Savills webinar: Adaptation and evolution of rural estates ...

39

Savills webinar: Adaptation and evolution of rural estates and farming businesses 3 rd November 2020

Transcript of Savills webinar: Adaptation and evolution of rural estates ...

Savills webinar: Adaptation

and evolution of rural

estates and farming

businesses

3rd November 2020

Today’s speakers

Andy Green

Hoare & Co.

Emily Norton

Savills

Charlotte Patterson-Ryan

Womble Bond Dickinson (UK) LLP

Venetia Hoare

Hoare & Co.

2

Alexander Dickinson

Womble Bond Dickinson (UK) LLP

Lucian Cook

Savills

Johnny Dudgeon

Savills

Andy Green

Hoare & Co.

The Outlook for Interest Rates

Andy Green, head of Treasury, C. Hoare & Co.

4

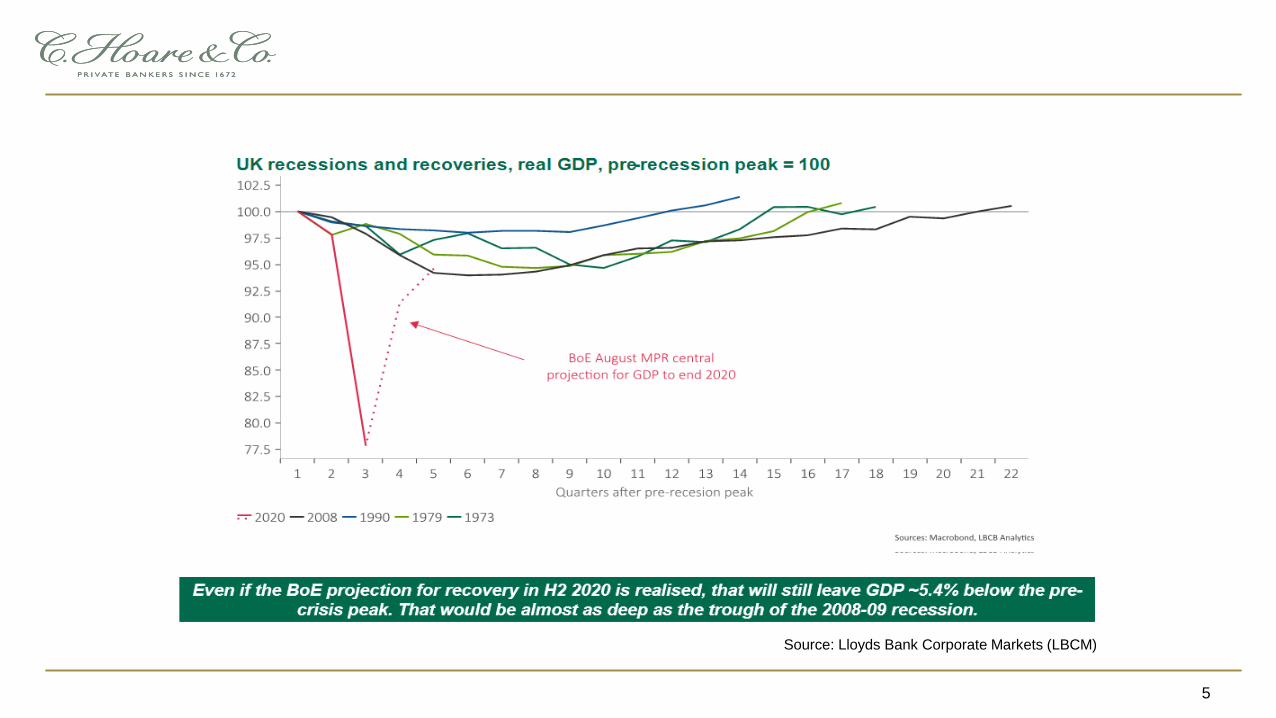

5

Source: Lloyds Bank Corporate Markets (LBCM)

