Rjomrt-blog Rjomrt Daily Previews 04-21-2014 (2)

8

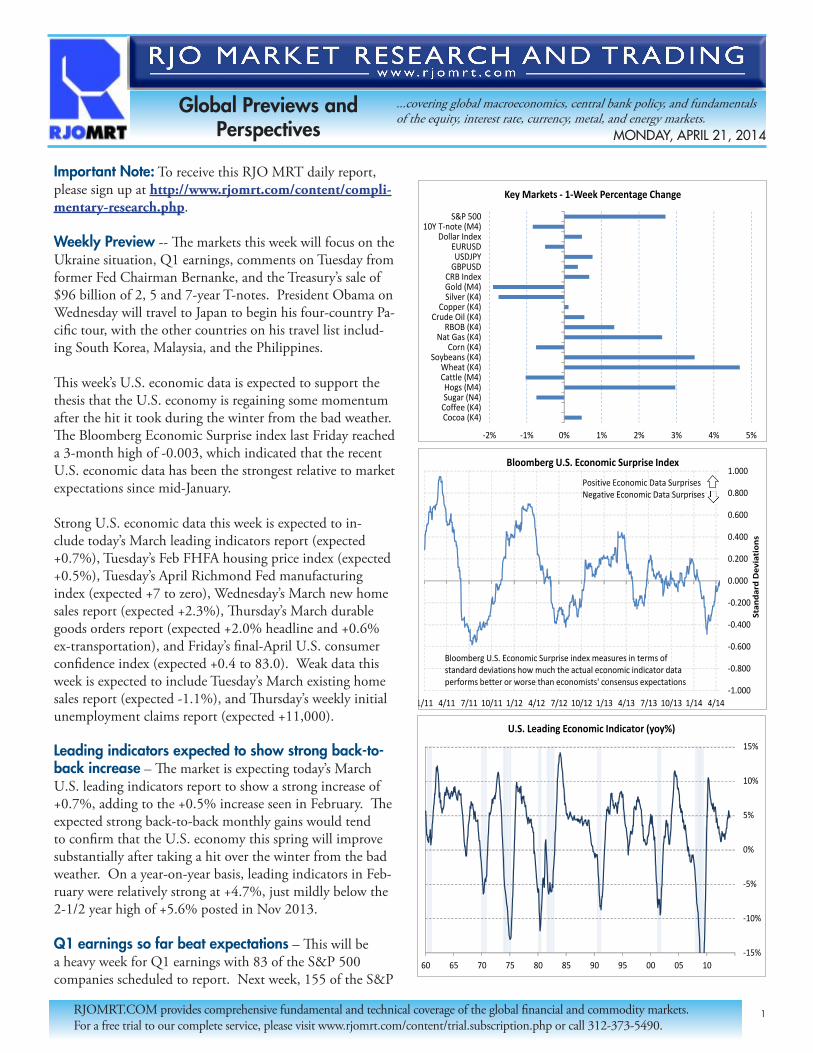

1 Global Previews and Perspectives ...covering global macroeconomics, central bank policy, and fundamentals of the equity, interest rate, currency, metal, and energy markets. RJOMRT.COM provides comprehensive fundamental and technical coverage of the global financial and commodity markets. For a free trial to our complete service, please visit www.rjomrt.com/content/trial.subscription.php or call 312-373-5490. Important Note: To receive this RJO MRT daily report, please sign up at http://www.rjomrt.com/content/compli- mentary-research.php. Weekly Preview -- e markets this week will focus on the Ukraine situation, Q1 earnings, comments on Tuesday from former Fed Chairman Bernanke, and the Treasury’s sale of $96 billion of 2, 5 and 7-year T-notes. President Obama on Wednesday will travel to Japan to begin his four-country Pa- cific tour, with the other countries on his travel list includ- ing South Korea, Malaysia, and the Philippines. is week’s U.S. economic data is expected to support the thesis that the U.S. economy is regaining some momentum after the hit it took during the winter from the bad weather. e Bloomberg Economic Surprise index last Friday reached a 3-month high of -0.003, which indicated that the recent U.S. economic data has been the strongest relative to market expectations since mid-January. Strong U.S. economic data this week is expected to in- clude today’s March leading indicators report (expected +0.7%), Tuesday’s Feb FHFA housing price index (expected +0.5%), Tuesday’s April Richmond Fed manufacturing index (expected +7 to zero), Wednesday’s March new home sales report (expected +2.3%), ursday’s March durable goods orders report (expected +2.0% headline and +0.6% ex-transportation), and Friday’s final-April U.S. consumer confidence index (expected +0.4 to 83.0). Weak data this week is expected to include Tuesday’s March existing home sales report (expected -1.1%), and ursday’s weekly initial unemployment claims report (expected +11,000). Leading indicators expected to show strong back-to- back increase – e market is expecting today’s March U.S. leading indicators report to show a strong increase of +0.7%, adding to the +0.5% increase seen in February. e expected strong back-to-back monthly gains would tend to confirm that the U.S. economy this spring will improve substantially after taking a hit over the winter from the bad weather. On a year-on-year basis, leading indicators in Feb- ruary were relatively strong at +4.7%, just mildly below the 2-1/2 year high of +5.6% posted in Nov 2013. Q1 earnings so far beat expectations – is will be a heavy week for Q1 earnings with 83 of the S&P 500 companies scheduled to report. Next week, 155 of the S&P MONDAY, APRIL 21, 2014 -15% -10% -5% 0% 5% 10% 15% 60 65 70 75 80 85 90 95 00 05 10 U.S. Leading Economic Indicator (yoy%) -2% -1% 0% 1% 2% 3% 4% 5% S&P 500 10Y T-note (M4) Dollar Index EURUSD USDJPY GBPUSD CRB Index Gold (M4) Silver (K4) Copper (K4) Crude Oil (K4) RBOB (K4) Nat Gas (K4) Corn (K4) Soybeans (K4) Wheat (K4) Cattle (M4) Hogs (M4) Sugar (N4) Coffee (K4) Cocoa (K4) Key Markets - 