Scaling Solar Solar Power financing for private sector ... · Solar Power financing for private...

52

Scaling Solar – Solar Power financing for private sector projects in Emerging Market Karsten Fuelster Country Manager for Germany Austria and Switzerland Hamburg 25-26 April, 2017

Transcript of Scaling Solar Solar Power financing for private sector ... · Solar Power financing for private...

Scaling Solar –

Solar Power financing for private

sector projects in Emerging Market

Karsten Fuelster

Country Manager for Germany

Austria and SwitzerlandHamburg

25-26 April, 2017

2

•2

3

What Is Scaling Solar?

Scaling Solar is a “one-stop-shop” solution for governments to procure grid-tied solar PV rapidly, competitively and with lower transaction costs

First implementation in Zambia was “proof of concept”

Bringing global solar trends to SSA countries (lower tariffs driven by competition)

Scaling Solar: a suite of WBG services/instruments under a single umbrella

Competitive, transparent procurement

WB sector engagement

Standardized, balanced contracts

Competitive financing and risk mitigation instruments (WB Guarantee and PRI)

“Packaged” approach

The challenge:

Large, unmet demand for electricity in SSA

Market scale and high perceived risk

Procurement (delays & uncertainty)

Lack of competition and high transaction costs

The opportunity:

Good solar energy endowment in SSA

Solar PV is quick to build and cost-competitive

Private investors’ interest

A Market Failure – creating an Opportunity A WBG Solution: Scaling Solar

4•6•4

●

●

●

●

●

●

●

●

5

How Does It Work in Practice?

Project Preparation

Tender Process & Award

Construction

& OperationBid Preparation

1 2 3

Financial Close

4 5

• Technical and economic analysis for optimal size and location of PV plants

• Site investigation

• Legal & regulatory analysis

• Standard tender documents

• Standard project documents

• Attachment of stapled financing, insurance and credit enhancement

• Request for qualification

• Bidder consultation

• Request for proposals

• Proposal review and award

• Signing of project documents

• Finalization of equipment,construction and operation contracts

• Final project approvals

• Finalization of loan agreements, insurance and risk management

• Construction

• Commissioning

• Operation

6 to 12 months 6 months 6 months

• Several WBG instruments brought together under a single product offering

• Client governments would engage in a single mandate to access the “one-stop-shop”

6•7•6

7•7

8•12•8

9•9

10

What Have We Achieved So Far?

• Broad market recognition in Africa: 1,000 MW+ under development, 5 mandates in 4 countries (Zambia x 2, Senegal, Ethiopia, Madagascar) and active discussions in many more

• First implementation in Zambia validated concept: lowest tariff in Africa to date, faster than anywhere else on the continent

• Strong momentum to roll out outside of Sub Saharan Africa (e.g. Tunisia, Afghanistan, Cambodia…etc.)

Ethiopia

Kenya

Mandated

In Active Discussion

Zambia

(Up to 600MW)*

Senegal

(Up to 200MW)Nigeria

The Sahel Region

“These are the lowest solar power

tariffs seen to date in Africa, and

among the lowest prices for solar

anywhere in the world – a game

changer for Zambia and other

countries in the region facing

electricity shortages”

- PV Magazine, Jun 15, 2016

“[The Scaling Solar Program] reduces risk to

investors with a suite of guarantees…the IFC

offers low-priced loans; the World Bank

guarantees that governments will buy the power

generated by the projects; and the group's

Multilateral Investment Guarantee Agency offers

political insurance in case of a war or civil

unrest.”

- Scientific American, Nov 2, 2016

Madagascar

(30 – 40MW)

Ethiopia

(Up to 500MW)

“The drive to create new markets will

also require new guarantee instruments

and a sharp focus on programmes that

can be scaled for maximum impact. The

World Bank Group’s Scaling Solar is one

example.”

- World Economic Forum, Jan 11, 2017

“Senegal follows Zambia in

joining WBG's Scaling Solar

program”

“The effort will bring a

needed injection of

electricity to Senegal, where

just over half the population

has access to electricity”

- Bloomberg, Feb 10, 2016

* Including Zambia Round 1 of up to 100MW and Zambia Round 2 of up to 500MW, with first phase of up to 200MW

Kenya

Tanzania

11

Scaling Solar Tender Results in Zambia

6.0c/kWh non-indexed is equivalent to an average in current dollars over contract life of 4.7c/kWh

Neoen Site Enel Site

Neoen / First Solar 6.0150 6.1350

ENEL Green Power 7.7989 7.8390

Access / EREN Zambia 1 8.2879 8.9509

MULILO Zambia PV1 Consortium 8.4000 8.4000

EDF Energies Nouvelles 10.0400 9.9850

SEP / AVIC Intl 10.6000 10.6000

Projects were developed and tender was prepared and executed to conclusion in 9 months

12

Scaling Solar in Zambia

Quality sponsors, competitive tariff and speed of implementation

• Round 1: 76MW from two winning bids

• Round 2: up to 500MW (planned) with the 1st Phase of 200MW just launched

• WBG value-added:

• IFC Advisory

• WB guarantees and sector engagement

• IFC Financing: IFC A loan + IFC-Canada Climate Change Program financing

• IFC mandated lead arranger for balance financing

Round 1 Location Round 1 Highlights

Winning Sponsors(selected out of 48 bidders)

Neoen + First Solar

Enel Green Power

Tariff US¢6.0/kWh US¢7.8/kWh

Size 48MW 28MW

Time to Market

• Launch of prequalification – Oct. ‘15• Bid submission and selection – May ‘16• PPA signing – Nov. ‘16• Financial close (expected) – Apr. ’17• Commercial operation (expected) –

Dec. ‘17

13

Name Title Phone Numbers Email

Karsten Fuelster Principal Investment

Officer

+49 69 74348250

+49 170 90 22 605

THANK YOU!

