A Satellite View NORTH AFRICA = ARAB AFRICA Sub-Saharan Africa = Black Africa.

Upload

gerald-fosterCategory

view

230download

0

Rudie NelStellenbosch University South [email protected]

Gerhard NienaberUniversity of Pretoria

South [email protected]

a

Accounts for about 10% of South Africa's manufacturing exports - crucial cog in the economy

Contributes about 7.5% to South Africa's gross domestic product (GDP)

Provides employment to about 36 000 people

Separate tax effective from 1 September 2010 levied on new vehicles per gram per kilometre of CO2 emissions exceeding 120g/km (SARS 2010:192)

USD$ 10,56 per gram exceeding 120g/km

Average tax rate of between 2,3% - 3,6% expected (SARS 2010:192)

Purpose = attempt to reduce CO2 emissions by influencing consumer purchasing decisions (encouraging purchase of lower CO2-emitting vehicles)

Prospects of achieving its purpose in South Africa could be affected by the following factors (Nel 2009:4):

The design of the vehicle emissions tax Effective in reducing CO2 emissions?

Risk of unilateral implementation? Could affect competitiveness

Legislation Influence fiscal policy and planning as well as the effectiveness

of the tax base or the instruments used

Consumer attitudes Fiscal policy should not only target consumers

A model system for the assessment of the effects of vehicle and fuel emissions tax on CO2 emissions (Hayashi, Kato & Val 2001)

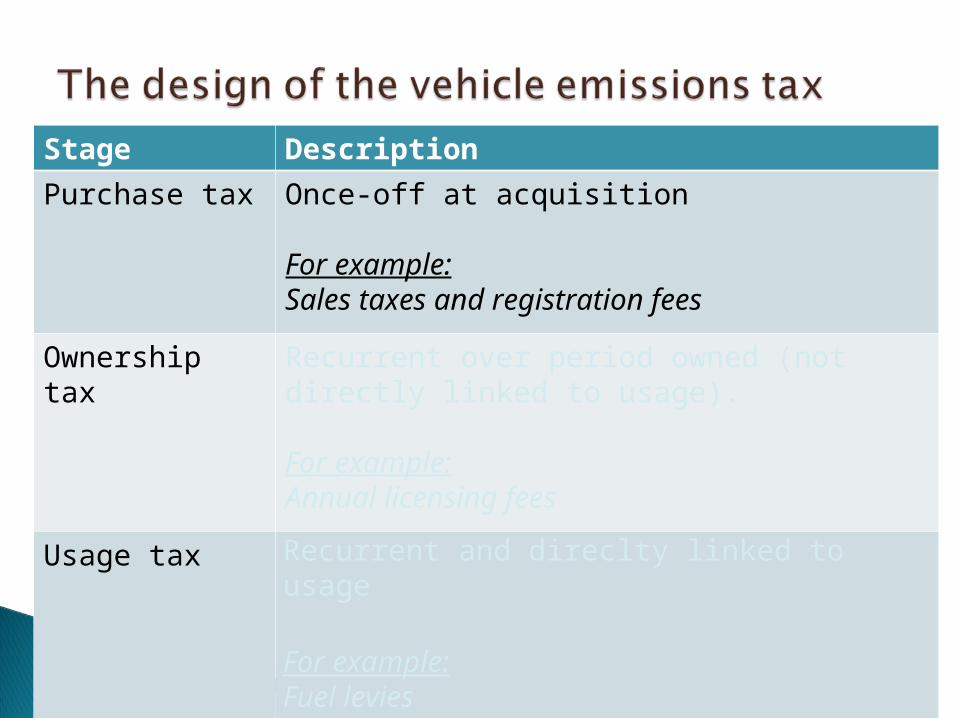

Categorised into three stages: Purchase tax Ownership tax Usage tax

Levying taxes in certain stages might be more effective in reducing CO2 emissions than in other stages

Stage Description

Purchase tax Once-off at acquisition

For example:Sales taxes and registration fees

Ownership tax Recurrent over period owned (not directly linked to usage).