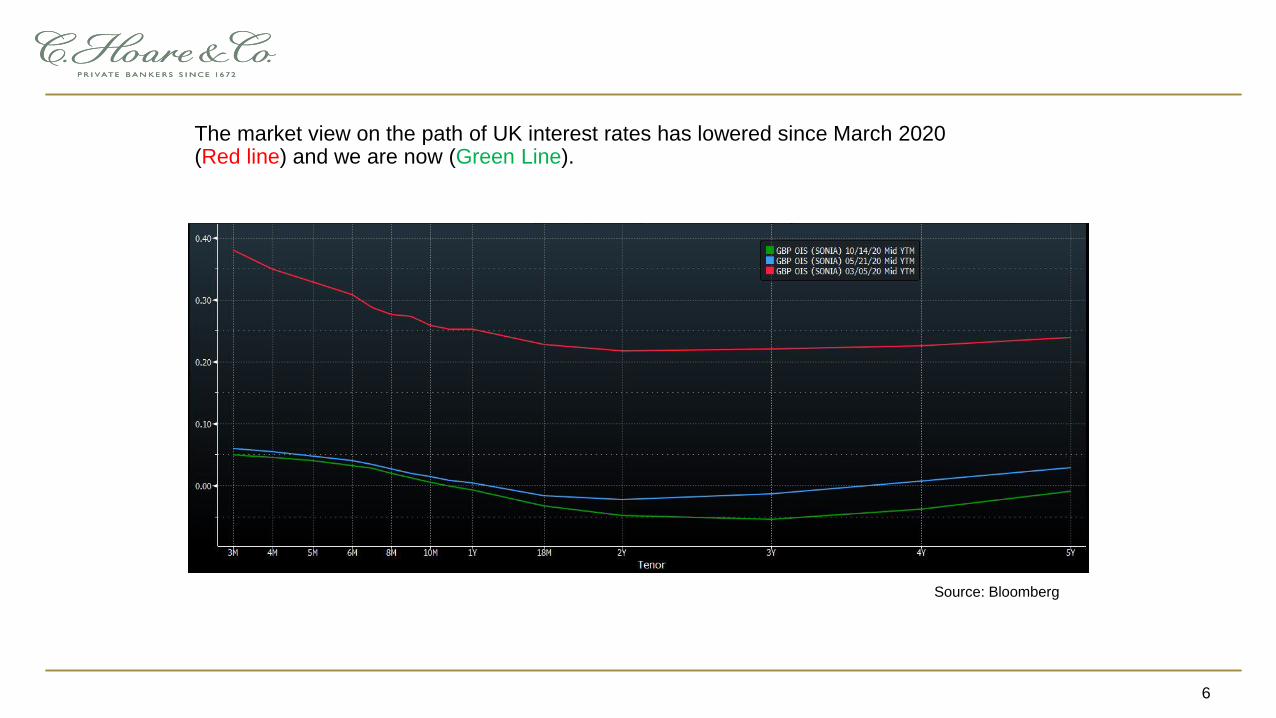

The market view on the path of UK interest rates has lowered since March 2020 (Red line) and we are now (Green Line).

