Saudi Economic Perspectives - AlAhli · Saudi Economic Perspectives 2014 ... from the heydays of...

19

Saudi Economic Perspectives 2014 - 2015 Growth Moderation on the Horizon

Transcript of Saudi Economic Perspectives - AlAhli · Saudi Economic Perspectives 2014 ... from the heydays of...

1

Saudi Economic Perspectives

2014 - 2015

Growth Moderation on the Horizon

Contents

Executive Summary 1

2014 and 2015 Projections 2

1. Global Economic Developments 3

2. Saudi Economic Develpments and Outlook 8

2.1 Real sector 8

2.2 Fiscal and External Balances 11

2.3 Monetary Developments 13

2.4 Financial Sector 15

2.5 Risks 17

Said A. Al ShaikhGroup Chief Economist

Authors

Tamer El ZayatSenior Economist/Editor

Majed A. Al-GhalibSenior Economist

[email protected] Sources: SAMA and NCB

Growth Moderation on the Horizon

• The world economy will continue to experience a multi-stage growth, given thedivergenteconomicoutlooksfortheadvancedandemergingcountries,aninflectionfromtheheydaysofthecrisiswhentheemergingeconomieswerethelocomotiveforgrowth.Thedeviationon interest ratesbetweentheemergingeconomiesandtheirdevelopedcounterparts is expected towiden, in contrast to2008and2009wherebyaccommodativepolicieswereadoptedacrosstheboard.TheInternationalMonetaryFund(IMF)projectshigherglobalgrowthin2014and2015at3.6%and3.9%,respectively,yetbelowthe5.1%registeredin2010.

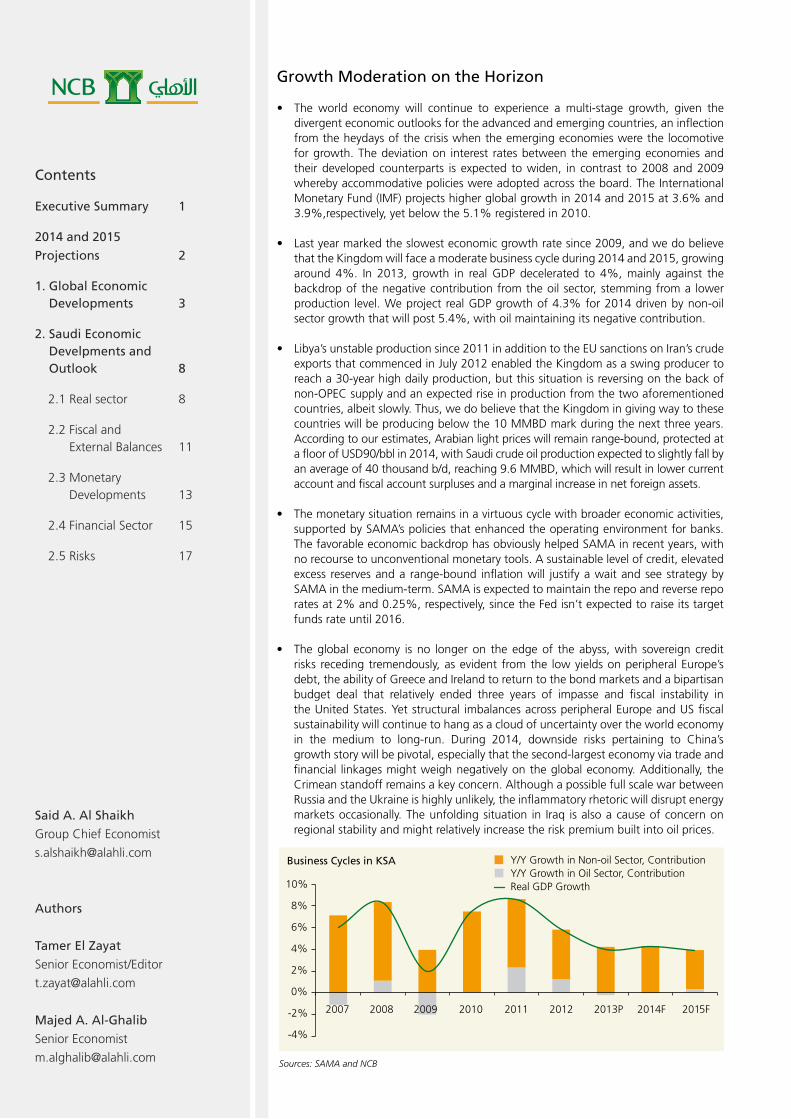

• Lastyearmarkedtheslowesteconomicgrowthratesince2009,andwedobelievethattheKingdomwillfaceamoderatebusinesscycleduring2014and2015,growingaround 4%. In 2013, growth in realGDP decelerated to 4%,mainly against thebackdropofthenegativecontributionfromtheoilsector,stemmingfroma lowerproduction level.WeprojectrealGDPgrowthof4.3%for2014drivenbynon-oilsectorgrowththatwillpost5.4%,withoilmaintainingitsnegativecontribution.

• Libya’sunstableproductionsince2011inadditiontotheEUsanctionsonIran’scrudeexportsthatcommencedinJuly2012enabledtheKingdomasaswingproducertoreacha30-yearhighdailyproduction,butthissituationisreversingonthebackofnon-OPECsupplyandanexpectedriseinproductionfromthetwoaforementionedcountries,albeitslowly.Thus,wedobelievethattheKingdomingivingwaytothesecountrieswillbeproducingbelowthe10MMBDmarkduringthenextthreeyears.Accordingtoourestimates,Arabianlightpriceswillremainrange-bound,protectedatafloorofUSD90/bblin2014,withSaudicrudeoilproductionexpectedtoslightlyfallbyanaverageof40thousandb/d,reaching9.6MMBD,whichwillresultinlowercurrentaccount and fiscal account surpluses and a marginal increase in net foreign assets.

• Themonetarysituationremainsinavirtuouscyclewithbroadereconomicactivities,supportedbySAMA’spoliciesthatenhancedtheoperatingenvironmentforbanks.ThefavorableeconomicbackdrophasobviouslyhelpedSAMAinrecentyears,withnorecoursetounconventionalmonetarytools.Asustainablelevelofcredit,elevatedexcess reservesanda range-bound inflationwill justifyawaitandseestrategybySAMAinthemedium-term.SAMAisexpectedtomaintaintherepoandreversereporatesat2%and0.25%,respectively,sincetheFedisn’texpectedtoraiseitstargetfundsrateuntil2016.

• Theglobal economy isno longeron theedgeof theabyss,with sovereign creditrisks recedingtremendously,asevident fromthe lowyieldsonperipheralEurope’sdebt,theabilityofGreeceandIrelandtoreturntothebondmarketsandabipartisanbudget deal that relatively ended three years of impasse and fiscal instability in theUnitedStates.Yetstructural imbalancesacrossperipheralEuropeandUSfiscalsustainabilitywillcontinuetohangasacloudofuncertaintyovertheworldeconomyin the medium to long-run. During 2014, downside risks pertaining to China’sgrowthstorywillbepivotal,especiallythatthesecond-largesteconomyviatradeandfinancial linkagesmightweighnegativelyontheglobaleconomy.Additionally,theCrimeanstandoffremainsakeyconcern.AlthoughapossiblefullscalewarbetweenRussiaandtheUkraineishighlyunlikely,theinflammatoryrhetoricwilldisruptenergymarketsoccasionally.Theunfoldingsituation in Iraq isalsoacauseofconcernonregional stability and might relatively increase the risk premium built into oil prices.

Y/Y Growth in Non-oil Sector, ContributionY/Y Growth in Oil Sector, ContributionReal GDP Growth

-4%

-2%

0%

2%

4%

6%

8%

10%

2008 2009 2010 2011 2012 2013P 2014F 2015F

Business Cycles in KSA

2007

2

Real Sector

WeightedAverageKSACrudeSpotPrice,ArabLight,USD/BBL 77.6 108.1 110.2 106.4 102.0 100.0 105.6 5M14

AverageDailyCrudeOilProduction,MMBD 8.2 9.3 9.8 9.6 9.6 9.7 9.7 5M14

GDPatCurrentMarketPrices,SARbillion 1,975.5 2,510.7 2,752.3 2,806.7 2,877.08 2,902.8 - -

GDPatCurrentMarketPrices,USDbillion 526.8 670.4 734.9 749.4 768.2 775.1 - -

RealGDPGrowthRate 7.4% 8.6% 5.8% 4.0% 4.3% 3.9% - -

OilSectorGDPGrowthRate 0.3% 11.0% 5.7% -1.0% -0.2% 1.7% - -

Non-oilSectorGDPGrowthRate 9.6% 8.0% 5.8% 5.4% 5.4% 4.5% - -

Population,million 27.6 28.4 29.2 30.0 30.7 31.4 - -

PopulationGrowthRate 3.4% 2.9% 2.9% 2.7% 2.5% 2.0% - -

GDP/Capita,USD 19,112.7 23,625.3 25,172.6 24,986.4 25,533.7 25,264.5 - -

CPIInflation,Y/Y%Change,Average 3.8% 3.7% 2.9% 3.5% 3.0% 3.2% 2.7% May-14

External Sector

MerchandiseTradeBalance,USDbillion 153.7 244.7 246.6 222.7 206.1 197.7 - -

OilExports,USDbillion 215.2 317.6 341.6 324.9 303.1 294.6 - -

Non-oilExports,USDbillion 35.9 47.1 51.0 54.1 57.7 60.3 - -

MerchandiseImports,USDbillion (96.7) (119.0) (140.7) (152.0) (154.7) (157.2) - -

InvisiblesTradeBalance,USDbillion (87.0) (86.2) (81.8) (90.1) (82.6) (83.6) - -

NetFactorIncome,USDbillion 7.0 9.7 11.0 10.8 11.4 13 - -

NetUnilateralTransfers,USDbillion (27.9) (29.4) (30.4) (35.9) (38.7) (40) - -

CurrentAccountBalance,USDbillion 66.8 158.5 164.8 132.6 123.5 114.1 - -

CurrentAccountBalance/GDP 12.7% 23.6% 22.4% 17.7% 15.7% 14.4% - -

NetForeignAssetswithSAMA,USDbillion 441.0 535.9 648.5 717.7 753.6 791.3 729.6 Apr-14

