Sample Construction Only Loan Estimate Closing …€¦ · Sample Construction Only Loan Estimate &...

20

Sample Construction Only Loan Estimate & Closing Disclosure Six-month, Interest-Only Construction Note with a Fixed Rate Interest Due only on the Amount Advanced Amount and Timing of Advances Unknown 800-847-1653 [email protected] www.bankerscompliance.com

Transcript of Sample Construction Only Loan Estimate Closing …€¦ · Sample Construction Only Loan Estimate &...

Sample Construction Only

Loan Estimate &

Closing Disclosure

Six-month, Interest-Only Construction Note with a Fixed Rate Interest Due only on the Amount Advanced Amount and Timing of Advances Unknown

www.bankerscompliance.com

Banker’s Compliance Consulting, Inc. Phone: 800-847-1653 Email: [email protected]

Website: www.bankerscompliance.com

Construction Loans & TRID Back in March, the CFPB addressed construction loans as part of the Federal Reserve’s Outlook Live series. If you missed it, you can still register and listen to the webinar. We want to touch on some of the key takeaways from this webinar, and also explain, “How BCC would do it”. For your benefit, we’ve put together a TRID Construction Loan Packet that includes a sample Loan Estimate and Closing Disclosure that reflects our preferred method of disclosing these multiple-advance loans. The packet also includes a key, which walks you through and explains some of the more complex fields of the sample disclosure. These are being provided as a supplementary document to this article.

Understandably, there’s been a lot of confusion and frustration over construction lending. If you do construction lending, the CFPB could have done us all a favor by at least giving us a model form as an example of how this was all supposed to look. This is why we feel it’s important for us to give you a sample disclosure.

Our example is a construction-only loan with monthly interest-only payments. Interest is charged only on the amount advanced, with the amount and timing of advances being unknown.

First off, here are some important things to remember:

• You have options. There could be a number of different ways to accuratelydisclose a construction loan, but the disclosures need to reflect the actualterms of the note. So, if you’re disclosing the construction phase separately,the disclosure(s) should reflect only that transaction, regardless of whetheryou’re doing the permanent financing.

• You can still rely on the assumptions in Appendix D if you don’t know theamount or timing of advances. If you’re only charging interest on the amountadvanced, you’re allowed to estimate the monthly payments based on half thecommitment amount being advanced for the entire construction period. Theability to do so impacts several items on both the Loan Estimate and theClosing Disclosure, including payment amounts and the APR.

1

• There is a “primary” (i.e. “with a seller”) version of both the Loan Estimate andClosing Disclosure. You’re able to use the primary version of the forms for allyour transactions and we would recommend it when it comes to constructionloans. If there is no seller involved in the transaction, you are able to use the“alternate” versions of the forms. Just remember that if you issue a LoanEstimate on the primary/“With a seller” version, you need to stick with thatversion on your Closing Disclosure as well (and vice versa).

• When disclosing both the Purpose and the Product, there are hierarchies tobe followed. For example, if a loan is to buy a lot that will secure the loan andbe built upon, you have a purchase transaction for TRID, even though themajority of the funds are going towards construction. If you pay off theconstruction loan with permanent financing and both are secured by the sameproperty, the purpose for the permanent financing (for TRID) is a refinance.

• Likewise, a construction loan that has both an interest-only payment featureas well as a balloon payment feature must reflect only the interest-onlyfeature in the product description. Why? Well, because the rule states thatan interest-only payment feature trumps a balloon payment feature and youonly disclose one. In other words, because the CFPB said so.

There are some things, such as the Calculating Cash to Close table, that canmake you feel like disclosing a construction loan is a science experimentgone wrong. While you have to stay within the boundaries of the rule’srequirements, you do have options. We do feel it’s possible for this to allmake sense (eventually, anyway J).

Loan Terms The Loan Terms Chart is where the ability to use Appendix D first impacts the disclosures. You disclose the amount of the initial payment due at the initial interest rate. Most construction loans that we see have interest-only payments based on the amount advanced. However, if you don’t know when advances will be made, you use Appendix D, which allows you to calculate the interest based on half the commitment amount being advanced for the entire construction period.

The most confusing part, however, may be that you answer “NO” to the question of “Can this amount increase after closing” for a fixed-rate construction-only loan. Granted, this seems to fly in the face of “clear and conspicuous” because you know that the payment absolutely could increase. However, under Appendix D, you assume that half of the amount is advanced for the entire term of the loan, no more or less.

Many construction loans contain a Balloon Payment at the end of the term and you’re required to disclose the maximum amount of a balloon payment and when it will occur. To determine the amount to disclose, the principal amount here will be the entire loan amount; however, the amount of interest that will also be due is again determined based on half of the commitment amount. So, the maximum balloon payment is the sum of the loan amount and the interest payment due when half of the amount is advanced.

Projected Payments When we look at the Projected Payments table, the first column should show the same payment amount that you disclosed in the Loan Terms table. If the payment is interest-only, you must also designate under the amount that the payment amount is “only interest”. On a fixed-rate construction-only loan, you won’t show a range. This follows the same logic as why we state “NO” the amount cannot increase in the Loan Terms table. You don’t disclose a range just because you don’t know when or how much advances will be because Appendix D allows us to assume interest based on half of the loan amount being advanced during the entire construction period. So, construction-only, fixed-rate loans with interest-only payments will likely only have two columns, one reflecting the interest-only payment for year 1 (you must use whole years) and one column for the Final Payment (the Balloon).

Also part of the Projected Payments section is the Estimated Taxes, Insurance & Assessments. Remember that the rules for disclosing the Estimated Taxes, Insurance, & Assessments require you to project what the insurance and taxes will be after any known improvements are made to the property, regardless of whether those improvements will be made with your loan funds. How? You need to use the best information reasonably available. In other words, you can’t just guess. Have a process in place for determining this information.

Loan Costs and Other Costs Some of you have draw and inspection fees, but you’re not sure how many will be charged. Again, you need to base the disclosure on the best information available at the time of the disclosure. If you don’t know the exact schedule of fees, you may base the estimated charge on similar past transactions.