6

Source: Bloomberg

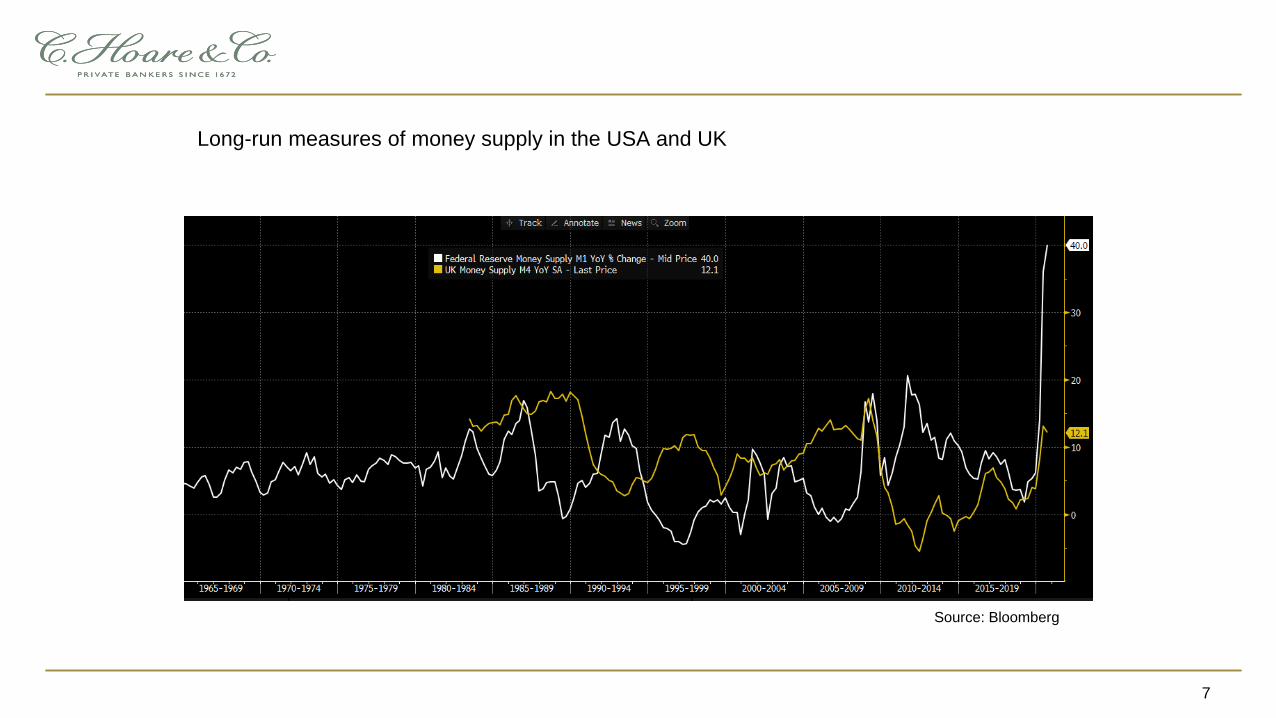

Long-run measures of money supply in the USA and UK

7

Source: Bloomberg

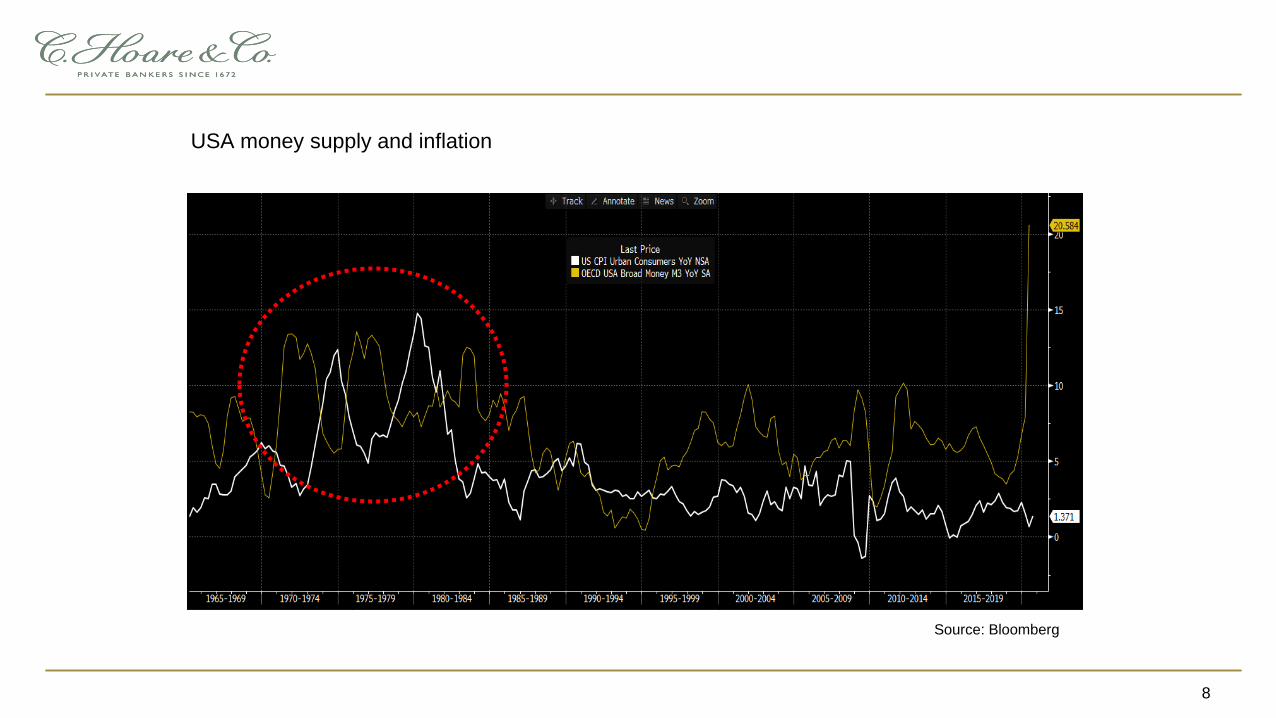

USA money supply and inflation

8

Source: Bloomberg

Key takeaways:

• The UK/world economic outlook is uncertain.

• Unemployment is likely to rise, particularly amongst 16-24-year olds.

• Negative rates are possible.

• Watch for bank bad-debt provisions.

• Low inflation for the next year or two, but what then?

• Watch money supply.

9

Important information

The information contained within this document is believed to be correct but cannot be guaranteed. Opinions constitute our judgement as at the date shown and are subject to change. The document is not intended as an offer or solicitation to buy or sell securities or any other investment or banking product, nor does it constitute a personal recommendation.

The research and analysis contained herein have been procured, and may have been acted upon, by C. Hoare & Co. or a connected company for its own purposes, and the results are being made available to you only incidentally. In the unlikely event of C. Hoare & Co. being unable to meet its liabilities, The Financial Services Compensation Scheme will come into operation. C. Hoare & Co. participates in the Financial Ombudsman Service. Further details are available on request.

C. Hoare & Co. is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority with firm reference number 122093. Regd. in England No. 240822 Regd. office: 37 Fleet Street London EC4P 4DQ Swift: HOABGB2L DX: 125 London/Chancery Lane.

Published on 26/10/2020.

