Risk management framework for construction projects in developing countries

17

This article was downloaded by: [University of Connecticut] On: 18 August 2013, At: 05:48 Publisher: Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK Construction Management and Economics Publication details, including instructions for authors and subscription information: http://www.tandfonline.com/loi/rcme20 Risk management framework for construction projects in developing countries Shou Qing Wang a b , Mohammed Fadhil Dulaimi c d & Muhammad Yousuf Aguria e a Department of Construction Management, Tsinghua University, Beijing 100084, China b Dept of Building, National University of Singapore c Faculty of the Built Environment, University of the West of England, Bristol, Coldharbour Lane, Bristol, BS16 1QY, UK d Dept of Building, National University of Singapore e Dept of Building, National University of Singapore Published online: 13 May 2010. To cite this article: Shou Qing Wang , Mohammed Fadhil Dulaimi & Muhammad Yousuf Aguria (2004) Risk management framework for construction projects in developing countries, Construction Management and Economics, 22:3, 237-252, DOI: 10.1080/0144619032000124689 To link to this article: http://dx.doi.org/10.1080/0144619032000124689 PLEASE SCROLL DOWN FOR ARTICLE Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) contained in the publications on our platform. However, Taylor & Francis, our agents, and our licensors make no representations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose of the Content. Any opinions and views expressed in this publication are the opinions and views of the authors, and are not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be relied upon and should be independently verified with primary sources of information. Taylor and Francis shall not be liable for any losses, actions, claims, proceedings, demands, costs, expenses, damages, and other liabilities whatsoever or howsoever caused arising directly or indirectly in connection with, in relation to or arising out of the use of the Content. This article may be used for research, teaching, and private study purposes. Any substantial or systematic reproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in any form to anyone is expressly forbidden. Terms & Conditions of access and use can be found at http:// www.tandfonline.com/page/terms-and-conditions

-

Upload

muhammad-yousuf -

Category

Documents

-

view

219 -

download

3

Transcript of Risk management framework for construction projects in developing countries

This article was downloaded by: [University of Connecticut]On: 18 August 2013, At: 05:48Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House,37-41 Mortimer Street, London W1T 3JH, UK

Construction Management and EconomicsPublication details, including instructions for authors and subscription information:http://www.tandfonline.com/loi/rcme20

Risk management framework for construction projectsin developing countriesShou Qing Wang a b , Mohammed Fadhil Dulaimi c d & Muhammad Yousuf Aguria ea Department of Construction Management, Tsinghua University, Beijing 100084, Chinab Dept of Building, National University of Singaporec Faculty of the Built Environment, University of the West of England, Bristol, ColdharbourLane, Bristol, BS16 1QY, UKd Dept of Building, National University of Singaporee Dept of Building, National University of SingaporePublished online: 13 May 2010.

To cite this article: Shou Qing Wang , Mohammed Fadhil Dulaimi & Muhammad Yousuf Aguria (2004) Risk managementframework for construction projects in developing countries, Construction Management and Economics, 22:3, 237-252, DOI:10.1080/0144619032000124689

To link to this article: http://dx.doi.org/10.1080/0144619032000124689

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) containedin the publications on our platform. However, Taylor & Francis, our agents, and our licensors make norepresentations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose of theContent. Any opinions and views expressed in this publication are the opinions and views of the authors, andare not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be relied upon andshould be independently verified with primary sources of information. Taylor and Francis shall not be liable forany losses, actions, claims, proceedings, demands, costs, expenses, damages, and other liabilities whatsoeveror howsoever caused arising directly or indirectly in connection with, in relation to or arising out of the use ofthe Content.

This article may be used for research, teaching, and private study purposes. Any substantial or systematicreproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in anyform to anyone is expressly forbidden. Terms & Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

*Author for correspondence. E-mail: [email protected]

Introduction

Prevalent 1997 recession which stagnated Singapore’seconomy and created a saturated construction industry hascompelled Singapore’s investors, developers and contractorsto explore new vistas globally. It is clear that competingin a small domestic market offers very little opportunitiesfor the industry to grow. The Construction 21 Report(C21 Steering Committee, 1999) has therefore firmly putthe issue of ‘building the external wing of the constructionindustry’ on the agenda to promote and encourageSingaporean construction firms to venture overseas.However, the same report recognizes that to perform wellin the international construction market especially in

Risk management framework for construction projectsin developing countries

SHOU QING WANG*1, MOHAMMED FADHIL DULAIMI2 and MUHAMMADYOUSUF AGURIA3

1Department of Construction Management, Tsinghua University, Beijing 100084, China; formerly, Dept ofBuilding, National University of Singapore2Faculty of the Built Environment, University of the West of England, Bristol, Coldharbour Lane, Bristol, BS161QY, UK; formerly, Dept of Building, National University of Singapore3Dept of Building, National University of Singapore

It is important to manage the multifaceted risks associated with international construction projects, in particularin developing countries, not only to secure work but also to make profit. This research seeks to identify andevaluate these risks and their effective mitigation measures and to develop a risk management frameworkwhich the international investors/ developers/ contractors can adopt when contracting construction workin developing countries. A survey was conducted and twenty-eight critical risks were identified, categorizedinto three (country, market and project) hierarchical levels and their criticality evaluated and ranked. Foreach of the identified risks, practical mitigation measures have also been proposed and evaluated. Almost allmitigation measures have been perceived by the survey respondents as effective. A risk model, named AlienEyes’ Risk Model, which shows the hierarchical levels of the risks and the influence relationship among therisks, is also proposed. Based on the findings, a qualitative risk mitigation framework was finally proposedwhich will benefit the risk management of construction project in developing countries.

Keywords: Risk management, risk identification, risk mitigation, risk model, international constructionproject, developing countries

developing countries will not be easy as the risk of workingin a foreign environment is multifaceted.

Nonetheless, demands for infrastructure and services indeveloping countries have created much greater opportu-nities compared to the stagnant domestic constructionindustry and motivated Singaporean firms to ventureoverseas. China is one of such developing countries in whichthe opportunity for Singaporean firms is likely to be greatespecially after China’s admission to WTO in 2001 andChina’s success in bidding for the 2008 Olympic Games.

The aim of this research is to help international con-struction firms, especially Singaporean construction firms,identify the risks foreign construction firms may face inoperation in developing countries and to develop a riskmanagement framework to aid their effort in mitigatingsuch risks. The research objectives are:

Construction Management and Economics (March 2004) 22, 237–252

Construction Management and EconomicsISSN 0144-6193 print/ISSN 1466-433X online © 2004 Taylor & Francis Ltd

http://www.tandf.co.uk/journalsDOI: 10.1080/0144619032000124689

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Wang et al.238

• to develop a model for identifying, categorizing andrepresenting the risks associated with internationalconstruction projects;

• to validate the model through an international surveyto identify and evaluate the critical risks associatedwith construction projects in developing countrieswith emphasis on China;

• to identify and evaluate the practical measures formitigating these risks;

• to formulate a risk management framework thatcan be adopted by international construction firms,including Singaporean firms, seeking work indeveloping countries.

