Risk and Value in Banking and Insurance - Roma Tre...

47

Università Luigi Bocconi Risk and Value in Banking and Insurance Operational Risk

Transcript of Risk and Value in Banking and Insurance - Roma Tre...

Università Luigi Bocconi

Risk and Value in Banking and Insurance

Operational Risk

Oper

atio

nal R

isk

Agenda

• Operational risk: definition • Peculiarities of operational risk • Measuring operational risk • From OR measurement to OR management • The Basel Committee capital requirements

3

OR: a definition problem

Some major banks’ definitions • “The risk that deficiencies in info systems or internal controls will

result in unexpected loss. The risks associated with human error, systems failure and inadequate procedures and controls”

• “The potential of any activity to damage the organization, including physical, financial and legal risks”

• “Risk that deficiencies in information systems or internal controls will result in financial loss, failure to meet regulatory requirements or an adverse impact on the bank’s reputation”

• “The risk of loss through inadequate systems, controls and procedures, human error or management failure”

• All risks which are not banking (ie it excludes credit, market, and trading risks, and those arising from business decisions etc.)

Oper

atio

nal R

isk

4

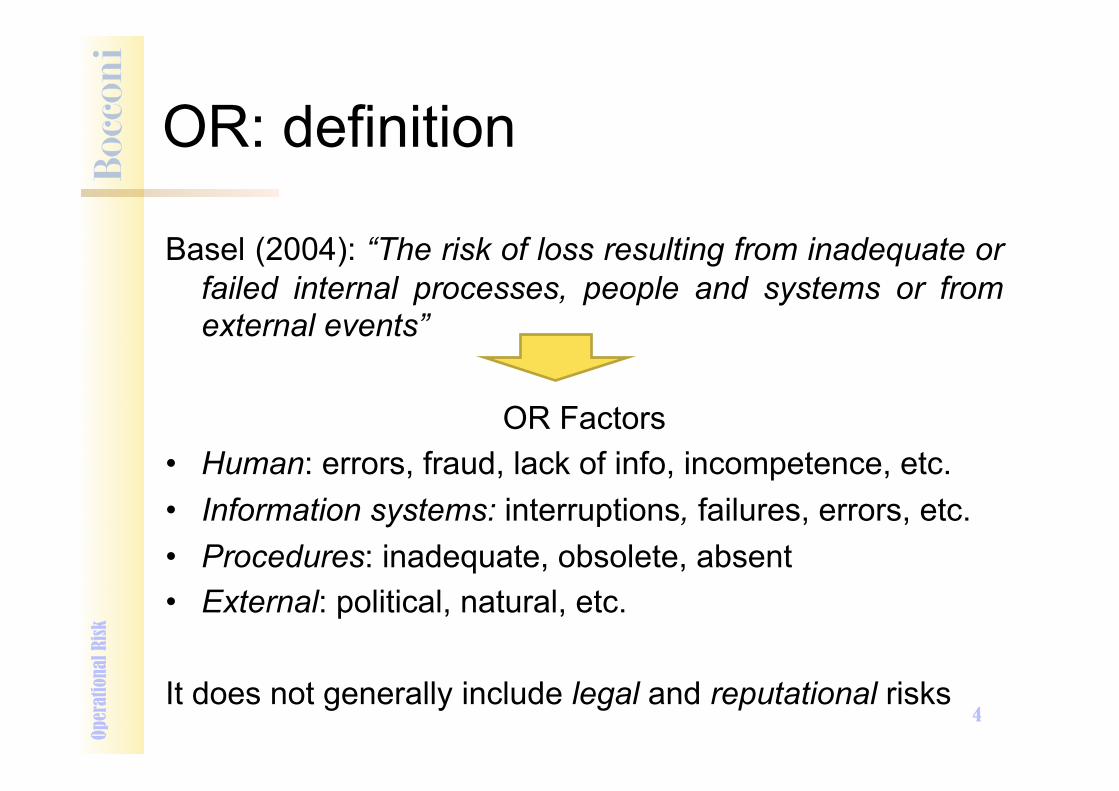

OR: definition

Basel (2004): “The risk of loss resulting from inadequate or failed internal processes, people and systems or from external events”

OR Factors

• Human: errors, fraud, lack of info, incompetence, etc. • Information systems: interruptions, failures, errors, etc. • Procedures: inadequate, obsolete, absent • External: political, natural, etc. It does not generally include legal and reputational risks

Oper

atio

nal R

isk

5

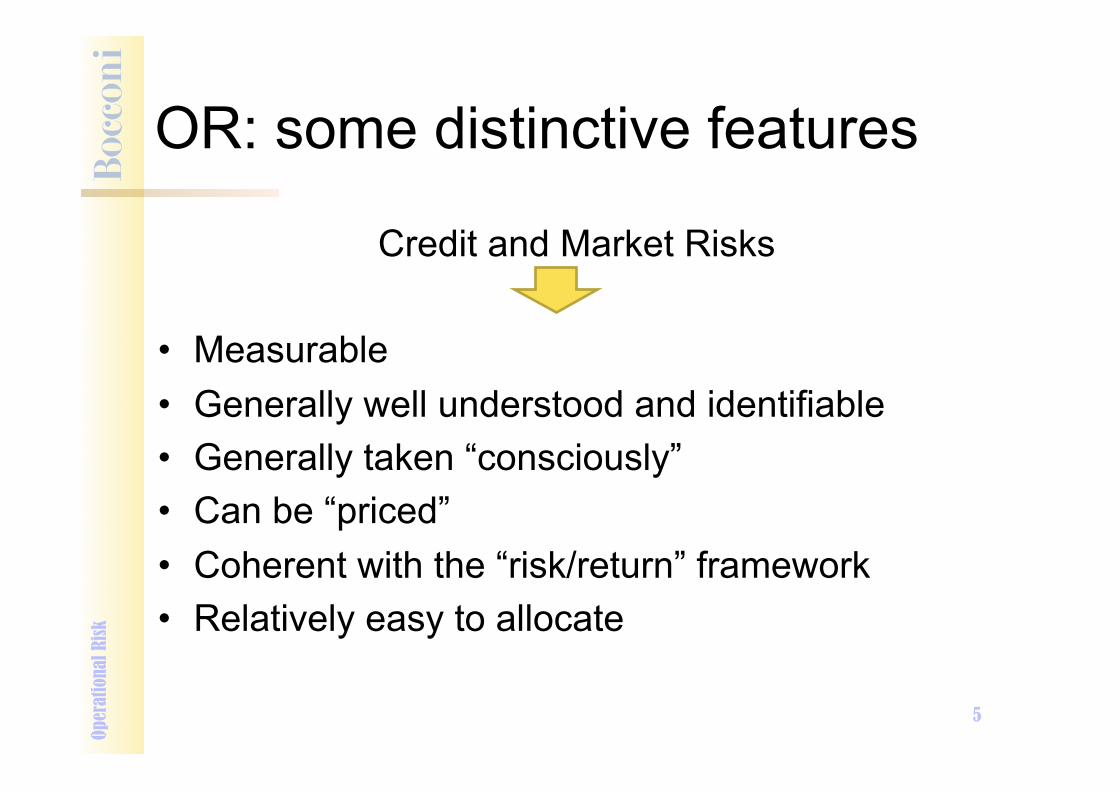

OR: some distinctive features

Credit and Market Risks

• Measurable • Generally well understood and identifiable • Generally taken “consciously” • Can be “priced” • Coherent with the “risk/return” framework • Relatively easy to allocate

Oper

atio

nal R

isk

6

OR: some distinctive features

Operational Risk

• Difficult to quantify • Generally poorly understood • Generally taken “inevitably” • Cannot be “priced” ! no liquid market • Not always coherent with the “risk/return”

framework

Oper

atio

nal R

isk

7

Measuring OR

Problems

• Some events have non-measurable consequences (e.g. loss of reputation)

• Lack of historical data • Some events are very rare (natural disasters) • History is often a poor indicator of future potential

events

Oper

atio

nal R

isk

8

Measuring OR

Two types of events

• LFHI: low frequency (rare events - low probability), high impact (severity) events (large negative consequences-losses)

• HFLI: high frequency (high probability), low impact (severity) events (low losses)

Oper

atio

nal R

isk

9

" Due to mismanagement in the day to day business activity " Can be reduced by improving efficiency/effectiveness of procedures " Expected losses can be estimated through an adequate data base

Severity

HFLI Events

" Low frequency often does not allow to understand what are the real causes behind them

" The lack of internal historical data requires to use external data sources

LFHI Events

Freq

uenc

y

Oper

atio

nal R

isk

Measuring OR

10

Measuring OR

Typical process structure 1. Identification of potential risk sources (mapping) 2. Estimate of event probability ! PE 3. Estimate of severity (amount of potential loss) !