FOR FURTHER INFORMATION CONTACT:

Webpage: www.scalingsolar.org

IFC’S ACTIVITIES IN THE

POWER SECTOR

Table of contents

IFC in the Power Sector – Overview

IFC’s Track Record in the Power Sector – Regions and Projects

IFC’s Track Record in the Power Sector – Power Sub-Sectors

IFC’s Value-Add in Power Transactions

16

25

31

38

16

IFC in the Power Sector

Overview

16

17

IFC Power SectorIFC is a Leading Investor in the Emerging Markets Power Sector

• IFC’s FY2016 Power gross commitments amounted to US$2.0 bn (9% CAGR since 2012)

• IFC’s FY2016 Renewable Energy* gross commitments amounted to US$1.0 bn (53% of IFC Power)

IFC Invests in:

• Generation – 40,000+ MWs to date

• Transmission – 13 investments to date, including financing of greenfield private transmission assets

• Distribution – 36 investments to date, reaching > 160 million customers

• Early stage start ups in the renewable energy space

• Financial intermediaries (banks, PE funds) who reach smaller assets/companies

• Platforms, HoldCos and sub-sovereign entities with regional or global footprint

Note: All Renewable Energy Generation and Energy Efficiency projects are accounted for

17

18

East Asia & the Pacific

1%

Sub-Saharan Africa35%

Europe & Central Asia

25%

South Asia15%

Middle East & North Africa

24%

FY2016 Power HighlightsIFC Gross Commitments of US$2.0 Billion

Solar Generation

9%

Wind Generation

13%

Hydro Generation

9%

Thermal Generation

57%

Other (Holding Companies, Distribution)

12%

Note: IFC year-end is June 30th

FY2016 Commitment Activity: US$2.0 billion invested, including US$850 million for IFC’s own account and

US$1.1 billion of mobilization

FY2016 Power Commitment Activity by Region

(incl. mobilization)

FY2016 Power Commitment Activity by Sector

(incl. mobilization)

18

19

Latin America & the Caribbean

21%

East Asia & the Pacific

8%

Sub-Saharan Africa15%

Europe & Central Asia

20%

South Asia17%

Middle East & North Africa

19%

FY2016 Power HighlightsIFC Committed Balance of US$5.8 Billion

Solar Generation

12%

Wind Generation

15%

Hydro Generation

22%Biomass and Geothermal

3%

Thermal Generation27%

Distribution8%

RE via Funds/FIs/Hold Cos9%

Other (Holding Companies, Utilities, EE)4%

Note: IFC year-end is June 30th

Total Committed Balance by Region

IFC Power

Total Committed Balance by Sector

IFC Power

FY2016 Committed Portfolio: US$5.8 billion of committed debt and equity as of June 2016. Power

represents 43% of US$13.4 billion committed debt and equity in all Infrastructure

19

20

Far-reaching experience arranging and financing complex power projects worldwide

IFC’s Global Power Footprint

Select power projects recently financed by IPP across the globe*

Turkey EnerjiSA $990 mLender / Arranger,

2008, 2011

Georgia Shuakhevi $284 mLender / Arranger /

Investor, 2015

Iraq MGES Power $375 mLender / Arranger /

Investor, 2016

Turkey Akfen Energy $100 m Investor, 2016

Europe / Middle East

South

AfricaAbengoa CSP $413 m

Lender / Arranger

2012, 2015

Nigeria Azura $276 m Lender / Arranger, 2014

Senegal Cap des Biches $100 mInvestor /

Arranger, 2015

Africa

Region

Mainstream

Africa$23 m Investor, 2016

Africa

Asia

India Ostro Energy $180 mLender /

Arranger, 2016

PakistanChina Three

Gorges$125 m Investor, 2015

Bangladesh United Power $21 m Lender, 2016

*Amounts represent total financing committed and mobilized by IFC

Panama Penonome $300 mLender /

Arranger, 2014

Honduras SunEdison $147 mLender /

Arranger, 2014

Costa Rica Reventazon $100 m Lender, 2014

Mexico Aura Solar $75 mLender,

Arranger, 2014

Latin America

20

Global clients are half our business

• We have long-term partnerships with key clients

• We have been partnering with renewable energy companies

expanding into emerging markets

• We help clients access capital at project, holdco and corporate

levels and via capital markets

“Local” clients are becoming regional / global

• Local power companies invest in their own country

• Local power companies expand into other emerging markets

• Local industrials expand into the power sector

• Our local clients are becoming a larger share of our business as

market reform increases opportunities for private investment in

the power sector

We work with emerging renewable energy companies

• We have supported newly started local renewable energy firms,

as they begin to build their first projects

We work with sub-sovereign entities and governments to create

vehicles for private participation

21

IFC’s Clients in the Power SectorDiverse Clients Trust IFC as a Power Sector Partner

21

• Developing countries have a clear need to power economic growth and to improve the quality of life of their citizens (e.g. access

to lighting and communications)

• Need to diversify generating sources and where possible, deploy indigenous power rather than using foreign exchange to

import fuel

• Climate change and environmental concerns tied to use of coal, gas and oil fired power generation persist

• As capital costs decline, solar, wind and other forms of renewable energy present increasingly attractive opportunities for private

investors in emerging markets

IFC’s Case For RenewablesFueling Growth and Combating Climate Change

IFC’s Commitment Activity in Renewable Energy

3

22

The Asset

2016 Best Energy/Renewable Energy Deal of the Year – Gulpur - Pakistan

2016 Best Energy/Renewable Energy Deal of the Year – Tenaga Generasi - Pakistan

African Banker Awards

2016 Infrastructure Deal of the Year – Azura Edo IPP (nominee)

2013 Deal of the Year – Umeme - Uganda

Infrastructure Investor

2015 Middle East Deal of the Year – Jordan Seven Sister

Middle East Solar Industry Association Awards

2014 Commercial Advisor of the Year – 7 Solar PV Projects - Jordan

Project Finance International

2014 Global Multilateral of the Year

2013 Latin America Power Deal of the Year – Alto Maipo - Chile

2013 Latin America Solar Deal of the Year – San Andres – Chile

Infrastructure Journal

2015 Asia Pacific Hydropower Award – Gulpur - Pakistan

2014 IJGlobal Middle Eastern Renewables Award

23

IFC’s Track Record in the Power SectorRecent Award Winning Recognition from the Market

•2323

24

From Patient Equity to

Long Term Debt Sector Expertise

Country Risk

Mitigation

Environmental &

Social Risk

Management

Advisory

Services

EQUITY

Up to 20% in project or

company

Start-up equity / co-

developer (IFC

InfraVentures)

