Roth 403b Power Point

21

Piedmont Healthcare www. ing.com Marie Cox CRM The Roth 403(b) Your 403(b). Made Better

-

Upload

jacknickelson -

Category

Documents

-

view

747 -

download

0

description

Transcript of Roth 403b Power Point

Piedmont Healthcarewww. ing.com

Marie CoxCRM

The Roth 403(b)Your 403(b). Made Better

Insurance - Banking - Asset Management 2

You should consider the investment objectives, risks, and charges and expenses of the variable product and its underlying fund options; or mutual funds offered through a retirement plan, carefully before investing. The prospectuses/prospectus summaries/information booklets contain this and other information, which can be obtained by contacting your local representative. Please read the information carefully before investing.

Products and services are offered through the ING Family of Companies. Securities offered through ING Financial Advisers, LLC (member SIPC). The information is provided for your education only. Neither ING or its affiliated companies or representatives provide tax or legal advice. Please consult a tax adviser or attorney before a tax-related investment/insurance decision. C08-1114-018 (11/08) ELC.E.P.MS.462-1 (11/08)

Insurance - Banking - Asset Management 3

The ING Difference…

Fresh approach

to life planning

Straight talk

about financial realities

Personalized solutions

that take the whole picture into account

Insurance - Banking - Asset Management 4

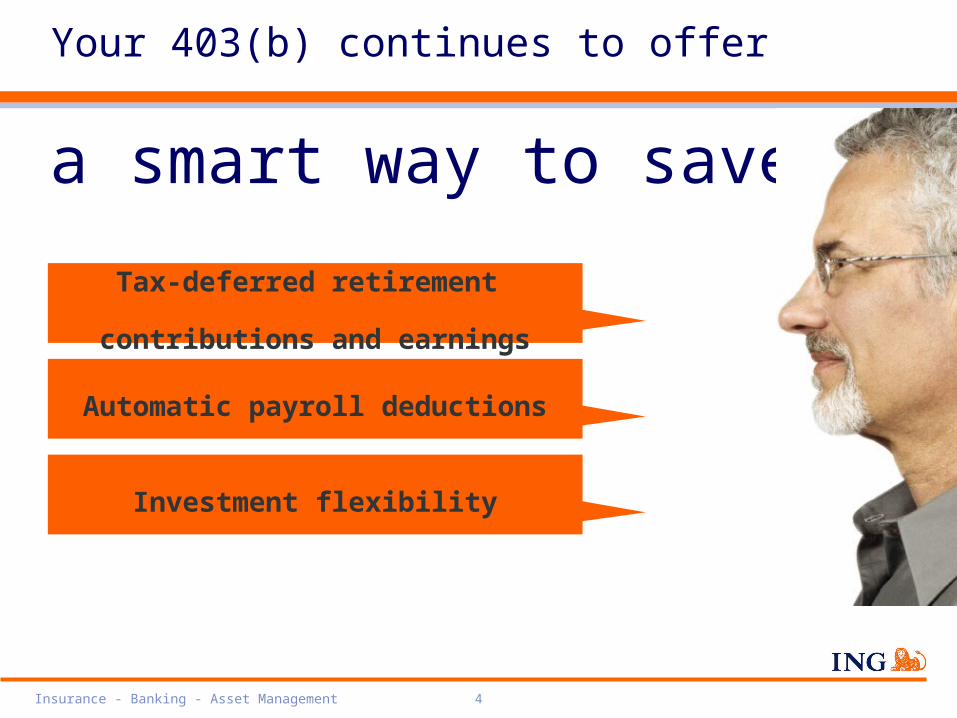

a smart way to save.