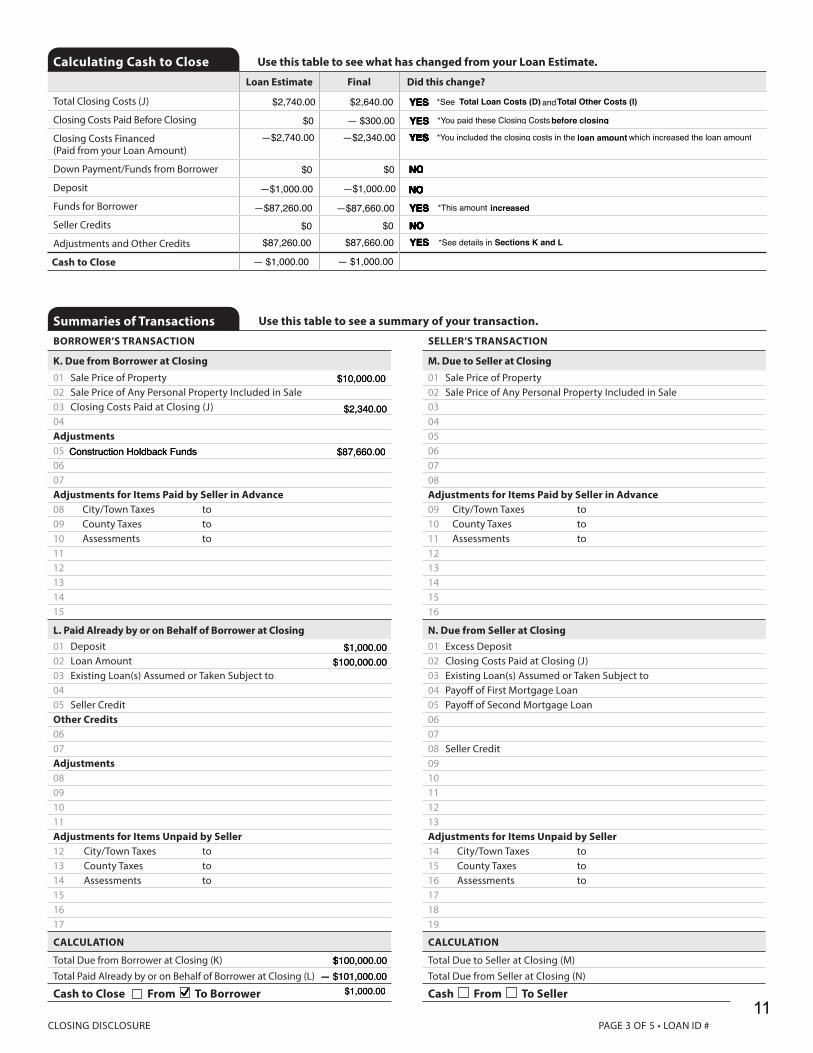

Holdback What to do with those funds that you’re holding for construction disbursements has probably wreaked the most havoc on your disclosures.

First off, it’s important to realize that you have options. There’s more than one way to address a “construction holdback”. We’ve heard of different options from a number of different places. Not all were mentioned during the webinar. In fact, the CFPB doesn’t like the term “holdback” and are reluctant to use it because it’s not defined.

Make sure, however, that you label the holdback funds in a way that’s consistent with other loan documents, including the Note. If other documents don’t address or label these funds, label them in a way that best allows the consumer to identify what they are for.

Here are some options for how to show the holdback funds:

1. On the primary (with a seller) Loan Estimate and Closing Disclosure, disclosethe holdback in the Calculating Cash to Close table as a positive numberwithin the Adjustments and Other Credits section, which offsets the negativenumber that results from the required calculation for Funds for Borrower (Debtbeing satisfied – Loan Amount). The amount is then also disclosed inSection K (under Adjustments) in the Summaries of Transactions on theClosing Disclosure.

So, take a $100,000 construction loan. Let’s say a lot is being purchased for$10,000 and the remaining funds are being held for future construction draws.The Funds for Borrower would be determined by $10,000 - $100,000 for atotal of - $90,000. You would then list a positive $90,000 for Adjustments andOther Credits on the Loan Estimate and in Section K of the ClosingDisclosure (which will roll into the Adjustments in the Calculating Cash toClose table on the Closing Disclosure). This method is reflected in ourexample.

2. Disclose the holdback in Section H (Other), which rolls it into the TotalClosing Costs, Section J, and the Calculating Cash to Close table. Caution,as this will greatly inflate your closing costs!

On the primary disclosures, that amount would be offset by the negativenumber for Funds for Borrower (Third Party Payments – Loan amount).

Take our $100,000 construction loan example from above. Even if there areno other closing costs, the total closing costs will be disclosed as $90,000!The Funds for Borrower would be determined by $10,000 - $100,000 for atotal of - $90,000 to offset the total closing costs.

On the alternate Loan Estimate and Closing Disclosure, disclosing theholdback in Section H, Other, will result in your total closing costs being alarge negative number. This would be offset in the Calculating Cash to Closetable, at least in part, by the positive loan amount.

Applicants who are actually “shopping” (or who just look at the disclosure) willlikely be alarmed if your closing costs are $90,000 more than the bank downthe street. Remember, that the Total Closing Costs appear on the first pageof the disclosure as well.

4

3. Disclose the holdback as a Payoff or Payment.

On the primary Loan Estimate and Closing Disclosure, the holdback wouldthen be factored into the Funds for Borrower calculation (Third-partypayments – Loan amount) of the Calculating Cash to Close table. In theexample above, you would take the sum of both the $10,000 lot purchase andthe $90,000 holdback and subtract the loan amount, which in this case wouldleave you with $0. The math works if you never show the holdback, but thatseems confusing as well. If you show the holdback in the transactionsummaries on the Closing Disclosure, you’re not doing an apples-to-applescomparison back to the Loan Estimate.

