Risk Report

6

r r i i s s k k r r e e p p o o r r t t w w i i t t h h H H e e n n r r i i o o t t t t G G r r o o u u p p , , I I n n c c . . Workplace and Risk Management topics aimed at business owners, managers and other organizational leaders. A A P P R R I I L L 2 2 0 0 1 1 2 2 Business Interruption What is it & why is it necessary? Three components & their important facts Benchmarks Henriott News & Updates GLC & Accident Fund Partnership “C’Mon Man!” THIS JUST IN…. An introduction to Business Interruption Insurance and why it’s necessary for your business “Human beings, who are almost unique in having the ability to learn from the experience of others, are also remarkable for their apparent disinclination to do so.” ~ Douglas Adams basketman

-

Upload

henriott-group-inc -

Category

Documents

-

view

216 -

download

0

description

April 2012

Transcript of Risk Report

rriisskk rreeppoorrtt wwiitthh HHeennrriiootttt GGrroouupp,, IInncc..

Workplace and Risk Management topics aimed at business

owners, managers and other organizational leaders.

AAPP

RRII LL

2200

1122

BBuussiinneessss

IInntteerrrruuppttiioonn

What is it & why is it necessary?

Three components & their

important facts

Benchmarks

HHeennrriiootttt

NNeewwss && UUppddaatteess

GLC & Accident Fund

Partnership

“C’Mon Man!”

TTHHIISS JJUUSSTT IINN……..

An introduction to Business Interruption Insurance and why it’s necessary for your business

“Human beings, who are almost unique in having the ability to learn from the experience of others, are also remarkable for their apparent disinclination to do so.”

~ Douglas Adams

bas

ketm

an

his stat, brought to you by the Insurance Information Institute, is a

bit startling if you ask me. That’s why we’re going to shift our focus in this and possibly the next edition of the Risk Report to one line of insurance that is critical in helping businesses survive following a significant loss – Business Interruption. I have to admit, in my prior life as a Corporate Controller of a large manufacturer, I used to have responsibility for the

insurance program. I’m also a recovering CPA, so theoretically should be good with numbers! Despite all that, I always dreaded the annual email, phone call or worse yet, the in my office request from our very persistent and proactive broker (first person to guess who that might have been gets a free cup of coffee) suggesting it was time to discuss Business Interruption and complete a Business Income worksheet. The conversation sort of when like this….”C’Mon man, really? Do we have to? Can’t you just

fill that out for us?” The same reply came year after year…. “Yes”,” Yes” and “Over my Dead Body”. Now that I’ve been on the other side of the desk for the past 10+ years and our firm has been working with clients to help them identify and manage their business risks, I’ve seen first-hand the importance of this coverage. However, for one reason or another, it’s rarely given the attention and priority it deserves. So, our goal in this Risk Report is to describe what this insurance is and why it’s necessary, and to identify the three major components of Business Interruption Insurance and certain assumptions or factors to consider for each.

T

TTHHIISS JJUUSSTT IINN…….. OVER 25% OF ALL BUSINESSES THAT

CLOSE DOWN FOLLOWING A DISASTER

NEVER OPEN AGAIN!