SUB-DEBT

Terms tailored to meet

project needs

DEBT

Long Maturities Tailored

to Project Needs

Fixed/Floating Rates,

Local Currencies

Flexible Amortization

Profile

Syndication/Mobilization

from commercial banks

and DFIs

Deep sector

knowledge gained

from experience

In-house

Engineers:

In-house Market

Expertise

In-house

Regulatory

Expertise

Government

Relations

Neutral broker

Role

World Bank

Synergies

Partial Credit

Guarantees

(PCG)

MIGA

Coordinated

approach

across WBG

services

• MIGA PRI

• IDA PCG

Environmental and

Social Best

Practices

Equator Principles

Modeled after IFC

Standards

Governance

Private sector

perspective to

governments

Introductions +

matchmaking

Cross-border

support + Sector

knowledge

Access to Donor

Funding/Con-

cessionary

Support

Coordination/Car-

bon Finance

Programs to

assist client,

including: Local

Supplier

Development,

Corporate

Governance,

Community

Development

Funding

IFC’s Value-Add in Power Transactions

24

25

IFC’s Track Record in the Power Sector

Regions and Projects

25

• 2015 First platform company investment with a Chinese SOE going outside its

market (CSAIL, Pakistan)

• 2012 First smart grid investment (Kalkitech, India)

• 2011 India's first private transmission company (Powerlinks)

• 2010

• First international commercial bank project financing for wind in China (CWP)

• Early stage equity solar investments in Thailand (SPC)

• 2009

• Pre-IPO equity investment in partially privatized vertically integrated

geothermal company, with subsequent corporate loans in the Philippines

(PNOC-EDC)

• First grid tied solar PV investment in India (Azure)

• 2007 First IPPs in country (Magat Hydro - Philippines)

• 2006 First private small hydro in China (Zhongda)

• 2005 First merchant/quasi-merchant hydros in India (Allain Duhangan)

• Local currency: First power project in local currency by a multilateral in China

(Guangzhou Development Industry Holdings, 2005)

26

IFC’s Track Record in the Power SectorPioneer Investments in Asia

26

27

Ostro Energy (India): Renewable platform company promoted by Actis, which is building two

wind farms with an aggregate capacity of up to 197.4 MW, in the state of Andhra Pradesh

India. Actis is well-known to IFC. Together they have 8 co-investments globally across sectors

with a strong pipeline of projects.

Azure Karnataka (India): Three greenfield solar power plants of respectively 40 MW, 50MW &

40MW in Karnataka, India under a 25-year PPA. This project is part of a government of

Karnataka solar program with a target of installing 2,000 MW of private sector solar projects by

2021. IFC has an existing relationship with Azure through equity and debt investments.

FRV Solar (Jordan): 50MW solar PV power plant developed by Fotowatio Renewable

Ventures B.V. The project is amongst the four that have been awarded under Round II of the

solar energy EOI process that was initiated by the government of Jordan. It follows last year’s

successful investments by IFC in 7 projects in the country (‘Jordan Seven Sisters’), which

represented 90 MW of the 200 MW capacity awarded under Round I.

Jordan

IFC: US$ 21.2 mn

Mobilized: US$ 25.6 mn

Feb 2016

India

IFC: US$32 mn

Mobilized: US$82 mn

Dec 2015

India

IFC: INR 4.0 bn

Mobilized: INR 12.0 bn

May 2016

IFC’s Track Record in the Power SectorRecent RE Investments in Asia

27

• 2015

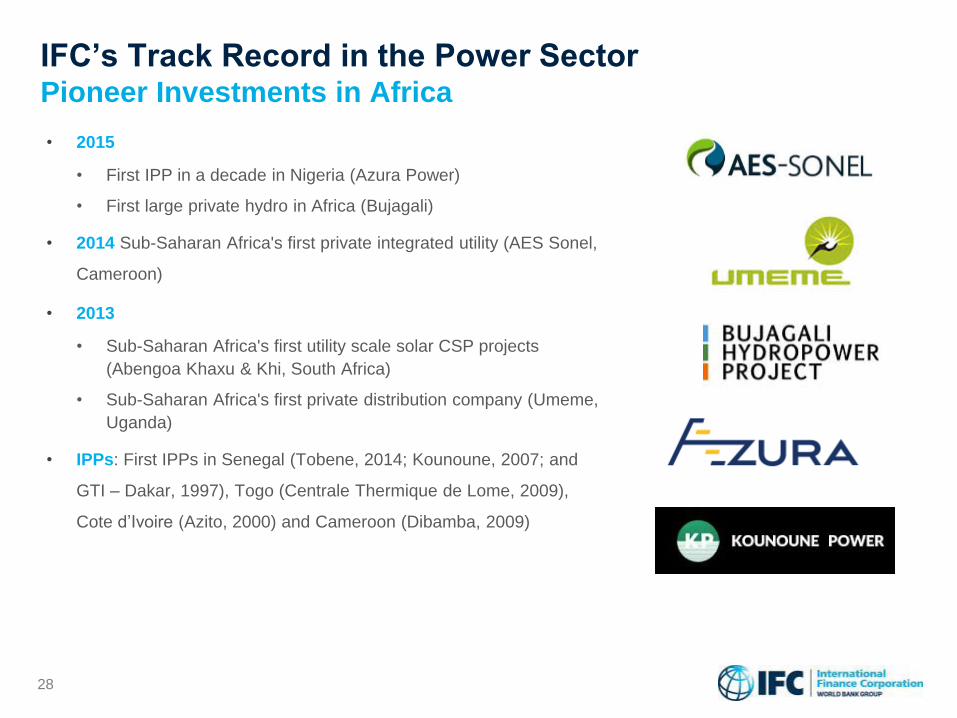

• First IPP in a decade in Nigeria (Azura Power)

• First large private hydro in Africa (Bujagali)

• 2014 Sub-Saharan Africa's first private integrated utility (AES Sonel,

Cameroon)

• 2013

• Sub-Saharan Africa's first utility scale solar CSP projects

(Abengoa Khaxu & Khi, South Africa)