Concepts of risk and risk management

Risk is a multi-facet concept. In the context of construc-tion industry, it could be the likelihood of the occurrenceof a definite event/factor or combination of events/factorswhich occur during the whole process of constructionto the detriment of the project (Faber, 1979), a lack ofpredictability about structure outcome or consequencesin a decision or planning situation (Hertz and Thomas,1983), the uncertainty associated with estimates ofoutcomes – there is a chance that results could be betterthan expected as well as worse than expected (Lifson andShaifer, 1982), etc. This research has adopted the moregeneral and broad definition of risk as presented by Faber(1979).

In addition to the different definitions of risk, there arevarious ways for categorizing risk for different purposestoo. For example, some categorize risks in constructionprojects broadly into external risks and internal riskswhile others classify risk in more detailed categories ofpolitical risk, financial risk, market risk, intellectualproperty risk, social risk, safety risk, etc (Songer et al.,1997).

The typology of the risks seems to depend mainly uponwhether the project is local (domestic) or international.The internal risks are relevant to all projects irrespectiveof whether they are local or international. Internationalprojects tend to be subjected to the external risk suchas unawareness of the social conditions, economic andpolitical scenarios, unknown and new procedural for-malities, regulatory framework and governing authority,etc. These risks gain predominance when the considera-tion is solely given to international projects alone(Flanagan and Norman, 1993).

Hastak and Shaked (2000) classified all risks specificto whole construction scenario into three broad levels,i.e. country, market and project levels. The research hasfound this classification useful in portraying the influenceof one risk on the others and in prioritizing the mitiga-tion measures for each of the risks. Country level risksare seen as a function of the political and macroeconomic

stability. They materialize when the authorities of thecountry expropriate property, introduce foreign currencyexchange or trade restrictions or change trade legislation,etc. Macroeconomic stability is partly linked to thestance of fiscal and monetary policy, and to a country’svulnerability to economic shocks. Construction marketlevel risks, for a foreign firm, include technologicaladvantage over local competitors, availability of con-struction resources, complexity of regulatory processes,and attitude of local and foreign governments towards theconstruction industry while project level risks are specificto construction sites and include logistic constraints,improper design, site safety, improper quality controland environmental protection, etc (Thobani, 1999).

Risk is inherent and difficult to deal with, and thisrequires a proper management framework both oftheoretical and practical meanings. Risk management isa formal and orderly process of systematically identify-ing, analysing, and responding to risks throughout thelife-cycle of a project to obtain the optimum degree ofrisk elimination, mitigation and/or control. Significantimprovement to construction project management per-formance may be achieved from adopting the process ofrisk management (Flanagan and Norman, 1993).

The types of exposure to risk that an organization isfaced with are wide-ranging and vary from one organiza-tion to another. These exposures could be the risk ofbusiness failure, the risk of project financial losses, theoccurrences of major construction accidents, default ofbusiness associates and dispute and organization risks. Itis desirable to understand and identify the risks as earlyas possible, so that suitable strategy can be implementedto retain particular risks or to transfer them to minimizeany likely negative aspect they may have.

A systematic approach to risk management in construc-tion industry consists of three main stages: a) risk identi-fication; b) risk analysis and evaluation; and c) riskresponse. The risk management process begins with theinitial identification of the relevant and potential risksassociated with the construction project. It is of consid-erable importance since the process of risk analysis andresponse management may only be performed on identi-fied potential risks. Risk analysis and evaluation is theintermediate process between risk identification andmanagement. It incorporates uncertainty in a quantitativeand qualitative manner to evaluate the potential impact ofrisk. The evaluation should generally concentrate on riskswith high probabilities, high financial consequences orcombinations thereof which yield a substantial financialimpact. Once the risks of a project have been identifiedand analysed, an appropriate method of treating risk mustbe adopted. Within a framework of risk management,contractors should decide how to handle or treat eachrisk and formulate suitable risk treatment strategies ormitigation measures. These mitigation measures are

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Risk management in developing countries 239

generally based on the nature and potential consequencesof the risk. The main objective is to remove as muchas possible the potential impact and to increase the levelof control of risk. The more control of one mitigationmeasure on one risk the more effective the measure is.The process of risk management does not aim to removecompletely all risks from a project. Its objective is todevelop an organized framework to assist decision makersto manage the risks, especially the critical ones, effectivelyand efficiently (Perry and Haynes, 1985).

Past research on risk management

There is extensive literature in the field of risk managementof construction projects. For example, Bajaj et al. (1997)identified, investigated and evaluated the process of riskidentification. They found that the most frequently usedmethod of risk identification is the top-down approachtechnique, where the project is analysed from an overallpoint of view. Baker et al. (1999) believed personal andcorporate experience, engineering judgement, and brain-storming to be effective ways for identifying new risksand for qualitative use. Ramcharran (1998) identifiedthe risks usually faced by the engineering/constructionservice providers in a foreign country, while Kalayjian(2000) identified further the risks that are specific tothe developing countries. Haarmeyer and Mody (1997)explained the critical risks by focusing on specific devel-oping countries such as Guinea and Mexico. Jaselskis andTalukhaba (1998) described the main characteristics ofdeveloping countries and identified the top informationrequirements in 15 key areas for architectural, engineering,and construction firms. Thobani (1999) discussed theproper risk allocation in developing countries arguing thatinvestors should bear the exchange and interest rate risks.Many researchers also draw lessons of risk managementfrom international construction projects in developingcountries (Raftery et al., 1998; Li et al., 1999; etc).

In the context of China, Silk and Black (2000) proposedseveral mitigation strategies for the risks in China andstrongly recommended the joint venture (JV) type ofvehicle. Luo (2001) concluded further that share controlis the most favorable method of JV management in China.Wang et al. (2000a, 2000b) identified and evaluated theunique and critical risks associated with the build-operate-transfer (BOT) projects in China. Cheng and Chung (2001)found that the monopoly in China power projects lendsitself to major corruption and proposed several mitigationmeasures.

Other researchers have examined the different approachesto risk management in some developing countries, forexample, the risk of differences between enterprise stakeholders in several projects (Yeo and Tiong, 2000), therisk management of a power project in India (Guptaand Sravat, 1998), the risks in a hydro power project in

Turkey (Ozdoganm and Birgonul, 2000) and the commonrisks in Kazakhstan (Munns et al., 2000).

Research method

To meet the research objectives four research tasks havebeen carried out mainly through literature review, inter-views and discussions as well as an international survey,as graphically presented in Figure 1.

As shown in Figure 1, the research began with a heavyliterature review to compile the list of risks of construc-tion project and the list of mitigation measures for eachof the risks identified as well as to examine existing riskmodels. Then the risks and their mitigation measuresidentified were filtered and a risk model and a risk man-agement framework proposed after discussion among theresearch team members together with some experiencedacademicians. To validate the proposed risk model andrisk management framework, it needs to understand wellthe criticality of the identified risks and the effectivenessof the mitigation measures. Therefore, an internationalquestionnaire survey was carried out. After analysing thesurvey results, the risk model and risk managementframework were improved and documented.