LGE 4. Estimate of expected loss ! EL = PE x LGE 5. Estimate of unexpected loss (UL) and VaR/EC

Oper

atio

nal R

isk

11

The first step is to build up a list of potential events Example: Internal Fraud • Theft • Disruption of goods • Falsification • Identity appropriation • Tax evasion • Corruption • Insider trading • Balance sheet alteration • Functional power abuse • Collusion

Identification of risk factors Op

erat

iona

l Risk

12

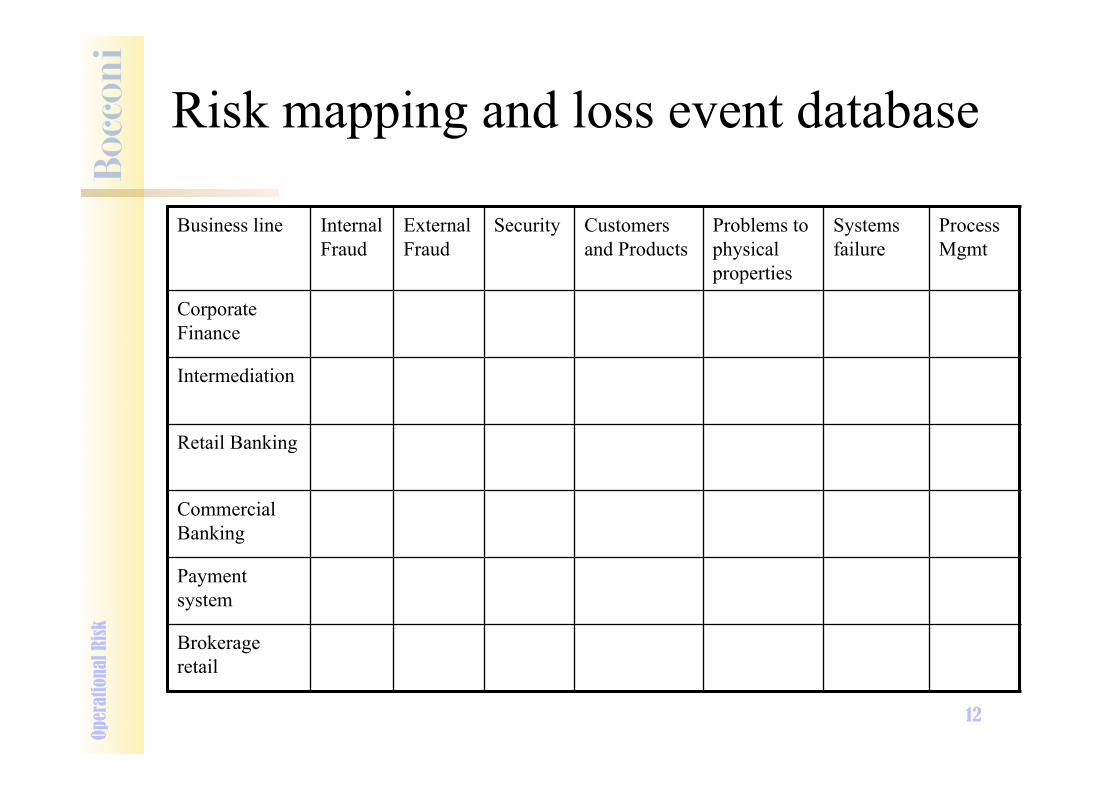

Risk mapping and loss event database

Business line Internal Fraud

External Fraud

Security Customers and Products

Problems to physical properties

Systems failure

Process Mgmt

Corporate Finance

Intermediation

Retail Banking

Commercial Banking

Payment system

Brokerage retail

Oper

atio

nal R

isk

13

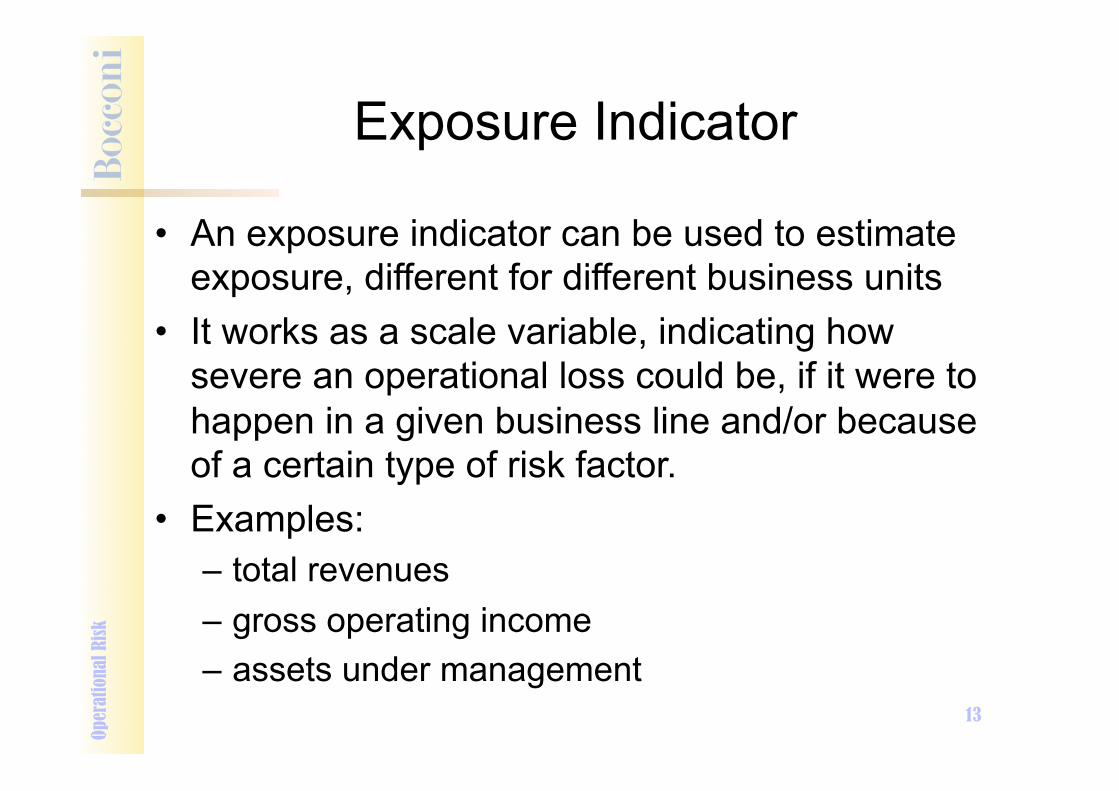

Exposure Indicator Op

erat

iona

l Risk

• An exposure indicator can be used to estimate exposure, different for different business units

• It works as a scale variable, indicating how severe an operational loss could be, if it were to happen in a given business line and/or because of a certain type of risk factor.

• Examples: – total revenues – gross operating income – assets under management

14

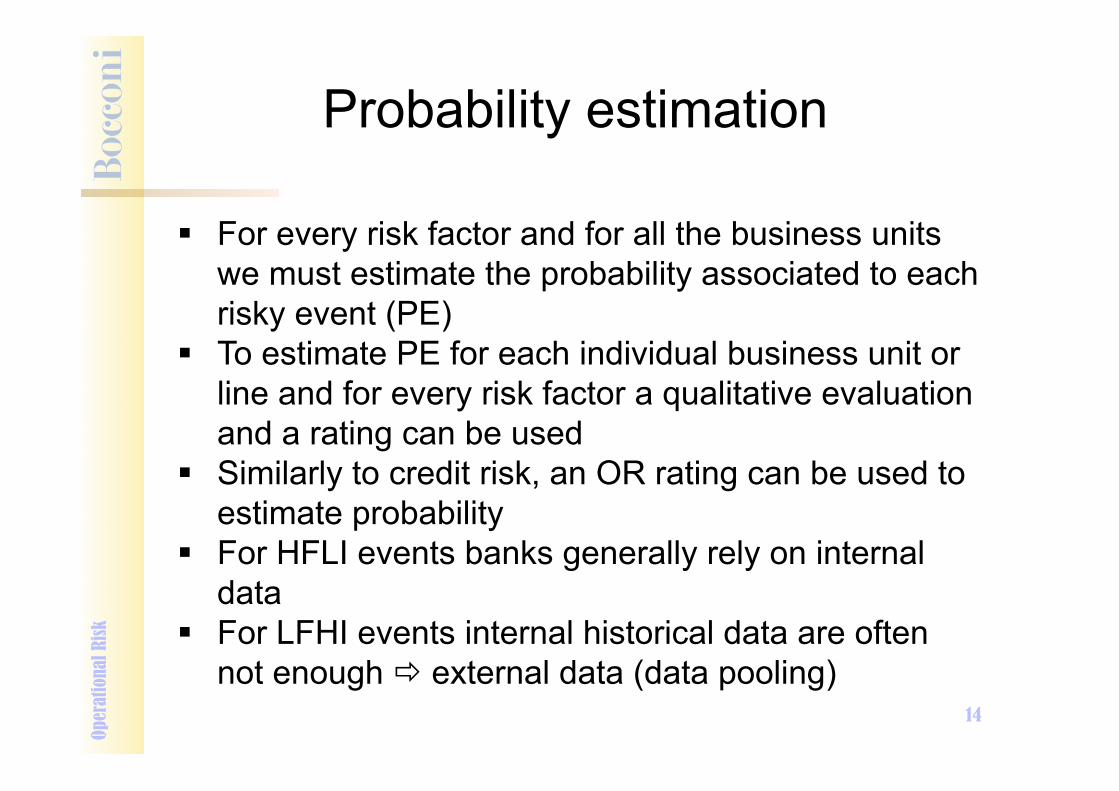

Probability estimation

" For every risk factor and for all the business units we must estimate the probability associated to each risky event (PE)