• Sub-Saharan Africa's first private distribution company (Umeme,

Uganda)

• IPPs: First IPPs in Senegal (Tobene, 2014; Kounoune, 2007; and

GTI – Dakar, 1997), Togo (Centrale Thermique de Lome, 2009),

Cote d’Ivoire (Azito, 2000) and Cameroon (Dibamba, 2009)

28

IFC’s Track Record in the Power SectorPioneer Investments in Africa

28

• 2016 First equity investment in a CCGT asset in Iraq (Unit Investment)

• 2015

• First equity investment in Turkish power sector (Gama Enerji)

• First privately financed grid connected solar PV projects in MENA, innovative

structuring approach to simultaneously close seven separate deals (Seven Sisters

program, Jordan)

• 2013 First private distribution company in Pakistan (Karachi Electric)

• 2012 First internationally financed wind IPP in Pakistan (Zorlu)

• 2011

• First transborder power export project from Georgia to Turkey (Paravani)

• First wind project financed under a market based support mechanism (EDPR

Romania)

• 2009

• First wind farm project financings in Bulgaria (AES)

• First international commercial bank project financing for wind in Turkey (Rotor

Elektrik)

• First hydro IPP in Pakistan (84MW Laraib)

• First electricity disco privatization in Jordan (EDCO)

• 2008 First merchant plant financing in Turkey (Enerjisa)

29

IFC’s Track Record in the Power SectorPioneer Investments in EMENA

29

• 2015

• The largest wind farm in Central America (Penonome, Panama)

• First private wind farm in Jamaica (BMR Wind)

• Largest solar PV plant in Latin America and largest merchant solar PV plant in the world (Luz del Norte in

Chile)

• 2013

• First utility scale solar PV project in Mexico (Aura Solar)

• First IPO of a Brazilian private power company (CPFL)

• 2011

• Landmark geothermal project financings in Nicaragua (San Jacinto)

• First wind farm project financings in Mexico (Eurus and La Mata-La Ventosa)

• Merchant HPP: First merchant/quasi-merchant hydros in Chile (2007 Hidromaule and 2005 La Higuera)

• IPPs: First IPP in Mexico (Merida III, 1998)

• Transmission: Lender to first privatizations in Peru (ISA, 2002), Bolivia (TDE, 2002) and Chile (Transelec, 2003)

• Local currency: First power project financing in local currency by a multilateral in the region (Brazil)

30

IFC’s Track Record in the Power SectorPioneer Investments in Latin America

30

31

IFC’s Track Record in the Power Sector

Power Sub-Sectors

31

32

IFC Experience:

105 investments with a total capacity of 23,000 MW. Latest projects include:

Nigeria

Azura Edo IPP 450 MW

OCGT plant

US$80 mn debt

US$178 mn mob.

2015

Bangladesh

Bibiyana II 341MW

CCGT plant

US$75 mn debt

2015

Iraq

MGES Power 500MW

CCGT plant

US$250 mn

debt&equity

US$125 mn mob.

2016

Senegal

Tobene 96 MW

HFO fired

US$38 mn debt

US$87 mn mob.

2015

Senegal

Cap des Biches 53MW

HFO fired

US$9 mn equity

US$91 mn mob.

2016

IFC Power Sub-SectorsMajor Investor in fossil-fuel based Thermal Generation

* as of July 2016.

IFC Approach:

• Increased focus on natural

gas

• Climate friendly measures,

e.x. energy efficiency, gas

flaring reduction

• Diesel and heavy fuel oil

where limited alternatives

exist

32

33

Vietnam

GEC 78MW

Run-of-river

US$10 mn equity

2016

South Africa

Gulpur 102MW

Run-of-river

US$50 mn debt

US$72 mn mob.

2015

Armenia

Vorotan 402MW

Reservoir

US$13 mn

debt&equity

2015

Pakistan

CSAIL 2GW

US$125 mn equity

2014

Turkey

Karaca 78MW

Reservoir

US$44 mn debt

2016

IFC Power Sub-SectorsExtensive Track Record in Hydro Power Generation

* as of July 2016.

IFC Approach:

• Increased focus on natural

gas

• Climate friendly measures,

e.x. energy efficiency, gas

flaring reduction

• Diesel and heavy fuel oil

where limited alternatives

exist

IFC Experience:

87 investments with a total capacity* of 7,100 MW. Latest projects include:

33

34

Panama

Penonome 215MW

US$99 mn debt

US$204 mn mob.

2014

India

Green Infra 242MW

US$55 mn debt

US$110 mn mob.

2015

Pakistan

Gul Ahmed 50MW

US$15 mn

debt&equity

US$36 mn mob.

2015

* as of July 2016.

IFC Power Sub-SectorsLeading Investor in Wind Power in Emerging Markets

India

Ostro Energy 198MW

US$30 mn debt

US$120 mn mob.

2016

Brazil

Enel Wind 342MW

US$200 mn debt

US$300 mn mob.

2014

IFC Experience:

50 investments with a total capacity* of 3,600 MW. Latest projects include:

IFC Approach:

• Products that optimize

leverage, e.g. deferrable

subordinated debt that take

more wind risk layered on

top of senior debt

• Can mobilize concessional

financing where appropriate

• We understand new

regulatory support

mechanisms bundling of

small hydros

34

IFC Power Sub-SectorsIncreasing Focus on Solar Power Generation

35

South Africa

Abengoa Xina 100 MW

CSP

US$43 mn debt

2014

India

Acme Solar NSM 100MW

Solar PV

US$33 mn debt

US$65 mn mob.

2014

India

Azure Karnataka 130MW

Solar PV

US$30 mn debt

US$70 mn mob.

2015

Honduras

SunEdison HON3 82MW

Solar PV

US$46 mn debt

US$81 mn mob.

2014

Jordan

Seven Sisters 90MW

Solar PV

US$80 mn debt

US$116 mn mob.

2014* as of July 2016.

IFC Experience:

77 investments with a total capacity* of 1,600 MW. Latest projects include:

IFC Approach:

• Utility-scale plants

• Best-in-class start up

developers

• Developing relationships

with suppliers

• Can mobilize concessional

financing where appropriate

• We understand new

regulatory support

mechanisms and regulatory

support risk

35

36

Philippines

EDC

US$83 mn debt

2009

Nicaragua

San Jacinto 36MW

US$50 mn debt

US$140 mn mob.

