.3% 146,588 7.4% Corporation tax (excl North Sea) 2,976 6.4% 32,900 9.0% Capital gains tax 246 0.5% 4,336 5.7% Other taxes on income & wealth 265 0.6% 2,976 8.9% National insurance contributions 8,393 18.1% 101,597 8.3% VAT 9,554 20.6% 109,803 8.7% Fuel duties 2,296 5.0% 26,798 8.6% Stamp duties 506 1.1% 8,919 5.7% Tobacco duties 1,129 2.4% 9,878 11.4% Alcohol duties 981 2.1% 10,180 9.6% Betting and gaming and duties 115 0.2% 1,221 9.4% Air passenger duty 213 0.5% 2,637 8.1% Insurance premium duty 251 0.5% 3,002 8.4% Landfill tax 97 0.2% 1,075 9.0% Climate change levy 64 0.1% 678 9.5% Aggregates levy 52 0.1% 283 18.4% Inheritance tax 164 0.4% 2,915 5.6% Vehicle excise duty 475 1.0% 5,937 8.0% Non-domestic rates 1,933 4.2% 23,968 8.1% Council tax 1,987 4.3% 25,964 7.7% Other taxes, royalties & adjustments 1,028 2.2% 12,831 8.0% Interest and dividends 237 0.5% 2,807 8.4% Gross operating surplus 2,498 5.4% 23,564 10.6% Rent and other current transfers 47 0.1% 529 8.8% Total current revenue (excluding North Sea revenue) 46,297 100% 561,386 8.2%

North Sea revenue Per capita share 942 11,250 8.4% Geographical share 10,573 11,250 94.0% Total current revenue (including North Sea revenue)

Per capita share 47,239 572,636 8.2% Geographical Share 56,871 572,636 9.9% Source: Scottish Government, ‘Government Expenditure and Revenues Scotland 2011-12’, 2013 Reserved Taxes Over the last 35 years the overall tax take in the UK has been relatively stable at around 38% of GDP. Since 2001-02 income tax, capital gains tax and national insurance contributions have made up on average 55% of total tax receipts. They declined from a peak of 58% in 2008-09 and 2009-10 to 54% in 2011-12. VAT has delivered an average of 19%, although stood at 21% of total tax revenue in 2011-12. Corporation tax contributes an average of 10% of tax revenue70.