1-Week Percentage Change -1.000 -0.800 -0.600 -0.400 -0.200 0.000 0.200 0.400 0.600 0.800 1.000 1/11 4/11 7/11 10/11 1/12 4/12 7/12 10/12 1/13 4/13 7/13 10/13 1/14 4/14 Standard Deviations Bloomberg U.S. Economic Surprise Index Bloomberg U.S. Economic Surprise index measures in terms of standard deviations how much the actual economic indicator data performs better or worse than economists' consensus expectations Positive Economic Data Surprises Negative Economic Data Surprises

-

Upload

christopher-zylstra -

Category

Documents

-

view

214 -

download

0

Transcript of Rjomrt-blog Rjomrt Daily Previews 04-21-2014 (2)

1

Global Previews and Perspectives

...covering global macroeconomics, central bank policy, and fundamentals of the equity, interest rate, currency, metal, and energy markets.

RJOMRT.COM provides comprehensive fundamental and technical coverage of the global financial and commodity markets. For a free trial to our complete service, please visit www.rjomrt.com/content/trial.subscription.php or call 312-373-5490.

Important Note: To receive this RJO MRT daily report, please sign up at http://www.rjomrt.com/content/compli-mentary-research.php.

Weekly Preview -- The markets this week will focus on the Ukraine situation, Q1 earnings, comments on Tuesday from former Fed Chairman Bernanke, and the Treasury’s sale of $96 billion of 2, 5 and 7-year T-notes. President Obama on Wednesday will travel to Japan to begin his four-country Pa-cific tour, with the other countries on his travel list includ-ing South Korea, Malaysia, and the Philippines.

This week’s U.S. economic data is expected to support the thesis that the U.S. economy is regaining some momentum after the hit it took during the winter from the bad weather. The Bloomberg Economic Surprise index last Friday reached a 3-month high of -0.003, which indicated that the recent U.S. economic data has been the strongest relative to market expectations since mid-January.

Strong U.S. economic data this week is expected to in-clude today’s March leading indicators report (expected +0.7%), Tuesday’s Feb FHFA housing price index (expected +0.5%), Tuesday’s April Richmond Fed manufacturing index (expected +7 to zero), Wednesday’s March new home sales report (expected +2.3%), Thursday’s March durable goods orders report (expected +2.0% headline and +0.6% ex-transportation), and Friday’s final-April U.S. consumer confidence index (expected +0.4 to 83.0). Weak data this week is expected to include Tuesday’s March existing home sales report (expected -1.1%), and Thursday’s weekly initial unemployment claims report (expected +11,000).

Leading indicators expected to show strong back-to-back increase – The market is expecting today’s March U.S. leading indicators report to show a strong increase of +0.7%, adding to the +0.5% increase seen in February. The expected strong back-to-back monthly gains would tend to confirm that the U.S. economy this spring will improve substantially after taking a hit over the winter from the bad weather. On a year-on-year basis, leading indicators in Feb-ruary were relatively strong at +4.7%, just mildly below the 2-1/2 year high of +5.6% posted in Nov 2013.

