Robin Fleming – Group CEO May 20, 2016 · BSP entered into a sale agreement in January 2015 to...

37

Presentation to Shareholders Robin Fleming – Group CEO May 20, 2016

Transcript of Robin Fleming – Group CEO May 20, 2016 · BSP entered into a sale agreement in January 2015 to...

Presentation to Shareholders Robin Fleming – Group CEO May 20, 2016

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

11.3%

7.7%

4.9%

13.3%

9.9%

4.3%

2.4% 2.0% 2.7%

- 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000

2011 2012 2013 2014 2015 2016F2017F2018F2019F

In U

SD’m

PNG GDP PNG growth rate

Economic Indicators 2014 2015E 2016F

GDP growth 13.3% 9.9% 4.3%

Non-mining GDP 1.2% 2.4% 3.4%

Inflation (headline) 5.2% 5.1% 5.7%

Deficit % of GDP 8.3% 4.9% 3.8%

Debt to GDP ratio 35.5% 34.7% 35.8%

• PNG’s GDP has normalised after posting strong growth at an average rate of circa 8% over the last decade. Total GDP growth is expected to be around 4.3% in 2016.

• The fall in commodity prices has had an impact on government revenue. • The non-mineral sectors have the potential to support a more inclusive, balanced and

sustainable growth. • There is a mixed view on the market and the economy, with BSP noting a general view of

‘cautious optimism’ among businesses.

PNG economic environment

2

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

• Extractive industries (Oil & Gas and Mining) have been the main driver of growth in the recent past. • Primary industry improved with 23% contribution to economic activity. • Oil & gas was the main % contributor to GDP in 2015 and 2016, and this is expected to moderate to

1.3% in 2016, compared to 8% in 2015.

Economic activity drivers

3

* Others include; community & social services, Finance, real estate & business services and electricity.

Percentage contribution to GDP growth GDP contribution by economic activity-2015

Oil & Gas 18%

Construction 18%

Agriculture 23%

Mining 4%

Manufacturing 7%

Wholesale & Retail

8%

Transport 6%

Others 16%

1.3%

0.5%

0.9%

0.3%

0.3%

0.9%

-2.0% 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0%

Oil & Gas

Construction

Agriculture

Mining

Manufacturing

Others 2016F 2015 2014

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

5.8

6.4

0.01.02.03.04.05.06.07.0

Dec'11 Dec'12 Dec'13 Dec'14 Dec'15

Inflation (%, quarterly)

0.30

0.35

0.40

0.45

0.50

0.55

Mar'12 Mar'13 Mar'14 Mar'15 Mar'16

USD AUD

• Headline inflation is estimated at 6.4% in December 2015, compared to 6.6% in the previous year. Inflation is expected to moderate to around 6% in 2016.

• The lower economic growth and other developments are non-inflationary and Bank of PNG is expected to maintain a neutral monetary policy stance over the next six months.

PNG economic environment - Inflation

4

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Group Profit Before Tax (Kina’ million)

5

165

719 766

-

100

200

300

400

500

600

700

800

900

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Axis

Titl

e

GPBT

Kina

, Mill

ions

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Group Profit After Tax (Kina’ million)

6

112

507 532

-

100

200

300

400

500

600

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ki

na, M

illio

ns

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Group Profit & Loss Trends

(Millions of Kina) 2011 2012 2013 2014 2015

CAGR, last 5 Years

Income Net Interest Income 597 682 741 885 1,006 11.0% Foreign Exchange Income 193 224 353 267 179 -1.5% Fee and other Income 304 380 428 346 362 3.6%

Total Income 1,094 1,285 1,522 1,499 1,547 7.2% Expenses

Operating Expenses (520) (581) (641) (554) (559) 1.4% Depreciation and SW Amort'n (53) (84) (176) (123) (115) 16.7% Loan Provisioning (25) (71) (94) (77) (90) 28.9% Non-Lending Losses (27) (15) (17) (26) (17) -8.2%

Profit before tax 468 534 595 719 766 10.3% Tax expense (119) (138) (170) (212) (234) 14.5% Share of Profits from Assoc. 6 11 12 10 2

Profit after tax 356 408 436.8 507.3 531.9 8.4% EPS (toea) 75.9 86.9 93.1 108.3 113.8 8.4% Dividends per share (toea) 47.3 55.0 58.0 66.0 78.5 10.7%

7

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Group Total Assets (Kina ’billion)