2011

Philippines

Energy Dev II 5MW

US$75 mn debt

2011

* as of July 2016.

IFC Power Sub-SectorsExperience in Geothermal Power Generation

IFC Approach:

• Understand the sector-

specific challenges of

resource risk and long

project cycle

• Innovative structuring

allowing for stage

disbursement to full

resource completion

• Exploring ways to finance

resource development

• In-house technical expertise

• Mobilization of concessional

financing where appropriate

IFC Experience:

• Investments in Nicaragua and Philippines

• Corporate finance. Project finance of integrated (steam + plant) and

plant-only projects

• Experience with both equity and debt financing

36

37

Kenya

KPLC

US$50 mn debt

2013

Turkey

AkCez II

US$106 mn debt

US$58 mn mob.

2015

Brazil

Equatorial

US$99 mn equity

2013

* as of July 2016.

IFC Power Sub-SectorsExperience in Transmission and Distribution

IFC Approach:

• Financing capital

expenditure programs for

distribution companies,

including recently privatized

companies – e.g. Sedas

(Turkey), Umeme (Uganda),

CEZ (Albania), EVN

(Macedonia) and rural

electrification concessions –

e.g. Comasel (Senegal)

• Financing of greenfield

private transmission assets

– e.g. Powerlink (India) and

privatized transmission

assets (e.g. TDE, Bolivia)

IFC Experience:

36 distribution and 13 transmission investments*. Latest projects include:

37

38

IFC’s Value-Add in Power Transactions

38

IFC Approach:

• Bring the entire financing package to the

table through own account investment

and / or mobilization

• Equity Mobilization through the Asset

Management Company (part of the

WBG): US$ 8.7 billion AUM as of

September 2015

• Debt Mobilization through Managed

Colending Portfolio Program (MCPP) or

syndication

IFC Experience:

From 2010 to 2015, IFC mobilized over US$8.0 billion for power investments

from commercial lenders and DFIs

39

IFC’s Value-Add in Power TransactionsMobilization of Capital

Iraq

MGES Power

Mobilization

US$125 mn

2016

India

Ostro Energy

Mobilization

US$120 mn

2016

Senegal

Cap des Biches

Mobilization

US$91 mn

2016

Brazil

Enel

Mobilization

US$300 mn

2014

Mexico

Eurus

Mobilization

US$375 mn

2010

39

40

IFC’s Value-Add in Power TransactionsIFC InfraVentures as Project Co-Developer

IFC InfraVentures Approach:

• US$150 million fund to provide

development capital to infrastructure

projects, mainly in IDA (low-income)

countries (*)

• Up to US$8 million in cash and “sweat”

for projects in early stages of

development

• Act as co-developer for such projects,

adding value by:

• experienced staff working

alongside the sponsor, helping

structure the project and

increase bankability and equity

investors’ appetite

• giving access to the World

Bank’s global presence and

knowledge of local environments

(*) For a list of IDA countries, see http://www.worldbank.org/ida/borrowing-countries.html

Nepal

Upper Trishuli-1

216MW Hydro

US$500 mn

Project cost

2012

Kenya

Kipeto 100MW

Wind

US$320 mn

Project cost

2013

Georgia

CEI 400MW

Hydro

US$700 mn

Project cost

2011

Senegal

Tobene 96MW

HFO fired

US$165 mn

Project cost

2014

Nigeria

MBSO 120MW

Solar

US$240 mn

Project cost

2015

IFC Experience:

40

• In energy projects change in regulation is a

key risk (feed-in tariffs, tax credits, etc)

• IFC provides

• Assessment of stability and

predictability of a country’s regulatory

framework

• Support for increased competition and

fair market access

• Support in case of regulatory changes

• Experience in market reform efforts leads to

deep in-house power market expertise

• Teams work for governments and companies

from either side of the “Chinese wall”

• We leverage our relationship with the World

Bank (IBRD)

41

IFC’s Value-Add in Power TransactionsLocal Regulatory Frameworks and Market Reforms

Argentina

• At the request of the Secretariat of Energy, helped draft the PPA for the first

renewable power auction under the new Renewable Electricity Law in Argentina

• In coordination with the World Bank, helped prepare a USD 500 million PRG to

guarantee potential termination events for 1,000 MW of renewable energy

projects

• At the request of the Secretariat of Energy, helped review the FODER Trust

Joinder Agreement (payment scheme), RFP (bid documents) and the

compatibility of both documents with the PPA and PRG

• Targeting 2-3 renewable energy projects for USD 150 mm in IFC A-loans and

additional mobilization from bilateral banks and commercial banks to support

Argentina’s new renewable energy program

Mexico

• Actively participated providing comments and feedback to Mexico’s new

Electricity Law and its regulations

• Presented in several workshops best-practice on the workings of deregulated

markets to the Secretariat of Energy, Regulator, System Operator and Industrial

Groups

• Designed and structured the first wholesale and retail aggregator to

commercialize power and green certificates under Mexico’s new deregulated

power sector with the hope to help offload contractual commitments from the

State Owned Utility (CFE)

• Targeting investments in renewable power and CCGTs under hybrid contractual

and merchant schemes under the new deregulated scheme

IFC ExperienceIFC’s View on Regulatory Frameworks

41

Annex

42

IFC: A MEMBER OF THE WORLD BANK GROUP

Conciliation

and

arbitration of

investment

disputes

Guarantees

of foreign

direct

investment’s

non-

commercial

risks

Interest-free

loans and

grants to

governments

of poorest

countries

Loans to

middle-income

and credit-

worthy low-

income

country

governments

Solutions in

private sector

development

IBRDInternational

Bank for

Reconstruction

and

Development

IDAInternational

Development

Association

IFCInternational

Finance

Corporation

MIGAMultilateral

Investment

and Guarantee

Agency

ICSIDInternational

Centre for

Settlement of

Investment

Disputes

4343

Providing Development Solutions … Customized To Meet Client Needs

A member of the World Bank Group

Provides debt and equity investment, risk-

management, advice, resource mobilization

AAA credit rating; nearly 60-year history in

emerging markets

Present in 100 countries

IFC is the largest global development institution focused exclusively

on the private sector in developing countries.44

Loans

Equity

Trade Finance

Syndications

Blended

Finance

- Project and Corporate Financing

- On-lending through intermediary institutions

- Direct equity investments (up to 20% of company’s equity)

