Risk Management for Hedge Funds - OptiRisk Systems - carisma.1...Risk Management for Hedge Funds M A...

67

1 © 2008 Cambridge Systems Associates Limited www.cambridge-systems.com 4 4 th th Annual CARISMA Conference Annual CARISMA Conference London 1 London 1 st st July 2008 July 2008 Risk Management for Hedge Funds Risk Management for Hedge Funds M A H Dempster Centre for Financial Research Statistical Laboratory University of Cambridge & Cambridge Systems Associates Limited [email protected] www-cfr.jbs.cam.ac.uk

Transcript of Risk Management for Hedge Funds - OptiRisk Systems - carisma.1...Risk Management for Hedge Funds M A...

1

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

44thth Annual CARISMA Conference Annual CARISMA Conference London 1London 1stst July 2008July 2008

Risk Management for Hedge FundsRisk Management for Hedge Funds

M A H Dempster

Centre for Financial ResearchStatistical Laboratory

University of Cambridge&

Cambridge Systems Associates Limited

[email protected] www-cfr.jbs.cam.ac.uk

2

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

OutlineOutline

• Introduction

• Portfolio Performance and Risk Measures

• Robust Portfolio Optimization

• Long Short Equity Strategies for Alpha

• Credit Trading Strategies for Absolute Return

• Conclusions

3

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

MarkowitzMarkowitz Portfolio ConstructionPortfolio ConstructionClassical mean variance portfolio optimization (MVO) assumes r is distributed multivariate Gaussian (normal) with mean μand n x n covariance matrix Σ to maximize a tradeoff between expected return and portfolio return volatility subject to constraints Markowitz (1952)

( , )N μ Σ

'x xΣ

max . .

x x xs t Ax b

μ λ′ ′− Σ= Ex

pect

ed R

etur

n

Volatility

4

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Departures From Classical Distributional Departures From Classical Distributional AssumptionsAssumptions

In practice when Σ is estimated as from historical returns series on individual instruments/strategies the estimate is generally not positive definite and must be ‘corrected’

Moreover extensive modern research on various classes of instruments has shown that approximate normality depends upon• the instrument class• the period over which returns – assumed independent – are

defined (predicted)

Σ̂

5

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

As a result many alternative distributions for returns have been applied to portfolio construction for stocks, bonds, FX, futures, etc.

Four characteristics are at issue

• Higher moments than the two – mean and variance – which define all moments of the Gaussian distribution

• Tail behaviour

• More general dependency between contemporaneous returns than correlation

• Intertemporal dependencies between returns

μ 2σ

6

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Hedge Fund Annual Returns in 2005Hedge Fund Annual Returns in 2005

Source: P. Davis, Hedge funds lose big returns appeal, Financial Times Fund Management, May 1 2006

7

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Credit Loss DistributionCredit Loss Distribution

-20

-50

-80

-110

-140

-170

-200

-230

-260

-290

-320

-350

-380

-410

-440

-470

Portfolio Loss ($m)

Catastrophe Loss

Unxexpected Loss

Expected Loss

8

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Specification of NonSpecification of Non--NormalityNormalityFor skewed return distributions with non-normally shaped densities at least two more moments are considered

• Skew is the third moment which measures a long –downside – tail and is usually measured relative to as an index ofskewness

• Kurtosis is the fourth moment which gives the shape of the shoulders of the density – usually relative to as an index ofkurtosis or relative to that of the standard normal density whose value is 3

When return density tails are ‘fat’ or ‘long and thin’ no moments may existwhich leads to the use of α-stable or extreme value distributions where density tails decay polynomially for extreme values rather than exponentially as with Gaussian or Student t distributions

3( )i iΕ − Εr r

4( )i iΕ − Εr r

3σ

4σ

9

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Portfolio Performance and Risk MeasuresPortfolio Performance and Risk Measures

10

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Sharpe RatioSharpe RatioHow do we find the optimal portfolio P ?

