Saudi Petrochemical Sector › ScheduleReports › 82c2b1a1_TasiPetroS… · Saudi Petrochemicals...

34

Saudi Petrochemicals Sector Petrochemicals –Industrial Saudi Arabia 25 May 2015 January 18, 2010 US$110bn 30.3% US$253mn Market cap Free float Avg. daily volume Disclosures Please refer to the important disclosures at the back of this report. Powered by EFA Platform Key themes Although an oversupply situation prevails, changes in the oil industry dynamics has resulted in a jump in crude prices over the last few weeks. This has helped petrochemical product prices move up to a certain extent although the uptrend sustainability remains to be seen as global economic growth remains uneven and industrial outlook in China remains weak. These factors will pose headwinds for Saudi petrochemical players. Implications Based on Q1 results, crude and petrochemical product price trends, global macroeconomic situation and company-specific reasons, we have adjusted our earnings and dividend estimates. We have revised target prices across the board and adjusted ratings of two companies as well. What do we think? Stock Rating Price Target SABIC Overweight SAR125.5 SAFCO Neutral SAR127.4 Sipchem Neutral SAR34.3 NIC Neutral SAR26.3 Yansab Neutral SAR52.6 APC Neutral SAR59.8 SPC Underweight SAR14.1 YTD Performance (Rebased to 100) 80 100 120 140 160 Jan-15 Feb-15 Mar-15 Apr-15 May-15 SABIC Sipchem SAFCO NIC Yansab APC SPC TASI Source: Bloomberg, Al Rajhi Capital Note: Market data is of May 12, 2015 closing. Research Department ARC Research Team Tel +966 11 211 9370, [email protected] Saudi Petrochemical Sector Headwinds persist; Valuations expensive Demand dampness and lower petrochemical product prices have impacted the performance of Saudi petrochemical companies in Q1. Since then, oil prices have surged and product prices have followed its trend. However, the sustainability of the product price uptick remains to be seen amid oil price volatility. Also, an uneven global economic growth and a muted industrial scenario in China indicate demand dampness over the near term. Based on Q1 results, crude and petrochemical product price trends, macroeconomic situation in key markets and company-specific reasons, we have revised our earnings and dividend estimates. We continue with our Overweight rating on SABIC. We have revised down our rating on SAFCO and SPC to Neutral and Underweight respectively. We have Neutral rating on rest of the petrochemical stocks under our coverage. Oil and global economy: After dipping to a six-year low of ~US$45 a barrel in mid-January, Brent surged to US$69 as a fall in the rig count in the US, drop in the inventory levels and a stable demand from Asia boosted sentiments. However, a pending deal of the Western powers with Iran, which would lift the oil embargo (not immediately though), and continuation of OPEC’s production policy has restrained a further surge. Additionally, industrial activities remained lackluster in China as demand from some of its key markets remained lull. As a result, Saudi companies posted dismal Q1 numbers (net profit 53% down y-o-y). Based on oil market dynamics, we expect prices to be in the $60-70 range for the rest of 2015. Although, product prices have jumped in the last few weeks, we believe it is primarily due to higher oil prices rather than demand strength. Shale exploration brings in petrochemical investments: A sharp jump in shale exploration in recent years along with proven high reserves have emboldened leading producers to undertake new/debottlenecking projects in North America. These producers will be able to keep ethylene cash costs low as compared to their naphtha peers. This will keep global petrochemical prices under check, impacting the bottom-lines and margins of Saudi players. In need of long-term strategies: Saudi companies, despite government support, have limited themselves to being producers of basic/intermediate products. Given the scenario, we believe Saudi players need to move downstream in the value chain, either through vertical integration organically or inorganically. This will bolster their product portfolio and improve their long- term profitability. However, such projects would require shifting toward heavier feedstock. Valuation expensive: The announcement of the date of opening up of the market to foreign investors brought in cheers among Saudi investors. Sentiments drove petrochemical sector stocks, which jumped in the range of 7% to 35% QTD (except SAFCO). Saudi Petrochemical Index currently trades at 17.4x (P/E 2015E), in line with its global peer group - MSCI World Chemicals Index and S&P Chemicals Index – averages of 17.8x and 17.9x respectively. We do not see any more expansion in valuation multiples. Based on Q1 results, oil and petrochemical market dynamics and company-specific reasons, we have revised target prices of the companies under coverage, except Yansab. SABIC remains our favorite in Saudi petrochemical space. We have revised our rating on SAFCO to Neutral due to urea price pressure and multiple delays in the commencement of its fifth unit. Also, we have downgraded SPC to Underweight given its failure to attend structural problems.

Transcript of Saudi Petrochemical Sector › ScheduleReports › 82c2b1a1_TasiPetroS… · Saudi Petrochemicals...

Saudi Petrochemicals Sector Petrochemicals –Industrial Saudi Arabia

25 May 2015

January 18, 2010

US$110bn 30.3% US$253mn Market cap Free float Avg. daily volume

Disclosures Please refer to the important disclosures at the back of this report. Powered by EFA Platform

Key themes

Although an oversupply situation prevails, changes in the oil industry dynamics has resulted in a jump in crude prices over the last few weeks. This has helped petrochemical product prices move up to a certain extent although the uptrend sustainability remains to be seen as global economic growth remains uneven and industrial outlook in China remains weak. These factors will pose headwinds for Saudi petrochemical players.

Implications

Based on Q1 results, crude and petrochemical product price trends, global macroeconomic situation and company-specific reasons, we have adjusted our earnings and dividend estimates. We have revised target prices across the board and adjusted ratings of two companies as well.

What do we think?

Stock Rating Price Target

SABIC Overweight SAR125.5

SAFCO Neutral SAR127.4

Sipchem Neutral SAR34.3

NIC Neutral SAR26.3

Yansab Neutral SAR52.6

APC Neutral SAR59.8

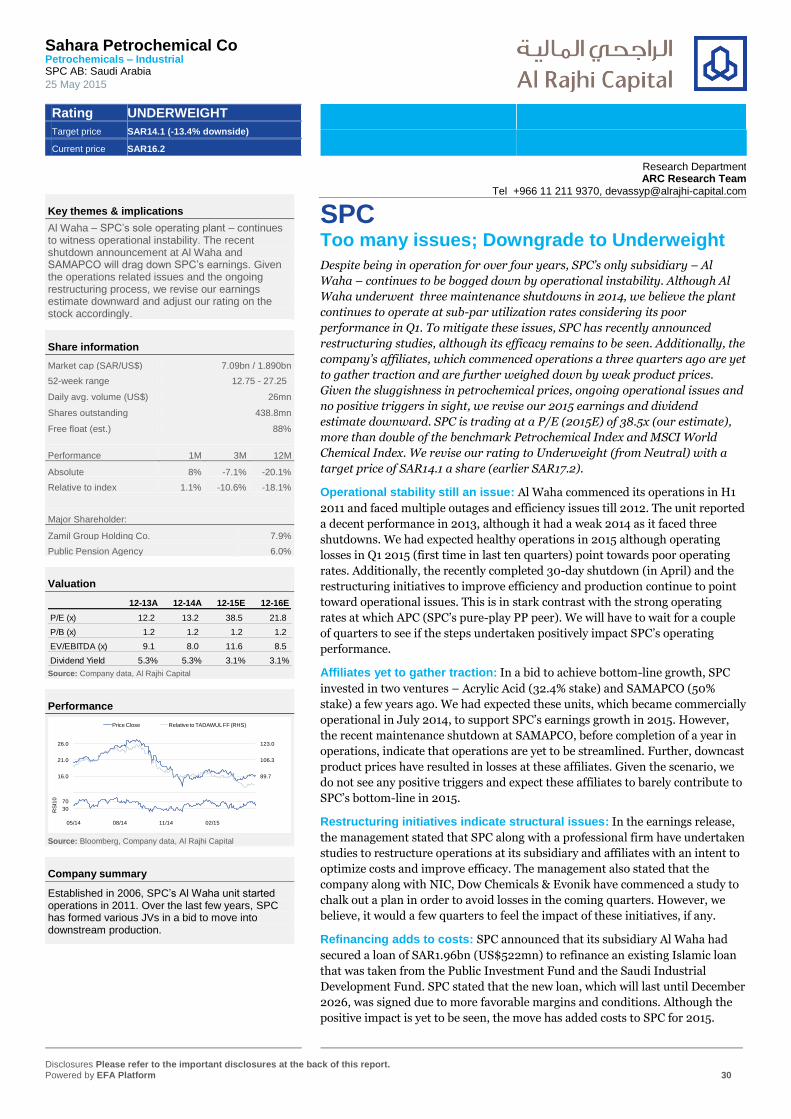

SPC Underweight SAR14.1

YTD Performance (Rebased to 100)

80

100

120

140

160

Jan-15 Feb-15 Mar-15 Apr-15 May-15

SABIC Sipchem SAFCO NIC

Yansab APC SPC TASI Source: Bloomberg, Al Rajhi Capital Note: Market data is of May 12, 2015 closing.

Research Department ARC Research Team

Tel +966 11 211 9370, [email protected]

Saudi Petrochemical Sector Headwinds persist; Valuations expensive Demand dampness and lower petrochemical product prices have impacted the

performance of Saudi petrochemical companies in Q1. Since then, oil prices

have surged and product prices have followed its trend. However, the

sustainability of the product price uptick remains to be seen amid oil price

volatility. Also, an uneven global economic growth and a muted industrial

scenario in China indicate demand dampness over the near term. Based on Q1

results, crude and petrochemical product price trends, macroeconomic

situation in key markets and company-specific reasons, we have revised our

earnings and dividend estimates. We continue with our Overweight rating on

SABIC. We have revised down our rating on SAFCO and SPC to Neutral and

Underweight respectively. We have Neutral rating on rest of the petrochemical

stocks under our coverage.

Oil and global economy: After dipping to a six-year low of ~US$45 a barrel in

mid-January, Brent surged to US$69 as a fall in the rig count in the US, drop in

the inventory levels and a stable demand from Asia boosted sentiments.

However, a pending deal of the Western powers with Iran, which would lift the

oil embargo (not immediately though), and continuation of OPEC’s production

policy has restrained a further surge. Additionally, industrial activities remained

lackluster in China as demand from some of its key markets remained lull. As a

result, Saudi companies posted dismal Q1 numbers (net profit 53% down y-o-y).

Based on oil market dynamics, we expect prices to be in the $60-70 range for the

rest of 2015. Although, product prices have jumped in the last few weeks, we

believe it is primarily due to higher oil prices rather than demand strength.

Shale exploration brings in petrochemical investments: A sharp jump in

shale exploration in recent years along with proven high reserves have

emboldened leading producers to undertake new/debottlenecking projects in

North America. These producers will be able to keep ethylene cash costs low as

compared to their naphtha peers. This will keep global petrochemical prices

under check, impacting the bottom-lines and margins of Saudi players.

In need of long-term strategies: Saudi companies, despite government

support, have limited themselves to being producers of basic/intermediate

products. Given the scenario, we believe Saudi players need to move

downstream in the value chain, either through vertical integration organically or

inorganically. This will bolster their product portfolio and improve their long-

term profitability. However, such projects would require shifting toward heavier

feedstock.

Valuation expensive: The announcement of the date of opening up of the

market to foreign investors brought in cheers among Saudi investors.

Sentiments drove petrochemical sector stocks, which jumped in the range of 7%

to 35% QTD (except SAFCO). Saudi Petrochemical Index currently trades at

17.4x (P/E 2015E), in line with its global peer group - MSCI World Chemicals

Index and S&P Chemicals Index – averages of 17.8x and 17.9x respectively. We

do not see any more expansion in valuation multiples. Based on Q1 results, oil

and petrochemical market dynamics and company-specific reasons, we have

revised target prices of the companies under coverage, except Yansab. SABIC

remains our favorite in Saudi petrochemical space. We have revised our rating

on SAFCO to Neutral due to urea price pressure and multiple delays in the

commencement of its fifth unit. Also, we have downgraded SPC to Underweight

given its failure to attend structural problems.

Saudi Petrochemicals

Sector Petrochemicals –Industrial

Disclosures Please refer to the important disclosures at the back of this report. 2

Crude & petrochemical dynamics Oil volatile; petrochemicals prices range-bound Uptick in oil prices boosting optimism… Brent crude, after halving from the peak seen in June 2014, continued to remain under

pressure and touched a low of US$45 in January 2015. However, the steep fall in crude prices

made oil exploration uneconomic, especially for unconventional oil explorers in the US. This

has resulted in a sharp decline in the rig count, which has fallen to 668 (as of May 10, source:

BHI), a fall for straight 22 weeks and the lowest since September 2010. The drop in US oil

production coupled the geo-political unrest in the Middle East (Yemen unrest, Syria and Iraq

crises) has led to an upward pressure on crude prices, which has jumped ~48% from its

recent low crossing US$69 a barrel mark. The rise in Brent prices pushed up naphtha, which

surged ~49% since the January-low, supporting petrochemical prices. However, Brent prices

have fallen to ~US$66, pressuring naphtha prices, which will have a trickle down impact on

the petrochemical product prices in absence of strong demand environment.

