S Corp Eligibility & Available Elections

39

What’s New Type Here 10 - S Corporation Eligibility & Available Elections 1 Page 177-205

Transcript of S Corp Eligibility & Available Elections

What’s NewType Here

10 - S Corporation Eligibility & Available Elections 1

Page 177-205

II. Number of ShareholdersShareholder limit problem solved with a couple of partnerships – PLR 201544020

10 - S Corporation Eligibility & Available Elections 2

Page 178

III. Allowed Shareholders

HOWEVER

Subject to Unrelated Business Income Tax (UBIT) –Organization must report income on Form 990T and may have income tax liability

10 - S Corporation Eligibility & Available Elections 3

Page 179

III. Allowed Shareholders

10 - S Corporation Eligibility & Available Elections 4

Page 179

Any plan organized under IRC 401 Caution

Other Retirement Plans Watch for failure to distribute

Subject to UBIT –

IRAs (i.e. SEPs, SIMPLE IRAs, and ROTHs) are not qualified shareholders

III. Allowed Shareholders

10 - S Corporation Eligibility & Available Elections 7

Page 179

Non-voting stock is not another class IF both voting and non-voting shares have identical rights to liquidation and distribution. All events must be per share per day.

V. One Class of Stock Rules

10 - S Corporation Eligibility & Available Elections 10

Page 181

V. One Class of Stock RulesIn the event there a distributions that do not conform to the corporate agreements will not alone create a second class as well.

10 - S Corporation Eligibility & Available Elections 12

Page 181

V. One Class of Stock RulesPractices should always demand that we advise our clients to NEVER take disproportionate distributions and if it happens simply repair and do not panic

10 - S Corporation Eligibility & Available Elections 15

Page 182

V. One Class of Stock RulesH. The real DANGER

Disproportionate distributions or loans are most likely to be attacked as compensation or taxable gift

10 - S Corporation Eligibility & Available Elections 17

Page 184

V. One Class of Stock Rules

Current attitude at IRS – If S status is inadvertently terminated fix ASAP

10 - S Corporation Eligibility & Available Elections 18

Page 184

VI. Qualified SubchapterS Trusts (QSSTs)

All items from the S-Corp to the beneficiary must be passed through, regardless of whether they were in fact distributed, i.e. QSSTs act like a disregarded entity.

10 - S Corporation Eligibility & Available Elections 19

Page 184

VI. Qualified SubchapterS Trusts (QSSTs)

A QSST can be used for both income and estate planning as an effective transfer tool.

10 - S Corporation Eligibility & Available Elections 21

Page 185

VI. Qualified SubchapterS Trusts (QSSTs)

Inadvertent termination due to failure to make an election – Indicative of “accidental failures”.

10 - S Corporation Eligibility & Available Elections 22

Page 187

VII. Electing Small Business Trusts (ESBTS)

Carefully monitor during estate administration to avoid invalid trust ownership that can create an ineligible S/H –Relief is available for errors, Rev. Proc. 2013-30. (No family aggregation rule for 100 S/H limit)

10 - S Corporation Eligibility & Available Elections 23

Page 187

2410 - S Corporation Eligibility & Available Elections

S Corporation Eligibility ChecklistPage 189

VIII. Filing an S Election on Form 2553The Compliance Issues – Failure of any of the three items will make the election invalid

1. The corporation must make the election as evidenced by the signature of a corporate officer

2. The acceptance of the shareholders evidenced by signature, this can be made on separate statements and attached to Form 2553.

3. The indication of the tax year

10 - S Corporation Eligibility & Available Elections 25

Page 190

VIII. Filing an S Election on Form 2553B. The filing of Form 2553

which can be done with the 1120S is a corrective procedure.

C. The entity is an S Corporation until terminated – this can be done voluntarily or by oops I made a mistake.

10 - S Corporation Eligibility & Available Elections 26

Page 190

VIII. Filing an S Election on Form 2553Tax TipConsider using the practitioner’s address to insure all notices of deficiency of Form 2553 are received by your office as there are only thirty days to repair a flawed election and use PDS (Proof of Delivery Service)Maintain file copies of: S Corporation S status acceptance letter Corporate formation documents Form 2553 with signature dates

10 - S Corporation Eligibility & Available Elections 28

Page 191

IX. Shareholder’s ConsentA. All shareholders must sign and

consent is binding.