P maximises the reward-to-variability ratio

Sharpe Ratio:

A good active manager• maximises the Sharpe Ratio• maximises the slope of his Capital Allocation Line (CAL)• has a steeper CAL than a passive investor who has CML

( )P f PS R σ= ⎡ − ⎤⎣ ⎦rE

11

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Portfolio Performance MeasuresPortfolio Performance Measures

Under classical independent returns assumptions portfolio performance over a specified horizon is measured in terms of one or more of portfolio• Return• Sharpe ratio

• Excess return over a suitable ‘risk free’ rate normalised by return volatility

• Sortino ratio• Excess return normalised by downside volatility – the square root of semi-variance

• Information ratio• Excess return relative to a suitable benchmark – usually a market index – normalized

by excess return volatility or tracking error

• Maximum drawdown• Stirling ratio

• Return (or excess return) normalized by maximum drawndown

12

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Tail Risk MeasuresTail Risk Measures

Appropriate to such skewed distributions are tail measures of risk (dispersion) such as

• Value at risk (VaR)

• Expected (VaR) shortfall or tail loss

• Regret or expected loss relative to a benchmark (e.g. 0)

α≤ − ={ }iP VaRr

−Ε +( )i VaRr

( )i+Ε r

13

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Value at RiskValue at RiskMeasures maximum unexpected loss

• For a given holding period

• For a given confidence level

• Chosen by the portfolio manager

Prob

abili

ty

90%99%

Market Value-v

P{XT < -v} = z

VaR is the quantity v

14

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Tail Risk MeasuresTail Risk Measures

Expected shortfall(expected tail loss, conditional VaR)• The average loss conditional on the

losses being greater than VaR

Regret• Expected value of all returns less

than a benchmark return (e.g. 0)

Expected shortfall

15

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Expected ShortfallExpected Shortfall

Expected Shortfall (at 99%) is the average of the worst 1% of losses

16

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Contemporaneous Return DependencyContemporaneous Return Dependency

Classical return dependency and volatility is given in terms of a correlation matrix

But extreme returns between two instruments tend to be more correlated than returns under normal market conditions – that is tail dependencies of their marginal densities exist which cannot be captured by spherical distributions such as the Gaussian or t distributions

ρ ρ σ σ= Σ =( ) defined by : ( )ij ij i jR

17

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

CopulasCopulas

Sklar (1959) observed that a general multivariate distribution function F for r can be written in terms of its marginal distribution functions Fi as

where the copula distribution function C with uniform marginalson [0,1] is a pure measure of dependency between the elements ofr

Many alternative copulas have been proposed for different instrument returns

1 1 11( ) : ( ( ), ..., ( ))n

nF r C F r F r− −=

18

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

IntertemporalIntertemporal DependencyDependency

Intertemporal return dependency must be specified by postulating a stochastic process for returns – in either continuous or discrete time – which exhibits the appropriate path dependent behaviour

Proposed specifications range from volatility clustering in the classical model (e.g. using Garch models) through diffusions, pure jump Levy processes and fractional Brownian motion in continuous time to long range autocorrelated and fractal and multi-fractalprocesses with rapidly increasing complexity of estimation and simulation

19

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Stationary Stationary ErgodicErgodic ReturnsReturns

One general specification that encompasses many other specific generalizations is a stationary ergodic specification for the process rwhich means that the joint distribution of returns at a set of times depends only on their relative time intervals so that and the time average along any sample path converges to μ

Another relevant extreme return measure is drawdown defined in terms of a return process path ri at t as

μΕ =tr

0sup { }i it tr rτ τ≤ ≤ −

20

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Portfolio Value and DrawdownPortfolio Value and Drawdown

Source: Krokmal et al. (2003)

21

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Stirling RatioStirling RatioProfit divided by maximum drawdown over a specified period

Used by traders and hedge fund investors to assess performance of systematic trading funds

Defined in the Pertrac User Manual www.pertrac.com but a trader will be indifferent between strategies that have a drawdown of less than a particular amount

This indifference is reflected in the modified Stirling ratio given by

where modified drawdown := max(drawdown, 2%)and return and drawdown are measured as a percentage of (notional) traded assets

When returns are negative the return alone is used

Provides a continuous sensible ordering for all return/drawdown combinations

returnS : = 1 + modified drawdown

22

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Coherent Risk MeasuresCoherent Risk MeasuresIn almost all portfolio construction expected portfolio return is balanced against asuitable risk measure

