Saving for Retirement and Investing for Growth - … · 2017-02-05 · Saving for Retirement and...

15

Saving for Retirement and Investing for Growth Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’ Presentation of the Report, Brussels 18 September 2013 Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 1 S AVING FOR R ETIREMENT AND I NVESTING FOR G ROWTH Report of the CEPS ECMI Task Force on long-term investing and retirement savings LAUNCH OF THE REPORT BRUSSELS, 18 SEPTEMBER 2013 Download at www.eurocapitalmarkets.org/SFR or www.ceps.eu/book/SFR · Contact us at [email protected] Centre for European Policy Studies · European Capital Markets Institute · For the Report, Mirzha de Manuel Aramendía · All Rights Reserved Karel Lannoo CEO of CEPS, General Manager of ECMI Senior Rapporteur to the Task Force Welcome

Transcript of Saving for Retirement and Investing for Growth - … · 2017-02-05 · Saving for Retirement and...

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 1

SAVING FOR RETIREMENT AND

INVESTING FOR GROWTH Report of the CEPS ECMI Task Force on long-term investing and retirement savings

L A U N C H O F T H E R E P O R T

B R U S S E L S , 1 8 S E P T E M B E R 2 0 1 3

D o w n l o a d a t w w w . e u r o c a p i t a l m a r k e t s . o r g / S F R o r w w w . c e p s . e u / b o o k / S F R · C o n t a c t u s a t e c m i @ c e p s . e u

Centre fo r European Po l i c y S tud ies · European Cap i ta l Marke ts Ins t i tu te · For the Report , Mi rz ha de Manue l Aramendía · Al l R ights Reserved

Karel Lannoo CEO of CEPS, General Manager of ECMI

Senior Rapporteur to the Task Force

Welcome

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 2

1. Welcome remarks – Karel Lannoo, CEO of CEPS

2. Key recommendations – Allan Polack, Task Force Chairman

3. Presentation of the report – Mirzha de Manuel, CEPS ECMI

4. Expert comments and reactions

– Nadia Calviño, Deputy Director General, DG Markt

– Patrick Hoedjes, Director of Operations, EIOPA

– Paul Woolley, London School of Economics

5. Debate and questions

Agenda

In-house expertise

2003

.... an incipient

single market

2008

.... MiFID and

UCITS effects

2012

.... the future

after the crisis

2013

.... long-term

and pensions

A v a i l a b l e f o r f r e e d o w n l o a d a t w w w . c e p s . e u a n d w w w . e u r o c a p i t a l m a r k e t s . o r g

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 3

We wish to thank…

Carmignac Gestion

– Who provided seed sponsoring for this research project

Task Force Observers

– European Commission, EIOPA, EIB, OECD, French Ministry of Ecology and Energy, Danish

FSA, Caisse des Dépôts, EurofinUse

– Numerous academics and experts who contributed to the meetings

Task Force Members

– 61 individuals, 31 companies and organisations (full list in annex to the final report)

Task Force Chairman

– Allan Polack (CEO of Nordea Asset Management) on a personal capacity

DISCLAIMER: Only the policy recommendations presented at the beginning of the report reflect the general

consensus reached by task force members (although not every member may agree with every aspect of each

recommendation). The members were given the opportunity to comment on the draft final report, but its

contents were drafted independently by CEPS ECMI and may only be attributed to the rapporteurs.