70 HMRC, ‘HMRC Tax & NIC Receipts: Monthly and annual historical record’, 21 September 2012

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 25

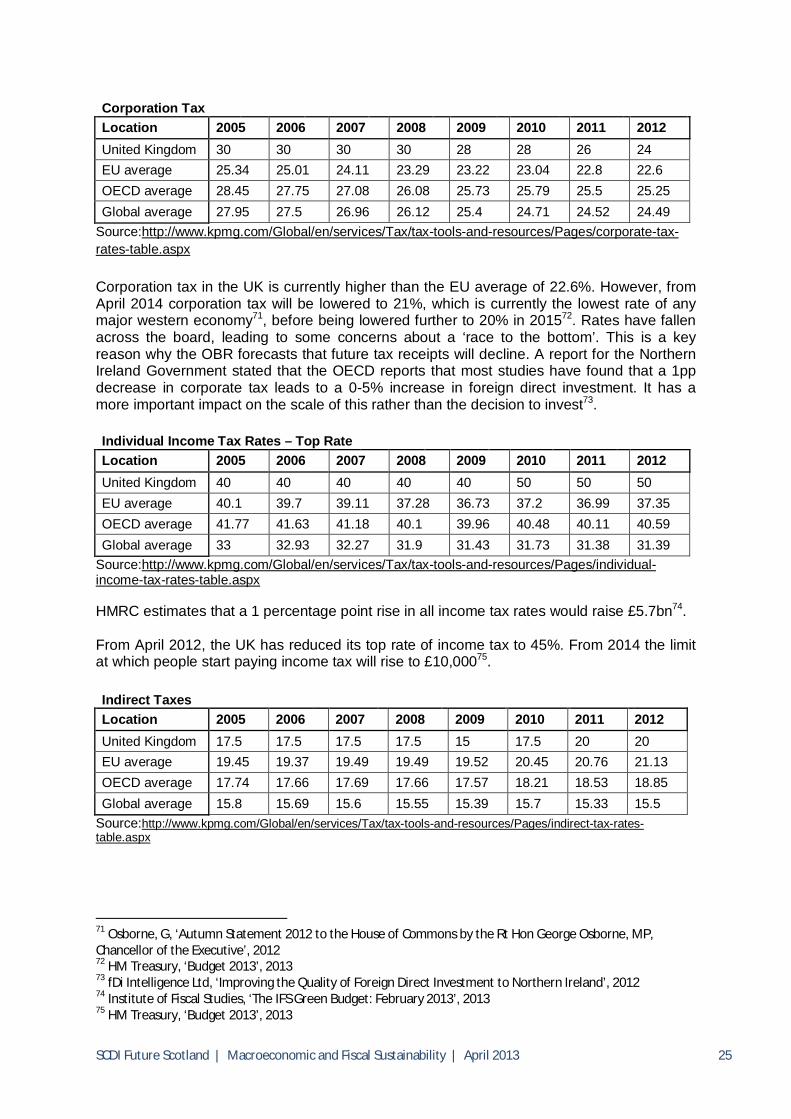

Corporation Tax Location 2005 2006 2007 2008 2009 2010 2011 2012 United Kingdom 30 30 30 30 28 28 26 24 EU average 25.34 25.01 24.11 23.29 23.22 23.04 22.8 22.6 OECD average 28.45 27.75 27.08 26.08 25.73 25.79 25.5 25.25 Global average 27.95 27.5 26.96 26.12 25.4 24.71 24.52 24.49

Source:http://www.kpmg.com/Global/en/services/Tax/tax-tools-and-resources/Pages/corporate-tax-rates-table.aspx Corporation tax in the UK is currently higher than the EU average of 22.6%. However, from April 2014 corporation tax will be lowered to 21%, which is currently the lowest rate of any major western economy71, before being lowered further to 20% in 201572. Rates have fallen across the board, leading to some concerns about a ‘race to the bottom’. This is a key reason why the OBR forecasts that future tax receipts will decline. A report for the Northern Ireland Government stated that the OECD reports that most studies have found that a 1pp decrease in corporate tax leads to a 0-5% increase in foreign direct investment. It has a more important impact on the scale of this rather than the decision to invest73. Individual Income Tax Rates – Top Rate Location 2005 2006 2007 2008 2009 2010 2011 2012 United Kingdom 40 40 40 40 40 50 50 50 EU average 40.1 39.7 39.11 37.28 36.73 37.2 36.99 37.35 OECD average 41.77 41.63 41.18 40.1 39.96 40.48 40.11 40.59 Global average 33 32.93 32.27 31.9 31.43 31.73 31.38 31.39

Source:http://www.kpmg.com/Global/en/services/Tax/tax-tools-and-resources/Pages/individual-income-tax-rates-table.aspx HMRC estimates that a 1 percentage point rise in all income tax rates would raise £5.7bn74. From April 2012, the UK has reduced its top rate of income tax to 45%. From 2014 the limit at which people start paying income tax will rise to £10,00075. Indirect Taxes Location 2005 2006 2007 2008 2009 2010 2011 2012 United Kingdom 17.5 17.5 17.5 17.5 15 17.5 20 20 EU average 19.45 19.37 19.49 19.49 19.52 20.45 20.76 21.13 OECD average 17.74 17.66 17.69 17.66 17.57 18.21 18.53 18.85 Global average 15.8 15.69 15.6 15.55 15.39 15.7 15.33 15.5

Source:http://www.kpmg.com/Global/en/services/Tax/tax-tools-and-resources/Pages/indirect-tax-rates-table.aspx

