Roadshow June 27-29, 2005 Silvio de Carvalho Executive Director.

56

Roadshow June 27-29, 2005 Silvio de Carvalho Executive Director

-

date post

22-Dec-2015 -

Category

Documents

-

view

216 -

download

2

Transcript of Roadshow June 27-29, 2005 Silvio de Carvalho Executive Director.

Roadshow

June 27-29, 2005

Silvio de CarvalhoExecutive Director

2

Agenda

Brazilian Economy

Brazilian Banking System

Highlights

Strategy and In-depth Results

Performance of the Shares

3

Brazilian Macroeconomic Scenario

Floating exchange rate and outstanding adjustment in external

accounts

Monetary policy: inflation expectation and growth

Fiscal policy: accomplishment of fiscal targets, even without IMF

surveillance

Credit expansion: private sector crowding out

Baseline scenario

Brazil: towards investment grade

4

Recent overvaluation of the real

Jun-05 2.4

1.01.52.02.53.03.54.04.55.05.56.06.57.0

Ja

n-8

4

Ja

n-8

5

Ja

n-8

6

Ja

n-8

7

Ja

n-8

8

Ja

n-8

9

Ja

n-9

0

Ja

n-9

1

Ja

n-9

2

Ja

n-9

3

Ja

n-9

4

Ja

n-9

5

Ja

n-9

6

Ja

n-9

7

Ja

n-9

8

Ja

n-9

9

Ja

n-0

0

Ja

n-0

1

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Effective basket 92-93 average R$/US$ Euro

Collor-ItamarPeriod

Pegged currency

Floating exchange rate

Plano Real

3.2

Real exchange rate

5

Trade surplus continues to widen

25

30

35

40

45

50

55

60

65

70

75

80

85

90

95

100

105

Jan

-03

Feb

-03

Mar-

03

Ap

r-0

3

May-0

3

Jun

-03

Jul-

03

Au

g-0

3

Sep

-03

Oct-

03

Nov-0

3

Dec-0

3

Jan

-04

Feb

-04

Mar-

04

Ap

r-0

4

May-0

4

Jun

-04

Jul-

04

Au

g-0

4

Sep

-04

Oct-

04

Nov-0

4

Dec-0

4

Jan

-05

Feb

-05

Mar-

05

Ap

r-0

5

May-0

5 6

8

10

12

14

16

18

20

22

24

26

28

30

32

34

36

38

Exports (L) Imports (L) Trade balance (R)

Trade surplus – accumulated in 12-months

US$ billion

Source: Central Bank of Brazil

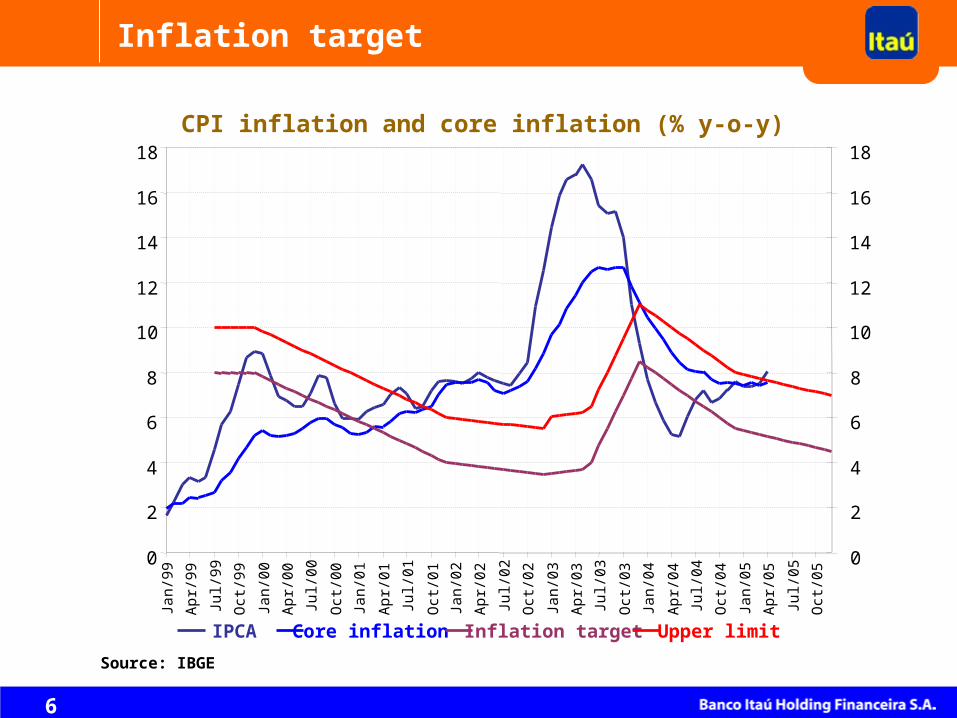

6

Inflation target

Source: IBGE

0

2

4

6

8

10

12

14

16

18Ja

n/9

9

Apr/

99

Jul/9

9

Oct

/99

Jan/0

0

Apr/

00

Jul/0

0

Oct

/00

Jan/0

1

Apr/

01

Jul/0

1

Oct

/01

Jan/0

2

Apr/

02

Jul/0

2

Oct

/02

Jan/0

3

Apr/

03

Jul/0

3

Oct

/03

Jan/0

4

Apr/

04

Jul/0

4

Oct

/04

Jan/0

5

Apr/

05

Jul/0

5

Oct

/05

0

2

4

6

8

10

12

14

16

18

IPCA Core inflation Inflation target Upper limit

CPI inflation and core inflation (% y-o-y)

