Russell Galer Financial Affairs Division Directorate of Financial, Fiscal and Enterprise Affairs

28

Pension Fund Governance: OECD Principles, Governance & Investment International Seminar on Pension Reform for Civil Servants and Complementary Pension Funds Brazilia, Brazil 1-2 October 2003 Russell Galer Financial Affairs Division Directorate of Financial, Fiscal and Enterprise Affairs Organisation for Economic Co-operation and Development

-

Upload

hiram-miles -

Category

Documents

-

view

29 -

download

0

description

Pension Fund Governance: OECD Principles, Governance & Investment International Seminar on Pension Reform for Civil Servants and Complementary Pension Funds Brazilia, Brazil 1-2 October 2003. Russell Galer Financial Affairs Division Directorate of Financial, Fiscal and Enterprise Affairs - PowerPoint PPT Presentation

Transcript of Russell Galer Financial Affairs Division Directorate of Financial, Fiscal and Enterprise Affairs

Pension Fund Governance:OECD Principles, Governance &

Investment

International Seminar on Pension Reform for Civil Servants and Complementary Pension Funds

Brazilia, Brazil1-2 October 2003

Russell GalerFinancial Affairs DivisionDirectorate of Financial, Fiscal and Enterprise AffairsOrganisation for Economic Co-operation and Development

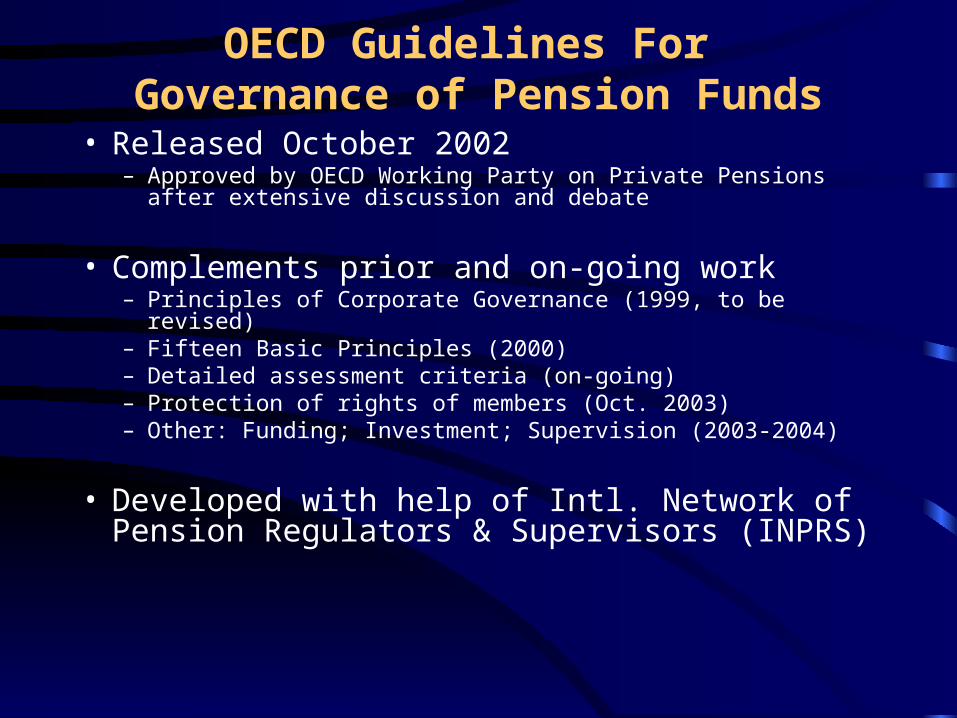

OECD Guidelines For Governance of Pension Funds

• Released October 2002– Approved by OECD Working Party on Private Pensions after

extensive discussion and debate

• Complements prior and on-going work– Principles of Corporate Governance (1999, to be revised) – Fifteen Basic Principles (2000)– Detailed assessment criteria (on-going)– Protection of rights of members (Oct. 2003)– Other: Funding; Investment; Supervision (2003-2004)

• Developed with help of Intl. Network of Pension Regulators & Supervisors (INPRS)

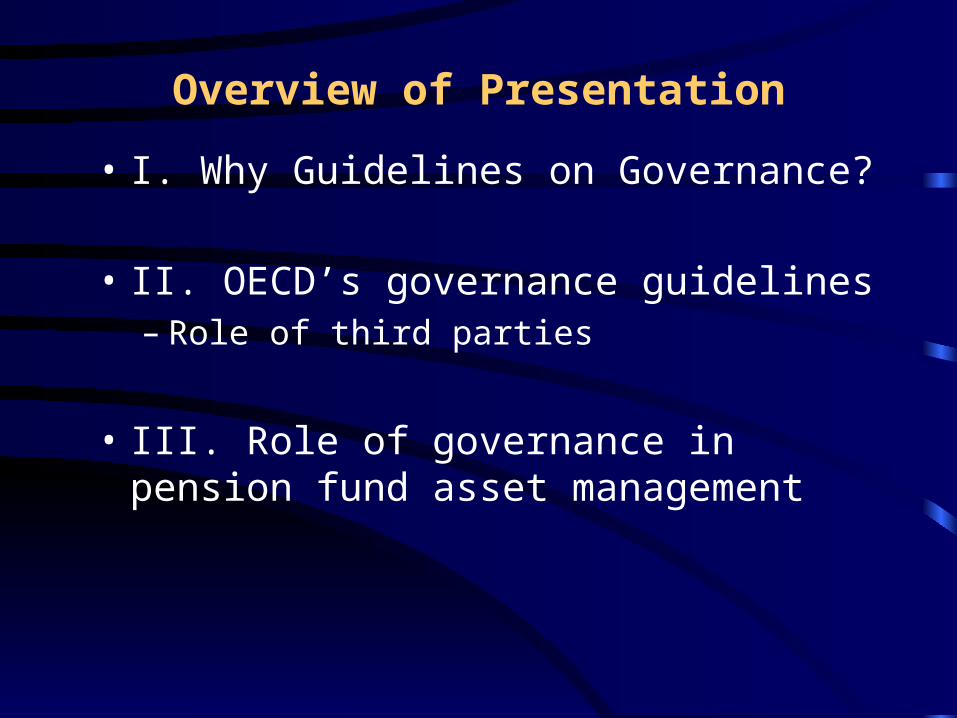

Overview of Presentation

• I. Why Guidelines on Governance?