8

4.73

15.8 18.2

- 2 4 6 8

10 12 14 16 18 20

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Kina

, Bill

ion

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Group Balance Sheet Trends

(Millions of Kina) 2011 2012 2013 2014 2015

CAGR, last 5 Years

Assets

Cash & Short Term Deposits 1,501 2,134 3,476 2,988 3,257 16.8% Loans & Advances 4,301 4,805 5,306 6,757 8,622 14.9% Investments 4,724 4,861 5,571 4,663 4,929 0.9% Fixed Assets and Intangibles 627 750 779 773 797 4.9% Other Assets 510 787 629 636 592 3.0%

Total Assets 11,663 13,336 15,761 15,817 18,196 9.3% Liabilities

Customer Deposits 9,366 10,861 12,201 12,708 14,595 9.3% Non-Lending Provisions 170 109 143 216 183 1.5% Other Liabilities 801 898 1,798 1,092 1,389 11.6%

Total Liabilities 10,337 11,867 14,142 14,016 16,167 9.4% Shareholder Equity 1,344 1,466 1,619 1,800 2,029 8.6%

9

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Group Income Growth 2011-2015 (K’million)

10

597 682 741 885

1,006

202 254

286

305 310

193

224

353 267

179

28

49

142 26 30

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2011 2012 2013 2014 2015

Net Interest Income Banking Fee and Commissions

Fx Income Net Insurance Income

K'M

ilion

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Group Expense 2011-2015 (K’Million)

11

520 581

641 554 559

53

84

176

123 115 25

71

94

77 90 27

15

17

26 17

0

100

200

300

400

500

600

700

800

900

1,000

2011 2012 2013 2014 2015

Operating Expenses Depreciation and SW Amort'nLoan Provisioning Non Lending Losses

K’M

illio

n

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Suva

VANUA LEVU

VITI LEVUNadi

Lomaloma

Taveuni

Navua Suva CentralDominion House

Centre Point

Sigatoka

SavusavuNabowalu

Labasa

Ovalau

Vunisea

KorovouLautoka

Tavua

Ba

Rakiraki

FIJIFIJI Labasa

VANUA LEVU

Taveuni Savusavu

Nabowalu

Rakiraki

Ovalau

Lomaloma

Tavua

Lautoka Ba

Nadi

Korovou

Suva Suva Central Dominion House Pacific House Centre Point

Navua Sigatoka

Vunisea

VITI LEVU

SOLOMON IS.