10

Policy outlook

Emily Norton

Head of Rural Research

3 November 2020

And why now is the right time to make decisions

12

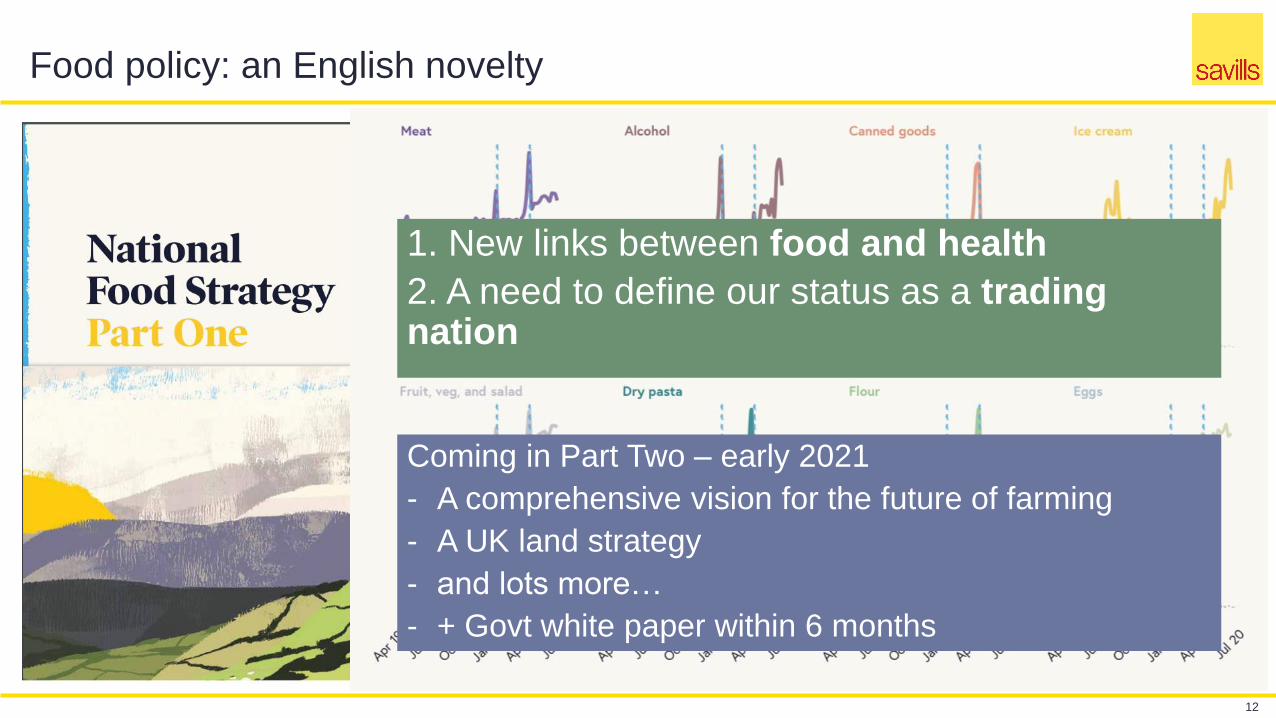

Food policy: an English novelty

1. New links between food and health

2. A need to define our status as a trading nation

Coming in Part Two – early 2021

- A comprehensive vision for the future of farming

- A UK land strategy

- and lots more…

- + Govt white paper within 6 months

13

Trade policy: Who to believe?

Published LMPs visible to community

14

“The recent ELMS consultation were explicit that ELMS was not a replacement for the BPS or Countryside Stewardship…”

1.Environment Bill now back in Committee…

2.Environment is about regulation as well as investment

3.DEFRA consultation this autumn on “the best approaches to designing a future regulatory system. As part of this process we should consider the role our agricultural standards play in achieving goals in the 25YEP and net zero.”

Risk: Customers

and markets

Research: best and

highest use

Resilience: diversify up as

well as outRegeneration

How to prepare for ELMS?

Environment Policy

15

Why now? Farmland supply

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

£ p

er

he

cta

re

Supply/Turnover (farmland)