" To estimate PE for each individual business unit or line and for every risk factor a qualitative evaluation and a rating can be used

" Similarly to credit risk, an OR rating can be used to estimate probability

" For HFLI events banks generally rely on internal data

" For LFHI events internal historical data are often not enough ! external data (data pooling)

Oper

atio

nal R

isk

15

Risk factor Qualitative rank

Rating (1= low risk;

10 = high risk)

Probability range

1. Human resources

- fraud Intermediate/Low 3 0,3%-0,5%

- incompetence Intermediate 5 1,0%-2,0%

- Rule violation High 9 7,0%-10,0%

2. Technology

- systems Intermediate 4 0,5%-1,0%

- programming mistakes Intermediate/High 8 5,0%-7,0%

- telecommunication Low 2 0,1%-0,3%

3. Process

- model risk High 10 >10,0%

- transaction risk Intermediate 6 2,0%-3,0%

- documentation risk Intermediate/Low 3 0,3%-0,5%

4. External factors

- political risk Low 1 0,0%-0,1%

- regulatory/fiscal risk Intermediate/High 8 5,0%-7,0%

- natural events Low 2 0,1%-0,3%

Example Op

erat

iona

l Risk

16

Internal Fraud External

Fraud Employment Practices and

Workplace Safety Clients,

Products and Business Services

Damage to Physical Assets

Business Disruption

and System Failure

Execution, Delivery and

Process Management

Total

Corporate Finance 4 (0,01%) 3

(0,01%) 16 (0,06%) 15

(0,05%) 8 (0,03%) 1

(0,00%) 33 (0,12%) 80

(0,29%)

Trading and Sales 16 (0,06%) 6

(0,02%) 37 (0,14%) 112

(0,41%) 10 (0,04%) 39

(0,14%) 1.114 (4,07%) 1.334

(4,87%)

Retail Banking 593 (2,17%) 7.798

(28,49%) 579 (2,12%) 1.273

(4,65%) 837 (3,06%) 570

(2,08%) 6.807 (24,87%) 18.457

(67,43%)

Commercial Banking 93 (0,34%) 1.180

(4,31%) 55 (0,20%) 66

(0,24%) 285 (1,04%) 474

(1,73%) 1.463 (5,35%) 3.616

(13,21%)

Payment and Settlement 22

(0,08%) 961 (3,51%) 9

(0,03%) 57 (0,21%) 40

(0,15%) 64 (0,23%) 752

(2,75%) 1.905 (6,96%)

Agency and Custody Services 6

(0,02%) 7 (0,03%) 12

(0,04%) 69 (0,25%) 17

(0,06%) 11 (0,04%) 356

(1,30% 478 (1,75%)

Asset Management 4 (0,01%) 4

(0,01%) 21 (0,08%) 35

(0,13%) _ 6 (0,02%) 360

(1,32%) 430 (1,57%)

Retail Brokerage 7 (0,03%) 2

(0,01%) 12 (0,04%) 122

(0,45%) 28 (0,10%) 291

(1,06%) 609 (2,22%) 1.071

(3,91%)

Total 745 (2,72%) 9.961

(36,39%) 741 (2,71%) 1.749

(6,39%) 1.225 (4,48%) 1.456

(5,32%) 11.494 (41,99%) 27.371

(100,00%)

Sample: 30 international banks Number of events for each BL and type of

event Op

erat

iona

l Risk

17

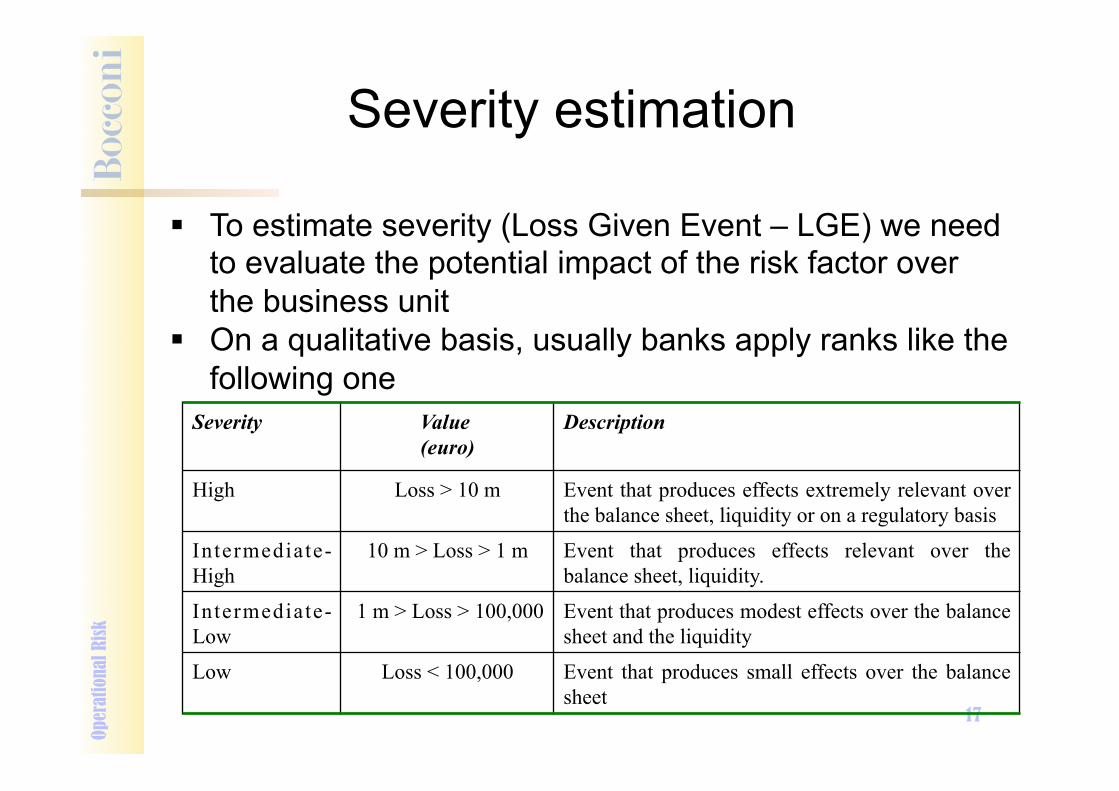

" To estimate severity (Loss Given Event – LGE) we need to evaluate the potential impact of the risk factor over the business unit

" On a qualitative basis, usually banks apply ranks like the following one

Severity estimation

Severity Value (euro)

Description

High Loss > 10 m Event that produces effects extremely relevant over the balance sheet, liquidity or on a regulatory basis

Intermediate-High

10 m > Loss > 1 m Event that produces effects relevant over the balance sheet, liquidity.

Intermediate-Low

1 m > Loss > 100,000 Event that produces modest effects over the balance sheet and the liquidity