On the alternate Loan Estimate and Closing Disclosure, treating the holdbackas a Payoff or Payment means it is reflected as a negative number in theCalculating Cash to Close table; the negative number will again be offset, atleast in part, by the positive loan amount. Also, include it in the Payoffs andPayments table on the Closing Disclosure.

We recommend Option #1. While the CFPB didn’t specifically endorse this option during their webinar, we feel it does the best job of showing the customer the terms of their legal obligation, or what is actually happening with the transaction. Now, this option won’t be available to you if you’re using the alternate forms. If that’s the case, either option #2 or #3 will work. It just depends on whether you want to explain the holdback as either being part of the higher closing costs or shown as a Payoff or Payment. Given those options, we would recommend going with option #3 and treating the holdback as a payoff. We don’t like the second option (which was the first option offered by the CFPB) because it inflates your total closing costs. It seems difficult to explain and confusing to a consumer.

Adjustable Payment There’s also been quite a bit of confusion as to whether a balloon payment by itself triggers the Adjustable Payment table. However, a construction-only loan with interest-only payments and a balloon does not trigger the Adjustable Payment table because the loan is not changing to a different payment stream (such as principal and interest payments); it is simply coming due and the rule has different requirements for disclosing the balloon payment.

Again, there are options. Options are often frustrating because it’s easier to just say, “Tell me how to do it so it’s not wrong” or “…so I don’t get written up for it”. We understand. We encourage you; however, to use these options to your advantage. Your system may use a different method for construction loans, or other closed-end loans with multiple advances. Those could be okay as well. If you stay within the framework of the rule and your disclosures accurately reflect the transaction, we believe you’ll be okay.

5

Loan Terms Can this amount increase after closing?

Loan Amount

Interest Rate

Monthly Principal & InterestSee Projected Payments below for your Estimated Total Monthly Payment

Does the loan have these features?

Prepayment Penalty

Balloon Payment

DATE ISSUED APPLICANTS

PROPERTY SALE PRICE

LOAN TERM 30 years PURPOSE PurchasePRODUCT 5 Year Interest Only, 5/3 Adjustable RateLOAN TYPE Conventional FHA VA _____________LOAN ID # 1330172608RATE LOCK NO YES, until

Loan Estimate

Projected Payments

Payment Calculation

Principal & Interest

Mortgage Insurance

Estimated EscrowAmount can increase over time

Estimated Total Monthly Payment

Estimated Taxes, Insurance & AssessmentsAmount can increase over time

Before closing, your interest rate, points, and lender credits can change unless you lock the interest rate. All other estimated closing costs expire on

Save this Loan Estimate to compare with your Closing Disclosure.

PAGE 1 OF 3 • LOAN ID # 1330172608LOAN ESTIMATE

Visit www.consumerfinance.gov/mortgage-estimate for general information and tools.

See Section G on page 2 for escrowed property costs. You must pay for other property costs separately.

This estimate includes In escrow? Property Taxes Homeowner’s Insurance Other:

Costs at Closing

Estimated Closing Costs Includes in Loan Costs + in Other Costs – in Lender Credits. See page 2 for details.

Estimated Cash to Close Includes Closing Costs. See Calculating Cash to Close on page 2 for details.

John & Mary Consumer123 Oak St.Anytown, NE 12345

2/1/16

NO

*You will have to pay at the end of year 1.$100,208

Year 1 Final Payment

$208.33 $100,208.33

0

0

$208.33

0

0

$100,208.33

XX

NONO$150

$208.33

$100,000

5% NO

NO

YES

NO

X

X

only interest

a month

987 Maple St., Anytown, NE 12345$10,000

6 mo.Purchase5 mo. Interest Only, Fixed Rate

2/16/16

2/1/16

— $1,000

$2,740 $2,190 $550 $0

ABC BANK1000 Main St - Anytown, NE 12345

1A2B3C

6

Loan Costs Other Costs

A. Origination Charges % of Loan Amount (Points) Desk Review Fee $150 Loan Origination Fee $1,000Processing Fee $300Rate Lock Fee $525Underwriting Fee $675Verification Fee $200

B. Services You Cannot Shop For Appraisal Fee $305Credit Report Fee $30Flood Determination Fee $35Lender’s Attorney $400

C. Services You Can Shop For Pest Inspection Fee $125Survey Fee $150Title – Courier Fee $32Title – Lender’s Title Policy $100Title – Settlement Agent Fee $300Title – Title Search $150

D. TOTAL LOAN COSTS (A + B + C)

E. Taxes and Other Government Fees Recording Fees and Other Taxes Transfer Taxes es

F. Prepaids Homeowner’s Insurance Premium ( months) Mortgage Insurance Premium ( months) Prepaid Interest ( per day for days @ ) Property Taxes ( months)

G. Initial Escrow Payment at Closing Homeowner’s Insurance per month for 3 mo. Mortgage Insurance per month for 0 mo. Property Taxes per month for 3 mo.

H. Other Real Estate Broker Administration Fee $200Title – Owner’s Title Policy (optional) $1,436

I. TOTAL OTHER COSTS (E + F + G + H)

J. TOTAL CLOSING COSTS D + I Lender Credits

Total Closing Costs (J) Closing Costs Financed (Paid from your Loan Amount) Down Payment/Funds from Borrower Deposit Funds for Borrower Seller Credits Adjustments and Other Credits

Estimated Cash to Close

Calculating Cash to Close

PAGE 2 OF 3 • LOAN ID # 1330172608LOAN ESTIMATE

Closing Cost Details

Inspection Fee $200Origination Charge $1,000

$1,200

Appraisal FeeCredit ReportFlood Determination

$500$25$15

Title - Lender’s Title InsuranceTitle - Settlement Agent Fee

$300$150

$540

$450

$50$50

6 $300$300

Title - Owner’s Title Insurance (optional) $200$200

$2,190

$550

$2,740$2,740

$2,740— $2,740

$0

$0$87,260

— $1,000— $87,260

— $1,000

7

LENDER NMLS/ LICENSE IDLOAN OFFICER NMLS/ LICENSE IDEMAIL PHONE

Comparisons Use these measures to compare this loan with other loans.