Allan Polack Chairman of the CEPS ECMI Task Force

CEO of Nordea Asset Management

Recommendations

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 4

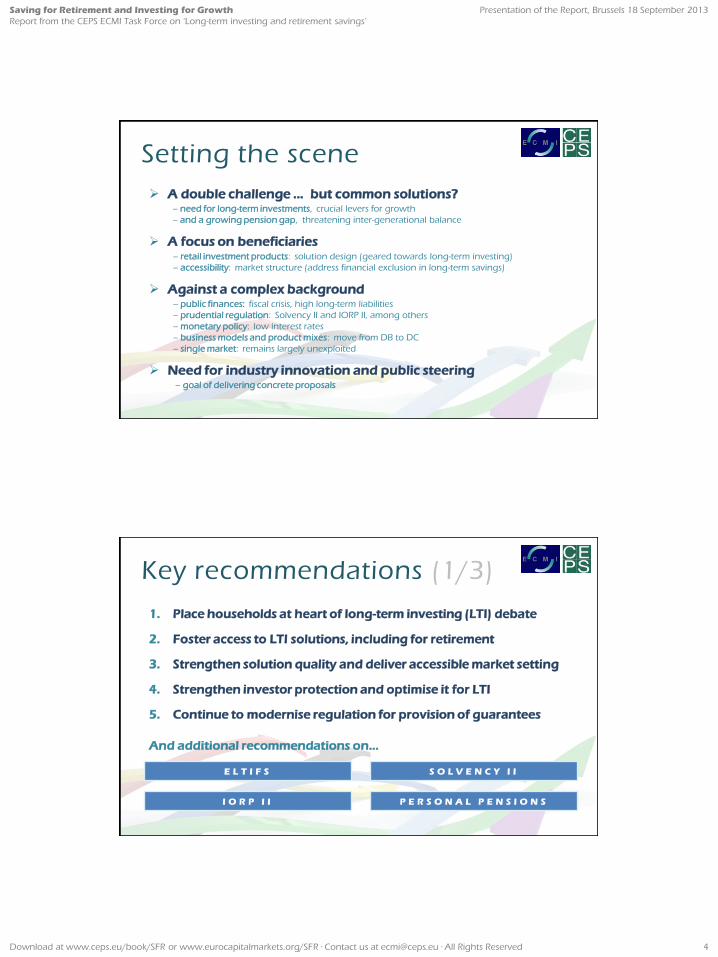

Setting the scene

A double challenge … but common solutions? – need for long-term investments, crucial levers for growth

– and a growing pension gap, threatening inter-generational balance

A focus on beneficiaries – retail investment products: solution design (geared towards long-term investing)

– accessibility: market structure (address financial exclusion in long-term savings)

Against a complex background – public finances: fiscal crisis, high long-term liabilities

– prudential regulation: Solvency II and IORP II, among others

– monetary policy: low interest rates

– business models and product mixes: move from DB to DC

– single market: remains largely unexploited

Need for industry innovation and public steering – goal of delivering concrete proposals

1. Place households at heart of long-term investing (LTI) debate

2. Foster access to LTI solutions, including for retirement

3. Strengthen solution quality and deliver accessible market setting

4. Strengthen investor protection and optimise it for LTI

5. Continue to modernise regulation for provision of guarantees

And additional recommendations on…

Key recommendations (1/3)

E L T I F S S O L V E N C Y I I

I O R P I I P E R S O N A L P E N S I O N S

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 5

1. Place households at heart of long-term investing (LTI) debate – Households are owners or beneficiaries of 60% of financial assets in Europe

– And they face growing need to save more and more efficiently

2. Foster access to LTI solutions, including for retirement – Households need easily accessible, high-quality and cost-efficient long-term solutions

– More standardisation to raise visibility, mitigate complexity and burden of choice

3. Strengthen solution quality and deliver accessible market setting – Not only volatile market returns, poor solution design and poorly organised markets

– Single market potential should be fully exploited (processing, taxation)

4. Strengthen investor protection and optimise it for LTI – Advice can be too onerous, need for simple standardised “defaults” (under execution-only)

– Suitability should consider costs for long-term solutions, given effect of compounding

5. Continue to modernise regulation for provision of guarantees – But reconcile with long-term investing and economic reality (illiquid assets, sovereign bonds)

– Cautious approximation of capital requirements for IORPs, full account taken of diversity

Key recommendations (2/3)

Key recommendations (3/3)

E L T I F S S O L V E N C Y I I

I O R P I I P E R S O N A L P E N S I O N S

Commission ELTIF proposal valuable

But will it work for retail investors?