Low Loss < 100,000 Event that produces small effects over the balance sheet

Oper

atio

nal R

isk

18

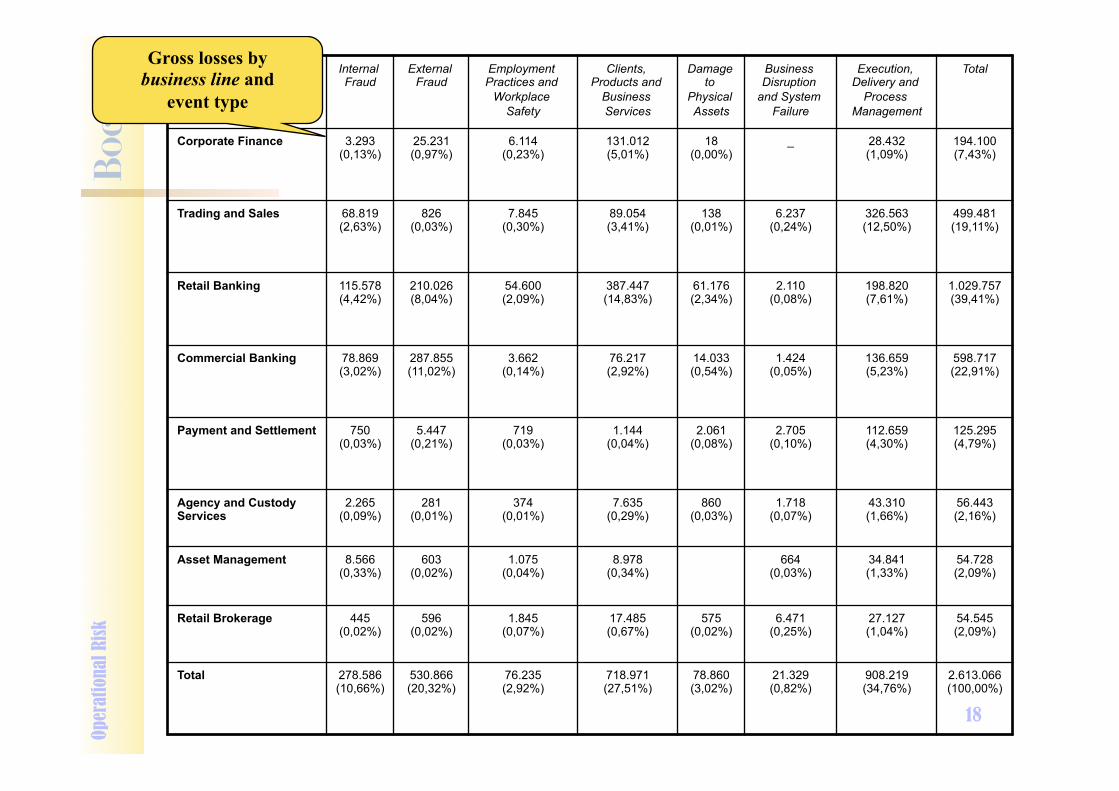

Internal Fraud External

Fraud Employment Practices and

Workplace Safety

Clients, Products and

Business Services

Damage to

Physical Assets

Business Disruption

and System Failure

Execution, Delivery and

Process Management

Total

Corporate Finance 3.293 (0,13%) 25.231

(0,97%) 6.114 (0,23%) 131.012

(5,01%) 18 (0,00%) _ 28.432

(1,09%) 194.100 (7,43%)

Trading and Sales 68.819 (2,63%) 826

(0,03%) 7.845 (0,30%) 89.054

(3,41%) 138 (0,01%) 6.237

(0,24%) 326.563 (12,50%) 499.481

(19,11%)

Retail Banking 115.578 (4,42%) 210.026

(8,04%) 54.600 (2,09%) 387.447

(14,83%) 61.176 (2,34%) 2.110

(0,08%) 198.820 (7,61%) 1.029.757

(39,41%)

Commercial Banking 78.869 (3,02%) 287.855

(11,02%) 3.662 (0,14%) 76.217

(2,92%) 14.033 (0,54%) 1.424

(0,05%) 136.659 (5,23%) 598.717

(22,91%)

Payment and Settlement 750 (0,03%) 5.447

(0,21%) 719 (0,03%) 1.144

(0,04%) 2.061 (0,08%) 2.705

(0,10%) 112.659 (4,30%) 125.295

(4,79%)

Agency and Custody Services 2.265

(0,09%) 281 (0,01%) 374

(0,01%) 7.635 (0,29%) 860

(0,03%) 1.718 (0,07%) 43.310

(1,66%) 56.443 (2,16%)

Asset Management 8.566 (0,33%) 603

(0,02%) 1.075 (0,04%) 8.978

(0,34%) 664 (0,03%) 34.841

(1,33%) 54.728 (2,09%)

Retail Brokerage 445 (0,02%) 596

(0,02%) 1.845 (0,07%) 17.485

(0,67%) 575 (0,02%) 6.471

(0,25%) 27.127 (1,04%) 54.545

(2,09%) Total 278.586

(10,66%) 530.866 (20,32%) 76.235

(2,92%) 718.971 (27,51%) 78.860

(3,02%) 21.329 (0,82%) 908.219

(34,76%) 2.613.066 (100,00%)

Gross losses by business line and

event type Op

erat

iona

l Risk

19

Info sources Op

erat

iona

l Risk

Table 5 – Information sources for the measurement of OR Probability of event (PE) Loss given event (LGE)

! Internal audit reports ! Internal historical events data ! Management reports ! Experts’ opinions (Delphi techniques1) ! Vendors’ estimates ! Budgets ! Business plans

! Management interviews ! Internal historical loss data ! Historical loss data from other banks or

consortium data series ! Industry benchmark ! External estimates (consultants,

dataproviders, vendors, etc.) Source: adapted from Crouhy, Galai, Mark (2000)

1 Delphi are iterative techniques aimed at developing consensus among different people which can be used to obtain a group estimate of the probability of future events.

20

The Basel Committee Survey

0,00%

10,00%

20,00%

30,00%

40,00%

50,00%

60,00%

70,00%C

orpo

rate

Fina

nce

Trad

ing

& S

ales

Ret

ail B

anki

ng

Com

me

rcia

l

Ban

king

Paym

ent

&

Set

tlem

ent

Age

ncy

&

Cus

tody

Ass

et

Man

agem

ent

Ret

ail B

roke

rage

Business line

Ripartizione % del numero d i eventi d i perd ita e de ll'importo medio de lle perd ite per business line (30 banche - 1998-2000)

Number of loss events Gross Loss Amount

Oper

atio

nal R

isk

21

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

30,00%

35,00%

40,00%

45,00%

InternalFraud

ExternalFraud

Employmentpractices &w orkplace

safety

Clients,products &

bus.services

Damage tophysicalassets

Bus.disruption &system fail.

Execution,delivery &process

mgmt

Tipo di evento rischioso

Distribuzione % numero eventi di perdita e perdite medie per tipo di evento - Dati relativi a 30 banche (1998-2000)

Number of loss events Gross Loss Amount

The Basel Committee Survey Op

erat

iona

l Risk

22

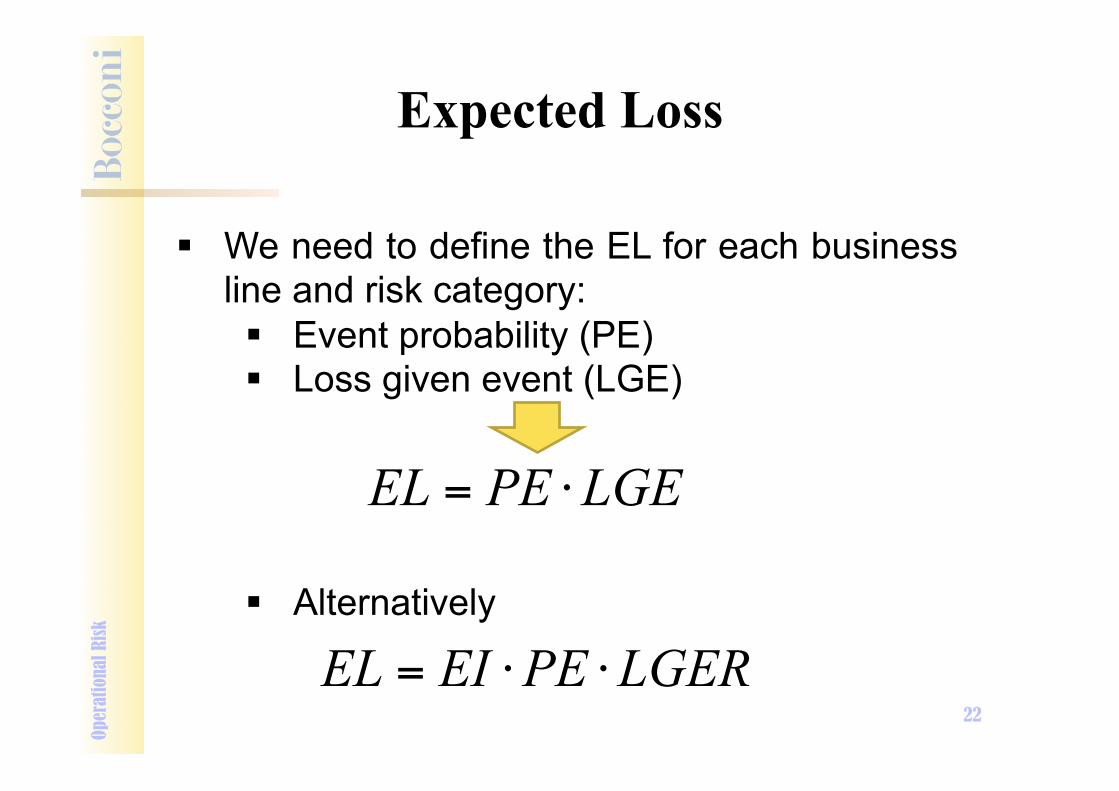

Expected Loss

" We need to define the EL for each business line and risk category: " Event probability (PE) " Loss given event (LGE)