Honiara Honiara Point Cruz Ranadi

Gizo

Noro

Munda

Auki

SAMOA

Salelologa Apia Apia Vaitelei

TONGA

Vava’u

Nuku’ alofa

COOK IS. Aitutaki

Manuea

Atiu

Mitiaro

Mauke

AVARUA

Mangaia

Southern Islands

Rarotonga

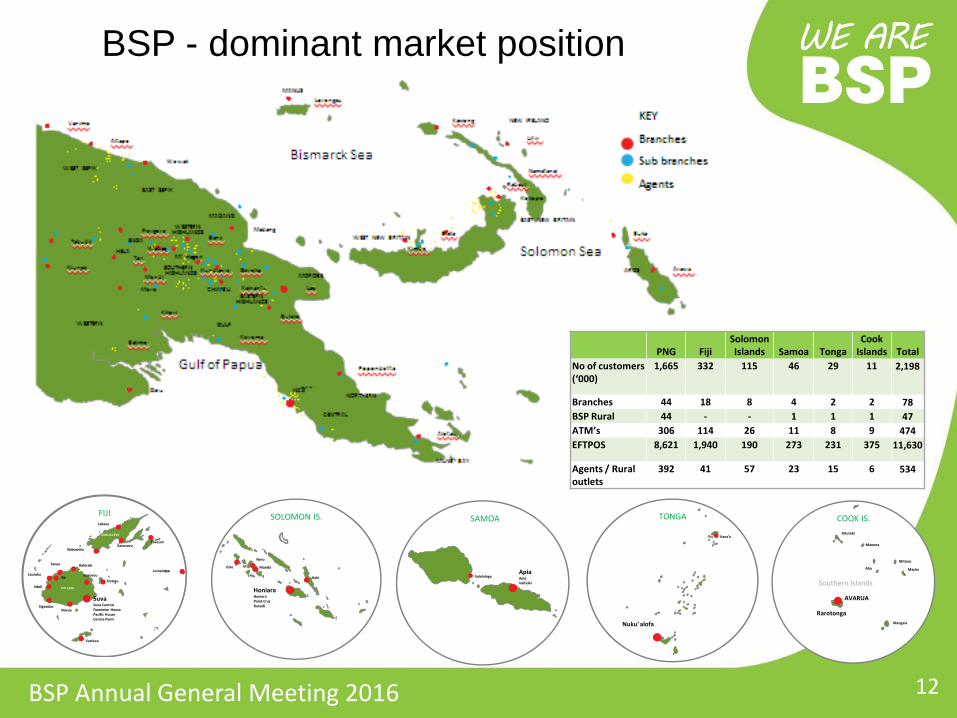

BSP - dominant market position

PNG Fiji Solomon Islands Samoa Tonga

Cook Islands Total

No of customers (‘000)

1,665 332 115 46 29 11 2,198

Branches 44 18 8 4 2 2 78 BSP Rural 44 - - 1 1 1 47 ATM’s 306 114 26 11 8 9 474 EFTPOS 8,621 1,940 190 273 231 375 11,630

Agents / Rural outlets

392 41 57 23 15 6 534

12

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

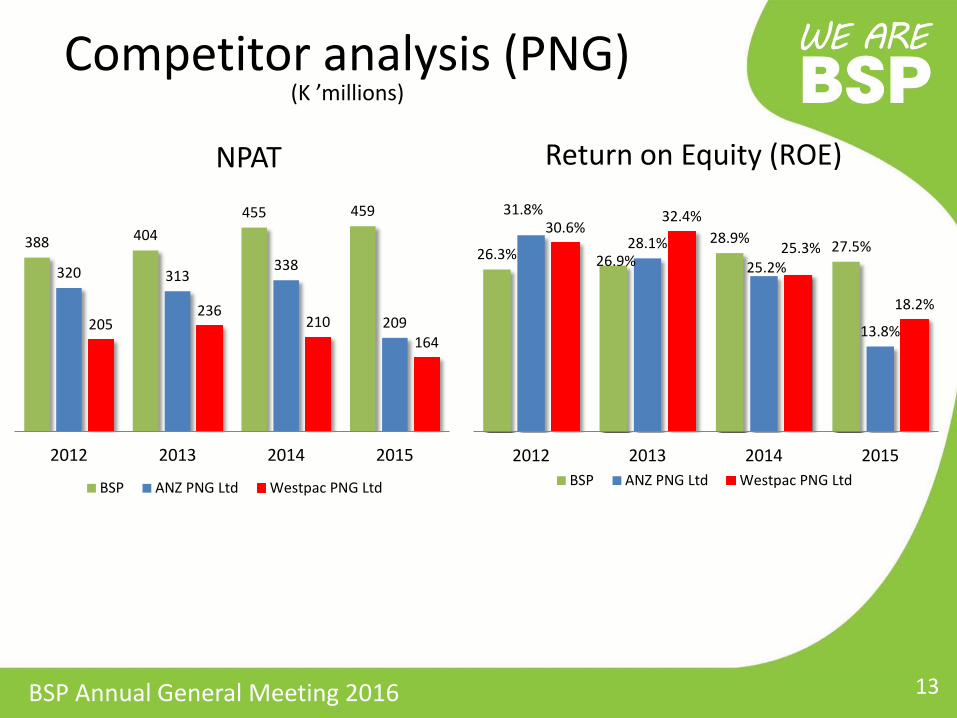

Return on Equity (ROE) NPAT

Competitor analysis (PNG) (K ’millions)

13

388 404 455 459

320 313 338

209 205 236

210 164

2012 2013 2014 2015

BSP ANZ PNG Ltd Westpac PNG Ltd

26.3% 26.9% 28.9% 27.5%

31.8%

28.1% 25.2%

13.8%

30.6% 32.4%

25.3%

18.2%

2012 2013 2014 2015BSP ANZ PNG Ltd Westpac PNG Ltd

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Loans-PNG (K’ million)

14

3,964

5,271

6,094

2,968

3,154

3,516

1,635

1,618

1,683

2013

2014

2015

0 5,000

KSL WPAC ANZ BSP

BSP 53% ANZ

30%

KSL 3%

WPAC 14%

Market share – September 2015

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Deposits-PNG (K’ million)