- Private equity funds

- Guarantee of trade-related payment obligations of

approved financial institutions

- Capital mobilization to serve developmental needs

- Over 60 co-financiers: commercial banks, fund, and DFIs

- Concessional funds are blended with IFC’s own resources

to finance initiatives & achieve impact that would

otherwise be unattainable

Derivatives &

Structured

Finance

- Interest rate, Currency, or Commodity-price hedges

provided to clients

- Credit guarantees and Structuring Advice

45

FY 2016:

US$8.1 billion

committed

FY 2016:

US$2.6 billion

committed

FY 2016: Average

outstanding balance

of US$2.8 billion

FY 2016: US$7.7

billion syndicated

FY 2016: US$117

million committed

Providing Development Solutions … Broad Product Range in Investment Services

45

46

Latin America & the Caribbean

24%

East Asia & the Pacific21%

Europe & Central Asia19%

South Asia13%

Sub-Saharan Africa12%

Middle East & North Africa

9%

Other2%

FY2016 IFC HighlightsIFC Own Commitments of US$11.1 Billion

Financial Markets40%

Infrastructure16%

Agribusiness & Forestry

10%

Consumer & Social Services

9%

Oil, Gas & Mining8%

Manufacturing7%

Telecom. & Information5%

Funds5%

Note: IFC year-end is June 30th

FY2016 Commitment Activity: US$18.9 billion invested in 344 projects and 78 countries, including

US$11.1 billion for IFC’s own account and US$7.7 billion of mobilization

Current Trends: Equity investments are an increasing priority, from 5% of commitments in 2008 to 23% in FY2016

Increasing focus on Sub-Saharan Africa, increasing from 1% of commitments in 2008 to 12.6% in

FY2016

Focus on large transformational engagements

FY2016 Commitment Activity by RegionFY2016 Commitment Activity by Sector

46

47

IFC – Infrastructure & Natural Resources

Overview

47

Power Utilities Transport

Infrastructure

Transport

Services

Natural

Resources

• Generation,

thermal and

renewable

• Transmission

• Distribution

• Integrated

Utilities

• Water, Waste

• Privatized

Public

Services

• Airports

• Ports

• Roads

• Railroads

• Logistics

• Shipping

• Airlines

• Rolling Stock

• Oil & Gas

• Gas

Distribution

• Mining

• Pipelines

• LNG

Local presence in key markets

Extended team covering both global giants and local leaders

48

Infrastructure & Natural ResourcesInvesting Across Sectors and Regions

48

49

Latin America & the Caribbean

12%

East Asia & the Pacific28%

Sub-Saharan Africa18%

Europe & Central Asia

18%

South Asia6%

Middle East & North Africa

15%

World3%

FY2016 Infra HighlightsIFC Own Commitments of US$2.6 Billion

Electric Power32%

Transportation23%

Oil, Gas & Mining31%

Utilities9%

Other5%

Note:

- IFC year-end is June 30th

- The charts represent IFC Own Account Commitment Activity

FY2016 Commitment Activity: US$6.5 billion invested, including US$2.6 billion for IFC’s own account and

US$3.9 billion of mobilization

FY2016 Committed Portfolio: US$13.3 billion

FY2016 Commitment Activity by Region

(Own Account)

FY2016 Commitment Activity by Sector

(Own Account)

49

50

List of IFC InvestmentsWind Power Generation

* As of July 2016.

Project Subsector Region CountryIFC Investment

($ million)

Power Share

($ million)

Mobilization

amount

($ million)

Total Power

Share and

Mobilization

($ million)

Infrastructure

Project CountMW IDA

Debt, Equity

or Both

InfraV-Kipeto Wind Sub-Saharan Africa Kenya 1.9 0.0 0.0 0.0 0.0 0.0 0.0 Debt

Ostro Andhra Wind South Asia India 29.5 29.5 120.0 149.5 1.0 96.6 0.0 Debt

Metro Power - B Wind Middle East and North Africa Pakistan 0.0 0.0 22.5 22.5 1.0 50.0 1.0 Debt

Ostro AP Wind Wind South Asia India 30.8 30.8 0.0 30.8 1.0 100.9 0.0 Debt

FY16 Subtotal 62.1 60.2 142.5 202.7 3.0 247.5 1.0

Rudine WPP Wind Europe and Central Asia Croatia 24.9 24.9 31.1 56.0 1.0 34.2 – Debt

BMR Wind Wind Latin America and the Caribbean Jamaica 10.0 10.0 – 10.0 1.0 34.0 – Debt

Gul Ahmed Wind Wind Middle East and North Africa Pakistan 14.9 14.9 36.4 51.2 1.0 50.0 1.0 Both

Green Infra Wind Wind South Asia India 55.2 55.2 110.0 165.2 1.0 242.4 – Debt

Enel Wind Brazil Wind Latin America and the Caribbean Brazil – – 108.5 108.5 – – – Debt

DJ Energy Wind South Asia India – – 55.3 55.3 – 106.3 – Debt

Uttar Urja Wind Wind South Asia India – – 44.5 44.5 – 85.5 – Debt

Dawood TGL Wind Middle East and North Africa Pakistan 29.5 29.5 44.0 73.5 1.0 49.5 1.0 Both

Penonome Wind Wind Latin America and the Caribbean Panama 99.0 99.0 - 99.0 1.0 215.0 – Debt

FY15 Subtotal 233.5 233.5 429.8 663.2 6.0 816.8 2.0

Tafila Rate Swap Wind Middle East and North Africa Jordan 2.7 2.7 – 2.7 1.0 – – Debt

Tafila Wind Wind Middle East and North Africa Jordan 69.1 69.1 151.7 220.8 1.0 117.0 – Debt

Metro Power Wind Middle East and North Africa Pakistan 25.8 25.8 – 25.8 1.0 50.0 1.0 Both