…however supply situation still remains ample Over the past seven years, oil demand has risen just over 6mbpd (source: US EIA) or at an

average of ~1mbpd a year. Interestingly, most of the incremental demand has been taken care

of by the rise in US shale production, while OPEC production remained stagnated. For 2015,

the US energy agency anticipates a 1mbpd demand growth (vs. 0.9mbpd in 2014) while

nearly all the incremental demand is expected to be met by rising shale production indicating

tepid demand for OPEC oil. The US EIA expects an incremental demand of 1.1mbpd y-o-y in

2015 to touch 93.6mbpd while supply is up 1mbpd to 95.2mbpd indicating oversupply. OPEC

has been pumping oil at record levels with average production standing at 31.3mbpd in April

(source: Bloomberg). An oversupply situation, the likelihood of lifting sanctions on Iran and

maintaining production status-quo at the OPEC June meeting are expected to keep a tab on

oil prices over the near term. We expect oil price to hover in the range of US$60-70 a barrel

for the rest of 2015. However, a sudden disruption in Iraq or Libya due to the prevailing

geopolitical tensions and a faster-than-expected economic/industrial recovery in Euro zone

and China can be viewed as upside risks.

Figure 1 Brent & naphtha recover, although remain range-bound Figure 2 Growth in oil supply globally

0

20

40

60

80

100

120

Jun-14 Sep-14 Dec-14 Mar-15

Brent Naphtha

1.3

-1.8

1.4

0.3

1.4

-1.0

0.1

0.1

0.6

0.6

0.4

1.0

1.21.6

0.9

-0.4

1.1

-0.2-0.5

0.20.4

-0.2

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

2008 2009 2010 2011 2012 2013 2014 2015E

mbpd

OPEC US Rest of the world Source: Bloomberg, Al Rajhi Capital Note: Rebased to 100 Source: US EIA, Al Rajhi Capital

Petrochemical prices jump; albeit remain lower y-o-y Petrochemical prices have climbed up double-digit as crude prices rose over 20% YTD (over

43% since the lowest point seen in January). However, product prices still very much lower y-

o-y. In addition to low oil prices, we attribute lower product prices to weak manufacturing

scenario in China and muted demand in Europe. Having said that, we do not expect product

prices to jump considerably from current levels unless oil prices move up on a sustained

basis. Additionally, strong positives in the Chinese and European industrial scenario would

be needed to push up petrochemical prices.

Saudi Petrochemicals

Sector Petrochemicals –Industrial

Disclosures Please refer to the important disclosures at the back of this report. 3

Ethylene (+23.4% YTD) and propylene (10.6%) prices moved upward primarily shutdown at

Shell’s Moerdijk cracker in the Netherlands and other crackers running at a higher rate amid

supply tightness due to outage of some plants (source: ICIS). A tighter supply-demand

balance was seen in Asia due to a limited supply from Europe and the Middle East, resulting

in a strong price uptick over the last couple of months. Given the current macroeconomic and

crude price scenarios we expect ethylene to move in the range of US$1200-1300 a ton while

propylene prices should be in the range of US$1100-1200 a ton over the next few months.

An uptick in ethylene prices coupled with a tight inventory position and shutdowns in the

Middle East pushed up polyethylene (PE) prices over the past couple of months. Overall

HDPE and LDPE prices moved up 6.9% and 11.5% YTD respectively although they continued

to be lower y-o-y. Similar dynamics apply to polypropylene (PP), whose prices climbed 16.4%

YTD. We anticipate PE prices to be in the range of US$1350-1550 (both grades included),

while PP should trade at prices of US$1300-1400 a ton over the near term.

Figure 3 Ethylene and propylene prices Figure 4 Polyethylene and polypropylene prices

600

800

1000

1200

1400

1600

1800

Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15

US$/ton

Ethylene Propylene

900

1100

1300

1500

1700

Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15

US$/ton

Polyethylene Polypropylene Source: Bloomberg, Al Rajhi Capital Source: Bloomberg, Al Rajhi Capital

Mono-ethylene glycol (MEG) prices continue to be governed by crude and ethylene price

trends. This, along with a limited availability of feedstock in Europe, lower operating rates

and a few plant shutdowns in Asia have tightened the supply situation (source: ICIS), which

resulted in firming of MEG prices (+29% YTD). Demand for MEG, which has applications in

anti-freeze and polyethylene terephthalate (PET) industries, is expected to remain steady as

the winter season comes to an end but PET industries operations pickup in summer. Further,

shutdowns in Europe and Middle East (Yansab) will support MEG prices in the near term.

We expect MEG prices to hover in the range of US$1200-1300 over the next few months.

After a weak Q1, methanol prices picked up following the crude trend. After this uptick we

expect prices to remain stable around its long-term average of around US$350 a ton.

Figure 5 MEG prices Figure 6 Methanol prices

800

900

1000

1100

1200

1300

1400

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

200

300

400

500

600

Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15

US$/ton

Source: Bloomberg, Al Rajhi Capital Source: Bloomberg, Al Rajhi Capital

Saudi Petrochemicals

Sector Petrochemicals –Industrial

Disclosures Please refer to the important disclosures at the back of this report. 4

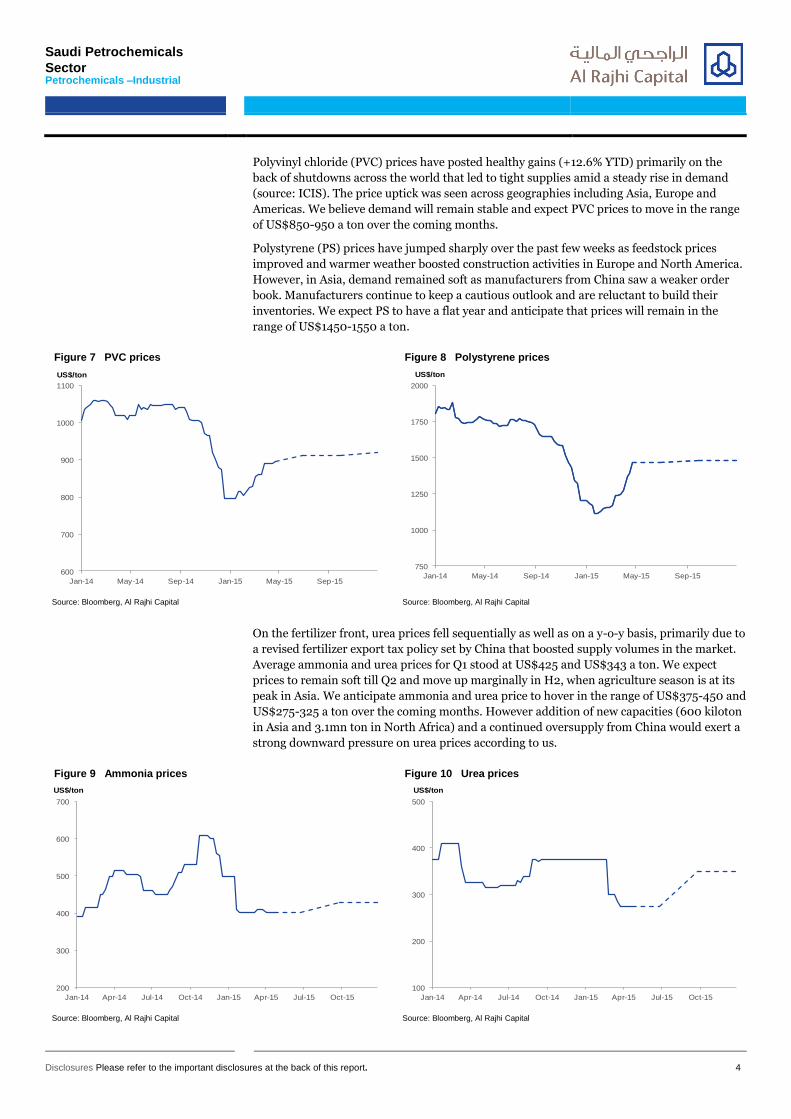

Polyvinyl chloride (PVC) prices have posted healthy gains (+12.6% YTD) primarily on the

back of shutdowns across the world that led to tight supplies amid a steady rise in demand

(source: ICIS). The price uptick was seen across geographies including Asia, Europe and

Americas. We believe demand will remain stable and expect PVC prices to move in the range

of US$850-950 a ton over the coming months.

Polystyrene (PS) prices have jumped sharply over the past few weeks as feedstock prices

improved and warmer weather boosted construction activities in Europe and North America.

However, in Asia, demand remained soft as manufacturers from China saw a weaker order

book. Manufacturers continue to keep a cautious outlook and are reluctant to build their

inventories. We expect PS to have a flat year and anticipate that prices will remain in the

range of US$1450-1550 a ton.

Figure 7 PVC prices Figure 8 Polystyrene prices

600

700

800

900

1000

1100

Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15

US$/ton

750

1000

1250

1500

1750

2000

Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15

US$/ton

Source: Bloomberg, Al Rajhi Capital Source: Bloomberg, Al Rajhi Capital

On the fertilizer front, urea prices fell sequentially as well as on a y-o-y basis, primarily due to

a revised fertilizer export tax policy set by China that boosted supply volumes in the market.

Average ammonia and urea prices for Q1 stood at US$425 and US$343 a ton. We expect

prices to remain soft till Q2 and move up marginally in H2, when agriculture season is at its

peak in Asia. We anticipate ammonia and urea price to hover in the range of US$375-450 and

US$275-325 a ton over the coming months. However addition of new capacities (600 kiloton

in Asia and 3.1mn ton in North Africa) and a continued oversupply from China would exert a

strong downward pressure on urea prices according to us.

Figure 9 Ammonia prices Figure 10 Urea prices

200

300

400

500

600

700

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

US$/ton

100

200

300

400

500

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

US$/ton

Source: Bloomberg, Al Rajhi Capital Source: Bloomberg, Al Rajhi Capital

Saudi Petrochemicals

Sector Petrochemicals –Industrial

Disclosures Please refer to the important disclosures at the back of this report. 5

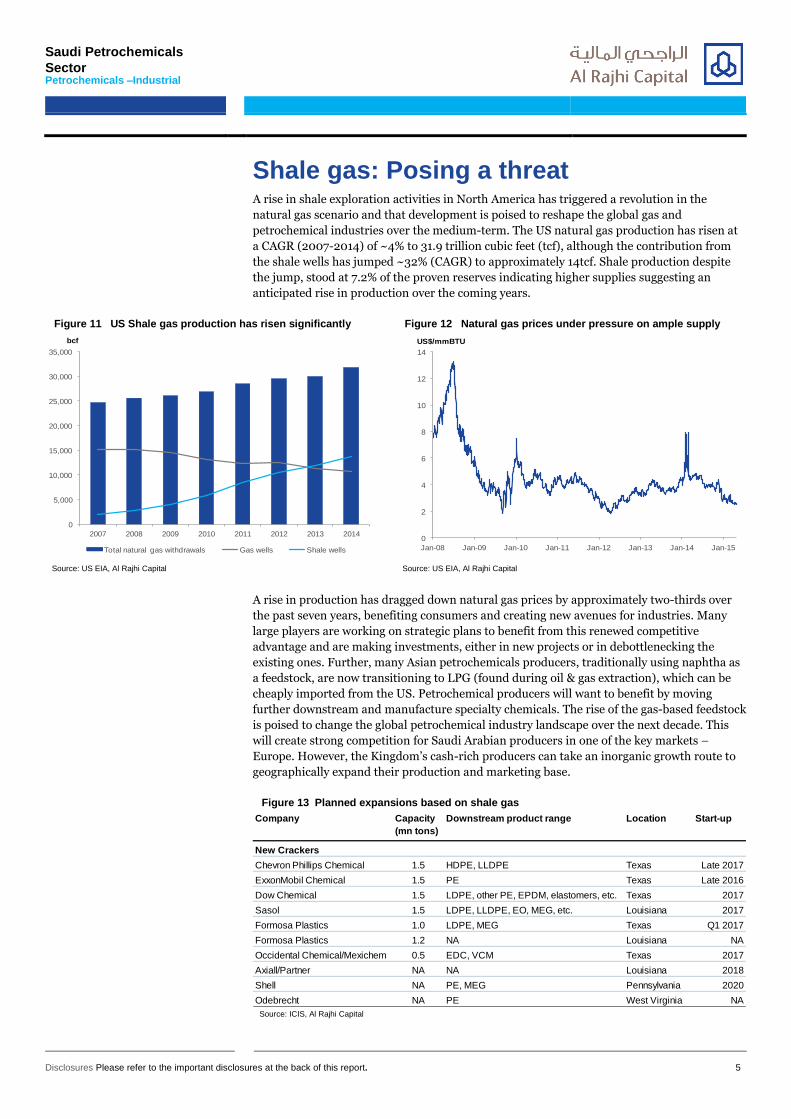

Shale gas: Posing a threat A rise in shale exploration activities in North America has triggered a revolution in the

natural gas scenario and that development is poised to reshape the global gas and

petrochemical industries over the medium-term. The US natural gas production has risen at

a CAGR (2007-2014) of ~4% to 31.9 trillion cubic feet (tcf), although the contribution from

the shale wells has jumped ~32% (CAGR) to approximately 14tcf. Shale production despite

the jump, stood at 7.2% of the proven reserves indicating higher supplies suggesting an

anticipated rise in production over the coming years.