In 5 Years Total you will have paid in principal, interest, mortgage insurance, and loan costs.

Principal you will have paid off.

Annual Percentage Rate (APR) Your costs over the loan term expressed as a rate. This is not your interest rate.

Total Interest Percentage (TIP) The total amount of interest that you will pay over the loan term as a percentage of your loan amount.

Other Considerations

Additional Information About This Loan

MORTGAGE BROKER NMLS/ LICENSE IDLOAN OFFICER NMLS/ LICENSE IDEMAIL PHONE

PAGE 3 OF 3 • LOAN ID # 1330172608LOAN ESTIMATE

Confirm ReceiptBy signing, you are only confirming that you have received this form. You do not have to accept this loan because you have signed or received this form.

Applicant Signature Date Co-Applicant Signature Date

We may order an appraisal to determine the property’s value and charge you for this appraisal. We will promptly give you a copy of any appraisal, even if your loan does not close. You can pay for an additional appraisal for your own use at your own cost.

If you sell or transfer this property to another person, we will allow, under certain conditions, this person to assume this loan on the original terms. will not allow assumption of this loan on the original terms.

This loan requires homeowner’s insurance on the property, which you may obtain from a company of your choice that we find acceptable.

If your payment is more than ___ days late, we will charge a late fee of .

Refinancing this loan will depend on your future financial situation, the property value, and market conditions. You may not be able to refinance this loan.

We intend to service your loan. If so, you will make your payments to us.

to transfer servicing of your loan.

Appraisal

Assumption

Homeowner’s Insurance

Late Payment

Refinance

Servicing

$101,250

1.25%

x

15 5% of the monthly interest payment.

x

ABC Bank123456789Bob [email protected]

$100,00010.754%

x

15 5% of the monthly interest payment.

x

ABC Bank123456789Bob [email protected]

8

Projected Payments

Loan Terms

CLOSING DISCLOSURE PAGE 1 OF 5 • LOAN ID # 0000000000

Payment Calculation

Principal & Interest

Mortgage Insurance

Estimated EscrowAmount can increase over time

Estimated Total Monthly Payment

Estimated Taxes, Insurance & AssessmentsAmount can increase over timeSee page 4 for details See Escrow Account on page 4 for details. You must pay for other property

costs separately.

This estimate includes In escrow? Property Taxes Homeowner’s Insurance Other:

Can this amount increase after closing?

Loan Amount

Interest Rate

Monthly Principal & InterestSee Projected Payments below for your Estimated Total Monthly Payment

Does the loan have these features?

Prepayment Penalty

Balloon Payment

Closing Costs Includes $5,877.00 in Loan Costs + $7,642.43 in Other Costs – $0 in Lender Credits. See page 2 for details.

Cash to Close Includes Closing Costs. See Calculating Cash to Close on page 3 for details.

Costs at Closing

Transaction InformationBorrower

Seller

Lender

Loan InformationLoan Term Purpose Product

Loan Type Conventional FHA VA _____________

Loan ID # MIC #

Closing InformationDate Issued Closing Date Disbursement Date Settlement Agent File # Property

Sale Price

This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate.Closing Disclosure

3/1/163/8/163/8/16XYZ Title Co.1000987 Maple St.Anytown, NE 12345$10,000

John & Mary Consumer123 Oak St.Anytown, NE 12345Jim & Sally Seller1200 Pine St.Anytown, NE 12345ABC Bank

6 mo.Purchase5 mo. Interest Only,Fixed Rate

1A2B3C

x

XX

$100,000

5%

$208.33

NO

YES

NO

NO

NO

*You will have to pay $100,208 at the end of year 1.

Final PaymentYear 1

$208.33

00 0

$100,208.33

$208.33 $100,208.33

NONO

$150.00a month

— $1,000.00

$2,090.00 $550.00 $0$2,640.00

0

.

,

x

XX

NO

YES

NO

NO

NO

Final PaymentYear 1

only interest

00 0

NONO

0

3/1/163/8/163/8/16XYZ Title Co.1000987 Maple St.Anytown, NE 12345$10,000

John & Mary Consumer123 Oak St.Anytown, NE 12345Jim & Sally Seller1200 Pine St.Anytown, NE 12345ABC Bank

6 mo.Purchase5 mo. Interest Only,Fixed Rate

1A2B3C

x

XX

$100,000

5%

$208.33

NO

YES

NO

NO

NO

*You will have to pay $100,208 at the end of year 1.

Final PaymentYear 1

$208.33

00 0

$100,208.33

$208.33 $100,208.33

NONO

$150.00a month

— $1,000.00

$2,090.00 $550.00 $0$2,640.00

0

.

,

x

XX

NO

YES

NO

NO

NO

Final PaymentYear 1

only interest

00 0

NONO

0

9

Loan Costs

CLOSING DISCLOSURE PAGE 2 OF 5 • LOAN ID # 0000000000

Borrower-Paid Seller-Paid Paid by OthersAt Closing Before Closing At Closing Before Closing

A. Origination Charges 01 % of Loan Amount (Points)02 03 04 05 06 07 08 B. Services Borrower Did Not Shop For 01 02 03 04 05 06 07 08 09 10 C. Services Borrower Did Shop For 01 02 03 04 05 06 07 08 D. TOTAL LOAN COSTS (Borrower-Paid)Loan Costs Subtotals (A + B + C)

J. TOTAL CLOSING COSTS (Borrower-Paid)Closing Costs Subtotals (D + I)Lender Credits

Closing Cost Details

E. Taxes and Other Government Fees 01 Recording Fees Deed: Mortgage: 02 F. Prepaids 01 Homeowner’s Insurance Premium ( mo.) 02 Mortgage Insurance Premium ( mo.)03 Prepaid Interest ( per day from to )04 Property Taxes ( mo.)05 G. Initial Escrow Payment at Closing 01 Homeowner’s Insurance per month for mo.02 Mortgage Insurance per month for mo.03 Property Taxes per month for mo.04 05 06 07 08 Aggregate AdjustmentH. Other01 02 03 04 05 06 07 08 I. TOTAL OTHER COSTS (Borrower-Paid)Other Costs Subtotals (E + F + G + H)

Other Costs

Inspection FeeOrigination Charge

$200.00$1,000.00

$1,200.00

Appraisal Fee to Appraisal Inc.Credit Report to Credit Reports Inc.Flood Determination to Noah’s Flood Service

$425.00$25.00$15.00

$465.00

Title - Lender’s Title Insurance to Any County Title Co.Title - Settlement Agent Fee to Any County Title Co.