InfraV-Indo Wind Wind East Asia and Pacific Indonesia 2.0 2.0 – 2.0 1.0 – – Debt

InfraV-Ivicom Wind Europe and Central Asia Serbia 3.5 3.5 – 3.5 1.0 – – Debt

Enel Wind Brazil Wind Latin America and the Caribbean Brazil 200.0 200.0 100.0 300.0 1.0 342.3 – Debt

DJ Energy Wind South Asia India 27.5 27.5 – 27.5 1.0 85.0 1.0 Debt

Jath Power (NSL) Wind South Asia India 12.0 12.0 – 12.0 1.0 40.0 1.0 Debt

Uttar Urja Wind Wind South Asia India 22.2 22.2 – 22.2 1.0 85.0 1.0 Debt

FY14 Subtotal 364.8 364.8 251.7 616.5 9.0 719.3 4.0

Bhilwara Captive Wind South Asia India 7.5 7.5 – 7.5 1.0 20 1.0 Debt

Bhilwara R'ts 3 Wind South Asia India 1.0 1.0 – 1.0 1.0 – 1.0 Equity

InfraV-Lamuwind Wind Sub-Saharan Africa Kenya 3.0 3.0 – 3.0 1.0 – 1.0 Debt

InfraV-Singida Wind Sub-Saharan Africa Tanzania 4.0 4.0 – 4.0 1.0 – 1.0 Debt

Inox Rajasthan Wind South Asia India 50.0 50.0 – 50.0 1.0 100 1.0 Debt

NSL Wind Wind South Asia India 18.4 18.4 – 18.4 1.0 75 1.0 Debt

NSL Power Wind South Asia India 5.0 5.0 – 5.0 – – – Debt

Amakhala Wind Wind Sub-Saharan Africa South Africa 70.7 70.7 – 70.7 1.0 134 – Debt

Amakhala Swap Wind Sub-Saharan Africa South Africa 2.8 2.8 – 2.8 1.0 – – Debt

InfraV-Kipeto Wind Sub-Saharan Africa Kenya 2.0 2.0 – 2.0 1.0 – 1.0 Debt

Jelinak Wind Europe and Central Asia Croatia 20.1 20.1 30.4 50.5 1.0 30 – Debt

FY13 Subtotal 184.5 184.5 30.4 214.9 10.0 359.4 7.0

Bhilwara Wind Wind South Asia India 14.0 14.0 – 14.0 1.0 50 1.0 Debt

NSL Power Wind South Asia India 20.0 20.0 – 20.0 1.0 28 1.0 Equity

Pestera Power Wind Europe and Central Asia Romania 39.0 39.0 14.1 53.1 1.0 90 – Debt

Zorlu Pakistan Wind Middle East and North Africa Pakistan 38.1 38.1 – 38.1 1.0 56 1.0 Debt

Techno Wind Wind South Asia India 4.7 4.7 – 4.7 – – – Debt

InfraV-Renovatio Wind Europe and Central Asia Moldova 3.0 3.0 – 3.0 1.0 – 1.0 Debt

Sibenik WPP Wind Europe and Central Asia Croatia 24.8 24.8 43.4 68.2 1.0 44 – Debt

Cernavoda Power Wind Europe and Central Asia Romania – – 22.1 22.1 – – – Debt

FY12 Subtotal 143.6 143.6 79.6 223.2 6.0 267.3 4.0

Cernavoda Power Wind Europe and Central Asia Romania 60.8 60.8 – 60.8 1.0 138 – Debt

EDF La Ventosa Wind Latin America and the Caribbean Mexico 28.9 28.9 102.5 131.5 1.0 68 – Debt

Senok WindEnergy Wind South Asia Sri Lanka 1.9 1.9 – 1.9 1.0 10 1.0 Equity

Enerjisa-II 1 Wind Europe and Central Asia Turkey 27.6 27.6 165.6 193.2 0.2 119 – Debt

China WindPower Wind East Asia and Pacific China – – 95.0 95.0 – – – Debt

FY11 Subtotal 156.1 156.1 363.1 519.2 5.2 471.4 3.0

Grand Total 1,144.6 1,142.7 1,297.1 2,439.8 39.2 2,881.7 21.0

China WindPower Wind East Asia and Pacific China 55 55 – 55 1.0 201 – Debt

Eurus Wind Latin America and the Caribbean Mexico 71 42.6 – 42.6 0.5 250 – Debt

FY10 Subtotal 126.0 97.6 - 97.6 1.5 451.0 -

AES Kavarna Wind Europe and Central Asia Bulgaria 51.8 51.8 – 51.8 1.0 156 – Debt

Rotor Elektrik Wind Europe and Central Asia Turkey 71.51 71.51 – 71.51 1.0 135 – Debt

Norvind Wind Latin America and the Caribbean Chile 30.75 30.75 – 30.75 1.0 50 – Debt

FY09 Subtotal 154.1 154.1 - 154.1 3.0 341.0 -

Grand Total 1,424.6 1,394.3 1,297.1 2,691.5 43.7 3,673.7 21.0

48

51

List of IFC InvestmentsSolar Power Generation

Project Subsector Region CountryIFC Investment

($ million)

Power Share

($ million)

Mobilization

amount

($ million)

Total Power

Share and

Mobilization

($ million)

Infrastructure

Project CountMW IDA

Debt, Equity

or Both

InfraV-MBSO Solar Sub-Saharan Africa Nigeria 1.5 1.5 – 1.5 1.0 – 1.0 Debt

FRV Solar Jordan Solar Middle East and North Africa Jordan 21.2 21.2 20.6 41.8 1.0 50.0 – Debt

Azure_PV_40MW Solar South Asia India 9.2 9.2 – 9.2 1.0 40.0 – Debt

Azure_Raj_40MW Solar South Asia India 9.2 9.2 – 9.2 1.0 40.0 – Debt

Azure Sunrise Solar South Asia India 11.5 11.5 – 11.5 1.0 50.0 – Debt

FY16 Subtotal 52.5 52.5 20.6 73.1 5.0 180.0 1.0

CTIF OGE Solar Sub-Saharan Africa Tanzania 3.4 1.7 - 1.7 0.5 - 0.5 Debt

Luz del Norte Solar Latin America and the Caribbean Chile 60.0 60.0 – 60.0 1.0 141.0 – Debt