• II. OECD’s governance guidelines– Role of third parties

• III. Role of governance in pension fund asset management

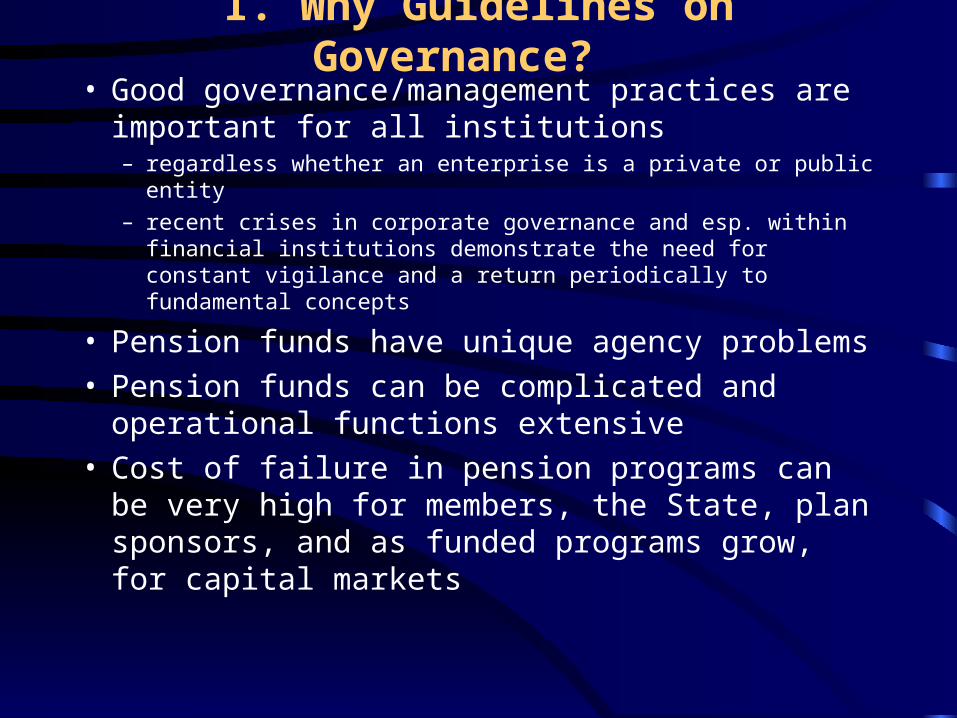

I. Why Guidelines on Governance? • Good governance/management practices are

important for all institutions– regardless whether an enterprise is a private or public entity

– recent crises in corporate governance and esp. within financial institutions demonstrate the need for constant vigilance and a return periodically to fundamental concepts

• Pension funds have unique agency problems• Pension funds can be complicated and operational

functions extensive• Cost of failure in pension programs can be very

high for members, the State, plan sponsors, and as funded programs grow, for capital markets

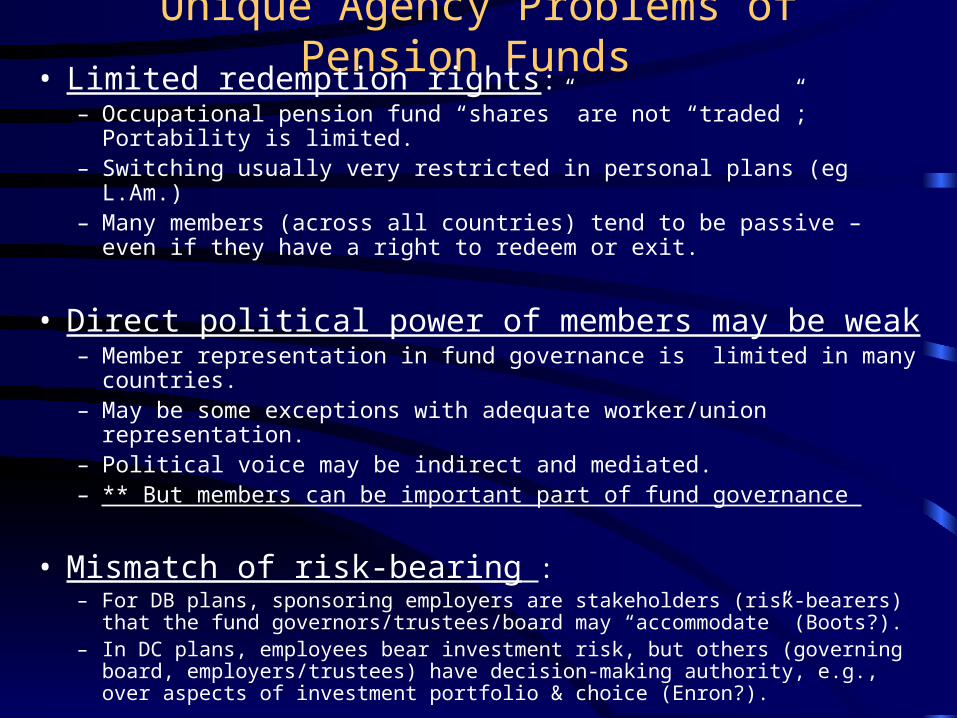

Unique Agency Problems of Pension Funds • Limited redemption rights:

– Occupational pension fund “shares” are not “traded”; Portability is limited. – Switching usually very restricted in personal plans (eg L.Am.)– Many members (across all countries) tend to be passive – even if they have

a right to redeem or exit.

• Direct political power of members may be weak– Member representation in fund governance is limited in many countries. – May be some exceptions with adequate worker/union representation. – Political voice may be indirect and mediated. – ** But members can be important part of fund governance

• Mismatch of risk-bearing :– For DB plans, sponsoring employers are stakeholders (risk-bearers) that the fund

governors/trustees/board may “accommodate” (Boots?). – In DC plans, employees bear investment risk, but others (governing board,

employers/trustees) have decision-making authority, e.g., over aspects of investment portfolio & choice (Enron?).

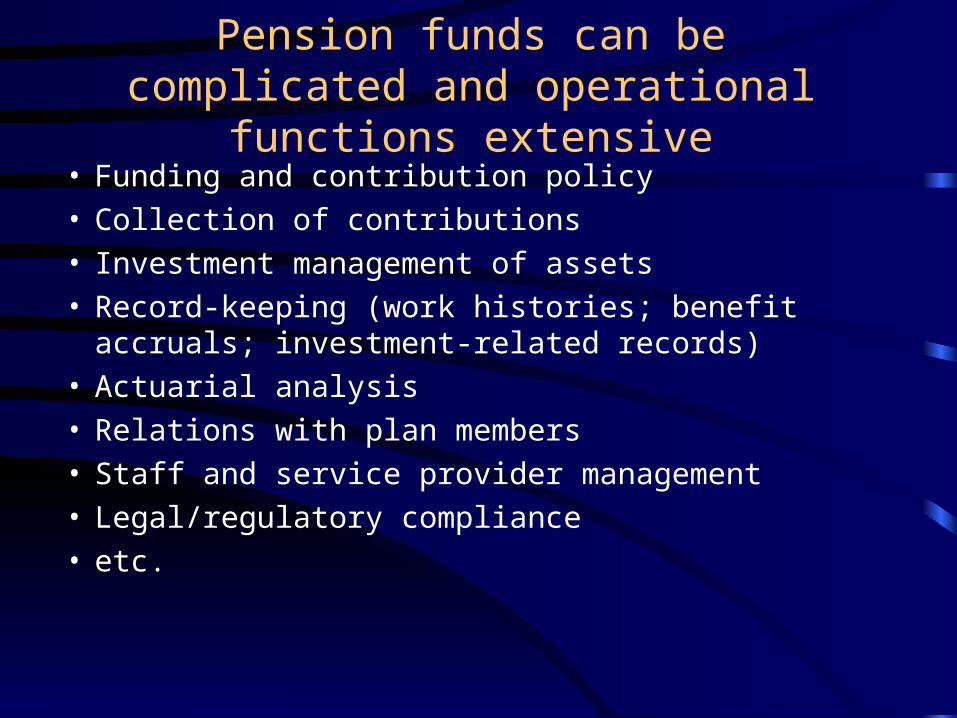

Pension funds can be complicated and operational functions extensive

• Funding and contribution policy• Collection of contributions• Investment management of assets• Record-keeping (work histories; benefit accruals; investment-

related records)• Actuarial analysis• Relations with plan members• Staff and service provider management• Legal/regulatory compliance • etc.