Fiscal Sector (Central Government)

BudgetedExpenditure,SARbillion 540.0 580.0 690.0 820.0 855.0 914.9 - -

ActualRevenues,SARbillion 741.6 1117.8 1247.4 1156.4 1089.7 1066.0 - -

ActualExpenditure,SARbillion 653.9 826.7 873.3 976.0 1005.3 1035.5 - -

ExpenditureOverrun,% 21.1% 42.5% 26.6% 19.0% 17.6% 13.2% - -

TotalRevenues/GDP 37.5% 44.5% 45.3% 41.2% 37.1% 35.9% - -

TotalExpenditure/GDP 33.1% 32.9% 31.7% 34.8% 34.2% 34.9% - -

OverallBudgetBalance,SARbillion 87.7 291.1 374.1 180.3 84.4 30.6 - -

BudgetBalance/GDP 4.4% 11.6% 13.6% 6.4% 2.9% 1.0% - -

Break-EvenOilPrice 64.1 75.3 73.9 82.6 87.1 90.1 - -

Financial Sector

USD/SARExchangeRate 3.75 3.75 3.75 3.75 3.75 3.75 3.75 Apr-14

GrowthinBroadMoney(M3) 5.0% 13.3% 13.9% 10.9% 11.7% 9.5% 13.3% Apr-14

GrowthinCredittothePrivateSector 4.8% 11.0% 16.4% 12.1% 11.4% 11.0% 12.0% Apr-14

Average3MSARDepositRate 0.7% 0.7% 0.9% 1.0% 0.9% 1.2% 1.0% 4M14

Average3MUSDDepositRate 0.3% 0.3% 0.4% 0.3% 0.3% 0.5% 0.3% 4M14

Spread,inBasisPoints,SAIBOR-LIBOR 39.8 40.9 55.2 68.7 60.0 70.0 69.4 4M14

2014 and 2015 Projections

Ourmacroeconomicprojectionsarebasedonanaveragecrudeoilprice(ArabianLight)ofUSD102/bblandanaveragedailycrudeoilproductionlevelof9.6MMBD(outofwhich77%isexported)in2014.Thedecreaseinoilrevenueswillweighnegativelyonthefiscalandcurrentaccountsurplusesthatwillfallinpercentagetermsto2.9%and15.7%outofGDP,respectively.RealGDPgrowthisexpectedtoriseby4.3%,duemainlytoanexpectedgrowthinnon-oilsectorby5.4%,drivenbytheprivatesectorthatwilloffsetthenegativecontributionofoil.Thekeybeneficiariesin2014willremaintobetheconstructionandmanufacturingsectors,growingat6%and5%,respectively.Ourprojectionsforthetwosectorsaresupportedbybuoyantactivityintheprojects’marketandstrongbusinessconfidence.Lookingahead,eventhoughtheKingdommighthavedecoupledfromtherestoftheworldduringthefinancialcrisiswhetheritbeonthemacroeconomicorthebankingfront,thenextfiveyearsmightprovetobeachallengingtimeforpolicymaking.Range-boundcrudeoilpricesandreducedproductionmightmaterialize,withtheincreasedpossibilityofoversupplyfromOPECandnon-OPEC,whichwillweighnegativelyonoilrevenuesandwill reversetheheftytwinsurplusesofrecentyears.Against thisbackdrop, thegovernmentmighthave toprudentlymanage its risingexpenditureand/ordeploy the substantial net foreign assets and the unutilized debt capacity that can act as countercyclical buffers that smoothoutthebusinesscycle if itsurprisedtothedownside,anunlikelyscenario,giventheresilienceoftheSaudibankingandcorporatesectors.Yet,wearemoreinclinedtofavortheformercourseofactionthatcontainsthegrowthinexpendituresinceitwillmitigateanymediumtolong-termconcernspertainingtofiscalsustainability.

Key Macroeconomic Indicators

Sources: Reuters, SAMA and NCB

2010 2011 2012 2013P 2014F 2015F Latest Date

NCB PERSPECTIVES | JUNE 2014

3

A. Global Economic Developments

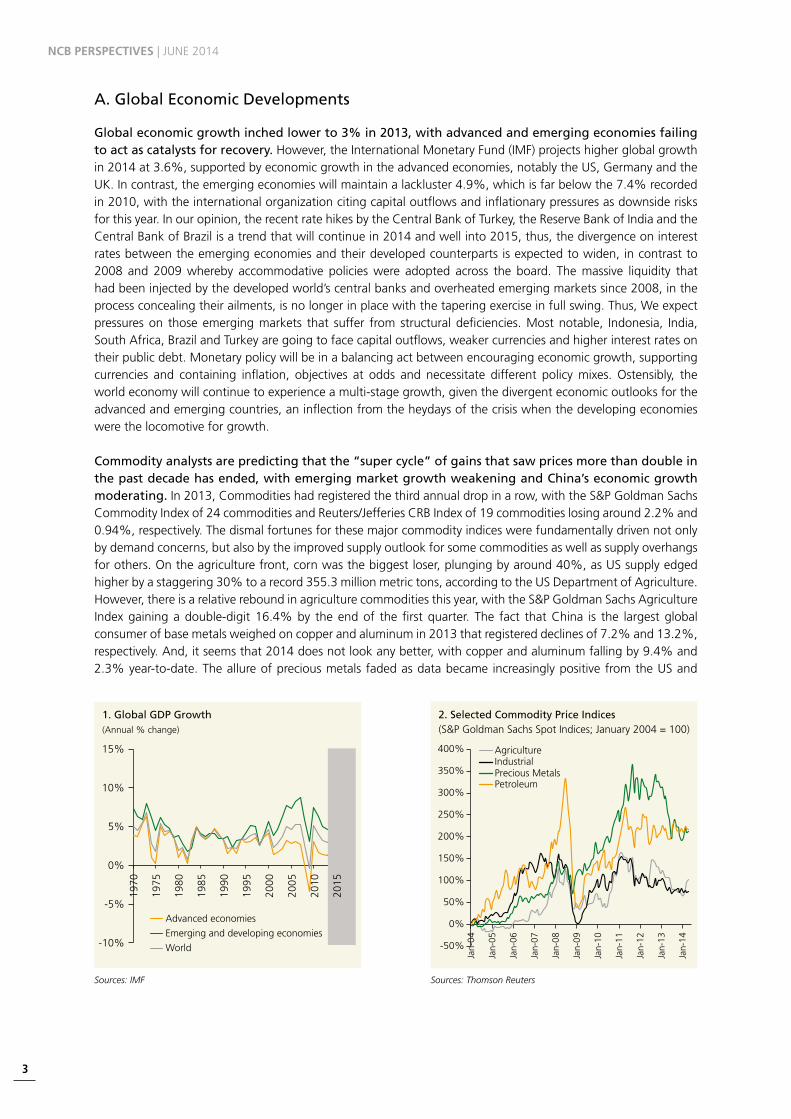

Global economic growth inched lower to 3% in 2013, with advanced and emerging economies failing to act as catalysts for recovery.However,theInternationalMonetaryFund(IMF)projectshigherglobalgrowthin2014at3.6%,supportedbyeconomicgrowthintheadvancedeconomies,notablytheUS,GermanyandtheUK.Incontrast,theemergingeconomieswillmaintainalackluster4.9%,whichisfarbelowthe7.4%recordedin2010,withtheinternationalorganizationcitingcapitaloutflowsandinflationarypressuresasdownsiderisksforthisyear.Inouropinion,therecentratehikesbytheCentralBankofTurkey,theReserveBankofIndiaandtheCentralBankofBrazilisatrendthatwillcontinuein2014andwellinto2015,thus,thedivergenceoninterestratesbetweentheemergingeconomiesandtheirdevelopedcounterpartsisexpectedtowiden,incontrastto2008 and 2009whereby accommodative policieswere adopted across the board. Themassive liquidity thathadbeeninjectedbythedevelopedworld’scentralbanksandoverheatedemergingmarketssince2008,intheprocessconcealingtheirailments,isnolongerinplacewiththetaperingexerciseinfullswing.Thus,Weexpectpressureson thoseemergingmarkets that suffer fromstructuraldeficiencies.Mostnotable, Indonesia, India,SouthAfrica,BrazilandTurkeyaregoingtofacecapitaloutflows,weakercurrenciesandhigherinterestratesontheirpublicdebt.Monetarypolicywillbeinabalancingactbetweenencouragingeconomicgrowth,supportingcurrencies and containing inflation, objectives at odds and necessitate different policymixes.Ostensibly, theworldeconomywillcontinuetoexperienceamulti-stagegrowth,giventhedivergenteconomicoutlooksfortheadvancedandemergingcountries,aninflectionfromtheheydaysofthecrisiswhenthedevelopingeconomieswerethelocomotiveforgrowth.

Commodity analysts are predicting that the “super cycle” of gains that saw prices more than double in the past decade has ended, with emerging market growth weakening and China’s economic growth moderating.In2013,Commoditieshadregisteredthethirdannualdropinarow,withtheS&PGoldmanSachsCommodityIndexof24commoditiesandReuters/JefferiesCRBIndexof19commoditieslosingaround2.2%and0.94%,respectively.Thedismalfortunesforthesemajorcommodityindiceswerefundamentallydrivennotonlybydemandconcerns,butalsobytheimprovedsupplyoutlookforsomecommoditiesaswellassupplyoverhangsforothers.Ontheagriculturefront,cornwasthebiggestloser,plungingbyaround40%,asUSsupplyedgedhigherbyastaggering30%toarecord355.3millionmetrictons,accordingtotheUSDepartmentofAgriculture.However,thereisarelativereboundinagriculturecommoditiesthisyear,withtheS&PGoldmanSachsAgricultureIndexgainingadouble-digit16.4%by theendof thefirstquarter. The fact thatChina is the largestglobalconsumerofbasemetalsweighedoncopperandaluminumin2013thatregistereddeclinesof7.2%and13.2%,respectively.And,itseemsthat2014doesnotlookanybetter,withcopperandaluminumfallingby9.4%and2.3%year-to-date.TheallureofpreciousmetalsfadedasdatabecameincreasinglypositivefromtheUSand

Sources: IMF Sources: Thomson Reuters

Advanced economies

Emerging and developing economies

World

1. Global GDP Growth(Annual % change)

-10%

-5%

0%

5%

10%

15%

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2. Selected Commodity Price Indices(S&P Goldman Sachs Spot Indices; January 2004 = 100)

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

AgricultureIndustrialPrecious MetalsPetroleum

4

Europe,withinvestorsembracingequitiesandelevatingglobalstockpricesbythehighest infouryears.GoldendedlastyeararoundUSD1,200/Ozmark,a28%annualdecline,thefirstannualdropsince2000,asinvestorswithdrewUSD38.6billionfromgoldfunds.Ontheinvestmentfront,riskaversionwasapparentfromthereducedinflowstocommodity-relatedexchange-tradedproductsthatfellbyarecordUSD88billiontoUSD332billionin2013.Lookingforwardinto2014,commoditiesmightrecoverpartofthelossesincurredlastyearduetobaseeffects,butitishighlyunlikelythatwewillwitnessanysubstantialand/orsustainablegains.