A financial position (portfolio) is described by a real valued mapping X from a set Ω of scenarios ω to money which we may take to be the random portfolio return(value)

A coherent monetary risk measure ρ satisfies the conditions Artzner et al. (1997)

• Positive homogeneity (position size invariance)

• Monotonicity(more is better)

• Translation invariance (additional capital reduces risk)

• Subadditivity(diversification benefit)

: ' x=X r

ρ λ λρ λ ρ= ∀ ≥ ⇒ =( ) ( ) 0 (0) 0X X

(a.s.) ( ) ( )ρ ρ≤ ⇒ ≥X Y X Y

ρ ρ ρ ρ= − ⇒ + =( ) ( ) ( ( )) 0+ m m X X X X

( ) ( ) ( ) convex+ρ ρ ρ ρ≤ + ⇒X Y X Y

23

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Convex Risk MeasuresConvex Risk Measures

Given a family of of probability distributions P on Ω we may represent a CRM as

By positive homogeneity and subadditivity a coherent risk measure is easily seen to be convex i.e.

When risk increases with position size convex risk measures not positively homogeneous are appropriate Foellmer &Schied (2003)

ρ ∈ℑ= Ε −( ) sup [ ]F P PX X

ℑ

[ ]( (1 ) ) ( ) (1 ) ( ) 0,1ρ λ λ λρ λ ρ λ+ − ≤ + − ∀ ∈……X Y X Y

24

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

CRMsCRMs and Convex Risk Surfacesand Convex Risk SurfacesThe hedging benefit H is nonnegative for a CRM Acerbi (2003)

Moreover the risk surface corresponding to portfolios given by as x varies is convex for a CRM which implies that minimal risk portfolios can be found by convex optimization

However VaR is not a coherent (or convex) risk measure since it failsthe axiom of subadditivity

Indeed examples of portfolios of Gaussian returns dependent through a non-Gaussion copula can be constructed for which the hedging benefit for VaR is negative

( , ) : ( ) ( ) ( )Hρ ρ ρ ρ= + − +X Y X Y X Y

( ' )xρ r

ρ

25

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Expected Shortfall is CoherentExpected Shortfall is Coherent

Expected shortfall (tail loss) relative to VaR for an absolutely continuous distribution is coherent and hence yields a convex risksurface although this is not necessarily so for a finite distribution of scenarios (data paths) without a more precise definition

26

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

1D Risk Surface for 1D Risk Surface for VaRVaR and ESand ES

Source: Acerbi (2003)

27

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Risk Surfaces for a 25 Bond PortfolioRisk Surfaces for a 25 Bond Portfolio

Source: Acerbi (2003)

%Quantile

28

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Spectral Risk MeasuresSpectral Risk Measures

A risk measure ρ is law invariant if i.e. it depends only on the CDF and hence is estimatable from data

Two portfolios X and Y are comonotonic if they are driven by the same risk factor Z so that for some non-decreasing functions f and g

A risk measure is comonotonically additive if X and Y comonotonic implies it is additive

( ) ( )Fρ ρ= XXo f F X X

= =: ( ) and : ( )f gX Z Y Z

ρ

29

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Spectral Risk MeasuresSpectral Risk Measures

A coherent risk measure which is both law invariant and comonotonically additive is called a spectral measure with representation

Alternatively this class of risk measures is given by

Acerbi(2001)

μρ μ μ= Ε∫1

0

( ) ( ) ( ) for a measure on [0,1] pS d p Kusuoka (2001)X X

φρ φ φ= ∫1

0

( ) ( ) (p) dp where is a on [0,1] p F non - increasing probability density-1XX

30

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Expected Shortfall and Expected Shortfall and VaRVaR SpectraSpectra

Source: Acerbi (2007)

31

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Robust Portfolio EstimationRobust Portfolio Estimation

32

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

MVO Sensitivity to Input VariationsMVO Sensitivity to Input Variations

33

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Portfolio RiskPortfolio RiskFor an n asset portfolio the standard deviation or volatility of the portfolio return

where are the standard deviations of the returns of assets Ai and is the covariance between assets i and j