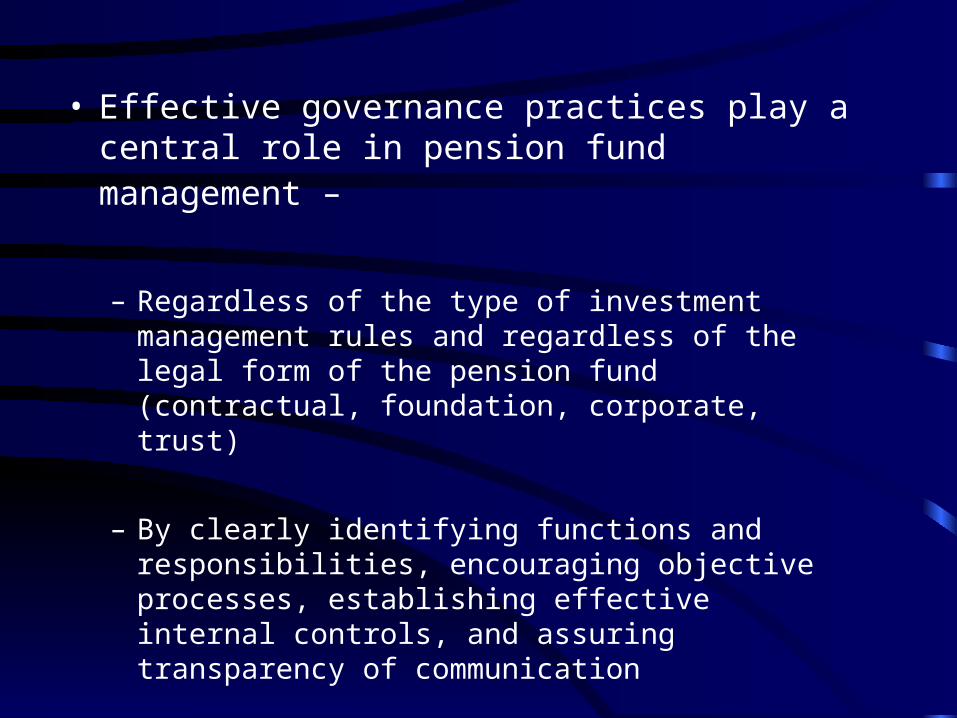

• Effective governance practices play a central role in pension fund management –

– Regardless of the type of investment management rules and regardless of the legal form of the pension fund (contractual, foundation, corporate, trust)

– By clearly identifying functions and responsibilities, encouraging objective processes, establishing effective internal controls, and assuring transparency of communication

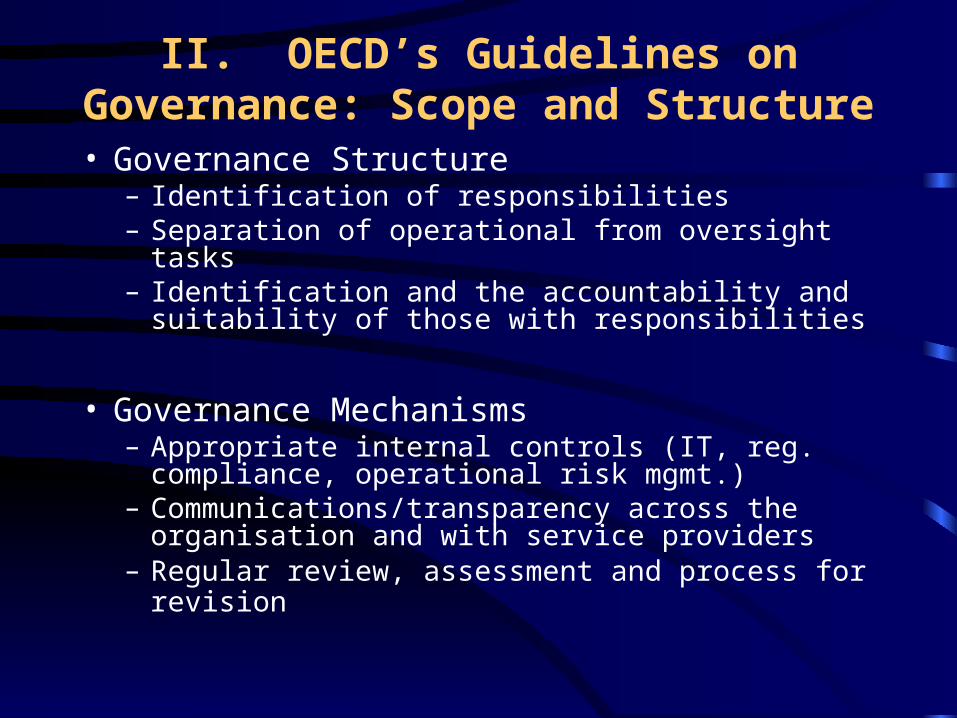

II. OECD’s Guidelines on Governance: Scope and Structure

• Governance Structure– Identification of responsibilities– Separation of operational from oversight tasks– Identification and the accountability and suitability of

those with responsibilities

• Governance Mechanisms– Appropriate internal controls (IT, reg. compliance,

operational risk mgmt.)– Communications/transparency across the organisation

and with service providers– Regular review, assessment and process for revision

12 governance guidelines

• STRUCTURE• Identification of

responsibilities• Governing body• Expert advice*• Auditor*• Actuary*• Custodian*

• MECHANISMS• Internal Controls• Reporting• Disclosure• Redress

Structure: Who is responsible for what tasks? • WHO? Clearly vest power in an identified

governing body– Establish accountability of governing body to members

and competent authorities; legal liability

• DOING WHAT? Establish appropriate, clear division of operational & oversight responsibilities

– Set forth legal form, governance structure and plan objectives in relevant documents (statute, by-laws, contracts, trust instruments, etc.)

• ARE THEY CAPABLE? Ensure suitability of those with with operational and oversight responsibilities

– Integrity; professionalism

– Encourage use of experts/professionals if necessary to assure fully informed decision-making and fulfillment of responsibilities

Governance – Internal ControlsGovernance – Internal Controlsn Transparency of process, including effective lines Transparency of process, including effective lines

of communication and reporting within an of communication and reporting within an organisation and with external service providersorganisation and with external service providers

n Appropriate risk management Appropriate risk management

n Effective regulatory compliance programsEffective regulatory compliance programs

n Regular testing, monitoring and updating of Regular testing, monitoring and updating of information technology systems and processesinformation technology systems and processes

n Identification, monitoring, correcting/sanctioning Identification, monitoring, correcting/sanctioning of conflict of interest matters and of the of conflict of interest matters and of the improper use of privileged information improper use of privileged information

Governance - External PartiesGovernance - External Parties

n Pension funds should utilize specialized Pension funds should utilize specialized industry expertise where needed industry expertise where needed

n Third parties may exert independent oversight Third parties may exert independent oversight of the governing body and internal operations, of the governing body and internal operations, performing a crucial monitoring functionperforming a crucial monitoring function