The questionnaire was designed based on the knowledgeobtained from literature review, interviews and discus-sions. Hastak and Shaked’s (2000) three-level (country,market and project) risk categorization has been adoptedfor this questionnaire. The questionnaire encompasses allmajor risks that are likely to be encountered in interna-tional construction projects especially those in developingcountries (Table 1) as well as all the practical mitigationmeasures for each of the risks identified (Table 2). Thequestionnaire was amended several times while conductingreview and discussion sessions with five local academicsand professionals and its final version is represented inTable 1 and Table 2 (Wang and Dulaimi, 2002).

As the evaluation of the criticality of risk is a complexsubject shrouded in uncertainty and vagueness, suchvague terms are unavoidable since project managers findit easier accessing risks in qualitative linguistic terms. Toimprove the preciseness and reliability of the survey, aseven-degree rating system for the criticality of risks andthe effectiveness of mitigation measures, as shown inTable 3, have been adopted.

The survey was carried out from September to December2001 targeting project sponsors, developers, investors andcontractors from all over the world who have experiencein the initiation, funding, planning and construction ofinternational construction projects in developing countries.In total 400 hardcopy questionnaires were sent out by postto selected companies which are filtered from variouslists, e.g. CNR of international investors, developers andcontractors, and softcopy was also sent by email to the

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Wang et al.240

CNBR (Co-operative Network for Building Researchers)members asking them to help disseminate the question-naire to suitable practitioners. However, the respondentrate was unexpectedly low and only 31 valid replies(7.75%) were received although an incentive that surveyparticipants will get the research report was stated inthe questionnaire. One of the reasons may be that thequestionnaire is very comprehensive consisting of 10 A4pages, which may discourage some potential respondentsfrom participating the survey. This low response rate wouldlimit the generalization of the findings of the study.Nevertheless, the survey results are still meaningful as the31 respondents are all at high management level in theirrespective companies and have concrete experience ininternational construction projects in developing countries.

In addition, they have all shown great interests in the research,have filled in the questionnaire carefully and provided alot of valuable comments. The following summarize thekey findings of the survey. For more details, please referto Wang and Dulaimi (2002).

The risk criticality and mitigation measureeffectiveness

Criticalities of risks and risk levels

The criticality of the identified risks as shown in Table 4is listed along with statistical indicators, the mean andstandard deviation (SD), sorted by criticality ranking.

Figure 1 Research tasks

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Risk management in developing countries 241

The Total Criticality Index is the sum of all ratedindexes (1 to 7) for each risk by all respondents while theMean Criticality Index is the average index for each riskobtained by dividing the Total Criticality Index by totalnumber of respondents. The ranking of risks is directlybased on the Mean Criticality Index.

It could be seen from Table 4 that 22 out of 28 riskshaving mean criticality index between 4 (i.e. Critical) and6 (i.e. Very Much Critical). It follows that respondentsperceive about 78% of identified risks within critical tovery critical range.

It could also be seen from Table 5 that out of the top

Level

Level I: country levelApproval and permit: Delay or refusal of project approval and permit by local governmentChange in law: Local government’s inconsistent application of new regulations and lawsJustice reinforcement: Lack of legal judgment reinforcementGovernment influence on disputes: Unnecessary and unjust influence by local government on court proceedings

regarding project disputesCorruption: Corrupt local government officials demand bribes or unjust rewardsExpropriation: Due to political, social or economic pressures, local government takes over the facility run by

foreign firm without giving reasonable compensationQuota allocation: Failure in obtaining fair import/export quota allocation from local governmentPolitical instability: Frequent changes in government; agitation for change of government or disputes between

political parties or different organs of the stateGovernment policies: Government policies on foreign firms, e.g. mandatory joint venture (JV); mandatory

technology transfer; differential taxation of foreign firms, etc.Cultural differences: Differences in work culture, education, values, language, racial prejudice, etc., between

foreign and local partners.Environmental protection: Stringent regulation which will have an impact on construction firms’ poor attention to

environmental issuesPublic image: Victim of prejudice from public due to different local living standards, values, culture, social system,

etcForce majeure: The circumstances that are out of the control of both foreign and local partners, such as flood,

fires, storms, epidemic diseases, war, hostilities and embargoLevel II: market levelHuman resource: Foreign firms face difficulties in hiring and keeping suitable and valuable employees.Local partner’s creditworthiness: Information on local partner’s accounts lucidity, financial soundness, foreign

exchange liquidity, staff reliabilityCorporate fraud: Unexpected increases in turnover, unexpected resignation of financial adviser, letter of credits

with ‘unreasonably round figures’, intentional or unintentional negligence either by auditors, bankers or creditorsTermination of Joint Venture (JV): Unfair dividends, e.g. assets, shares and benefits, to foreign firm by local

partner upon termination of JV contractForeign exchange and convertibility: Fluctuation in currency exchange rate and/or difficulty of convertibilityInflation and interest rates: Unanticipated local inflation and interest rates due to immature local economic and

banking systemsMarket demand: Inadequate forecast about market demandCompetition: Competition from other international investors/developers/contractors.Level III: project levelCost overrun: Unavailability of sufficient cash flow, improper measurement and pricing of Bill of Quantities

(BOQ), ill planned schedule and client’s delay in paymentImproper design: Unanticipated design changes and errors in design/drawings resulting from the difference in local

design custom and practices.Low construction productivity: Obsolete technology and practices by local partner; or low labour productivity of

local workforce owing to poor skills or inadequate supervisionSite safety: High rate of accidents during construction or operation phasesImproper quality control: Local partner tolerance of defects and inferior qualityImproper project management: Improper project planning, budgeting; inadequate project organization structure;

and incompetence of local project teamIntellectual property protection: Former local employees, partners and/or third parties steal company’s intellectual

property, commercial secrets or patent formulae

ID

A1A2A3A4

A5A6

A7A8

A9

B1

E1

E2

G1

B2B3

B4

B5

C1C2

H1H2

C3

D1

D2

D3D4D5

F1

Table 1 Risks under hierarchy levels and their definitions

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Wang et al.242

Mitigation measures

Mitigation measures for risk #A1: approval and permitEnsure the project is complying with local planning commission’s development planEnsure the feasibility study report and contract depict local government, local partner and foreign party’s actual

intentions (like anticipated profits, risk sharing)Prepare and submit all necessary documents and feasibility study report in a timely manner to local government

departmentsEstablish JV with renowned local partners, especially the central government agencies or state owned enterprisesMaintain good relationship with local government and higher officialsAsk local government to establish one stop agency for all approvalsPre-package all approvals when signing contract with project clientObtain support of foreign firm’s home government and international monetary institutions like World Bank and