$300.00$125.00

$425.00

$25.00 $25.00 $50.00

$300.006

$50.00

$300.00

Real Estate Commission to ABC RealtorsTitle - Owner’s Title Insurance (optional) to Any County Title Co.

$250.00

$600.00$200.00

Transfer Tax $200.00

$2,090.00$2,090.00

$200.00

$300.00$550.00

$300.00$2,340.00$2,640.00

$800.00

.

6

Transfer Tax

Inspection FeeOrigination Charge

$200.00$1,000.00

$1,200.00

Appraisal Fee to Appraisal Inc.Credit Report to Credit Reports Inc.Flood Determination to Noah’s Flood Service

$425.00$25.00$15.00

$465.00

Title - Lender’s Title Insurance to Any County Title Co.Title - Settlement Agent Fee to Any County Title Co.

$300.00$125.00

$425.00

$25.00 $25.00 $50.00

$300.006

$50.00

$300.00

Real Estate Commission to ABC RealtorsTitle - Owner’s Title Insurance (optional) to Any County Title Co.

$250.00

$600.00$200.00

Transfer Tax $200.00

$2,090.00$2,090.00

$200.00

$300.00$550.00

$300.00$2,340.00$2,640.00

$800.00

.

6

Transfer Tax

10

Calculating Cash to Close

BORROWER’S TRANSACTION

K. Due from Borrower at Closing 01 Sale Price of Property 02 Sale Price of Any Personal Property Included in Sale03 Closing Costs Paid at Closing (J) 04 Adjustments05 0607Adjustments for Items Paid by Seller in Advance08 City/Town Taxes to 09 County Taxes to10 Assessments to11 12 131415

L. Paid Already by or on Behalf of Borrower at Closing 01 Deposit 02 Loan Amount 03 Existing Loan(s) Assumed or Taken Subject to04 05 Seller Credit Other Credits0607 Adjustments0809 10 11 Adjustments for Items Unpaid by Seller12 City/Town Taxes to 13 County Taxes to 14 Assessments to15 1617

CALCULATION

Total Due from Borrower at Closing (K) Total Paid Already by or on Behalf of Borrower at Closing (L)

Cash to Close From To Borrower

SELLER’S TRANSACTION

M. Due to Seller at Closing 01 Sale Price of Property 02 Sale Price of Any Personal Property Included in Sale03 04 05 06 07 08Adjustments for Items Paid by Seller in Advance09 City/Town Taxes to 10 County Taxes to11 Assessments to12 13141516

N. Due from Seller at Closing 01 Excess Deposit02 Closing Costs Paid at Closing (J) 03 Existing Loan(s) Assumed or Taken Subject to04 Payoff of First Mortgage Loan 05 Payoff of Second Mortgage Loan06 07 08 Seller Credit 09 10111213Adjustments for Items Unpaid by Seller14 City/Town Taxes to 15 County Taxes to 16 Assessments to17 1819

CALCULATION

Total Due to Seller at Closing (M) Total Due from Seller at Closing (N)

Cash From To Seller

Summaries of Transactions

CLOSING DISCLOSURE PAGE 3 OF 5 • LOAN ID # 0000000000

Loan Estimate Final Did this change?

Total Closing Costs (J)

Closing Costs Paid Before Closing

Closing Costs Financed (Paid from your Loan Amount)

Down Payment/Funds from Borrower

Deposit

Funds for Borrower

Seller Credits

Adjustments and Other Credits

Cash to Close

Use this table to see a summary of your transaction.

Use this table to see what has changed from your Loan Estimate.

$0

$0

—$1,000.00

$0$87,260.00

—$2,740.00

$2,640.00

— $300.00

$0

—$1,000.00

—$87,660.00$0

$87,660.00

Total Loan Costs (D) Total Other Costs (I)and

YES

NO

NO

YESNO

Sections K and L

— $1,000.00

$10,000.00

$2,340.00

$87,660.00Construction Holdback Funds

$1,000.00$100,000.00

$100,000.00— $101,000.00

*This amount

*See

before closing*You paid these Closing Costs

YES

NO

NO

YESNO

*See details in

*You included the closing costs in the , which increased the loan amountloan amount

YES

YES

YES

increased

YES

NO

NO

YESNO

$

YES

NO

NO

NO

YES

YES

YES

$1,000.00

$2,740.00

YES

NO

NO

YESNO

$10,000.00

$2,340.00

$87,660.00Construction Holdback Funds

$1,000.00$100,000.00

$100,000.00— $101,000.00

YES

NO

NO

YESNO

YES

YES

YESYES

NO

NO

YESNO

$

YES

NO

NO

NO

YES

YES

YES

$1,000.00

— $1,000.00

—$87,260.00

—$2,340.00

11

AssumptionIf you sell or transfer this property to another person, your lender

will allow, under certain conditions, this person to assume this loan on the original terms.

will not allow assumption of this loan on the original terms.

Demand FeatureYour loan

has a demand feature, which permits your lender to require early repayment of the loan. You should review your note for details.

does not have a demand feature.

Late PaymentIf your payment is more than ___ days late, your lender will charge a late fee of ________________________________________________

Negative Amortization (Increase in Loan Amount)Under your loan terms, you

are scheduled to make monthly payments that do not pay all of the interest due that month. As a result, your loan amount will increase (negatively amortize), and your loan amount will likely become larger than your original loan amount. Increases in your loan amount lower the equity you have in this property.

may have monthly payments that do not pay all of the interest due that month. If you do, your loan amount will increase (negatively amortize), and, as a result, your loan amount may become larger than your original loan amount. Increases in your loan amount lower the equity you have in this property.

do not have a negative amortization feature.