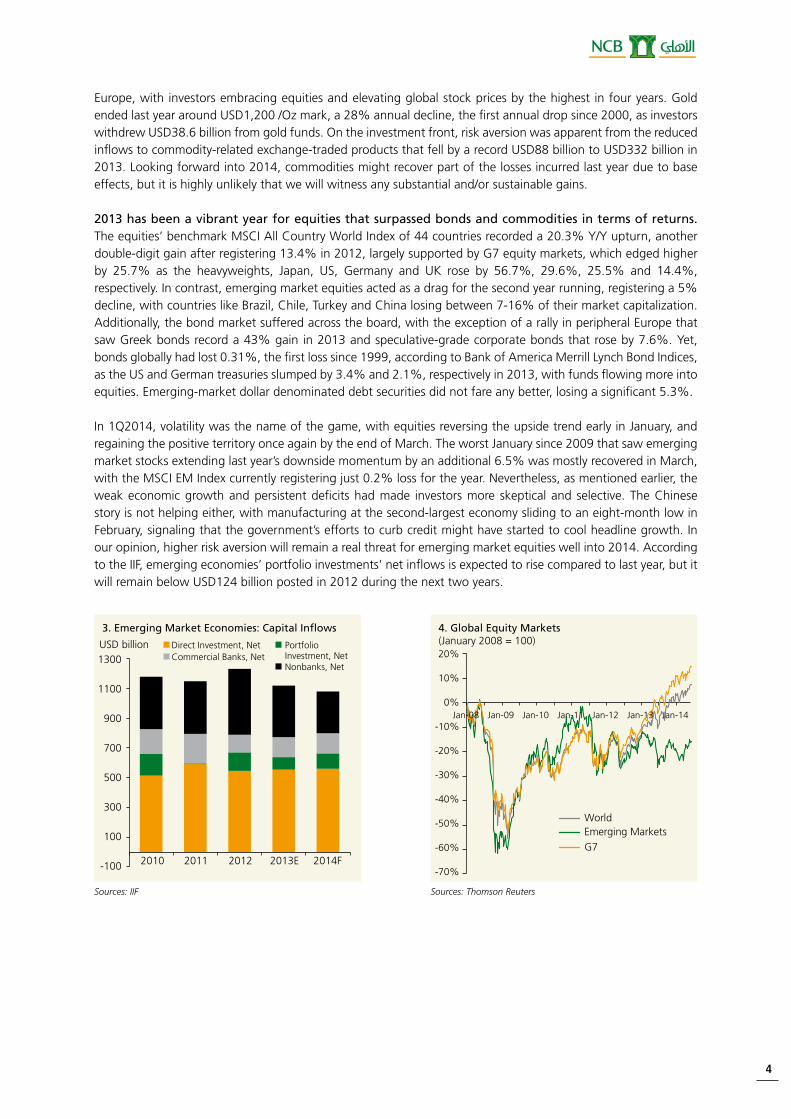

2013 has been a vibrant year for equities that surpassed bonds and commodities in terms of returns. Theequities’benchmarkMSCIAllCountryWorldIndexof44countriesrecordeda20.3%Y/Yupturn,anotherdouble-digitgainafterregistering13.4%in2012,largelysupportedbyG7equitymarkets,whichedgedhigherby 25.7% as the heavyweights, Japan, US, Germany and UK rose by 56.7%, 29.6%, 25.5% and 14.4%,respectively.Incontrast,emergingmarketequitiesactedasadragforthesecondyearrunning,registeringa5%decline,withcountrieslikeBrazil,Chile,TurkeyandChinalosingbetween7-16%oftheirmarketcapitalization.Additionally,thebondmarketsufferedacrosstheboard,withtheexceptionofarallyinperipheralEuropethatsawGreekbondsrecorda43%gainin2013andspeculative-gradecorporatebondsthatroseby7.6%.Yet,bondsgloballyhadlost0.31%,thefirstlosssince1999,accordingtoBankofAmericaMerrillLynchBondIndices,astheUSandGermantreasuriesslumpedby3.4%and2.1%,respectivelyin2013,withfundsflowingmoreintoequities.Emerging-marketdollardenominateddebtsecuritiesdidnotfareanybetter,losingasignificant5.3%.

In1Q2014,volatilitywasthenameofthegame,withequitiesreversingtheupsidetrendearlyinJanuary,andregainingthepositiveterritoryonceagainbytheendofMarch.TheworstJanuarysince2009thatsawemergingmarketstocksextendinglastyear’sdownsidemomentumbyanadditional6.5%wasmostlyrecoveredinMarch,withtheMSCIEMIndexcurrentlyregisteringjust0.2%lossfortheyear.Nevertheless,asmentionedearlier,theweakeconomicgrowthandpersistentdeficitshadmade investorsmore skepticaland selective.TheChinesestoryisnothelpingeither,withmanufacturingatthesecond-largesteconomyslidingtoaneight-monthlowinFebruary,signalingthatthegovernment’seffortstocurbcreditmighthavestartedtocoolheadlinegrowth.Inouropinion,higherriskaversionwillremainarealthreatforemergingmarketequitieswellinto2014.AccordingtotheIIF,emergingeconomies’portfolioinvestments’netinflowsisexpectedtorisecomparedtolastyear,butitwillremainbelowUSD124billionpostedin2012duringthenexttwoyears.

4. Global Equity Markets(January 2008 = 100)20%

10%

0%

-10%

-20%

-30%

-40%

-50%

-60%

-70%

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

WorldEmerging MarketsG7

3. Emerging Market Economies: Capital Inflows

2010 2011 2012 2013E 2014F

1300

1100

900

700

500

300

100

-100

USD billion Direct Investment, Net Portfolio Investment, NetCommercial Banks, NetNonbanks, Net

Sources: IIF Sources: Thomson Reuters

NCB PERSPECTIVES | JUNE 2014

5

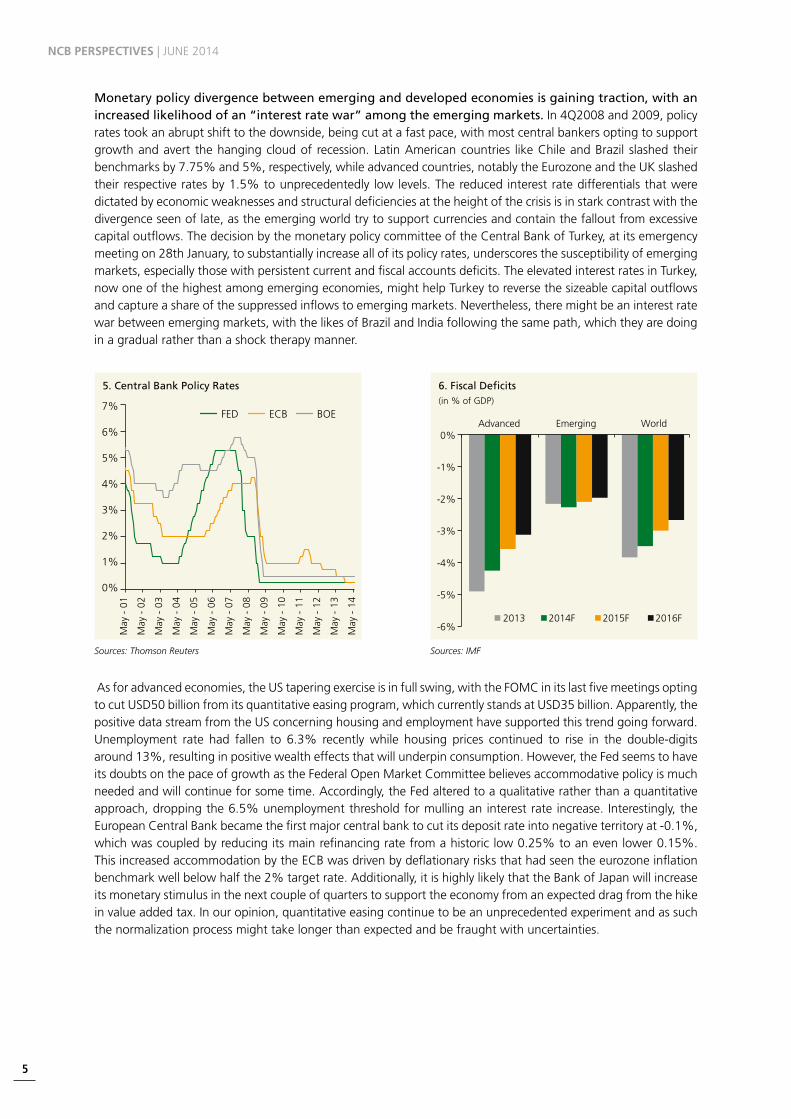

Monetary policy divergence between emerging and developed economies is gaining traction, with an increased likelihood of an “interest rate war” among the emerging markets.In4Q2008and2009,policyratestookanabruptshifttothedownside,beingcutatafastpace,withmostcentralbankersoptingtosupportgrowthandavert thehangingcloudof recession.LatinAmericancountries likeChileandBrazil slashedtheirbenchmarksby7.75%and5%,respectively,whileadvancedcountries,notablytheEurozoneandtheUKslashedtheirrespectiveratesby1.5%tounprecedentedly lowlevels.Thereducedinterestratedifferentialsthatweredictatedbyeconomicweaknessesandstructuraldeficienciesattheheightofthecrisisisinstarkcontrastwiththedivergenceseenoflate,astheemergingworldtrytosupportcurrenciesandcontainthefalloutfromexcessivecapitaloutflows.ThedecisionbythemonetarypolicycommitteeoftheCentralBankofTurkey,atitsemergencymeetingon28thJanuary,tosubstantiallyincreaseallofitspolicyrates,underscoresthesusceptibilityofemergingmarkets,especiallythosewithpersistentcurrentandfiscalaccountsdeficits.TheelevatedinterestratesinTurkey,nowoneofthehighestamongemergingeconomies,mighthelpTurkeytoreversethesizeablecapitaloutflowsandcaptureashareofthesuppressedinflowstoemergingmarkets.Nevertheless,theremightbeaninterestratewarbetweenemergingmarkets,withthelikesofBrazilandIndiafollowingthesamepath,whichtheyaredoingin a gradual rather than a shock therapy manner.