Automatic payroll deductions

Investment flexibility

Tax-deferred retirement

contributions and earnings

Your 403(b) continues to offer

Insurance - Banking - Asset Management 5

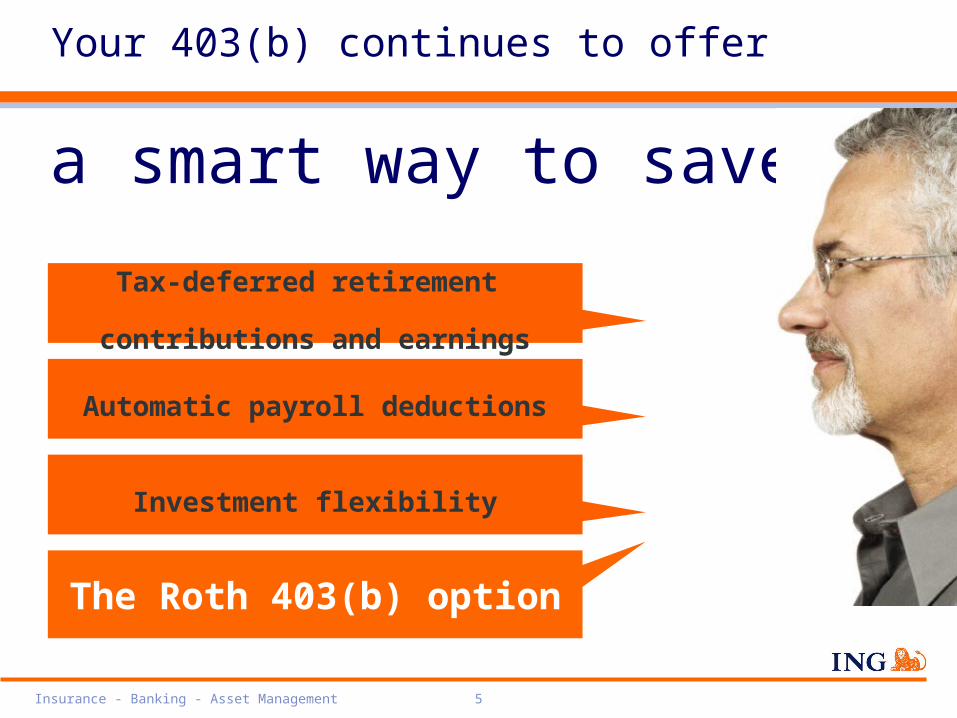

a smart way to save.

Automatic payroll deductions

Investment flexibility

Tax-deferred retirement

contributions and earnings

Your 403(b) continues to offer

The Roth 403(b) option

Insurance - Banking - Asset Management 6

A Roth 403(b) offers you the potential for

tax-free

income whenyou retire.

Certain qualifying conditions apply.

What’s the big deal?