Partial PaymentsYour lender

may accept payments that are less than the full amount due (partial payments) and apply them to your loan.

may hold them in a separate account until you pay the rest of the payment, and then apply the full payment to your loan.

does not accept any partial payments.If this loan is sold, your new lender may have a different policy.

Security InterestYou are granting a security interest in

You may lose this property if you do not make your payments or satisfy other obligations for this loan.

CLOSING DISCLOSURE PAGE 4 OF 5 • LOAN ID # 0000000000

Loan Disclosures

Escrow AccountFor now, your loan

will have an escrow account (also called an “impound” or “trust” account) to pay the property costs listed below. Without an escrow account, you would pay them directly, possibly in one or two large payments a year. Your lender may be liable for penalties and interest for failing to make a payment.

Escrow

Escrowed Property Costs over Year 1

Estimated total amount over year 1 for your escrowed property costs:

Non-Escrowed Property Costs over Year 1

Estimated total amount over year 1 for your non-escrowed property costs:

You may have other property costs.

Initial Escrow Payment

A cushion for the escrow account you pay at closing. See Section G on page 2.

Monthly Escrow Payment

The amount included in your total monthly payment.

No Escrow

Estimated Property Costs over Year 1

Estimated total amount over year 1. You must pay these costs directly, possibly in one or two large payments a year.

Escrow Waiver Fee

will not have an escrow account because you declined it your lender does not offer one. You must directly pay your property costs, such as taxes and homeowner’s insurance. Contact your lender to ask if your loan can have an escrow account.

In the future, Your property costs may change and, as a result, your escrow pay-ment may change. You may be able to cancel your escrow account, but if you do, you must pay your property costs directly. If you fail to pay your property taxes, your state or local government may (1) impose fines and penalties or (2) place a tax lien on this property. If you fail to pay any of your property costs, your lender may (1) add the amounts to your loan balance, (2) add an escrow account to your loan, or (3) require you to pay for property insurance that the lender buys on your behalf, which likely would cost more and provide fewer benefits than what you could buy on your own.

Additional Information About This Loan

155% of the monthly interest payment.

987 Maple St.Anytown, NE 12345

$1,800.00

155% of the monthly interest payment.

987 Maple St.Anytown, NE 12345

$1,800.00

12

Contact Information

Other Disclosures

Confirm Receipt

By signing, you are only confirming that you have received this form. You do not have to accept this loan because you have signed or received this form.

Applicant Signature Date Co-Applicant Signature Date

CLOSING DISCLOSURE PAGE 5 OF 5 • LOAN ID # 0000000000

Total of Payments. Total you will have paid after you make all payments of principal, interest, mortgage insurance, and loan costs, as scheduled.

Finance Charge. The dollar amount the loan will cost you.

Amount Financed. The loan amount available after paying your upfront finance charge.

Annual Percentage Rate (APR). Your costs over the loan term expressed as a rate. This is not your interest rate.

Total Interest Percentage (TIP). The total amount of interest that you will pay over the loan term as a percentage of your loan amount.

Loan Calculations

?Lender Mortgage Broker Real Estate Broker (B) Real Estate Broker (S) Settlement Agent

Name Ficus Bank FRIENDLY MORTGAGE BROKER INC.

RELIABLE REALTY CO. REALTY PROS ABC Settlement

Address 4321 Raven Blvd.Somecity, MD 54321

1234 Terrapin Dr.Somecity, MD 54321

1776 Chesapeake St.Ste 405Anytown, MD 12345

3456 Oriole Ave. Anytown, MD 12345

5432 Free State Blvd. Ste 405Somecity, MD 54321

NMLS ID 111111 222222

License ID

Contact Joe Smith JIM TAYLOR KELLY GREEN STEVE WALSH NANCY WILSON

Contact NMLS ID 487493 394784

Contact License ID

Email [email protected]

JTAYLOR@ FRNDLYMTGBRKR.CO

NWILSON@ ABCSETTLEMENT.COM

Phone 111-222-3333 333-444-5555 444-555-6666 555-666-7777 666-777-8888

?

AppraisalIf the property was appraised for your loan, your lender is required to give you a copy at no additional cost at least 3 days before closing. If you have not yet received it, please contact your lender at the information listed below.

Contract DetailsSee your note and security instrument for information about

• what happens if you fail to make your payments, • what is a default on the loan,• situations in which your lender can require early repayment of the

loan, and • the rules for making payments before they are due.

Liability after ForeclosureIf your lender forecloses on this property and the foreclosure does notcover the amount of unpaid balance on this loan,

state law may protect you from liability for the unpaid balance. If you refinance or take on any additional debt on this property, you may lose this protection and have to pay any debt remaining even after foreclosure. You may want to consult a lawyer for more information.

state law does not protect you from liability for the unpaid balance.

RefinanceRefinancing this loan will depend on your future financial situation, the property value, and market conditions. You may not be able to refinance this loan.

Tax DeductionsIf you borrow more than this property is worth, the interest on the loan amount above this property’s fair market value is not deductible from your federal income taxes. You should consult a tax advisor for more information.

Questions? If you have questions about the loan terms or costs on this form, use the contact information below. To get more information or make a complaint, contact the Consumer Financial Protection Bureau at www.consumerfinance.gov/mortgage-closing?

$2,590.00

$101,550.00

$98,660.00

1.25%

10.645%

ABC Bank

123456789

987654321Bob Banker

123-456-7890

1000 Main StreetAnytown, NE 12345

112233

998877

NE

NE

Dirt Sellers Inc.

1200 Oak St.Anytown, NE 12345

7712345John Smith

19283746

123-456-5678

XYZ Title Co.

1200 Main St.Anytown, NE 12345

8877666Sally Title

123-456-1122

13

Banker’s Compliance Consulting 800-847-1653

1

Sample Construction Loan Estimate and Closing Disclosure Key Six-month, Interest-Only Construction Note with a Fixed Rate

Interest Due only on the Amount Advanced Amount and timing of Advances Unknown

LOAN ESTIMATE

Property: The address of the security property

Sale Price: “Sale Price” is used since the security property (i.e. the lot) is being purchased with $10,000 of the loan proceeds.