FED ECB BOE

5. Central Bank Policy Rates

7%

6%

5%

4%

3%

2%

1%

0%

May

- 0

1

May

- 0

2

May

- 0

3

May

- 0

4

May

- 0

5

May

- 0

6

May

- 0

7

May

- 0

8

May

- 0

9

May

- 1

0

May

- 1

1

May

- 1

2

May

- 1

3

May

- 1

4

6. Fiscal Deficits(in % of GDP)

0%

-1%

-2%

-3%

-4%

-5%

-6%2013 2014F 2015F 2016F

Advanced Emerging World

Sources: Thomson Reuters Sources: IMF

Asforadvancedeconomies,theUStaperingexerciseisinfullswing,withtheFOMCinitslastfivemeetingsoptingtocutUSD50billionfromitsquantitativeeasingprogram,whichcurrentlystandsatUSD35billion.Apparently,thepositivedatastreamfromtheUSconcerninghousingandemploymenthavesupportedthistrendgoingforward.Unemployment rate had fallen to 6.3% recentlywhile housing prices continued to rise in the double-digitsaround13%,resultinginpositivewealtheffectsthatwillunderpinconsumption.However,theFedseemstohaveitsdoubtsonthepaceofgrowthastheFederalOpenMarketCommitteebelievesaccommodativepolicyismuchneededandwillcontinueforsometime.Accordingly,theFedalteredtoaqualitativeratherthanaquantitativeapproach,droppingthe6.5%unemploymentthresholdformullinganinterestrateincrease. Interestingly,theEuropeanCentralBankbecamethefirstmajorcentralbanktocutitsdepositrateintonegativeterritoryat-0.1%,whichwascoupledbyreducingitsmainrefinancingratefromahistoriclow0.25%toanevenlower0.15%.ThisincreasedaccommodationbytheECBwasdrivenbydeflationaryrisksthathadseentheeurozoneinflationbenchmarkwellbelowhalfthe2%targetrate.Additionally,itishighlylikelythattheBankofJapanwillincreaseitsmonetarystimulusinthenextcoupleofquarterstosupporttheeconomyfromanexpecteddragfromthehikeinvalueaddedtax.Inouropinion,quantitativeeasingcontinuetobeanunprecedentedexperimentandassuchthenormalizationprocessmighttakelongerthanexpectedandbefraughtwithuncertainties.

6

Even though fiscal consolidation remains a priority for most countries, China and Japan might opt for fiscal stimuli in 2014. ThedisappointingeconomicindicatorsfromChinaareincreasinglypointingtowardsapossibledeviationfromthe7.5%growthtargetsetbytheStateCouncilinMarch.Asaresult,thegovernmenthasannouncedinAprilamini-stimulusthatincludesrailwayspending,expansionofcredittosmall-scaleenterprisesandextensionofcreditforpurchasingcheaphomes.Eventhough,suchmeasurescannotbecomparedtothe4trillionYuanpackageduringthefinancialcrisis,wedobelievethattheChineseauthoritieswillstepuptheireffortstosupporteconomicgrowthtoavertsocialunrest.Inouropinion,thecommunistpartydocument,whichhave been issued in November 12th and entailed plans to increase the role of consumption and market forces at theexpenseofexportsandstate-ledinvestment,isalong-termstrategythatwillnotchangethegovernment’sfixationwithshort-termgrowth.Additionally,ontheJapanesefront,theincreaseinvalueaddedtaxfrom5%to8%anditsexpecteddragontheeconomymightforcethegovernmenttocompileanotherfiscalstimuluspackagethisyear.Infact,theJapanesefinanceministryhasannouncedplanstospend40%oftheoutlaysforthefiscalyearstartingAprilin2Q2014tomitigatetheweaknessinhouseholdconsumption.However,incontrasttoChina,Japan’sfinancesareindireshapegiventhepersistenttradeandbudgetdeficits,whichwilllimitthescopeand magnitude of additional fiscal spending.

Box 1: Oil… Range-Bound Movement in 2014

Crudeoilpricesended lastyear intheredafter fourconsecutiveannual increases,withthetwobenchmarksBrentandtheArabianlightfallingby2.6%and3.5%,respectively.Thefirstannualdecline,sincethedouble-digitplungewitnessedin2009,waslargelydrivenbydemanddownsiderisksthatemanatedfromweakeningChineseeconomicdataandthepossibledragsonemergingmarkets,giventhetradelinkageswiththeworld’ssecond-largesteconomy.Nevertheless,thedownsidetrajectorywouldhavebeensignificantifnotforthesupplydisruptionsandconcerns,notably,theslumpinLibya’soilsuppliessinceJulyandinstabilityinSouthSudan.Ontheinventoryfront,themarketslookwellsuppliedwhencrudeoilstocksintheOECDisassessedespeciallywiththeforwarddemandcoveratacomfortable55.3daysattheendoflastyear,albeitlowerthanthefive-yearaverageof 58 days.

Onthesupplyfrontin2014,itseemsthegeopoliticaluncertaintyintheMiddleEast,theUkrainian/RussianstandoffoverCrimeaandsupplydisruptionsfromsomeOPECmemberswillcontinueforsometime,thus,sustainingthistightmarketbalanceandriskpremiumduringthenearterm.Thiswillrelativelybalancetherisingoutputfromnon-OPECproducersthataccountsfor60%ofglobalproduction,mainlyfromtheUS,CanadaandBrazil.Webelievethattheoversupplytheme,pertainingtoOPEC,thathavebeenpropagatedbytheendoflastyear,amidspeculationthatIranandLibyawillbeabletorestoresuppliesrestrainedrespectivelybysanctionsandpoliticalunrest,willnotmaterializethisyear,giventhatmajorLibyanexportportscontinuetobedisruptedbyinfightingbetweenmilitantgroups.Additionally,eventhoughIraniancrudeproductionhavebeenincreasingoflateafteraninterimaccordthateasedrestrictionscameintoeffectinJanuary,thetalkswithWesterncounterpartsinJulyregardingTehran’snuclearprogrammightbecomplicated,asalways.Againstthisbackdrop,OPEC’sproductionwillbecriticalinsupportingpricesinanenvironmentofrisingnon-OPECsupplyandiftheunlikelybecamelikely,asurgeinIranianandLibyancrudeexports.ThefactthatOPEC’soilproductionwasbelowthe30MMBDquota,agreedinDecember2011,forfiveoutofthelastsevenmonthssinceSeptember2013,reflectsadamancytomaintainasemblanceofnormalcyintheoilmarkets.Yet,theissueofaccommodatingthereturnofIran,LibyaandIraqwillcontinuetoposemedium-termchallengesonOPEC,especiallyforSaudiArabiathatbenefitedfromrampingupitsproduction,givenitsswingproducerstatus.

Theoildemandoutlookhasrelativelyimprovedonthebackofhigherdemandandastrongerglobaleconomy,withtheworld’sGDPexpectedtogrowby3.6%in2014,higherthanthe3%registeredlastyear.Non-OECDcountries, ledbyChina,willaccountforalmostalloftheexpectedconsumptiongrowthduringthenexttwoyears.Accordingly,theIEAhadincreaseditsworldwidecrudeconsumptionforecast,projectinganincrementalgrowthof1.4MMBDin2014,a1.5%annualgrowthrate.TheEIAandOPEC,aftersimilarupwardrevisions,are

NCB PERSPECTIVES | JUNE 2014

7

Sources: EIA Sources: EIA

Real GDP Growth, Contribution

0

20

40

60

80

100

120

80

82

84

86

88

90

92

94

96

1Q10 1Q11 1Q12 1Q13 1Q14 1Q15

USD/bblMMBD World Demand, LHSWTI, RHS

Projections

OECD Forward Demand Cover

40

45

50

55

60

65

May

-09

May

-10

May

-11

May

-12

May

-13

May

-14

Days

anticipatingincreasesbyaround1.2MMBDand1.1MMBD,respectively,in2014.Eventhoughglobaleconomicactivityhasimprovedlately,downsideriskspertainingtoChina’sgrowthstoryprevail.Ingenerating40-50%oftotalincrementaloildemandinrecentyears,Chinawillremainpivotalininfluencingoilmarketfundamentals,thus,alowerheadlinegrowthrateforthesecond-largestoilconsumerwillexertpressureonoilprices.However,theChineseStateCouncilandthePBOClookmore inclinedtowardstargetedstimulusandmonetaryeasing,whichmightreduceconcernsfortheremainderof2014.However,onamedium-termnote,thedrivetowardsrebalancingtheeconomy,reducingenvironmentaldegradationandencouragingmarketforces,willnegativelyimpactChineseincrementaloildemand,untiltheneededtransitionends.

Toconclude,Wedobelievethatoilmarketsareexpectedtoremain ina range-boundmovementduringtheyear,especiallythatoillacksstrongdirectionalmomentumforBrentpricestoremainabovetheUSD110/barrelmark,asincreasedsuppliesfromnon-OPECproducersareexpectedtooffsetdownsideriskspertainingtoChina’seconomicgrowth.Yet,asmentionedearlier,OPECwillbeinstrumentalinmitigatingsupplyconcernsbybalancingoutthemarket.Hence,weseeArabianlightpricesprotectedatafloorofUSD90/bblandonaveragetosettleatUSD102/bblin2014.