For example:Annual licensing fees

Usage tax Recurrent and direclty linked to usage

For example:Fuel levies

Stage Description

Purchase tax Once-off at acquisition

For example:Sales taxes and registration fees

Ownership tax Recurrent over period owned (not directly linked to usage)

For example:Annual licensing fees

Usage tax Recurrent and direclty linked to usage

For example:Fuel levies

Stage Description

Purchase tax Once-off at acquisition.

For example:Sales taxes and registration fees

Ownership tax Recurrent over period owned (not directly linked to usage)

For example:Annual licensing fees

Usage tax Recurrent and direclty linked to usage

For example:Fuel levies

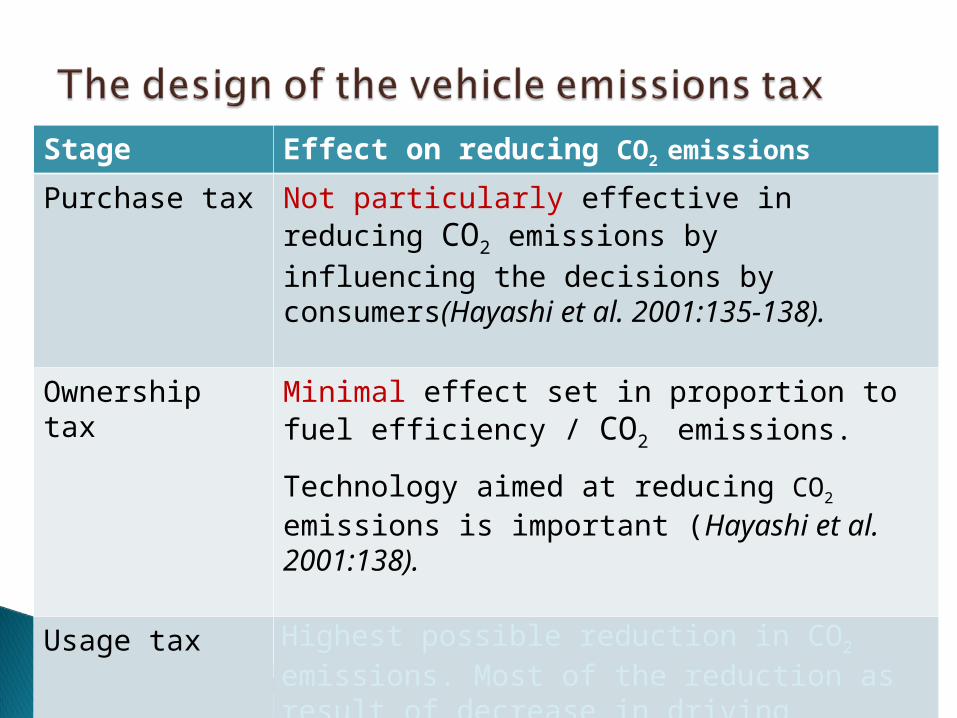

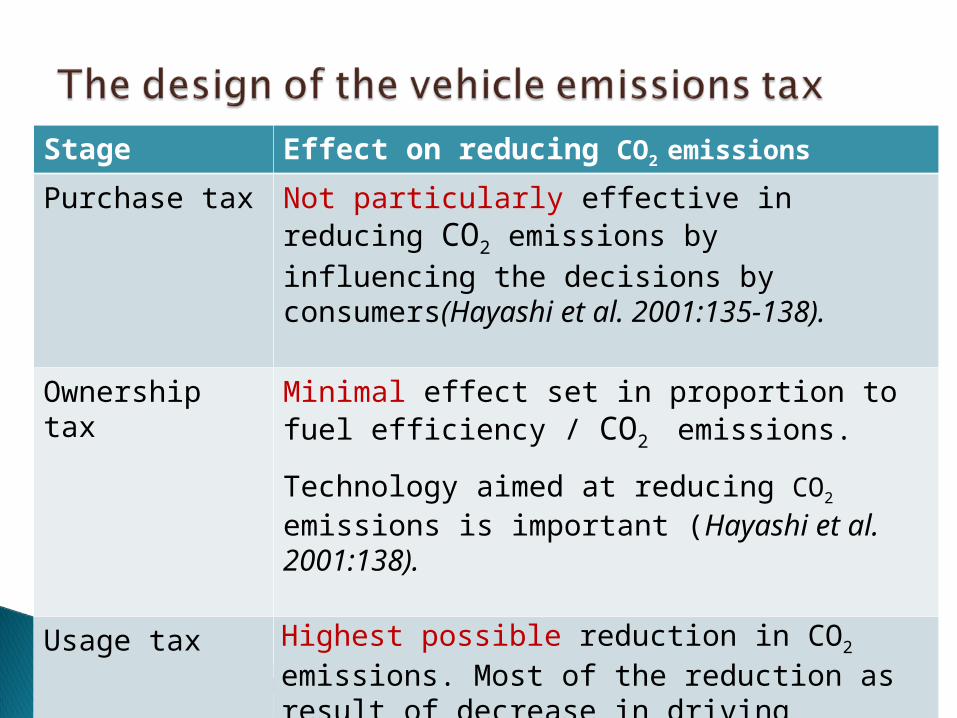

Stage Effect on reducing CO2 emissions

Purchase tax Not particularly effective in reducing CO2 emissions by influencing the decisions by consumers(Hayashi et al. 2001:135-138).

Ownership tax Minimal effect set in proportion to fuel efficiency / CO2 emissions.

Technology aimed at reducing CO2 emissions is important (Hayashi et al. 2001:138).

Usage tax Highest possible reduction in CO2 emissions. Most of the reduction as result of decrease in driving distance (Hayashi et al. 2001:135).

Stage Effect on reducing CO2 emissions

