Risk Management

68

09 th May,2015 BHASKAR PANDA

-

Upload

irfan-mulla -

Category

Documents

-

view

9 -

download

0

description

Risk Management

Transcript of Risk Management

09th May,2015

BHASKAR PANDA

Agenda

Risk Management – An introduction

Risk Management Tools

Options

Swaps

Derivative Regulations

ISDA documentation

Client Scoping & Credit Limits

Risk Management

Risk can be defined as condition in which there is a possibility of an adverse deviation from an expected or hoped-for outcome.

Risk can adversely affect the financial position of a company. Hence, risk needs to be proactively managed.

Risk Management is an important function in which top management needs to be actively involved.

Types of Risks Business Financial – Foreign Exchange, Interest Rates, Commodities Operational Credit Liquidity Legal and Regulatory Reputational

Risk Management

Currency Exposure

Interest rate Exposure

Cross Border tradeForeign Currency Liability / Asset Liability / Asset

ImportsUSD,EUR( Capex /

Normal trade)

ExportsUSD,EUR

LoansUSD,JPY

etc

Funds/Investments/OverseasDividend from subsidiaries

Loans

(Rupee/Fcy) Deposits

Types of FX and Interest Rate Exposures

• The Risk Management process contains the some generic steps irrespective of the type of risk, organisation, or function.

There are 5 5 steps

in the RM process

Exposure Analysis

Forecasting

Benchmarking

Hedging

Reporting and review

Steps in Financial Risk Management

Exposure Analysis consists of identifying, determining the magnitude and currencies of the contracted or projected cash flows.

Exposure Analysis will need studying of the following aspects – FX cash flows - Determination of the amounts and timing. Variability of the cash flows - how certain the amounts and/or

timing are? Inflow-outflow mismatches/gaps. Time mismatches/gaps. Currency mix.

Estimation of cash flows should be made across product lines and markets to account for diversification and net exposure should be arrived.

Cash flows can either be committed i.e. those appearing on the Balance Sheet (receivables or payables or loans) and probable i.e. those anticipated to occur with a great deal of certainty.

Step 1 – Exposure Analysis

Benchmarking aims to set a minimum possible/desirable rate for the company’s exposures.

Questions to ask in benchmarking – Is it the Forward rate / Spot rate at the time of the “birth” of exposure (e.g. PO / Invoice raised)? Or is it the Forward rate / Spot rate at the time of the crystallisation of the exposure (e.g. LC opened / exports billed)? Or is it the Spot rate at the time of receiving / making the payment.

Step 2 - Benchmarking

After determining its exposures and benchmarks, an idea has to be formed as to where the market is headed in the coming months.

Forecasts beyond six months can be unreliable. The focus of forecasting is on the following –

Direction or trends in FX rates. Underlying assumptions behind the forecasts. Probability that the forecasts would come true. Possible extent of the move. Hedging will be on done the basis of such forecasts

Step 3 - Forecasting

Most visible and glamorised part of Risk Management. Role of hedging to achieve the pre-determined

benchmarks. Hedging should ideally be put into effect after

determining stop-loss levels. Hedging could one be the following –

Natural Hedging - For example, netting exports and imports or matching revenues with costs.

Hedging using financial instruments such as forwards, options, and swaps.

Step 4 – Hedging…1

Usually, the extreme strategies are not followed. Being fully open means being exposed to high risks. Being fully hedged means losing on profitable opportunities. Mostly companies are partly hedged and partly open; the proportion depends on the market forecasts and benchmarks.

Profit Centre Concept - Treasury expected to generate a net profit on the exposure over a period of time. Aggressive strategy.

Cost Centre Concept - Treasury is required to ensure that the cash-flows are not affected beyond a certain point. Defensive strategy

Hedging via options

Keeping exposure fully hedged thru Fwds

Undertaking selective hedging

Churning (booking & cancellations )

Keeping exposure fully open – Do nothing

High Risk

Low Risk

Step 4 – Hedging…2

Some practical questions while deciding a hedge policy What is our company’s hedging philosophy? Low risk, Low reward?

High risk, high reward? Or Low risk & reasonable reward? What are the hedging instruments? Do nothing ,Forwards or Options,

Hedge as a combination of forwards and options? What is our benchmark rate? Is it the Forward rate / Spot rate at the

time of the crystallisation of exposure (e.g. PO/invoice raised)? Or is it the Spot rate at the time of receiving the payment.

How much of our exposure should always be open to take advantage of sudden market movements in our favour? 20%, 30% or more ?

What should be the tenor of our hedges? 3 months, 6 months, 1 year or more? Should it cover only committed exposures or also probable ones?

If market movements is not in our favour for the open positions, what is our policy? Do we have a stop loss in mind – 50 paisa, 1 rupee or more ?

Is my competitors’ policies affecting my margins? Is he hedged at a better rate and thus my margins are getting squeezed?

Step 4 – Hedging…3

Risk management policies should be subject to review based on periodic reporting

Reports include: (a) profit/loss status on open contracts after marking-to-market (b) profitability versus benchmark (c) expected changes of overall exposures due to forecasted exchange/interest rate movements

The review analyses whether (a) benchmarks set are valid and effective in controlling the exposures (b) what the market trends are and (c) whether overall strategy is working or needs change.

Over-hedging can happen in case probable exposure does not materalise. Solution is to either rollover the hedge or to cancel it. Could result in a loss in case of the latter.

Under-hedging can happen due to incorrect forecasting or due to unanticipated market movements. Could lead to loss situation.

Step 5 – Reporting & Review…1

Emphasis on Stop Losses A firm’s risk management decisions are based on forecasts

which are but estimates of reasonably unpredictable trends. Hence it is imperative to have stop loss arrangements in order to

rescue a firm if forecasts go awry. For this, certain monitoring systems should be in place to detect

critical levels in foreign exchange rates for appropriate measures to be taken

Step 5 – Reporting & Review…2

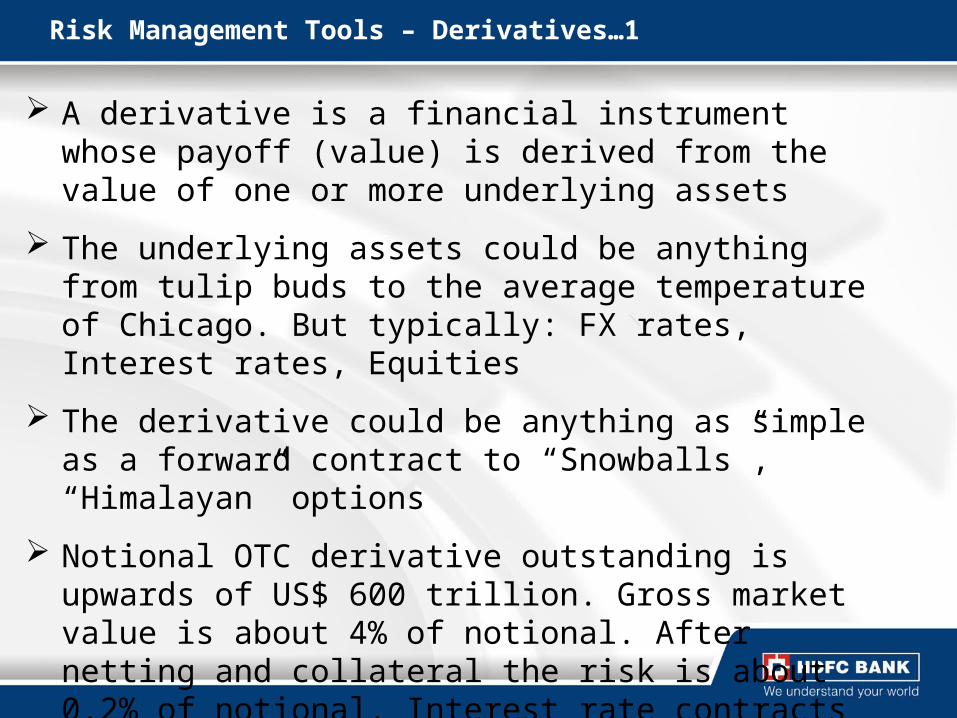

Risk Management Tools – Derivatives…1

A derivative is a financial instrument whose payoff (value) is derived from the value of one or more underlying assets