Q1 earnings so far beat expectations – This will be a heavy week for Q1 earnings with 83 of the S&P 500 companies scheduled to report. Next week, 155 of the S&P

MONDAY, APRIL 21, 2014

-15%

-10%

-5%

0%

5%

10%

15%

60 65 70 75 80 85 90 95 00 05 10

U.S. Leading Economic Indicator (yoy%)

-2% -1% 0% 1% 2% 3% 4% 5%

S&P 50010Y T-note (M4)

Dollar IndexEURUSDUSDJPY

GBPUSDCRB IndexGold (M4)Silver (K4)

Copper (K4)Crude Oil (K4)

RBOB (K4)Nat Gas (K4)

Corn (K4)Soybeans (K4)

Wheat (K4)Cattle (M4)Hogs (M4)Sugar (N4)

Coffee (K4)Cocoa (K4)

Key Markets - 1-Week Percentage Change

-1.000

-0.800

-0.600

-0.400

-0.200

0.000

0.200

0.400

0.600

0.800

1.000

1/11 4/11 7/11 10/11 1/12 4/12 7/12 10/12 1/13 4/13 7/13 10/13 1/14 4/14

Stan

dard

Dev

iati

ons

Bloomberg U.S. Economic Surprise Index

Bloomberg U.S. Economic Surprise index measures in terms of standard deviations how much the actual economic indicator data performs better or worse than economists' consensus expectations

Positive Economic Data SurprisesNegative Economic Data Surprises

RJO MRT GLOBAL PREVIEWS & PERSPECTIVES

2

500 companies will report earnings. Notable reports this week include Halliburton and Netflix on Monday; McDon-alds, AT&T, and Yum Brands on Tuesday; Apple, Procter & Gamble, and Texas Instruments on Wednesday; Microsoft, Amazon, Visa, UPS, Starbucks, Time Warner, and Caterpil-lar on Thursday; and Ford and Moody’s on Friday.

Q1 earnings expectations improved to +1.7% from +0.9% a week earlier due to some better-than-expected earnings reports last week, according to Thomson Reuters I/B/E/S. Of the 83 S&P 500 companies that have reported earnings thus far, 63% have beaten earnings, which is right on the long-term average, according to Thomson I/B/E/S. After weak earnings growth for Q1, the market is expecting an improvement to +8.1% in Q2, +11.4% in Q3, and +11.2% in Q4.

U.S. may soon decide on new sanctions on Russia since there has been no de-escalation of tensions -- Vice President Biden will visit Kiev on today and Tuesday to meet with Ukrainian leaders in a show of U.S. sup-port. Meanwhile, there has been no sign of de-escalation after Russia last Thursday agreed with the U.S. Europe and Ukraine to de-escalate tensions. Instead, Russian-supported separatists in eastern and southern Ukraine said they would not abide by the agreement and there were shoot-outs in eastern Ukraine over the weekend. We believe there is a good chance that the U.S. within the next 2-3 weeks will announce broader sanctions on Russia since the situation is not likely to improve. Two members of the Senate Foreign Relations Committee over the weekend (Democratic Sena-tor Chris Murphy and Republican Senator Bob Corker) called for stepped-up sanctions on Russia, including sector-wide sanctions on Russia’s oil and banking sectors.

The global stock markets will not take sector-wide sanctions on Russia well considering that they will hurt the European and global economies as well. Yet broader sanctions are likely necessary to discourage Russia from a continuous series of similar takeovers of its neighbors in coming years. Broader sanctions are also necessary as a warning to China not to engage in similar takeovers in the large number of territorial disputes it has with its neighbors.

Overseas news dominated by Chinese and European PMIs -- In overseas news this week, the European markets are closed today for Easter Monday. China’s HSBC April manufacturing PMI report on Tuesday night is expected to show a small +0.3 point increase to 48.3, reversing part of the -0.5 point drop to 48.0 seen in March. On Wednesday, Germany’s April manufacturing PMI is expected to show a small +0.1 point increase to 53.8 while the Eurozone April manufacturing PMI is expected to be unchanged at 53.0,

1112131415161718192021222324252627282930

9501000105011001150120012501300135014001450150015501600165017001750180018501900

1/11 7/11 1/12 7/12 1/13 7/13 1/14

P/E

Ratio

S&P

500

Inde

x

S&P 500 Index vs Forward Price/Earnings Ratio

S&P 500 Forward P/E Ratio

S&P 500 Index (daily data)