TheunfoldingsituationinIraqwouldposeanupsiderisktoourforecast,withthecentralgovernmentlosingitsgriponthesecond-largestcity,Mosul.Thisheightenedgeopoliticaluncertaintymightmeanarelativelyhigherriskpremiumtobebuilt intooilpricesgoingforward. It isourownopinion,however,thatthemarketshavebeen largely factoring in geopolitical risks in prices especially that the region has not experienced a semblance of normalcyinalongtime.Currently,theimpactonIraq'scrudeoilexportsislimitedespeciallythattheconflictiscontainedinthewesternandnorthernpartsofthecountryandfarfromthesouth,whichhousethree-quartersofIraq'scrudeoutput.Thethreebiggestoilfields,namelyRumaila,MajnoonandWestQurna-2,aswellastheexportterminalofBasralieinthesouth,andassuchasignificantdropinoutputandexportsishighlyunlikelyfortheshort-termatleast.

8

B. Saudi Economic Developments and Outlook

I. Real Sector

Last year marked the slowest economic growth rate since 2009, and we do believe that the Kingdom will face a moderate business cycle during 2014 and 2015, growing around 4%. In 2013, growth inaggregateoutput,realGDP,deceleratedto4%,mainlyagainstthebackdropofthenegativecontributionfromtheoilsector,stemmingfromalowerproductionlevel.Saudioiloutputfellbyaround1.6%in2013,averaging9.64MMBD,whichweighednegativelyontheoilsectorGDPthatdeclinedby1%,thelargestcontractionsince2009.Nevertheless,thecontractionintheoilsectorwasmorethanoffsetbynon-oilGDPgrowththatgrewbyaround5.4%.Importantly,thenon-oilprivatesectorincreasedby5.97%Y/Y,drivenbyconstruction,trade,andmanufacturing.Theeconomicgrowthoutlookfor2014willcontinuetobedrivenbynon-oilgrowth,withoilmaintainingitsnegativecontribution.WeprojectrealGDPgrowthof4.3%for2014duemainlytothenon-oilsectormaintaininglastyear’spaceof5.4%,drivenbytheprivatesector,mainlymanufacturingandconstruction.Ourassumptioncentersonatightmarketbalanceinoilmarketsthatlimitstheupsidepotentialforcrudepricesand results in a marginal decline in Saudi oil production during the forecast period.

Contribution of the oil sector to economic growth will remain negative. Libya’sunstableproductionsince2011inadditiontotheEUsanctionsonIran’scrudeexportsthatcommencedinJuly2012enabledtheKingdomasaswingproducertoreacha30-yearhighdailyproduction,butthissituationisreversingonthebackofnon-OPECsupplyandanexpectedriseinproductionfromthetwoaforementionedcountriesduringthenextcoupleofyears.Accordingly, complianceamongOPECmembershasbeen risingsince July2013,with theKingdomcuttingitsproductionlevelsfromaround10.05MMBDinAugustandSeptember2013toaslowas9.60MMBDinMarch.Thus,wedobelievethattheKingdomingivingwaytothesecountrieswillbeproducingbelowthe10MMBDmarkduringthenextthreeyears.Accordingtoourestimates,Saudicrudeoilproductionisexpectedtofallbyanaverageofonly40thousandb/d,reaching9.6MMBD,whichwillweighnegativelyonrealoilGDPthatwillcontractby0.2%in2014.Furthermore,innominalterms,withtheweightedaverageArablightpricesfallingfromUSD106.4/bbl in2013toestimatedUSD102/bbl in2014,oil revenuesareexpectedtoplungeby6.8%toaroundSAR965billion,belowtheSAR1trillionmarkthathasbeenregisteredoverthelastthreeyears.Ourbaselinescenarioforthemedium-termthatprojectsrange-boundmovementinoilpricesandslowergrowthinSaudicrudeproductionwillnecessitatefiscalprudencegoingforward.

7. Real GDP Growth, Contribution

-2%

0%

2%

4%

6%

8%

10%

2010 2011 2012 2013P 2014F 2015F

OilNon-oil PublicNon-oil Private

Real GDP

8. Saudi Crude Oil Production

7.00

7.50

8.00

8.50

9.00

9.50

10.00

2008 2009 2010 2011 2012 2013P 2014F 2015F

MMBD

Sources: SAMA and NCB Sources: OPEC and NCB

NCB PERSPECTIVES | JUNE 2014

9

The non-oil sector will be the driving force for economic growth in 2014, remaining above the 5% threshold for the third year in a row.Realnon-oilGDPin2013grewbyaround5.4%,largelydrivenbythestellarperformanceofthenon-oilprivatesector.TheprivatesectormaintaineditssignificantcontributiontorealGDPat58.9%,growingby5.97%,whichillustratesthevibrantrolethatprivateenterprisesareassumingintheSaudieconomy.Themaindriversofprivatesectorgrowthweretheconstruction,retail,andthemanufacturingsectors,whichposted8.8%,6.6%and5.3%annualgrowth, respectively.Thisvibrancyof theprivatesectoremanated from the enhanced business confidence and the improved financing environment. Evidently, thegrowth in commerce andmanufacturing benefited from the pickup in credit, receiving SAR28.7 billion andSAR13.6billion,respectively,inincrementalloansandadvancesfrombanksin2013,whichrepresentsanannualincreaseof14%and10.7%.Theboosttobusinessconfidenceunderpinnedthevalueofawardedconstructioncontracts that registeredanall-timehigh.Oneof thepromisinggrowthdrivers forcorporateSaudi isnon-oilexportsthatreachedahistoricalUSD54.1billionlastyearandthat,inourview,willgainmomentum,alongwithdomesticdemand,giventheverticalandhorizontaldiversificationplansthatwillenhancetheabsorptivecapacityoftheeconomy.Theaforementionedbusinesscyclewilllikelymoderateonthebackofrelativelylessfavorableoildynamics,a13%reductioninthebudgetallocationforcapitalexpenditureandthetighterimplementationof labor regulations.

Acloserlookattheslowerpaceofincreaseingovernmentexpenditureandbudgetoverrunduringthelastthreeyearswillresultinarelativelylowerdirectandindirectstimuli.SincetheRoyaldecreesannouncedin2011,theannualgrowthingovernmentexpenditurehadfallenfromastaggering26.4%to11.8%coupledbyasimilarreductioninthebudgetoverrunfrom42.5%to19%,in2011and2013,respectively.Therisingconcernsonfiscalpolicysustainability,especiallyonhigherproductionoutsideOPECandrange-boundoilpriceswilllikelymakethegovernmentmoreprudentandconservative,eventhoughsubstantialnetforeignassetsandlowerdebtlevelscansustainexpansionarypolicies.Weexpectnon-oilsectorgrowthtoremainelevated,albeitlowerthanthe10-yearaverage,recording5.4%in2014,withthenon-oilprivatesectorregistering6.2%asmostsectorscontinuetoreapthebenefitsofthemyriadofprojectsstillcomingon-streamfromthe2008-2013capitalexpenditureboom.

The key beneficiaries in 2014 will remain to be the construction and manufacturing sectors, growing at 6% and 5%, respectively.Our projections for the two sectors are supported by buoyant activity in theprojects’market and strong business confidence. During 2013, the value of awarded construction contractsremainedabovetheSAR200billionthresholdforthethirdyearinarow,registeringarecordSAR293.4billion.TheawardedcontractsintherealestateandmanufacturingsectorsrespectivelyreachedSAR40billionandSAR22.3billionin2013,thesecondandthirdlargestsharesacrossallsectors,surpassedonlybythetransportationandpowersectors.Ostensibly,theroleofthegovernmentiscritical,wherebyitsignedapproximately2,441capitalexpenditurerelatedcontractswiththeprivatesectorvaluedatanestimatedSAR161.5billion,12%Y/Yincrease,according to the Ministry of Finance.

Aswepointedout,themoderationthemeishighlylikelyduringthisyearandnext,whichhadbeenunderscoredbyNCB’sBusinessOptimismIndex(BOI)thatdippedfrom54pointsin4Q2013to50pointsin2Q2014duetoapullbackinexpectationsonallparametersthatincludevolumeofsales,newordersandsellingprices.Mostofthenon-hydrocarbonsectorsareexpectedtomoderate,withtheconstructionandmanufacturingsectorsregisteringindexvaluesbelowthecompositeindexforthenon-hydrocarbonsectorin2Q2014,standingat49pointsforeach.However,manufacturingfirmsdisplayedasteadyoutlook,with67%ofthefirmsexpectinganimprovementindemandfortheirproducts.AccordingtotheBOI,respondentshavecitedgovernmentlaborregulationsandtheavailabilityoflaboraschallengesimpactingbusinessoperations.Wedobelievethatthesechallengeswillremainshort-termbottlenecksforcompaniesseekinglow-skilledexpatriateworkers,especiallyaftertherecentdecisionsbytheInteriorMinistrytotoughenpunishmentonillegals,whichcomplimentsendeavorsbytheLaborMinistryto regulate the labor market.

FDI inflows are expected to moderate going forward. Structural reformscontinueunabatedly, improvingtheKingdom’sbusinessenvironmentanditsattractivenessforforeigncapitalinflows.TheWorldBank’sDoingBusiness2014reportrankedtheKingdom26thoutof189countriesforeaseofdoingbusiness.The2013/14GlobalCompetitivenessReportpreparedbytheWorldEconomicForumalsorankedSaudiArabiaat20outof148countries,aheadofChina,Turkey,BrazilandIndia.AccordingtotheWorldInvestmentReport2013,issuedbytheUnitedNationsConferenceonTradeandDevelopment(UNCTAD),theKingdomwasthesecond-largestFDIrecipientinWestAsia,withreceiptstotalingUSD12.2billionin2012,surpassedonlybyTurkeythatpostedUSD12.4billionandfollowedbyafellowGCCmember,theUAE,thatcameinthirdwithUSD9.6billion.However,theinflowsfellby25.3%comparedtoUSD16.3billionin2011,andWebelievethatFDIwillmoderateinthenext

10

coupleofyearsmimickinganexpectedrelativeslowdownintheSaudibusinesscycleandastheprojects’marketplateau.Accordingly,theshareofFDIingrossfixedcapitalformation(GFCF)willcontinuetohoveraround10%,belowfiguresregisteredforthepreviousthreeyears,yetsignificantlyhigherthanthe1.5%averageratepostedduringtheperiod1995-2004.