Figure 11 US Shale gas production has risen significantly Figure 12 Natural gas prices under pressure on ample supply

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2007 2008 2009 2010 2011 2012 2013 2014

bcf

Total natural gas withdrawals Gas wells Shale wells

0

2

4

6

8

10

12

14

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

US$/mmBTU

Source: US EIA, Al Rajhi Capital Source: US EIA, Al Rajhi Capital

A rise in production has dragged down natural gas prices by approximately two-thirds over

the past seven years, benefiting consumers and creating new avenues for industries. Many

large players are working on strategic plans to benefit from this renewed competitive

advantage and are making investments, either in new projects or in debottlenecking the

existing ones. Further, many Asian petrochemicals producers, traditionally using naphtha as

a feedstock, are now transitioning to LPG (found during oil & gas extraction), which can be

cheaply imported from the US. Petrochemical producers will want to benefit by moving

further downstream and manufacture specialty chemicals. The rise of the gas-based feedstock

is poised to change the global petrochemical industry landscape over the next decade. This

will create strong competition for Saudi Arabian producers in one of the key markets –

Europe. However, the Kingdom’s cash-rich producers can take an inorganic growth route to

geographically expand their production and marketing base.

Figure 13 Planned expansions based on shale gas

Company Capacity

(mn tons)

Downstream product range Location Start-up

New Crackers

Chevron Phillips Chemical 1.5 HDPE, LLDPE Texas Late 2017

ExxonMobil Chemical 1.5 PE Texas Late 2016

Dow Chemical 1.5 LDPE, other PE, EPDM, elastomers, etc. Texas 2017

Sasol 1.5 LDPE, LLDPE, EO, MEG, etc. Louisiana 2017

Formosa Plastics 1.0 LDPE, MEG Texas Q1 2017

Formosa Plastics 1.2 NA Louisiana NA

Occidental Chemical/Mexichem 0.5 EDC, VCM Texas 2017

Axiall/Partner NA NA Louisiana 2018

Shell NA PE, MEG Pennsylvania 2020

Odebrecht NA PE West Virginia NA Source: ICIS, Al Rajhi Capital

Saudi Petrochemicals

Sector Petrochemicals –Industrial

Disclosures Please refer to the important disclosures at the back of this report. 6

Saudi Petrochemical Sector Integration and innovation to be key drivers

Downstream movement and advancement in product portfolio needed Saudi petrochemical producers historically have been at an advantage given their access to

cheap feedstock. However, the limited gas availability and its increasing demand have

prompted the government to stop subsidized gas allocation to new petrochemical complexes.

Consequently, the newly-commissioned projects and those in the pipeline will have to depend

on liquid feedstock. e.g. The Sadara Complex (an Aramco - Dow JV) will be the first complex

in the GCC region that will crack naphtha and use it for downstream production. Although

the liquid feedstock is offered at a sizeable discount to international market prices in Saudi

Arabia, dependence on this will expose these projects to feedstock price volatility. While gas-

based feedstock producers (who receive gas at a fixed cost) will benefit/lose on a rise/drop in

product prices, profitability of naphtha-based producers will depend on whether the rise/fall

in crude (and in turn naphtha) prices has been factored in prices of the end products.

Despite being at an advantage, only a few Saudi producers have strategically moved

downstream and created an integrated petrochemical value chain (e.g. Sipchem) while many

producers continue to engage in manufacturing basic/intermediate products, limiting margin

growth. Further, we believe most Saudi players tend to lag in terms of research &

development investments, which hold them back from introducing innovative products. With

new and highly-integrated petrochemical facilities being built on the back of the shale boom,

we believe the vertical integration and product innovation will be the key growth drivers for

Saudi petrochemical producers going forward.

Foreign investment expectations drive up valuations

Valuations expensive; higher than historical averages With exceptions of SAFCO, Sipchem and APC, which moved up marginally, all other

petrochemical stocks under coverage had posted negative returns during January to March

2015 period. However, the news of opening up of the market to foreign investors boosted

investor sentiments resulting in a double-digit surge in stock prices (viz. APC: +35% QTD,

SABIC: +28.7%, Yansab: +27.6%) of most of the stocks pushing up valuations. Petrochemical

sector is considered to be among the core sectors in which a major portion of foreign capital

is expected to come as the industry benefits from strong government support primarily in the

form of allocation of subsidized feedstock.

Currently, Saudi Petrochemical Index (17.4x, 2015E) trades at a premium to the broader

TASI (16.4x) and largely in line to its global peer sector indices – the MSCI World Chemical

Index (17.8x) and the S&P500 Chemical Index (17.9x). We found that Saudi Petrochemical

Index trades at a premium to its historic average (12-month blended forward P/E over the

last five years) of 16.6x, indicating expensive valuations.

We analyzed the stocks under our coverage and found their performance similar to that of the

Petrochemical Index. We also found that prices of petrochemical stocks under our coverage

are above one standard deviation of historic expected P/E, indicating valuations are

stretched. Below, we chart examples of SABIC and Yansab, whose price movement has

crossed the upper P/E band as the stocks jumped in the last couple of weeks following the

finalization of date of opening up of Tadawul.

Saudi Petrochemicals

Sector Petrochemicals –Industrial

Disclosures Please refer to the important disclosures at the back of this report. 7

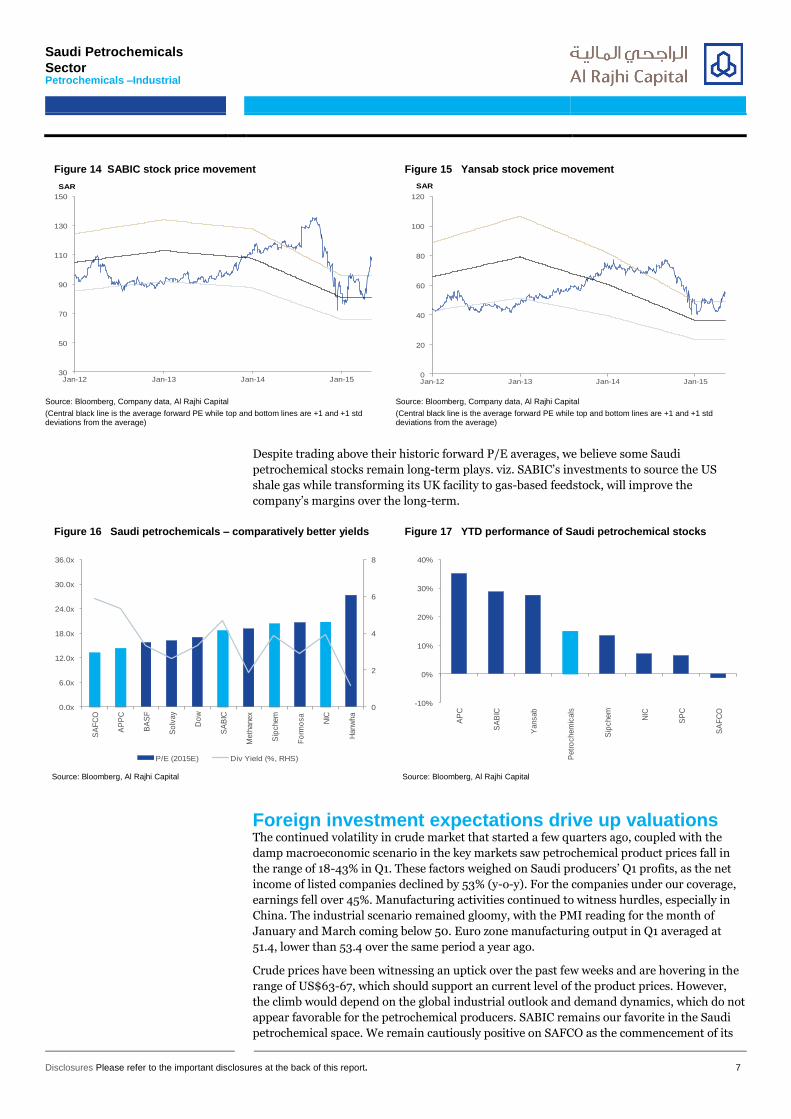

Figure 14 SABIC stock price movement Figure 15 Yansab stock price movement

30

50

70

90

110

130

150

Jan-12 Jan-13 Jan-14 Jan-15

SAR

0

20

40

60

80

100

120

Jan-12 Jan-13 Jan-14 Jan-15

SAR

Source: Bloomberg, Company data, Al Rajhi Capital

(Central black line is the average forward PE while top and bottom lines are +1 and +1 std deviations from the average)

Source: Bloomberg, Company data, Al Rajhi Capital

(Central black line is the average forward PE while top and bottom lines are +1 and +1 std deviations from the average)

Despite trading above their historic forward P/E averages, we believe some Saudi

petrochemical stocks remain long-term plays. viz. SABIC’s investments to source the US

shale gas while transforming its UK facility to gas-based feedstock, will improve the

company’s margins over the long-term.

Figure 16 Saudi petrochemicals – comparatively better yields Figure 17 YTD performance of Saudi petrochemical stocks

0

2

4

6

8

0.0x

6.0x

12.0x

18.0x

24.0x

30.0x

36.0x

SA

FC

O

AP

PC

BA

SF

So

lvay

Do

w

SA

BIC

Meth

anex

Sip

chem

Fo

rmo

sa

NIC

Hanw

ha

P/E (2015E) Div Yield (%, RHS)

-10%

0%

10%

20%

30%

40%

AP

C

SA

BIC

Yansab

Petr

ochem

icals

Sip

chem

NIC

SP

C

SA

FC

O

Source: Bloomberg, Al Rajhi Capital Source: Bloomberg, Al Rajhi Capital

Foreign investment expectations drive up valuations The continued volatility in crude market that started a few quarters ago, coupled with the

damp macroeconomic scenario in the key markets saw petrochemical product prices fall in

the range of 18-43% in Q1. These factors weighed on Saudi producers’ Q1 profits, as the net

income of listed companies declined by 53% (y-o-y). For the companies under our coverage,

earnings fell over 45%. Manufacturing activities continued to witness hurdles, especially in

China. The industrial scenario remained gloomy, with the PMI reading for the month of

January and March coming below 50. Euro zone manufacturing output in Q1 averaged at

51.4, lower than 53.4 over the same period a year ago.

Crude prices have been witnessing an uptick over the past few weeks and are hovering in the

range of US$63-67, which should support an current level of the product prices. However,

the climb would depend on the global industrial outlook and demand dynamics, which do not

appear favorable for the petrochemical producers. SABIC remains our favorite in the Saudi

petrochemical space. We remain cautiously positive on SAFCO as the commencement of its

Saudi Petrochemicals

Sector Petrochemicals –Industrial

Disclosures Please refer to the important disclosures at the back of this report. 8

fifth unit should trigger earnings growth although lower urea prices will pose hurdles. We are

Neutral on rest of the companies for now. The commencement of the EVA/LDPE plant

should offer earnings and margin growth for Sipchem. SPC has decided to undertake

restructuring initiatives at its Al Waha and Acrylic Acid units, which would bring in expenses

related to the same. Meanwhile, Yansab will be undertaking a prolonged shutdown, which

will impact its Q2 profits.

Figure 18 Q1 performance of petrochemical companies under coverage

SAR mn

Q1 2014 Q1 2015% change y-o-y Q1 2014 Q1 2015% change y-o-y

SABIC 49,221 35,564 -27.7% 6441.7 3934.6 -38.9%

SAFCO 1,178 962 -18.3% 842.5 590.0 -30.0%

Sipchem 917 826 -9.9% 68.7 80.6 17.4%

NIC 4,414 3,942 -10.7% 320.8 -332.5 NM

Yansab 2,318 1,717 -25.9% 555.7 285.1 -48.7%

APC 669 468 -30.1% 137.5 89.6 -34.8%

SPC 321 262 -18.4% 99.9 -49.5 NM

Total 59,038 43,741 -25.9% 8,467 4,598 -45.7%

Revenues Net income

Source: Bloomberg, Tadawul, Al Rajhi Capital

Lower earnings to impact dividends Saudi petrochemical players have witnessed a rapid growth over the past few years on the

back of strong government support and favorable business dynamics. The free cash flow

(FCF) of the companies under our coverage has risen at 27.6% CAGR (2010-2014), while the

cash positioned strengthened to SAR87.6bn at 10% CAGR. Debts have come down by a

significant volume over the same period. A shortage of feedstock in the Kingdom has

restrained organic growth, while almost none of the players have attempted to grow

inorganically at the global levels. With strong coffers, we believe petrochemical companies

would continue to dividend payouts over the near-term. However, with earnings expected to

decline in 2015, we anticipate a fall in dividend per share for most of the companies under

our coverage.