15

10,880

10,888

11,018

4,621

4,780

4,821

3,219

2,918

3,063

2013

2014

2015

0 5,000 10,000

KSL WPAC ANZ BSP

BSP 56%

ANZ 25%

KSL 3%

WPAC 16%

Market share – September 2015

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Profit After Tax- Fiji (FJD ‘million)

52 49

40

64

37

50 47 47

6 6 8 8 3

9

21

31

-3 -7 -5 -3

5 6

-20

-10

-

10

20

30

40

50

60

70

2012 2013 2014 2015

ANZ

WBC

BOB

BSP

Bred Bank

HFC

16

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Total Assets-Fiji (FJD ‘million)

1,932

2,200

2,443

2,970

1,437

1,407

1,280

1,925

570

490

403

667

116

1,458

1,670

1,862

69

89

126

233

383

557

-400 100 600 1,100 1,600 2,100 2,600 3,100

2012

2013

2014

2015

HFC

Bred Bank

BSP

BOB

WBC

ANZ

17

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Profit After Tax- SI (SBD ‘million)

18

32

20 22 19

33.0 36.0

26.0 30 29.2

33.7

43.2

-

5

10

15

20

25

30

35

40

45

50

2012 2013 2014 2015ANZ WBC BSP

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Performance- SI

19

Return on Equity (ROE) Return on Assets (ROA)

16%

11% 13% 12%

30% 31%

20%

0%

13% 11% 11%

9%

2012 2013 2014 2015ANZ WBC BSP

3%

1% 2% 1%

5% 5%

3%

0%

2% 2% 2% 2%

2012 2013 2014 2015ANZ WBC BSP

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Westpac Acquisition: 1. BSP entered into a sale agreement in January 2015 to acquire

Westpac’s operations in Solomon Islands, Vanuatu, Samoa, Tonga and Cook Islands for A$125m.

2. Completed acquisition of Samoa, Tonga and Cook Islands on July 10th, 2015 and integration with BSP has been successful

3. Acquisition of Solomon Islands operations was completed in October 2015. Currently undergoing system integration.

4. Regulatory approval for Vanuatu acquisition has been granted by the Reserve Bank of Vanuatu; acquisition plans are currently on track, with completion of transition currently anticipated to happen in July 2016.

Strategic Focus 2016/17

20

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

BSP Finance 1. Business Finance operations in Fiji and PNG are progressing

well and are tracking to business plans, since their inception in late 2014. Financial and operational success targets have been set and pursued for continuation of loan book growth and profitability, and operational efficiency.

2. BSP Finance will follow BSP’s regional expansion program by exploring opportunities to expand to other geographies that BSP Bank already exist in.

3. BSP Finance is also exploring market entry opportunities outside of the Pacific Region.

Strategic Focus 2016/17

21

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

19.8% 17.4%

13.9% 19.4% 19.0%

4.4% 4.9%

4.1%

4.6% 4.1%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Tier 1 Tier 2 Minimum BPNG requirement

Capital Adequacy

Capital Management

• The Capital Base of the BSP Group exceeds regulatory standards for an adequately capitalised bank

• A slight drop from 24% to 23.1% in part reflecting acquisition of Westpac businesses in the South Pacific