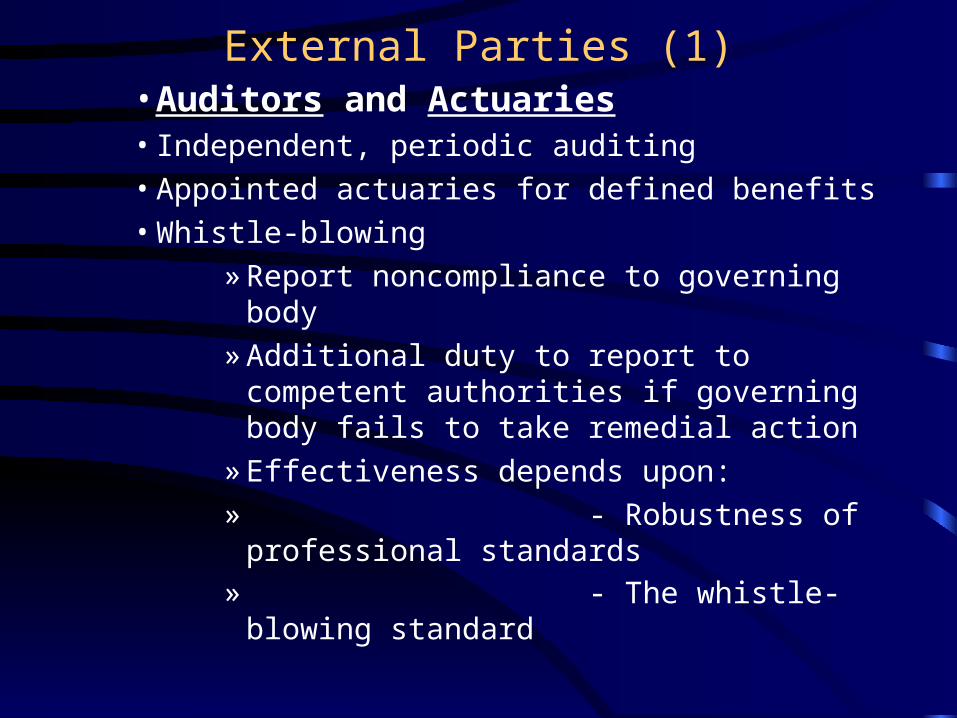

External Parties (1)• Auditors and Actuaries• Independent, periodic auditing

• Appointed actuaries for defined benefits

• Whistle-blowing

» Report noncompliance to governing body

» Additional duty to report to competent authorities if governing body fails to take remedial action

» Effectiveness depends upon:

» - Robustness of professional standards» - The whistle-blowing standard

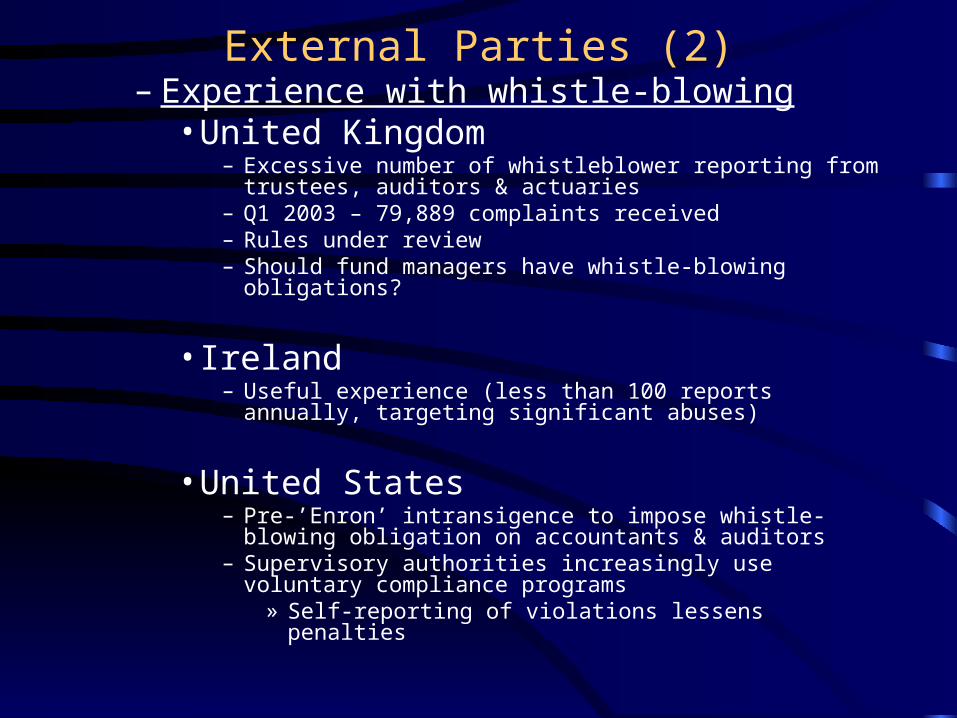

External Parties (2)– Experience with whistle-blowing

• United Kingdom– Excessive number of whistleblower reporting from trustees,

auditors & actuaries – Q1 2003 – 79,889 complaints received – Rules under review– Should fund managers have whistle-blowing obligations?

• Ireland – Useful experience (less than 100 reports annually, targeting

significant abuses)

• United States – Pre-’Enron’ intransigence to impose whistle-blowing obligation

on accountants & auditors– Supervisory authorities increasingly use voluntary compliance

programs» Self-reporting of violations lessens penalties

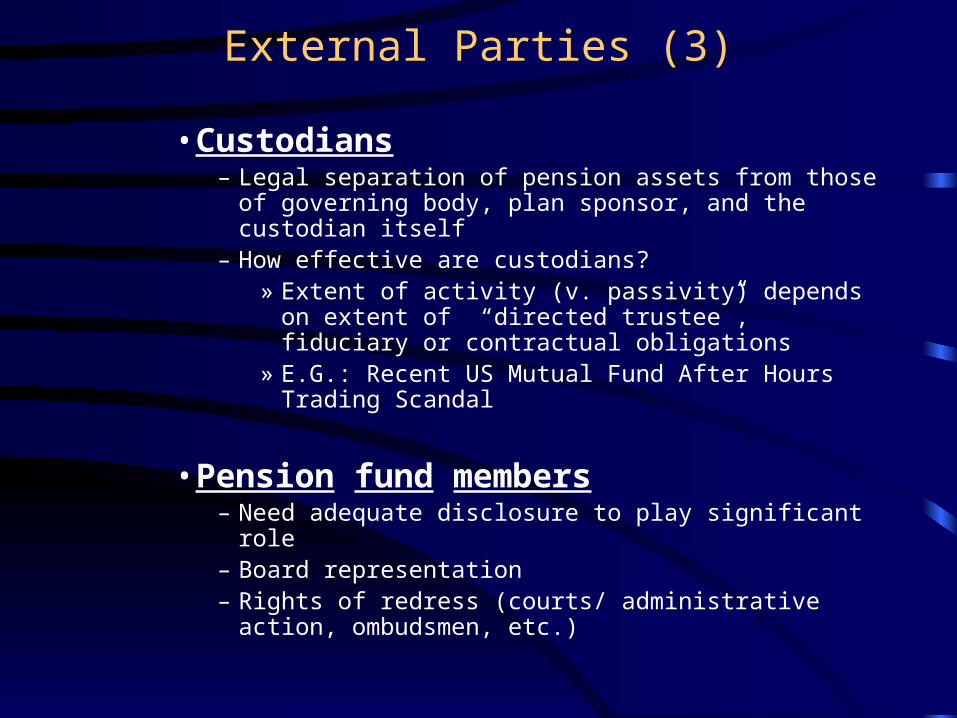

External Parties (3)

• Custodians– Legal separation of pension assets from those of

governing body, plan sponsor, and the custodian itself– How effective are custodians?

» Extent of activity (v. passivity) depends on extent of “directed trustee”, fiduciary or contractual obligations

» E.G.: Recent US Mutual Fund After Hours Trading Scandal

• Pension fund members– Need adequate disclosure to play significant role – Board representation – Rights of redress (courts/ administrative action,

ombudsmen, etc.)