Source: Savills research, Defra

Source: Savills Research

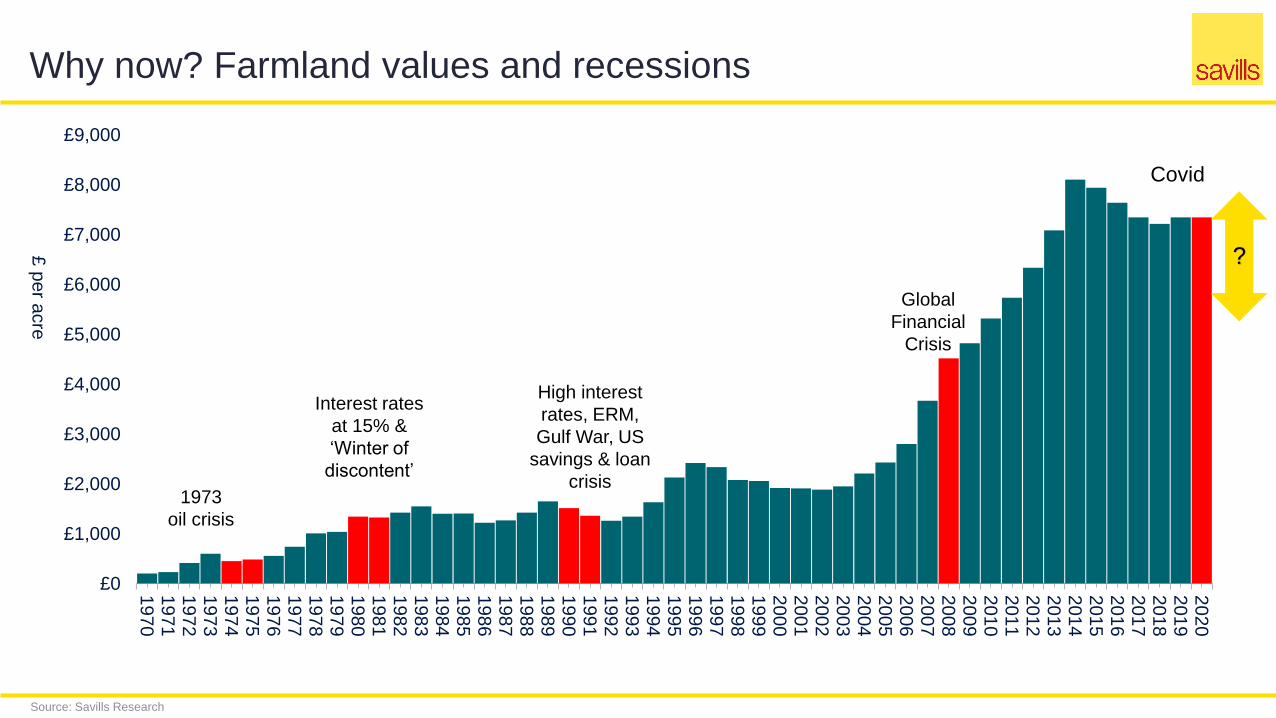

Why now? Farmland values and recessions

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

£0

£1,000

£2,000

£3,000

£4,000

£5,000

£6,000

£7,000

£8,000

£9,000

£ p

er a

cre

1973

oil crisis

Global

Financial

Crisis

?

Covid

Interest rates

at 15% &

‘Winter of

discontent’

High interest

rates, ERM,

Gulf War, US

savings & loan

crisis

17

Why now? Farmland supply, farmland values and forestry values

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

-

5,000

10,000

15,000

20,000

25,000

Su

pp

ly (

farm

lan

d o

nly

)

£ p

er

he

cta

re

Average GB Farmland Value / ha Forest £/net ha Supply/Turnover (farmland)

Source: Savills research, Defra

Charlotte Patterson-Ryan

Womble Bond Dickinson (UK) LLP

womblebonddickinson.com

Charlotte Patterson-Ryan

Building resilience: Making the

most of your advisors and

innovative work practices to

navigate Covid-19

Innovation and Resilience

p21

Surviving and

thriving

Innovation

Resilience

Innovation

Solar

Retirement Lifestyle Villages

Vineyards

Residential Developments

Re-financing

Residential Property

Disposals

Real time examples

Other examples of innovation

Drive through Farm Shops

Art installations

Vertical Farming

What role do advisors play?

Technical Knowledge

Professional Networks

Business Acumen

Use of technology

Evolving working practices

Early engagement

Momentum

Transparency

Venetia Hoare

Hoare & Co.

Alexander Dickinson

Womble Bond Dickinson (UK) LLP

Lucian Cook

Savills

30

Black Swans & Ugly DucklingsWhat’s really going on in the Residential Market?

3rd November 2020

31

Putting the recent events in context

60

65

70

75

80

85

90

95

100

105

Index of Monthly Economic Output Low price growth coming

into lockdown

Low interest ratesSwift

action to protect

jobs andhousehold finances

Changing lifestyles

and property needs

Stamp duty

holiday

Source: ONS

Source: Nationwide: RICS, TwentyCI 32

A remarkable recovery in the housing market

-100

-80

-60

-40

-20

0

20

40

60

80

100

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Oct-

15

Feb

-16

Jun

-16

Oct-

16

Feb

-17

Jun

-17

Oct-

17

Feb

-18

Jun

-18

Oct-

18

Feb

-19

Jun

-19

Oct-

19

Feb

-20

Jun

-20

Oct-

20

RIC

S –

Bala

nce o

f O

pin

ion

Ann

ua

l H

ou

se P

rice G

row

th

Nationwide House Price Growth RICS New Buyer Enquiries

0%

25%

50%

75%

100%

125%

150%

175%

200%

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20

Co

mp

are

d to

sa

me

pe

rio

d la

st ye

ar

Key market metrics

Agreed Sales New Instructions Price Reductions

Source: Savills Client Survey 33

56%more inclined to work from home more regularly in the

future

62%said the amount of garden

or outside space had become more important

74%said the experience of Covidhad caused them to reassess

their work-life balance

39% significantly so

Village

location

More attractive to 48%(39% in April)

increasing to 54% for those with school age children(46% in April)