Insurance - Banking - Asset Management 7

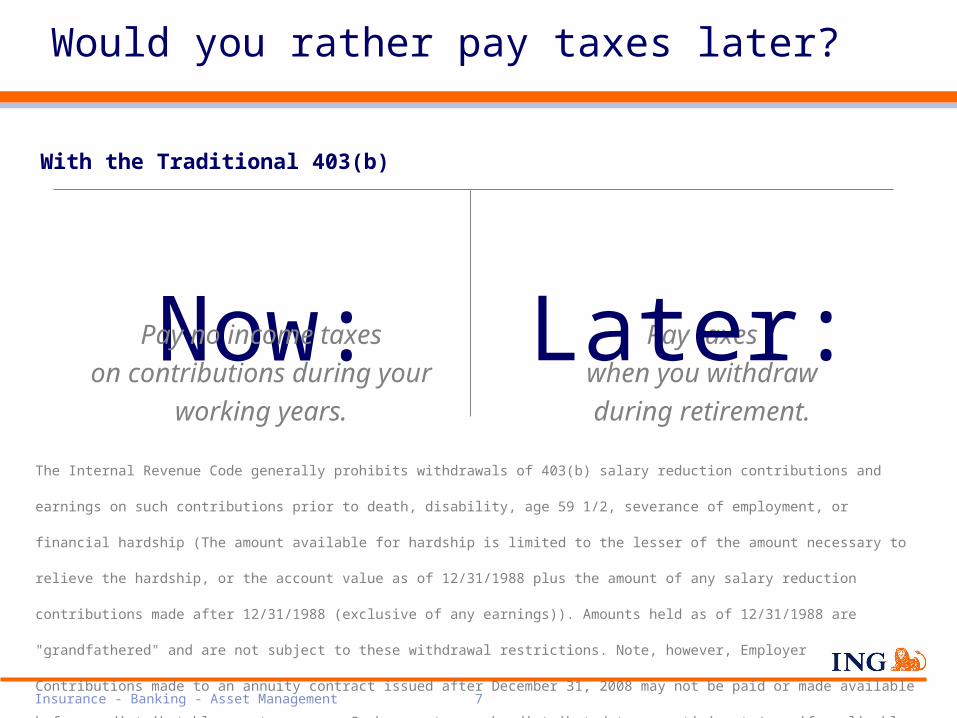

With the Traditional 403(b)

Now:Pay no income taxes

on contributions during your

working years.

Pay taxes

when you withdraw

during retirement.

Later:The Internal Revenue Code generally prohibits withdrawals of 403(b) salary reduction contributions and earnings on such contributions prior to death, disability, age 59 1/2,

severance of employment, or financial hardship (The amount available for hardship is limited to the lesser of the amount necessary to relieve the hardship, or the account

value as of 12/31/1988 plus the amount of any salary reduction contributions made after 12/31/1988 (exclusive of any earnings)). Amounts held as of 12/31/1988 are

"grandfathered" and are not subject to these withdrawal restrictions. Note, however, Employer Contributions made to an annuity contract issued after December 31, 2008 may

not be paid or made available before a distributable event occurs. Such amounts may be distributed to a participant (or, if applicable, the beneficiary) upon the participant’s

severance from employment, or upon the occurrence of an event, such as after a fixed number of years, the attainment of a stated age, or disability.

Note that distributions from the Roth 403(b) are subject to taxation on the portion attributable to earnings if made before Qualified Distribution provisions are satisfied.

Would you rather pay taxes later?

Insurance - Banking - Asset Management 8

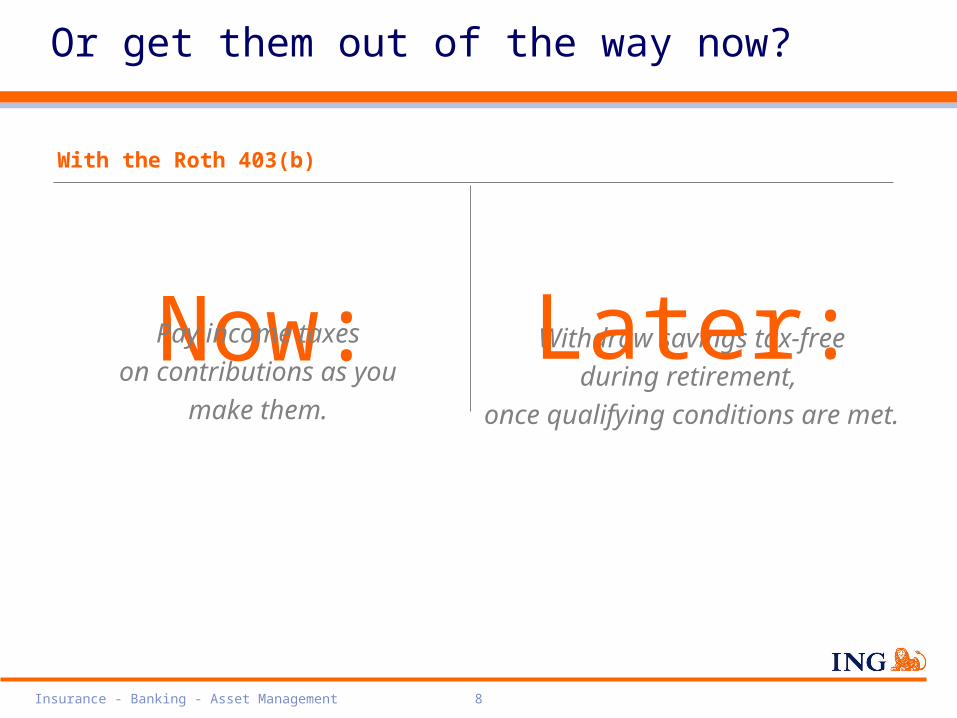

With the Roth 403(b)

Now:Pay income taxes

on contributions as you

make them.