The underlying assets could be anything from tulip buds to the average temperature of Chicago. But typically: FX rates, Interest rates, Equities

The derivative could be anything as simple as a forward contract to “Snowballs”, “Himalayan” options

Notional OTC derivative outstanding is upwards of US$ 600 trillion. Gross market value is about 4% of notional. After netting and collateral the risk is about 0.2% of notional. Interest rate contracts comprise about 77% of the total followed by foreign exchange at 11%

Foreign exchange risks Forward contractsOptionsSwapsFutures Foreign borrowings / assetsCurrency swaps

Interest rate risks Interest rate swapsForward rate agreements (FRA)Caps /Floors/ Collars

Commodity price risks FuturesOptionsSwaps

Credit risks Letter of credit (L/C)Credit insuranceCredit default swaps

Risk Management Tools – Derivatives…2

Spot & Forwards

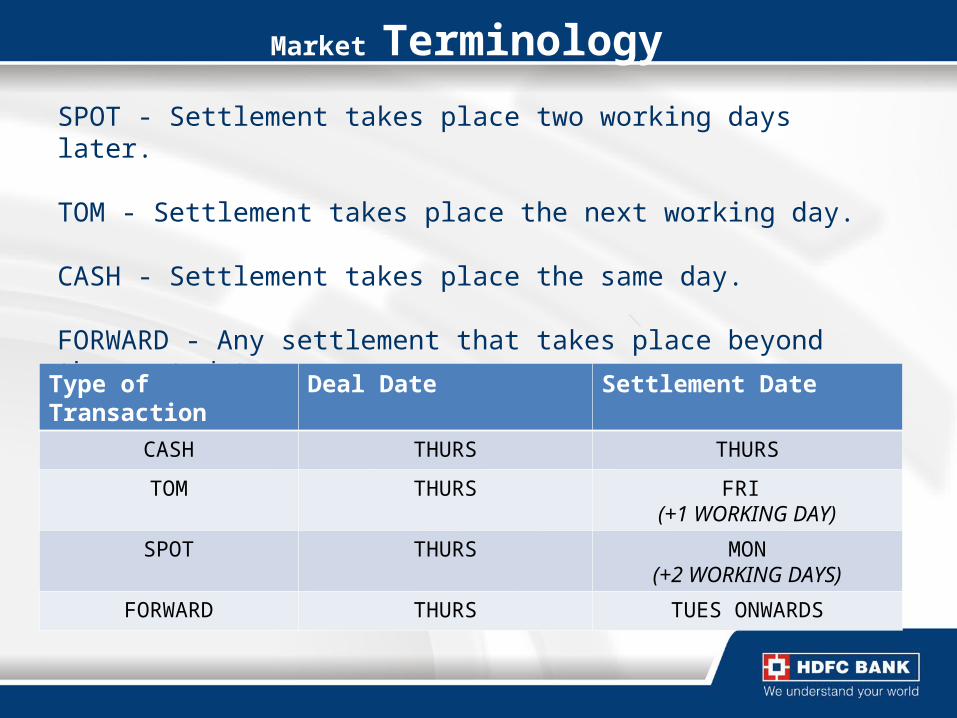

Market Terminology

SPOT - Settlement takes place two working days later.

TOM - Settlement takes place the next working day.

CASH - Settlement takes place the same day.

FORWARD - Any settlement that takes place beyond the spot date

Type of Transaction Deal Date Settlement Date

CASH THURS THURS

TOM THURS FRI (+1 WORKING DAY)

SPOT THURS MON(+2 WORKING DAYS)

FORWARD THURS TUES ONWARDS

Exchange rateExchange rate

An exchange rate is the price of one currency expressed in terms of another currency

• Base currency• Term / Variable currency

For example

1 USD = INR 64.0000 1 EUR = USD 1.1215Quotation- Rupee

A quote comprises of a Bid and an Offer

On 08 May,2015 1 USD = INR 64.00/02

You can sell USD 1 M at 64.0000 and get INR 6.40 crores for value date 12 May 2015You can buy USD 1 M at 64.02 for INR 6.402 crores for value date 12 May 2015

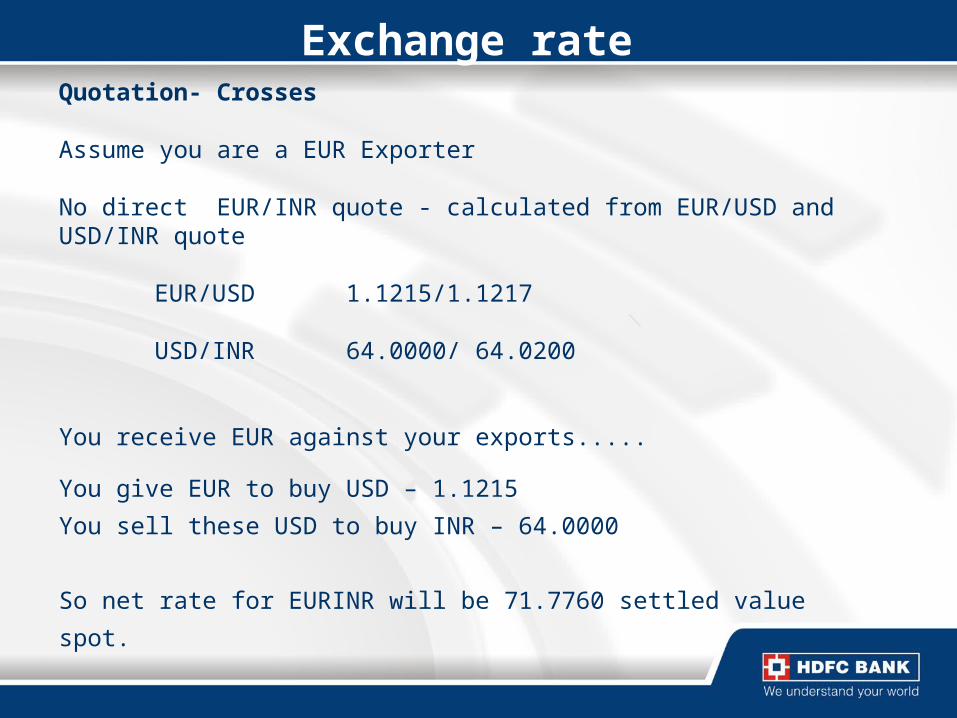

Exchange rateQuotation- Crosses

Assume you are a EUR Exporter

No direct EUR/INR quote - calculated from EUR/USD and USD/INR quote

EUR/USD 1.1215/1.1217

USD/INR 64.0000/ 64.0200

You receive EUR against your exports.....