Need to cope with financial exclusion

Proposal on long-term balanced funds

Matching adjustment essential

Could comprise expected cash flows?

Could be reflected on capital charges?

Issue of zero charges for sovereigns

Great diversity in Europe

Security and steering mechanisms

Support qualitative approximation

Cautious quantitative approximation

Blueprint for pan-European solutions

Regulated “defaults”

Principles for solution design

Attention to processing and taxation

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 6

Mirzha de Manuel Research Fellow , CEPS ECMI

Rapporteur to the Task Force

Presentation

SAVING FOR RETIREMENT AND

INVESTING FOR GROWTH

Mirzha de Manuel Aramendía

CEPS ECMI Research Fellow

R a p p o r t e u r t o t h e T a s k F o r c e

A u t h o r o f t h e R e p o r t

D o w n l o a d a t w w w . e u r o c a p i t a l m a r k e t s . o r g / S F R o r w w w . c e p s . e u / b o o k / S F R

Mirz ha de Manue l Aramendía · Al l R ights Reserved · Contac t ec mi@ c eps .eu

PRESENTATION OF THE REPORT

Brussels, 18 September 2013

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 7

1. The issues… as we see them At macro level: need for long-term financing

At micro-level: need for long-term investing solutions

Ultimately, money from beneficiaries towards pensions

2. Mobilising household savings… in solutions that deliver

3. Guarantees play a role… but are challenged

4. DC offers opportunities… but are not immediate Need for industry drive and regulatory intervention

5. Opportunities maximised within a single market For investors to benefit from best practices and lower costs

For efficient allocation of resources and macro-economic convergence

Index

DISCLAIMER: The content of this presentation is only attributable to the author and not to Task Force members.

1 . T H E I S S U E S … A S W E S E E T H E M ( 1 / 2 )

Households are the biggest holders of financial assets

in Europe, mostly l iquid (with virtuous exceptions)

Europe needs more long-term financing and wishes to

mitigate bespoke short -termism in financial markets

Households 23 (43%)

Institutional investors

14.9 (28%)

Banks 11.9 (22%)

Others 4 (7%)

37% 21%

22% 45%

41% 21%

0%

20%

40%

60%

80%

100%

Liquidity Intermediation

(+) (+) (+) (−) (−) (−) *€ tn, McKinsey * BCG

58%

20%

64%

17% 27%

46%

0%

20%

40%

60%

80%

100%

UK Spain Holand Italy Germany France

Illiquid (private pensions and life insurance) * BCG

Share of household financial assets.... Household financial assets....

* EC

INVESTMENT

UNIVERSE

RISK

APPETITE

INVESTMENT

BELIEFS

LIABILITY

PROFILE

DECISION

MAKING

LONG-TERM

INVESTMENT

* WEF

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 8

1 . T H E I S S U E S … A S W E S E E T H E M ( 2 / 2 )

Risk aversion is on the rise – due only to macro

fundamentals or also to inadequate intermediation?

Yet, cit izens need returns to fi l l a growing pension gap

(while fiscal capacity remains l imited)

35% 37% 32%

26% 22% 28%

0%

10%

20%

30%

40%

50%

2000 2010 2000 2010 2000 2010

Currency and deposits

Shares and other equity

Insurance technical reserves

35% 38% 41%

20%

32% 36%

44%

20%

42% 43% 49%

27%

10%

20%

30%

40%

50%

… plan to favour stable deposits

… are interest in a guaranteed return

product

… perceive funds bear too much risk

… plan to move money from stocks and mutual

funds to bonds

Share of retail investors who... Year 2010 Year 2011 Year 2012

* BCG

Share of household financial assets....