7

Inflationary expectations converging back toward the target

Median of market expectations for IPCA (%)

20056.35

20065.00

4.0

4.5

5.0

5.5

6.0

6.5

7.0

Jan-04 Mar-04 May-04 Jul-04 Sep-04 Nov-04 Jan-05 Mar-05 May-05

2005 2006

Source: Focus Survey/Central Bank of Brazil

8

Growth resumption and recent convergencetowards potential growth

2.4%

1.1%

0.1%

-0.5%

1.9%

4.2% 4.0%

2.5%

0.2%0.7%

2.5%

1.4%1.2%

4.9%4.6%

-1%

0%

1%

2%

3%

4%

5%

19

98

.I

19

98

.III

19

99

.I

19

99

.III

20

00

.I

20

00

.III

20

01

.I

20

01

.III

20

02

.I

20

02

.III

20

03

.I

20

03

.III

20

04

.I

20

04

.III

20

05

.I

15

16

17

18

19

20

21

1997.I

V

1998.I

I

1998.I

V

1999.I

I

1999.I

V

2000.I

I

2000.I

V

2001.I

I

2001.I

V

2002.I

I

2002.I

V

2003.I

I

2003.I

V

2004.I

I

2004.I

V

2005.I

I

2005.I

V

GDPGrowth accumulated in 4 quarters

Fixed Investment/GDP (%) -Prices as of the previous year average 2005:

19.5%

average 2004: 18.8%

Source:IBGE and Banco Itaú´s projection

9

Primary surplus since 1998

-2.47%

-7.49%

5.01%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

Dec/

98

Jun/9

9

Dec/

99

Jun/0

0

Dec/

00

Jun/0

1

Dec/

01

Jun/0

2

Dec/

02

Jun/0

3

Dec/

03

Jun/0

4

Dec/

04

Nominal deficit Interest payments Primary surplus

Apr-05

Fiscal policy stance

Source: Central Bank of Brazil

10

Increase in the private investment/GDP (%)

Source: Central Bank of Brazil

Total Credit and Public Sector Debt

20

25

30

35

40

45

50

55

60

65

Jul-9

4

No

v-9

4

Ma

r-9

5

Jul-9

5

No

v-9

5

Ma

r-9

6

Jul-9

6

No

v-9

6

Ma

r-9

7

Jul-9

7

No

v-9

7

Ma

r-9

8

Jul-9

8

No

v-9

8

Ma

r-9

9

Jul-9

9

No

v-9

9

Ma

r-0

0

Jul-0

0

No

v-0

0

Ma

r-0

1

Jul-0

1

No

v-0

1

Ma

r-0

2

Jul-0

2

No

v-0

2

Ma

r-0

3

Jul-0

3

No

v-0

3

Ma

r-0

4

Jul-0

4

No

v-0

4

Ma

r-0

5

% GDP

20

22

24

26

28

30

32

34

36

38

40% GDP

Net public debt Total credit

11

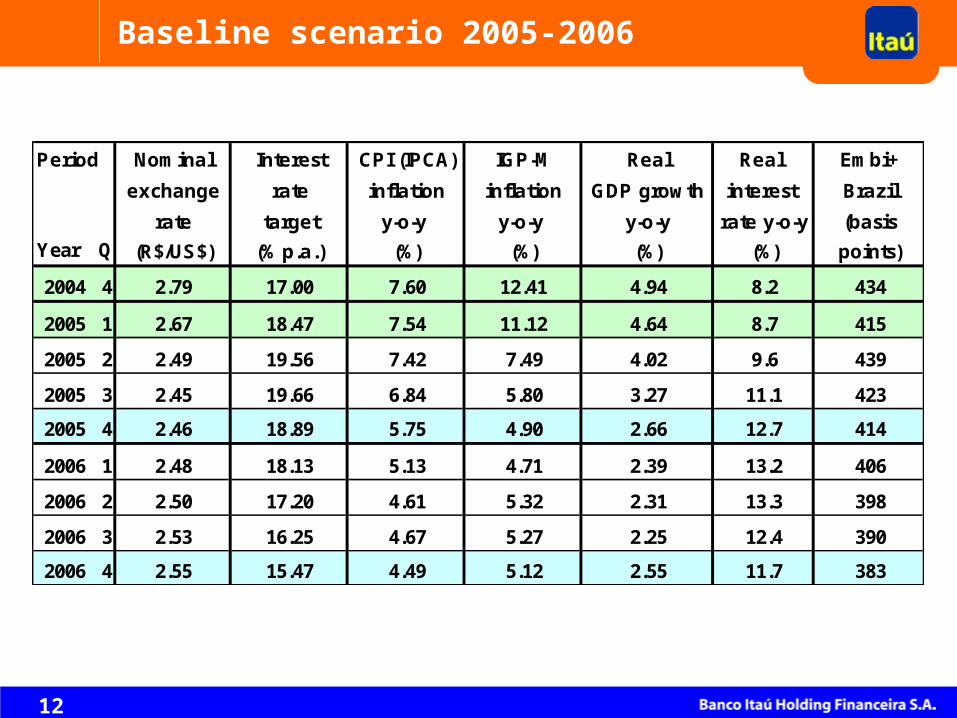

Baseline scenario 2005-2006

Hypothesis:

Exchange rate: remains constant in real terms, taking into account the difference between Brazil’s CPI (IPCA) inflation and US PPI inflation

Inflation expectations: 6.2% in 2005 and 5.0% in 2006 (Focus Survey on June 17, 2005)

Interest rate path: compatible with limiting aggregate demand acceleration in order to bring inflation back to the target path

Primary budget surplus: 4.25% of GDP in 2005 and 2006

GDP linear growth trend: 3.0% in 2005 and 3.5% in 2006

Commodities’ prices remain constant in the forecasting horizon

World trade real growth: 9.5% in 2005 and 8% in 2006

12

Baseline scenario 2005-2006

Period Nominal Interest CPI (IPCA) IGP-M Real Real Embi+

exchange rate inflation inflation GDP growth interest Brazil

rate target y-o-y y-o-y y-o-y rate y-o-y (basis

Year Q (R$/US$) (% p.a.) (%) (%) (%) (%) points)

2004 4 2.79 17.00 7.60 12.41 4.94 8.2 434

2005 1 2.67 18.47 7.54 11.12 4.64 8.7 415

2005 2 2.49 19.56 7.42 7.49 4.02 9.6 439

2005 3 2.45 19.66 6.84 5.80 3.27 11.1 423

2005 4 2.46 18.89 5.75 4.90 2.66 12.7 414

2006 1 2.48 18.13 5.13 4.71 2.39 13.2 406

2006 2 2.50 17.20 4.61 5.32 2.31 13.3 398

2006 3 2.53 16.25 4.67 5.27 2.25 12.4 390

2006 4 2.55 15.47 4.49 5.12 2.55 11.7 383

13

Investment grade

• The external indicators project the possibility of Brazil reaching an investment grade rating in 2008

(D/X = external debt/current account receipts equal to 1)

• Fiscal indicators lag behind, but by 2008 there is a chance that debt as % of GDP in clear declining trend would also qualify Brazil to that rating

US$ billion 2003 2004 2005 2006 2007 2008 2009 2010

Net FDI 9.9 8.5 10.0 10.0 10.0 10.0 10.0 10.0Current account/GDP 0.8% 1.9% 1.0% 0.4% 0.4% 0.7% 1.0% 1.3%

Primary Surplus (% GDP) 4.4% 4.6% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3%Public debt / GDP 57.2% 51.8% 51.4% 51.0% 48.0% 45.6% 43.7% 41.9%Current account 4.0 11.6 6.4 2.6 3.3 5.9 8.5 11.2Trade balance 24.8 33.7 31.4 28.8 28.8 29.5 30.7 32.0External debt with IMF 28.3 24.3 17.5 9.1 0.0 0.0 0.0 0.0

Total external debt (with intercia)235.4 220.3 211.2 188.7 166.0 149.1 129.6 107.3Gross Reserves 49.3 52.3 57.5 49.1 41.0 41.0 41.0 41.0Real FX devaluation 0.1% -5.4% -5.5% 0.0% 0.0% 0.0% 0.0% 0.0%Inflation rate 9.3% 7.6% 5.7% 4.0% 3.8% 3.9% 4.0% 4.0%Real interest rate 13% 8% 11% 10% 8% 6% 7% 7%Real GDP growth 0.5% 5.2% 2.5% 2.8% 4.5% 3.3% 2.9% 3.0%

International trade growth 15.2% 18.5% 9.5% 6.0% 4.5% 4.5% 4.5% 4.5%

D/X Moody's 2.62 1.92 1.68 1.38 1.14 1.02 0.87 0.70

14

Agenda

Brazilian Economy

Brazilian Banking System

Highlights

Strategy and In-depth Results

Performance of the Shares

15

Brazilian Banking System

Macro Characteristics Micro Scenario

Huge fixed costs Cost reduction / efficiency Strongly capitalized Room for growth in credit Satisfactory level of provisioning Conservative approach

Advanced risk management Advanced banking supervision; preparation for Basel II

Importance of banking service fees Specific for each segment

Profitable Target: to keep profitability in lower margins scenario

Oriented to services Intensive use of technology, focused

on self-service and Internet All bills are paid in the banks

Huge transaction volumes

High spreads Falling due to decline in interest rates

Dimension Differentiated needs

High reserve requirements High impact over spreads

16

Declining Interest Rates x Increasing Loan Demand: New Revenue Dynamics

Growing Fee Earnings and Tighter Cost Control To Offset Lower Treasury Gains

Focus on Higher-Yielding Consumer Finance and SME Lending

Efforts of Client Acquisition and Gains of Scale

Government Still Attracts Large Portions of the System’s Liquidity; Gradual Replacement of Bonds By Loans