You give EUR to buy USD – 1.1215

You sell these USD to buy INR – 64.0000

So net rate for EURINR will be 71.7760 settled value spot.

Forward Rates A forward contract is an obligation to buy or sell an agreed amount of one currency in exchange for other currency (Notional Value) for an agreed future date (Expiry Date) at an agreed exchange rate (Strike Price) for a specific underlying.•Simplest form of hedging with locked in a fixed rate for a date or a range of days•A contract once booked can be utilized in full or part prior to the defined maturity.Rationale•The structure provides an opportunity to lock into the exchange rate prior to the maturity of the underlying exposure.•It also protects the underlying from being exposed to volatilities in the spot market.•The hedge cost can be ascertained upfront and thus the end value of the underlying asset in local currency terms is known. It aids in projecting revenues and controlling costs for underlying linked to foreign exchange.Risks •It restricts participation in further exchange rate movements – you are locked into a fixed rate.•The MTM (mark-to market) of the contract will vary vs. the current market rate and could be in the money or out of the money at any point during the tenor of the contract. In the event the MTM of the contract exceeds the tolerance level indicated by the Bank it may be required to pledge incremental collateral. •In the event the underlying ceases to exist then the hedge has to be unwound at the prevailing market rate (which could be out of the money). The utilization rate of the contract prior to the maturity will be adjusted (expect for option dated contracts).

Forward Rates

When in premia they are quoted- Ex USDINR Forwards

For USD INR Spot-64.00/64.02

When in discount they are quoted Ex GBPUSD Forwards

For GBPUSD spot 1.5424/1.5426

*Pip refers to (1/10000)

Tenor Forward Premia (Paisa )

Net Rate for booking forward

1month 40/42 64.40/64.44

2 month 81/83 64.81/64.85

Tenor Forward Premia (Pips)*

Net Rate for booking forward

1 month -4.3/-4.06 1.54197/1.542194

2 month -7.8/-7.50 1.54162/1.54185

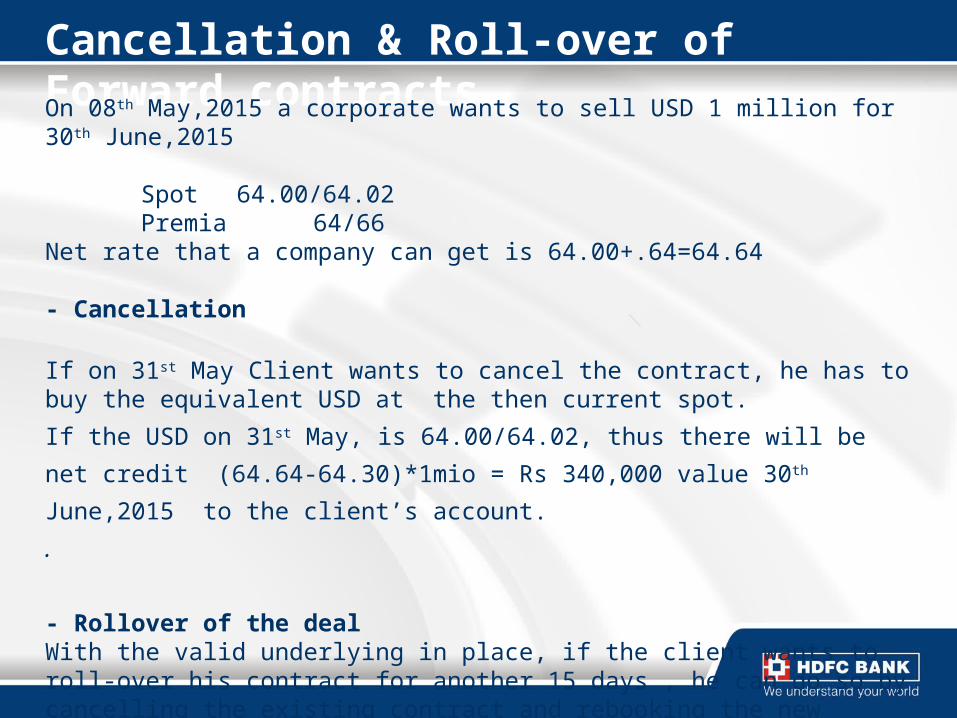

Cancellation & Roll-over of Forward contractsOn 08th May,2015 a corporate wants to sell USD 1 million for 30th June,2015

Spot 64.00/64.02 Premia 64/66

Net rate that a company can get is 64.00+.64=64.64

- Cancellation

If on 31st May Client wants to cancel the contract, he has to buy the equivalent USD at the then current spot.

If the USD on 31st May, is 64.00/64.02, thus there will be net credit (64.64-

64.30)*1mio = Rs 340,000 value 30th June,2015 to the client’s account.

.

- Rollover of the dealWith the valid underlying in place, if the client wants to roll-over his contract for another 15 days , he can do so by cancelling the existing contract and rebooking the new contract for another 15 days.

Options

Options

A Call Option is a financial derivative which gives the option holder the right but NOT the obligation to

BUY the underlying asset at a predetermined price at sometime in the future

A Call Option is a financial derivative which gives the option holder the right but NOT the obligation to

BUY the underlying asset at a predetermined price at sometime in the future

A Put Option is a financial derivative which gives the option holder the right but NOT the obligation to

SELL the underlying asset at a predetermined price at sometime in the future

A Put Option is a financial derivative which gives the option holder the right but NOT the obligation to

SELL the underlying asset at a predetermined price at sometime in the future

Options

“sometime in the future”“sometime in the future”

At a specific time in the future (Expiry)

At a specific time in the future (Expiry)

“European”“European”

At anytime in the future between now and ExpiryAt anytime in the future between now and Expiry

“American”“American”

“pre-determined price” STRIKE (X)

“underlying asset” Stock price/index, FX rates, IR…(S)

“Long” = bought, “Short” = sold

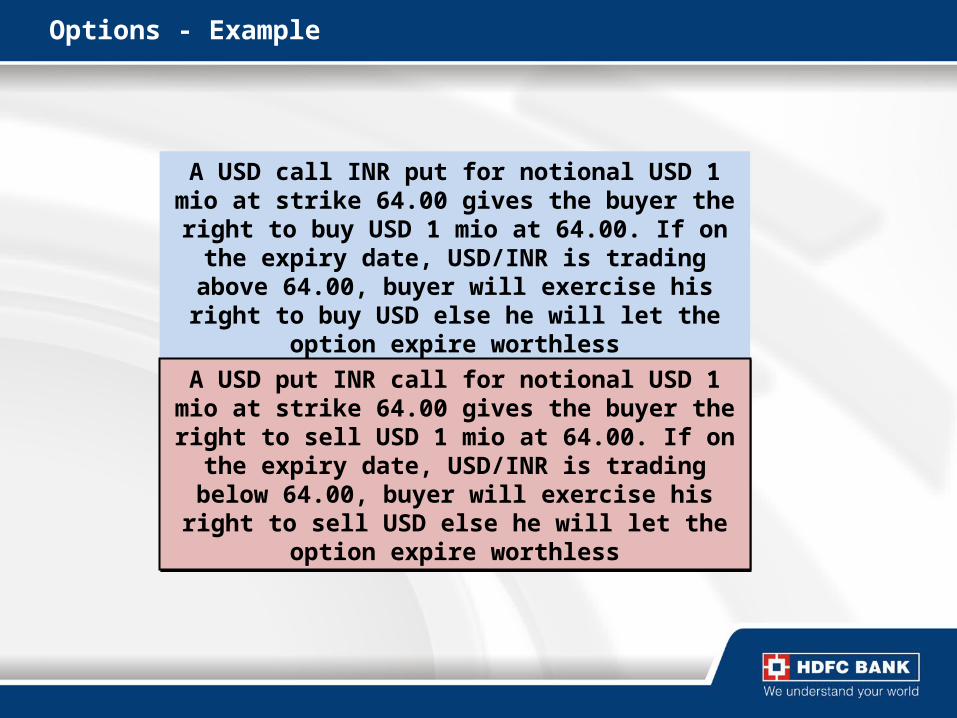

Options - Example

A USD call INR put for notional USD 1 mio at strike 64.00 gives the buyer the right to buy USD 1