* OECD

5 9.5 20.2 25.3 40.2 68.8

97.6

170.5

243.5

379

468.8

374

0

100

200

300

400

500

LT HU IE CZ RO PL IT ES FR UK DE Other

EU pension gap (€ billions per annum, retiring 2011-2051)...

* AVIVA * SG

2 . M O B I L I S I N G H O U S E H O L D S A V I N G S … I N S O L U T I O N S T H A T D E L I V E R ( 1 / 1 )

Funded pensions and other solutions do not always

deliver – low market returns but also high costs

1.83%

-1.11%

-5%

-3%

-1%

1%

3%

5% Dec 2001 - Dec 2010

Dec 2007 - Jun 2011

* OECD

Average annual real net investment return of pension funds....

Great diversity in Europe… unexploited single market potential

1.4% 1.3%

1.0% 0.9%

0.5% 0.5% 0.4% 0.4% 0.4% 0.3% 0.2%

0.1%

0.0%

0.4%

0.8%

1.2%

1.6%

Czech Rep Spain Hungary Slovenia Slovak Rep Greece Poland Netherlands Finland Norway Belgium Denmark * OECD

Operating costs as a share of total assets for pension funds....

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 9

3 . G U A R A N T E E S P L A Y A R O L E … B U T A R E C H A L L E N G E D ( 1 / 2 )

The provision of guarantees necessitates long-term

investing (ALM) but is challenged by low rates…

Fwd 23-04-13

Fwd 06-09-04

Spot 23-04-13

Spot 06-09-04

0

1

2

3

4

5

6

3 …

9 …

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

Yie

ld in

%

Residual maturity in years

4.5% 4.4%

3.8%

2.3% 2.6%

2.2%

3.1% 3.6%

2.7%

0.4%

1.7%

0.7%

0%

1%

2%

3%

4%

5%

Generali Allianz Axa

Running yield Average guarantee in force

New money yield Average new guarantee

Euro-area yield curve, illustrative spread 2004-2013.... Average and new yield vs. guarantees in life insurance....

* ECB * Morgan

Stanley

…and the uncertain impact of revised prudential standards

100%

Covered bonds (AAA, 1 year)

20%

Covered bonds (AAA, 5 years)

EEA government bonds

13%

Corporate bonds (AAA, 5 years)

EEA government bonds

1.6%

Corporate bonds (B, 5 years)

EEA government bonds

1.5%

EEA & OECD equities

EEA government bonds

* CGFS

Stylised illustration of trade-offs between asset classes, based on Solvency II standard formula under QIS 5 (charges for spread risk and equity risk only)...

3 . G U A R A N T E E S P L A Y A R O L E … B U T A R E C H A L L E N G E D ( 2 / 2 )

Contentious issues, operational constraints and

potential solutions within Solvency I I

CONTENTIOUS ISSUES

►Assets held to maturity versus

available for trading…

adjustment on the liability

side of the balance sheet

discount rate for liabilities:

matching adjustment (MA)

►Calibration of capital charges…

steepness: duration & rating

arguably inaccurate reflection

of risks in less liquid assets

► Zero risk-weights for EAA

sovereign debt…

distortion to asset allocation

OPERATIONAL CONSTRAINTS

► In applying the MA…

separate default & spread risk

eligible liabilities and assets

reinvestment & other risks

rebalancing of portfolios

best reporting format

►Calculating standard charges…

availability & quality of data

limitations embedded in

methodologies & risk metrics

► Political and economic risks…

calculation of charges

euro-area crisis & institutions

POTENTIAL SOLUTIONS

►Broader and more flexible

application of MA could…

foster long-term investment

(LTI) in assets different to bonds

but is difficult to supervise,

given discretion left to insurers

► To avoid discouraging LTI…

extended MA

interim arrangements

pending new calculations?