Net Exports

Change in Inventory

Gross Fixed Capital Formation

Private Final Consumption Expenditure

Government FinalConsumption Expenditure

Real GDP

10. Real GDP Growth by Expenditure, Contribution

-10%

0%

10%

20%

2008 2009 2010 2011 2012

Sources: SAMA and NCB Sources: SAMA and NCB

Inflation is likely to hover around 3% this year, with the recent sharp increase in commodity prices moderating by the 2H2014 and offset by lower imported inflation. In2013,pricesedgedhigher,averaging3.5% due to higher food prices. The liquid state of the economy was supportive of higher consumptionexpenditure,whichdroveuplocalfoodpricesthataveraged5.7%Y/Y,higherthan4.5%Y/Yregisteredin2012.Ontherentalcomponent,pricesmaintainedaslightlyhigherpacethan2012,albeitlowcomparedtothe2007-2011periodbyaveraging3.5%in2013.Acceleratingtheimplementationofthemortgagelawwillpositivelyimpactthelocalrealestatemarketbyprovidingfinancingtohomeseekers.Lookingahead,thecostofbuildingmaterialsisnotexertingupwardpressureonprices,withtheaveragepricesfortimber,cables,ironandcementfallingyear-to-dateby1.7%,1.2%,0.9%and0.6%,respectively,bytheendofFebruary2014.Itisimportanttonotethattherobustgrowthinprivatecreditingeneralandconsumerloansinparticularwillconstituteanupsiderisk toour forecast forheadline inflation.Withunemploymentat the lowest level since2009,11.5%by theendof4Q2013,anexpectedincreaseindisposableincomewillboostprivateconsumptionexpenditure,whichposteda7.2%increaselastquarter.However,thedollar-positiveeffectduetotaperingwillunderpintheheadlineinflationrate,whichwillremaininarange-boundmovementaround3%thisyear.

Manufacturing

Construction

Transport andCommunication

Other Sectors

Electricity and Water

Trade, Hotels, and Restaurants

Financial, Insurance, andReal Estate Services

9. Non-oil GDP Growth, Contribution

2009 2010 2011 2012 2013P 2014F0%

2%

4%

6%

8%

10%

11. Drivers of Inflation

Renovation, Rent and Fuel

Other

Foodstuff and Beverage

Overall CPI

-2%

0%

2%

4%

6%

8%

10%

12%

Apr-08 Apr-09 Apr-10 Apr-11 Apr-12 Apr-13 Apr-14

12. Imported InflationJanuary 2010 = 100

-10%

-5%

0%

5%

10%

15%

20%

25%

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11A

pr-1

1Ju

l-11

Oct

-11

Jan-

12A

pr-1

2Ju

l-12

Oct

-12

Jan-

13A

pr-1

3Ju

l-13

Oct

-13

Jan-

14A

pr-1

4

SAR/GBPSAR/EUR

Trade Weighted Dollar

Sources: SAMA Sources: SAMA

NCB PERSPECTIVES | JUNE 2014

11

II. Fiscal and External Balances

The next five years might prove to be a challenging time for policy making, with range-bound crude oil prices and contained production weighing negatively on oil revenues and, thus, reversing the hefty fiscal and current account surpluses of recent years. Even though the government’s 2014 budget doesnot provide oil price and production level assumptions,we believe that both revenues and expenditures areunderstated.TheMinistryofFinanceestimatesrevenuesandexpendituresatSAR855billionforeach,projectingabreak-even.Basedonannouncedrevenues,thegovernmentseemstohaveassumedtheaverageoilpriceatUSD73/bblforthisyear.WithourforecastofUSD102/bblfortheaverageArabianlightspotpricesand9.6MMBDforaverageoilproduction,weprojectabudgetsurplusofSAR84billion,or2.9%ofestimatedGDPin2014.Thedeclineinthesurpluswillbelargelyduetoafallinactualrevenues,expectedatSAR1090billion,withoilrevenuesregisteringSAR965billion,whichis6.8%belowactuallevelin2013.Additionally,ontheexpenditureside,thegovernmentwillmostlikelyexceedbudgetedexpenditures,albeitatamere3%,tobreachtheSAR1trillionmark,ashasbeenhistoricallythecase,however,thisfigurewillbethelowestbudgetoverrunsince1998.Accordingtoourforecast,actualcapitalexpenditureswilllikelyendupabovethebudgetedfigureofSAR248billiontoreachSAR251billionin2014.Againstthisbackdropofprojectedhigherexpendituresandlowerrevenues,thebreak-evenoilpricerequiredtobalancethebudgetwillrisefromUSD83/bbllastyeartoUSD87/bblin2014.

The current account balance will fall to the lowest level since 2010 in absolute terms, registering USD124 billion. Basedonouroilpriceandproductionassumptions,Weexpectoilexportrevenuestodeclineby6.7%toUSD303billion.Nevertheless,non-oilexportsareexpectedtopartiallyoffsetthecontractioninoilrevenues,growingby6.8%toUSD58billionduetoanexpectedimprovementintheglobalandGCCeconomicoutlook.ThereisadownsiderisktoourprojectionthatcanarisefromfurtherdeteriorationinChina’seconomicgrowth,especiallythatthesecond-largesteconomyhadbeensufferingfromsloweconomicgrowthandcontractioninmanufacturingoflate,whichmightimpactits14%shareoftheKingdom’snon-oilexports.Onaggregate,totalexportsareforecastedtorecordUSD361billionin2014comparedwithUSD376billioninthepreviousyear.Asforimports,theyareexpectedtogrow1.8%toUSD155billion,whichisarecordvalue.Thismarginalincreasewilllargelybeduetomoderatingdomesticdemand,asevidentfromtheyeartodatedeclineinthevalueofthesettledandnewlyopenedLettersofCredit(LCs)thatplungedby8.3%Y/Yforeach,withfoodstuffandmotorvehiclesaidingthefall.Accordingly,weexpectthecurrentaccountsurplustofall toUSD124billionthisyear,15.7%relative toGDP, smaller than theUSD133billion in2013.Thestill robustexternalpositionwill reflectfavorablyonnetforeignassetsthisyear.In2013,theseassetsgrewby10.7%toreachUSD717.7billionbytheendofDecember,andWeexpecttheywillbuildup,albeitataslowerpace,toUSD754billionin2014,coveringmorethan58monthsofimports,withthelargestshareinUSDdenominatedliquidassets.

13. Government Revenue and Expenditure Balance

SAR billion 2012 2013 2014 Budget 2014 Forecast

Total Revenue 1,247 1,156 855 1,090

Oil 1,145 1,035 735 965

Non-Oil 103 121 120 125

TotalExpenditure 873 976 855 1,005

Current 612 664 607 754

Capital 262 312 248 251

Deficit/Surplus 374 180 0 84

Sources: SAMA and NCB

The government continues to allocate funds to specialized credit institutions to support balanced development. BasedontheMOFannouncement,aroundSAR85.3billionin2014willbedisbursedbyspecializedcreditinstitutionstofinanceindustrialprojectsandtosupportsocialdevelopment,thus,complementingprivatecreditgrowththat recorded12.4%Y/Y inMarch2014.Acase inpoint is theSAMAPCOproject forethylenedichlorideandcausticsoda,wherebyPublicInvestmentFund(PIF)isextendingaloanworthSAR0.7billion.TheSaudiIndustrialDevelopmentFund(SIDF)hasalsorecentlyapproved19loansvaluedatSAR2.8billionfor15newindustrialprojectsandtheexpansionof4projects.Onaggregate,theoutstandingloansofgovernmentspecialized

12

credit institutionshavereachedarecordSAR268.6billion,expandingby7.7%toaddaroundSAR19.3billionduringthefirstthreequartersoflastyear.OntheSMEfront,theSaudiCreditandSavingBankhasfinanced1,495ofsuchestablishments,grantingmorethanSAR376millionunderthe“Masarat”program.AdditionalmeasuresoffinanceforSMEscontinuetogainground,withtheLoanGuaranteeProgram“Kafala”facilitatingcreditwortharoundSAR2.3billionin2013to1173establishments,representing28.7%oftheaggregatebeneficiariessincetheinceptionoftheprograminJanuary2006.

Current Account Balance / GDP

Budget Balance / GDP

14. Twin Surpluses

0%

5%

10%

15%

20%

25%

2010 2011 2012 2013P 2014F 2015F

15. Government Expenditure

Capital Expenditure

Current Expenditure

SAR billion

(100)

100

300

500

700

900

1,100

2010 2011 2012 2013P 2014F 2015F

Sources: SAMA and NCB Sources: SAMA and NCB

The Kingdom’s stable macroeconomic backdrop and the move towards streamlining regulations continue to be widely and positively recognized by renowned institutions. Accordingly, Standard andPoor’shadaffirmedtheKingdom’ssovereignratingatAA-withapositiveoutlookin2013andFitchupgradedit inMarch2014toAAwithastableoutlook.Thedecisionsbytheratingagencieswerepromptedbystronggovernment finances, which have largely withstood oil price volatility and the global economic crisis. ThisenhancedabilitytocontainshocksandsmoothbusinesscycleswillcontinuetosupportSaudiArabia’spositiveeconomicoutlook,goingforward.PublicdomesticdebtwasreducedfurtherfromSAR98.85billiontoSAR75.1billionin2013,amountingto2.7%relativetoGDP.WebelievethatgovernmentdebtwillremainbelowSAR100billion threshold for this year and next.