Public Sector Banks Still Dominant: 45% of Deposits

More Aggressive Competition, Not Price Wars

Current Scenario

17

1. Citigroup2. Crédit Agricole Group 3. HSBC Holdings4. Bank of America Corp.5. JP Morgan Chase & Co.6. Mizuho Financial Group7. Mitsubishi Tokyo8. Royal Bank of Scotland9. Sumitomo Mitsui10. BNP Paribas20. ABN AMRO Bank109. Bradesco113. Bank of Taiwan114. Banco Itaú116. Standard Bank Group117. Banco do Brasil171. Unibanco

December 2003

Assets

1,2641,1051,034

736771

1,285975806950989668617041818024

US$Billion

2nd

4th

5th

15th

13th

1st

8th

10th

9th

7th

18th

139th

125th

197th

115th

117th

268th

Rank

BIS

12.0 %10.5 %12.0 %11.9 %11.8 %11.4 %13.0 %11.8 %11.4 %12.9 %11.7 %19.9 %14.6 %

19.8 %14.8 %13.7 %18.6 %

Index

6755554443383735343223544442

SE(1)

US$ Billion

ROA

%

167th

633rd

401st

154th

382th

638th

536th

361st

755th

569th

510th

309th

816th

17th

283rd

169th

84th

Rank (*)

Source: The Banker Top 1000 - July/04 (1) Stockholder´ Equity

2.1 %0.7 %1.2 %2.2 %1.3 %0.7 %0.9 %1.4 %0.4 %0.8 %0.9 %1.5 %0.3 %4.7 %1.6 %2.1 %2.8 %

The Banker Top 1000

18

Capital (Tier One) / Assets (%)

9.2%

14.2%

12.3%11.4%11.7%

9.1%9.9%

9.1%10.2%

12.0%11.9%11.1%

9.1%7.8%

4.3% 4.4% 4.5% 4.7% 4.7% 4.6% 4.6% 4.5% 4.7% 4.9% 4.7% 4.6% 4.5% 4.4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

90 91 92 93 94 95 96 97 98 99 00 01 02 03

Brazilian Banks 1,000 Largest Banks in the World

Source: THE BANKER - Top 1000 – July 2004

19

1. Citigroup2. Bank of America Corp.3. HSBC4. JP Morgan Chase & Co.5. RBS Group†6. Wells Fargo & Co.7. UBS AG8. Wachovia Corp.9. Santander10. Barclays13. Morgan Stanley19. Merrill Lynch & Co.20. US Bancorp21. Credit Suisse Group22. Goldman Sachs23. Lloyds TSB47. Hang Seng Bank49. Bank of New York Co. Inc.56. Banco Itaú Holding Financeira S.A. 65. Kookmin Bank67. Bradesco97. Banco do Brasil S.A.139. Unibanco

BanksMarket Cap.

251,782188,517177,236133,058108,009103,82998,23785,24279,85770,94465,20357,16557,03855,76455,41454,43826,00023,96120,27716,14415,6719,8105,238

US$ Million

United StatesUnited StatesUnited KingdomUnited StatesUnited KingdomUnited StatesSwitzerlandUnited StatesSpainUnited KingdomUnited StatesUnited StatesUnited StatesSwitzerlandUnited StatesUnited KingdomHong kongUnited StatesBrasilKoreaBrasilBrasilBrasil

Country

Source : UBS Global Banks Valuations 03/08/05

Itaú is the 2nd largest bank

by Market Cap. in

Emerging Markets

Global Banks Valuations

20

Agenda

Brazilian Economy

Brazilian Banking System

Highlights

Strategy and In-depth Results

Performance of the Shares

21

69.681.8

127.0146.4

130.3118.8111.1

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

27.334.3

45.4 44.653.3

44.8

57.0

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

6.6 7.69.0

11.914.0

12.514.6

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

7.3 8.110.0

14.217.1

8.611.6

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

+15.3% +16.8%

+27.4%

+35.2%

Highlights

Assets (R$ Billion)

Credit Operations (R$ Billion)

Stockholders’ Equity (R$ Billion)

Technical Provisions – Insurance, Pension Plans and Capitalization (R$ Billion)

22

3,0612,373

10,2209,224

7,2505,892

4,541

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

1,841

3,776

8761,141

3,152

2,3772,389

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

7,056

8,770

2,3812,183

9,0148,425

5,996

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

3,6994,277

6,165

1,405 1,794

3,465

5,121

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

+30.3% +27.7%

+9.1% +29.0%

Highlights

Net Income (R$ Million)

Administrative Expenses (R$ Million)

Banking Service Fees (R$ Million)

Net Interest Margin (R$ Million)

23

27.7%31.5%

26.3% 26.5% 27.0%31.2%

35.1%

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

2,6%2,9%

2,1%

2,7%2,9% 2,8%

3,2%

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

14.4%16.9%

18.4%19.8% 20.6% 19.8%

18.3%

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

67.2%62.1% 58.2% 54.5% 52.4%

58.0%49.4%

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

Obs: Annualized quarterly indexes.