B. Consent is required of anyone who held shares during tax year until date of filing

C. If curative action is required of the S-Election ALL shareholders (including deceased shareholders) who held stock until the date of the filing are required to consent to S status.

10 - S Corporation Eligibility & Available Elections 29

Page 192

IX. Shareholder’s ConsentI. Can the taxpayer change their

mind?

1. Have until the final day for making the election, i.e. 15th day of the third month.

2. It is a if the election never occurred.

3. Only some number greater than 50%, the number required to elect revocation, are required to sign for rescission.

Yes or No

Election

10 - S Corporation Eligibility & Available Elections 31

Page 193

X. QSUB Election

In all things S-Corp another demonstration that IRS is willing to overlook procedural errors. Best practice – get procedures in place.

10 - S Corporation Eligibility & Available Elections 33

Page 195

XI. Repairing a Late or Invalid S Election

A. An S election is invalid if:1. Ineligible corporation2. Form 2553 not properly

completed

B. IRS does have statutory authority to waive invalid election and allow S election to become effective.

10 - S Corporation Eligibility & Available Elections 34

Page 195

XI. Repairing a Late or Invalid S Election

C. The specifics – IRC 1362(f) permits the IRS to treat the entity as S status qualified during the period of failure if:

1. The failure was inadvertent2. It is corrected within a reasonable period

after discovery3. During the failed period the entity and the

shareholders agree to be treated as an S Corp

10 - S Corporation Eligibility & Available Elections 35

Page 195

TAX TIP – When the Rev. Proc. fails, you may consider beggingWHY:

1. Cheaper than a PLR

2. Gives you a chance to work on your writing skills

3. Story telling is a lost art

XII. Methods of Obtaining Relief from a Late or Invalid S Corporation Election

10 - S Corporation Eligibility & Available Elections 38

Page 196-197

With all the noise, chatter and problems of fixing many elections IRS in the September of 2013 provides Rev. Proc. 2013-30 effective date 09/03/2013.

XIII. Revenue Procedure 2013-30, Late Election Relief

10 - S Corporation Eligibility & Available Elections 39

Page 197

The request can be made within 3 years and 75 days of the Effective Date

The relief is also available for returns that have been late filed.

But you need a reasonable cause

XIII. Revenue Procedure 2013-30, Late Election Relief

10 - S Corporation Eligibility & Available Elections 40

Page 198

XIV. General Requirements for Relief Under Rev. Proc. 2013-30

Type Here

10 - S Corporation Eligibility & Available Elections 41

Page 198

XV. General Procedural Requirements for Relief Under Rev. Proc. 2013-30

To obtain the relief under the Rev. Proc. the taxpayer must:A. Properly complete election form.B. Demonstrate the Reasonable Cause/Inadvertence

1. What is the reasonable cause2. What actions were taken to correct the mistake

on discovery.

10 - S Corporation Eligibility & Available Elections 43

Page 198

XV. General Procedural Requirements for Relief Under Rev. Proc. 2013-30

To obtain the relief under the Rev. Proc. the taxpayer must:C. File the election form with the Service Center in

one of three manners.1. Attach to current year Form 1120S2. Attach to late filed prior year Form 1120S

Initial return(s) that include Form 2553 need to carefully reflect the instructions of Rev. Proc. 2013-30. When late filing multiple returns ALL returns would appear as follow:

10 - S Corporation Eligibility & Available Elections 44

Page 199

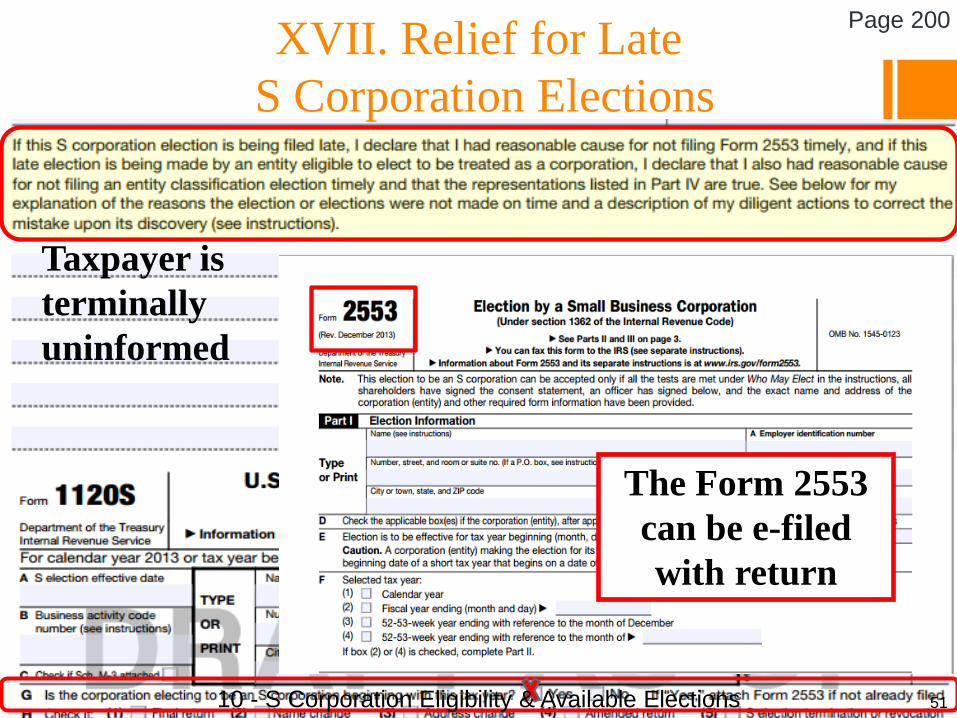

When filing Form 2553 with Form 1120S it is critical that tax year, effective date and Box G all be completed correctly

XV. General Procedural Requirements for Relief Under Rev. Proc. 2013-30

INCLUDES LATE ELECTION FILED PURSUANT TO REV. PROC. 2013-30

10 - S Corporation Eligibility & Available Elections 45

Page 199

XV. General Procedural Requirements for Relief Under Rev. Proc. 2013-30

To obtain the relief under the Rev. Proc. the taxpayer must:C. File the election form with the Service Center in

one of three manners.3. Submit the election form to the IRS Service

Center with 3 years and 75 days of effective date

10 - S Corporation Eligibility & Available Elections 46

Page 199

Change 2016 Form 1120S to 2017 Form 1120S

XV. General Procedural Requirements for Relief Under Rev. Proc. 2013-30

3. The election can be filed independent of Form 1120S by sending to IRS Service Center that return was to be filed at within the relief period of 3 years and 75 days

10 - S Corporation Eligibility & Available Elections 48

Page 199

XV. General Procedural Requirements for Relief Under Rev. Proc. 2013-30

D. All requests for relief should always include a statement of signed under Penalties of Perjury.

Signed by a corporate officer, not by the preparer, not by the attorney and not by a POA but by the officer.

10 - S Corporation Eligibility & Available Elections 49

Page 200

File the 2553: Insure that form is signed by authorized person All persons that were shareholders at any time

during period of relief requested sign statements “under penalties of perjury” including statements that: All returns have been filed. All items of income and expense were

included on the shareholders return consistent with the election.

XVII. Relief for LateS Corporation Elections

10 - S Corporation Eligibility & Available Elections 50

Page 200

XVII. Relief for LateS Corporation Elections

Taxpayer is terminally uninformed

The Form 2553 can be e-filed with return

10 - S Corporation Eligibility & Available Elections 51

Page 200

The taxpayer has filed as an S Corp in the past and IRS says “We have NO record of the entity filing Form 2553” – The taxpayer should indicate:A. This is not relief under Rev. Proc. 2013-30.B. Failure is solely due to no Form 2553 on file.C. All shareholders treated every year as S Corporation

shareholders on Form 1040.D. More than 6 months has passed since initial filing.E. No IRS notification has been received by the entity or

any shareholders within 6 months of initial filing.F. Entity completes and files Form 2553.

XVIII. Relief for S Corpsthat have Filed Returns

10 - S Corporation Eligibility & Available Elections 52

Page 201

Rev. Proc. 2013-30

NEWPage 203

10 - S Corporation Eligibility & Available Elections 53

Rev. Proc. 2013-30

NEWPage 204

10 - S Corporation Eligibility & Available Elections 54

Rev. Proc. 2013-30

NEWPage 205

10 - S Corporation Eligibility & Available Elections 55