" Alternatively

LGEPEEL ⋅=

Oper

atio

nal R

isk

LGERPEEIEL ⋅⋅=

23

Let us imagine 2 BU with the same EL but with different volatility

Business Unit A B

PE 0.2% 10%

LGE – ml euro 100 2

EL – ml euro 0.2 0.2

LFHI HFLI

Expected Loss Op

erat

iona

l Risk

24

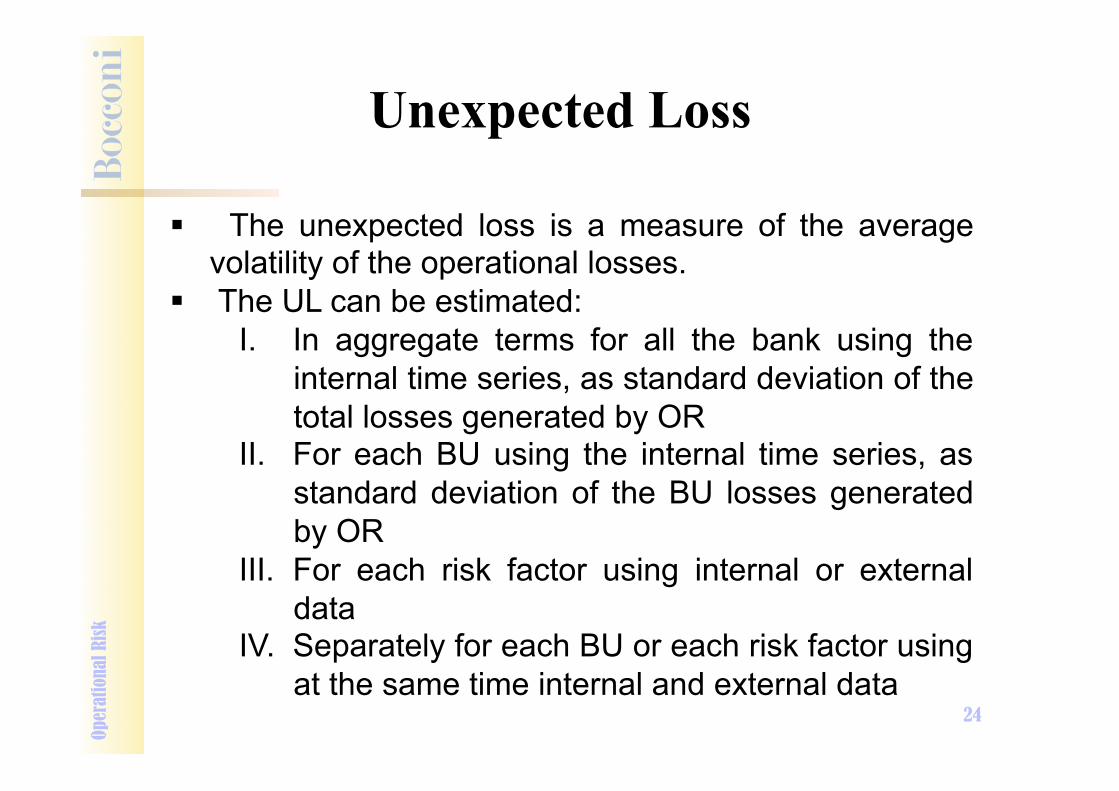

" The unexpected loss is a measure of the average volatility of the operational losses.

" The UL can be estimated: I. In aggregate terms for all the bank using the

internal time series, as standard deviation of the total losses generated by OR

II. For each BU using the internal time series, as standard deviation of the BU losses generated by OR

III. For each risk factor using internal or external data

IV. Separately for each BU or each risk factor using at the same time internal and external data

Unexpected Loss Op

erat

iona

l Risk

25

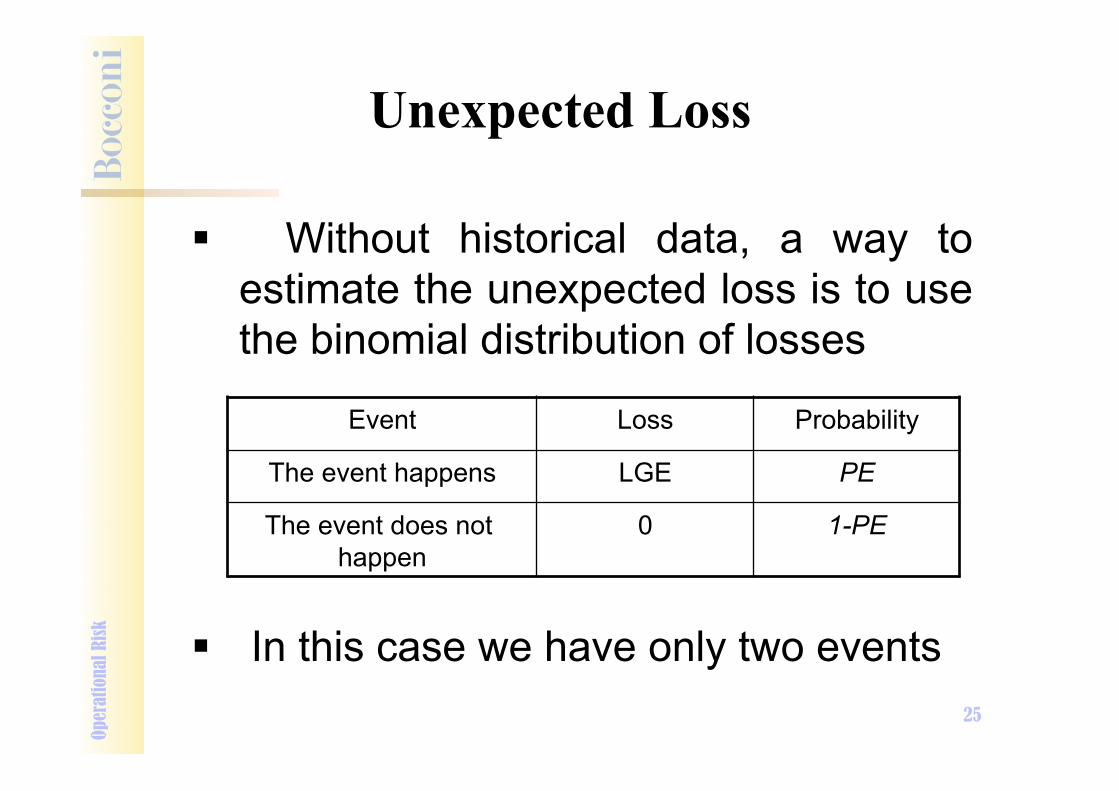

" Without historical data, a way to estimate the unexpected loss is to use the binomial distribution of losses

" In this case we have only two events

Event Loss Probability

The event happens LGE PE

The event does not happen

0 1-PE

Unexpected Loss Op

erat

iona

l Risk

26

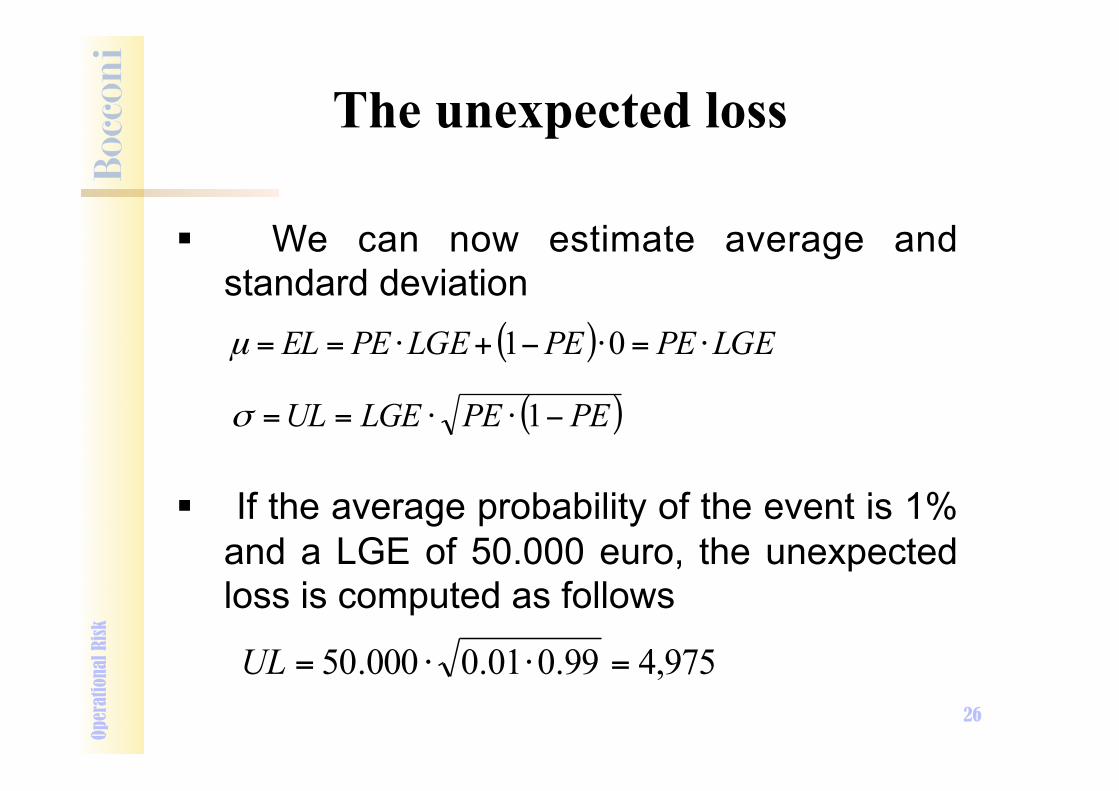

" We can now estimate average and standard deviation

" If the average probability of the event is 1% and a LGE of 50.000 euro, the unexpected loss is computed as follows