16. Domestic Public Debt

Gross Domestic Public Debt/GDP

Net Domestic Public Debt/GDP -60%

-40%

-20%

0%

20%

2007 2008 2009 2010 2011 2012 2013

Sources: SAMA and NCB Sources: SAMA

17. Government Deposits at SAMA

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 -

200

400

600

800

1,000

1,200

1,400

1,600

1,800

SAR billion

2010+69 bn

2011+194 bn

2012+329 bn

2013+125 bn

NCB PERSPECTIVES | JUNE 2014

13

III. Monetary Developments

Saudi Arabia’s monetary system continues to be awash with liquidity as elevated oil prices and production resulted in higher revenues that underpinned broader economic activities.Ontheregulatoryfront,SAMA’sproactivestancecontainedliquidityrisks,ensuredcompliancewithBaselIIIrequirementsaheadofscheduleandassessedthesoundnessoflocalbanksviastressteststhatreflectedlowersystemicrisks.Additionally,SAMAwaskeentoensurepricestabilityforbusinessesandconsumerstobenefitfromthebuoyanteconomy.Openmarketoperationsthatmopupexcessliquidityhavebeenacceleratingandbytheendof2013SAMAhasissuedSAR179.1billionworthofT-bills.Theconservativepolicyapproachwasaccentuatedbythebuildupofnetforeignassets,whichwassupportedbytheinfluxofoilrevenues.SAMA’snetforeignassetsundermanagementincrementallyincreasedbySAR238.8billion,9.8%,duringlastyear,reachingSAR2.7trillionbytheendof1Q14.ItiswidelyexpectedthatthemajorityofforeignassetsareinvestedinUSD-denominatedfixed-incomesecurities,whichprovideastablereturnalbeitlowerthanotherriskieralternatives.Thelock-stepnatureofSaudimonetarypolicywiththeUSisanimportantfactorthatwillsupportourviewofnochangetothedomesticbenchmarks,withSAMAkeepingtherepoat2%andthereverserepoat0.25%.

19. Interbank Market Rates

0%

1%

2%

3%

4%

5%

6%

May

-08

May

-09

May

-10

May

-11

May

-12

May

-13

May

-14

3M SAIBOR

3M USD LIBOR

18. SAMA and US Federal Reserve Policy Rates

May

-09

May

-08

May

-10

May

-11

May

-12

May

-13

May

-14

Reverse Repo Rate

Repo Rate

Federal Funds rate

0%

1%

2%

3%

4%

5%

6%

Sources: Thomson ReutersSources: Thomson Reuters and SAMA

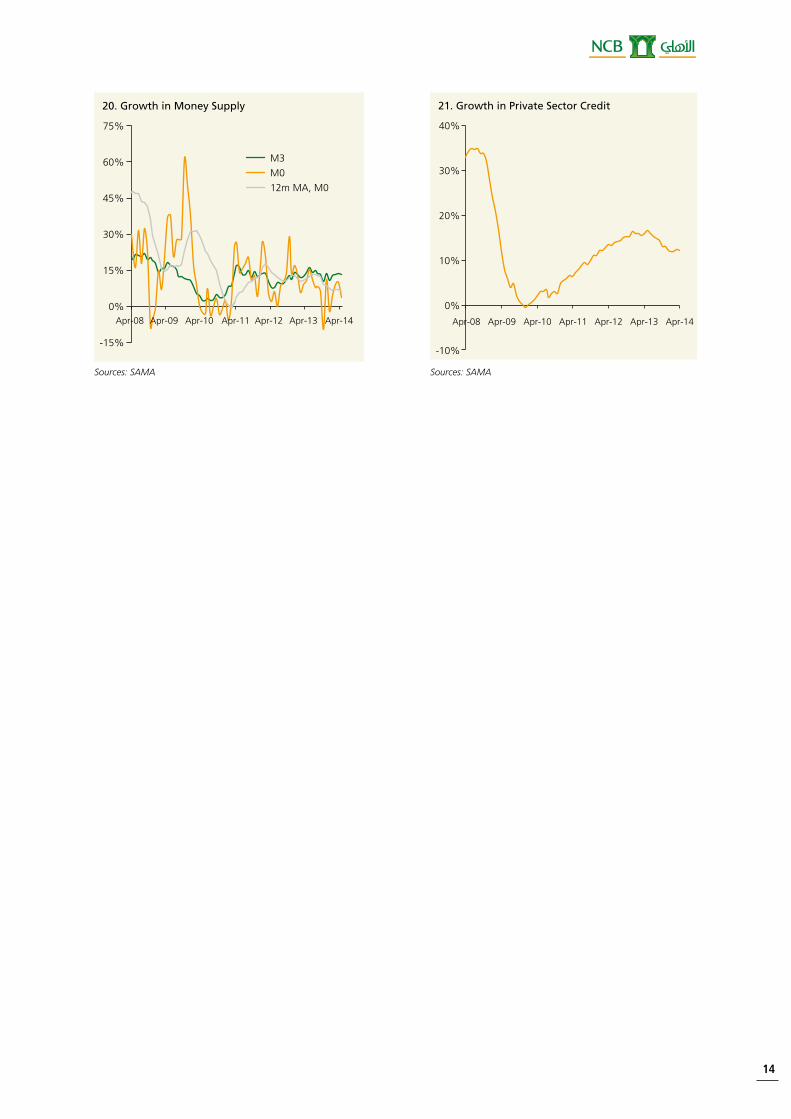

The sustainable pace of monetary aggregates reduces the risk of overheating the economy. During 2013,themonetarybase(M0)recordeditsfirstannualcontractionsince2008.ThenarrowestmonetarymeasuresettledatSAR343.5billionbytheendofDecember,slightlylowerthan2012’sSAR350.6billion.ThedeclineisnotrepresentativeofanegativesituationasthelargestcomponentofM0,depositswithSAMA,decreasedgivenlocalbanks’preferencetoutilizetheirexcessreservesforgrantingcredit.Accordingly,thecreditmarketwitnessedanotherhealthyyearbyexpandingat12.1%Y/Y.Additionally,moneysupply(M3)maintaineditsdouble-digitgrowth, recording 10.9%on an annual basis. The local financial system remains liquidwith excess reservessettlingat54.2%lastyear.SaudibanksheldSAR1.4trillionworthoftotaldepositsbytheendoflastyearthatrepresentmorethan70%oftheirtotal liabilitiesandcontinuetoprovideastablefundingbase.Thecapacityutilization,representedbytheloans-to-depositsratio,droppedto79.9%bytheendoflastyearafterpeakinginAugustat83.1%.Interestingly,localbankscontinuedtoaccumulatenetforeignassetsthatgrewby9.6%toreachSAR149.3billionin1Q2014afteramarginal2.1%increaseduring2013.Asfortheinterbankmarket,WeexpecttheSAIBORtoremainaroundthe100bpslevelintheshort-termduetothehealthycashlevelsofmostSaudi banks.

14

20. Growth in Money Supply

-15%

0%

15%

30%

45%

60%

75%

M3

M0

12m MA, M0

Apr-08 Apr-09 Apr-10 Apr-11 Apr-12 Apr-13 Apr-14

21. Growth in Private Sector Credit

-10%

0%

10%

20%

30%

40%

Apr-08 Apr-09 Apr-10 Apr-11 Apr-12 Apr-13 Apr-14

Sources: SAMA Sources: SAMA

NCB PERSPECTIVES | JUNE 2014

15

IV. Financial Sector

The Saudi banking system capitalized on reforms implemented during the financial crisis and posted record profits in 2013. The vibrancy of the private sector underpinned economic activities,which, in turn,providedopportunitiesforbankstoexpandtheirbalancesheets,ascenariothatislikelytomaterializethisyearaswell.Eventhoughlowinterestrateskeptnetinterestmarginscontained,the12locallyincorporatedbanksbytheendoflastyearrecordedastaggeringSAR37.6billion,anannualgrowthof7.1%,supportedbyvolume-growthincredit.Saudibanksincreasedtheiraveragecreditmaturitiesbyfocusingonlong-termloansthatrecordedagrowthof16.1%Y/Y,reachingatotalofSAR305.2billion.Additionally,non-performingloansandprovisionssignificantlydeclinedby21.7%and15.1%,respectively,asbanksimprovedtheirassetquality.TheSaudifinancialsystemhasalwayscompliedwithinternationalstandardsandSAMAhasalreadystartedguidingbankstowardsembracingBaselIIIstandards,proppingupcapitalbufferswithcapitaladequacylevelsstandingat17.8%wellaboverequirementsandasthebankingindustryincreaseditssharecapitalrecentlyby27.5%.Movingforward,thebankingsystemissecuredbyampleliquiditylevelsandcapitalbuffers,indicativeofamuchhealthierindustrygoingforward.

As 2013 was bullish for equities on a global scale, Tadawul managed to reach levels unseen since 2008 by climbing 25.5%.Followingastutteringstart inthefirstquarteroflastyear,thelocalequityindexgainedmomentumonthebackofattractivevaluationsascorporateprofitabilitysoared.ThemarketnetincomeexceededtheSAR100billionlevelbyrising6.6%Y/Y,whichattractedinvestorsintoriskierassets.Theglobalbullmarketalsosupportedpriceshigher,withrelativelylowersystemicrisksfacingtheworldeconomy.Thestrongerlocaldemandpushedtheprice-to-earningsratiobytheendoflastyearto15.52from12.75multiplein2012.Earlierthisyear,theDOWandNASDAQhave reached record highs and theirmomentumpositively spilled over on Tadawul,whichgained11.0%during1Q14.Theriseinbusinessactivitythattranslatedtorisingprofitsincreasedtheleveloftradingin1Q14toanaverageofSAR7.3billion,adouble-digitincreasecomparedtolastyear.However,themarketisstillstructurallyburdenedwithover90%individualtradersthatdoesn’tprovidethestabilityneededtowithstandshocks.Ontheprimarymarketfront,themarket’sdepthwasexpandedbyfiveinitialpublicofferings(IPOs)during2013,withatotalworthofaroundSAR2.0billionandanaverageoversubscriptionof7.5multiple,higherthanpreviousyear’s5.1multiple.Lookingahead,theprimarymarketisexpectedtoflourishthisyearandreacharecordhigh.However,itisnotexpectedthatTadawulwillovershootthe10,000thresholdbymuch,atleast for this year.