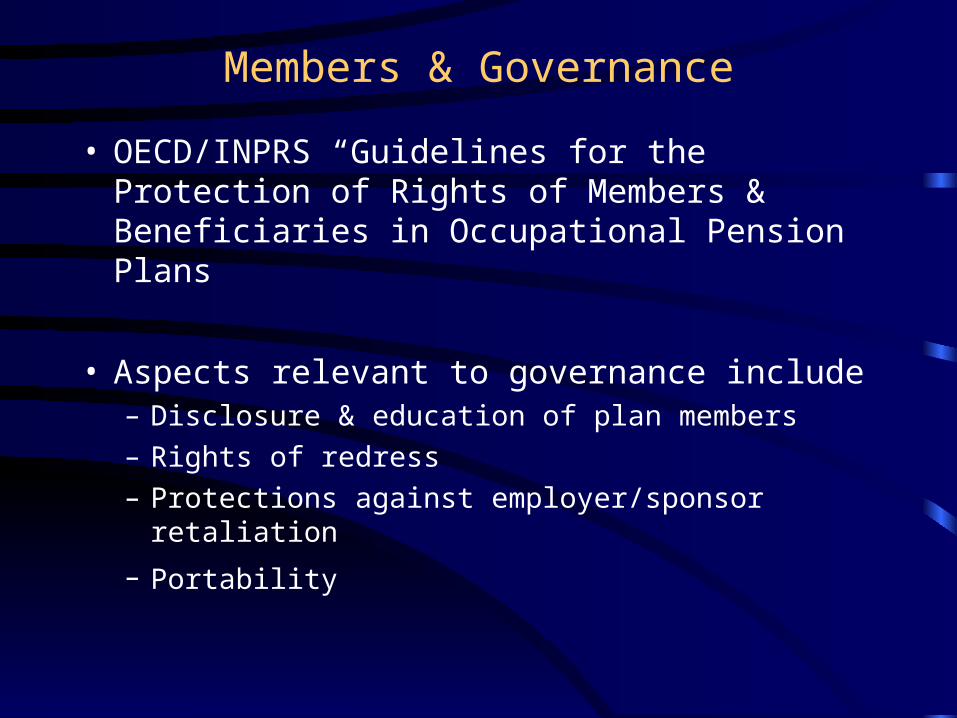

Members & Governance

• OECD/INPRS “Guidelines for the Protection of Rights of Members & Beneficiaries in Occupational Pension Plans

• Aspects relevant to governance include – Disclosure & education of plan members

– Rights of redress

– Protections against employer/sponsor retaliation

– Portability

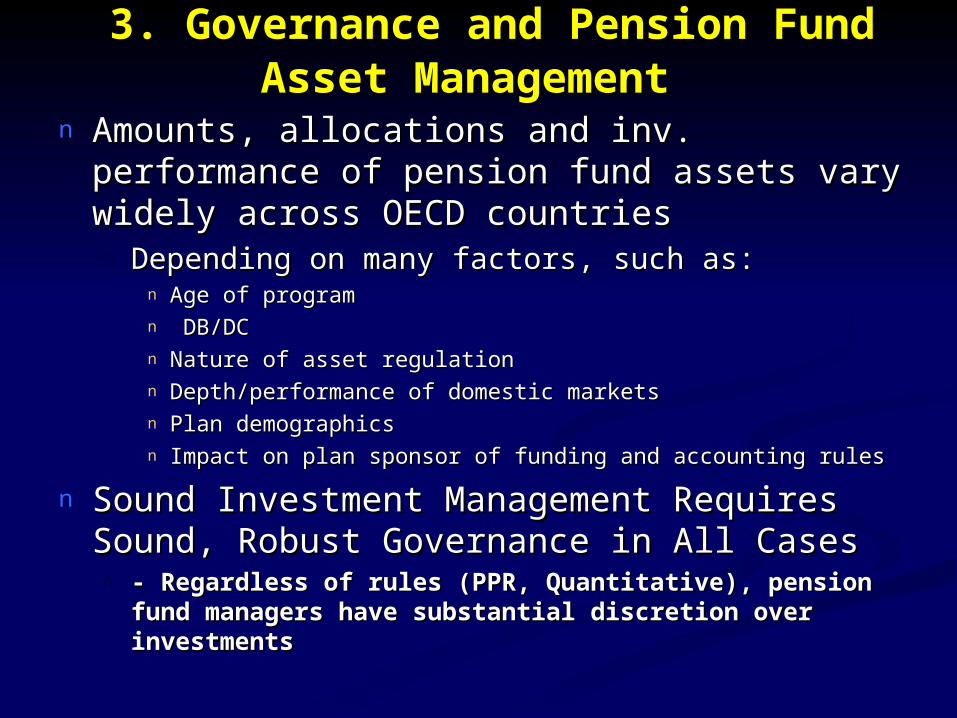

3. Governance and Pension Fund 3. Governance and Pension Fund Asset ManagementAsset Management

n Amounts, allocations and inv. performance of pension Amounts, allocations and inv. performance of pension fund assets vary widely across OECD countriesfund assets vary widely across OECD countriesn Depending on many factors, such as:Depending on many factors, such as:

n Age of programAge of programn DB/DCDB/DCn Nature of asset regulationNature of asset regulationn Depth/performance of domestic marketsDepth/performance of domestic marketsn Plan demographicsPlan demographicsn Impact on plan sponsor of funding and accounting rulesImpact on plan sponsor of funding and accounting rules

n Sound Investment Management Requires Sound, Sound Investment Management Requires Sound, Robust Governance in All CasesRobust Governance in All Casesn - Regardless of rules (PPR, Quantitative), pension fund managers - Regardless of rules (PPR, Quantitative), pension fund managers

have substantial discretion over investmentshave substantial discretion over investments

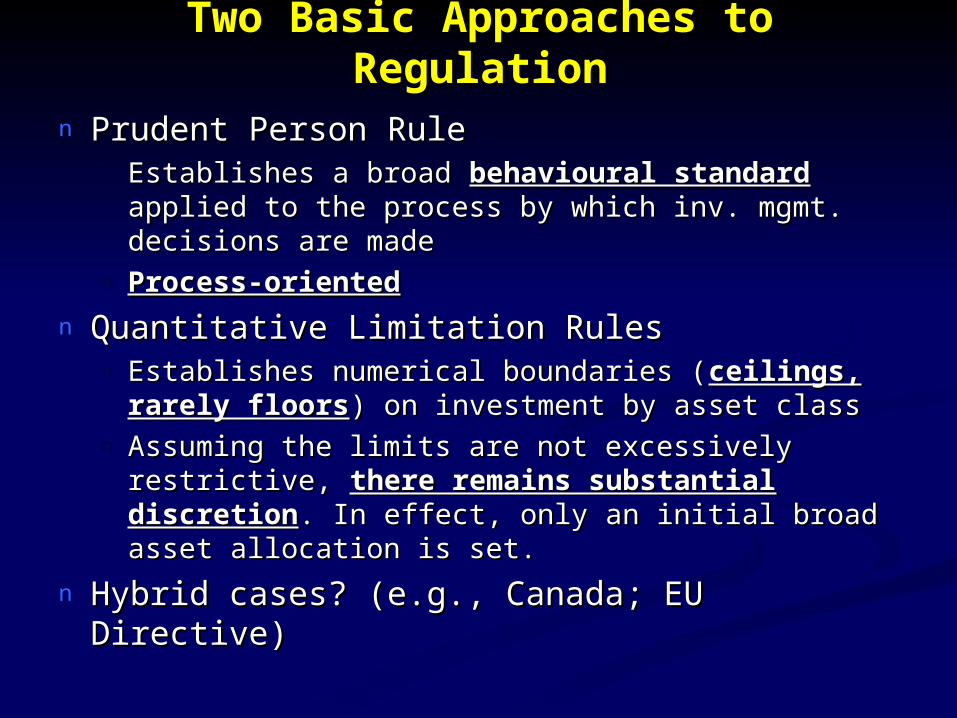

Two Basic Approaches to Two Basic Approaches to RegulationRegulation

n Prudent Person RulePrudent Person Rulen Establishes a broad Establishes a broad behavioural standardbehavioural standard applied to the applied to the