► Introduce macro-economic &

institutional aspects…

in the debate on LTI

In conclusion: standard capital charges and solvency ratios

are needed but emphasis should be on supervision

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 10

4 . D C O F F E R S O P P O R T U N I T I E S … B U T A R E N O T I M M E D I A T E ( 1 / 1 )

DC offers more leeway in asset al location but

incentives need to be al igned with long -term investing

Issues identified in solution design and market structure

highlight difficulties in al igning incentives

13%

52%

2% 6% 6%

15%

7% 11%

47%

1%

12%

24%

1% 4%

0%

10%

20%

30%

40%

50%

Cash and deposits

Sovereign bonds

Loans Equity UCITS / mutual f.

Unallocated insurance

Other investments

Protected DC schemes Unprotected DC schemes

* OECD

Asset allocation…

0%

20%

40%

60%

80%

100%

Defined benefit Defined contribution Hybrid

Occupational pension funds in 2011…

* EIOPA

M A R K E T S T R U C T U R E :

− Product proliferation and consumer segmentation

− Difficulties for individuals to approach the market

− Widespread financial exclusion

− Potential for abuse due to consumer captivity

− Inefficient processing architecture

− Lack of standardisation

S O L U T I O N D E S I G N :

− Unclear retirement purpose and governance

− Liquidity profile inconsistent with pension objective

− Asset allocation skewed towards short-term assets

− Inadequate or simplistic investment practices

− Unsophisticated or poor risk management

− Communications lacking behavioural purpose

5 . O P P O R T U N I T I E S M A X I M I S E D W I T H I N A S I N G L E M A R K E T ( 1 / 2 )

Single market holds potential for efficiencies, both

for headline costs and long-term investing

R² = 0.6471

0.0%

0.4%

0.8%

1.2%

1.6%

0 100,000 200,000 300,000

Ad

min

istr

ati

on

exp

en

ses

/ to

tal a

sse

ts

Total assets (GBP millions)

R² = 0.4255

0.0%

0.4%

0.8%

1.2%

1.6%

0 1,000 2,000

Total assets (EUR millions)

Scale and costs

UK DC schemes…

Scale and costs

German DC schemes…

* BCG

Single market is also an opportunity to deliver greater

accessibility and long-term investment focus

Addressing both solution design and market structure :

– tackling financial exclusion as regards long-term savings / investments

– ensuring industry delivers primarily to end investors

Delivering easily accessible default solution (s):

– no perfect solution exists, instead need to balance trade-offs

– customisation vs. cost – sophistication vs. cost – LTI vs. size – transferability vs. LTI

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 11

5 . O P P O R T U N I T I E S M A X I M I S E D W I T H I N A S I N G L E M A R K E T ( 2 / 2 )

A blueprint for pan-European personal pensions

in six building blocks

S O L U T I O N D E S I G N D E F A U L T S O L U T I O N ( S )

Principle-based rules for non-default solution (s)

Explicit consideration of retirement purpose and long-term

investment horizons and practices

Long-term absolute-return objectives (replacement rates)

Link to de-accumulation phase (annuities, draw-downs)

Product regulation of default solution (s)

Life-cycling and life-styling features or options (limited or

restricted range)

Eligible assets and permissible investment practices

Allocation range per asset class, including less-liquid assets

S O L U T I O N P R O V I D E R S I N F R A S T R U C T U R E

Resources and expertise

Alignment of incentives with l-t investment horizon

Conflicts of interest in asset management value chain

Industrial organisation and market structure policy (volume,

access to less-liquid assets classes, cost)

Pan-European processing architecture

Pan-European clearing house for default options

Administration of contributions

Unbundling of services with lower efficient scale

Uniform regulation of holding rights and transfers

C O M M U N I C A T I O N D I S T R I B U T I O N

Full fee transparency, based on harmonised fee structures

Standardised pre-contractual disclosure, supported by a

single pan-European online information point

Annual statements focused on replacement rates and

follow-up actions by members

Special suitability requirements, with broad market

coverage and explicit consideration of costs

Professional standards for sales staff

Execution-only access for default solution (s) supported by

publicly-provisioned information

In sum…

At micro-economic level, LTI depends on retail solutions – focus should be on beneficiaries and end investors