Highlights

ROE (%)

ROA (%)

BIS Ratio (%)

Efficiency Ratio (%)

24

3,0763,1463,0733,1723,1923,184

2,995

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

3,7753,293

3,6243,157

2,5981,998

1,427

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

21,34620,13320,02121,150

17,926

13,77712,064

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

42,450 45,31642,058

44,99243,21545,40947,524

2000 2001 2002 2003 2004 1stQ/04

1stQ/05

(*) Without Credicard and FIC employees.

Highlights

Branches+CSBs

Internet Banking Clients (In million)

ATMs

Employees

(*)

25

Agenda

Brazilian Economy

Brazilian Banking System

Highlights

Strategy and In-depth Results

Performance of the Shares

26

2. Growth of Credit Portfolio on the quarter of 7.0%: Personal Credit (22.2%) and Automobile (17.3%);

5. Full amortization of the goodwill: Associating process with LASA, amounting R$ 182 million (after tax effects);

3. Growth of Provisions: Constitution of R$ 150 million of Exceeding Provision for Loan Losses on the quarter, amounting R$ 1,150 million;

Maintenance of Additional Provision for Securities Portfolio of R$ 400 million;

1. Results: Net Income of R$ 1,141 million with an increase of 10.8% q-o-q and of 30.3% when compared to the net income of R$ 876 million of the 1st. Q/04; ROE 35.1%; Earnings per share R$ 10.04;

4. Delinquency: Maintenance of the Nonperforming Loans ratio in 2.9%;

6. Creation of a new segment – Consumer Credit - Itaucred: disclosure of the result of operations performed in channels for non-account customers.

Highlights

27

Itaú

CorporationItaucredItaú BBAItaubanco

Segmentation

28

Itaú

ItaucredItaú BBAItaubanco

Banking

Credit Cards

Insurance, Pens. Plans

and Capitalization

Resources Managed

Segmentation

Corporation

29

R$ Million

(*) Rural and Mortgage Loans – Loans linked to the availability of Demand deposits and Savings deposits.

Mar 31, 05 Dec 31, 04 Mar 31, 04Var Mar, 05

-Dec, 04Var Mar, 05

-Mar, 04

Individuals 20,770 18,272 12,769 13.7%. 62.7%

Loans to Companies 31,891 30,467 28,255 4.7% 12.9%

Small and Medium Sized 9,037 8,571 5,650 5.4% 60.0%

Corporate 22,854 21,896 22,605 4.4% 1.1%

Mandatory Loans (*) 4,351 4,536 3,732 -4.1% 16.6%

Total - Loans 57,012 53,275 44,757 7.0% 27.4%

Public Securities - Brazil 7,218 7,486 12,939 -3.6% -44.2%

Private Securities 11,660 12,145 9,526 -4.0% 22.4%

Total - Securities 18,878 19,631 22,465 -3.8% -16.0%

Total 75,890 72,906 67,221 4.1% 12.9%

Exposure – Loans and Securities

30

16,890

47,40750,980

19,596

27,253

34,282

44,581

53,27557,012

38,419 38,659

29,615

23,674

14,058

16,916

45,414

0

10,000

20,000

30,000

40,000

50,000

60,000

1998 1999 2000 2001 2002 2003 2004 2005 (*)

Credit Operations Credit Operations including Endorsements and Sureties

R$ Million

CAGR: 21.5%

CAGR: 22.9%

Credit Operations

(*) On March 31, 2005.

Credit Portfolio

31

9

34

16

41

2004

Restricted Loans

Individuals

Small and Medium-sized companies

Corporate Loans

In %

9

29

11

51

2003

40%

8

36

16

40

Mar/2005

52%

Change in the mix of the Credit Portfolio

32

Coverage Ratio (*)

202% 204%210%

220% 221%

0%

50%

100%

150%

200%

250%

Mar-04 Jun-04 Sep-04 Dec-04 Mar-05

Nonperforming Loans Ratio (%)

4.03.5

3.22.9 2.9

5.66.0 5.6

6.57.3

0.80.9

1.51.81.9

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Mar-04 Jun-04 Sep-04 Dec-04 Mar-05

Nonperforming Loans Ratio – GlobalNonperforming Loans Ratio – IndividualsNonperforming Loans Ratio – Companies

(*) Provision for Loan Losses / Total Nonperforming Loans

We are not expecting an ongoing improvement in these indicators, because of the focus on credit products with higher margins, but, at the same time, with a higher credit risk.

Nonperforming Loans Ratio and Coverage Ratio

33

SecuritiesAdjust. market value

Additional Provision

Total

(*) Values differ from the one published in note “Market Value” because they are net of the additional provision for securities.