process by which inv. mgmt. decisions are madeprocess by which inv. mgmt. decisions are maden Process-orientedProcess-oriented

n Quantitative Limitation RulesQuantitative Limitation Rulesn Establishes numerical boundaries (Establishes numerical boundaries (ceilings, rarely floorsceilings, rarely floors) )

on investment by asset classon investment by asset classn Assuming the limits are not excessively restrictive, Assuming the limits are not excessively restrictive, there there

remains substantial discretionremains substantial discretion. In effect, only an initial . In effect, only an initial broad asset allocation is set.broad asset allocation is set.

n Hybrid cases? (e.g., Canada; EU Directive)Hybrid cases? (e.g., Canada; EU Directive)

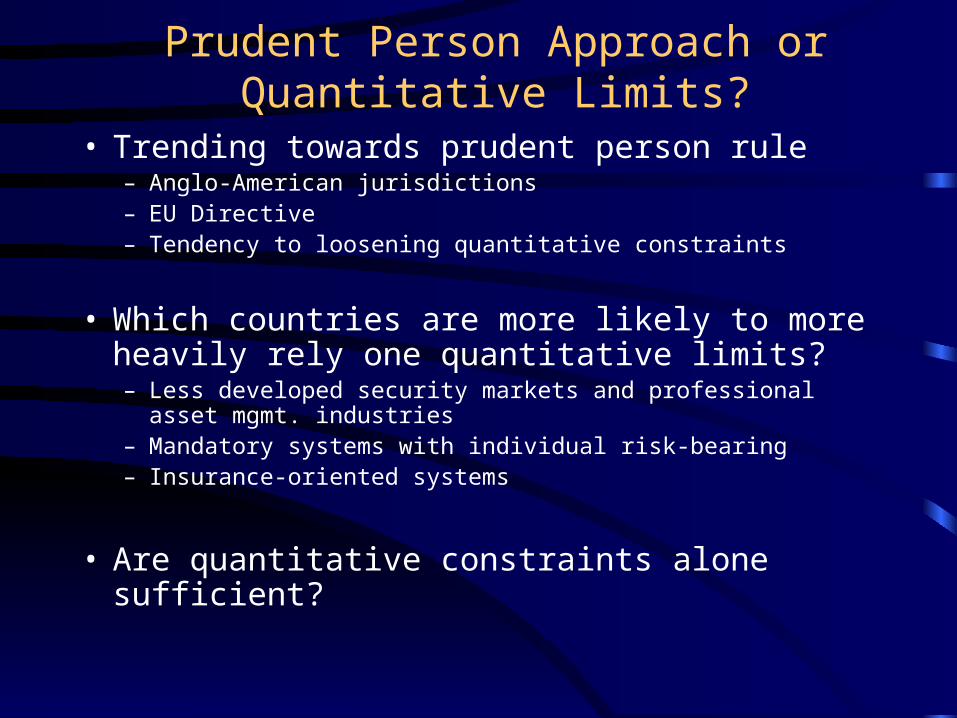

Prudent Person Approach or Quantitative Limits?

• Trending towards prudent person rule– Anglo-American jurisdictions– EU Directive– Tendency to loosening quantitative constraints

• Which countries are more likely to more heavily rely one quantitative limits?– Less developed security markets and professional asset mgmt.

industries– Mandatory systems with individual risk-bearing– Insurance-oriented systems

• Are quantitative constraints alone sufficient?

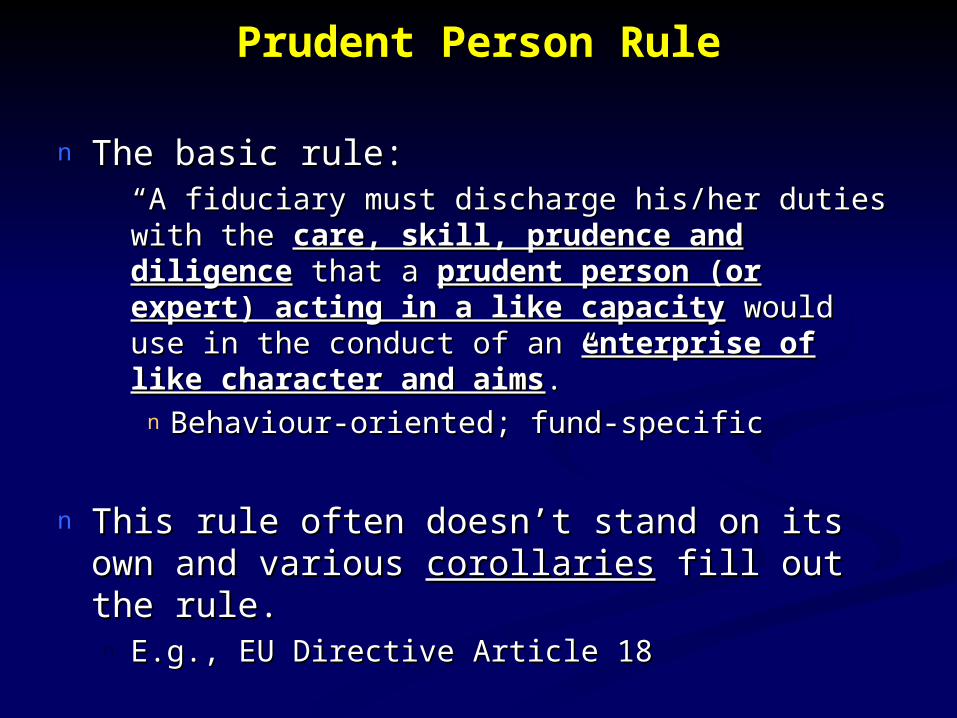

Prudent Person RulePrudent Person Rule

n The basic rule: The basic rule: n ““A fiduciary must discharge his/her duties with the A fiduciary must discharge his/her duties with the care, care,

skill, prudence and diligenceskill, prudence and diligence that a that a prudent person (or prudent person (or expert) acting in a like capacityexpert) acting in a like capacity would use in the conduct would use in the conduct of an of an enterprise of like character and aimsenterprise of like character and aims.”.”n Behaviour-oriented; fund-specificBehaviour-oriented; fund-specific

n This rule often doesn’t stand on its own and various This rule often doesn’t stand on its own and various corollariescorollaries fill out the rule. fill out the rule. n E.g., EU Directive Article 18E.g., EU Directive Article 18