Europe is focusing on prudential rules (and rightly so) – low interest rates represent a risk to financial stability

And there is space to further align those with LTI – but supervisors will need more resources and powers

But the world is moving away from DB into DC – need for a pan-European framework for personal pensions

And pension markets are becoming quasi-markets – policy-makers need to ensure they deliver value primarily to investors (not to industry)

Where the single market potential remains unexploited – in addition to efficiencies, need for macro-economic convergence

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 12

The Report SETTING

THE SCENE

What is long-term

investing?

Investors

Asset classes

Underlying

What is the focus of the

report?

Beneficiaries

Retail investment

products

Retail long-term investing

today

Diversity in Europe

Intermediation

Liquidity

Awareness / risk aversion

Incomplete single market

C H APTER 1

Long-term investing

and retirement savings

Guarantees and

prudential rules

Institutional long-term

investing today

Diversity in guarantees

Investment practices

Prudential safeguards

Adapting to low interest

rates

Risks to financial stability

In transition to limited

guarantees

Product mixes &

business models

Awaiting regulatory change

Solvency II principles

Point of contention

Potential solutions

Lessons for IORP reform

PERSONAL

PENSIONS

C H APTER 3

Private pensions today

Market structure

Solution design

A blueprint for pan-

European pensions

Diversity in Europe

Insufficient coverage and

low contributions

High costs & low returns

Demand & supply dynamics

Scale & infrastructure

Single market potential

Shortcomings identified

Key trade-offs in design

SINGLE

MARKET

C H APTER 2

Less liquid funds

Occupational pensions

Investor protection

Direct investments

Commission ELTIF proposal

Long-term balanced funds

Accompanying market

structure

Challenges in IORP reform

Potential benefits

Recommendations

Specifics for long-term

investment products

Disclosure & sale process

Thank you!

F r e e f u l l d o w n l o a d a t

www.eurocapita lmarkets .org/SFR

o r www.ceps .eu/book/SFR

( P r i n t e d c o p i e s a v a i l a b l e f o r p u r c h a s e )

Mirz ha de Manue l Aramendía · Al l R ights Reserved · Contac t ec mi@ c eps .eu

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 13

Nadia Calviño Deputy Director General, DG Internal Market and Services

European Commission

Comments

Patrick Hoedjes Director of Operations, EIOPA

(European Insurance and Occupational Pensions Authority)

Comments

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 14

Paul Woolley Senior Fellow and Chairman of the Advisory Board

Centre for the Study of Capital Market

Dysfunctionality, London School of Economics

Comments

Debate

Nadia Calviño Deputy Director General DG Internal Market and Services

European Commission

Patrick Hoedjes Director of Operations European Insurance and

Occupational Pensions Authority

Paul Woolley Research Fellow and Chairman Centre for the Study of Capital

Market Dysfunctionality, LSE

Allan Polack CEO Nordea Asset Management

Chairman of the Task Force

Karel Lannoo CEO and General Manager CEPS ECMI

Rapporteur to the Task Force

Mirzha de Manuel Research Fellow CEPS ECMI

Author of the Report

Saving for Retirement and Investing for Growth

Report from the CEPS ECMI Task Force on ‘Long-term investing and retirement savings’

Presentation of the Report, Brussels 18 September 2013

Download at www.ceps.eu/book/SFR or www.eurocapitalmarkets.org/SFR ∙ Contact us at [email protected] ∙ All Rights Reserved 15

Good bye!

Centre fo r European Po l i c y S tud ies · European Cap i ta l Marke ts Ins t i tu te · For the Report , Mi rz ha de Manue l Aramendía · Al l R ights Reserved

Download at www.ceps.eu/book/SFR

or www.eurocapitalmarkets.org/SFR