Purchase tax Not particularly effective in reducing CO2 emissions by influencing the decisions by consumers(Hayashi et al. 2001:135-138).

Ownership tax Minimal effect set in proportion to fuel efficiency / CO2 emissions.

Technology aimed at reducing CO2 emissions is important (Hayashi et al. 2001:138).

Usage tax Highest possible reduction in CO2 emissions. Most of the reduction as result of decrease in driving distance (Hayashi et al. 2001:135).

Stage Effect on reducing CO2 emissions

Purchase tax Not particularly effective in reducing CO2 emissions by influencing the decisions by consumers(Hayashi et al. 2001:135-138).

Ownership tax Minimal effect set in proportion to fuel efficiency / CO2 emissions.

Technology aimed at reducing CO2 emissions is important (Hayashi et al. 2001:138).

Usage tax Highest possible reduction in CO2 emissions. Most of the reduction as result of decrease in driving distance (Hayashi et al. 2001:135).

Stage Effect on reducing CO2 emissions

Purchase tax Not particularly effective in reducing CO2 emissions by influencing the decisions by consumers(Hayashi et al. 2001:135-138).

Ownership tax Minimal effect set in proportion to fuel efficiency / CO2 emissions.

Technology aimed at reducing CO2 emissions is important (Hayashi et al. 2001:138).

Usage tax Highest possible reduction in CO2 emissions. Most of the reduction as result of decrease in driving distance (Hayashi et al. 2001:135).