Asia Development Bank (ADB) against delay in approval and permitMitigation measures for risk #A2: change in law, and for risk #A3: justice reinforcementObtain local government guarantee to adjust tariff or extend concession period (for Build-Operate-Transfer

(BOT) projects)Maintain good relationship with local government and higher officialsObtain insurance for political risksInclude clauses for delays and additional payments in contract, which occur due to new rules or change in lawSeek support from international developers/contractors’ home governmentRely on combination of international consortium, joint international convention and insurance policies (especially

political insurance) to protect investment in the projectObtain support of international monetary institutions like World Bank and ADB against discrimination and

harassment by local government in legal proceduresMitigation measures for risk #A4: government influence on disputesProvide dispute settlement clauses in the contractEnsure the approval is sought at the right local government departmentsMaintain good relations with concerned local government officials and concerned authoritiesEstablish JV with local partners especially the central local government agencies or state owned enterprisesMitigation measures for risk #A5: corruptionEstablish JV with renowned local partners, especially the central local government agencies or state owned enterprisesEnter into contract with local government authorities to prevent corruptionSet aside a budget for unavoidable spendingCultural and commercial awareness training to management and key personal who may have to deal with corrupt

officialsTry to work directly with the business connections, i.e. do not hire broker or middlemanObtain all necessary approvals in timely manner to minimize chance for corrupt individual to obstruct workObtain support from foreign firm’s home government and international monetary institutions like World Bank and

ADB against misuse of power by local government or its agenciesMaintain good relations with concerned local government officials and concerned authoritiesMitigation measures for risk #A6: expropriationBe informed of political developments by making use of information sources like international security and risk

assessment companiesDevelop contingency plans and obtain insurance for expropriation possibilityEstablish JV with local partners especially the central local government agencies or state owned enterprisesRely on combination of international consortium and insurance policies (especially political insurance)Maintain good relations with concerned local government officials and concerned authoritiesObtain support from foreign firm’s home government and international monetary institutions like World Bank and

ADB against expropriation by local government or its agenciesMitigation measures for risk #A7: quota allocationEstablish good relations with officials in concerned ministriesPrepare and submit all necessary reports and feasibility study on timeEstablish JV with local partners especially the central local government agencies or state owned enterprisesObtain support from foreign firm’s home government and international monetary institutions like World Bank and

ADB against unfair quota allocationMitigation measures for risk #A8: political instabilityDevelop own contingency plans for possible political instability, such as plan for emergency evacuationSeek incorporation of termination or delay clauses in contract

Table 2 Mitigation measures for each of the risks identified

ID

M1M2

M3

M4M5M6M7M8

M1

M2M3M4M5M6

M7

M1M2M3M4

M1M2M3M4

M5M6M7

M8

M1

M2M3M4M5M6

M1M2M3M4

M1M2

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Risk management in developing countries 243

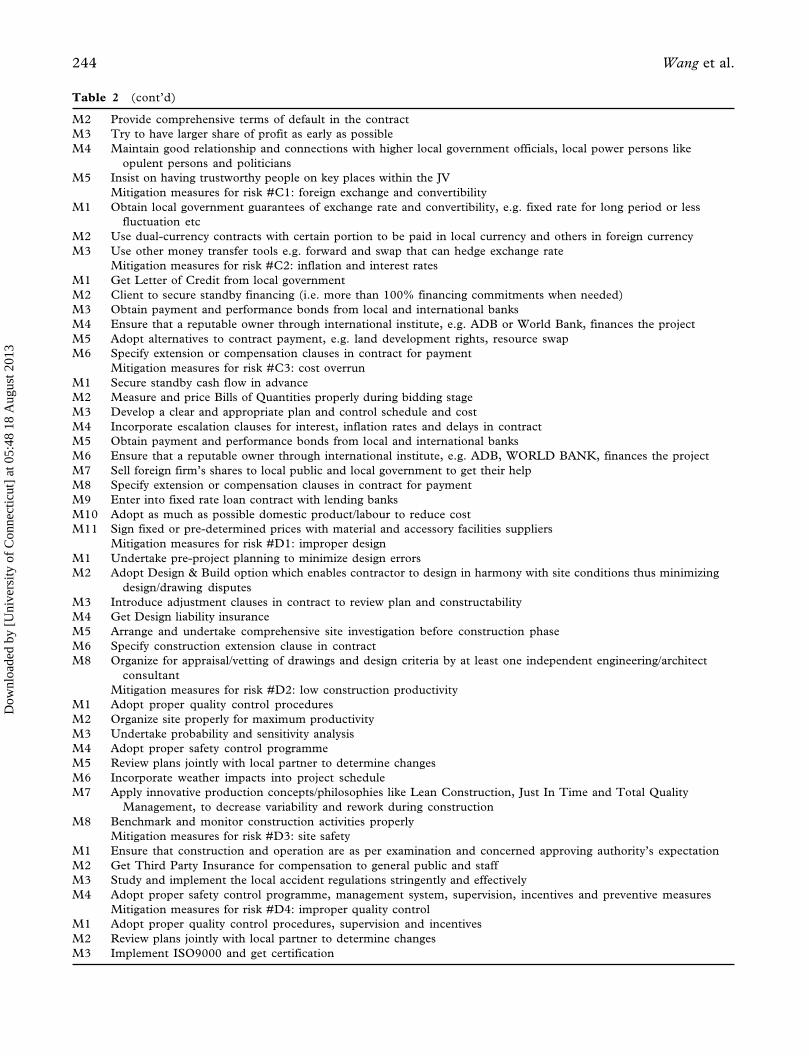

Table 2 (cont’d)

Obtain insurance for political risks from international finance and risk assessment agenciesBe informed of political developments by using information sources like international security and risk assessment

companiesRely on combination of international consortiumEstablish JV with local partners especially the central local government agencies or state owned enterpriseMaintain good relationship and connections with higher local government officials, local power sources like

opulent persons and politiciansObtain support from foreign firm’s home government during anticipated insurgencyMitigation measures for risk #A9: government policiesEstablish JV with local partners especially the central local government agencies or state owned enterpriseMaintain good relationship and connections with higher local government officials, local power sources like

opulent persons and politiciansObtain support from foreign firm’s home government during anticipated insurgencyTransfer ordinary technology only but keep the key onesSeek reasonable compensation scheme (lump sum, share in JV, profit) for technology transferStudy carefully the differential taxation and find legal and reasonable measures to reduce taxesMitigation measures for risk #B1: cultural differencesUndertake comprehensive negotiations and agreement with local government and partnersDevise unambiguous and agreed risk sharing code at the time of contractTry to have as large an equity share as possible thus ensuring control of Board of DirectorsInsist on having trustworthy people on key places within the JVHire company’s own competent native language-speaking employee, even though some of the staff understand