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

91 93 95 97 99 01 03 05 07 09 11 13

S&P 500 Earnings Growth (yoy%)

Q4-09: +206%Q1-10: +58%

Consensus for Q1-Q4 2014

Source: Thomson One

Earnings Consensus: Annual: 2013: +5.8%; 2014 +11.3%Quarterly4Q13: +9.9%1Q14: +1.7%2Q14: +8.1%3Q14: +11.4%4Q14: +11.2%

both remaining comfortably above the expansion-contraction level of 50.0. The Bank of England on Wednesday will release the minutes from its April 9-10 policy meeting. Germany’s April IFO business climate index on Thursday is expected to fall -0.3 points to 110.4. Japan’s March CPI on Thursday is expected to edge higher to +1.6% y/y from +1.5% in Feb.

RJO MRT GLOBAL PREVIEWS & PERSPECTIVES

3

Market Recap

• U.S. weekly initial unemployment claims rose +2,000 to 304,000, less than expectations of +15,000 to 315,000. Weekly continuing claims unexpectedly fell -11,000 to 2.739 million, better than expectations of a +4,000 increase to 2.780 million and the lowest in 6-1/3 years.

• The Apr Philadelphia Fed manufacturing index rose +7.6 to 16.6, better than expectations of +1.0 to 10.0 and the fastest pace of expansion in 7 months.

• German Mar PPI fell -0.3% m/m and -0.9% y/y, weaker than expecta-tions of unch m/m and -0.7% y/y.

• Market closes

• Stock Market -- The S&P 500 index on Thursday closed slightly higher. Bullish factors included (1) the +2,000 increase in U.S. weekly initial unemployment claims, less than expectations of +15,000, (2) the +7.6 point increase in the Apr Philadelphia Fed manufacturing index to a 7-month high of 16.6, better than expectations of +1.0 to 10.0. Bearish factors included (1) disappointing earnings results from Google, IBM, and UnitedHealth Group, and (2) the ongoing crisis in Ukraine where there was no sign of the de-escalation that Russia agreed to last Thursday. Closes: S&P 500 +0.14%, Dow Jones -0.10%, Nasdaq +0.04%.

• Interest Rates -- Jun 10-year T-note futures prices on Thursday tumbled to a 1-1/2 week low and closed lower as stronger-than-expect-ed U.S. economic data on weekly initial unemployment claims and the Apr Philadelphia Fed manufacturing index bolstered speculation the Fed will continue to taper QE3 and may be closer to raising interest rates. Closes: TYM4 -20.00, FVM4 -11.00.

• Forex -- The dollar index on Thursday closed little changed. The dollar found support on stronger-than-expected U.S. economic data (weekly initial unemployment claims and Apr Philadelphia Fed manufacturing index), which supported the outlook for the Fed to continue to taper QE3. Strength in stocks, however, limited the upside for the dollar on reduced safe-haven demand. Closes: Dollar index +0.074 (+0.09%), EUR/USD unch, USD/JPY +0.011 (+0.01%).

• Metals -- Metals prices on Thursday settled mixed: GCM4 -9.6 (-0.74%), SIK4 -0.038 (-0.19%), HGK4 +0.0195 (+0.64%). Precious metals retreated as stronger-than-expected U.S. economic data on week-ly jobless claims and the Apr Philadelphia Fed manufacturing index bolstered the outlook for the Fed to continue to taper QE3. Copper prices gained as stronger-than-expected U.S. economic data improved the demand outlook for industrial metals.

• Energy -- May crude and gasoline prices on Thursday closed higher with May gasoline at a 7-1/2 month high. Bullish factors included (1) better-than-expected U.S. economic data on weekly jobless claims and the Apr Philadelphia Fed manufacturing index, which signals strength in the U.S. economy and energy demand, and (2) the ongoing Ukraine crisis and concern any further escalation of hostilities could lead to a disruption of energy supplies throughout Europe. Closes: CLK4 +0.54 (+0.52%). RBK4 +0.0165 (+0.54%).