Figure 19 Robust coffers to aid dividend payment

0

15,000

30,000

45,000

60,000

75,000

0

20,000

40,000

60,000

80,000

100,000

2010 2011 2012 2013 2014

SAR mnSAR mn

Total Cash FCF (RHS)

Source: Bloomberg, Al Rajhi Capital

Saudi Petrochemicals

Sector Petrochemicals –Industrial

Disclosures Please refer to the important disclosures at the back of this report. 9

Risks Geopolitical situation may impact supply scenario: The prevailing civil war in Libya and

Iraq has been destabilizing oil production over the past few months. The cooling off scenario

may boost production, while a rise in conflict may result in lower production levels, which

may impact oil prices either ways. If the Iran nuclear deal succeeds and the embargo is taken

off, an additional supply from Iran may come in the market sharply pressurizing oil

downward.

A sharp jump/decline in oil prices: Petrochemical product prices still move largely in

tandem with crude prices despite a decline in oil-petrochemical prices correlation. A sudden

surge/drop in crude prices culminating in a high/low oil price environment will

positively/negatively impact the earnings of petrochemical companies over the coming

quarters.

Global macroeconomic scenario: Demand for petrochemical products can be positively

correlated to global economic and industrial growth. Improved industrial activities in China

and a rise in demand from end markets (Europe/Asia) can result in an uptick in

petrochemical prices, positively impacting the bottom-lines of Saudi petrochemical

companies.

Rise in feedstock prices: Saudi petrochemical companies receive ethane feedstock at highly

subsidized rates. With gas paucity looming over the Kingdom over the past few years, the

government has been mulling revision in feedstock prices. Although this seems to be a rare

event in the global oil/gas supply glut environment, a potential rise in feedstock prices will

affect the earnings of Saudi producers and also dent their margins.

Saudi Basic Industries Corp Petrochemicals – Industrial SABIC AB: Saudi Arabia

25 May 2015

Rating OVERWEIGHT

Target price SAR125.5 (22.0% upside)

Current price SAR102.5

Disclosures Please refer to the important disclosures at the back of this report. Powered by EFA Platform 10

Key themes & implications

SABIC has been battling low product prices, which have been affected by downcast crude prices. We believe this to be a strong near-term headwind, which will impact the company’s earnings and margins. However, a large project pipeline, impending shale gas investments and transformation of its Europe facility should boost earnings and margins over the medium term. Meanwhile, opening up of the Saudi stock market will act a catalyst and help in valuation expansion.

Share information

Market cap (SAR/US$) 308.6bn / 82.28bn

52-week range 72.52 - 135.5

Daily avg. volume (US$) 128mn

Shares outstanding 3,000mn

Free float (est.) 21%

Performance 1M 3M 12M

Absolute 17.5% 8.2% -13.5%

Relative to index 10.6% 4.7% -11.5%

Major Shareholder:

Public Investments Funds (PIF) 70.0%

GOSI 5.6%

Valuation

12-13A 12-14A 12-15E 12-16E

P/E (x) 12.2 13.2 18.1 16.1

P/B (x) 2.0 1.9 1.9 1.8

EV/EBITDA (x) 7.0 7.2 8.3 7.7

Dividend Yield 4.9% 5.3% 4.9% 4.9% Source: Company data, Al Rajhi Capital

Performance

72.0

76.4

80.8

85.1

89.5

93.9

98.3

102.6

107.0

66

76

86

96

106

116

126

136

146

Price Close Relative to TADAWUL FF (RHS)

-10

30

70

05/14 08/14 11/14 02/15

RS

I10

Source: Bloomberg, Company data, Al Rajhi Capital

Company summary

Established in 1976, SABIC is the largest listed company in the GCC region. The company is 70% owned by the Saudi government, providing it a solid financial and regulatory backing. SABIC has grown from producing 6mtpa of petrochemicals in the 1980s to over 60mtpa currently, and accounts for over 80% of Saudi Arabia’s petrochemical output.

SABIC Long-term value play SABIC is among the top petrochemical companies worldwide and is the largest

and most stable enterprise in the GCC region. The company has been reeling

under pressure over the past couple of quarters on account of a steep drop in

product prices and a demand sluggishness in its key markets. Further, heavy

dependence on the fixed-price ethane feedstock has dented its margins. Despite

these near-term issues, we believe SABIC is a value play over the long-term as

the company is working on trimming down feedstock costs by employing shale

gas feedstock at its European operations. Further, the opening up of the Saudi

market is expected to be a key driver for SABIC’s valuations as investors will

seek to take position in a operationally healthy, government supported mature

company. Additionally, the company’s robust balance sheet allows it to make

value-boosting investments/acquisitions. Also, SABIC’s dividend yield of ~5%

remains attractive among dividend-seeking investors. We continue with our

Overweight rating on stock and revise target price to SAR125.5 a share (earlier

SAR106.1).

Improving oil prices: Historically, SABIC’s top and bottom-line have been

closely related to oil prices. A steep decline in the crude prices over the past

couple of quarters has resulted in a trickle-down impact on product prices

impacting SABIC’s earnings. However, a recovery in oil prices on the back of a

decline in US shale production should bode well for petrochemical prices. This

should support SABIC’s earnings over the medium-term. Further, SABIC’s

improving downstream value chain should positively influence its bottom-line

over the coming years.

Figure 1 Oil and SABIC stock price movement along with SABIC’s net income

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

0

25

50

75

100

125

150

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

SAR mn

Oil Stock price Net profit (RHS)

22,030

9,074

21,529

29,24224,780

23,433

Source: Bloomberg, Company data, Al Rajhi Capital (Oil and SABIC stock price rebased to 100)

US signs shale to boost margins over medium term: Recently, SABIC

announced that it has entered into a deal with a US shale gas supplier. Although

SABIC has not disclosed any details, it stated that the company will use US shale

gas at UK-based Teesside plant. Also, the company has already began work on

modifying the ~860ktpa ethylene plant, which is expected to be ready by 2016.

While SABIC will benefit from cheaper gas (compared to European gas prices),

transitioning to a gas-fed unit will help the company garner higher profits and

improve its margins at its UK operations to a large extent. We expect SABIC to

implement this strategy at other non-Saudi plants going forward, enabling

margin expansion over the long term.

Research Department ARC Research Team

Tel +966 11 211 9370, [email protected]

SABIC Petrochemicals – Industrial 25 May 2015

Disclosures Please refer to the important disclosures at the back of this report. 11

SABIC to attract foreign investments: SABIC – Saudi Arabia’s largest company by market

cap and revenues – receives strong support from the government. The company’s widespread

geographic footprint, healthy operations, diverse product portfolio and robust balance sheet

are expected to draw investors, once the Saudi stock market opens its doors to qualified

foreign investors in June 2015. We believe opening up of Tadawul to foreign direct

investment would be a key catalyst for SABIC’s valuation expansion.

Healthy yield for dividend-seeking investors: SABIC’s strong coffers (cash of ~SAR80bn

as of Q1 2015) cushions the blow of any uncertain intermittent performance and enables it to

pay dividends on a regular basis. The company paid dividends of SAR5 a share in both

FY2012 and FY2013 (payout: ~60%), and increased DPS to SAR5.5 in FY2014 (payout:

~70%). However, we expect SABIC to decrease DPS to SAR5 in 2015 (payout: ~90%) on

account of lower earnings y-o-y due to weak petrochemical prices and sluggish demand. This

translates to a healthy dividend yield of 4.9% at current prices.

Valuation: SABIC’s currently trades at a forward P/E of 18.1x, in line with that of the MSCI

World Chemical Index (17.8x) and S&P500 Chemical Index (17.9x) . However, given the

project the company’s investment plans, project pipeline and the opening up of the market,

we believe the company is a long-term value play despite near-term headwinds. Using the

blended methodology of weighted average of DCF and Relative Valuation, we arrive at a

target price of SAR125.5 a share. Given the upside, we have an Overweight rating on the

company.

Risks

1. SABIC’s performance depends significantly on petrochemical product prices, which in turn

depend on crude prices. A sudden surge/decline in oil prices will impact product prices

resulting in higher/lower-than expected earnings.

2. In a bid to expand inorganically, SABIC may make high-cost acquisitions, which could

dilute its EPS.

SABIC Petrochemicals – Industrial 25 May 2015

Disclosures Please refer to the important disclosures at the back of this report. 12

Income Statement (SARmn) 12-12A 12-13A 12-14A 12-15E 12-16E

Revenue 189,026 189,038 188,899 156,535 170,078

Cost of Goods Sold (134,701) (133,729) (136,375) (113,096) (122,456)

Gross Profit 54,325 55,310 52,524 43,438 47,622

Government Charges

S.G. & A. Costs (13,390) (12,719) (13,615) (10,957) (11,905)

Operating EBIT 40,935 42,591 38,909 32,481 35,716

Cash Operating Costs (134,677) (132,416) (135,213) (109,005) (119,540)

EBITDA 54,348 56,622 53,686 47,530 50,538

Depreciation and Amortisation (13,413) (14,031) (14,777) (15,049) (14,822)

Operating Profit 40,935 42,591 38,909 32,481 35,716

Net financing income/(costs) (113) (200) 540 531 461

Forex and Related Gains

Provisions - - - - -

Other Income

Other Expenses - - - - -

Net Profit Before Taxes 40,822 42,391 39,449 33,012 36,177

Taxes (2,500) (2,300) (2,100) (1,750) (1,917)

Minority Interests (13,542) (14,863) (13,915) (14,205) (15,101)

Net profit available to shareholders 24,780 25,228 23,433 17,057 19,159

Dividends (15,000) (15,000) (16,500) (15,000) (14,996)

Transfer to Capital Reserve

12-12A 12-13A 12-14A 12-15E 12-16E

Adjusted Shares Out (mn) 3,000 3,000 3,000 3,000 3,000

CFPS (SAR) 17.24 18.04 17.38 15.44 16.36

EPS (SAR) 8.26 8.41 7.81 5.69 6.39

DPS (SAR) 5.00 5.00 5.50 5.00 5.00

Growth 12-12A 12-13A 12-14A 12-15E 12-16E

Revenue Growth -0.5% 0.0% -0.1% -17.1% 8.7%

Gross Profit Growth -12.6% 1.8% -5.0% -17.3% 9.6%

EBITDA Growth -10.4% 4.2% -5.2% -11.5% 6.3%

Operating Profit Growth -16.2% 4.0% -8.6% -16.5% 10.0%

Net Profit Growth -15.3% 1.8% -7.1% -27.2% 12.3%

EPS Growth -15.3% 1.8% -7.1% -27.2% 12.3%

Margins 12-12A 12-13A 12-14A 12-15E 12-16E

Gross profit margin 28.7% 29.3% 27.8% 27.8% 28.0%

EBITDA margin 28.8% 30.0% 28.4% 30.4% 29.7%

Operating Margin 21.7% 22.5% 20.6% 20.8% 21.0%

Pretax profit margin 21.6% 22.4% 20.9% 21.1% 21.3%

Net profit margin 13.1% 13.3% 12.4% 10.9% 11.3%

Other Ratios 12-12A 12-13A 12-14A 12-15E 12-16E

ROCE 14.1% 14.4% 13.1% 10.7% 11.6%

ROIC 16.5% 17.7% 17.8% 14.9% 15.6%

ROE 17.3% 16.6% 14.7% 10.4% 11.5%

Effective Tax Rate 6.1% 5.4% 5.3% 5.3% 5.3%

Capex/Sales 5.7% 6.2% 8.3% 8.0% 8.0%

Dividend Payout Ratio 60.5% 59.5% 70.4% 87.9% 78.3%

Valuation Measures 12-12A 12-13A 12-14A 12-15E 12-16E

P/E (x) 12.5 12.2 13.2 18.1 16.1

P/CF (x) 6.0 5.7 5.9 6.7 6.3

P/B (x) 2.1 2.0 1.9 1.9 1.8

EV/Sales (x) 2.3 2.1 2.0 2.5 2.3

EV/EBITDA (x) 8.0 7.0 7.2 8.3 7.7

EV/EBIT (x) 10.6 9.3 9.9 12.2 10.9

EV/IC (x) 1.9 1.9 1.9 1.8 1.8

Dividend Yield 4.9% 4.9% 5.3% 4.9% 4.9% Source: Company data, Al Rajhi Capital

SABIC Petrochemicals – Industrial 25 May 2015

Disclosures Please refer to the important disclosures at the back of this report. 13