native languageProvide dispute settlement clauses in the contractMitigation measures for risk #B2: human resourceOnly take over the local partner’s competent staff when merging with the partner or during the contract processSign formal employment contract with every staffEmploy staff on a contract through one local partner who is more familiar with one local set-up than foreign firmDecide on recruitment and selection criteria in consultation with one local partnerForeign firm should insist on having trustworthy people on key places within the JVOffer training to new and existing staffOffer better remuneration/incentive packages to staffMitigation measures for risk #B3: local partner’s creditworthinessGain accurate financial and other information from international and independent security and risk evaluation

agenciesExamine the target company’s financial viability, technical and management competence and connections with

local governmentMaintain good relationships with top local government officers at state or provincial level to gain more information

about prospective local partnerInsist on having trustworthy people on key places within the JVObtain guarantees or other credit support from reliable and credit worthy local and international entitiesHave clear contractual terms and conditions, agree on one accounting standard and define clear authority and

responsibility in contractPay careful attention to contract translationHire company’s own competent native language-speaking employee, even though some of the staff understand

native languageInsist that bilingual (English and local language) documents are prepared simultaneously and agreed in final form

by all partiesDefine clearly the merging scope of assets, employees, shares, organization, strategies, etc. when merging with a

local partnerMitigation measures for risk #B4: corporate fraudGet information about local partner’s credibility from its present and past business partnersInsist on having trustworthy people on key places within the JVMonitor present status and par/face value of share dealings of the JVVisit/check the factory or business regularly and irregularlyAll parties should agree on one accounting standard and hire one independent accountantMitigation measures for risk #B5: termination of Joint VentureChoose to establish a cooperative JV and partnership

M3M4

M5M6M7

M8

M1M2

M3M4M5M6

M1M2M3M4M5

M6

M1M2M3M4M5M6M7

M1

M2

M3

M4M5M6

M7M8

M9

M10

M1M2M3M4M5

M1

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Wang et al.244

Provide comprehensive terms of default in the contractTry to have larger share of profit as early as possibleMaintain good relationship and connections with higher local government officials, local power persons like

opulent persons and politiciansInsist on having trustworthy people on key places within the JVMitigation measures for risk #C1: foreign exchange and convertibilityObtain local government guarantees of exchange rate and convertibility, e.g. fixed rate for long period or less

fluctuation etcUse dual-currency contracts with certain portion to be paid in local currency and others in foreign currencyUse other money transfer tools e.g. forward and swap that can hedge exchange rateMitigation measures for risk #C2: inflation and interest ratesGet Letter of Credit from local governmentClient to secure standby financing (i.e. more than 100% financing commitments when needed)Obtain payment and performance bonds from local and international banksEnsure that a reputable owner through international institute, e.g. ADB or World Bank, finances the projectAdopt alternatives to contract payment, e.g. land development rights, resource swapSpecify extension or compensation clauses in contract for paymentMitigation measures for risk #C3: cost overrunSecure standby cash flow in advanceMeasure and price Bills of Quantities properly during bidding stageDevelop a clear and appropriate plan and control schedule and costIncorporate escalation clauses for interest, inflation rates and delays in contractObtain payment and performance bonds from local and international banksEnsure that a reputable owner through international institute, e.g. ADB, WORLD BANK, finances the projectSell foreign firm’s shares to local public and local government to get their helpSpecify extension or compensation clauses in contract for paymentEnter into fixed rate loan contract with lending banksAdopt as much as possible domestic product/labour to reduce costSign fixed or pre-determined prices with material and accessory facilities suppliersMitigation measures for risk #D1: improper designUndertake pre-project planning to minimize design errorsAdopt Design & Build option which enables contractor to design in harmony with site conditions thus minimizing

design/drawing disputesIntroduce adjustment clauses in contract to review plan and constructabilityGet Design liability insuranceArrange and undertake comprehensive site investigation before construction phaseSpecify construction extension clause in contractOrganize for appraisal/vetting of drawings and design criteria by at least one independent engineering/architect

consultantMitigation measures for risk #D2: low construction productivityAdopt proper quality control proceduresOrganize site properly for maximum productivityUndertake probability and sensitivity analysisAdopt proper safety control programmeReview plans jointly with local partner to determine changesIncorporate weather impacts into project scheduleApply innovative production concepts/philosophies like Lean Construction, Just In Time and Total Quality

Management, to decrease variability and rework during constructionBenchmark and monitor construction activities properlyMitigation measures for risk #D3: site safetyEnsure that construction and operation are as per examination and concerned approving authority’s expectationGet Third Party Insurance for compensation to general public and staffStudy and implement the local accident regulations stringently and effectivelyAdopt proper safety control programme, management system, supervision, incentives and preventive measuresMitigation measures for risk #D4: improper quality controlAdopt proper quality control procedures, supervision and incentivesReview plans jointly with local partner to determine changesImplement ISO9000 and get certification

Table 2 (cont’d)

M2M3M4

M5

M1

M2M3

M1M2M3M4M5M6

M1M2M3M4M5M6M7M8M9M10M11

M1M2

M3M4M5M6M8

M1M2M3M4M5M6M7

M8

M1M2M3M4

M1M2M3

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Risk management in developing countries 245

Mitigation measures for risk #D5: improper project managementHire competent project management teamEmploy local staff with bilingual abilityClear definition of each staff’s scope of workConflict resolution clause in contract and specify construction extension clause in contract if client causes the delayProvide notice provision and notice period in contractProvide clauses on schedule delay and additional payment if caused by clientMitigation measures for risk #E1: environmental protectionAdopt strict pollution control measuresEngage both local and international pollution control specialistsComply with international and/or local environmental laws, standards and regulationsInclude disclaimer in contract for present pollution level (conduct survey to see clear picture)Mitigation measures for risk #E2: public imageComply with local and international civil laws and standards, local social and cultural valuesMaintain good reputation and image to the publicGive donations to renowned non-governmental organizations, which are involved in elevating the living conditions

of poorParticipate actively in public relation activates and charityMitigation measures for risk #F1: intellectual property protectionPlace restrictive covenants (promises) in the contracts of employeesExploit local legislation to get protection against unauthorized use of confidential informationEnsure that the local partner appreciates the advantages of having exclusive rights to that property i.e.

shareholding in protection of intellectual propertyLimit the duration of technology transfer contractNegotiate on amount and speed of technology transferConfirm whether a good local intellectual property protection scheme is in place for the key intellectual property

like trademark, patent or copyright lawInsist on having trustworthy people on key places within the JVIntellectual property rights training to all key employees by sending them to seminarsMitigation measures for risk #G1: force majeureA party which fails to meet his contractual obligation due to force majeure must notify the other one within a

reasonable timeObtain local government guarantee to adjust tariff or extend concession period (for BOT projects)Insure all of the insurable force majeure risksObtain local government’s guarantee to provide financial help when neededInclude delay clauses for contingency plan in contractMitigation measures for risk #H1: market demandEmploy reputable third party consultant to forecast market demandMaintain good relationship and connections with higher local government officials, local power sources like

opulent persons and politiciansMitigation measures for risk #H2: competitionConduct market study and obtain exact information of competitive projectsAdopt as much as possible domestic product/labour to reduce costEstablish agreement with local government agency to reduce/exempt from import formalitiesMaintain good relationship and connections with higher local government officials, local power sources like

opulent persons and politicians

Table 2 (cont’d)