( ) LGEPEPELGEPEEL ⋅=⋅−+⋅== 01µ

( )PEPELGEUL −⋅⋅== 1σ

975,499.001.0000.50 =⋅⋅=UL

The unexpected loss Op

erat

iona

l Risk

27

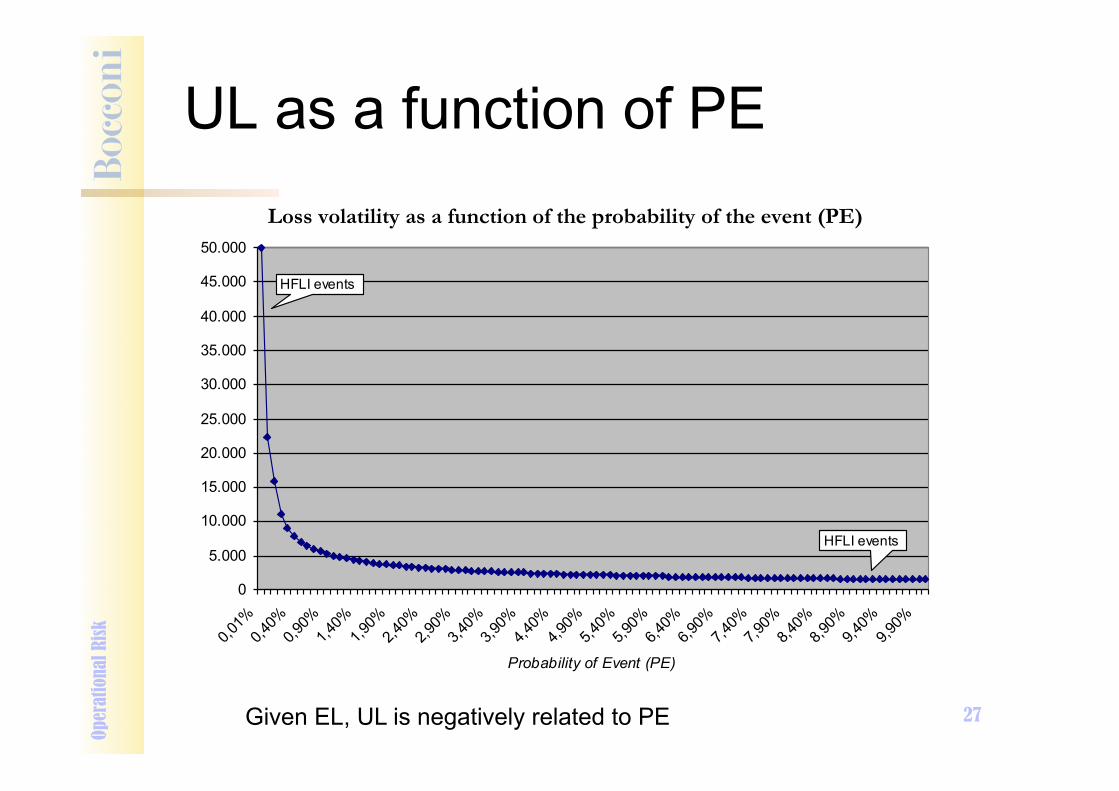

UL as a function of PE Op

erat

iona

l Risk

Loss volatility as a function of the probability of the event (PE) Unexpected loss corresponding to an expected loss of 500,000 euro

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

50.000

0,01%

0,40%

0,90%

1,40%

1,90%

2,40%

2,90%

3,40%

3,90%

4,40%

4,90%

5,40%

5,90%

6,40%

6,90%

7,40%

7,90%

8,40%

8,90%

9,40%

9,90%

Probability of Event (PE)

UL

- Eur

o 00

0s

HFLI events

HFLI events

Given EL, UL is negatively related to PE

28

" If LGE is not deterministic

If sigma LGE = 20%, PE = 1%, LGE = 50,000 UL = 11,169 euro > 4,975 euro with constant LGE

The unexpected loss Op

erat

iona

l Risk

( )( )2 2 2 21 (1 )LGE LGEPE PE LGE PE PE PEσ σ σ= ⋅ − + ⋅ + ⋅ − ⋅

( )( )2 21 LGEPE PE LGE PEσ σ= ⋅ − + ⋅

29

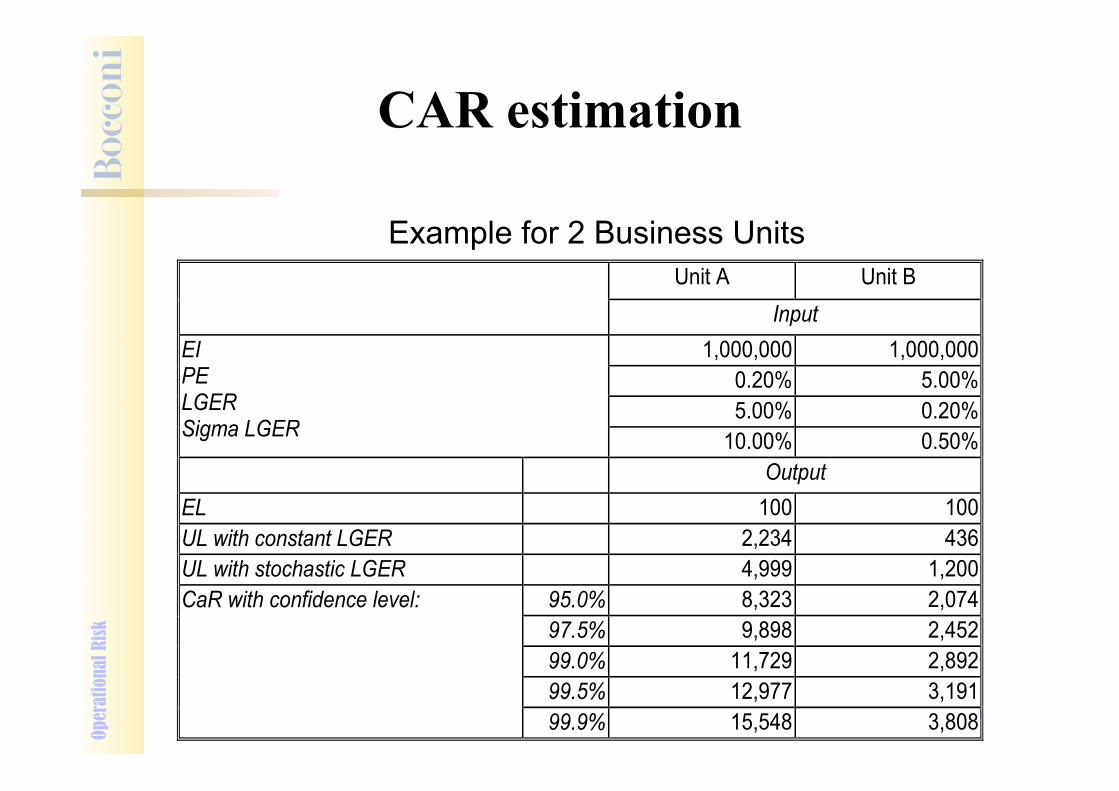

CAR estimation

" How to estimate VAR? " Starting from a functional form of RO

losses, the same for all the BU of the bank " Defining a capital multiplier to apply to the

unexpected loss " Estimating the economic capital absorbed

by each bank unit, multiplying the UL to the capital multiplier

%%, CLCLOR kULCaR ⋅=

• CaRRO,CL is the VaR under a confidence level

• kCL% is the capital multiplier.