71 Osborne, G, ‘Autumn Statement 2012 to the House of Commons by the Rt Hon George Osborne, MP, Chancellor of the Executive’, 2012 72 HM Treasury, ‘Budget 2013’, 2013 73 fDi Intelligence Ltd, ‘Improving the Quality of Foreign Direct Investment to Northern Ireland’, 2012 74 Institute of Fiscal Studies, ‘The IFS Green Budget: February 2013’, 2013 75 HM Treasury, ‘Budget 2013’, 2013

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 26

Institute of Fiscal Studies ‘Mirrlees Review’ of UK Tax System (2012) The Institute of Fiscal Studies’ Mirrlees Review brought together, under Professor Sir James Mirlees, a group of international experts, to identify the characteristics of a good tax system for any open developed economy in the 21st century, to assess the extent to which the UK tax system conforms to these ideals, and to recommend how it might realistically be reformed in that direction. Its main recommendations were:

1. Abolish stamp duty and base council tax on up to date values. 2. Simplify the benefit system and increase incentives to work. 3. Improve work incentives for those around the pension age – To increase total

employment by over 200,000 and total earnings by nearly £3bn. 4. Integrate income tax and National Insurance. 5. Impose equivalent to VAT on financial services. Extend VAT. 6. Extend Emissions Trading Scheme and consistently tax emission sources. 7. Work toward a comprehensive system of congestion charging, replacing most of fuel

duty - Protect £38bn of national income from fuel duty as fuel efficiency increases and electric cars become more common and reduce revenues, while more effectively addressing the economic, social and environmental costs of carbon emissions, congestion, noise, accidents.

8. Radically overhaul taxation of savings to improve incentives to savings. 9. Increase attractiveness of equity finance in the corporate tax system - Increase

national income by as much as 1.4% or more than £20bn. The Scottish Government’s Fiscal Commission has agreed that the Review would provide “a helpful starting point” for its consideration of the principles for the design of an effective tax system for an independent Scotland76. Reserved Taxes Clearly, many other proposals are advocated to reduce or increase specific taxes or to create or abolish taxes. A financial transactions tax of 0.1% on bonds and shares and 0.01% on derivatives is to be introduced by 11 EU member states, excluding the UK77. Its claimed benefits include raising €30-35bn per year while at the same time discouraging speculative trading and reducing volatility. Its claimed disbenefits include increasing cost of capital, therefore, reducing the flow of profitable projects, decrease levels of real production, expansion, capital investment and employment78. The so-called Mansion and Bankers’ Bonuses taxes are prominent politically. The Scotch whisky industry is among those to propose equalising excise duty across all alcoholic drinks. It is calculated that this would increase revenue by around £1bn79. Devolved Taxes The Scottish Parliament’s tax revenues-raising powers are relatively limited. It presently has responsibility for two main taxes, council tax and non-domestic rates, as well as the ability, as yet unexercised, to vary the rate of income tax by 3p in the pound. From 2015, the UK rate will be reduced by 10 percentage points for taxpayers in Scotland and the Scottish Parliament will have to determine a Scottish Rate of Income Tax through its own budget. A basket of smaller taxes will also be devolved at the same time. 76 Barnes, E., ‘Scottish Independence: SNP’s Radical Tax Plan’, Scotland on Sunday, 31 March 2013 77 Šemeta, A., ‘The Robin Hood tax takes a step closer’, The Guardian, 21 February 2013 78 Pomeranets, A., ‘Financial Transaction Taxes: International Experiences, Issues and Feasibility’, Bank of Canada Review, Autumn 2012 79 Scotch Whisky Association, ‘Budget Submission 2011’, 2011

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 27

The council tax has been frozen in Scotland since 2007. This has resulted in an income shortfall of around £490m80. Council tax bands are based on the estimated market value of each house on 1 April 1991, and no revaluation exercises have taken place since. This means current tax bills do not account for subsequent price changes. Council tax is a regressive tax. Properties are more heavily concentrated in the tax bands, and the charges rise more slowly than values, meaning that the more a house is worth the less as a proportion of the value is paid as council tax81. Non-domestic rates are projected to generate £2.66bn in 2014-15, with growth of 7.2% and 9.4% over two years. Revenues would have risen by 38% between 2007-08 and 2014-15. This is primarily based on assumptions of higher economic growth generating higher receipts. There has been no economic modelling of the impact of these increases in revenues on businesses. The Scottish poundage rate will be matched with England’s at least until 2014-15. The Scottish Government provides reliefs valued on average at more than £500m, notably the Small Business Bonus. There has been no economic modelling of the impact of these on economic growth82.

