Sayef presentation for ABAD seminar (7-Nov-2013)

17

HBFCL’s role on Development of Low Cost and Affordable Housing in Pakistan Syed Sayef Hussain Managing Director ABAD Seminar in Karachi on November 7, 2013

-

Upload

sayefhussain -

Category

Economy & Finance

-

view

92 -

download

0

Transcript of Sayef presentation for ABAD seminar (7-Nov-2013)

HBFCL’s role onDevelopment of Low Cost and Affordable

Housing in Pakistan

Syed Sayef HussainManaging Director

ABAD Seminar in Karachi on November 7, 2013

Vision & Mission Statements

VisionTo be the prime housing finance institution of the country,

providing affordable housing solutions to low and middle income groups of population by encouraging new constructions in small

and medium housing (SMH) sector.

2

Mission

To be a socially responsible and commercially sustainable housing finance institution.

Established in 1952 as a Public Sector Specialized Housing Finance

Institution to serve low and middle income segments of population

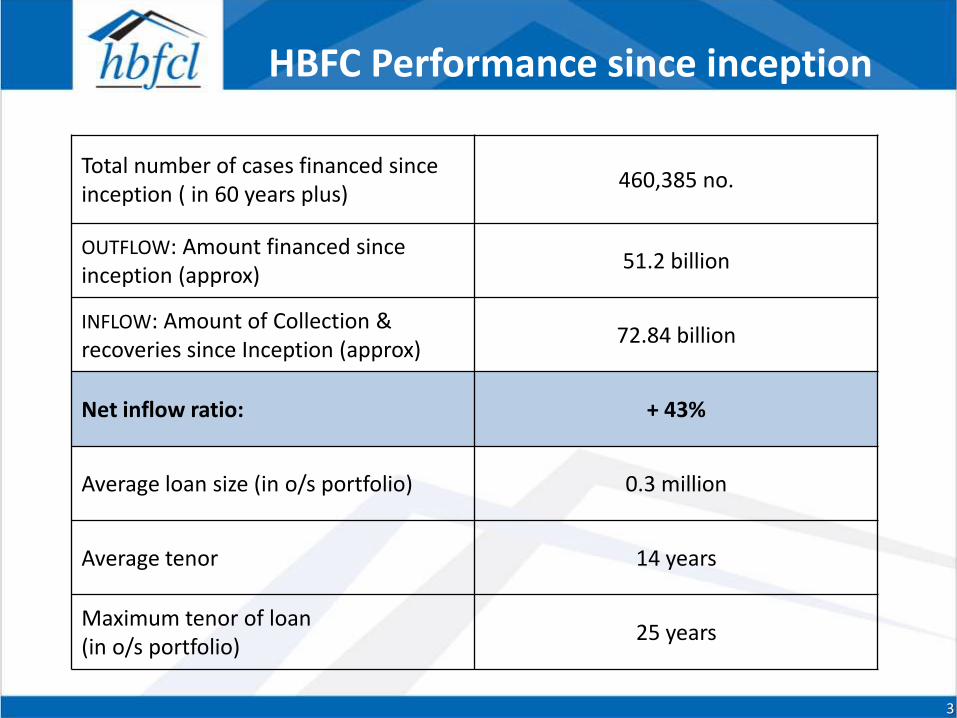

HBFC Performance since inception

Total number of cases financed since inception ( in 60 years plus)

460,385 no.

OUTFLOW: Amount financed since inception (approx)

51.2 billion

INFLOW: Amount of Collection & recoveries since Inception (approx)

72.84 billion

Net inflow ratio: + 43%

Average loan size (in o/s portfolio) 0.3 million

Average tenor 14 years

Maximum tenor of loan (in o/s portfolio)