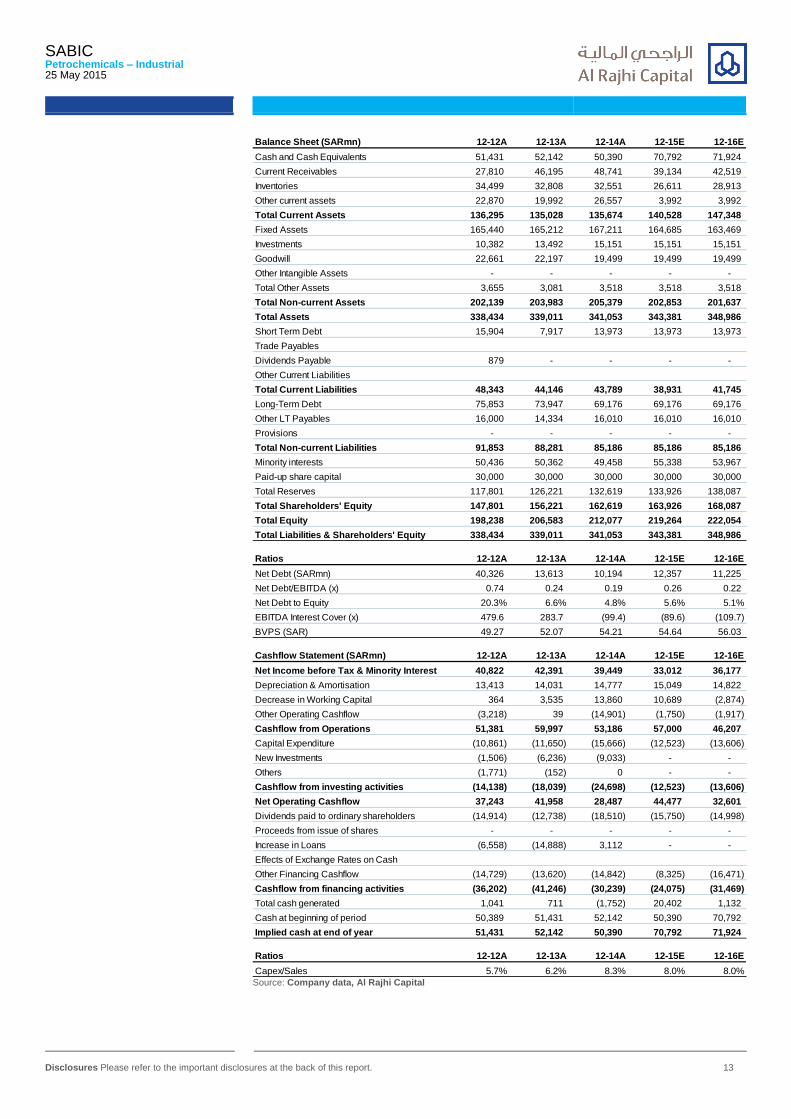

Balance Sheet (SARmn) 12-12A 12-13A 12-14A 12-15E 12-16E

Cash and Cash Equivalents 51,431 52,142 50,390 70,792 71,924

Current Receivables 27,810 46,195 48,741 39,134 42,519

Inventories 34,499 32,808 32,551 26,611 28,913

Other current assets 22,870 19,992 26,557 3,992 3,992

Total Current Assets 136,295 135,028 135,674 140,528 147,348

Fixed Assets 165,440 165,212 167,211 164,685 163,469

Investments 10,382 13,492 15,151 15,151 15,151

Goodwill 22,661 22,197 19,499 19,499 19,499

Other Intangible Assets - - - - -

Total Other Assets 3,655 3,081 3,518 3,518 3,518

Total Non-current Assets 202,139 203,983 205,379 202,853 201,637

Total Assets 338,434 339,011 341,053 343,381 348,986

Short Term Debt 15,904 7,917 13,973 13,973 13,973

Trade Payables

Dividends Payable 879 - - - -

Other Current Liabilities

Total Current Liabilities 48,343 44,146 43,789 38,931 41,745

Long-Term Debt 75,853 73,947 69,176 69,176 69,176

Other LT Payables 16,000 14,334 16,010 16,010 16,010

Provisions - - - - -

Total Non-current Liabilities 91,853 88,281 85,186 85,186 85,186

Minority interests 50,436 50,362 49,458 55,338 53,967

Paid-up share capital 30,000 30,000 30,000 30,000 30,000

Total Reserves 117,801 126,221 132,619 133,926 138,087

Total Shareholders' Equity 147,801 156,221 162,619 163,926 168,087

Total Equity 198,238 206,583 212,077 219,264 222,054

Total Liabilities & Shareholders' Equity 338,434 339,011 341,053 343,381 348,986

Ratios 12-12A 12-13A 12-14A 12-15E 12-16E

Net Debt (SARmn) 40,326 13,613 10,194 12,357 11,225

Net Debt/EBITDA (x) 0.74 0.24 0.19 0.26 0.22

Net Debt to Equity 20.3% 6.6% 4.8% 5.6% 5.1%

EBITDA Interest Cover (x) 479.6 283.7 (99.4) (89.6) (109.7)

BVPS (SAR) 49.27 52.07 54.21 54.64 56.03

Cashflow Statement (SARmn) 12-12A 12-13A 12-14A 12-15E 12-16E

Net Income before Tax & Minority Interest 40,822 42,391 39,449 33,012 36,177

Depreciation & Amortisation 13,413 14,031 14,777 15,049 14,822

Decrease in Working Capital 364 3,535 13,860 10,689 (2,874)

Other Operating Cashflow (3,218) 39 (14,901) (1,750) (1,917)

Cashflow from Operations 51,381 59,997 53,186 57,000 46,207

Capital Expenditure (10,861) (11,650) (15,666) (12,523) (13,606)

New Investments (1,506) (6,236) (9,033) - -

Others (1,771) (152) 0 - -

Cashflow from investing activities (14,138) (18,039) (24,698) (12,523) (13,606)

Net Operating Cashflow 37,243 41,958 28,487 44,477 32,601

Dividends paid to ordinary shareholders (14,914) (12,738) (18,510) (15,750) (14,998)

Proceeds from issue of shares - - - - -

Increase in Loans (6,558) (14,888) 3,112 - -

Effects of Exchange Rates on Cash

Other Financing Cashflow (14,729) (13,620) (14,842) (8,325) (16,471)

Cashflow from financing activities (36,202) (41,246) (30,239) (24,075) (31,469)

Total cash generated 1,041 711 (1,752) 20,402 1,132

Cash at beginning of period 50,389 51,431 52,142 50,390 70,792

Implied cash at end of year 51,431 52,142 50,390 70,792 71,924

Ratios 12-12A 12-13A 12-14A 12-15E 12-16E

Capex/Sales 5.7% 6.2% 8.3% 8.0% 8.0% Source: Company data, Al Rajhi Capital

SAFCO Petrochemicals – Industrial SAFCO AB: Saudi Arabia

25 May 2015

Rating NEUTRAL

Target price SAR127.4 (7.7% upside)

Current price SAR118.3

Disclosures Please refer to the important disclosures at the back of this report. Powered by EFA Platform 14

Key themes & implications

SAFCO strongly benefits from subsidized gas feedstock and geographic proximity to its customers. However, multiple delays at its SAFCO-V project and depressed urea prices are key concerns, that will impact its 2015 earnings. We revise our target price and rating based on the Q1 earnings and recent news flow.

Share information

Market cap (SAR/US$) 49.28bn / 13.14bn

52-week range 103.6 - 135.2

Daily avg. volume (US$) 17.7mn

Shares outstanding 416.7mn

Free float (est.) 32%

Performance 1M 3M 12M

Absolute 2% -2.9% -8.9%

Relative to index -4.9% -6.4% -6.9%

Major Shareholder:

SABIC 42.9%

GOSI 17.1%

Valuation

12-13A 12-14A 12-15E 12-16E

P/E (x) 12.5 12.4 13.3 10.5

P/B (x) 4.8 5.0 4.6 4.0

EV/EBITDA (x) 9.5 9.6 10.2 8.0

Dividend Yield 10.1% 5.9% 5.9% 5.9% Source: Company data, Al Rajhi Capital

Performance

87.0

90.1

93.3

96.4

99.5

102.6

105.8

108.9

112.0

100.0

105.0

110.0

115.0

120.0

125.0

130.0

135.0

140.0

Price Close Relative to TADAWUL FF (RHS)

-10

30

70

05/14 08/14 11/14 02/15

RS

I10

Source: Bloomberg, Company data, Al Rajhi Capital

Company summary

SAFCO is the Kingdom’s first petrochemical company. The company started commercial production in 1970. Today, SAFCO is ranked among the largest urea fertilizer producers in the world. The company has a combined capacity of ~5mtpa for the production of ammonia, urea and other derivatives. With the SAFCO-V unit expected to commence in Q3 2015, the company’s total production capacity is expected to increase by another 2.2mtpa.

SAFCO Muted urea prices, delays – key overhangs SAFCO, with total running capacities of ~5mtpa of ammonia and urea, is one

of the world’s leading ammonia fertilizer companies. Healthy operations,

stable demand for its products and a strong support from its parent company

SABIC have helped the company grow and become a debt-free company.

However, over the past few quarters, SAFCO has been facing product price

pressure, especially on account of a liberal export tax policy by China, which

has flooded the market with excess fertilizers. New capacities coming on

stream over the next few months will further exert a downward pressure on

prices. Also, SAFCO has delayed beginning of commercial operations at its fifth

unit (SAFCO-V) multiple times, which has added uncertainty. We believe these

factors to be key overhangs on SAFCO’s earnings over the next few quarters

and this might affect dividend payout as seen in 2015. We remain cautious on

SAFCO and revise our earnings and dividends estimates. We revise our rating

on the company to Neutral (from Overweight) with a target price of SAR127.4

a share (earlier SAR135.8).

SAFCO-V commencement delayed again: Despite SAFCO-V beginning trial

operations in December 2014, the commercial commencement of the plant has

been delayed twice. Recently, SAFCO announced that it has further deferred the

commencement till June-end. Due to the late beginning, SAFCO would lose on

additional volumes that it could otherwise have supplied to its Asian customers

during the monsoon season that coincides with Q3, thereby impacting the

company’s 2015 earnings. We expect SAFCO-V to contribute to margin

expansion only in 2016 once initial glitches are sorted out and the plant’s

operations streamline.

China’s fertilizer tax policy to be a dampener: For 2015, China introduced a

constant export tax on urea as against the seasonally varying rates that existed in

2014. The export tax will be flat CNY80/ton (US$13/ton) in 2015 vs. CNY40/ton

from July-October and CNY40/t +15% (of urea prices FOB) for the remainder of

2014. We believe that lower tariff will result in higher urea export volumes,

which will keep urea prices under pressure in 2015.

Urea prices to moderate: Urea prices have under pressure on account of high

export volumes from China. Average urea prices in Q2 2015 (till date) stood at

US$275 a ton (vs. US$343 in Q1, US$320 in Q2 2014). This will negatively

impact SAFCO’s Q2 earnings. Although we expect urea prices to climb in Q3

2015 on account of higher seasonal demand, we anticipate prices to be lower y-

o-y on the back of increased supply from China and new projects coming online

(600ktpa in Asia and over 3.1mtpa in North Africa).

Dividend yield may not be as attractive as earlier: SAFCO is known for

doling out handsome dividend payments. However, this was not the case in

2014, when the company decided to reduce DPS to SAR7 (SAR5.6 based on

revised number of shares), down from SAR12 (SAR9.6) a year earlier, citing

funding of SAFCO-V. With works at SAFCO-V complete we expect SAFCO to

raise DPS in 2015 to SAR7 (based on revised number of shares). At current price

levels, this translates to a dividend yield of 5.9%. Although attractive, this is

sharply lower than the yield of over 7-8% SAFCO offered a few quarters ago.

Research Department ARC Research Team

Tel +966 11 211 9370, [email protected]

SAFCO Petrochemicals – Industrial 25 May 2015

Disclosures Please refer to the important disclosures at the back of this report. 15

Valuation: Using blended methodology of weighted average of DCF and Relative Valuation,

we arrive at a target price of SAR127.4 vs. earlier SAR135.8 a share (based on revised number

of shares). With limited upside potential, we revise our rating to Neutral (earlier Overweight).

Risks

1. An unexpectedly higher/lower supply from China could create a supply glut/erode supply

in the market strongly influence urea prices, impacting earnings.