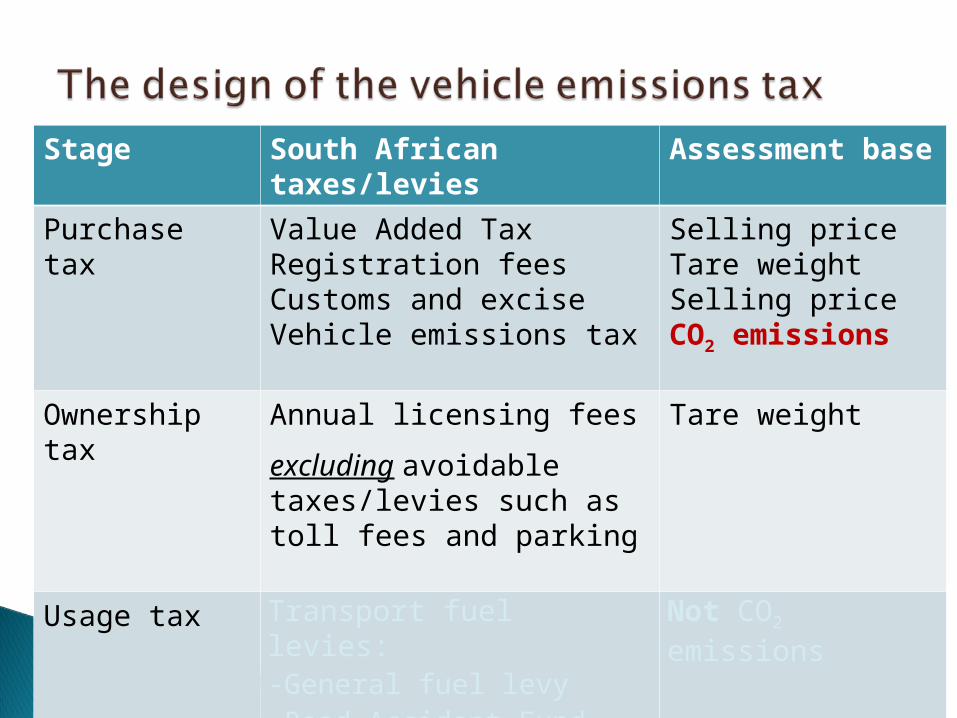

Stage South African taxes/levies

Assessment base

Purchase tax Value Added TaxRegistration feesCustoms and exciseVehicle emissions tax

Selling priceTare weightSelling priceCO2 emissions

Ownership tax

Annual licensing fees

excluding avoidable taxes/levies such as toll fees and parking

Tare weight

Usage tax Transport fuel levies: -General fuel levy-Road Accident Fund levy-Customs and excise levy

Not CO2

emissions

Stage South African taxes/levies

Assessment base

Purchase tax Value Added TaxRegistration feesCustoms and exciseVehicle emissions tax

Selling priceTare weightSelling priceCO2 emissions

Ownership tax

Annual licensing fees

excluding avoidable taxes/levies such as toll fees and parking

Tare weight

Usage tax Transport fuel levies: -General fuel levy-Road Accident Fund levy-Customs and excise levy

Not CO2

emissions

Stage South African taxes/levies

Assessment base

Purchase tax Value Added TaxRegistration feesCustoms and exciseVehicle emissions tax

Selling priceTare weightSelling priceCO2 emissions

Ownership tax

Annual licensing fees

excluding avoidable taxes/levies such as toll fees and parking

Tare weight

Usage tax Transport fuel levies: -General fuel levy-Road Accident Fund levy-Customs and excise levy

Not CO2

emissions

Stage South African taxes/levies

Assessment base

Purchase tax Value Added TaxRegistration feesCustoms and exciseVehicle emissions tax

Selling priceTare weightSelling priceCO2 emissions

Ownership tax

Annual licensing fees

excluding avoidable taxes/levies such as toll fees and parking

Tare weight

Usage tax Transport fuel levies: -General fuel levy-Road Accident Fund levy-Customs and excise levy

Not CO2

emissions

Stage South African taxes/levies

Assessment base

Purchase tax Value Added TaxRegistration feesCustoms and exciseVehicle emissions tax

Selling priceTare weightSelling priceCO2 emissions

Ownership tax

Annual licensing fees

excluding avoidable taxes/levies such as toll fees and parking

Tare weight

Usage tax Transport fuel levies: -General fuel levy-Road Accident Fund levy-Customs and excise levy

Not CO2

emissions

Stage South African taxes/levies

Assessment base

Purchase tax Value Added TaxRegistration feesCustoms and exciseVehicle emissions tax

Selling priceTare weightSelling priceCO2 emissions

Ownership tax

Annual licensing fees

excluding avoidable taxes/levies such as toll fees and parking

Tare weight

Usage tax Transport fuel levies: -General fuel levy-Road Accident Fund levy-Customs and excise levy

Not CO2

emissions

Stage South African taxes/levies

Assessment base

Purchase tax Value Added TaxRegistration feesCustoms and exciseVehicle emissions tax

Selling priceTare weightSelling priceCO2 emissions

Ownership tax

Annual licensing fees

excluding avoidable taxes/levies such as toll fees and parking

Tare weight

Usage tax Transport fuel levies: -General fuel levy-Road Accident Fund levy-Customs and excise levy

Not CO2

emissions

Focus on consumers

Focus on new vehicles

Current status of South African motor industry

No distinction between petrol and diesel driven

vehicles

The purpose of the vehicle emissions tax is to discourage the purchase of vehicles that emit higher CO2 emissions.