mio at 64.00. If on the expiry date, USD/INR is trading above 64.00, buyer will exercise his right

to buy USD else he will let the option expire worthless

A USD call INR put for notional USD 1 mio at strike 64.00 gives the buyer the right to buy USD 1

mio at 64.00. If on the expiry date, USD/INR is trading above 64.00, buyer will exercise his right

to buy USD else he will let the option expire worthless

A USD put INR call for notional USD 1 mio at strike 64.00 gives the buyer the right to sell USD 1

mio at 64.00. If on the expiry date, USD/INR is trading below 64.00, buyer will exercise his right

to sell USD else he will let the option expire worthless

A USD put INR call for notional USD 1 mio at strike 64.00 gives the buyer the right to sell USD 1

mio at 64.00. If on the expiry date, USD/INR is trading below 64.00, buyer will exercise his right

to sell USD else he will let the option expire worthless

Understanding the payoff – Long Underlying Asset

60

Unlimited Upside Gain

…but Unlimited Downside Risk!!

65

5

payoff

Underlying (S)54

-6

Payoff – Long Call Option

64

Unlimited Upside Gain

and now… no Downside risk!!

“ the right (to buy)”

“ but NOT the obligation”

70

5

Well….almost

54

S

0

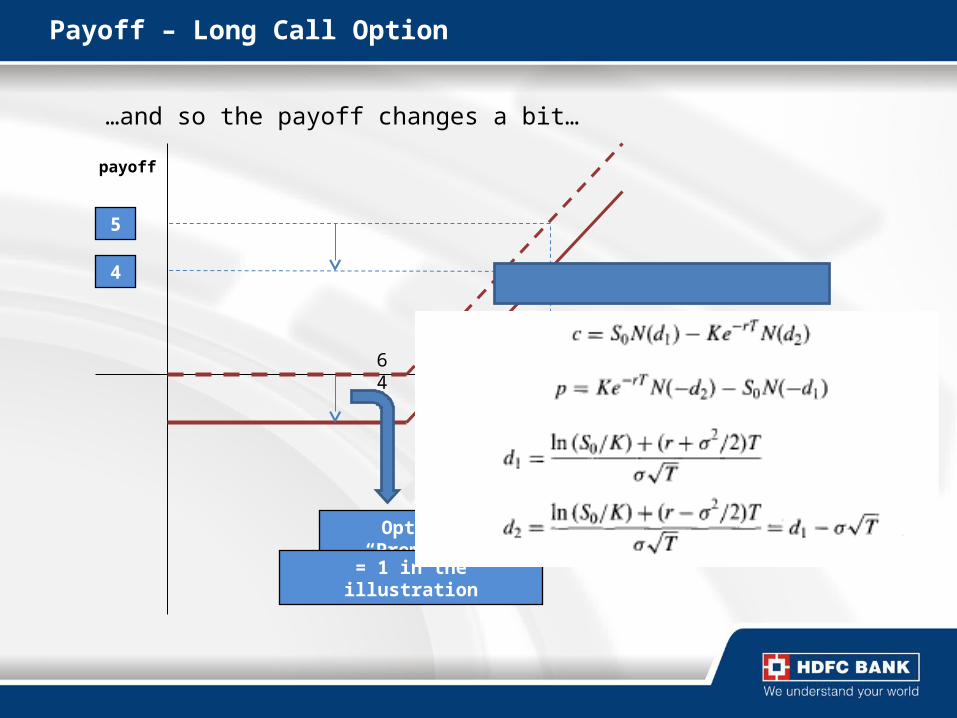

Payoff = max(S - 64, 0)Payoff = max(S - 64, 0)

Payoff – Long Call Option

64

…and so the payoff changes a bit…

65

5

4

Option “Premium”

= 1 in the illustration

payoff

S

Payoff – Long Put Option

60

The right to sell the underlying….but not the obligation

54

5

“ the right (to sell)” “ …but not the obligation”

payoff

S

Payoff = max(60 - S, 0)Payoff = max(60 - S, 0)

Payoff – Short Call, Short Put

Short Call

the Option writer has the obligation to sell the underlying to the Option holder at the Strike price

Hence limited upside (equal to the premium) but Unlimited downside risk

64

64

payoff

payoff

S

S

Short Put

the Option writer has the obligation to buy the underlying to the Option holder at the Strike price

Hence limited upside (equal to the premium) but Unlimited downside risk

FX option

Now we define the underlying asset: an FX rate, say USD/INR

payoff

Rs/USD

Strike = 60

e.g. The Call Option above on the USD/INR gives the holder the right but not the obligation to buy a Notional, say 1M USD at a rate of 60 R/$ after 12 months

Forward vs. Option Payoff

Buy Call Buy Put

X X

Payoff

Payoff

0 F

Buy Forward

Spot (S)0

F

Sell ForwardPayoff

Spot (S)

Payoff

Spot (S) Spot (S)

Vanilla Options and their Cost

Exporter Example

Spot : 64.00

1 year forward premium : 440 paise

1 year forward rate : 68.40

Option Costs

At the money Forward (ATMF) Put : Strike 68.40 : 205 paise

In the money (ITM) Put : Strike 69.00 : 233 paise

Out of the money (OTM / ATMS) Put : Strike 64.00 : 120 paise

Deeply Out of the Money (OTM) Put : Strike 58.00 : 55 paise

Buying Vanilla Options involve cash outflows for premium (mostly immediate)