22

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

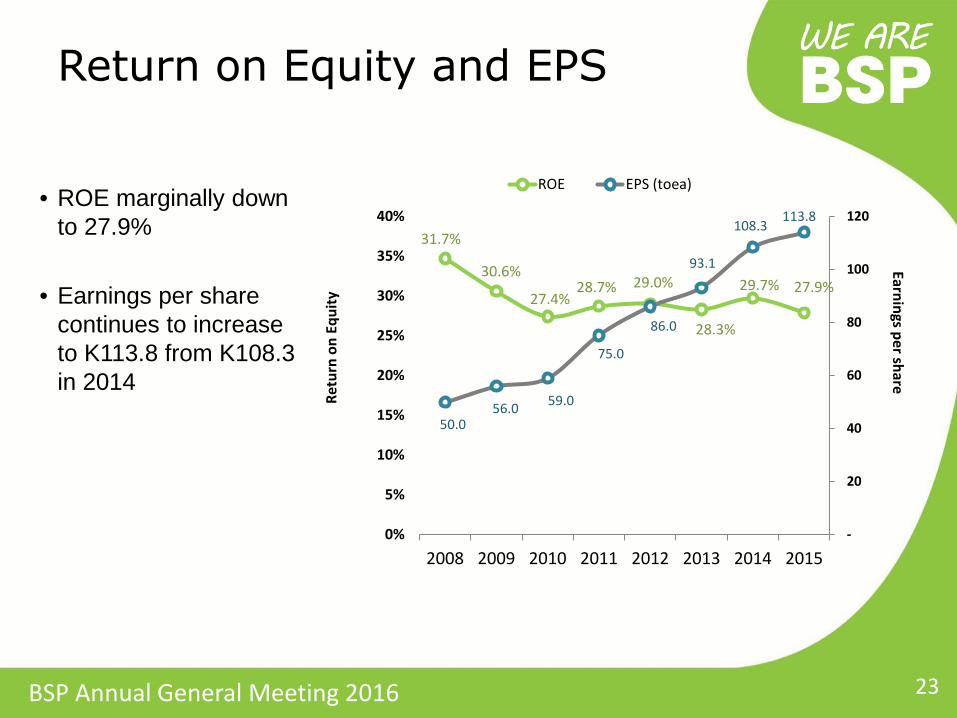

Return on Equity and EPS

• ROE marginally down to 27.9%

• Earnings per share continues to increase to K113.8 from K108.3 in 2014

23

31.7%

30.6%

27.4% 28.7% 29.0%

28.3%

29.7% 27.9%

50.0 56.0 59.0

75.0

86.0

93.1

108.3 113.8

-

20

40

60

80

100

120

0%

5%

10%

15%

20%

25%

30%

35%

40%

2008 2009 2010 2011 2012 2013 2014 2015

ROE EPS (toea)

Earnings per share Retu

rn o

n Eq

uity

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Non Performing Loans and Provisioning to Total Loans

• Non Performing loans increased in 2015, primarily driven by the impact from newly acquired operations in Tonga, Cook Islands, Samoa, and Solomon Islands.

• Provisioning also

increased to 4.9% in 2015.

24

3.8% 4.4%

5.0% 4.6% 4.9%

2.1% 1.2%

0.8% 0.6%

1.7%

FY2011 FY2012 FY2013 FY2014 FY2015

Provision to Loans NPL

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Q1/2016 Results

25

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

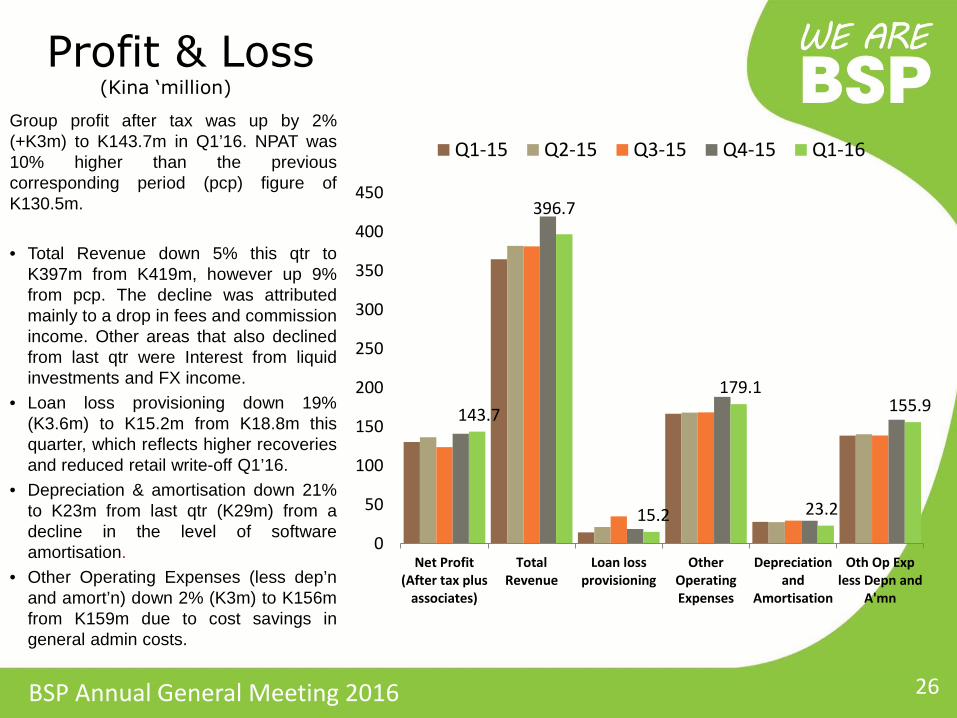

Group profit after tax was up by 2% (+K3m) to K143.7m in Q1’16. NPAT was 10% higher than the previous corresponding period (pcp) figure of K130.5m. • Total Revenue down 5% this qtr to

K397m from K419m, however up 9% from pcp. The decline was attributed mainly to a drop in fees and commission income. Other areas that also declined from last qtr were Interest from liquid investments and FX income.