Key News from Thursday, April 17

RJO MRT GLOBAL PREVIEWS & PERSPECTIVES

4

WWW.RJOMRT.COM LATEST POSTS

(BO) CFTC Commitments of Traders Recap for Data as of 04/15/14Technicals, FundamentalsApril 19, 2014; 10:14amThis post contains a summary of the latest CFTC Disaggregated Commitments of Traders data. As always, a historical look at this data can be found on the RJO MRT website at http://www.rjomrt.com/content/cftc.php ...more

(NG) Nat Gas Resumes Rebound, Defines New S-T Risk -by Dave TothTechnicalsApril 17, 2014; 12:10pmIn Tue’s Technical Blog we conceded that while that day’s failure below 4.522 confirmed a bearish divergence in momentum, that mo failure was of an insufficient scale to suggest anything but an interim corrective dip. Today’s smart recovery above ...more

(W) Wheat Rebound Defines New $6.91 S-T Key -by Dave TothTechnicalsApril 17, 2014; 11:15amThe hourly chart of the Jul contract below shows not only the past week’s smart recovery above prior 6.93-area resistance, but also yesterday’s relapse attempt that held at that former resistance-turned-support level of 6.91. Since this recent rebound failed to break 20-Mar’s key 7.25 high, the prospect that ...more

(C) S-T Corn Failure Early Sign of Trouble, Opportunity for Producers to Hedge -by Dave TothTechnicalsApril 17, 2014; 10:55amIn Tue’s Technical Blog we identified 10-Apr’s 5.00 low in the now-prompt Jul contract as our new short-term risk parameter this market needed to sustain gains above to avoid a momentum failure and maintain a broader bullish count. As a direct result of this morning’s break below 5.00, the hourly chart below shows that the market has ...more

(NG) EIA Weekly Nat Gas Storage RecapFundamentalsApril 17, 2014; 9:50am-Nat gas stocks rise, but less than expected...more

(AC) Ethanol Reaffirms Reversal, Defines New $2.429 Risk Parameter -by Dave TothTechnicalsApril 17, 2014; 9:20amIn 01-Apr’s Technical Blog we discussed the sustainability of Mar’s meteoric run at Jul’11’s 3.07 high and identified 27-Mar’s 2.518 corrective low as the risk ...more

(C) CBOT Grains Morning Comments -by Randy MittelstaedtFundamentalsApril 17, 2014; 8:20am-Talk of large Chinese soybean defaults continues-Wheat/corn sales solid, soybeans net positive again-USDA reports corn sold to S. Korea-S. Plains remain dry/corn belt to warm-EU crop estimate updates...more

(C) USDA Weekly Grain Export Sales Recap -by Randy MittelstaedtFundamentalsApril 17, 2014; 8:05am-Old crop soybean sales miniscule, but net positive-Old crop corn sales low end of expectations but larger than “needed”-Wheat sales solid, old crop above expectations-Soybean meal sales weaker than expected/”needed”...more

(CT) Toggle July Cotton Directional Bias Around $0.9348 -by Dave TothTechnicalsApril 17, 2014; 7:20amTo this point the sell-off attempt from 26-Mar’s 96.76 high in the now-prompt Jul contract has unfolded ...more

(SB) Sugar, Cocoa Stuck in Consolidation Ranges -by Dave TothTechnicalsApril 17, 2014; 6:45amJUL SUGARFollowing 14-Mar’s bearish divergence in momentum that defined 06-Mar’s 18.47 high as the prospective end to the Jan-Mar rally and exposed a larger-degree correction lower, the 240-min chart of the now-prompt Jul contract shows that this correction has ...more

Note: Subscribers may click on the “more” links above to retrieve the comment.Non-subscribers may sign up for a free trial at www.rjomrt.com/content/trial.subscription.php

RJO MRT GLOBAL PREVIEWS & PERSPECTIVES

5

(KC) $1.8105 Break Could Unlock Resumed Coffee Bull -by Dave TothTechnicals, Trade StrategiesApril 4, 2014; 8:45amOn the heels of mid-Mar’s sharp setback, it would be premature to ignore the past couple weeks’ mere lateral price action as corrective/consolidative ahead of resumed losses below 24-Mar’s 166.00 low. By the same token and against the longer-term bullish backdrop, a recovery above ...more

(ES) Bear & Bull S&P Option Strategies to Engage Key Nonfarm Payroll Report -by Dave TothTechnicals, Trade StrategiesApril 3, 2014; 9:20amIn yesterday’s Technical Blog we extolled the virtues of a still-constructive technical condition. With yesterday’s recovery above 21-Mar’s 1877 high, the market has rendered the Mar sell-off attempt a 3-wave and thus corrective affair consistent with the secular advance calling for a ...more

(HG) S-T Copper Failure Stems Recovery, May Re-Expose L-T Bear -by Dave TothTechnicals, Trade StrategiesApril 3, 2014; 6:35amOvernight’s failure below Tue’s 3.0170 minor corrective low confirms a bearish divergence in short-term momentum that defines yesterday’s 3.0740 high as one of developing importance and possibly the end of what we suspect is a bear market correction. As a result of this momentum failure and ...more