Purpose: “Purchase” is used because the security property (the lot) will be bought with loan proceeds.

Product: There are five months of interest-only payments, so the product reflects “5 mo. Interest Only, Fixed Rate”. The payment at the end of the six months is the balloon payment. The “Interest Only” feature is disclosed rather than the balloon payment because it “overrides” the balloon payment feature when both occur in the same transaction.

Loan Terms

Loan Amount: The face amount of the Note is $100,000.

Monthly Principal & Interest: Estimated interest is based on half the commitment amount being outstanding for the entire construction period:

½ the Commitment Amount

Initial Interest Rate

Months in a year

$50,000 * 5% / 12 = $208.33

The answer to “Can this amount increase after closing?” is NO because of the following:

• The loan has a fixed interest rate• Interest-only payments are in effect for the entire loan and Appendix D allows us to assume ½ of the

commitment amount is advanced for the entire construction period.

Balloon Payment: The balloon payment is based on the entire commitment amount plus the amount of interest due under the assumption that half the loan amount will be advanced for the entire construction period:

Estimated Monthly Interest

Note Amount

208.33 + $100,000 = $100,208.33

Projected Payments

Principal & Interest:

• Column one shows the interest-only payment, as calculated above.• No range is disclosed due to the fixed interest rate and the assumptions provided under Appendix D.• The final column represents the balloon payment, as calculated above.

Key-

Banker’s Compliance Consulting 800-847-1653

2

Estimated Taxes, Insurance & Assessments: The amounts need to be based on the replacement cost and taxable assessed value of the property in the first year after closing, including any improvements.

Calculating Cash to Close

Total Closing Costs (J):

Total Loan Costs Total Other Costs Lender Credits $2,190 + $550 - 0 = $2,740

Closing Costs Financed (Paid from your Loan Amount):

In this scenario, the only third-party payment at closing is the advance for the lot purchase.

Loan Amount Third-Party Payments other than closing costs

$100,000 - $10,000 = $90,000* If the required calculation results in a negative number or $0, $0 is disclosed for the Closing Costs Financed.

If the required calculation results in a positive number, it is disclosed as a negative number to reduce the cash to close. The amount cannot exceed the Total Closing Costs in Section J.

*Here, the calculation results in a positive $90,000, but since the closing costs financedcannot exceed the Total Closing Costs of $2,740, $2,740 is disclosed.

Down Payment/Funds from Borrower:

Third-party payments

Loan amount after any closing costs financed

$10,000 - (100,000 - $2,740) = -$87,260* *Since the calculation results in a negative number, it is disclosed as Funds for Borrowerand $0 is disclosed as the Down Payment/Funds from Borrower. If the result of thecalculation is a positive number, it would be disclosed as the Down Payment/Funds fromBorrower and $0 is disclosed as Funds for Borrower.

Funds for Borrower:

Third-party payments

Loan amount after any closing costs financed

$10,000 - (100,000 - $2,740) = -$87,260* *Since the calculation results in a negative number, it is disclosed as Funds for Borrowerand $0 is disclosed as the Down Payment/Funds from Borrower. If the result of therequired calculation is a positive number, that number would be disclosed as the DownPayment/Funds from Borrower and $0 is disclosed for Funds for Borrower.

Adjustments and Other Credits: The total amount of undisbursed construction funds is shown as a positive number, which offsets the large negative number in Funds for Borrower.

In other words, you show the undisbursed proceeds as a negative number (reducing the cash to close) going to the borrower in Funds for Borrower; however, you take those proceeds right back with a positive number in Adjustments and Other Credits, increasing the cash to close.

Adjustable Payment (AP) Table: The table is not triggered because there is no change in the payment stream. There are interest-only payments for the entire loan term until the balloon payment due at maturity.

Key-

Banker’s Compliance Consulting 800-847-1653

3

Adjustable Interest Rate (AIR) Table: The table is not triggered because this is a fixed-rate loan.

Comparisons

In 5 Years: The estimated interest to be paid can be based on the assumption of half the loan amount being outstanding for the entire construction period:

½ the Commitment

Amount

Interest Rate

Months in a Year

Months in loan term

Estimated Interest

$50,000 * 5% / 12 * 6 = $1,250

Estimated Interest

Note Amount

Total of Payments (Loan Term < 5 years)

$1,250 + $100,000 = $101,250* *Any closing costs not financed will need to be added to this amount

Annual Percentage Rate (APR): Estimated interest is again based on the assumption that half the note amount is outstanding for the entire construction period.

Estimated Interest

Prepaid Finance Charge

½ the Commitment

Amount

Prepaid Finance Charge

($1,250 + $1,365) * 100 / (50,000 - $1,365) = 5.37678627

Months in Loan Term

Months in a Year

5.37679 / 6 * 12 = 10.75358

Total Interest Percentage: The estimated interest is again based on ½ the commitment amount being outstanding for the entire construction period:

½ the Commitment

Amount

Interest Rate

Months in a Year

Months in loan term

Estimated Interest

Loan Amount

$50,000 * 5% / 12 * 6 = $1,250 / $100,000 = 1.25%

Other Considerations*

*The special consideration here for a construction loan is on the Loan Estimate for the permanent financing. If youwant to take advantage of the ability to reissue a Loan Estimate any time prior to 60 days before closing, the LoanEstimate for the permanent financing should reflect the following disclosure:

You may receive a revised Loan Estimate at any time prior to 60 days before consummation.

CLOSING DISCLOSURE

Property: The address of the security property

Sale Price: “Sale Price” is used since the security property (i.e. the lot) is being purchased with $10,000 of the loan proceeds.

Purpose: “Purchase” is used because the security property (the lot) will be bought with loan proceeds.