• Loan loss provisioning down 19% (K3.6m) to K15.2m from K18.8m this quarter, which reflects higher recoveries and reduced retail write-off Q1’16.

• Depreciation & amortisation down 21% to K23m from last qtr (K29m) from a decline in the level of software amortisation.

• Other Operating Expenses (less dep’n and amort’n) down 2% (K3m) to K156m from K159m due to cost savings in general admin costs.

Profit & Loss (Kina ‘million)

26

143.7

396.7

15.2

179.1

23.2

155.9

0

50

100

150

200

250

300

350

400

450

Net Profit(After tax plus

associates)

TotalRevenue

Loan lossprovisioning

OtherOperatingExpenses

Depreciationand

Amortisation

Oth Op Expless Depn and

A'mn

Q1-15 Q2-15 Q3-15 Q4-15 Q1-16

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

8.8

5.5

14.7

18.5

-

2

4

6

8

10

12

14

16

18

20

Loans Other IntEarningAssets

Deposits Total Assets

Kina

bill

ions

Q1-15 Q2-15 Q3-15 Q4-15 Q1-16Total Assets up 1% to K18.5b this qtr from K18.2b in Q4’15. The increase reflects increases in cash and loans and advances • Net loans increased by 1% to K8.8b this

qtr from K8.6b as at the end of Dec’15. Compared to the previous corresponding period of 2015, loans was up by 28% or K1.93b.

• Total deposits grew 1% to K14.7b from

K14.6b largely attributed to growth in deposits in SI, Samoa and Tonga.

Balance Sheet (Kina ‘billion)

27

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

55%

22%

45%

36% 36%

24%

PNG Fiji SolomonIslands

Cook Islands Tonga Samoa

Q1-15 Q2-15 Q3-15 Q4-15 Q1-16• BSP’s combined loans market

share remained unchanged at 40% this qtr compared to Q4’15, however it has improved by 1% compared from pcp in 2015.

• While Solomon Island market

share has slightly declined this qtr, growth in other countries have neutralised the overall position.

• Samoa, Tonga and Cook Islands have seen improved growth in their respective loan book market share compared to the last qtr.

Market Share Loans

28

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

55%

22%

62%

51%

37%

23%

PNG Fiji SolomonIslands

CookIslands

Tonga Samoa

Q1-15 Q2-15 Q3-15 Q4-15 Q1-16• BSP’s combined deposit market

share remained unchanged at 44% compared to Q4’15. The 1% drop in Fiji’s deposit market share and further 2% drop in the Cooks market share have been compensated for by the growth in other countries market share.

• Solomon Islands’ deposit market grew significantly to 62% from 58% in Q4’15, resulting from the combined operations of BSP and former Westpac operation, a significant growth from 39% in Q3’15.