Additional Provision for Loan Losses (PDD)

Financial Instruments: Market vs. Recorded Value(*)

R$ 540 million

R$ 400 million

R$ 3.7 billion

Mar. 31, 2005

R$ 1.15 billion

R$ 1.75 billion

R$ 733 million

R$ 400 million

R$ 3.8 billion

Dec. 31, 2004

R$ 1.0 billion

R$ 1.67 billion

R$ 712 million

R$ 545 million

R$ 4.0 billion

Mar. 31, 2004

R$ 1.0 billion

R$ 1.73 billion

Conservative Accounting Practices

34

R$ Million

(1) Mutual Funds and Consortium.(2) Adjusted in 4Q04 in R$ 124 million related to Collection Services for INSS.

1st Q/05 4th Q/04 Var 1Q05- 4Q04

Var 1Q05- 1Q04

Asset Management (1) 398 376 345 22 53

Current Account Services 349 327 289 22 60

Credit Cards 437 371 244 66 193

Sureties and Credits 271 266 195 4 76

Collection Services (2) 209 178 203 31 6

Other 131 158 129 (26) 2

Total 1,794 1,675 1,405 119 389

1st Q/04

Service Fees

35

R$ Million

03/31/05 12/31/04 03/31/04

Stockholders’ Equity

Interbank Deposits 4 14 9

Securities and Derivatives 555 620 693

Credit Operations 216 248 399

Investment on BPI 765 660 697 Time and Interbank Deposits and Funds from

acceptance and issuance of securities abroad9 (41) 71

Securitization of Payment Orders Abroad 91 93 109

Subordinated Debt and Treasury Shares 506 480 298

Total Unrealized 2,147 2,074 2,275

Unrealized Income/(Loss) (1) (2)

(1) Tax effects not considered.(2) Includes unrealized minority interest gains in Equity of R$ 336 million in March/05, R$ 299 million in December/04, R$ 399 million

in March/04.

Financial Instruments – Market Value

36

(1) Excludes endorsements and sureties.

Maturity of Operations (in days)

R$ Million

Credit Operations (*)

Securities and Derivatives

Total (A)

Assets

12,717

11,579

24,296

0-30

15,162

4,254

19,416

31-180

6,661

3,638

10,299

181-365

16,009

10,680

26,689

Over 365

50,980

30,150

81,130

Total

Deposits

Money Market

Total (B)

Liabilities

34,341

7,174

41,515

0-30

4,378

2,399

6,777

31-180

3,842

999

4,841

181-365

1,464

6,794

8,258

Over 365

44,025

17,367

61,392

Total

Total (A)-(B) (17,219) 12,639 5,457 18,431 19,738

March 31, 2005

37

R$ Million

Highlights of Pro Forma Segments

Note: The Consolidated figures do not represent the sum of the parts because certain intercompany transactions were eliminated only at the Consolidated level.

(1) Quarterly Net Income. (2) including Endorsements and Sureties.

Itaubanco Itaú BBA Itaucred Corporation Itaú

Net Income (1) 767 257 123 (7) 1,141 Allocated Capital Tier I 7,588 3,235 1,106 2,699 14,629 ROE (%) 47.0% 35.8% 52.4% -1.0% 35.1%Credit Portfolio (2) 23,928 22,472 10,612 - 57,012 Total Assets 119,595 40,919 10,275 5,358 146,403

Mar/05

Itaubanco Itaú BBA Itaucred Corporation Itaú

1,332 242 105 (648) 1,030 6,868 3,194 975 2,934 13,971

103.2% 33.9% 50.7% -63.2% 32.9%

22,070 22,051 9,154 - 53,275 101,119 33,902 8,863 6,597 130,339

Dec/04

Net Income (1)

Allocated Capital Tier I

ROE (%)

Credit Portfolio (2)

Total Assets

38

Itaubanco - Banking

Credit Cards

Insurance, Pension Pl. and Cap.

Mutual Funds and Managed Portfolio

Total

R$ Million

1st Q/05 4th Q/04 (*) Variation

469 637 (168)

105 69 36

132 101 31

61 38 23

767 846 (79)

1st Q/05

61.1%

8.0%

17.2%

13.7%

Itaubanco - BankingCredit CardsInsurance, Pension Plans and CapitalizationMutual Funds and Managed Portfolio

Diversification of income sourcesNot dependent only on interest rates

(*) Adjusted by eventual items of R$ 612 million in Net Interest Margin, R$ 124 million in Service Fees and of R$ 250 million in Tax Income and Social Contribution.

Consolidated Net Income

39

Credit Cards

R$ Million (Except where indicated)

Participation in the Net Income of Orbitall and Redecard

Nº of Cards - Itaucard (thousands)

Nº of Cards - Credicard (thousands) (*)

Nº of Cards - Total (thousands)

2004 2003 Variation

7,085

3,595

10,680

12,956

6,519

19,475

390

90

480

5,780

2,246

8,026

10,603

4,787

15,390

400

99

499

1,305

1,349

2,654

2,353

1,732

4,085

(10)

(9)

(19)

22.6%

60.0%

33.1%

22.2%

36.2%

26.5%

-2.5%

-9.1%

-3.8%

(*) Corresponds to the share of Credicard owned by Itaú – 50% at 2004 and 33% at 2003.

63 41 22 53.7%

Turnover - Itaucard

Turnover - Credicard (*)

Turnover - Total

Net Income - Itaucard

Net Income - Credicard (*)

Net Income - Total

40

R$ Million

The Combined Ratio has shown a falling trend for 8 quarters.