M1M2M3M4M5M6

M1M2M3M4

M1M2M3

M4

M1M2M3

M4M5M6

M7M8

M1

M2M3M4M5

M1M2

M1M2M3M4

Table 3 Rating system for risk criticality and mitigation measure effectiveness

Rating

1234567

Risk criticality

Not critical at allSlightly criticalSomehow criticalCriticalVery criticalVery much criticalExceptionally critical

Mitigation measure effectiveness

Not effective at allSlightly effectiveSomehow effectiveEffectiveVery effectiveVery much effectiveExceptionally effective

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Wang et al.246

11 most critical risks, seven risks (A1, A2, A3, A8, A5,A9 and A4) are in Country Level and this confirms thatthe Country Level is the most critical risk group. AsQuartiles are often used to divide populations into groupsand the third Quartile value is of important meaningwhich means that 25% of the populations are havingvalues greater than it, the third Quartile values of eachrisk levels are also shown in Table 5. The third Quartilevalue of Country Level Criticality is 4.85, the highest ofthe three levels, confirming again that the Country Levelis the most critical risk group. The next most criticalgroup of risks is the Market Level as it contains two outof 11 most critical risks (B3 and C2) with the 3rd Quartilevalue of 4.58 of Level Criticality. While the Project Levelrepresents only one risk (C3) in the top 11 most criticalrisks and with the lowest third Quartile value of 4.52 ofLevel Criticality.

Effectiveness of mitigation measures

Table 6 shows the mean effectiveness, rated by therespondents using the rating system in Table 3, of themitigation measures for each of the risks. It is under-standable that mitigation measures which are perceived

to be of higher effectiveness value should be implementedwith higher priority than that with less effectiveness one,i.e. the effectiveness dictates the implementation sequenceof mitigation measures.

Table 6 also shows that all mitigation measures havebeen rated between 3.7 and 5.7. Hence all respondentshave perceived the proposed measures as effective or veryeffective.

Proposed risk model

Risk influence matrix

Based on the above as well as literature review, interviewand discussion, general wisdom and logical deduction, itcould be drawn that there is relationship among risks atdifferent levels (Flanagan and Norman, 1993; Thobani,1999; Hastak and Shaked, 2000). The country level risksare influencing both the market and project levels risks,while the market level risks are influencing the projectlevel risks (Table 7). The country level risks are thereforemost dominant and at the highest hierarchical level whilethe project level risks are relatively the most dormant and

Table 4 Statistical results on the criticality of risks

Risk ID

A1A2A3B3A8C3A5C2A9A4B5B4H2C1H1D1D5D4A6B2D2A7G1D3B1E2F1E1

Risk description

Approval and permitChange in lawJustice reinforcementLocal partner’s creditworthinessPolitical instabilityCost overrunCorruptionInflation and interest ratesGovernment policiesGovernment influence on disputesTermination of JVCorporate fraudCompetitionForeign exchange and convertibilityMarket demandImproper designImproper project managementImproper quality controlExpropriationHuman resourceLow construction productivityQuota allocationForce majeureSite safetyCultural differencesPublic imageIntellectual property protectionEnvironment protection

Total criticality index

181.5161.5161.5154150.5150.5148143.5142.5141.5141.5141141140.5140.5140140138.5136.5129.5127.5126123122.5114110.5107106

Mean index

5.855.215.214.974.854.854.774.634.604.564.564.554.554.534.534.524.524.474.404.184.114.063.973.953.683.563.453.42

Risk rank

122455789

10101212141416161819202122232425262728

Standard deviation

1.301.421.421.361.981.581.361.391.391.371.551.461.361.271.641.431.540.922.011.431.281.481.911.381.711.371.541.26

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Risk management in developing countries 247

are in the lowest hierarchical level, just as were confirmedby the survey results summarized in Table 5.

Table 8, a much more comprehensive risk influencematrix, portrays the detailed influences of risks at onehigher level, the dominant risks, on the risks at one lowerlevel, the dormant risks (Flanagan and Norman, 1993;Thobani, 1999; Hastak and Shaked, 2000). It followsthat the risk mitigation strategy should prioritize the riskswith respect to dominance, i.e. the dominant risks shouldbe mitigated before or with higher priority over the dor-mant ones. The goal is not only to mitigate the dominantrisks but also their influence on subsequent dormantrisks, which will ultimately minimize the dormant risksas well.

Take for example the influence of the human resourcesrisk (B2, at the Market Level) on the cost overrun risk(C3, at the Project Level). ‘B2→C3’ means Risk B2 isinfluencing Risk C3. As suitable, competent and valuableemployee ensure availability of proper measurement andpricing of Bill of Quantities (BOQ), and proper schedule.Another example, ‘C1, C2→C3’ means Risk C1 (foreign

exchange and convertibility) and Risk C2 (inflation andinterest rates) both influencing Risk C3 (cost overrun).This is true as fluctuation in currency exchange rate and/or difficulty of convertibility brings out cost overrun. Andunanticipated local inflation and interest rates due toimmature local economic and banking systems putforward unavailability of sufficient cash flow, improperpricing of BOQ and client’s delay in payment, etc., all ofwhich will result in cost overrun.

Alien eyes’ risk model

Based on the above, if symbol A→B is used to representthe influence relationship of one event on the other, e.g.Risk A on Risk B, then the relationship among risks atthe three levels could be represented in the proposed riskmodel as illustrated in Figure 2.

Apropos to consideration for the proposed risk modelshown in Figure 2, some unique conceptual analogieswere found between an Alien (extraterrestrial beings) anda risk’s impact and interaction as discussed above. This

Table 5 Risk level criticality based on third Quartile value (75th percentile)

ID

A1A2A3A4A5A6A7A8A9B1E1E2G1

B2B3B4B5C1C2H1H2

C3D1D2D3D4D5F1

Level

Level I: Country LevelApproval and permitChange in lawJustice reinforcementGovernment influence on disputesCorruptionExpropriationQuota allocationPolitical instabilityGovernment policiesCultural differencesEnvironmental protectionPublic imageForce majeureLevel II: Market LevelHuman resourceLocal partner’s creditworthinessCorporate fraudTermination of joint venture (JV)Foreign exchange and convertibilityInflation and interest ratesMarket demandCompetitionLevel III: Project LevelCost overrunImproper designLow construction productivitySite safetyImproper quality controlImproper project managementIntellectual property protection

Criticality index(1, 2, . . . , 7)

5.855.215.214.564.774.404.064.854.603.683.423.563.97

4.184.974.554.564.534.634.584.50

4.854.524.113.954.474.523.45

Risk rank

122

107

192259

25282623

204

1210148

1318

5162124181627

Level criticality(3rd Quartile)

4.85

4.58

4.52

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Wang et al.248

is analogous to an Alien with two eyes. Secondly alienand risk share same nature as they both are uncertain,ambiguous, hard to understand, and may bring loss ordanger. Therefore, to better reflect the characteristics ofthe proposed risk model, it is referred to as the AlienEyes’ Risk Model.