Oper

atio

nal R

isk

30

CAR estimation Op

erat

iona

l Risk

Unit A Unit B Input

EI PE LGER Sigma LGER

1,000,000 1,000,000 0.20% 5.00% 5.00% 0.20%

10.00% 0.50% Output EL 100 100 UL with constant LGER 2,234 436 UL with stochastic LGER 4,999 1,200 CaR with confidence level: 95.0% 8,323 2,074

97.5% 9,898 2,452 99.0% 11,729 2,892 99.5% 12,977 3,191 99.9% 15,548 3,808

Example for 2 Business Units

31

CAR estimation

" OR capital at risk can also be estimated using simulation approaches

" The relative lack of historical data makes it advisable to use Monte Carlo simulations, which typically require less data than historical simulations

" Once a functional form of the OR loss distribution has been estimated or assumed, it is possible to simulate future losses associated with different scenarios and to build a simulated distribution on which the appropriate percentile can be read

Oper

atio

nal R

isk

32

OR Management

Objectives of an OR management system • Reduce the amount of OR • Eliminate the sources of OR • Allocate OR based on each BU contribution to its

generation • Give each BU an incentive to reduce it (example

through RAPM) • Estimate the amount of capital needed to support

it

Oper

atio

nal R

isk

33

OR Management

Three alternative otions " Keep: OR is kept by the bank ! typically HFLI

events " Insure: OR is �hedged� through insurance policies

! LFHI events (typically external events, where no moral hazard problem exists)

" Hedge: OR is �hedged� through investments in human resources, procedures, control systems, etc. ! HFHI events

" LFLI events are not relevant

Oper

atio

nal R

isk

34

" Active OR management can involve risk transfer or hedging tools " Insurance solutions

" e.g. rogue trading insurance " Financial solutions " Operational Risk Derivative " Catastrophe bond (CAT bonds) " OR swaps

Oper

atio

nal R

isk

OR Management

35

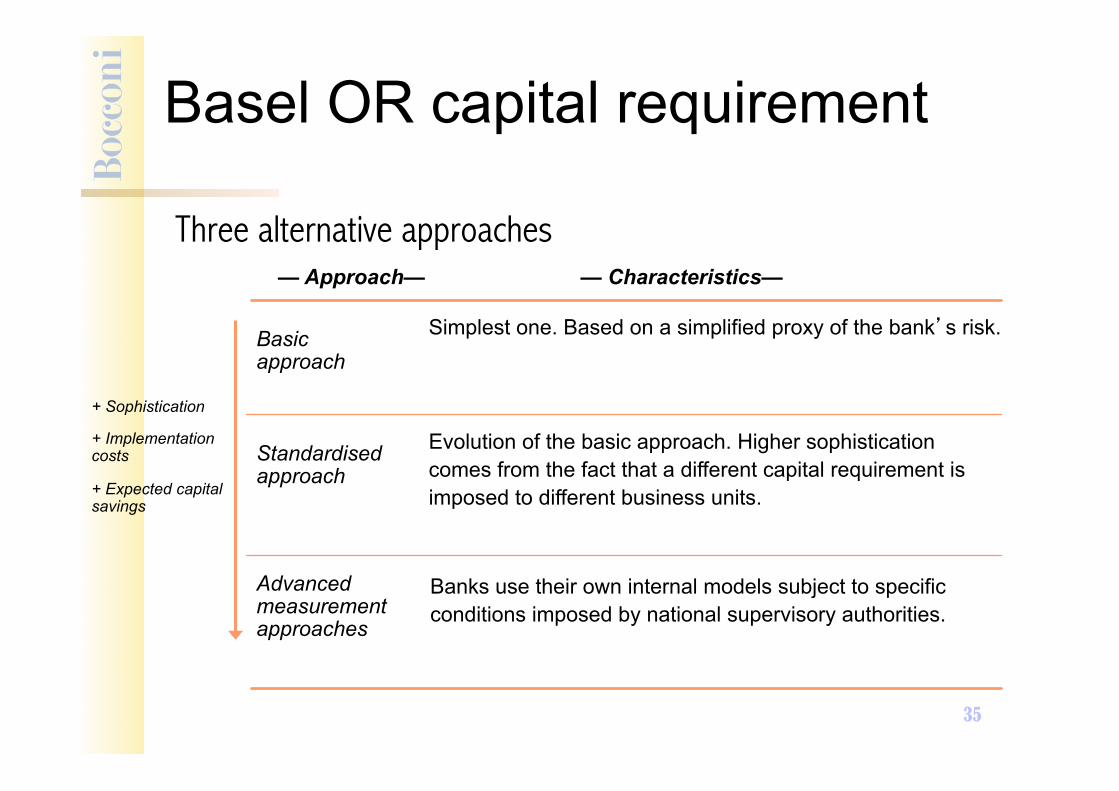

Basic approach

Standardised approach

Advanced measurement approaches

Simplest one. Based on a simplified proxy of the bank�s risk.

Evolution of the basic approach. Higher sophistication comes from the fact that a different capital requirement is imposed to different business units.

Banks use their own internal models subject to specific conditions imposed by national supervisory authorities.

Three alternative approaches — Approach— — Characteristics—

+ Sophistication

+ Implementation costs

+ Expected capital savings

Basel OR capital requirement

36

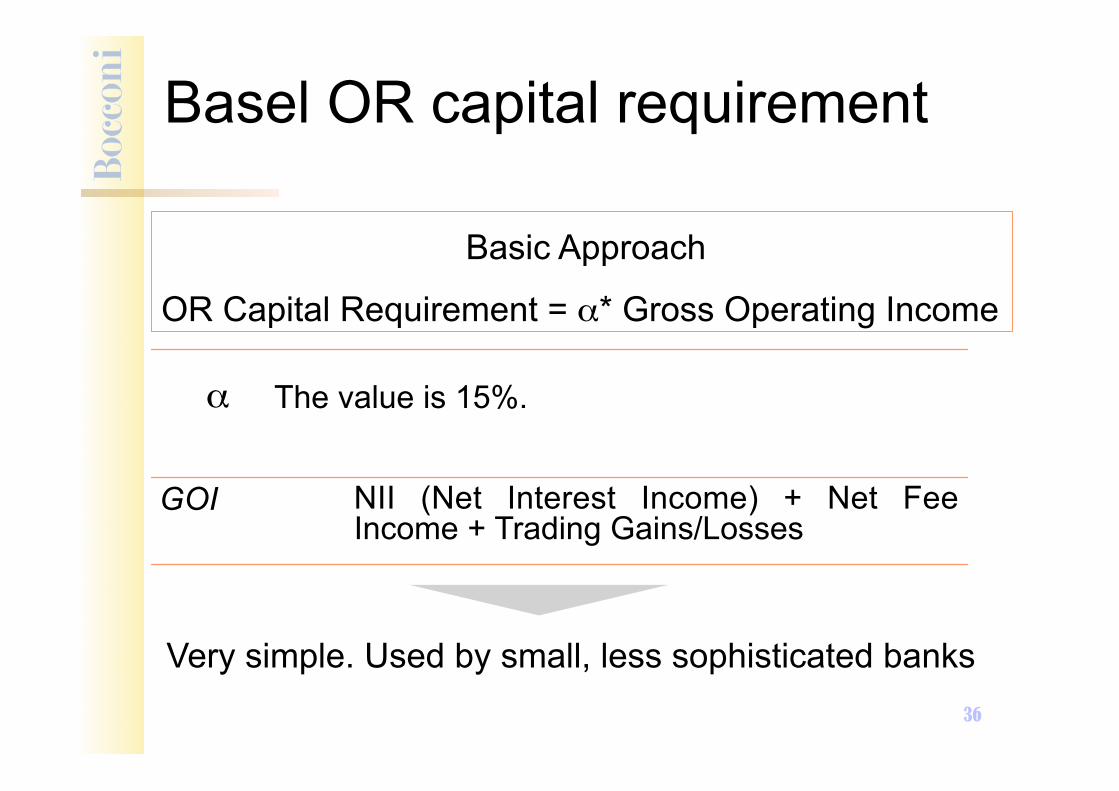

Basic Approach

OR Capital Requirement = α* Gross Operating Income

Very simple. Used by small, less sophisticated banks

α

GOI

The value is 15%.