1st Q/05 4th Q/04 VariationInsurance Premiums, Pension Plans Contributions and Premium Bonds Revenues 1,362 1,695 (333)

Changes in Technical Provisions (382) (843) 461 Selling Expenses (108) (103) (5) Insurance Claims, Pension Plans Benefits and Premium Bonds Redemption (690) (578) (112)

Other Operating Income/(Expenses) 1 15 (14) Operating Margin 183 186 (3) Financial Income 123 115 8 Non-Interest Expenses (143) (152) 9 Income Tax and Social Contribution (46) (23) (23) Other 15 (24) 39

132 101 31

Combined Ratio 90.9% 92.9% 2.0%

Claim Ratio 51.2% 49.7% 1.5%

Result of Ins., Pension Plans and Cap.

Insurance, Pension Plans and Capitalization

41

87.199.8

105.2

Mar-04 Dec-04 Mar-05

8.6

11.0 11.6

Assets under Management andTechnical Provisions

R$ Billion

Technical Provisions of Insurance, Pension Plans and Capitalization

Volume of Mutual Funds and Portfolios under Management

Growth of 20.8% in the volume of Funds and Portfolios under Management and 35.2% in the volume of Technical Provisions in relation to Mar/2004

42

Itaú

CorporationItaucredItaú BBAItaubanco

Corporate Operation

Segmentation

43

R$ Million

1º Tri/05 4º Tri/041st Q/05 4th Q/04 1st Q/04Var. 1Q/05

- 4Q/04Var. 1Q/05

- 1Q/04

Net Interest Margin 370 464 242 (94) 128 Result from Loan Losses 67 31 162 36 (95) Service Fees 80 84 64 (4) 16 Non-Interest Expenses (130) (159) (147) 28 17 Tax Income and Social Contribution (103) (151) (94) 49 (9) Other (27) (27) (17) 1 (10)

Net Income 257 242 210 16 47 Tier I Allocated Capital 3,235 3,194 2,768 41 467 ROE (%) 35.8% 33.9% 33.9%

Itaú BBA Pro Forma

44

Strategy

Itaú BBA: wholesale bank integrated into a financial conglomerate; Credit perspective for the corporate segment in Brazil: declining spreads, increase in

the competition, limited client base. Currently 51% of all our revenues are non-credit related;

Challenge: to maintain current profitability levels in the next years considering lower margins in credit;

Our strategy: compensate lower gains in credit with an increase in the distribution of non-credit related products and services to our clients through:

Cross-selling – continue to take advantage of the synergy with Itaú, by increasing the selling of structured treasury operations such as hedging and also simpler products such as payroll and collection;

Investment banking – segment likely to expand in the next 5 years (we expect that by the end of this period Brazil becomes an investment grade country).

Itaú BBA is well-positioned in investment banking – leader in fixed income issuances and reinforcing our variable income team in order to build a strong investment banking.

Investment banking currently stands for 5% of Itaú BBA´s revenues. In the next 5 to 6 years our goal is to increase this participation to 20%.

45

Itaú

CorporationItaucredItaú BBAItaubanco

FIC50% CBD50% Itaú

FAI50% LASA50% Itaú

Own stores

100% Itaú

Payroll Credit

FináustriaItaucred VehiclesBanco FiatIntercap

Vehicle Credit Cardsnon customers 50% Credicard

Credit for Individuals

46

Taií

New Brand Name (Itaú-based).

Focus on lower income

consumers.

Proprietary platform.

Uses the Itaú ATM network.

Diversifies credit-related

revenues.

Responsive and efficient.

Expansion of Focus on

direct consumer credit

Long term partnership: 20

years, and renewal option

Operating Management under the responsibility of Itaú

Exclusivity in exploitation

of financial products and

services to retailers’