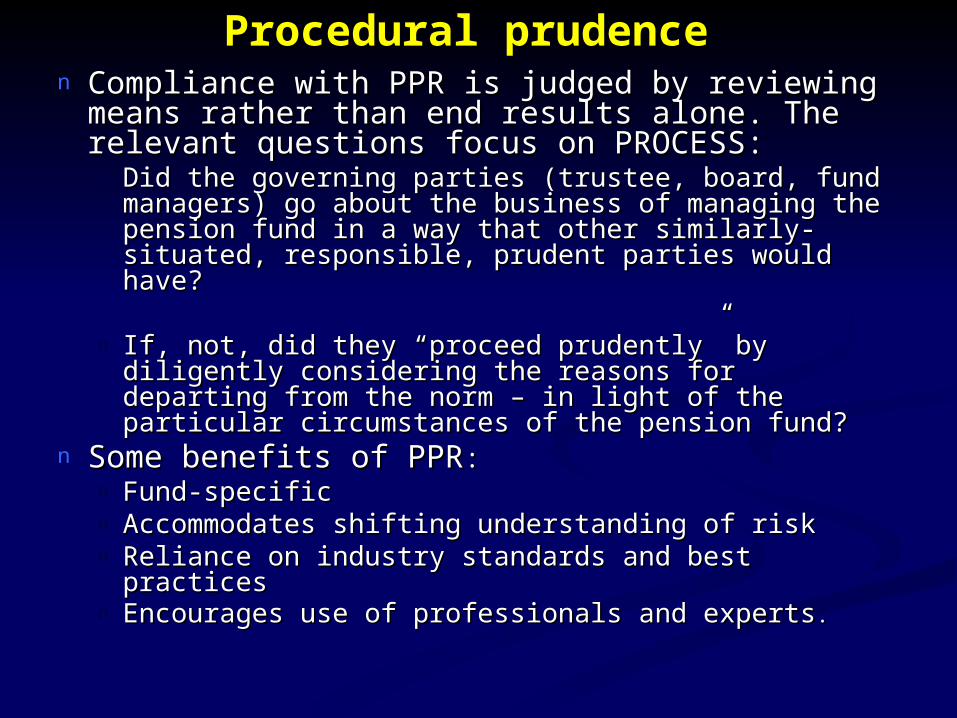

Procedural prudence Procedural prudence n Compliance with PPR is judged by reviewing means Compliance with PPR is judged by reviewing means

rather than end results alone. The relevant questions rather than end results alone. The relevant questions focus on PROCESS:focus on PROCESS: n Did the governing parties (trustee, board, fund managers) Did the governing parties (trustee, board, fund managers)

go about the business of managing the pension fund in a go about the business of managing the pension fund in a way that other similarly-situated, responsible, prudent way that other similarly-situated, responsible, prudent parties would have? parties would have?

n If, not, did they “proceed prudently” by diligently If, not, did they “proceed prudently” by diligently considering the reasons for departing from the norm – in considering the reasons for departing from the norm – in light of the particular circumstances of the pension fund?light of the particular circumstances of the pension fund?

n Some benefits of PPRSome benefits of PPR: : n Fund-specificFund-specificn Accommodates shifting understanding of riskAccommodates shifting understanding of riskn Reliance on industry standards and best practicesReliance on industry standards and best practicesn Encourages use of professionals and expertsEncourages use of professionals and experts..

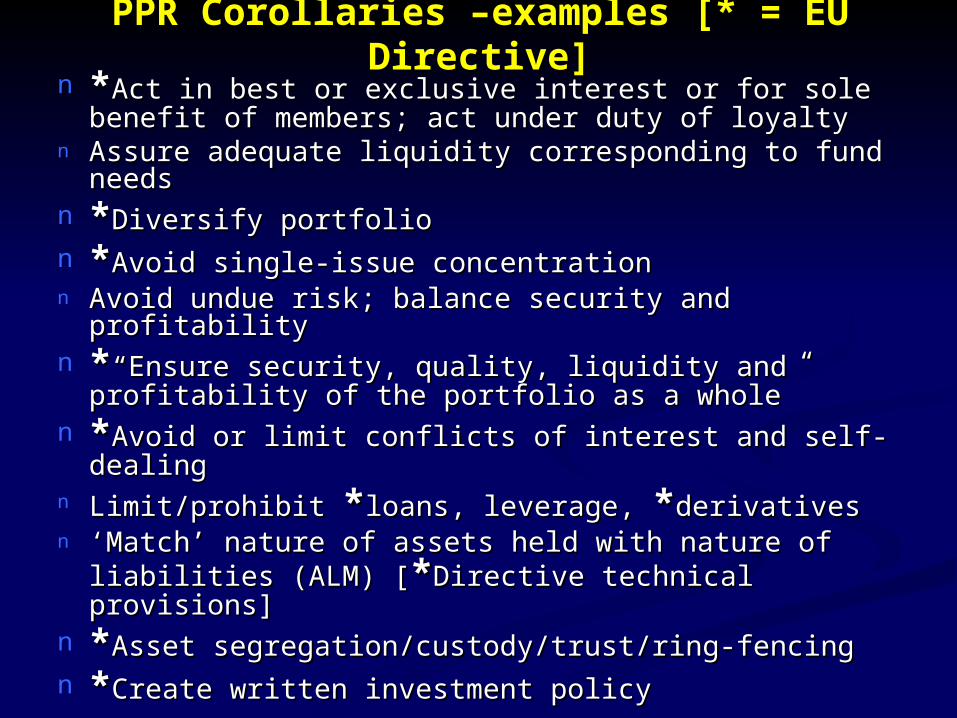

PPR Corollaries –examples [* = EU PPR Corollaries –examples [* = EU Directive]Directive]

n **Act in best or exclusive interest or for sole benefit of Act in best or exclusive interest or for sole benefit of members; act under duty of loyaltymembers; act under duty of loyalty

n Assure adequate liquidity corresponding to fund needsAssure adequate liquidity corresponding to fund needsn **Diversify portfolioDiversify portfolion **Avoid single-issue concentrationAvoid single-issue concentrationn Avoid undue risk; balance security and profitabilityAvoid undue risk; balance security and profitabilityn **“Ensure security, quality, liquidity and profitability of the “Ensure security, quality, liquidity and profitability of the

portfolio as a whole”portfolio as a whole”n **Avoid or limit conflicts of interest and self-dealingAvoid or limit conflicts of interest and self-dealingn Limit/prohibit Limit/prohibit **loans, leverage, loans, leverage, **derivativesderivativesn ‘‘Match’ nature of assets held with nature of liabilities (ALM) Match’ nature of assets held with nature of liabilities (ALM)

[[**Directive technical provisions]Directive technical provisions]n **Asset segregation/custody/trust/ring-fencingAsset segregation/custody/trust/ring-fencingn **Create written investment policy Create written investment policy