Withdraw savings tax-free

during retirement,

once qualifying conditions are met.

Later:

Or get them out of the way now?

Insurance - Banking - Asset Management 9

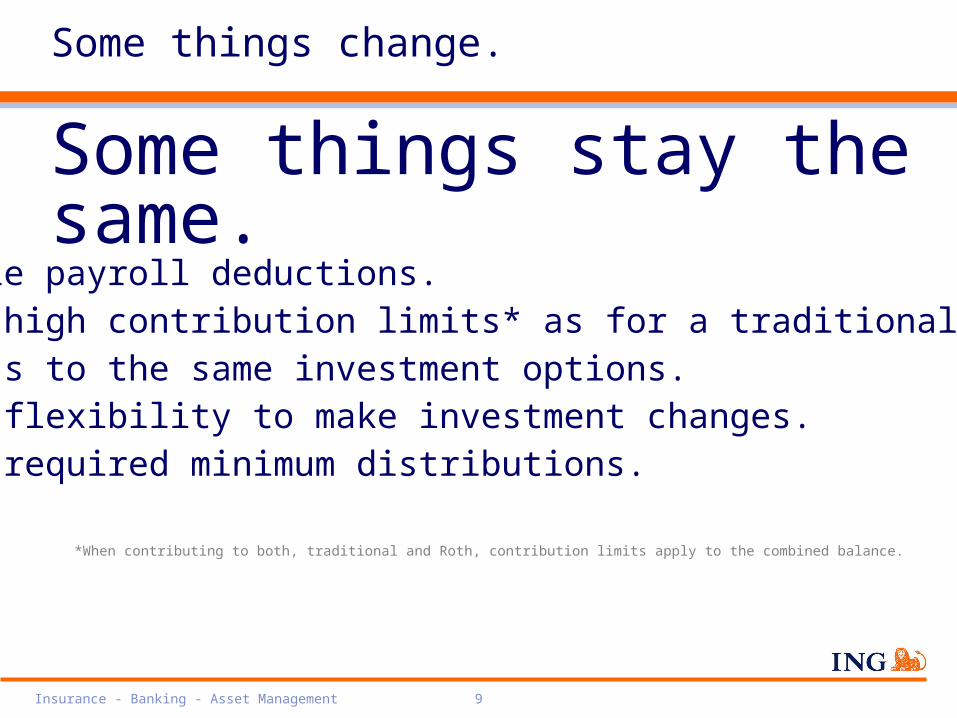

Some things stay the same.

Simple payroll deductions.Same high contribution limits* as for a traditional 403(b).Access to the same investment options.Same flexibility to make investment changes.Same required minimum distributions.

Some things change.

*When contributing to both, traditional and Roth, contribution limits apply to the combined balance.