Market Share Deposits

29

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

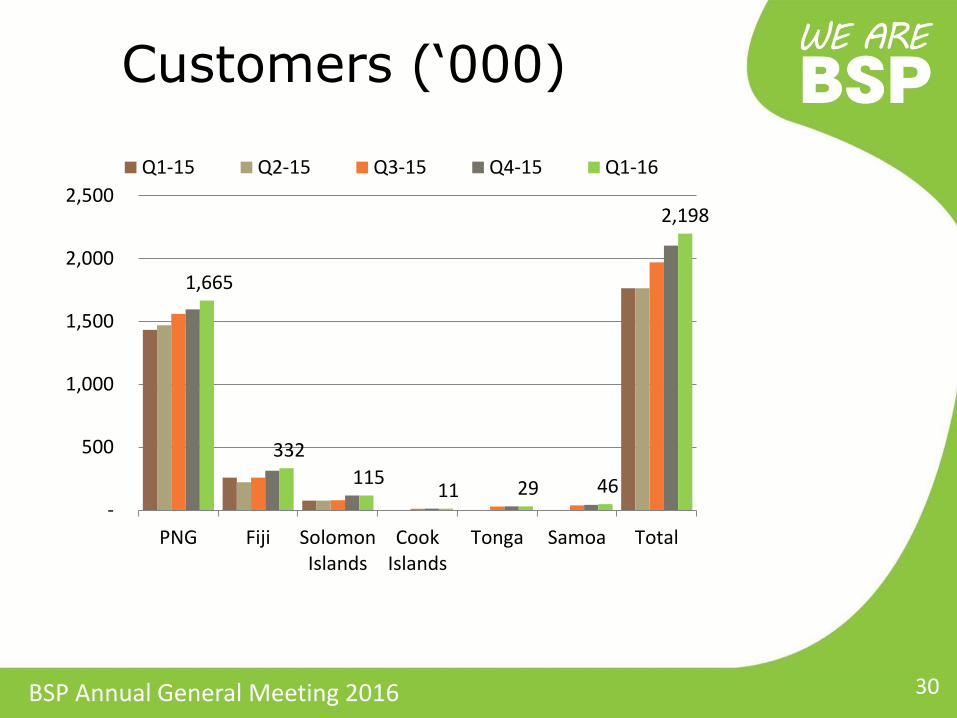

Customers (‘000)