22. Saudi Equity Market Index(January 2009 = 100)

-20%

0%

20%

40%

60%

80%

100%

120%

Jan-

09

Oct-09

Jul-1

0Apr

-11

Jan-

12

Oct-12

Jul-1

3Apr

-14

23. Saudi IPO Issuance

0

2

4

6

8

10

12

14

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2008 2009 2010 2011 2012 2013

SAR million

Capital Raised

Number of Issues, RHS

Sources: Tadawul Sources: Tadawul

16

Following a record setting year, the Sukuk market is becoming a viable alternative financing vehicle for local businesses.GlobalSukukissuancesdroppedduring2013toUSD118.2billion,falling15.1%mainlyduetoMalaysia’sweakerperformance.TheAsianmarketcontinuestoholdthetopspotforIslamicfinancingwithatotalnumberof637issueslastyearworthUSD80.9billion.SaudiArabiafirmlycameinsecondwitharecordsettingUSD15.2billionworthofSukuk,up36.4%Y/Y,through20issues.TheSukukissuancesofGACA’sGuaranteedSeniorSukukII(USD4billion)andAramco’sSadaraSukuk(USD2billion)werethelargestduring2013onaglobal-scale, cementing Saudi status in this rapidly growingmarket. Furthermore, SEC issued a two-tranche Islamicbondwithatenorof10yearsandafirstever30yearsSukuk,eachwithavalueofSAR3.75billion.Evidently,theextendedmaturitywillprovideapricingbenchmarkforlonger-tenorSukukandenergizeanalternativevenueforfinancinginfrastructureprojects.ThemajorityofissuancesweredenominatedinSaudiRiyalswithvaryingreturnratesfromaflat1.5%forIslamicDevelopmentBank’sissuancetoafluctuating6monthsSAIBORplus155bpsforSaudiHollandi’sTier2Sukuk.Inaddition,anumberofbanksoptedfortheShariahcompliantalternativetoboosttheirtier2capital,suchasSaudiBritishBank,NationalCommercialBank,andtheupcomingBanqueSaudiFransiissuance(SAR2billion).

24. Saudi Sukuk Issuance

Debt issued

Number of issues (RHS)

USD million

0

2

4

6

8

10

12

14

16

18

20

0

2

4

6

8

10

12

14

16

18

20

2007 2008 2009 2010 2011 2012 2013

25. Saudi Share of GCC Sukuk Issuance, 2013

58%

42%

KSA Rest of GCC

Sources: Zawya Sources: Zawya

NCB PERSPECTIVES | JUNE 2014

17

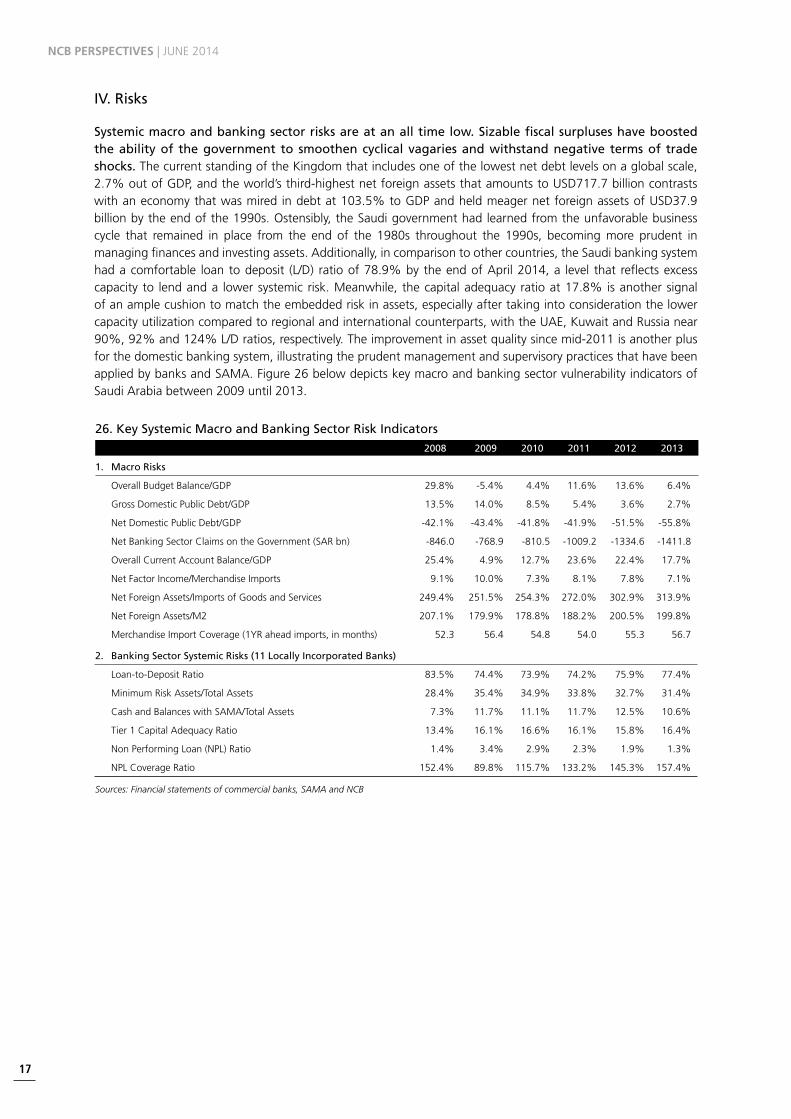

26. Key Systemic Macro and Banking Sector Risk Indicators 2008 2009 2010 2011 2012 2013

1. Macro Risks

OverallBudgetBalance/GDP 29.8% -5.4% 4.4% 11.6% 13.6% 6.4%

GrossDomesticPublicDebt/GDP 13.5% 14.0% 8.5% 5.4% 3.6% 2.7%

NetDomesticPublicDebt/GDP -42.1% -43.4% -41.8% -41.9% -51.5% -55.8%

NetBankingSectorClaimsontheGovernment(SARbn) -846.0 -768.9 -810.5 -1009.2 -1334.6 -1411.8

OverallCurrentAccountBalance/GDP 25.4% 4.9% 12.7% 23.6% 22.4% 17.7%

NetFactorIncome/MerchandiseImports 9.1% 10.0% 7.3% 8.1% 7.8% 7.1%

NetForeignAssets/ImportsofGoodsandServices 249.4% 251.5% 254.3% 272.0% 302.9% 313.9%

NetForeignAssets/M2 207.1% 179.9% 178.8% 188.2% 200.5% 199.8%

MerchandiseImportCoverage(1YRaheadimports,inmonths) 52.3 56.4 54.8 54.0 55.3 56.7

2. Banking Sector Systemic Risks (11 Locally Incorporated Banks)

Loan-to-DepositRatio 83.5% 74.4% 73.9% 74.2% 75.9% 77.4%

MinimumRiskAssets/TotalAssets 28.4% 35.4% 34.9% 33.8% 32.7% 31.4%

CashandBalanceswithSAMA/TotalAssets 7.3% 11.7% 11.1% 11.7% 12.5% 10.6%

Tier1CapitalAdequacyRatio 13.4% 16.1% 16.6% 16.1% 15.8% 16.4%

NonPerformingLoan(NPL)Ratio 1.4% 3.4% 2.9% 2.3% 1.9% 1.3%

NPLCoverageRatio 152.4% 89.8% 115.7% 133.2% 145.3% 157.4%

Sources: Financial statements of commercial banks, SAMA and NCB

IV. Risks

Systemic macro and banking sector risks are at an all time low. Sizable fiscal surpluses have boosted the ability of the government to smoothen cyclical vagaries and withstand negative terms of trade shocks. ThecurrentstandingoftheKingdomthatincludesoneofthelowestnetdebtlevelsonaglobalscale,2.7%outofGDP,andtheworld’sthird-highestnetforeignassetsthatamountstoUSD717.7billioncontrastswithaneconomythatwasmiredindebtat103.5%toGDPandheldmeagernetforeignassetsofUSD37.9billionbytheendofthe1990s.Ostensibly,theSaudigovernmenthadlearnedfromtheunfavorablebusinesscycle that remained in place from the end of the 1980s throughout the 1990s, becomingmore prudent inmanagingfinancesandinvestingassets.Additionally,incomparisontoothercountries,theSaudibankingsystemhadacomfortable loantodeposit (L/D) ratioof78.9%bytheendofApril2014,a level that reflectsexcesscapacity to lendanda lowersystemicrisk.Meanwhile, thecapitaladequacyratioat17.8%isanothersignalofanamplecushiontomatchtheembeddedriskinassets,especiallyaftertakingintoconsiderationthelowercapacityutilizationcomparedtoregionalandinternationalcounterparts,withtheUAE,KuwaitandRussianear90%,92%and124%L/Dratios,respectively.Theimprovementinassetqualitysincemid-2011isanotherplusforthedomesticbankingsystem,illustratingtheprudentmanagementandsupervisorypracticesthathavebeenappliedbybanksandSAMA.Figure26belowdepictskeymacroandbankingsectorvulnerabilityindicatorsofSaudiArabiabetween2009until2013.

18

The Economics Department Research TeamHead of Research

Said a. al ShaikhGroup Chief Economist

Macroeconomic Analysis

Tamer el ZayaT majed a. al-Ghalib yaSSer al-daWOOd Senior Economist/Editor Senior Economist Economist

[email protected] [email protected] [email protected]

Sector Analysis / Saudi Arabia

albara'a alWaZir ShahraZad a. faiSal Senior Economist Economist

[email protected] [email protected]

Management Information System

Sharihan al-manZalaWiEconomist

To be added to the nCb economics department distribution list

Please contact: Noel Rotap

Tel.:+966-2-646-3232

Fax:+966-2-644-9783

Email:[email protected]

disclaimer: TheinformationandopinionsinthisresearchreportwerepreparedbyNCB’sEconomicsDepartment.The

information herein is believed by NCB to be reliable and has been obtained from public sources believed to

bereliable.However,NCBmakesnorepresentationastotheaccuracyorcompletenessofsuchinformation.

Opinions,estimatesandprojectionsinthisreportconstitutethecurrentjudgmentoftheauthor/authors

asofthedateofthisreport.TheydonotnecessarilyreflecttheopinionsofNCBastothesubjectmatter

thereof.Thisreportisprovidedforgeneralinformationalpurposesonlyandisnottobeconstruedasadvice

to investors or an offer to buy or sell or a solicitation of an offer to buy or sell any financial instruments or

othersecuritiesortoparticipateinanyparticulartradingstrategyinanyjurisdictionorasanadvertisement

ofanyfinancialinstrumentsorothersecurities.Thisreportmaynotbereproduced,distributedorpublished

byanypersonforanypurposewithoutNCB’spriorwrittenconsent.