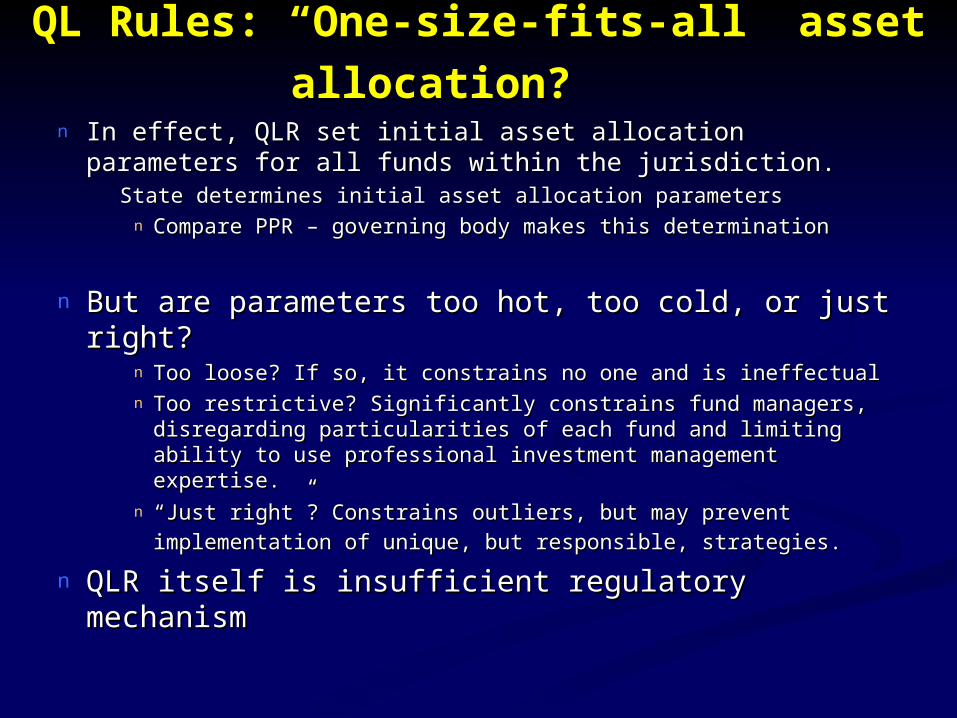

QL Rules: “One-size-fits-all” asset QL Rules: “One-size-fits-all” asset

allocation?allocation? n In effect, QLR set initial asset allocation parameters for all In effect, QLR set initial asset allocation parameters for all

funds within the jurisdiction. funds within the jurisdiction. n State determines initial asset allocation parametersState determines initial asset allocation parameters

n Compare PPR – governing body makes this determinationCompare PPR – governing body makes this determination

n But are parameters too hot, too cold, or just right?But are parameters too hot, too cold, or just right?n Too loose? If so, it constrains no one and is ineffectualToo loose? If so, it constrains no one and is ineffectualn Too restrictive? Significantly constrains fund managers, Too restrictive? Significantly constrains fund managers,

disregarding particularities of each fund and limiting ability to use disregarding particularities of each fund and limiting ability to use professional investment management expertise.professional investment management expertise.

n ““Just right”? Constrains outliers, but may prevent implementation Just right”? Constrains outliers, but may prevent implementation

of unique, but responsible, strategies.of unique, but responsible, strategies.

n QLR itself is insufficient regulatory mechanismQLR itself is insufficient regulatory mechanism

As a result, QLR jurisdictions use qualitative As a result, QLR jurisdictions use qualitative ‘corollaries’ ‘corollaries’

n Italy:Italy:n --Sole interest of members; Sole interest of members; n -Investment policy; -Investment policy; n -Diversification principle; -Diversification principle; n -Avoid single company concentration; -Avoid single company concentration;

-Efficient resource management (contain and minimize -Efficient resource management (contain and minimize transaction and management costs);transaction and management costs);

n -Governing body monitoring obligation; -Governing body monitoring obligation; n -3rd party depository; -3rd party depository; n -Use of professional investment managers [Fondi pensione -Use of professional investment managers [Fondi pensione

negoziali (FPN)]negoziali (FPN)]

As a result QLR jurisdictions use As a result QLR jurisdictions use ‘corollaries’ too‘corollaries’ too

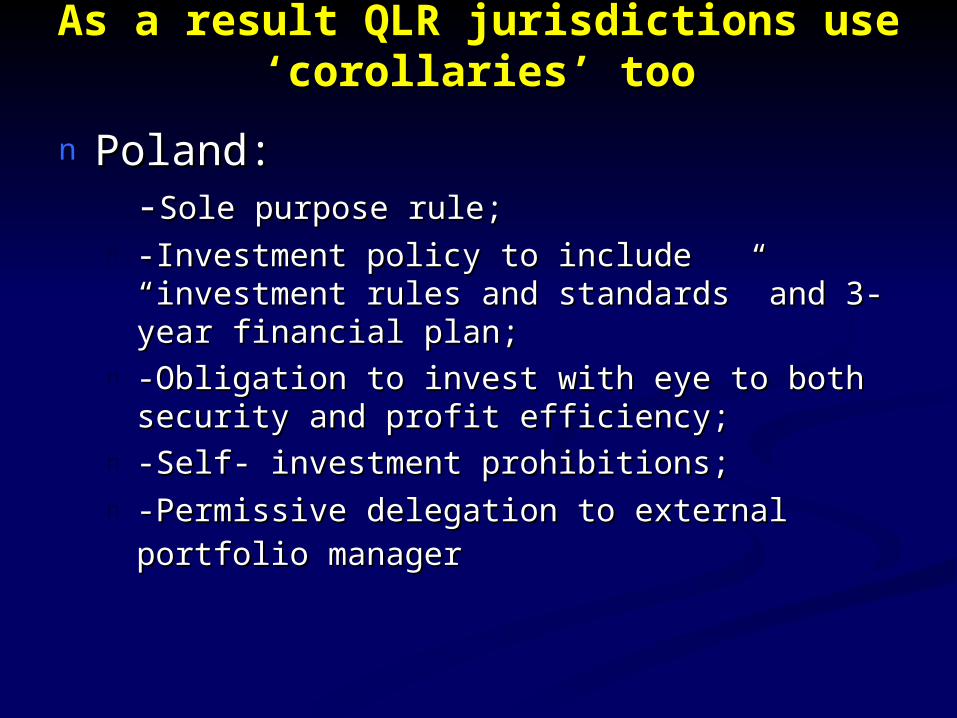

n Poland:Poland:n --Sole purpose rule; Sole purpose rule; n -Investment policy to include “investment rules and -Investment policy to include “investment rules and

standards” and 3-year financial plan; standards” and 3-year financial plan; n -Obligation to invest with eye to both security and profit -Obligation to invest with eye to both security and profit

efficiency; efficiency; n -Self- investment prohibitions; -Self- investment prohibitions;

n -Permissive delegation to external portfolio manager-Permissive delegation to external portfolio manager

As a result QLR jurisdictions use As a result QLR jurisdictions use ‘corollaries’ too‘corollaries’ too

n Slovak Republic [Supp. Pension Insur. Co.s Slovak Republic [Supp. Pension Insur. Co.s (SPICs)](SPICs)]n --Principle of careful and rational persons; Principle of careful and rational persons; n -1-year and 5-year financial plan and investment strategy; -1-year and 5-year financial plan and investment strategy; n -Liquidity requirement; -Liquidity requirement; n -Self-investment prohibition; -Self-investment prohibition; n -Independent custodian-Independent custodian

Why governance? Why governance?

n Investment management function alone is extremely Investment management function alone is extremely complex. PPR and QLR approaches both leave substantial complex. PPR and QLR approaches both leave substantial discretion to the pension fund’s governing body discretion to the pension fund’s governing body

n Determine investment policy in light of overall risk preferences, Determine investment policy in light of overall risk preferences, anticipated liquidity needs, contribution expectations, and long and short anticipated liquidity needs, contribution expectations, and long and short term plan obligationsterm plan obligations

n Establish asset allocation parameters of portfolioEstablish asset allocation parameters of portfolion Consider role of alternative asset classesConsider role of alternative asset classesn Consider investment style/techniques (passive/active; growth/value, etc.) Consider investment style/techniques (passive/active; growth/value, etc.) n Investment manager selection (internal/external)Investment manager selection (internal/external)n Individual security selection (stock-picking)Individual security selection (stock-picking)n Conducting necessary transactions (buy/sell; best execution)Conducting necessary transactions (buy/sell; best execution)n Consider fees and other costsConsider fees and other costsn Monitor and review of performance (benchmarking, etc.)Monitor and review of performance (benchmarking, etc.)n Reassessment of overall policy Reassessment of overall policy

Thank you.Thank you.