Estimate portfolio standard deviation using

2 2

1 12

n n

P i i i j i ji i j i

w w wσ σ σ= = <

= +∑ ∑ ∑

iσ

ijσ

2 2

1 1

ˆ ˆ ˆ2n n

P i i i j iji i i j

w w wσ σ σ= = <

= +∑ ∑∑

34

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Forecasting Forecasting CovariancesCovariancesRecall the definition of a covariance matrix Σ of a random vectorx as

where σi is the standard deviation (volatility) of the ith element xiand ρij is the correlation between xi and xj

Recall also that the random variable has variance

This implies Σ is nonnegative definite

( )( ) ( ): : i j ijσ σ ρ′Σ = − − =x x x xE E E

1: I

i iiα α

=′ = ∑x x

0α α′Σ ≥

35

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Choice of Financial InstrumentsChoice of Financial Instruments

A covariance matrix Σ is positive definite iffwhich occurs when no two elements of x are

perfectly -- positively or negatively -- correlated

This property cannot be guaranteed in sample estimates-- so the number of instruments (or factors) to use is an important decision problem!

0α αΣ >′ for 0α ≠

36

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

MVO RobustnessMVO RobustnessThe stability of mean variance portfolios with respect to small changes in the problem parameters– expected returns and return covariances – is notoriously bad

In practice this is compounded by estimation error using historical data for expected returns, return covariances for instruments and regression coefficients of factor models

The most important contributor to instability are historical estimates of covariance matrices with low condition numbers – the ratio of the smallest to the largest eigenvalue – often zero for many instruments and (relatively) short time series

37

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Correcting Estimation ErrorCorrecting Estimation ErrorFor uncorrelated returns the condition number of the estimated covariance matrix will be near one and the contours of portfolio variance will be near spherical and portfolios stable – unfortunately not usual

Three principal approaches to overcome this practical problem are available• Shrinkage techniques which move the historical covariance estimate toward a

well-behaved covariance matrix

• Bayesian approaches which combine the investor’s prior views with sample estimates using Bayes theorem

• Randomization techniques using bootstrap historical resampling or simulation

38

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

BayesBayes--Stein Expected Return Shrinkage Stein Expected Return Shrinkage

Techniques for shrinkage estimation are based on a fundamental result of Stein (1955) for expected value – e.g. expected return –which shows that with low sample sizes an optimal trade-off between estimator bias and estimator variation produces a more efficient estimate than the standard unbiased sample mean estimate

For sample expected returns this yields the Bayes-Stein shrinkage estimator for ( , )N μ Σ∼r

λ λμ α μ α αμ μ

λ λ σ−

−= − + =

′− −

Σ = ∑

1

21 1

ˆ1 2ˆ ˆ: (1 ) 1 : ˆ ˆ( 1) ( 1)

1ˆ ˆ ˆwhere is the of and : and 1 is called the

S

nii

NT

nlargest eigenvalue

target vector

39

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

LedoitLedoit--Wolf Covariance ShrinkageWolf Covariance Shrinkage

A similar shrinkage estimator has been applied by Ledoit & Wolf (2004) to the sample covariance matrix using the well-conditioned target matrix

A full Bayesian approach to expected return estimation mixes the investor’s prior views in the form of a density with the sampling distribution assumed to underly returns to obtain a posterior densityfor returns

The mode of the posterior density for r is the Bayes-Stein shrinkageestimator when the target is the prior expected return vector

λ

α α α =

=

′ − ΣΣ = − Σ + =

Σ −∑ 2

1

ˆ : to o b ta inˆ[( ) ]1ˆ ˆ ˆ: (1 ) : m in { , 1}ˆ ˆ[( ) ]

n

Tt tS t

C I

tr r rC

T tr C

μ̂ S π

40

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

BlackBlack--LittermanLitterman Equilibrium ModelsEquilibrium Models

Black & Litterman (1992) saw that unreasonable portfolios produced by MVO result from inconsistent risk and return forecasts

Their equilibrium expected (excess) returns correspond to the market portfolio for MVO with a given (excess) return covariance matrix – risk model – produced by solving