2. A change in monsoon pattern can affect urea demand and hurt SAFCO’s bottom-line.

SAFCO Petrochemicals – Industrial 25 May 2015

Disclosures Please refer to the important disclosures at the back of this report. 16

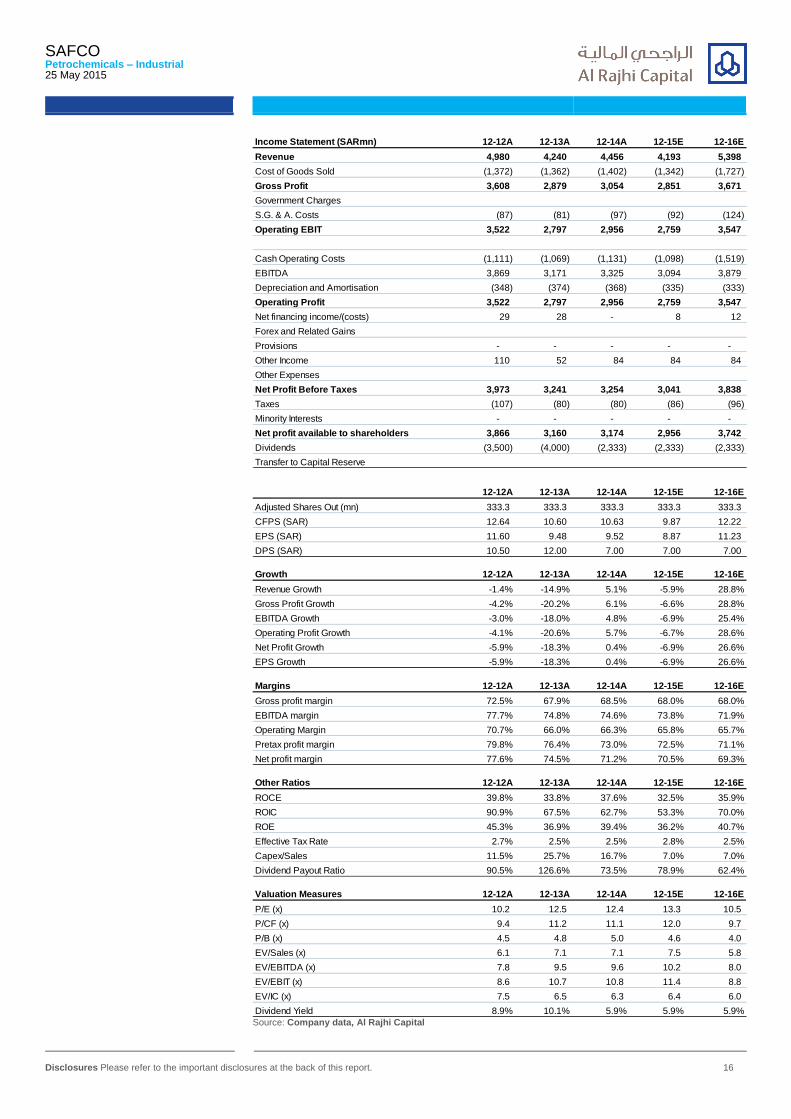

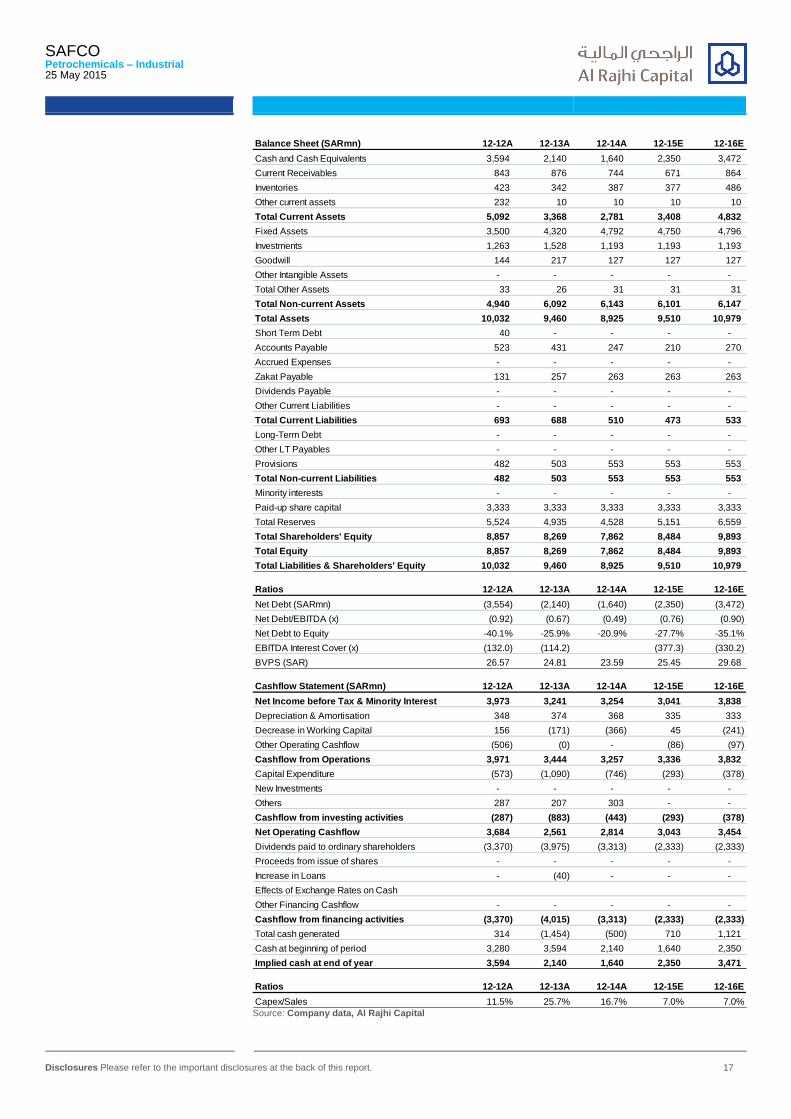

Income Statement (SARmn) 12-12A 12-13A 12-14A 12-15E 12-16E

Revenue 4,980 4,240 4,456 4,193 5,398

Cost of Goods Sold (1,372) (1,362) (1,402) (1,342) (1,727)

Gross Profit 3,608 2,879 3,054 2,851 3,671

Government Charges

S.G. & A. Costs (87) (81) (97) (92) (124)

Operating EBIT 3,522 2,797 2,956 2,759 3,547

Cash Operating Costs (1,111) (1,069) (1,131) (1,098) (1,519)

EBITDA 3,869 3,171 3,325 3,094 3,879

Depreciation and Amortisation (348) (374) (368) (335) (333)

Operating Profit 3,522 2,797 2,956 2,759 3,547

Net financing income/(costs) 29 28 - 8 12

Forex and Related Gains

Provisions - - - - -

Other Income 110 52 84 84 84

Other Expenses

Net Profit Before Taxes 3,973 3,241 3,254 3,041 3,838

Taxes (107) (80) (80) (86) (96)

Minority Interests - - - - -

Net profit available to shareholders 3,866 3,160 3,174 2,956 3,742

Dividends (3,500) (4,000) (2,333) (2,333) (2,333)

Transfer to Capital Reserve

12-12A 12-13A 12-14A 12-15E 12-16E

Adjusted Shares Out (mn) 333.3 333.3 333.3 333.3 333.3

CFPS (SAR) 12.64 10.60 10.63 9.87 12.22

EPS (SAR) 11.60 9.48 9.52 8.87 11.23

DPS (SAR) 10.50 12.00 7.00 7.00 7.00

Growth 12-12A 12-13A 12-14A 12-15E 12-16E

Revenue Growth -1.4% -14.9% 5.1% -5.9% 28.8%

Gross Profit Growth -4.2% -20.2% 6.1% -6.6% 28.8%

EBITDA Growth -3.0% -18.0% 4.8% -6.9% 25.4%

Operating Profit Growth -4.1% -20.6% 5.7% -6.7% 28.6%

Net Profit Growth -5.9% -18.3% 0.4% -6.9% 26.6%

EPS Growth -5.9% -18.3% 0.4% -6.9% 26.6%

Margins 12-12A 12-13A 12-14A 12-15E 12-16E

Gross profit margin 72.5% 67.9% 68.5% 68.0% 68.0%

EBITDA margin 77.7% 74.8% 74.6% 73.8% 71.9%

Operating Margin 70.7% 66.0% 66.3% 65.8% 65.7%

Pretax profit margin 79.8% 76.4% 73.0% 72.5% 71.1%

Net profit margin 77.6% 74.5% 71.2% 70.5% 69.3%

Other Ratios 12-12A 12-13A 12-14A 12-15E 12-16E

ROCE 39.8% 33.8% 37.6% 32.5% 35.9%

ROIC 90.9% 67.5% 62.7% 53.3% 70.0%

ROE 45.3% 36.9% 39.4% 36.2% 40.7%

Effective Tax Rate 2.7% 2.5% 2.5% 2.8% 2.5%

Capex/Sales 11.5% 25.7% 16.7% 7.0% 7.0%

Dividend Payout Ratio 90.5% 126.6% 73.5% 78.9% 62.4%

Valuation Measures 12-12A 12-13A 12-14A 12-15E 12-16E

P/E (x) 10.2 12.5 12.4 13.3 10.5

P/CF (x) 9.4 11.2 11.1 12.0 9.7

P/B (x) 4.5 4.8 5.0 4.6 4.0

EV/Sales (x) 6.1 7.1 7.1 7.5 5.8

EV/EBITDA (x) 7.8 9.5 9.6 10.2 8.0

EV/EBIT (x) 8.6 10.7 10.8 11.4 8.8

EV/IC (x) 7.5 6.5 6.3 6.4 6.0

Dividend Yield 8.9% 10.1% 5.9% 5.9% 5.9% Source: Company data, Al Rajhi Capital

SAFCO Petrochemicals – Industrial 25 May 2015

Disclosures Please refer to the important disclosures at the back of this report. 17

Balance Sheet (SARmn) 12-12A 12-13A 12-14A 12-15E 12-16E

Cash and Cash Equivalents 3,594 2,140 1,640 2,350 3,472

Current Receivables 843 876 744 671 864

Inventories 423 342 387 377 486

Other current assets 232 10 10 10 10

Total Current Assets 5,092 3,368 2,781 3,408 4,832

Fixed Assets 3,500 4,320 4,792 4,750 4,796

Investments 1,263 1,528 1,193 1,193 1,193

Goodwill 144 217 127 127 127

Other Intangible Assets - - - - -

Total Other Assets 33 26 31 31 31

Total Non-current Assets 4,940 6,092 6,143 6,101 6,147

Total Assets 10,032 9,460 8,925 9,510 10,979

Short Term Debt 40 - - - -

Accounts Payable 523 431 247 210 270

Accrued Expenses - - - - -

Zakat Payable 131 257 263 263 263

Dividends Payable - - - - -

Other Current Liabilities - - - - -

Total Current Liabilities 693 688 510 473 533

Long-Term Debt - - - - -

Other LT Payables - - - - -

Provisions 482 503 553 553 553

Total Non-current Liabilities 482 503 553 553 553

Minority interests - - - - -

Paid-up share capital 3,333 3,333 3,333 3,333 3,333

Total Reserves 5,524 4,935 4,528 5,151 6,559

Total Shareholders' Equity 8,857 8,269 7,862 8,484 9,893

Total Equity 8,857 8,269 7,862 8,484 9,893

Total Liabilities & Shareholders' Equity 10,032 9,460 8,925 9,510 10,979

Ratios 12-12A 12-13A 12-14A 12-15E 12-16E

Net Debt (SARmn) (3,554) (2,140) (1,640) (2,350) (3,472)

Net Debt/EBITDA (x) (0.92) (0.67) (0.49) (0.76) (0.90)

Net Debt to Equity -40.1% -25.9% -20.9% -27.7% -35.1%

EBITDA Interest Cover (x) (132.0) (114.2) (377.3) (330.2)

BVPS (SAR) 26.57 24.81 23.59 25.45 29.68

Cashflow Statement (SARmn) 12-12A 12-13A 12-14A 12-15E 12-16E

Net Income before Tax & Minority Interest 3,973 3,241 3,254 3,041 3,838

Depreciation & Amortisation 348 374 368 335 333

Decrease in Working Capital 156 (171) (366) 45 (241)

Other Operating Cashflow (506) (0) - (86) (97)

Cashflow from Operations 3,971 3,444 3,257 3,336 3,832

Capital Expenditure (573) (1,090) (746) (293) (378)

New Investments - - - - -

Others 287 207 303 - -

Cashflow from investing activities (287) (883) (443) (293) (378)

Net Operating Cashflow 3,684 2,561 2,814 3,043 3,454

Dividends paid to ordinary shareholders (3,370) (3,975) (3,313) (2,333) (2,333)

Proceeds from issue of shares - - - - -

Increase in Loans - (40) - - -

Effects of Exchange Rates on Cash

Other Financing Cashflow - - - - -

Cashflow from financing activities (3,370) (4,015) (3,313) (2,333) (2,333)

Total cash generated 314 (1,454) (500) 710 1,121

Cash at beginning of period 3,280 3,594 2,140 1,640 2,350

Implied cash at end of year 3,594 2,140 1,640 2,350 3,471

Ratios 12-12A 12-13A 12-14A 12-15E 12-16E

Capex/Sales 11.5% 25.7% 16.7% 7.0% 7.0% Source: Company data, Al Rajhi Capital

Sipchem Petrochemicals – Industrial SIPCHEM AB: Saudi Arabia

25 May 2015

Rating NEUTRAL

Target price SAR34.3 (5.9% upside)

Current price SAR32.4

Disclosures Please refer to the important disclosures at the back of this report. Powered by EFA Platform 18

Key themes & implications

Sipchem has successfully completed its Phase III project with the commencement of the EVA/LDPE plant. The company’s vertically integrated operations provide an opportunity for margin expansion; however, a full effect would only be seen after a few quarters. The recently-announced shutdown at its two plants will be a drag although a jump in methanol prices should relieve some pressure.