Key-

Banker’s Compliance Consulting 800-847-1653

4

Product: There are five months of interest-only payments, so the product reflects “5 mo. Interest Only, Fixed Rate”. The payment at the end of the six months is the balloon payment. The “Interest Only” feature is disclosed rather than the balloon payment because it “overrides” the balloon payment feature when both occur in the same transaction.

Loan Terms

Loan Amount: The face amount of the Note is $100,000.

Monthly Principal & Interest: Estimated interest is based on half the commitment amount being outstanding for the entire construction period:

½ the Commitment Amount

Initial Interest Rate

Months in a year

$50,000 * 5% / 12 = $208.33

The answer to “Can this amount increase after closing?” is NO because of the following:

• The loan has a fixed interest rate• Interest-only payments are in effect for the entire loan and Appendix D allows us to assume ½ of the

commitment amount is advanced for the entire construction period.

Balloon Payment: The balloon payment is based on the entire commitment amount plus the amount of interest due under the assumption that half the loan amount will be advanced for the entire construction period:

Estimated Monthly Interest

Note Amount

208.33 + $100,000 = $100,208.33

Projected Payments

Principal & Interest:

• Column one shows the interest-only payment, as calculated above.• No range is disclosed, due to the fixed interest rate and the assumptions provided under Appendix D.• The final column represents the balloon payment, as calculated above.

Estimated Taxes, Insurance & Assessments: The amounts need to be based on the replacement cost and taxable assessed value of the property in the first year after closing, including any improvements.

Calculating Cash to Close

For calculations in the Loan Estimate column (other than Closing Costs Paid Before Closing) see preceding Loan Estimate instructions.

Total Closing Costs (J):

Total Loan Costs Total Other Costs Lender Credits $2,090 + $550 - 0 = $2,640

Closing Costs Paid Before Closing:

Loan Estimate column is always $0

Key-

Banker’s Compliance Consulting 800-847-1653

5

“Final” column: The Borrower paid the Homeowner’s Insurance Premium ($300) before closing (See Borrower-Paid Before Closing column on page 2 of the Closing Disclosure).

Closing Costs Financed (Paid from your Loan Amount):

In this scenario, the only third-party payment at closing is the advance for the lot purchase.

Loan Amount Third-Party Payments other than closing costs

$100,000 - $10,000 = $90,000*

If the required calculation results in a negative number or $0, $0 is disclosed for the Closing Costs Financed.

If the required calculation results in a positive number, it is disclosed as a negative number to reduce the cash to close. The amount cannot exceed the sum of the amounts disclosed under Total Closing Costs (Section J) and Closing Costs Paid Before Closing.

*Here, the calculation results in a positive $90,000, but since the closing costsfinanced cannot exceed the sum of the Total Closing Costs of $2,640 and any ClosingCosts Paid Before Closing ($300), $2,340 is disclosed.

Down Payment/Funds from Borrower:

Third-party payments

Loan amount after any closing costs financed

$10,000 - (100,000 - $2,340) = -$87,660* *Since the calculation results in a negative number, it is disclosed as Funds forBorrower and $0 is disclosed as the Down Payment/Funds from Borrower. If the resultof the calculation is a positive number, that number would be disclosed as the DownPayment/Funds from Borrower and $0 is disclosed as Funds for Borrower.

Funds for Borrower:

Third-party payments

Loan amount after any closing costs financed

$10,000 - (100,000 - $2,340) = -$87,660* *Since the calculation results in a negative number, it is disclosed as Funds forBorrower and $0 is disclosed as the Down Payment/Funds from Borrower. Ifthe result of the calculation is a positive number, that number would bedisclosed as the Down Payment/Funds from Borrower and $0 is disclosed forFunds for Borrower.

Adjustments and Other Credits: The total amount of undisbursed construction funds is shown as a positive number, which offsets the large negative number in Funds for Borrower..

In other words, you show the undisbursed proceeds as a negative number (reducing the cash to close) going to the borrower in Funds for Borrower; however, you take those proceeds right back with a positive number in Adjustments and Other Credits, increasing the cash to close.

Summaries of Transactions

Due from Borrower at Closing: The amount of undisbursed construction loan proceeds held by the creditor is identified under Adjustments in Section K.

Adjustable Payment (AP) Table: The table is not triggered because there is no change in the payment stream. There are interest-only payments for the entire term of the loan until the balloon payment due at maturity.

Key-

Banker’s Compliance Consulting 800-847-1653

6

Adjustable Interest Rate (AIR) Table: The table is not triggered because this is a fixed-rate loan.

Loan Calculations

Total of Payments:

½ the Commitment Amount

Interest Rate

Months in a Year

Months in loan term

Estimated Interest

$50,000 * 5% / 12 * 6 = $1,250

Estimated Interest

Note Amount

Closing Costs Paid Before Closing

$1,250 + $100,000 + $300 = $101,550* *Any closing costs not financed will need to be added to this amount

Finance Charge:

Estimated Interest

Prepaid Finance Charge*

$1,250 + $1,340 = $2,590 *Inspection Fee, Origination Charge, Flood Determination andSettlement Agent Fee

APR: Estimated interest is again based on the assumption that half the note amount is outstanding for the entire construction period.

Estimated Interest

Prepaid Finance Charge

½ the Commitment

Amount

Prepaid Finance Charge

($1,250 + $1,340) * 100 / (50,000 - $1,340) = 5.3226

Months in Loan Term

Months in a Year

5.3226 / 6 * 12 = 10.645

Total Interest Percentage (TIP):

½ the Commitment

Amount

Interest Rate

Months in a Year

Months in loan term

Estimated Interest

Note Amount

Total Interest

Percentage $50,000 * 5% / 12 * 6 = $1,250 / $100,000 = 1.25%

Key-

![Fifty years of Soviet aircraft construction [only designs]](https://static.fdocuments.net/doc/165x107/5584eefbd8b42a78618b4d83/fifty-years-of-soviet-aircraft-construction-only-designs.jpg)

![APS Construction Update Nov2011 [Read-Only]](https://static.fdocuments.net/doc/165x107/61f541822ab9d82eab781bb5/aps-construction-update-nov2011-read-only.jpg)