Expected (excess) returns R are assumed uncertain with mean π and covariance matrix τΣ for τ a suitable shrinkage factor

λπ π λ

λ

′ ′− Σ = Σmax as 2

where is the producing the

MM M M M M

M M

x x x x

x penalty parameter market portfolio

πMx

41

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

BlackBlack--LittermanLitterman PortfoliosPortfoliosInvestor’s views have the effect of modifying expected returns Raccording to the uncertainty with which they are held in terms of

−τ expresses a level of confidence in the equilibrium expected returns π- P is a k x n matrix of investor view (long-short) portfolio weights

- g is the corresponding k vector of view portfolio expected returns with var(ε)=Ω

The Bayes solution for expected excess returns is

P g= +R ε

α τ τ πλ λ

− − − − −′ ′= Σ + Ω Σ + Ω′= +

1 1 1 1 1[( ) ] [( ) ] with where is a vector of different

BL

BL M

P P P gx x P kportfolio weights

weights on portfolio views

42

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Recent BlackRecent Black--LittermanLitterman ExtensionsExtensions

The Black-Litterman model is extended by Jones et al. (2007) to factor based structured equity portfolios

The basic model is extended in another direction by Giacometti et al. (2007) to consider other return distributions such as student t and alpha stable distributions and other risk measures such as VaRand expected tail risk

43

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Michaud Michaud ResamplingResamplingThe first to attempt to control the sampling error effects of covariance and expected return historical estimates on MVO by randomization was by Michaud (1998)

His procedure involves the following steps• Estimate from available historical data• Assuming and resample a large number of

scenarios from this distribution• Compute the efficient frontier corresponding to the estimates

and average to yield the resampled efficient frontier and corresponding MVO portfolios

This procedure has been generalized for other markets and risk measures by Meucci (2005) and Algren & Chriss (2003) have given an alternative randomization in terms of a uniform distribution of returns consistent with a specified ranking of expected returns

ˆˆ and μ Σμ μ μΣ = Σ Σ∼ ˆˆ( , ) set : and :=Nr

ω ∈Ω

ˆˆ( ) and ( ) for all μ ω ω ωΣ ∈Ω

44

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Efficiency of Michaud Efficiency of Michaud ResamplingResampling

The performance of Ledoit-Wolf shrinkage and resamplingrandomization was compared by Wolf (2006) who found the former superior to the latter and not significantly different from their combination

Moreover Scherer (2006) pointed out that without short selling restrictions the resampled frontier and the original correspond

Scherer also pointed out that Markowitz&Usman’s empirical finding that resampling is superior to a Bayesian model is ill-posed

45

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Scenarios as Randomization TechniquesScenarios as Randomization Techniques

Unlike MVO based on Gaussian return distributions scenario based techniques can allow any multivariate return distributions using scenarios that can be simulated, resampled from historical data or generated by quasi-random sequences

Often such return simulations will involve sampling marginal(individual instrument) returns combined through a specified copula

In general the scenario approach is a natural and intuitive form of randomization which makes the resulting portfolio decisions robustagainst a wide range of realized returns

46

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Robust OptimizationRobust Optimization

Following Ben-Tal & Nemirovski (1995, 2001) the robust MVO approach attempts to determine conservative worst-case parameter portfolios directly in terms of the problem

Meucci (2005) and Ceria & Stubbs (2006) give recent results

Pachamanova (2006) describes (limited) market tests which show good performance relative to ordinary MVO

μμ θ θ

μ

λμ

θ θ

Σ∈ Σ∈

Σ

′ ′− Σ

∈

min max2

. . where and are specified for parameter estimates

x x x

s t x Cuncertainty sets

Rx λ

47

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Long Short Equity Strategies for AlphaLong Short Equity Strategies for Alpha

48

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

LongLong--Short Equity PortfoliosShort Equity PortfoliosThe simplest approach to the construction of long-short equity portfolios is to drop the non-negativity condition on portfolio weights in MVO

However the aim of a long-short equity hedging strategy is to have portfolio excess returns uncorrelated with the market (index) in order to generate alpha – or absolute return – in all market conditions

To this end an additional market-neutral constraint in terms of the CAPM is imposed on MVO where estimates of the betas are used in the actual constraint