Share information

Market cap (SAR/US$) 11.89bn / 3.170bn

52-week range 22.80 - 43.26

Daily avg. volume (US$) 4.9mn

Shares outstanding 366.7mn

Free float (est.) 90%

Performance 1M 3M 12M

Absolute 13.4% 10.2% 7.9%

Relative to index 6.5% 6.7% 9.9%

Major Shareholder:

Al-Zamil Group Holding Co. 9.7%

Ikarus Petroleum Holding 8.2%

Valuation

12-13A 12-14A 12-15E 12-16E

P/E (x) 19.2 19.6 20.3 16.0

P/B (x) 2.1 2.0 1.9 1.9

EV/EBITDA (x) 11.8 12.3 11.4 10.4

Dividend Yield 3.9% 3.9% 3.9% 4.6% Source: Company data, Al Rajhi Capital

Performance

88.0

98.0

108.0

118.0

128.0

138.0

20.0

25.0

30.0

35.0

40.0

45.0

Price Close Relative to TADAWUL FF (RHS)

-10

30

70

05/14 08/14 11/14 02/15

RS

I10

Source: Bloomberg, Company data, Al Rajhi Capital

Company summary

Established in 1999, Sipchem produces methanol as well as other petrochemical intermediaries and derivatives, which are used across various industries. The company’s marketing subsidiary sells the produce along with other products. In 2011, Sipchem had acquired Aectra SA, which offers marketing and logistic support in the European markets.

Sipchem Integration yet to yield positive results Sipchem is among the Kingdom’s few integrated petrochemical producers with

a significant presence in the downstream value chain. The commencement of

the company’s Phase III - EA/BA plants in 2013 and EVA/LDPE plant in Q2

2015 should further boost its earnings despite a weak pricing environment in

Q1 and a shutdown in Q2. However, the entire effect of downstream

integration will take a couple of more quarters to reflect on Sipchem’s bottom-

line. After multiple shutdowns in 2014 we expect the company to operate at the

normal levels in 2015. Further, we expect Sipchem’s free cash flow to increase

on the back of a revival in the methanol prices and on completion of its planned

projects. This should enable the company maintain a DPS similar to 2014. We

continue to remain Neutral on the stock although we have revised our target

price to SAR34.3 (earlier SAR28.8) a share.

New units to improve earnings going forward: Sipchem has moved

downstream forming a vertically integrated petrochemical chain over the past

few years. With the recent commencement of the EVA/LDPE unit, Sipchem has

successfully completed its ambitious Phase III project. The company’s PBT

project is also expected to commence in H2 2015. These new facilities will

bolster product volumes helping Sipchem’s earnings grow over the medium to

long term.

Earnings revision: Weak methanol prices in Q1 and maintenance shutdown at

its EA (26 days) and carbon monoxide (20 days) plants in Q2 2015 are key drags

on the bottom-line while a healthy and sustained uptick in the methanol prices

in Q2 remains a key positive. Given this scenario, we have revised Sipchem’s

2015E net income marginally to SAR586.5mn (vs. SAR594mn earlier). We

expect Sipchem’s operating and net margins to get a boost in 2016, once the

downstream EVA/LDPE plant comes begins operations full throttle.

A healthy free cash flow to support dividends: Sipchem has spent a total of

over SAR4.6bn on capex over the last three years, a large portion of which has

now fructified in the form of the commencement of the remaining Phase III

units. Further, the PBT project is also on the verge of completion and would not

need large capex. Given this scenario, we expect a robust free cash flow of over

SAR1.15bn in 2015. Sipchem’s dividend payout stands in the range of ~70-80%

and we expect this trend to continue. We anticipate a 2015E DPS of SAR1.25,

which at translates into a modest dividend yield of 3.9% at current prices.

Valuation: Sipchem is trading at a P/E of 20.3x (2015E), a premium over Saudi

Petrochemical Index and MSCI World Chemical Index. Based on our blended

methodology involving the weighted average of DCF and Relative Valuation, we

have arrived at a target price of SAR34.3 for Sipchem. With an upside of ~6%

over the current price, we continue with a Neutral rating on the company.

Risks

1. A slower/faster-than expected production ramp-up at its new facilities are key

downside/upside risk.

2. Sipchem is an integrated petrochemical player. Any technical glitches in the

upstream set-up can have a trickledown effect on downstream production.

3. Methanol prices play a key role in Sipchem’s profitability. A steep decline/

surge in the prices will drag/lift the company’s profitability.

Research Department ARC Research Team

Tel +966 11 211 9370, [email protected]

Sipchem Petrochemicals – Industrial 25 May 2015

Disclosures Please refer to the important disclosures at the back of this report. 19

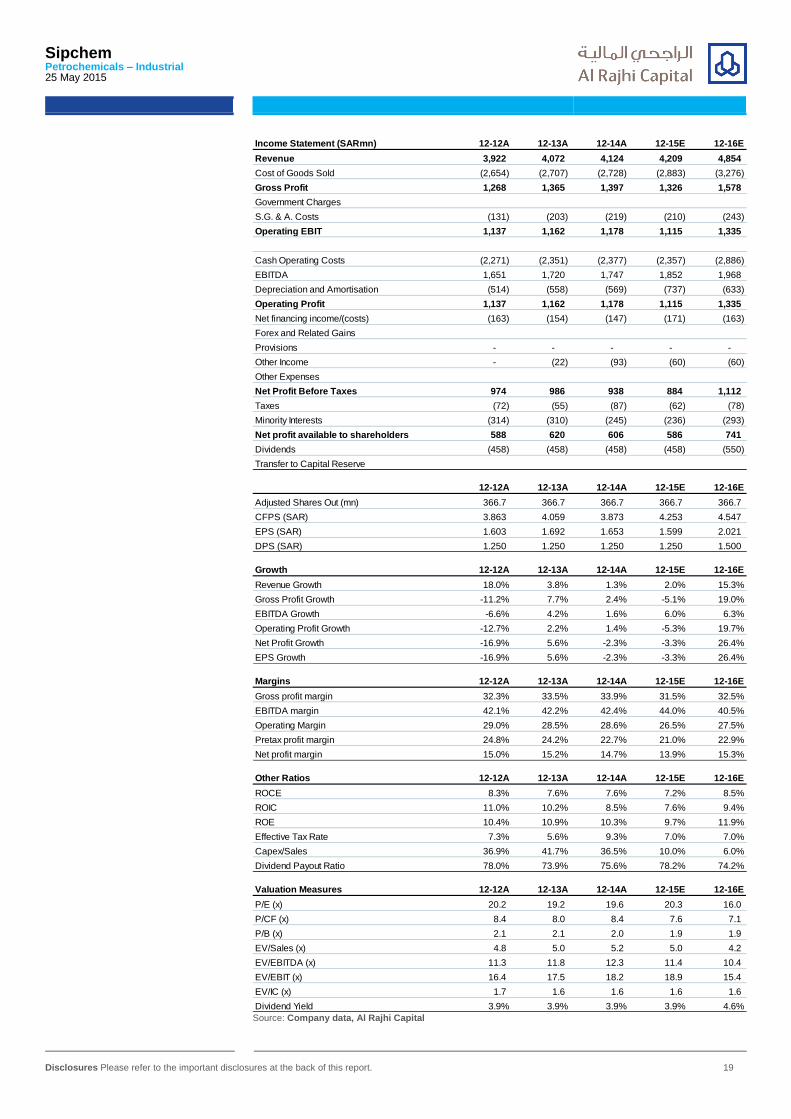

Income Statement (SARmn) 12-12A 12-13A 12-14A 12-15E 12-16E

Revenue 3,922 4,072 4,124 4,209 4,854

Cost of Goods Sold (2,654) (2,707) (2,728) (2,883) (3,276)

Gross Profit 1,268 1,365 1,397 1,326 1,578

Government Charges

S.G. & A. Costs (131) (203) (219) (210) (243)

Operating EBIT 1,137 1,162 1,178 1,115 1,335

Cash Operating Costs (2,271) (2,351) (2,377) (2,357) (2,886)

EBITDA 1,651 1,720 1,747 1,852 1,968

Depreciation and Amortisation (514) (558) (569) (737) (633)

Operating Profit 1,137 1,162 1,178 1,115 1,335

Net financing income/(costs) (163) (154) (147) (171) (163)

Forex and Related Gains

Provisions - - - - -

Other Income - (22) (93) (60) (60)

Other Expenses

Net Profit Before Taxes 974 986 938 884 1,112

Taxes (72) (55) (87) (62) (78)

Minority Interests (314) (310) (245) (236) (293)

Net profit available to shareholders 588 620 606 586 741

Dividends (458) (458) (458) (458) (550)

Transfer to Capital Reserve

12-12A 12-13A 12-14A 12-15E 12-16E

Adjusted Shares Out (mn) 366.7 366.7 366.7 366.7 366.7

CFPS (SAR) 3.863 4.059 3.873 4.253 4.547

EPS (SAR) 1.603 1.692 1.653 1.599 2.021

DPS (SAR) 1.250 1.250 1.250 1.250 1.500

Growth 12-12A 12-13A 12-14A 12-15E 12-16E

Revenue Growth 18.0% 3.8% 1.3% 2.0% 15.3%

Gross Profit Growth -11.2% 7.7% 2.4% -5.1% 19.0%

EBITDA Growth -6.6% 4.2% 1.6% 6.0% 6.3%

Operating Profit Growth -12.7% 2.2% 1.4% -5.3% 19.7%

Net Profit Growth -16.9% 5.6% -2.3% -3.3% 26.4%

EPS Growth -16.9% 5.6% -2.3% -3.3% 26.4%

Margins 12-12A 12-13A 12-14A 12-15E 12-16E

Gross profit margin 32.3% 33.5% 33.9% 31.5% 32.5%

EBITDA margin 42.1% 42.2% 42.4% 44.0% 40.5%

Operating Margin 29.0% 28.5% 28.6% 26.5% 27.5%

Pretax profit margin 24.8% 24.2% 22.7% 21.0% 22.9%

Net profit margin 15.0% 15.2% 14.7% 13.9% 15.3%

Other Ratios 12-12A 12-13A 12-14A 12-15E 12-16E

ROCE 8.3% 7.6% 7.6% 7.2% 8.5%

ROIC 11.0% 10.2% 8.5% 7.6% 9.4%

ROE 10.4% 10.9% 10.3% 9.7% 11.9%

Effective Tax Rate 7.3% 5.6% 9.3% 7.0% 7.0%

Capex/Sales 36.9% 41.7% 36.5% 10.0% 6.0%

Dividend Payout Ratio 78.0% 73.9% 75.6% 78.2% 74.2%

Valuation Measures 12-12A 12-13A 12-14A 12-15E 12-16E

P/E (x) 20.2 19.2 19.6 20.3 16.0

P/CF (x) 8.4 8.0 8.4 7.6 7.1

P/B (x) 2.1 2.1 2.0 1.9 1.9

EV/Sales (x) 4.8 5.0 5.2 5.0 4.2

EV/EBITDA (x) 11.3 11.8 12.3 11.4 10.4

EV/EBIT (x) 16.4 17.5 18.2 18.9 15.4

EV/IC (x) 1.7 1.6 1.6 1.6 1.6

Dividend Yield 3.9% 3.9% 3.9% 3.9% 4.6% Source: Company data, Al Rajhi Capital

Sipchem Petrochemicals – Industrial 25 May 2015

Disclosures Please refer to the important disclosures at the back of this report. 20