Difficult to justify the costs to Management in absence of specific hedge budget

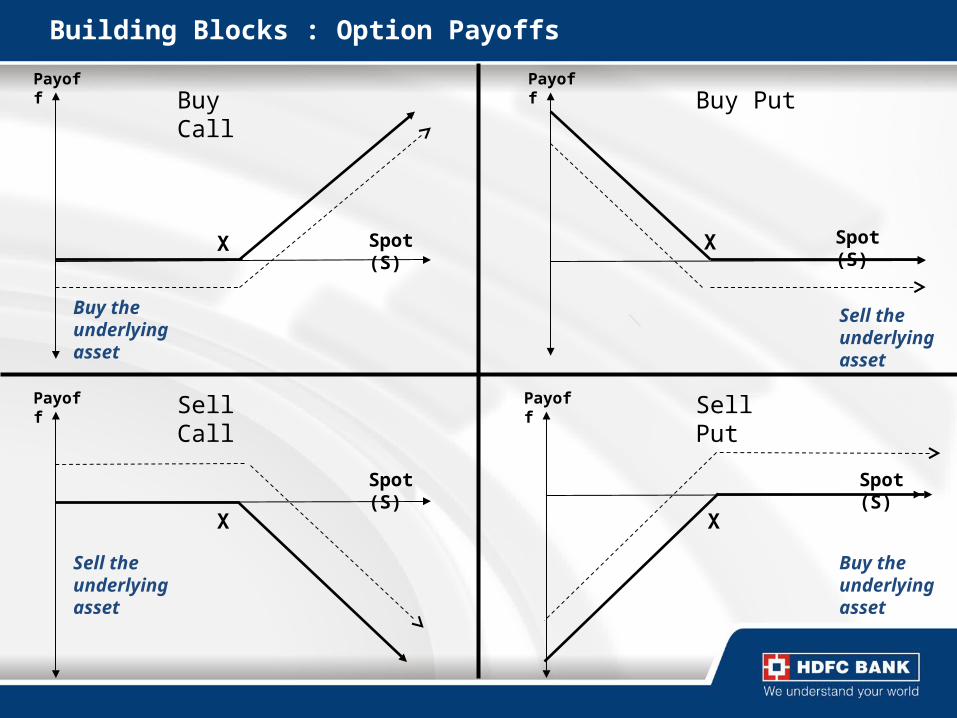

Building Blocks : Option Payoffs

Sell the underlying asset

Buy the underlying asset

X

Payoff

X

Payoff

Spot (S)

X

Payoff

Spot (S)

Spot (S)

X

Payoff

Spot (S)

Sell the underlying asset

Buy the underlying asset

Sell Call

Buy Call

Sell Put

Buy Put

Combinations (Cost Reduction Strategies)

64.00

74.00

RANGE FORWARD

Buy Put at 64.00

Sell Call at 74.00

Payoff

If Spot < 64.00 : Sell at 64.00

If 64.00 < Spot < 74.00: Sell at market

If Spot > 74.00: Obligation to sell at 74.00

Rationale

Cost effective strategy to execute the view that market shall be range-bound

(Cost of the structure : Zero Cost)

One can protect budgeted rate while gaining some more upside as compared to a forward

Range shall be larger when markets expect USDINR to go up (Calls are favoured) - Risk-reversal

Payoff

Spot (S) 0

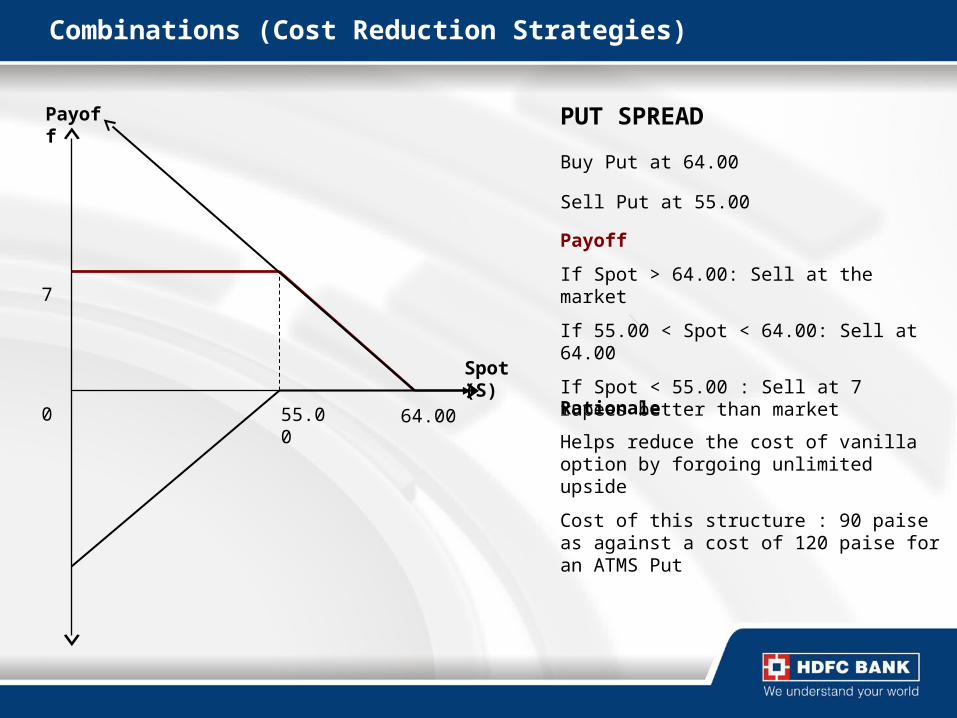

Combinations (Cost Reduction Strategies)

55.00 64.00

Payoff

Spot (S) 0

7

PUT SPREAD

Buy Put at 64.00

Sell Put at 55.00

Payoff

If Spot > 64.00: Sell at the market

If 55.00 < Spot < 64.00: Sell at 64.00

If Spot < 55.00 : Sell at 7 rupees better than market

Rationale

Helps reduce the cost of vanilla option by forgoing unlimited upside

Cost of this structure : 90 paise as against a cost of 120 paise for an ATMS Put

Swaps

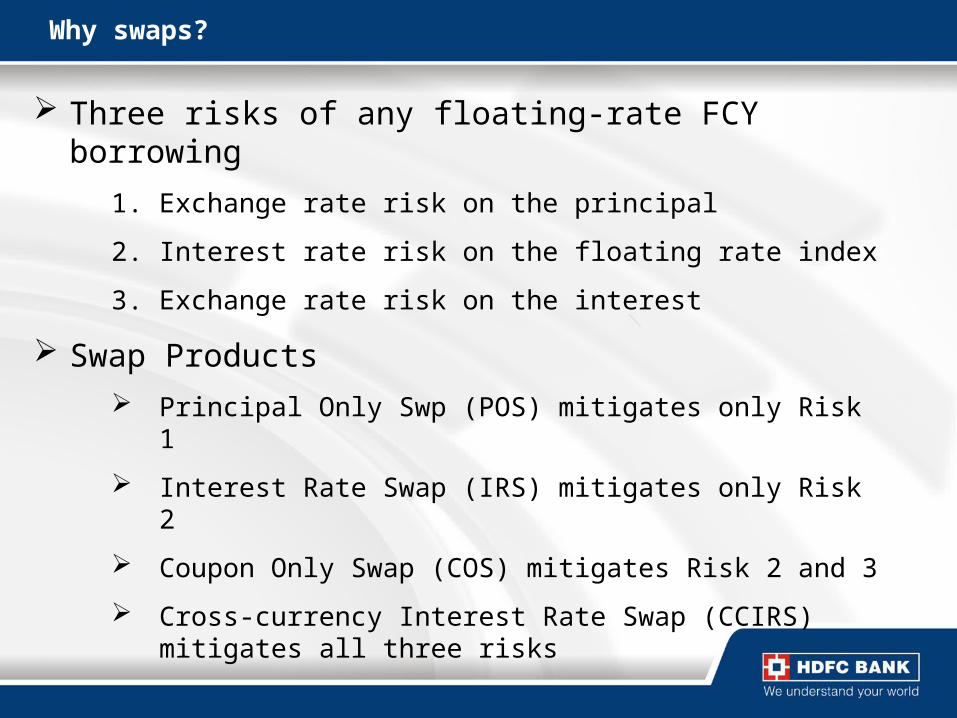

Why swaps?