Insurance - Banking - Asset Management 10

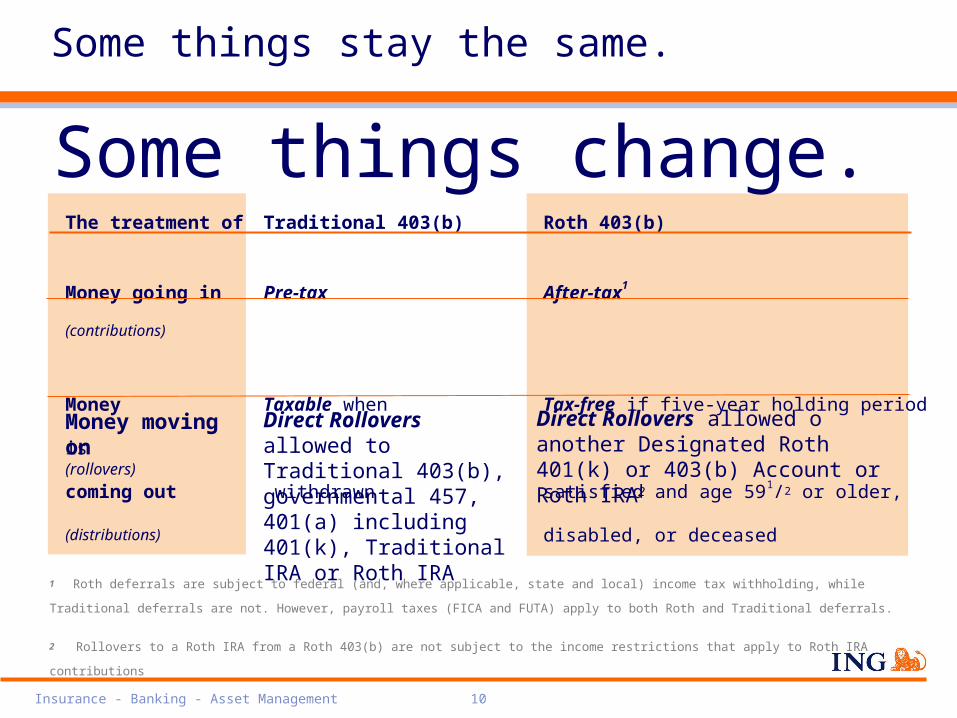

The treatment of Traditional 403(b) Roth 403(b)

Money going in Pre-tax After-tax1

(contributions)

Money Taxable when Tax-free if five-year holding period is

coming out withdrawn satisfied and age 591/2 or older,

(distributions) disabled, or deceased

Some things change.

Direct Rollovers allowed to Traditional 403(b), governmental 457, 401(a) including 401(k), Traditional IRA or Roth IRA

Direct Rollovers allowed o another Designated Roth 401(k) or 403(b) Account or Roth IRA2

Money moving on (rollovers)

1 Roth deferrals are subject to federal (and, where applicable, state and local) income tax withholding, while Traditional deferrals are not. However, payroll taxes

(FICA and FUTA) apply to both Roth and Traditional deferrals.

2 Rollovers to a Roth IRA from a Roth 403(b) are not subject to the income restrictions that apply to Roth IRA contributions

Some things stay the same.

Insurance - Banking - Asset Management 11

So, who might this be right for?

The Roth 403(b).

Insurance - Banking - Asset Management 12

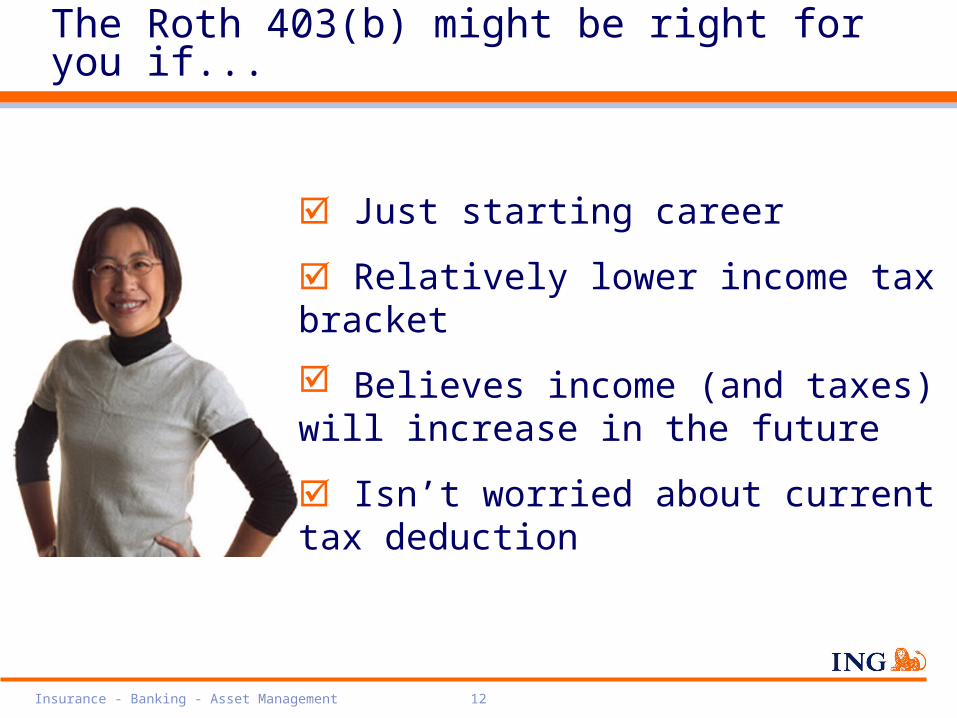

The Roth 403(b) might be right for you if...