WWhhaatt iiss BBuussiinneessss IInntteerrrruuppttiioonn IInnssuurraannccee

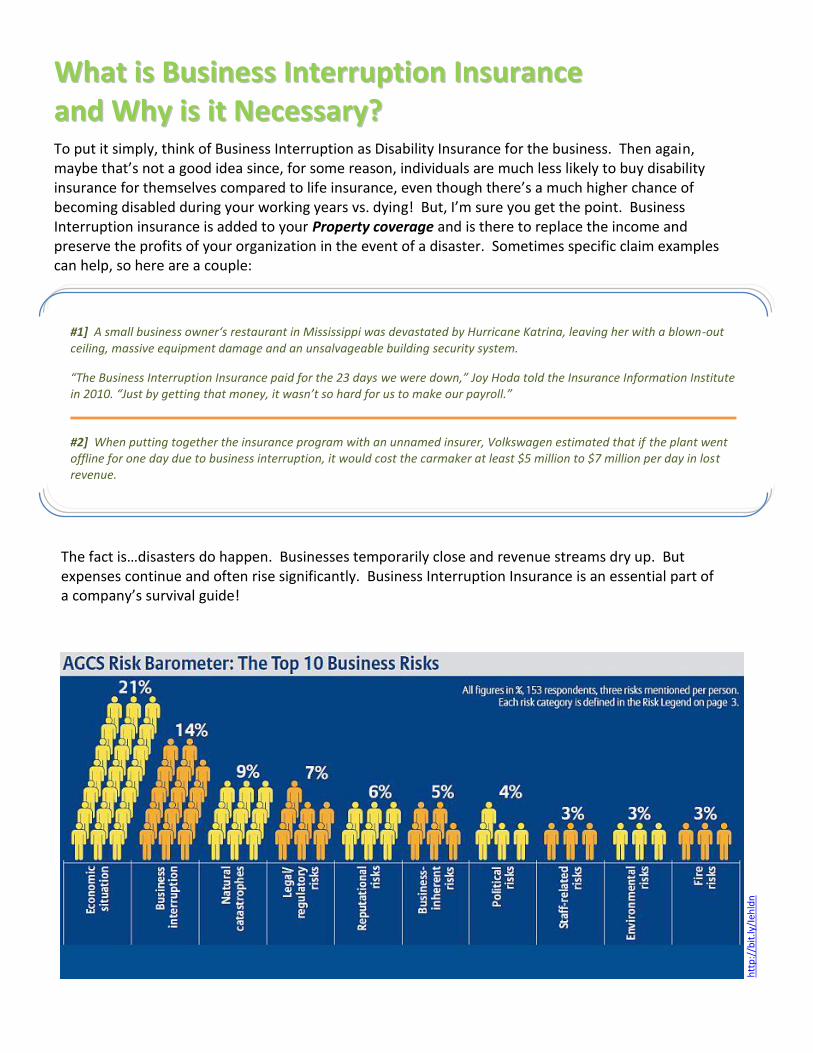

aanndd WWhhyy iiss iitt NNeecceessssaarryy?? To put it simply, think of Business Interruption as Disability Insurance for the business. Then again, maybe that’s not a good idea since, for some reason, individuals are much less likely to buy disability insurance for themselves compared to life insurance, even though there’s a much higher chance of becoming disabled during your working years vs. dying! But, I’m sure you get the point. Business Interruption insurance is added to your Property coverage and is there to replace the income and preserve the profits of your organization in the event of a disaster. Sometimes specific claim examples can help, so here are a couple:

#1] A small business owner‘s restaurant in Mississippi was devastated by Hurricane Katrina, leaving her with a blown-out ceiling, massive equipment damage and an unsalvageable building security system.

“The Business Interruption Insurance paid for the 23 days we were down,” Joy Hoda told the Insurance Information Institute in 2010. “Just by getting that money, it wasn’t so hard for us to make our payroll.”

#2] When putting together the insurance program with an unnamed insurer, Volkswagen estimated that if the plant went offline for one day due to business interruption, it would cost the carmaker at least $5 million to $7 million per day in lost revenue.

The fact is…disasters do happen. Businesses temporarily close and revenue streams dry up. But expenses continue and often rise significantly. Business Interruption Insurance is an essential part of a company’s survival guide!

htt

p:/

/bit

.ly/I

ehld

n

TThhee TTHHRREEEE CCoommppoonneennttss ooff BBuussiinneessss IInntteerrrruuppttiioonn

aanndd IImmppoorrttaanntt FFaaccttoorrss ffoorr EEaacchh

BUSINESS INCOME. This is designed to replace income your business would have incurred

had no loss occurred. Business income (“BI”) is generally defined as the net profit or loss before taxes, plus continuing normal operating expenses, including ordinary payroll (payroll for employees other than officers, executives, department managers or employees under contract). Coverage is generally limited to the loss of income sustained until the property is restored, and/or a specific timeframe following the loss.

Specific Items to Consider: * It’s important to review ordinary payroll annually and determine whether, and for

how long, you want to be able to retain your direct labor associates. In the past, many manufacturers for example, chose not to insure their direct labor costs—unskilled labor was easily replaced. That may or may not be true for your organization at the time of loss.