25 years

3

Way forward

4

We will be again activating following services,

which were launched in 2005-2008 and later

abandoned

1. Tele-monitoring through call centre &SMS service

2. Online payment verification

3. Online application submission

4. Mortgage locator on website

5. Services for Non-resident Pakistanis

6. Service Rep Offices and Customer Felicitation

Centres

7. E-Home Service

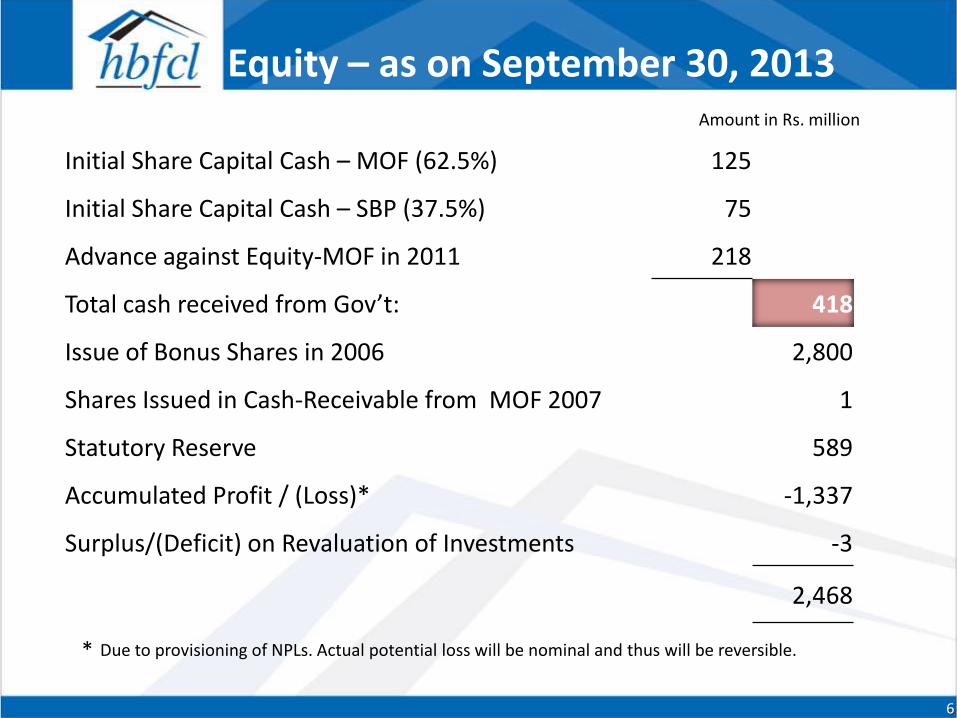

Equity – as on September 30, 2013

6

Amount in Rs. million

Initial Share Capital Cash – MOF (62.5%) 125

Initial Share Capital Cash – SBP (37.5%) 75

Advance against Equity-MOF in 2011 218

Total cash received from Gov’t: 418

Issue of Bonus Shares in 2006 2,800

Shares Issued in Cash-Receivable from MOF 2007 1

Statutory Reserve 589

Accumulated Profit / (Loss)* -1,337

Surplus/(Deficit) on Revaluation of Investments -3

2,468

* Due to provisioning of NPLs. Actual potential loss will be nominal and thus will be reversible.

SBP Credit Lines

(Amount in million)

Total SBP Credit Lines 16,496

Paid up to 2005 5,254

Outstanding SBP Credit Lines (No.58 to 64)

not paid from June 2006 onwards11,242

Mark-up Accrued @ 9.5 % per annum on SBP Credit Lines (Net off Profit & Loss sharing) –

as on Sep’13*

3,651

7

* Policy on SBP credit Lines was changed in … and is not according to original terms

Current loaning scheme

8

2004 2005 2006 2007 2008

2,546 2,187 2,254 3,359 3,859

Year to year disbursements since 2004:

2009 2010 2011 2012 2013

715 633 1,126 1,346 1,037*

(Amount in million)

* For 9 months up to Sept ‘13

NPLs ratio in current loaning scheme

9

2004 2005 2006 2007 2008

65% 52% 42% 40% 37%

Year to year NPL ratio since 2004:

2009 2010 2011 2012 2013

40% 50% 58% 60% 54%

(in %age)

10

We will again coming up with following products:

1) Ghar Izafa (Incremental Housing)

2) Ghar Asaish (House Furnishing)

3) Solar Panels Financing

4) Shops on Commercial Plots/Malls

5) Saving and Loan (Bachat Banay Ghar)

6) Co-branded credit card

7) Small Builders’ Finance

8) Builders’ Financing

9) Balance Transfer Facility

10)Ghar Pardesi (House for Non-resident Pakistanis)

11)Residential Hostels Finance

12)Loan for Land and Constructions

Way forward (new proposed schemes)

11

Way forward

12

Way forward

13

PM’s low cost housing scheme

• HBFCL expects that, under this scheme minimum affordable cost of a house would be Rs.1,500,000/-.

• HBFCL may take responsibility of providing 2,000 houses in designated cities.

• The total cost for this commitment would come to Rs.3 billion.

• HBFCL would like to have special credit line from the government to meet this commitment.

14

15

Issues and challenges

being faced by

HBFC

Pending issues faceing by HBFCL

• Uncertain future

• Presently no Board of Director, and no permanent

management for HBFCL

• Revision of terms of SBP credit Lines

• Restructuring of capital of HBFCL

• Meeting minimum capital requirements as set by SBP

• Prudential Regulations for SME Finance seemingly

too stringent SME house/construction finance

16

Long Term Liquidity Issue

• Pakistan Mortgage Refinance Company

• Mortgage backed Sukuks

• SBP Credit Lines

• Special Credit Lines for PM Housing Scheme

17

23