Just starting career

Relatively lower income tax bracket

Believes income (and taxes) will increase in the future

Isn’t worried about current tax deduction

Insurance - Banking - Asset Management 13

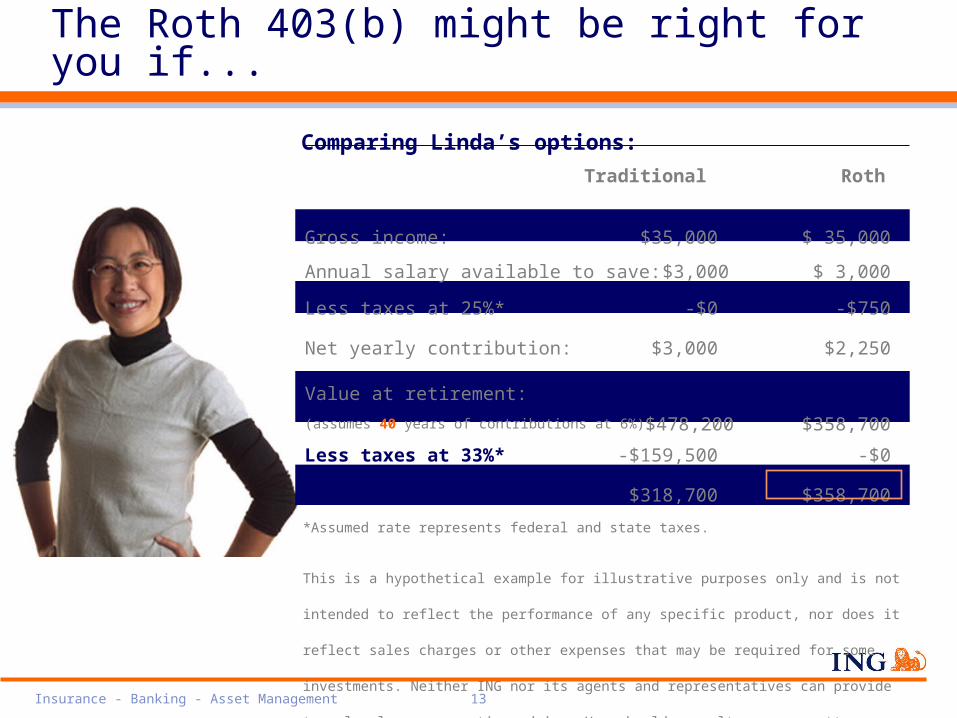

Traditional Roth

Pre-tax 403(b) After-tax 403(b)

Comparing Linda’s options:

After-tax value: $318,700 $358,700

Gross income: $35,000 $ 35,000

Less taxes at 33%* -$159,500 -$0

Annual salary available to save: $3,000 $ 3,000

Less taxes at 25%* -$0 -$750

Net yearly contribution: $3,000 $2,250

(totals over 40 years: $120,000 $90,000)Value at retirement:

(assumes 40 years of contributions at 6%) $478,200 $358,700

The Roth 403(b) might be right for you if...

*Assumed rate represents federal and state taxes.

This is a hypothetical example for illustrative purposes only and is not intended to reflect the performance of any specific

product, nor does it reflect sales charges or other expenses that may be required for some investments. Neither ING nor

its agents and representatives can provide tax, legal, or accounting advice. You should consult your own attorney or tax

advisor about your specific circumstances.