1ˆ ˆ: 0n

p i iixβ β

== =∑

0x ≥

49

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Derivatives and OverlaysDerivatives and OverlaysDerivatives and futures overlays are used to enhance portfolio returns – particularly for asset liabilitymanagement problems

For example a degree of market neutrality can be achievedfor a long only equity portfolio by shorting an appropriate index future or buying an index put option

FX futures contracts and cross currency swaps can be used to create a synthetic domestic portfolio from a global one

50

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Hedging RatioHedging RatioAnother important consideration is the desired long-short ratiowhich is decided by optimization in the simple approach taking no account of shorting (stock borrowing) costs

Alternatively long and short nonnegative portfolio weightsand and the budget constraints become

is fully hedged (the maximum short position under Regulation T) and ratios of 1: of 130:30 or 150:50 are often used to ensure approximate market neutrality

, 1L ii Lx

∈=∑ ,S ii S

x φ∈

=∑ [0,1]φ ∈

: 1φ =φ

0Lx ≥0Sx ≥

51

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Transactions CostsTransactions CostsIn trading situations particularly transactions costs and portfolio turnover are important features of realized portfolio returns

This is usually handled in MVO by asset position limitsbut can be treated explicitly in a typical situation which sees a portfolio rebalanced daily, weekly, monthly, quarterly, etc.

Relevant to portfolio optimization at each rebalance is the current portfolio xo

52

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Scenario Based Dynamic ModelsScenario Based Dynamic Models

By generating scenarios – by simulation, resampling or sampling using quasi-random sequences – for vector valued processes rather than simply for random vectors the same advantages as for tactical –one period – porfolio construction can be enjoyed for multiperiodstrategic portfolio construction

The techniques we will study for this setting involve what the actuaries call dynamic financial analysis (simulation) plus simultaneously optimizing decisions using stochastic optimization

53

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Long/Short Equity StrategyLong/Short Equity StrategyLong/short equity fund (hedging ratio as parameter)Select long and short portfolios on weekly basisControl turnoverObey sector constraintsStock selection based on historical data and analyst opinions

Used STOCHASTICSTM to generate and solve this stochastic programming model• StochSim to simulate equity returns• GSPL model(s) formulation (selected by user)• StochGen / StochOpt to create model instance and select optimal portfolios• Proprietary ‘trading’ interface to generate parameters for simulation, to select

model and time windows and display optimization results

54

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Dynamic Stochastic Programme ImplementationDynamic Stochastic Programme ImplementationSimulation is crucial in the optimization process but• difficult and complex for any application

• a separate problem to model building

• needs to concentrate only on key processes (others can be derived)

Input GUI

Simulation

Tree construction

Derived assets and processes

Model

GSPL

Solver

StochOpt

Output GUI

= Application specificparameters

key

processes derived processes

scenario treeproblem formulation

results

STOCHASTICSTMStochGen

55

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Long/Short Equity Fund SystemLong/Short Equity Fund SystemInput Output

Portfolio Selection

StochGen StochOpt

Optimization

Simulation

StochSim

56

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Single Period Model Alpha 2004Single Period Model Alpha 2004--2007 10.13%2007 10.13%

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

02/0

1/20

04

02/0

3/20

04

02/0

5/20

04

02/0

7/20

04

02/0

9/20

04

02/1

1/20

04

02/0

1/20

05

02/0

3/20

05

02/0

5/20

05

02/0

7/20

05

02/0

9/20

05

02/1

1/20

05

02/0

1/20

06

02/0

3/20

06

02/0

5/20

06

02/0

7/20

06

02/0

9/20

06

02/1

1/20

06

02/0

1/20

07

02/0

3/20

07

retu

rn

Without sector constraints

With sector constraints

TOPIX

1.47%1.45%Mean turnover (per week)

4340Mean number of short stocks

6261Mean number of long stocks

0.350.35Beta

1.421.44Sharpe ratio

11.19%11.31%Volatility (p.a.)

15.84%16.31%Return (p.a.)