80 Black, R.W., ‘Unlocking the Potential in Scotland’s Public Services; From Good to Great by 2020’, The David Hume Institute, N.96, 2012 81 Institute of Fiscal Studies, ‘The IFS Green Budget: February 2013’, 2013 82 STUC, ‘The economic and employment benefits of the Small Business Bonus Scheme’, 2012

SCDI Future Scotland | Macroeconomic and Fiscal Sustainability | April 2013 28

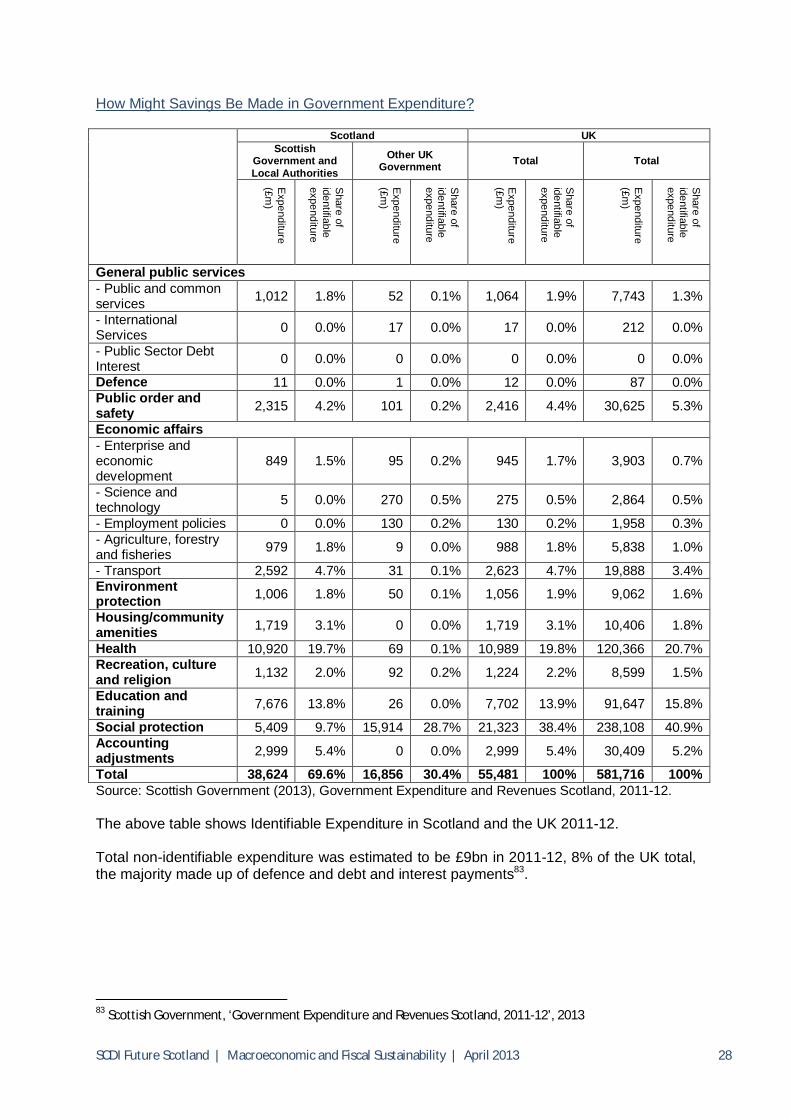

How Might Savings Be Made in Government Expenditure? Scotland UK

Scottish Government and Local Authorities

Other UK Government Total Total

Expenditure

(£m)

Share of

identifiable expenditure

Expenditure

(£m)

Share of

identifiable expenditure

Expenditure

(£m)

Share of

identifiable expenditure

Expenditure

(£m)

Share of

identifiable expenditure