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

A growing backlog of agreed deals

Deals Agreed Mortgage Approvals* Completed Transactions

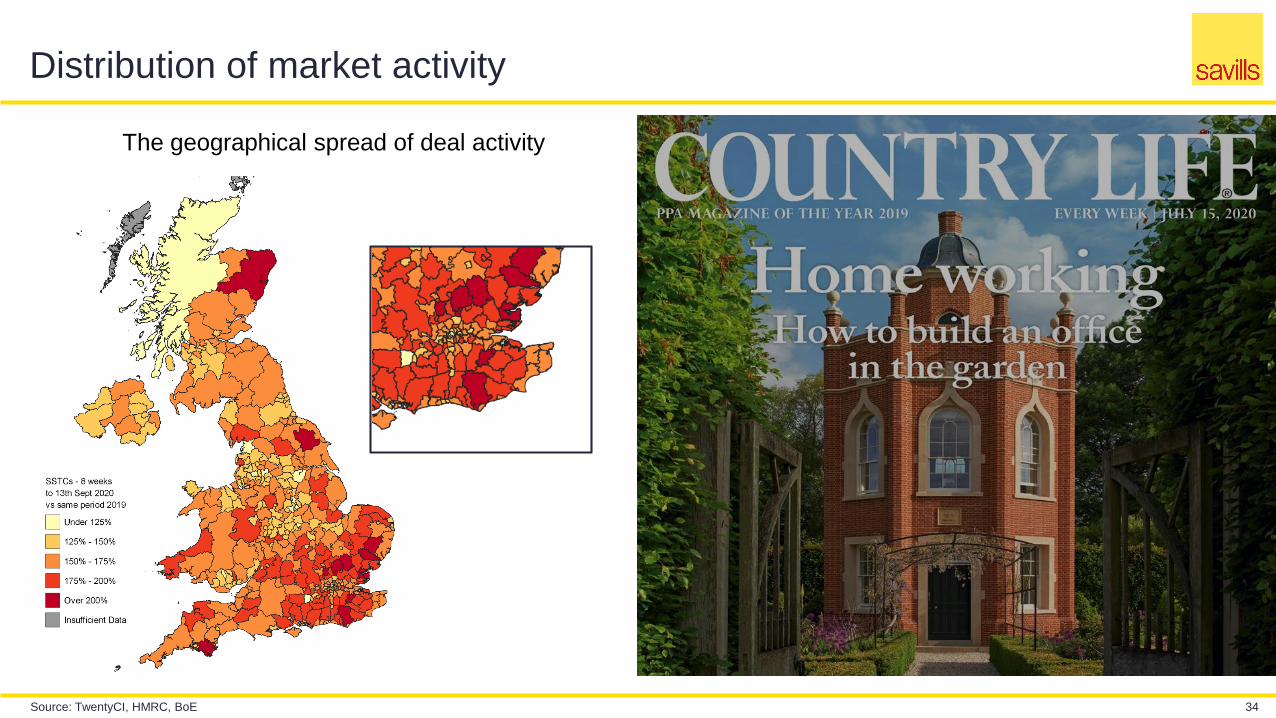

Source: TwentyCI, HMRC, BoE 34

Distribution of market activity

The geographical spread of deal activity

35

The move from a V to a w

Latest Economic Outlook(Morgan Stanley 01/11/2020)

Looking forward

36

Stamp duty holidays & surcharges will distort buyer behaviour in the next 9 months

2nd lockdown will reaffirm changing housing needs & priorities

The wider tax environment may act as a drag on future price growth

Interest rates are expected to be lower for much longer

Lifestyle changes will ultimately depend on the search for a vaccine

Economic pressures & Brexit will make it difficult to sustain current momentum

Forecasting in an uncertain world

37

Average UK House Price to rise by 4.0%

this year

Transactions to exceed 1m

over the course of the year

With a lot of agreed sales delayed until early 2021

Next year will be a year in

three parts with no net price

growth

Activity will be primarily driven

by home movers and cash buyers

over the next 2 years

Overall price growth of 20% expected over

5 years primarily due to

low interest rates

Thank you

© Savills 2020

38

Q&A’s

Andy Green

Emily Norton

Charlotte Patterson-Ryan

Venetia Hoare

39

Alexander Dickinson

Lucian Cook

Johnny Dudgeon