Insurance - Banking - Asset Management 14

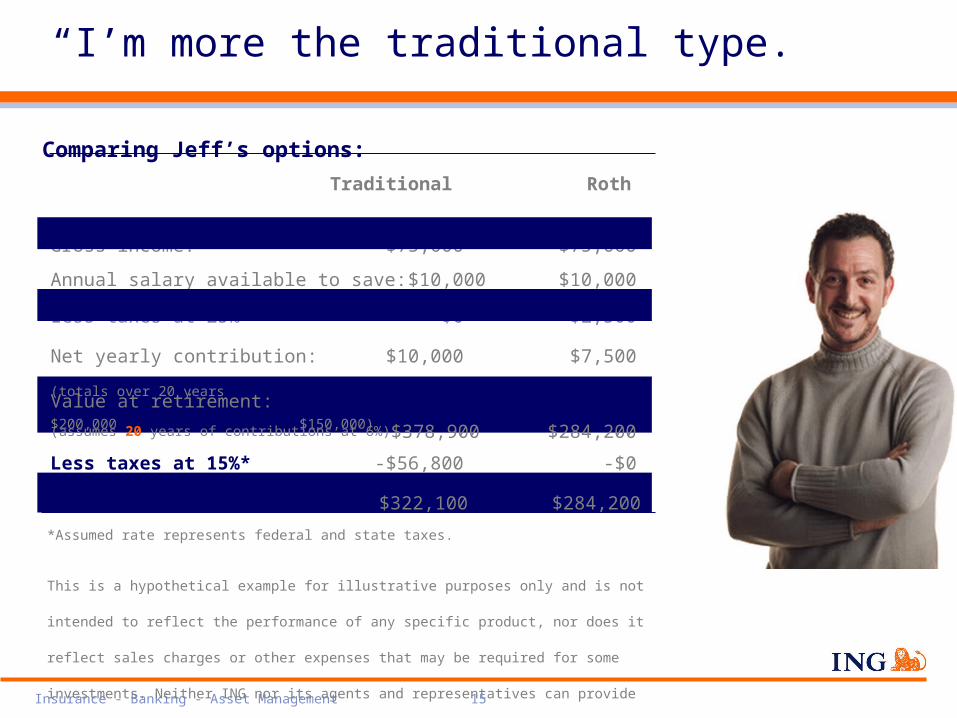

“I’m more the traditional type.”

Can’t really afford more taxes now

Needs more tax deductions

Doesn’t expect to be in a higher tax bracket when he retires

Insurance - Banking - Asset Management 15

Comparing Jeff’s options:

Traditional Roth

Pre-tax 403(b) After-tax 403(b)Gross income: $75,000 $75,000

Less taxes at 15%* -$56,800 -$0

Annual salary available to save: $10,000 $10,000

Less taxes at 25%* -$0 -$2,500

Net yearly contribution: $10,000 $7,500

(totals over 20 years $200,000 $150,000)Value at retirement:

(assumes 20 years of contributions at 6%) $378,900 $284,200

After-tax value: $322,100 $284,200

“I’m more the traditional type.”

*Assumed rate represents federal and state taxes.

This is a hypothetical example for illustrative purposes only and is not intended to reflect the performance of any specific

product, nor does it reflect sales charges or other expenses that may be required for some investments. Neither ING nor

its agents and representatives can provide tax, legal, or accounting advice. You should consult your own attorney or tax

advisor about your specific circumstances.

Insurance - Banking - Asset Management 16

“Both, please.”