WithWithout

57

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

MultiMulti--Period Model Alpha 2004Period Model Alpha 2004--2007 21.18%2007 21.18%

0.00

0.50

1.00

1.50

2.00

2.50

02/0

1/20

04

02/0

3/20

04

02/0

5/20

04

02/0

7/20

04

02/0

9/20

04

02/1

1/20

04

02/0

1/20

05

02/0

3/20

05

02/0

5/20

05

02/0

7/20

05

02/0

9/20

05

02/1

1/20

05

02/0

1/20

06

02/0

3/20

06

02/0

5/20

06

02/0

7/20

06

02/0

9/20

06

02/1

1/20

06

02/0

1/20

07

02/0

3/20

07

Date

Ret

urn

Return Including Transaction Cost

Return Of Topix

7.07%Mean turnover (per week)

40Mean number of short stocks

50Mean number of long stocks

0.09Beta

1.78Sharpe ratio

12.80%Volatility (p.a.)

22.77%Return (p.a.)

58

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Credit Trading Strategies for Absolute Credit Trading Strategies for Absolute ReturnReturn

59

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Portfolios With Skewed Return DistributionsPortfolios With Skewed Return DistributionsWe have already seen that for portfolios of instruments – such as bonds – with highly skewed return distributions portfolio volatility is inappropriate as a portfolio risk measure

More appropriate is a coherent tail based risk measure such as expected shortfall

However for such risk measures the analytical tractability of the volatility of Gaussian returns is lost and multivariate returndistributions must be discretized to result in a finite number ofscenarios for computational tractability

This results in the problem of controlling discrete sampling error for portfolio decisions and returns by sample size and variance reduction

60

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Expected Shortfall Portfolio ConstructionExpected Shortfall Portfolio ConstructionThe minimization of expected shortfall (tail loss) is more appropriate to bond portfolio construction than MVO and for a specified return and also tends to reduce the resulting portfolio volatility and other risk measures as well

Following Pflug, Rockafellar & Uryasev (2000-2001) the optimization problem is based on a set of n historically resampled or simulated scenarios

The solution gives both the optimal α-level VaR , the expected shortfall and the portfolio weights in terms of the problem

αψ α( )VaR

ψ ωψ ψ ω

α∈ +∈Ω′− −∑,

1min [ ( ( ) ) ] where represents the usual x C r x Cn

constraints

61

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

The Resulting LPThe Resulting LPThis nonlinear problem can be linearized using new variables

Since linear programming is a computationally powerful technique “for the first time risk managers face the problem of finding optimal portfolios with no restriction of size, complexity or distributional assumptions” Acerbi (2007)

Similar approaches can be applied to minimize drawdown-at-risk and spectral risk measures Acerbi (2007)

ω

ω ω ψ ωα

ω ψ ω ω∈Ω

≥ ∈ Ω −

′≥ − ∈ Ω

∑1( ) 0 for the by ( )

and the ( ) ( )

z zn

z r x

replacing objective

adding constraints

62

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

0% ratings migration correlation maximum return portfolio

Efficiency Analysis Efficiency Analysis

111.1156.21Max Loss

0.69%1.11%Prob of Loss

-2.340.96VaR

12.009.10Std. Dev.

13.5814.70Exp. Shortfall

58.8840.03Exp. Excess Return

MaxReturnFundPortfolio

0%Correlation

Fund

63

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Efficiency Analysis Efficiency Analysis

0% ratings migration correlation minimum risk portfolio

97.8156.21Max Loss

0.04%1.11%Prob of Loss

-30.740.96VaR

3.229.10Std. Dev.