Proposed risk mitigation framework

Prioritizing mitigation measures

As discussed earlier, the mitigation measures for onerisk should be prioritized with their effectiveness assummarized in Table 6 when they are implemented to

mitigate the risk. Furthermore, as there is influencingrelationship among risks under the three hierarchy risklevels, the prioritizing of mitigation measures should alsotake into account the risk hierarchy levels. This could beillustrated further by following example.

Let Risk A’s Mitigation Measure 1 = A1M, RiskB’s Mitigation Measure 1 = B1M and also assume therelationship between Risk A and Risk B is ‘A→B’ (i.e.Risk A is influencing Risk B or Risk B is influenced byRisk A), then there is ‘A1M→B1M’, which means thatRisk A’s Mitigation Measure 1 has to be implementedbefore the Mitigation Measure 1 for Risk B. This isbecause that Risk A is influencing Risk B and thereforeprioritizing the Mitigation Measure 1 for Risk A willhelp to reduce the possible occurrence of Risk B.

Note:< Influence of Country Level Risks on Market Level Risks� Influence of Country Level Risks on Project Level Risks← Influence of Market Level Risks on Project Level Risks

Table 7 Synopsis of risk influence among risk hierarchy levels

Market level risksProject level risks

Country level risks

<�

Market level risks

←

Note: Refer to Table 1 and Table 2 for risk and mitigation measure IDs.

Table 6 Effectiveness of mitigation measures for each risk

Risk

A1A2/A3A4A5A6A7A8A9B1B2B3B4B5C1C2C3D1D2D3D4D5E1E2F1G1H1H2

M1

5.284.984.974.254.204.924.604.734.504.405.054.924.834.654.275.104.885.054.905.405.405.284.984.625.074.605.25

M2

4.805.324.823.874.455.004.635.004.654.755.225.374.924.984.685.385.225.325.184.924.624.705.284.424.684.734.90

M3

4.604.525.084.834.924.924.904.204.734.404.734.784.384.775.125.404.574.704.984.685.125.334.024.785.03

4.65

M4

5.104.705.074.804.404.184.524.205.284.935.305.254.68

5.035.024.404.755.30

5.024.734.254.474.62

4.73

M5

5.654.15

4.274.80

4.284.624.855.454.975.535.03

4.204.755.254.80

4.77

4.645.00

M6

4.384.67

4.154.35

4.734.904.875.285.42

4.875.004.704.60

4.92

4.78

M7

4.534.23

4.05

4.78

5.285.33

3.724.584.77

5.03

M8

4.67

4.92

4.20

4.83

4.45

4.93

4.03

M9

5.08

4.45

M10

5.13

4.70

M11

5.05

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Risk management in developing countries 249

Table 8 Risk influence matrix

Country level risks

B2B3B4B5C1C2H1H2C3D1D2D3D4D5F1

A1

�

�

A2/A3

<

<<<

��

����

A4

<<

�

��

A5

<<<

<

����

A6

<

�

A7

<<<

�

A8

<<<<<

�

A9

<<

<<<

�

�

�

G1

<<<<<�

E1

��

E2

<

�

�

B1

<<<<

��

�

�

B2

←←←←←←←

B3

←

←

B4

←

←

B5

←

C1

←

←

C2

←

H1

←←

H2

←

Market level risks

Market levelrisks

Project levelrisks

Note: Refer to Table 1 for risk IDs and definitions< Influence of Country Level Risks on Market Level Risks� Influence of Country Level Risks on Project Level Risks← Influence of Market Level Risks on Project Level Risks

Figure 2 Proposed risk model – Alien Eyes’ Risk Model

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Wang et al.250

Therefore, for the example discussed in above section,since Risk C1 (foreign exchange and convertibility) andRisk C2 (inflation and interest rates), both at MarketLevel, are influencing another Risk C3 (cost overrun), atProject Level, mitigation measures M1, M2, M3 for RiskC1 and M1, M2, M3, M4, M5, M6 for Risk C2 areprerequisites, and M1, M2, M3, . . . , M11 for Risk C3must be the successor mitigation activities. (Refer toTable 2 for details of the respective mitigation measuresM1, M2, . . . , M11 for the risks C1, C2 and C3.)

Table 9 summarizes the prioritizing results of themitigation measures for risks at different risk levels basedon their effectiveness (Table 6) obtained from the survey.

Qualitative risk mitigation framework

Based on the risk criticalities (Table 4), the risk hierarchylevels (Table 5), the influence relationship among risks(Table 8 and Figure 2), the mitigation measure effective-ness (Table 6) and the prioritized mitigation measures(Table 9), a qualitative risk mitigation framework asshown in Figure 3 is proposed. This framework containsthe following steps.

Step 1 Define the nature of any identified risk, i.e.whether the risk is close in definition andscope to a risk listed in Table 1 and whichhierarchical level the risk falls in.

Step 2 Find the risk’s criticality from Table 4 andits proposed mitigation measures’ effectivenessfrom Table 6.

Step 3 Find the risk’s influence relationship withother risks from the Risk Influencing Matrixshown in Table 8.

Step 4 If the risk falls in the Level I, only themitigation measures (referred as group X)specific to this risk should be implementedbut the mitigation measures with highereffectiveness as shown in Table 6 with higherpriority, if the measures are applicable.

Step 5 If the risk falls in Level II, implement GroupX mitigation measures first followed byGroup Y measures which are specific to thislevel of risk. For the mitigation measures ofone risk, implement the measures withhigher effectiveness first.

Step 6 If the risk falls in Level III, the implementation

Table 9 Prioritizing mitigation measures for risks

Risk group

Country level risks

Market level risks

Project level risks

Risk code

A1A2/A3

A4A5A6A7A8A9B1E1E2G1B2B3B4B5C1C2H1H2C3D1D2D3D4D5F1

Implementation sequence (I . . . . XI) of mitigation measures based on theireffectiveness and the risk level

I

M5M2M3M8M3M2M3M2M4M1M3M1M6M6M5M5M2M3M2M1M3M5M2M4M1M1M7

II

M1M1M4M3M5M3M7M6M6M2M1M3M6M7M2M2M3M4M1M2M2M2M1M2M2M3M3

III

M4M4M1M4M2M1M6M1M5M4M4M5M7M4M4M1M1M6

M4M1M1M8M3M3M4M6

IV

M2M6M2M5M4M4M2M5M3M3M2M2M4M2M1M4

M2

M3M11M6M5M1

M6M5

V

M8M3

M1M6

M1M3M2

M4M2

M10M3M3

M1

M4M7M7

M5M1

VI

M7M7

M6M1

M4M4M1

M1M9

M5

M6M3M4

M2M4

VII

M3M5

M7

M5

M3M1

M5M4M3

M2

VIII

M6

M2

M8

M5

M10

M6

M8

IX

M8

M8

X

M3

M9

XI

M7

Note: Refer to Table 1 and Table 2 for IDs and definitions of risk and mitigation measure.