(CC) Cocoa Mo Failure, Waves, Frothy Sentiment Warn of Major Peak/Reversal Threat -by Dave TothTechnicals, Trade StrategiesApril 2, 2014; 11:00amToday’s clear break below 25-Mar’s initial counter-trend low of 2921 confirms a bearish divergence in momentum that we’ll discuss in more detail below. The important by-product of this RESUMED weakness is the market’s definition of TWO highs and risk parameters at ...more

(S) Bearish Soybean Hedge, Spec Option Strategies to Engage Grain Stocks Report -by Dave TothTechnicals, Trade StrategiesMarch 27, 2014; 10:10amThis morning’s Technical Blog describes the current constructive outlook on both old and new crop soybeans. For producers looking to take advantage of current lofty prices to hedge against a reversal lower and traders looking for a cautious way to speculate on a bearish Grain Stocks Report, the two option strategies below are advised to be considered. ...more

WWW.RJOMRT.COM RECENT TRADING RECOMMENDATIONS

Subscribers: Click on “more” links above to view the entire comment and please check the website for the latest trades.Non-subscribers may sign up for a free trial at www.rjomrt.com/content/trial.subscription.php

RJO MRT GLOBAL PREVIEWS & PERSPECTIVES

6

Global Financial & Commodity Event Calendar

Global Calendar - Monday 4/21/14Today’s News (ET release time) Mon US 0830 ET Mar Chicago Fed national activity index expected +0.06 to 0.20, Feb 0.14. 1000 ET Mar leading indicators expected +0.7%, Feb +0.5%. 1100 ET USDA weekly grain export inspections. 1600 ET USDA weekly crop progress. EUR n/a European markets closed for Easter Monday. UK n/a UK markets closed for Easter Monday.

Future News:Tue US 0900 ET Feb FHFA house price index expected +0.5% m/m, Jan +0.5% m/m. 1000 ET Apr Richmond Fed manufacturing index expected +7 to 0, Mar -1 to -7. 1000 ET Mar existing home sales expected -1.1% to 4.55 million, Feb -0.4% to 4.60 million. 1145 ET Former Fed Chairman Ben Bernanke speaks at the Economic Club of Canada on “8 Years of Crisis Man-

agement at the Federal Reserve and the Way Forward.” 1300 ET Treasury auctions $32 billion 2-year T-notes. 1500 ET USDA Mar Cold Storage. JPN 0100 ET Revised Japan Fed leading index CI, previous 108.5. Revised Feb coincident index CI, previous 113.4. EUR 0500 ET Eurozone Feb construction output, Jan +1.5% m/m and +8.8% y/y. 1000 ET Eurozone Apr consumer confidence expected unch at -9.3, Mar -9.3. CHI 2145 ET China HSBC Apr manufacturing PMI expected +0.3 to 48.3, Mar -0.5 to 48.0.Wed US 0700 ET Weekly MBA mortgage applications, previous +4.3% with purchase sub-index +1.3% and refi sub-index

+6.9%. 0945 ET Markit Apr manufacturing PMI expected +0.5 to 56.0, Mar 55.5. 1000 ET Mar new home sales expected +2.3% to 450,000, Feb -3.3% to 440,000. 1030 ET EIA Weekly Petroleum Status Report. 1300 ET Treasury auctions $35 billion 5-year T-notes. GER 0330 ET German Apr Markit/BME manufacturing PMI expected +0.1 to 53.8, Mar 53.7. Apr composite PMI

expected 0.3 to 54.0, Mar 54.3. EUR 0400 ET Eurozone Apr Markit manufacturing PMI expected unch at 53.0, Mar 53.0. Apr composite PMI ex-

pected -0.1 to 53.0, Mar 53.1. UK 0430 ET Minutes of the Apr 9-10 BOE policy meeting. 0430 ET UK Mar public sector net borrowing expected 8.5 billion pounds, Feb 7.5 billion pounds. 0600 ET UK Apr CBI trends total orders expected +1 to 7, Mar 6. Apr CBI trends selling prices expected -2 to