-26.3014.70Exp. Shortfall

40.7640.03Exp. Excess Return

MinRiskFundPortfolio

0%Correlation

Fund

64

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

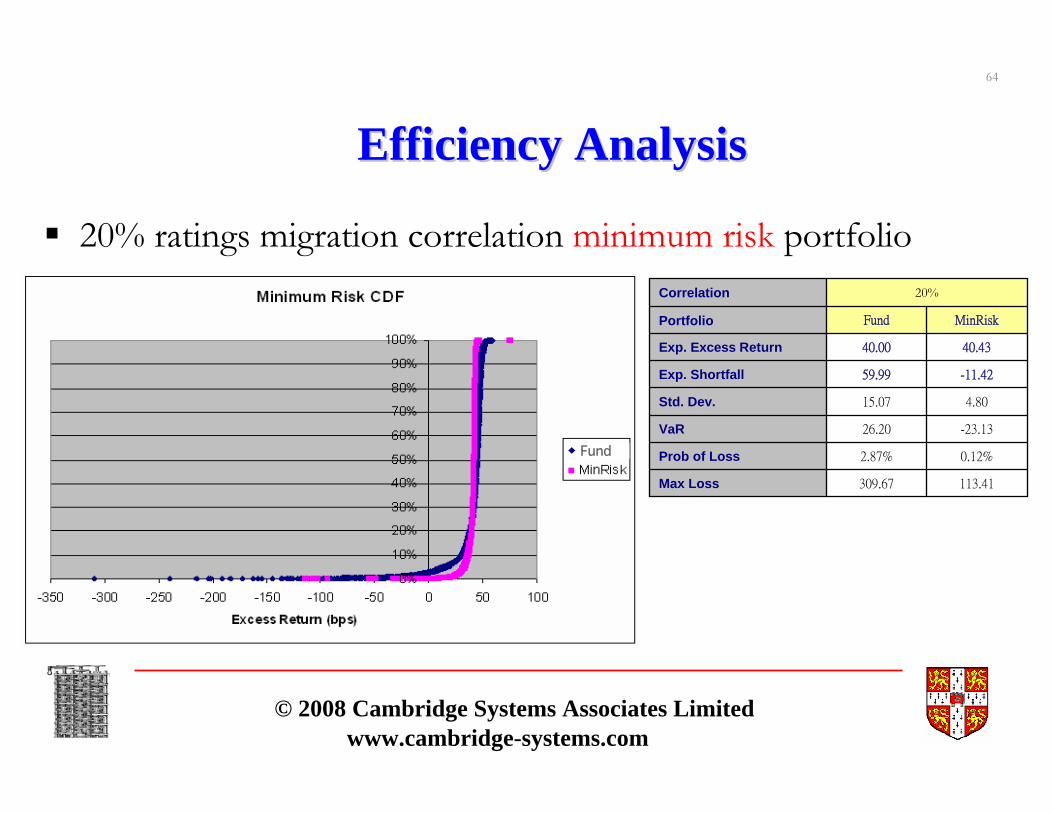

20% ratings migration correlation minimum risk portfolio

Efficiency Analysis Efficiency Analysis

113.41309.67Max Loss

0.12%2.87%Prob of Loss

-23.1326.20VaR

4.8015.07Std. Dev.

-11.4259.99Exp. Shortfall

40.4340.00Exp. Excess Return

MinRiskFundPortfolio

20%Correlation

Fund

65

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

20% ratings migration correlation maximum return portfolio

Efficiency Analysis Efficiency Analysis

244.47309.67Max Loss

1.85%2.87%Prob of Loss

19.8726.20VaR

16.7415.07Std. Dev.

60.0459.99Exp. Shortfall

60.0040.00Exp. Excess Return

MinRiskFundPortfolio

20%Correlation

Fund

66

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Efficiency Analysis: ConstraintsEfficiency Analysis: Constraints

Concentration risk limits for BBB (no ratings migration correlation) Fund vs Minimum Risk Portfolio

Banquo

-0.001

0.001

0.003

0.005

0.007

Obligor

Rat

io o

f tot

al p

ortfo

lio

LeewayPortfolio holdings

Minimum Risk Portfolio

-0.001

0.001

0.003

0.005

0.007

Obligor

Rat

io o

f tot

al p

ortfo

lio

LeewayPortfolio holdings

Fund

67

© 2008 Cambridge Systems Associates Limitedwww.cambridge-systems.com

Summary and ConclusionsSummary and Conclusions

The uses of MVO or other static optimization portfolio construction techniques depends on the tactical or trading application

We have briefly surveyed

• Portfolio performance and risk measures

• Basic MVO and its extensions

We have also outlined scenario based dynamic portfolio constructiontechniques which are applicable to strategic institutional and individual asset liability management

Such scenario based techniques have randomization advantages over alternatives in static tactical or trading applications