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Risk management in developing countries 251

sequence would be first Group X, secondGroup Y and lastly Group Z mitigationmeasures. For the general implementationsequence of mitigation measures, Table 9needs to be used.

Conclusions

Twenty-eight critical risks associated with internationalconstruction projects in developing countries were identi-fied and categorized into three hierarchy levels (Country,Market and Project). Of which, 22 were evaluated asCritical or Very Much Critical based on a 7-degree ratingsystem. The top 11 critical risks are: Approval and Permit,Change in Law, Justice Reinforcement, Local Partner’sCreditworthiness, Political Instability, Cost Overrun,Corruption, Inflation and Interest Rates, GovernmentPolicies, Government Influence on Disputes and Termi-nation of JV. The risks at Country level are more criticalthan that at Market level and the latter are more criticalthan that in Project level.

For each of the identified risks, practical mitigationmeasures were provided and evaluated. Almost all of themitigation measures were perceived by the respondentsto the survey as effective using a 7-degree rating system.

It is suggested that when mitigating a specific risk, themeasures with higher effectiveness should be given ahigher priority.

Taking into account the higher criticalities of higherrisk hierarchy levels, the mitigation measures should alsobe prioritized by the higher risk hierarchy level, i.e. therisks at higher hierarchy level should be mitigated firstwith higher priority with their respective more effectivemitigation measures.

A risk model, named Alien Eyes’ Risk Model, wasproposed which shows the three risk hierarchy levels andthe influence relationship among risks. This model willenable better categorizing of risks and representing theinfluence relationship among risks at different hierarchylevels as well as revealing the mitigating sequence/priorityof risks.

A qualitative risk mitigation framework integrating thekey findings of the research was also proposed providingdetailed risk management strategies and procedure thatinternational especially Singaporean firms, could adopt.The proposed framework is practical and relatively easyto apply.

Although the survey sample is relatively small, theauthors believe that the survey results are still meaningful.Nevertheless, more survey samples could be included soas to make the results more valid.

Figure 3 Proposed qualitative risk mitigation framework

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013

Wang et al.252

Acknowledgements

The authors would like to thank the National Universityof Singapore (NUS) for sponsoring this research; ProfGeorge Ofori, Department of Building, NUS, for pro-viding feedback on the draft questionnaire; all the inter-viewees and respondents of the survey for their valuableopinions, comments and responses; and all the fourreviewers of this paper, for their valuable comments andsuggestions.

References

Bajaj, D., Oluwoye, J. and Lenard, D. (1997) An analysisof contractor’s approaches to risk identification in NewSouth Wales, Australia. Construction Management andEconomics, 15, 363–9.

Baker, S., Ponniah, D. and Smith, S. (1999) Risk responsetechniques employed currently for major projects.Construction Management and Economics, 17, 205–13.

C21 Steering Committee (1999) Construction 21 Report.Singapore.

Cheng, A.T. and Chung, Y. (2001) Power corrupts. Asiaweek,9 February, 24–26.

Faber, W. (1979) Protecting Giant Projects: A Study of Problemsand Solutions in the Area of Risk and Insurance, Willis Faber,England, Ipswich, UK.

Flanagan, R. and Norman, G. (1993) Risk Management andConstruction, Blackwell Scientific, Oxford, UK.

Gupta, J.P. and Sravat, A.K. (1998) Development andproject financing of private power projects in developingcountries: a case study in India. International Journal ofProject Management, 16, 99–105.

Haarmeyer, D. and Mody, A. (1997) Private capital in waterand sanitation. Finance and Development, 34(1), 34–7.

Hastak, M. and Shaked, A. (2000) ICRAM-1: model forinternational construction risk assessment. Journal ofManagement in Engineering, 16(1), 59–67.

Hertz, D.B. and Thomas, H. (1983) Risk Analysis and ItsApplications, John Wiley & Sons, Inc., New York.

Jaselskis, E.J. and Talukhaba, A. (1998) Bidding operationsin developing countries. Journal of Construction Engineeringand Management, 124(3), 185–93.

Kalayjian, W.H. (2000) Third world markets: anticipatingthe risks. Civil Engineering, 70(5), 56–7.

Li, B., Tiong, R.L.K., Wong, W.F. and Chew, D.A.S. (1999)

Risk management in international construction jointventures. Journal of Construction Engineering and Management,125(4), 277–84.

Luo, J. (2001) Assessing management and performance ofSino–foreign construction joint ventures. ConstructionManagement and Economics, 19, 109–17.

Munns, A.K. Aloquili, O. and Ramsay, B. (2000) Jointventure negotiations and managerial practices in the newcountries of former soviet union. International Journal ofProject Management, 18, 403–13.

Ozdoganm, I.D. and Birgonul, M.T. (2000) A decision supportframework for projects sponsors in the planning stage ofBOT projects. Construction Management and Economics, 18,343–53.

Perry, J.G. and Hayes, R.W. (1985) Risk and its manage-ment in construction projects. Proceedings of Institution ofCivil Engineers, Part 1, 78, 499–521.

Raftery, J., Pasadilla, B., Chiang, Y.H., Hui, E.C.M. andTang, B.S. (1998) Globalization and construction industrydevelopment: implications of recent developments in theconstruction sector in Asia. Construction Management andEconomics, 16, 729–37.

Ramcharran, H. (1998) Obstacles and opportunities ininternational engineering services. Journal of Managementin Engineering, 14(5), 38–46.

Silk, M.A. and Black, S. (2000) Financing options for PRCwater projects. The China Business Review, July/August (http://www.chinabusinessreview.com/0007/black.html).

Songer, A.D., Diekmann, J. and Pecsok, R.S. (1997) Riskanalysis for revenue dependent infrastructure projects.Construction Management and Economics, 15, 377–82.

Thobani, M. (1999) Private infrastructure, public risk.Finance and Development, 36(1), 50–3.

Wang, S.Q., Tiong, R.L.K.R., Ting, S.K. and Ashley, D.(2000a) Evaluation and management of political risks inChina’s BOT projects. Journal of Construction Engineeringand Management, 126(3), 242–50.

Wang, S.Q., Tiong, R.L.K.R., Ting, S.K. and Ashley, D.(2000b) Evaluation and management of foreign exchangeand revenue risks in China’s BOT projects. ConstructionManagement and Economics, 18(2), 197–207.

Wang, S.Q. and Dulaimi, M.F. (2002) Building the ExternalWing of Construction: Managing Risk in InternationalConstruction Projects. Research Report R-296-000-044-112, Dept of Building, National University of Singapore.

Yeo, K.T. and Tiong, R.L.K. (2000) Positive managementof differences for risk reduction in BOT projects.International Journal of Project Management, 18, 257–65.

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 0

5:48

18

Aug

ust 2

013