customers

Retail partnershipsCBD and LASA

Credit for Individuals

47

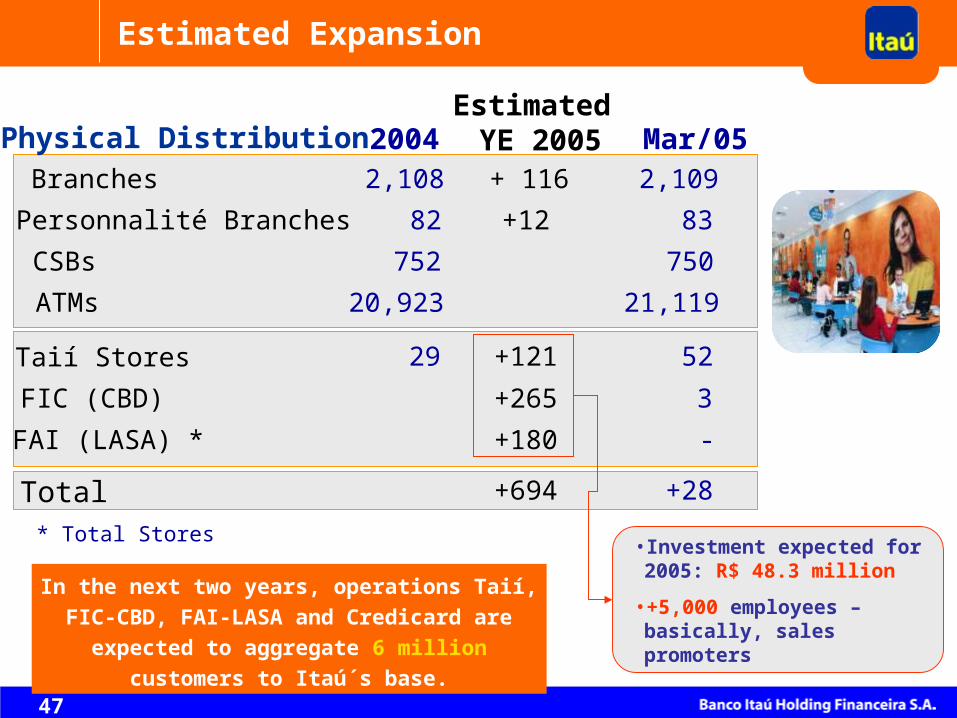

Estimated Expansion

2004

CSBs 752

FIC (CBD) +265

FAI (LASA) * +180

Physical DistributionEstimated

YE 2005Branches 2,108 + 116

Personnalité Branches 82 +12

ATMs 20,923

29 +121Taií Stores

Total +694

* Total Stores

Mar/05

750

2,109

83

21,119

52

3

-

+28

•Investment expected for 2005: R$ 48.3 million

•+5,000 employees – basically, sales promoters

In the next two years, operations Taií, FIC-CBD,

FAI-LASA and Credicard are expected to

aggregate 6 million customers to Itaú´s base.

48

3.3 millionOwn Credit Cards (Private Label)

Currently

FIC (CBD)

FAI (LASA) 186 thousand

480 thousandCredit Cards

FIC (CBD)

FAI (LASA) -

-Personal Loan Contracts

FIC (CBD)

FAI (LASA) 137 thousand

580 thousandConsumer Credit Contracts

FIC (CBD)

FAI (LASA) 32 thousand

4.7 millionTotal

In Quantities

Financial Products

49

5,780 5,951 6,261 6,639 7,085 7,518

2,245 2,308 2,413 2,4383,596 3,548

Dec-03 Mar-04 Jun-04 Sep-04 Dec-04 Mar-05

Itaucard Credicard

8,026 8,2598,674 9,077

10,680

In Thousand

Market Share: 20.7%

Leader in Brazil

Credit Card Base

Increase in Participation on Credicard

11,066

50

Agenda

Brazilian Economy

Brazilian Banking System

Highlights

Strategy and In-depth Results

Performance of the Shares

51

1.00 1.243.03 2.90

5.11 5.467.24 7.45

9.7212.11

4.956.04

7.46

15.85

21.41 21.36

27.66

33.33

0.983.26 2.88

15.99

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

22.00

24.00

26.00

28.00

30.00

32.00

34.00

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Evolution of Earnings per Share andDividends per Share (*)

CAGR = 28.6%

R$

(*) In the previous years per lot of thousand shares, as in 2004 a reverse split of shares was carried out.

CAGR = 26.2%

Dividends per Share (*)Earnings per Share (*)

52

119 148

362 343

602 629

808 829

1,108

1,372

1.00 1.24

3.03 2.90

5.46

7.24 7.45

5.11

9.72

12.11

0

200

400

600

800

1,000

1,200

1,400

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

0

2

4

6

8

10

12

14

Total Dividends Unitary Dividends

Highlight:

Increase in monthly

payments from R$ 0.17 to

R$ 0.21 per share on

May 2005

Evolution of Dividends

53

(*) Annualized

Evolution of ROE (%)

15.4%17.2%

18.9%

31.6%

26.3% 26.5% 27.0%

35.1%

27.7%

31.5%

1996 1997 1998 1999 2000 2001 2002 2003 2004 1st Q/05(*)

54

•Expansion of points of sale

•Continuity of growth in Credit

•Focus in consumer credit (Taií, FIC CBD, FAI LASA, Vehicles...)

•Credit Cards - Credicard operation

•Growth in number of customers

•Client retention

•Focus in cost-efficiency

Perspectives for 2005

55

US$

(1) With dividends reinvestment (2) Without dividends reinvestment

Evolution of US$ 100 Invested from June/95 to June/05

Preferred Shares Appreciation – in US$

0

100

200

300

400

500

600

700

800

900

1.000

95 96 97 98 99 00 01 02 03 04 05

Itaú (1)Itaú (2)

Bovespa

603

279279

875Itaú(1) Itaú(2) Ibov.

10 yers 24.22% 19.69% 10.82%

5 yers 20.03% 15.78% 3.28%

12 months 104.09% 97.66% 60.43%

Russian CrisisReal Devaluation

Mexican Crisis

Asian Crisis

Argentine Crisis

Attack to WTC Election

Period

Annual Average Appreciation in US$

Roadshow

June 27-29, 2005

Silvio de CarvalhoExecutive Director