Three risks of any floating-rate FCY borrowing

1. Exchange rate risk on the principal

2. Interest rate risk on the floating rate index

3. Exchange rate risk on the interest

Swap Products

Principal Only Swp (POS) mitigates only Risk 1

Interest Rate Swap (IRS) mitigates only Risk 2

Coupon Only Swap (COS) mitigates Risk 2 and 3

Cross-currency Interest Rate Swap (CCIRS) mitigates all three risks

CCIRS

CompanyCompany HDFC Bank Treasury

HDFC Bank Treasury

LenderLender

L+2.50% p.a. on USD notionalL+2.50% p.a. on USD notional

INR 620 million on repay dateINR 620 million on repay date

9.85% p.a. on INR notional9.85% p.a. on INR notional

USD 10 million on repay dateUSD 10 million on repay date

L+2.50% p.a. on USD

notional

L+2.50% p.a. on USD

notional

USD 10 million on repay date

USD 10 million on repay date

Loan details

Loan amount: $10 million

USD/INR spot: 64.00

Repayment: Bullet 5 years

Loan details

Loan amount: $10 million

USD/INR spot: 64.00

Repayment: Bullet 5 years

POS

CompanyCompany HDFC Bank Treasury

HDFC Bank Treasury

LenderLender

INR 620 million on repay dateINR 620 million on repay date

5.50% p.a. on INR notional5.50% p.a. on INR notional

USD 10 million on repay dateUSD 10 million on repay date

USD 10 million on repay date

USD 10 million on repay date

Loan details

Loan amount: $10 million

USD/INR spot: 64.00

Repayment: Bullet 5 years

Loan details

Loan amount: $10 million

USD/INR spot: 64.00

Repayment: Bullet 5 years

IRS

CompanyCompany HDFC Bank Treasury

HDFC Bank Treasury

LenderLender

L+2.50% p.a. on USD notionalL+2.50% p.a. on USD notional

4.00% on USD notional4.00% on USD notional

L+2.50% p.a. on USD

notional

L+2.50% p.a. on USD

notional

Loan details

Loan amount: $10 million

USD/INR spot: 64.00

Repayment: Bullet 5 years

Loan details

Loan amount: $10 million

USD/INR spot: 64.00

Repayment: Bullet 5 years

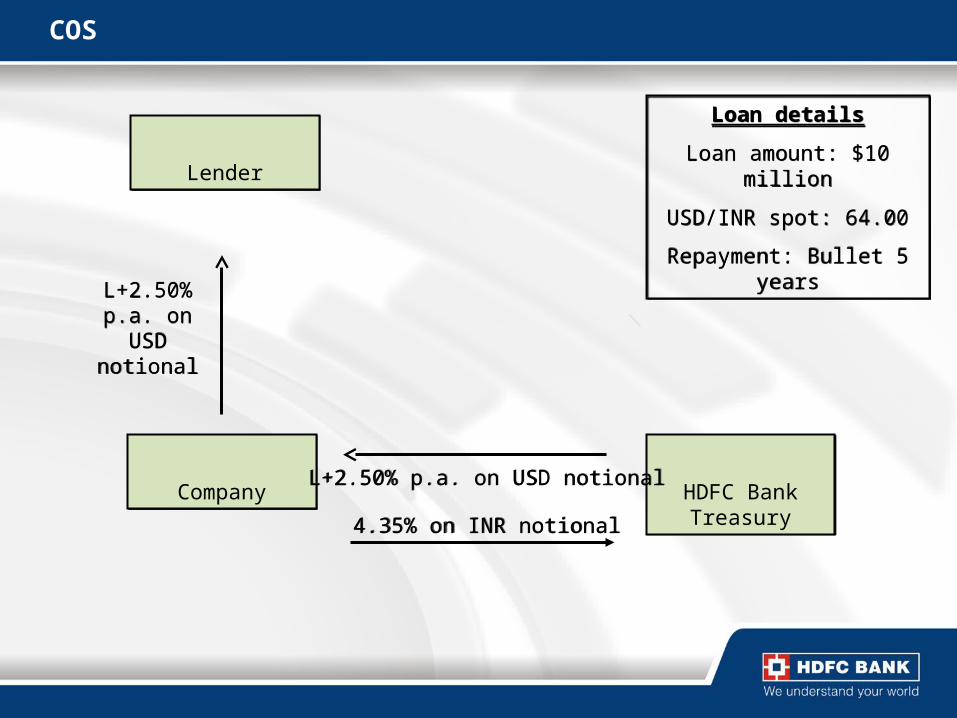

COS

CompanyCompany HDFC Bank Treasury

HDFC Bank Treasury

LenderLender

L+2.50% p.a. on USD notionalL+2.50% p.a. on USD notional

4.35% on INR notional4.35% on INR notional

L+2.50% p.a. on USD

notional

L+2.50% p.a. on USD

notional

Loan details

Loan amount: $10 million

USD/INR spot: 64.00

Repayment: Bullet 5 years

Loan details

Loan amount: $10 million

USD/INR spot: 64.00

Repayment: Bullet 5 years

Derivative Regulations

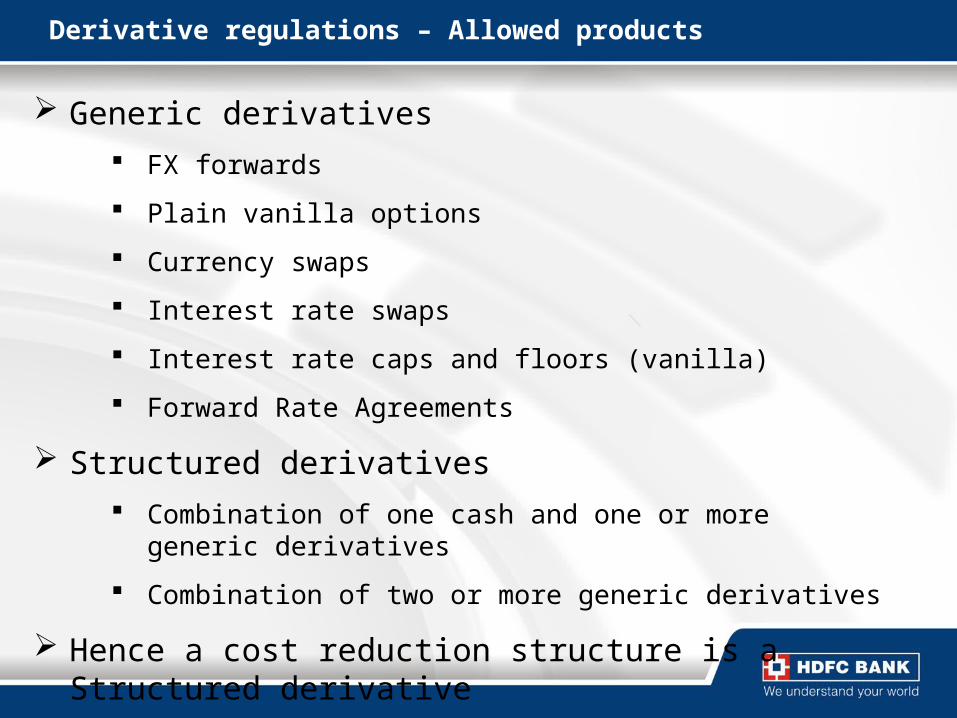

Derivative regulations – Allowed products

Generic derivatives

FX forwards

Plain vanilla options

Currency swaps

Interest rate swaps

Interest rate caps and floors (vanilla)

Forward Rate Agreements

Structured derivatives

Combination of one cash and one or more generic derivatives

Combination of two or more generic derivatives

Hence a cost reduction structure is a Structured derivative

Contracted exposures

Products allowed Forward ContractsVanilla Options, both FCY and INRCost Reduction options, both FCY and INRSwaps, both single and multi-currencyPurchase of Caps and Collars and FRA

Probable Exposure based on Past Performance

Products allowed

Forward ContractsVanilla Options, both FCY and INRCost Reduction options, both FCY and INR

Products under contracted / probable exposures

Underlying to be submitted in 15 days’ time. If not submitted within 15 days, contracts to be cancelled and gains on cancellations not to be passed on to customer.