10, Mar 12. Apr CBI business optimism expected +4 to 25, Mar 21. JPN 1950 ET Japan Mar corporate service price index expected +0.7% y/y, Feb +0.7% y/y.Thu US 0830 ET Weekly initial unemployment claims expected +11,000 to 315,000, previous +2,000 to 304,000. Weekly

continuing claims expected +1,000 to 2.740 million, previous -11,000 to 2.739 million. 0830 ET Mar durable goods orders expected +2.0% and +0.6% ex transportation, Feb +2.2% and +0.1% ex trans-

portation. March non-defense capital goods orders ex-aircraft expected +1.0%, Feb -1.4%. 0830 ET USDA weekly Export Sales. 1100 ET Treasury announces amount of 2-year floating-rate notes to be auctioned Apr 29 (previous $13 billion). 1300 ET Treasury auctions $29 billion 7-year T-notes. GER 0400 ET German Apr IFO business climate expected -0.3 to 110.4 Mar 110.7. Apr IFO current assessment ex-

pected +0.4 to 115.6, Mar 115.2. Apr IFO expectations expected -0.6 to 105.8, Mar 106.4. EUR 0500 ET ECB President Mario Draghi speaks at a conference in Amsterdam. UK 0600 ET UK Apr CBI reported sales expected +4 to 17, Mar 13. JPN 1930 ET Japan Mar national CPI expected +1.6% y/y, Feb +1.5% y/y. Mar national CPI ex-fresh food expected

+1.4% y/y, Feb +1.3% y/y. Mar national CPI ex food & energy expected +0.7% y/y, Feb +0.8% y/y. 1930 ET Japan Apr Tokyo CPI expected +3.1% y/y, Mar +1.3% y/y. Apr Tokyo CPI ex-fresh food expected

RJO MRT GLOBAL PREVIEWS & PERSPECTIVES

7

Global Financial & Commodity Event Calendar (continued)

+2.8% y/y, Mar +1.0% y/y. Apr Tokyo CPI ex food & energy expected +2.1% y/y, Mar +0.4% y/y. Fri US 0955 ET Final-April University of Michigan U.S. consumer confidence expected +0.4 to 83.0, early-April +2.6 to

82.6. 1500 ET USDA Mar Cattle on Feed. JPN 0030 ET Japan Feb all-industry activity index expected -0.7% m/m, Jan +1.0% m/m. GER 0200 ET German Mar import price index expected -0.1% m/m and -2.8% y/y, Feb -0.1% m/m and -2.7% y/y. UK 0430 ET UK Mar retail sales ex autos expected -0.5% m/m and +4.5% y/y, Feb +1.8% m/m and +4.2% y/y. Mar

retail sales including autos expected -0.4% m/m and +3.8% y/y, Feb +1.7% m/m and +3.7% y/y.Sun UK 1901 ET UK Apr Hometrack housing prices, Mar +0.6% m/m and +5.7% y/y. JPN 1950 ET Japan Mar retail sales, Feb +0.3% m/m and +3.6% y/y.

Week of Apr 28-May 2Mon US 1000 ET Mar pending home sales expected +0.6% m/m, Feb -0.8% m/m and -10.2% y/y. 1100 ET USDA weekly grain export inspections. 1600 ET USDA weekly crop progress. UK 0430 ET UK Apr Lloyds business barometer, Mar 44.Tue US 0900 ET Feb S&P/CaseShiller composite-20 home price index, Jan +0.85% m/m and +13.24% y/y. 1000 ET Apr consumer confidence (Conference Board) expected +1.2 to 83.5, Mar 82.3. 1300 ET Treasury auctions 2-year floating-rate notes. n/a FOMC begins 2-day policy meeting. GER 0200 ET German May GfK consumer confidence, Apr 8.5. 0800 ET German Apr CPI (EU harmonized), Mar +0.3% m/m and +0.0% y/y. EUR 0400 ET Eurozone Mar M3 money supply, Feb +1.3% y/y and +1.2% 3-mo avg. 0500 ET Eurozone Apr economic confidence, Mar 102.4. Apr business climate indicator, Mar 0.39. 0500 ET Revised Eurozone Apr consumer confidence. UK 0430 ET UK Q1 GDP, Q4 +0.7% q/q and +2.7% y/y. 0430 ET UK Feb index of services, Jan +0.4% m/m and +0.9% 3-mo/3-mo. 1905 ET UK Apr GfK consumer confidence, Mar -5. JPN 1915 ET Japan Apr Markit/JMMA manufacturing PMI, Mar 53.9. 1950 ET Japan Mar industrial production, Feb -2.3% m/m and +7.0% y/y. 2130 ET Japan Mar labor cash earnings, Feb unch y/y.Wed US 0700 ET Weekly MBA mortgage applications. 0815 ET Apr ADP employment change, Mar +191,000. 0830 ET Q1 employment cost index expected +0.5%, Q4 +0.5%. 0830 ET Q1 GDP expected +1.0% annualized q/q, Q4 +2.6% annualized q/q. Q1 personal consumption, Q4

+3.3%. Q1 GDP price index, Q4 +1.6%, Q1 core PCE deflator, Q4 +1.3% q/q. 0900 ET Treasury announces amounts of 3-year T-notes (previous $30 billion), 10-year T-notes (previous $21

billion) and 30-year T-bonds (previous $13 billion) to be auctioned in the Treasury’s quarterly refunding May 6-8.