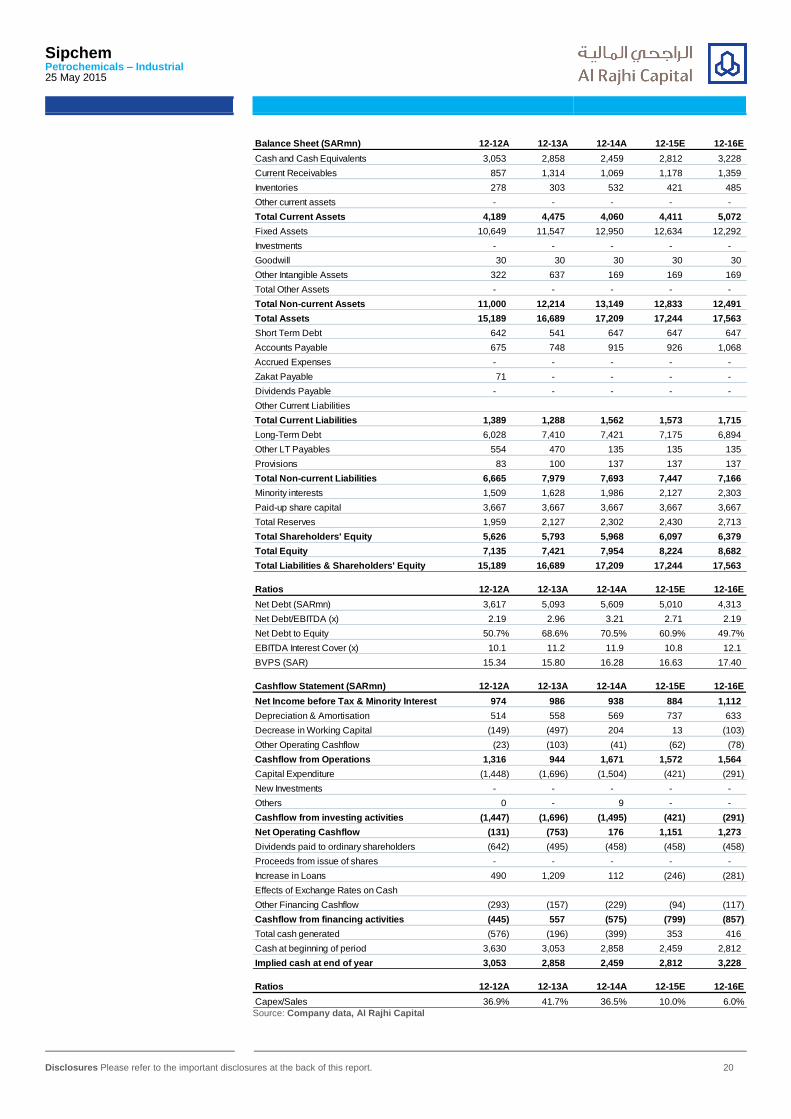

Balance Sheet (SARmn) 12-12A 12-13A 12-14A 12-15E 12-16E

Cash and Cash Equivalents 3,053 2,858 2,459 2,812 3,228

Current Receivables 857 1,314 1,069 1,178 1,359

Inventories 278 303 532 421 485

Other current assets - - - - -

Total Current Assets 4,189 4,475 4,060 4,411 5,072

Fixed Assets 10,649 11,547 12,950 12,634 12,292

Investments - - - - -

Goodwill 30 30 30 30 30

Other Intangible Assets 322 637 169 169 169

Total Other Assets - - - - -

Total Non-current Assets 11,000 12,214 13,149 12,833 12,491

Total Assets 15,189 16,689 17,209 17,244 17,563

Short Term Debt 642 541 647 647 647

Accounts Payable 675 748 915 926 1,068

Accrued Expenses - - - - -

Zakat Payable 71 - - - -

Dividends Payable - - - - -

Other Current Liabilities

Total Current Liabilities 1,389 1,288 1,562 1,573 1,715

Long-Term Debt 6,028 7,410 7,421 7,175 6,894

Other LT Payables 554 470 135 135 135

Provisions 83 100 137 137 137

Total Non-current Liabilities 6,665 7,979 7,693 7,447 7,166

Minority interests 1,509 1,628 1,986 2,127 2,303

Paid-up share capital 3,667 3,667 3,667 3,667 3,667

Total Reserves 1,959 2,127 2,302 2,430 2,713

Total Shareholders' Equity 5,626 5,793 5,968 6,097 6,379

Total Equity 7,135 7,421 7,954 8,224 8,682

Total Liabilities & Shareholders' Equity 15,189 16,689 17,209 17,244 17,563

Ratios 12-12A 12-13A 12-14A 12-15E 12-16E

Net Debt (SARmn) 3,617 5,093 5,609 5,010 4,313

Net Debt/EBITDA (x) 2.19 2.96 3.21 2.71 2.19

Net Debt to Equity 50.7% 68.6% 70.5% 60.9% 49.7%

EBITDA Interest Cover (x) 10.1 11.2 11.9 10.8 12.1

BVPS (SAR) 15.34 15.80 16.28 16.63 17.40

Cashflow Statement (SARmn) 12-12A 12-13A 12-14A 12-15E 12-16E

Net Income before Tax & Minority Interest 974 986 938 884 1,112

Depreciation & Amortisation 514 558 569 737 633

Decrease in Working Capital (149) (497) 204 13 (103)

Other Operating Cashflow (23) (103) (41) (62) (78)

Cashflow from Operations 1,316 944 1,671 1,572 1,564

Capital Expenditure (1,448) (1,696) (1,504) (421) (291)

New Investments - - - - -

Others 0 - 9 - -

Cashflow from investing activities (1,447) (1,696) (1,495) (421) (291)

Net Operating Cashflow (131) (753) 176 1,151 1,273

Dividends paid to ordinary shareholders (642) (495) (458) (458) (458)

Proceeds from issue of shares - - - - -

Increase in Loans 490 1,209 112 (246) (281)

Effects of Exchange Rates on Cash

Other Financing Cashflow (293) (157) (229) (94) (117)

Cashflow from financing activities (445) 557 (575) (799) (857)

Total cash generated (576) (196) (399) 353 416

Cash at beginning of period 3,630 3,053 2,858 2,459 2,812

Implied cash at end of year 3,053 2,858 2,459 2,812 3,228

Ratios 12-12A 12-13A 12-14A 12-15E 12-16E

Capex/Sales 36.9% 41.7% 36.5% 10.0% 6.0% Source: Company data, Al Rajhi Capital

NIC Diversified Operations – Industrial NIC AB: Saudi Arabia

25 May 2015

Rating NEUTRAL

Target price SAR26.3 (5.5% upside)

Current price SAR24.9

Disclosures Please refer to the important disclosures at the back of this report. Powered by EFA Platform 21

Key themes & implications

NIC despite its diversified operations, continues to remain under pressure due to the fall in product prices and the downcast TiO2 market. Additionally, the newly-commenced Acrylic Acid project is yet to gain full traction, while there is no clarity on the commencement of the ilmenite processing unit. Consequently, we have revised our earnings, dividends and target price downward.

Share information

Market cap (SAR/US$) 16.68bn / 4.447bn

52-week range 21.56 - 40.10

Daily avg. volume (US$) 26.4mn

Shares outstanding 668.9mn

Free float (est.) 87%

Performance 1M 3M 12M

Absolute 8.4% -11.9% -21.6%

Relative to index 1.5% -15.4% -19.6%

Major Shareholder:

GOSI 8.7%

Al Shair Co. for Trading 8.0%

Valuation

12-13A 12-14A 12-15E 12-16E

P/E (x) 12.2 14.7 20.7 15.5

P/B (x) 1.4 1.4 1.4 1.4

EV/EBITDA (x) 9.5 10.2 10.0 9.1

Dividend Yield 6.0% 4.0% 4.0% 5.0% Source: Company data, Al Rajhi Capital

Performance

73.0

82.0

91.0

100.0

109.0

118.0

19.0

24.0

29.0

34.0

39.0

44.0

Price Close Relative to TADAWUL FF (RHS)

-10

30

70

05/14 08/14 11/14 02/15

RS

I10

Source: Bloomberg, Company data, Al Rajhi Capital

Company summary

NIC is the first Saudi company that is fully owned by the private sector. NIC is the world’s second-largest and the Middle East’s only TiO2 producer. The company’s TiO2 is mainly used by the paints industry. NIC also produces basic petrochemicals (total capacity of ~3.3mtpa). NIC’s acrylic acid unit had commenced operations in July 2014.

NIC Reeling under dual pressure NIC’s presence in the petrochemicals and TiO2 segments has provided cushion

from the product price volatility. However, a steep decline in petrochemical

prices coupled with the sluggish TiO2 market has hurt the company’s 2014

performance. In Q1 2015, NIC is expected to continue facing pressure in both

the segments due to the drop in petrochemical prices and a muted TiO2

scenario. Additionally, the company had to bear losses on account of negative

valuation of risk-hedging derivatives, which led to a net loss in Q1. The

company stated that the much-awaited ilmenite processing unit will begin in

H2 2015, although we believe it will take a couple of quarters after

commencement to run at optimal levels. Meanwhile, the Acrylic Acid unit,

which had commenced operations in Q3 2014, is yet to gain traction. Given this

scenario, we have reduced our earnings and DPS estimates for 2015. We have

revised our target price downward to SAR26.3 (earlier SAR28.3) and retained

our Neutral rating on the stock.

Petrochemical prices revive, but lower y-o-y: NIC derives ~60% of its

revenues (before eliminations) from the petrochemical segment, which is

engaged in the production of basic olefins. Given the recent rise in oil price, we

expect the petrochemical segment to perform well sequentially going forward;

however, y-o-y performance will be negative in 2015. The commencement of the

downstream Acrylic Acid facility should offer some respite although considering

the Q1 results, we believe the project is yet to gain traction.

Weak TiO2 fundamentals: TiO2 prices, have been under pressure over the past

few quarters. In Q4 2014, Huntsman had announced that it will be closing one of

its Europe-based TiO2 facilities (100 ktpa) indicating the weak demand

environment. Despite the closure, we do not expect TiO2 prices to move up

given the fact that its key market – Europe – continues to be mired with weak

demand. We expect TiO2 prices to remain be lower 5-8% sequentially and 15-

18% y-o-y impacting NIC’s profits.

Change in estimates: Factoring in the conditions, net losses in Q1 and

expectations for the year ahead, we have revised our 2015 earnings estimates

down to SAR803.8mn (from SAR1.11bn). We have also revised downward our

dividend estimates to SAR1 a share, in line with the 2014 DPS. At current price

level, this translates into a modest 4% dividend yield.

Valuation: NIC trades at 20.7x its 2015E EPS, a premium over its Saudi and

international peer-group averages. With the changes in our estimates, we have

revised our target price down to SAR26.3 (from SAR28.3). With limited upside,

we have retained our Neutral rating on the stock.

Risks

1. A longer-than-expected delay in the commencement of the ilmenite unit will

impact the company’s margins. Similarly, a slower ramp-up of its Acrylic Acid

plants would further hurt its earnings.

2. Europe and the US are the key TiO2 markets. A sudden slowdown in the US

and/or further deterioration of the macroeconomic conditions in Europe will

further drag down the performance of the TiO2 segment.

Research Department ARC Research Team

Tel +966 11 211 9370, [email protected]

NIC Diversified Operations – Industrial 25 May 2015

Disclosures Please refer to the important disclosures at the back of this report. 22

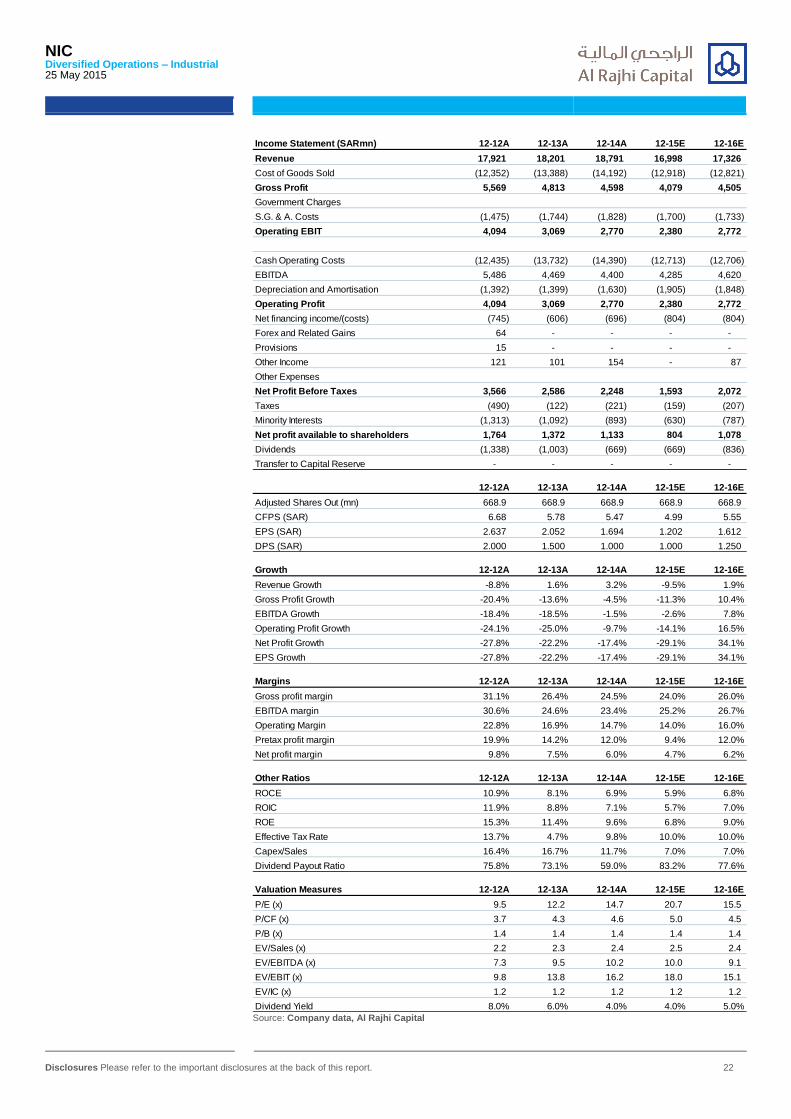

Income Statement (SARmn) 12-12A 12-13A 12-14A 12-15E 12-16E

Revenue 17,921 18,201 18,791 16,998 17,326

Cost of Goods Sold (12,352) (13,388) (14,192) (12,918) (12,821)

Gross Profit 5,569 4,813 4,598 4,079 4,505

Government Charges

S.G. & A. Costs (1,475) (1,744) (1,828) (1,700) (1,733)