If more than 3 instances of non-submission of underlying within 15 days in a single FY, then future contracts to be booked only on production of underlying upfront.

Annual (earlier quarterly) certificate from statutory auditor. Facility of rebooking (including rollovers) not permitted unless

exposure information submitted at beginning of FY. Where hedging done in third currency, then should be

expressly allowed by Risk Management Policy, duly approved by the Board.

Guidelines – Contracted Exposures…1

Overseas Direct Investment (equity/loan)

Exchange risk on market value to be hedged

Can be cancelled or rolled over on due dates

If hedge becomes naked in part or full, can continue up to maturity date but rollover permitted up to market value

• Dividend from subsidiary can be hedged provided that the dividend has been crystallized (for e.g. approved by shareholders in AGM)

• Hedge exchange risk of transactions denominated in foreign currency but settled in INR

To be settled in cash on maturity

Once cancelled cannot be rebooked except due to change in customs notifications.

Guidelines – Contracted Exposures…2

Allowed for hedging the probable exposure based on declaration in respect of merchandise goods as well as services.

Contracts booked during the current FY and outstanding contracts at any point of time not to exceed “the eligible limit” (for importers, only 25% of eligible limit)

The eligible limit (exports/imports) = Max (last FY exports/imports, avg. of exports/imports of last three FY).

The eligible limit to be computed and monitored separately for imports and exports.

Contracts booked in excess of 75% of eligible limit on deliverable basis only.

Contracts cancelled or rolled over or matured are blocked against the eligible limits.

Submission of audited declaration to be given by June 30.

Guidelines – Probable Exposures…1

AD banks can offer only after following conditions satisfied : An undertaking that all documentary evidence will be

produced before maturity of all contracts booked Quarterly certificate duly certified by statutory auditor

regarding amounts booked with other banks Aggregate of overdue bills to not exceed 10% of turnover

for exporter Aggregate outstanding contracts in excess of 50% eligible

limit allowed after following Statutory auditor certificate that all guidelines adhered

to while availing this facility Certificate of import/export turnover of the customer

during the past 3 years duly certified by statutory auditor

Guidelines – Contracted Exposures…2

OPTIONS

Cross currency optionsOnly buying of vanilla options allowed (subject to cost reduction facilities)Can be used for trade transactions .All guidelines of cross currency forwards also applicable.

FCY-INR Options:-Only buying of vanilla options allowed (subject to cost reduction facilities)All guidelines of FCY-INR forwards also applicableOptions can be used to hedge contingent liability arising out of submission of bid in foreign exchange

SWAPS

Both for FCY to INR and INR to FCY.Only incorporated resident entities can convert long term INR liability in to FCY subject to:-

Risk management systems of corporate

Natural hedge / economic exposureIn absence of natural hedge, only listed companies or unlisted companies with NW of the INR 200 Crs. can do after AD is satisfied about suitability and appropriateness and financial soundness of the customerOnce cancelled should not be rebooked or re-entered.

Derivative Guidelines

Copyrights © HDFC Bank Restricted

Only listed companies and their subsidiaries/JV/associates with common treasury and consolidated balance sheet OR Unlisted companies with NW of INR 200 crores provided: All products are fair valued on each reporting date Company follows section 211 of Companies Act Disclosures made in financial statements as prescribed ICAI press release

of 02 Dec 2005

Only trade transactions and ECB allowed to be hedged through cost reduction trades

Leveraged structures, digital options, barrier options, range accruals and any other not allowed

In case of trade transactions, maximum tenor allowed is 2 years For using cost reduction against past performance:

Minimum Net Worth of 200 crores Annual export and import turnover exceeding 1000 crores

Guidelines – Cost reduction structures

Documentation

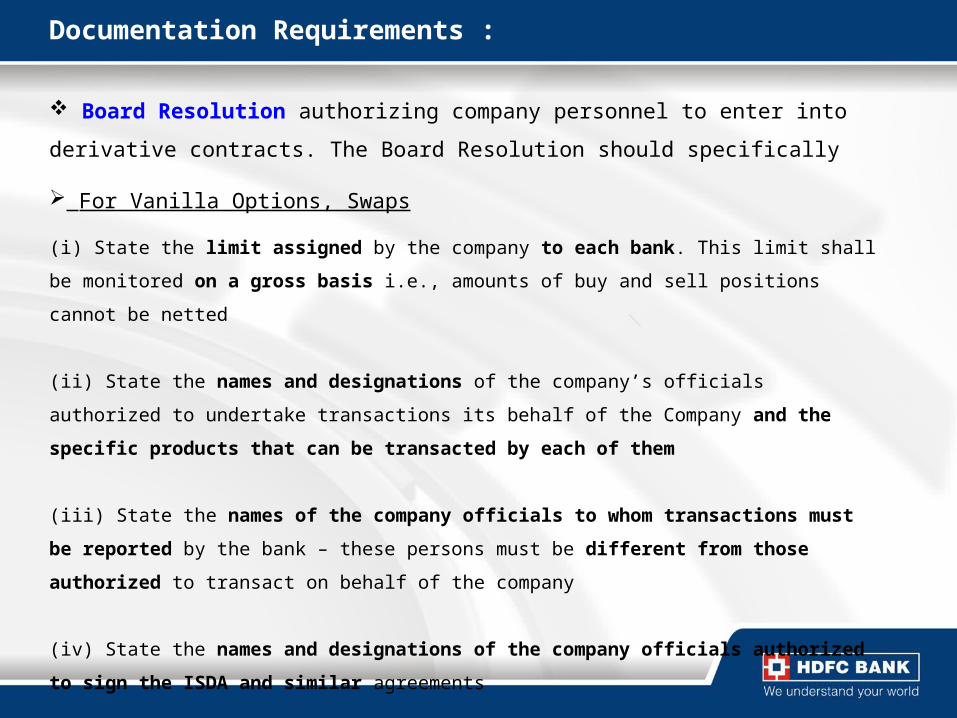

Documentation Requirements :

Board Resolution authorizing company personnel to enter into derivative

contracts. The Board Resolution should specifically

For Vanilla Options, Swaps

(i) State the limit assigned by the company to each bank. This limit shall be

monitored on a gross basis i.e., amounts of buy and sell positions cannot be netted

(ii) State the names and designations of the company’s officials authorized to

undertake transactions its behalf of the Company and the specific products that

can be transacted by each of them

(iii) State the names of the company officials to whom transactions must be

reported by the bank – these persons must be different from those authorized to

transact on behalf of the company

(iv) State the names and designations of the company officials authorized to

sign the ISDA and similar agreements

Documentation Requirements : Options

For Cost Reduction Options / Combination Structures

(i) State that the Company has in place a Board-approved Risk Management

Policy that sets out the following:

Guidelines on risk identification, measurement and control

Guidelines and procedures to be followed with respect to revaluation and monitoring of

positions

Designations of the Company’s officials authorized to undertake transactions on

behalf of the Company and limits assigned to each official on a per transaction basis

Accounting policy and disclosure norms to be followed in respect of derivative

transactions

A requirement to disclose the MTM valuations appropriately

A requirement to ensure separation of duties between front, middle and back

office

Mechanism regarding reporting of data to the Board including financial position of

transactions etc.