Adenium Jordan-1 Solar Middle East and North Africa Jordan 11.3 11.3 12.1 23.4 1.0 10.0 – Debt

Adenium Jordan 2 Solar Middle East and North Africa Jordan 11.3 11.3 12.1 23.4 1.0 10.0 – Debt

Adenium Jordan 3 Solar Middle East and North Africa Jordan 11.3 11.3 12.1 23.4 1.0 10.0 - Debt

Azure Clean Solar South Asia India 13.9 13.9 - 13.9 1.0 40.0 - Debt

Acme Solar NSM 1 Solar South Asia India 6.4 6.4 - 6.4 1.0 20.0 - Debt

Shamsuna PV Solar Middle East and North Africa Jordan 8.0 8.0 8.7 16.7 1.0 10.0 - Debt

Shamsuna Swap Solar Middle East and North Africa Jordan 0.2 0.2 - 0.2 1.0 - - Debt

Arabia One Solar Solar Middle East and North Africa Jordan 10.5 10.5 10.5 21.1 1.0 10.0 - Debt

Jordan Solar One Solar Middle East and North Africa Jordan 14.4 14.4 11.5 25.9 1.0 20.0 - Debt

Falcon PV Solar Middle East and North Africa Jordan 12.5 12.5 15.5 28.0 1.0 21.0 – Debt

Acme Solar NSM 2 Solar South Asia India 6.4 6.4 – 6.4 1.0 20.0 – Debt

Acme Solar NSM 3 Solar South Asia India 6.4 6.4 – 6.4 1.0 20.0 – Debt

Acme Solar NSM 4 Solar South Asia India 6.4 6.4 – 6.4 1.0 20.0 – Debt

Acme Solar NSM 6 Solar South Asia India 7.1 7.1 - 7.1 1.0 20.0 - Debt

CTIF OGE Solar Sub-Saharan Africa Tanzania 5.9 5.9 2.5 8.4 1.0 – 1.0 Debt

Azure CCPS-Rights2 Solar South Asia India 3.7 3.7 – 3.7 1.0 – – Debt

Azure Rights H Solar South Asia India 10.0 10.0 41.7 51.7 1.0 – – Debt

Abengoa CSP Xina Solar Sub-Saharan Africa South Africa 43.1 43.1 – 43.1 1.0 100.0 – Debt

AST Rights II Solar South Asia India 3.1 3.1 – 3.1 1.0 – – Debt

Adenium Holdco Solar Middle East and North Africa Jordan 12.0 12.0 – 12.0 1.0 – – Debt

Aura Solar II Solar Latin America and the Caribbean Honduras 25.7 25.7 64.3 90.0 1.0 61.0 1.0 Debt

Arabia One Swap Solar Middle East and North Africa Jordan 0.4 0.4 – 0.4 1.0 – 1.0 Debt

Valle Solar PV Solar Latin America and the Caribbean Honduras 30.0 30.0 60.5 90.5 1.0 70.0 1.0 Debt

Adenium 1 Swap Solar Middle East and North Africa Jordan 0.4 0.4 – 0.4 1.0 – 1.0 Debt

JSO Rate Swap Solar Middle East and North Africa Jordan 0.8 0.8 – 0.8 1.0 – 1.0 Debt

Adenium 2 Swap Solar Middle East and North Africa Jordan 0.4 0.4 – 0.4 1.0 – 1.0 Debt

Adenium 3 Swap Solar Middle East and North Africa Jordan 0.4 0.4 – 0.4 1.0 – 1.0 Debt

Falcon PV Swap Solar Middle East and North Africa Jordan 0.5 0.5 – 0.5 1.0 – 1.0 Debt

Gaia Equity Solar Middle East and North Africa MENA Region 25.0 25.0 – 25.0 1.0 – 1.0 Equity

SunEdison HON3 Solar Latin America and the Caribbean Honduras 45.7 45.7 – 45.7 1.0 80.8 1.0 Debt

SunEd HON3 Swap Solar Latin America and the Caribbean Honduras 1.2 1.2 - 1.2 1.0 - 1.0 Debt

FY15 Subtotal 397.9 396.3 251.5 647.7 32.5 683.8 12.5

Acme MP (25 MW) Solar South Asia India 12.0 12.0 - 12.0 1.0 25.0 1.0 Debt

ACWA Power OZZ Solar Middle East and North Africa Morocco 10.0 10.0 – 10.0 1.0 160.0 – Both

Sunergise Equity Solar East Asia and Pacific EAC Region 2.0 2.0 – 2.0 1.0 - – Equity

Azure CCD3 Solar East Asia and Pacific India 3.0 3.0 – 3.0 1.0 - 1.0 Equity

Korat 1 RI Solar East Asia and Pacific Thailand 0.2 0.2 - 0.2 1.0 - - Equity

Nakhon 1 RI Solar East Asia and Pacific Thailand 0.1 0.1 - 0.1 1.0 - - Equity

Sakon 1 RI Solar East Asia and Pacific Thailand 0.1 0.1 - 0.1 1.0 - - Equity

La Huayca II Solar Latin America and the Caribbean Chile 14.3 14.3 18.5 32.8 1.0 29.1 - Debt

SunEdison CAP Solar Latin America and the Caribbean Chile 65.0 65.0 - 65.0 1.0 100.0 - Debt

SunEdison MER Solar Latin America and the Caribbean Chile 37.5 37.5 - 37.5 1.0 50.7 - Debt

InfraV-SSOMali Solar Sub-Saharan Africa Mali 1.4 1.4 – 1.4 1.0 – 1.0 Equity

Chint/Sun Edison Solar South Asia Nepal 0.0 – 18.0 18.0 – – – Debt

SPC Korat 2 Solar East Asia and Pacific Thailand 0.6 0.6 – 0.6 – – – Debt

SPC Loei 1 Solar East Asia and Pacific Thailand 0.7 0.7 – 0.7 – – – Debt

FY14 Subtotal 146.9 146.9 36.5 183.4 11.0 364.8 3.0

49

52

List of IFC InvestmentsHydro Power Generation

50