30

1,665

332 115 11 29 46

2,198

-

500

1,000

1,500

2,000

2,500

PNG Fiji SolomonIslands

CookIslands

Tonga Samoa Total

Q1-15 Q2-15 Q3-15 Q4-15 Q1-16

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

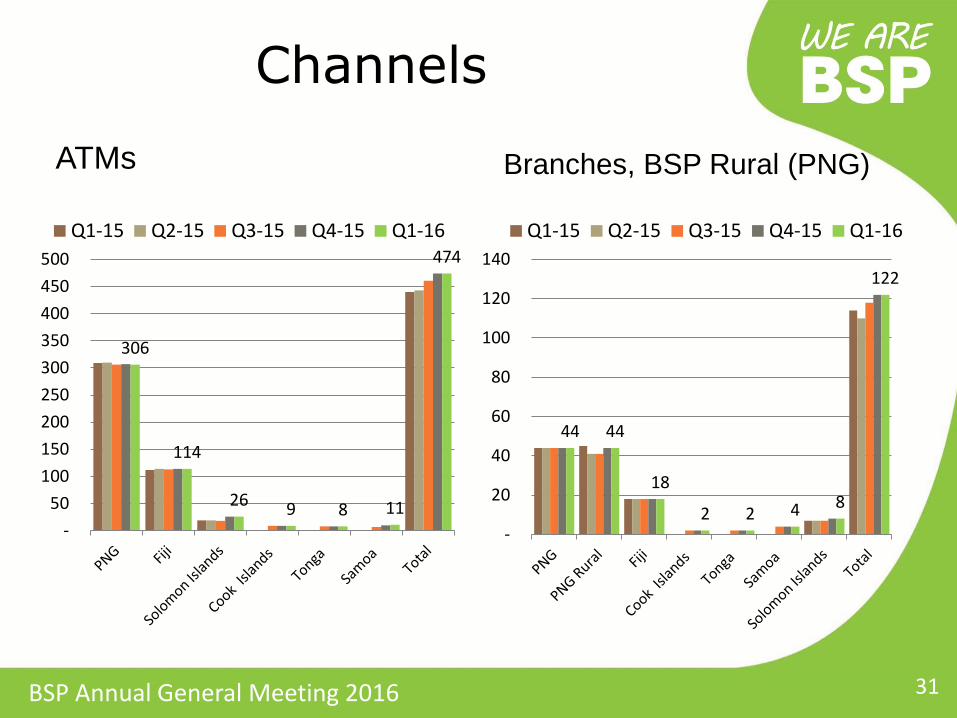

306

114

26 9 8 11

474

- 50

100 150 200 250 300 350 400 450 500

Q1-15 Q2-15 Q3-15 Q4-15 Q1-16

Branches, BSP Rural (PNG) ATMs

Channels

31

44 44

18

2 2 4 8

122

-

20

40

60

80

100

120

140Q1-15 Q2-15 Q3-15 Q4-15 Q1-16

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

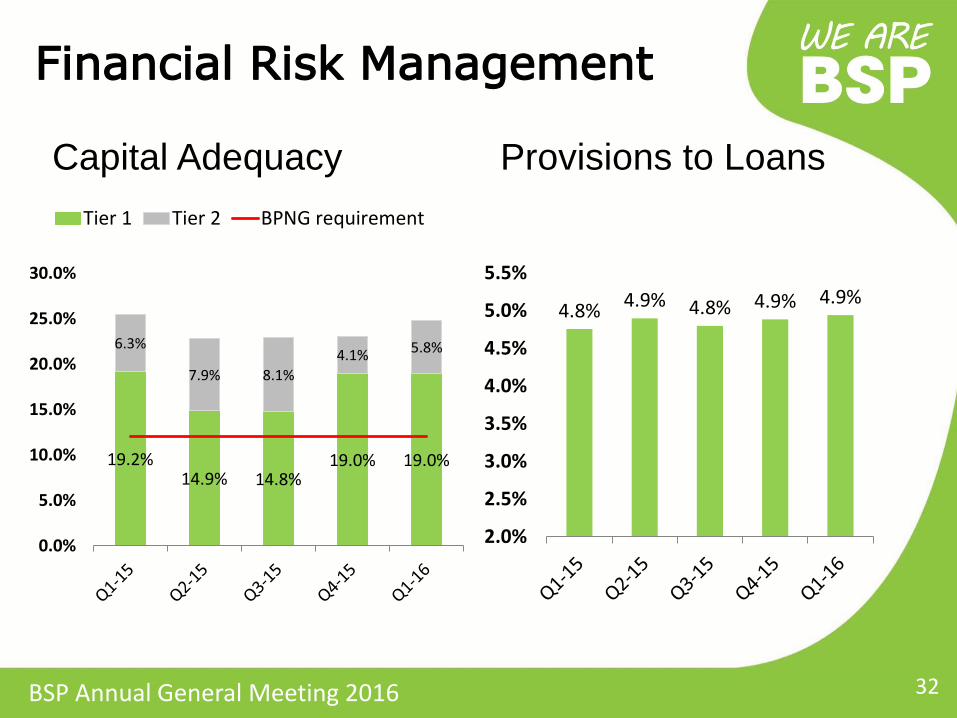

19.2% 14.9% 14.8%

19.0% 19.0%

6.3%

7.9% 8.1% 4.1% 5.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Tier 1 Tier 2 BPNG requirement

Provisions to Loans Capital Adequacy

Financial Risk Management

32

4.8% 4.9% 4.8% 4.9% 4.9%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

• Revenues – Q1/16 Revenue declined from the previous quarter. While interest income on loans grew,

it was offset by the drop in the level of FX activities, lower interest income from other interest earning assets and lower fees and commission income.

– The total operating expenses dropped to K179m this quarter from K188m, hence a savings of 6%. This was largely attributed to cost savings in general admin expenses, as well as lower amortization expenses on software

– Cost to income ratio for the Group increased by 0.4% to 45.1% reflecting Q1’16 reduced quarterly revenue vs. Q4’15

• Balance Sheet – Continued stable lending market share in PNG, with stabilizing deposit market. – Capital Adequacy for the Group as at March 2016 has increased from 23.1% in Dec’15 to

24.8%, well above BPNG requirement of 12%. • Others

- BSP Finance Ltd continues to grow it’s operation in both PNG & Fiji, and exploring growth opportunities outside these countries.

- New banking operations in Samoa, Tonga, Cook Islands and SI are progressing well. Regulatory approval granted by RBV, with completion of Vanuatu acquisition expected in July 2016.

Qtr.1-2016 Performance Summary

33

Sub - title of Presentation

Slide 1 BSP Annual General Meeting 2016

Share Price

K3.506bn market Cap

0.0

0.5

1.0

1.5

2.0

2.5

K6.20

K6.40

K6.60

K6.80

K7.00

K7.20

K7.40

K7.60

Mar-15 May-15 Jul-15 Sep-15 Nov-15 Jan-16 Mar-16

Closing price (Kina)

red

Volume traded (millions)

green Share Price

34

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Dividend

22.5 toea

• Interim

63 toea •Final

85.5 toea • Full

• 11.4% yield (on K7.50) • Payment on 24th June,

2016

35

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

• 2015 was an outstanding year with better than market performance

• Cost to income ratio of 44.7% reinforces a strong cost focus

• Capital adequacy, loan loss reserves, dividend yield and EPS all market leading

• BSP’s expansion in the South Pacific well executed

• Increasing contribution from non PNG Business

• BSP is a significant contributor to economic growth in PNG and the Pacific

Conclusion

36

Sub - title of Presentation Slide 1 BSP Annual General Meeting 2016

Thank You

37