Documentation Requirements : Options

For Cost Reduction Options / Combination Structures…contd.

(ii) State that the Company has laid down clear guidelines for

conducting the transactions and institutionalized the arrangements for a

periodical review of operations and annual audit of transactions to verify

compliance with the regulations.

The Board Resolution (irrespective of whether for generic or structured

options) must be signed by a person different from those authorized to

transact on behalf of the Company

Risk Disclosure Statement (not required for Only Forwards)

ISDA Agreement (Master FX Agreement in case Only Forwards)

Any other documentation prescribed by the bank

ISDA documentation

ISDA documentation

ISDA – Founded in 1985. 840 members from 60 countries including HDFC Bank.

40% of members are end-users.

1987 ISDA Interest Rate Swap Agreement & 1987 ISDA Interest Rate and Currency Exchange Agreement

1992 ISDA Master Agreement

2002 ISDA Master Agreement

Introduction of Close Out Amount

Introduction of Set off clause

Schedule to the ISDA Master

ISDA clauses requiring credit approval…1

Threshold amount

Usually 3% of net worth for both parties

Linked to Cross-Default clause of ISDA Master

Specified Entities

Usually “All Affiliates” for the counterparty

Affiliates means, subject to the Schedule, in relation to any person, any entity controlled, directly or indirectly, by the person, any entity that controls, directly or indirectly, the person or any entity directly or indirectly under common control with the person. For this purpose, “control” of any entity or person means ownership of a majority of the voting power of the entity or person.”

Linked to the Default under Specified Transaction, Cross-Default, Bankruptcy and Credit Event Upon Merger clauses of ISDA Master

ISDA clauses requiring credit approval…2

Credit Support Document

Usually None

Credit Support Provider

Usually None

MTM Clause

Not necessary when only plain vanilla options are intended

Credit Covenants

Not necessary when only plain vanilla options are intended

Not an industry standard

Important to select covenants which can withstand the test of time

Scoping clients & credit limits

Identifying exposures

Identifying exposures Exports including deemed exports Imports A2 payments Local payments indexed to FCY rates ECBs / FCY loans Overseas Direct Investments Commodity hedging

Current pricing for trade products Current hedging process Current banks for trade / hedging Capital account transactions

Our USPs including RBI liaison

PSR

PSR = PFE + Negative MTM

PFE = Potential Future Exposure. Defined as the maximum expected credit exposure over a specified period of time calculated at some level of confidence

Example 15.71% for USDINR 1 year, 26.32% for EURUSD 1 year

Assume PSR blocked is 10 crores of which 6 crores is on account of PFE and 4 crores on account of negative MTM. The actual risk at any point in time is the negative MTM + a small PFE to account for time taken for the unwind of deals

DPSR and FX PSR

DPSR is not necessarily more risky than FX PSR

PSR for certain specific deals

Spot bookings for Nostro credits Money already lying with us as inward remittance has come

LC / BC / FCY loan PSR lines required for forward / option booking to mitigate FX

risk associated with the liability

INR loan In absence of USD funds, client can take INR loan and swap it

into USD mimicking a USD loan

Sole banking clients In case of sudden market movement causing huge negative

MTM, extra lines needed especially for sole banking clients or clients where a substantial portion of flows routed through us

Else client exposed to risk of being unhedged which is not good for his Balance Sheet

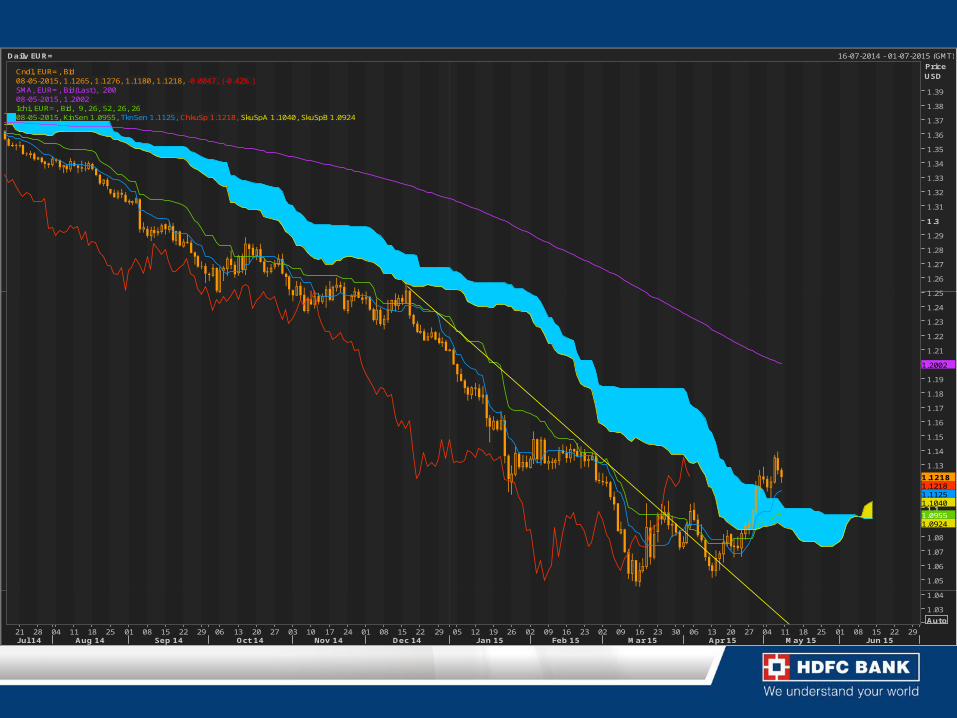

Daily EUR= 16-07-2014 - 01-07-2015 (GMT)

Cndl, EUR=, Bid08-05-2015, 1.1265, 1.1276, 1.1180, 1.1218, -0.0047, (-0.42%)SMA, EUR=, Bid(Last), 20008-05-2015, 1.2002Ichi, EUR=, Bid, 9, 26, 52, 26, 2608-05-2015, KinSen 1.0955, TknSen 1.1125, ChkuSp 1.1218, SkuSpA 1.1040, SkuSpB 1.0924

PriceUSD

Auto

1.03

1.04

1.05

1.06

1.07

1.08

1.09

1.1

1.11

1.12

1.13

1.14

1.15

1.16

1.17

1.18

1.19

1.2

1.21

1.22

1.23

1.24

1.25

1.26

1.27

1.28

1.29

1.3

1.31

1.32

1.33

1.34

1.35

1.36

1.37

1.38

1.39

1.1218

1.2002

1.0955

1.11251.1218

1.1040

1.0924

21 28 04 11 18 25 01 08 15 22 29 06 13 20 27 03 10 17 24 01 08 15 22 29 05 12 19 26 02 09 16 23 02 09 16 23 30 06 13 20 27 04 11 18 25 01 08 15 22 29J ul 14 Aug 14 Sep 14 Oct 14 Nov 14 Dec 14 Jan 15 Feb 15 Mar 15 Apr 15 May 15 Jun 15

Thank You

![Risk Management (3C05/D22) Unit 3: Risk Management · 2004. 4. 29. · Risk-management planning Risk resolution [Boehm 1991] Risk monitoring Software risk management steps & techniques](https://static.fdocuments.net/doc/165x107/6122993708b35f7a264d6759/risk-management-3c05d22-unit-3-risk-2004-4-29-risk-management-planning.jpg)