* Review your projected timeframe for resuming business. After a major loss, getting

up and running takes much longer than you may anticipate and can cost much

more, too.

* You may be back in business but your customers are still going to your competitor. An Extended Period of Indemnity extension may be necessary to give you more time to restore your business to pre-loss level.

EXTRA EXPENSE. This is designed to pay for necessary expenses incurred during the

period of restoration of the property. Extra expenses include those necessary to continue operating the business at its original location or at a temporary replacement location until the original location is repaired.

Specific Items to Consider: Not all businesses would lose customers after a major loss. For example, a law firm would retain its clients, and there would still be a flow of revenue; however, the costs involved in renting new office space, moving, and hooking up new phones and computers is considerable. Transitions are more expensive than you think. Increased rent, employee overtime, and moving costs are examples of extra expenses that service organizations should consider insuring.

CONTINGENT BUSINESS INTERRUPTION. This is an extension of coverage designed to cover

loss of income your business incurs due to a property loss at a key supplier or customer location. For example, if a key supplier experiences a fire at its plant and is unable to deliver parts or goods necessary for the continuation of your business, you may have a claim for a contingent business interruption loss.

Specific Items to Consider: Contingent Business Interruption is the most overlooked area of exposure to loss. Your interdependency on your supplier (under contract or not) or one large customer could put your business in jeopardy when that party suffers a major loss. Contingent Business Interruption coverage can fill this gap.

Determining the appropriate amount of Business Income coverage for an organization is unique to its individual needs and exposures and is the reason why, for most companies, a Business Income Worksheet will need to be completed and updated every year. However, as a guide for organizations to use, Travelers Indemnity Company developed a list of benchmarks by industry segment showing Business Income limits (assuming 100% ordinary payroll and benefits are included) as a percent of total revenues. I’ve included some of those industry benchmarks below and again – these are simply a guide and no replacement for a completed BI worksheet.

Hopefully the information above gives you a better idea of what the purpose of Business Interruption Insurance is and its overall importance to your insurance and risk management program. Next month we’ll discuss other elements of this coverage, including the BI Worksheet itself, how the deductible is typically applied, how claims are adjusted, options for how limits are paid in the event of a loss, etc.

Here’s another opportunity for a free cup of coffee…first person to respond back with why this coverage is added to your Property Form wins (can’t be the same person who answers the first Coffee Question)! Hint…what has to occur first for a BI claim to be filed?

BBuussiinneessss IInnccoommee

BBeenncchhmmaarrkkss

Manufacturing Non-Manufacturing Advanced Technology 58% Architects & Engineers 82%

Electrical Equipment 61% Auto Dealers 20%

Machinery 49% Building Materials 44%

Metals 47% Building Services Contractors 35%

Motor Vehicle & Parts 37% Hospitals & Healthcare 85%

Plastic & Rubber Goods 40% Hotels 50%

Printers 56% Retail Goods 42%

Wineries & Distilleries 59% Restaurants 60%

All Other Manufacturing 40% - 55% All Other Non-Manufacturing 30% - 35%

Henriott Group’s Milestone Risk Management program is aimed at helping your

company lower it’s Total Cost of Risk. Talk to your Henriott professional for more

information about this proprietary process.

CClliieenntt FFooccuusseedd.. RReessuullttss DDrriivveenn..

Check out our website blog series for real-life claims or lawsuits that we hear about in our work and make us sit back and say…C’Mon Man…Really?! Did you know that we also issue monthly reports for Employee Benefits and Personal Insurance? For a preview of these, click the following links!

Live Well, Work Well

Home Matters

If you would like to subscribe to either of these, simple send an email to [email protected] and specify which you are interested in receiving!

TThhee LLaatteesstt ……

HHeennrriiootttt NNeewwss && UUppddaatteess We know your time is important, so we strive to make our processes as convenient for you as possible! Since most of our client’s day-to-day needs with us will be routine change requests, we’ve found the “once and done” approach to be the most efficient method and one that has worked well for our clients over the years. To facilitate this, we’ve created a secure client portal on our website with online access to policies, change forms & claims instructions. Interested? If you are a client, please contact your account manager for additional details!

See you next month!

Bro

ugh

t to

yo

u b

y et

on