A tax benefit (tax deduction) could mitigate the effect of the vehicle emissions tax to act as a deterrent.

Based on study performed:◦Provisions of South African Income Tax Act do allow for a deduction for the vehicle emissions tax.

Vehicle emissions tax (purchase tax) is a step in the right direction

Design could however not be most effective in reducing CO2 emissions

Could be expanded to result in most reduction of CO2

emissions

A “feebate” policy and investing in fuel technologies Consisting of “carrots” (incentives) and “sticks” (additional taxes) Study performed in United States argued the merit and the

importance of manufacturers’ adoption of fuel economy technologies, which accounted for about 90% of the overall increase in fuel economy (Greene et al. 2005:758-759)

Vehicle emissions tax earmarked and allocated to vehicle manufacturers to encourage investment in technology to reduce CO2 emissions

Increasing fuel levies (should be pro-poor)

Introducing new charges (should be carefully considered)

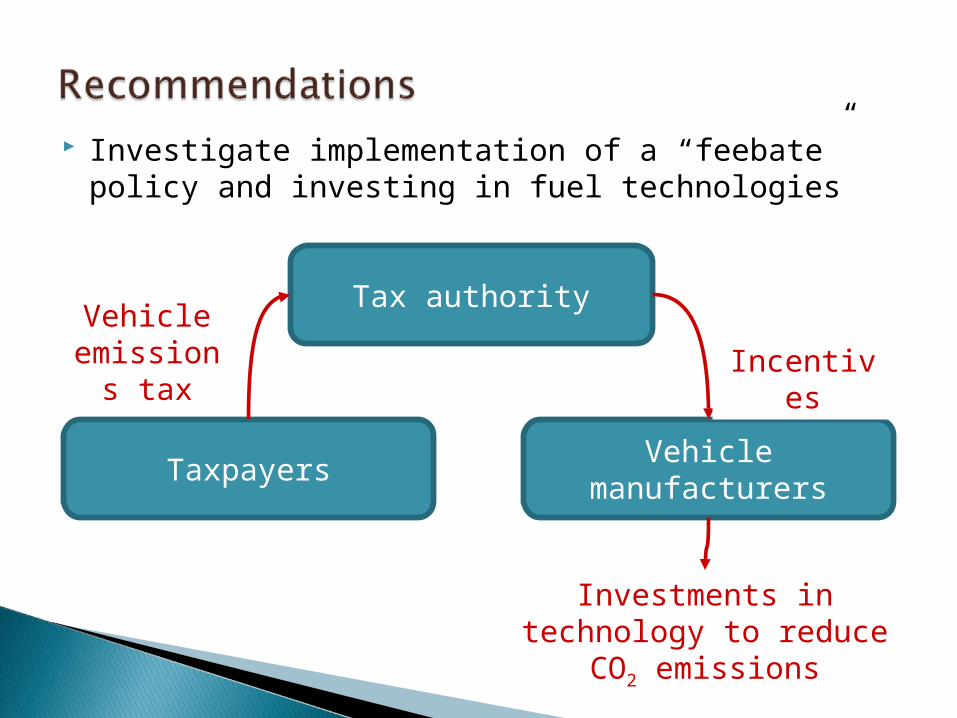

Investigate implementation of a “feebate” policy and investing in fuel technologies

Tax authority

TaxpayersVehicle

manufacturers

Vehicle emissions

taxIncentives

Investments in technology to reduce CO2

emissions

It is not only the government’s responsibility

Creating awareness of “carbon footprint”

Most effective fiscal reform initiative in reducing CO2

emissions might not be one that forces people to contribute, but rather one which encourages people to contribute and then rewards them if they do (Nel 2009:76)

Public participation and discussions among the different stakeholders (government, taxpayers and the motor industry)