Isn’t sure whether taxes will be higher or lower in retirement

Wants to diversify tax strategy

Still wants a current income tax deduction

Insurance - Banking - Asset Management 17

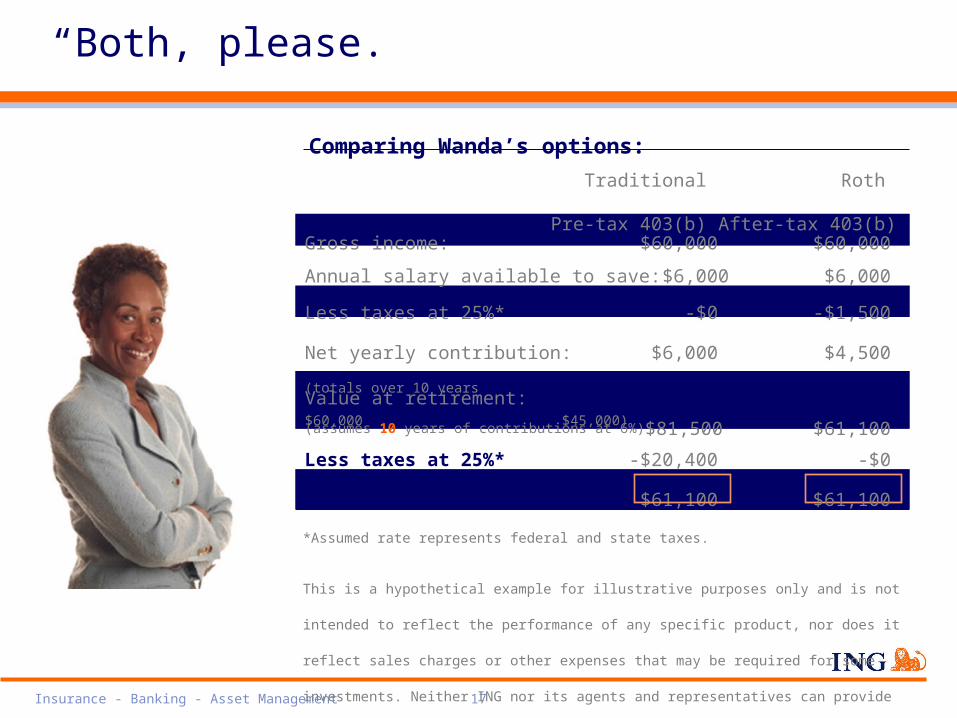

Value at retirement:

(assumes 10 years of contributions at 6%) $81,500 $61,100

Comparing Wanda’s options:

Traditional Roth

Pre-tax 403(b) After-tax 403(b)

Less taxes at 25%* -$20,400 -$0

Less taxes at 25%* -$0 -$1,500

Net yearly contribution: $6,000 $4,500

(totals over 10 years $60,000 $45,000)

Gross income: $60,000 $60,000

After-tax value: $61,100 $61,100

Annual salary available to save: $6,000 $6,000

“Both, please.”

*Assumed rate represents federal and state taxes.

This is a hypothetical example for illustrative purposes only and is not intended to reflect the performance of any specific

product, nor does it reflect sales charges or other expenses that may be required for some investments. Neither ING nor

its agents and representatives can provide tax, legal, or accounting advice. You should consult your own attorney or tax

advisor about your specific circumstances.

Insurance - Banking - Asset Management 18

Consider this … Are you looking for tax-free retirement income? Do you expect your taxes to be higher when you retire? Are you currently in a lower income tax bracket? Do you like the idea of diversifying your tax strategy like you

diversify your investment strategy? Are you looking to minimize taxes on your Social Security

benefits? Roth distributions do not affect taxation of Social Security benefits;

whereas traditional distributions might

There’s more …

Is Roth right for you?

These materials are not intended to be used to avoid tax penalties, and were prepared to support the promotion or marketing of the matter addressed in this document.

The taxpayer should seek advice from an independent tax advisor.

Insurance - Banking - Asset Management 19

Consider this.

If you answered “yes” to any of these, a Roth may make sense for you.

Are you already maxing out your Traditional 403(b) contributions? Can you afford a reduction in take-home pay to contribute the

same amount to your Roth 403(b)? For those already contributing to a Traditional 403(b) and wishing to

switch to a Roth 403(b) Are you looking to leave tax-free assets to your heirs?

A Roth 403(b) may be rolled over to Roth IRA: age 70 ½ required distributions do not apply to a Roth IRA

A traditional 403(b) may be rolled over to a Roth IRA which may be advantageous as set forth above. In order to complete the rollover to the Roth IRA, taxes will need to be paid on the traditional 403(b)

Is Roth right for you?

Insurance - Banking - Asset Management 20

What’s next?

Use our online calculator.

Time to take action.

Consult a professional.

Read on the topic.

Your 403(b).Made Better.

Thanks for Participating in The Roth 403(b)