0945 ET Apr Chicago PMI expected +0.5 to 56.4, Mar 55.9. 1030 ET EIA Weekly Petroleum Status Report. 1400 ET FOMC announces interest rate decision and pace of asset purchases. JPN 0000 ET Japan Mar vehicle production, Feb +7.1% y/y. 0100 ET Japan Mar construction orders, Feb +12.3% y/y. GER 0355 ET German Apr unemployment change, Mar -12,000. Apr unemployment rate, Mar 6.7%. EUR 0500 ET Eurozone Apr CPI estimate, Mar +0.5% y/y and Mar core CPI +0.7% y/y. CHI 2130 ET China Apr manufacturing PMI, Mar 50.3. Thu US 0730 ET Apr Challenger job cuts, Mar -30.2% y/y. 0830 ET Fed Chair Janet Yellen speaks to the Independent Community Bankers of America’s annual Washington

Policy Summit.

RJO MRT GLOBAL PREVIEWS & PERSPECTIVES

8

About RJO Market Research & Trading (MRT) and R.J. O’Brien

About RJO Market Research & Trading

RJO MRT is the research arm of R.J. O’Brien & Com-pany, the largest independent futures brokerage in the United States. A privately owned futures commission merchant, RJO is also one of the oldest futures broker-age firms, dating back to 1914.

RJO is a full clearing member of: the Chicago Mer-cantile Exchange Group (founding member of CME); Intercontinental Exchange (ICE); NYSE Liffe; and the Chicago Climate Exchange.

RJO services a global network of more than 330 intro-ducing brokers and some of the world’s largest financial, industrial and agricultural institutions.

Contact Information:

RJO Market Research & Trading222 South Riverside Plaza, Suite 900Chicago, Illinois 60606

Website InquiriesPhone: [email protected]

Customer Relationship CenterPhone: [email protected]

Copyright & Disclaimer

Copyright, 2013, All rights reserved. RJO Market Research & Trading. The information contained in this article is believed to be drawn from reliable sources but cannot be guaranteed. Neither the information presented, nor any opinions expressed, constitute a solicitation of the purchase or sale of any commodity. Those individuals acting on this information are responsible for their own actions. Any opinions expressed herein are subject to change without notice. Any reproduction or other use of this information and thoughts expressed herein without the written permission of the author is strictly prohibited. Commodity trading may not be suitable for all recipients of this information. The risk of loss in trading commodity futures and options can be substantial.

HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE SHOWN. IN FACT , THERE ARE FRE-QUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL PERFORMANCE RESULTS AND THE AC-TUAL RESULTS SUBSEQUENTLY ACHIEVED BY ANY PARTICULAR TRADING PROGRAM. ONE OF THE LIMITATIONS OF HYPOTHETICAL PERFORMANCES RESULTS IS THAT THEY ARE GENERALLY PRE-PARED WITH THE BENEFIT OF HINDSIGHT. IN ADDITION, HYPOTHETICAL TRADING DOES NOT IN-VOLVE FINANCIAL RISK AND NO HYPOTHETICAL TRADING RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING. FOR EXAMPLE, THE ABILITY TO WITH-STAND LOSSES OR TO ADHERE TO A PARTICULAR TRADING PROGRAM IN SPITE OF TRADING LOSSES ARE MATERIAL POINTS WHICH CAN ALSO ADVERSELY AFFECT ACTUAL TRADING RESULTS. THERE ARE NUMEROUS OTHER FACTORS RELATED TO THE MARKETS IN GENERAL OR TO THE IMPLEMEN-TATION OF ANY SPECIFIC TRADING PROGRAM WHICH CANNOT BE FULLY ACCOUNTED FOR IN THE PREPARATION OF HYPOTHETICAL PERFORMANCE RESULTS AND ALL OF WHICH CAN ADVERSELY AFFECT ACTUAL TRADING RESULTS.