NII (Net Interest Income) + Net Fee Income + Trading Gains/Losses

Basel OR capital requirement

37

• Each Business Line has a different β and gets its OR capital requirement

• Most large banks chose this approach

• In order to adopt this approach banks have to satisfy certain criteria related to OR mgmt

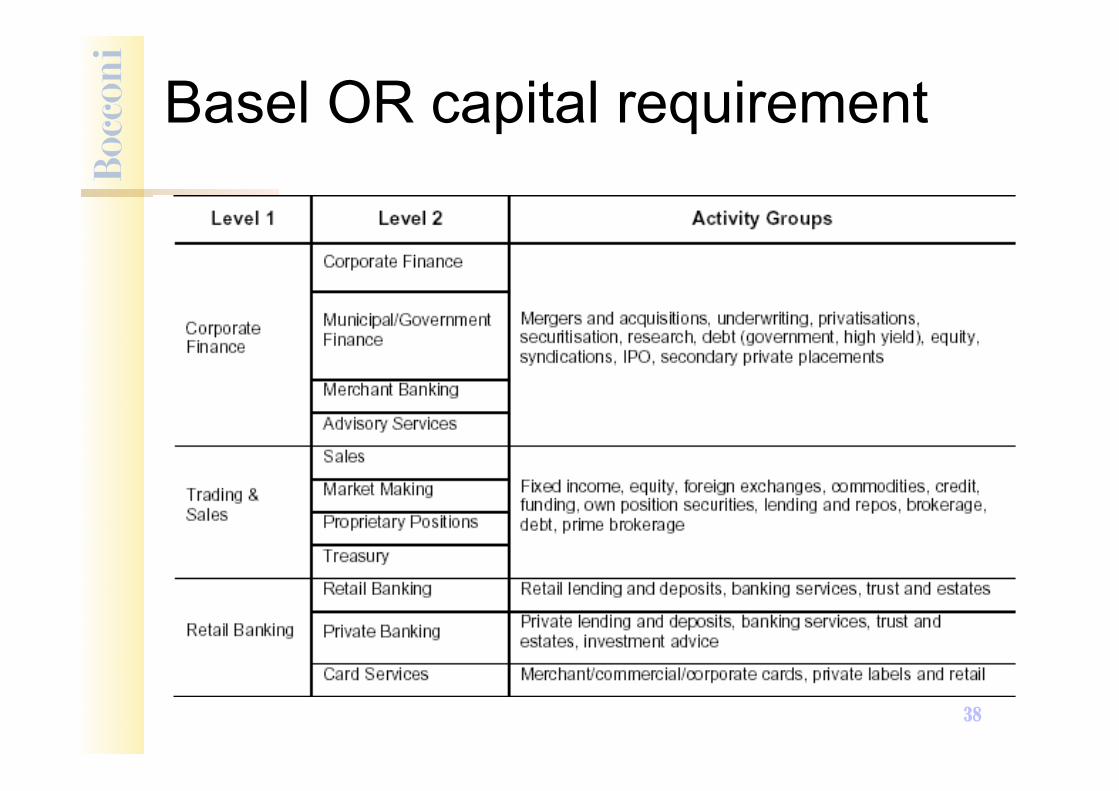

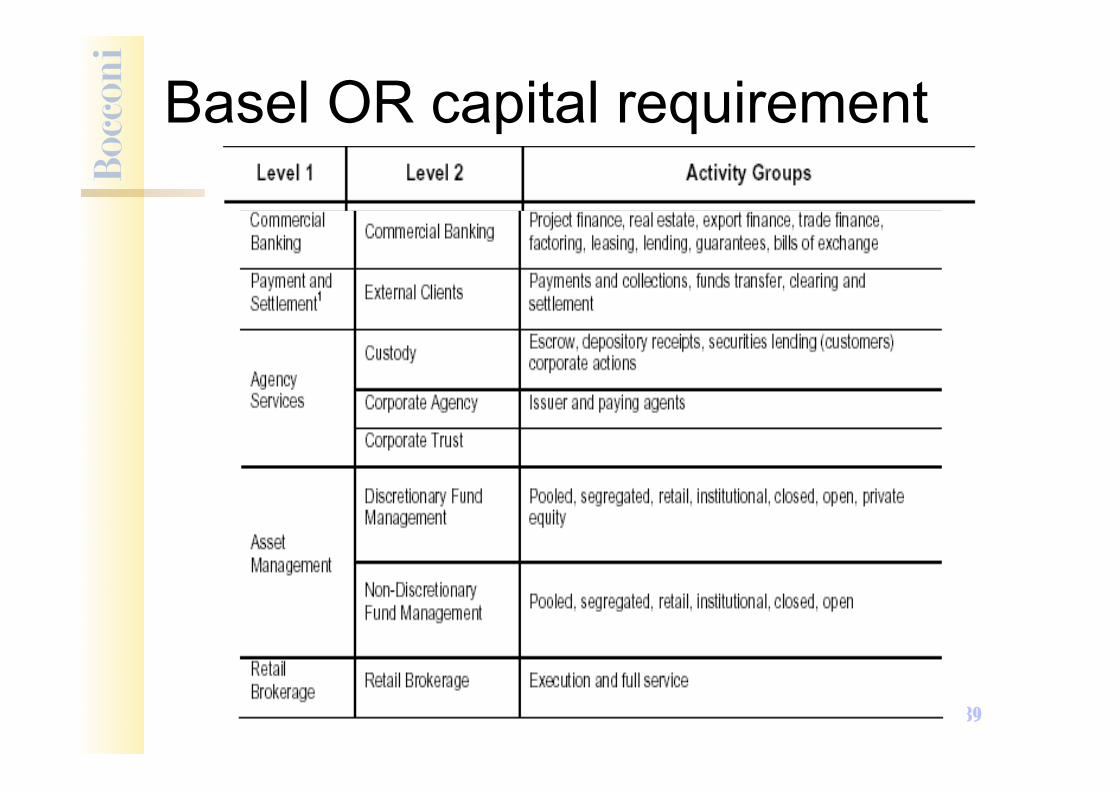

Business Unit Business Line

Corporate Finance

Trading & Sales

Retail Banking

Commercial Banking

Payment and Settlement

Agency Services and custody

Asset Management

Retail Brokerage

Investment Banking

Banking

Others

Standardized Approach OR Capital Requirement = ∑i βi * GOIi

Basel OR capital requirement

38

Basel OR capital requirement

39

Basel OR capital requirement

40

The different Beta values by Business line

BUSINESS LINE Factor Beta Corporate Finance 18% Trading & Sales 18% Retail Banking 12% Commercial Banking 15% Payment & Settlement 18% Agency Services and custody 15% Asset Management 12% Retail Brokerage 12%

Basel OR capital requirement

41

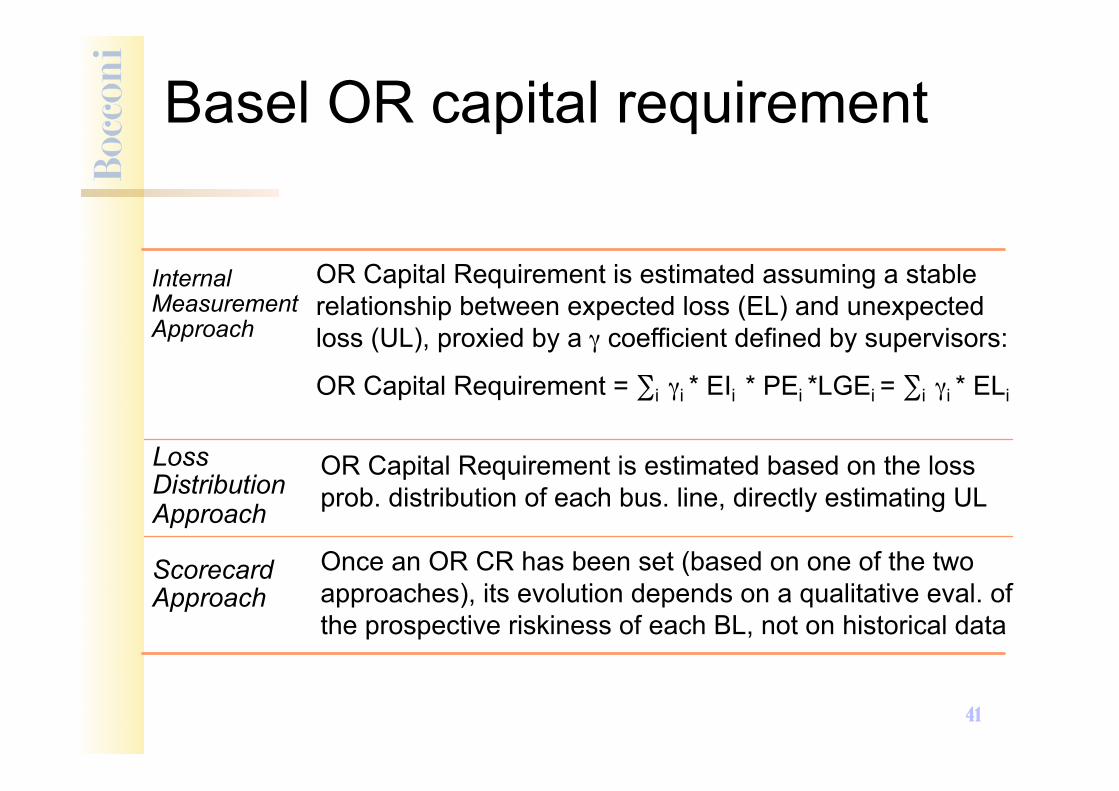

Internal Measurement Approach

Loss Distribution Approach

Scorecard Approach

Once an OR CR has been set (based on one of the two approaches), its evolution depends on a qualitative eval. of the prospective riskiness of each BL, not on historical data

OR Capital Requirement is estimated based on the loss prob. distribution of each bus. line, directly estimating UL

OR Capital Requirement is estimated assuming a stable relationship between expected loss (EL) and unexpected loss (UL), proxied by a γ coefficient defined by supervisors:

OR Capital Requirement = ∑i γi * EIi * PEi *LGEi = ∑i γi * ELi

Basel OR capital requirement

42

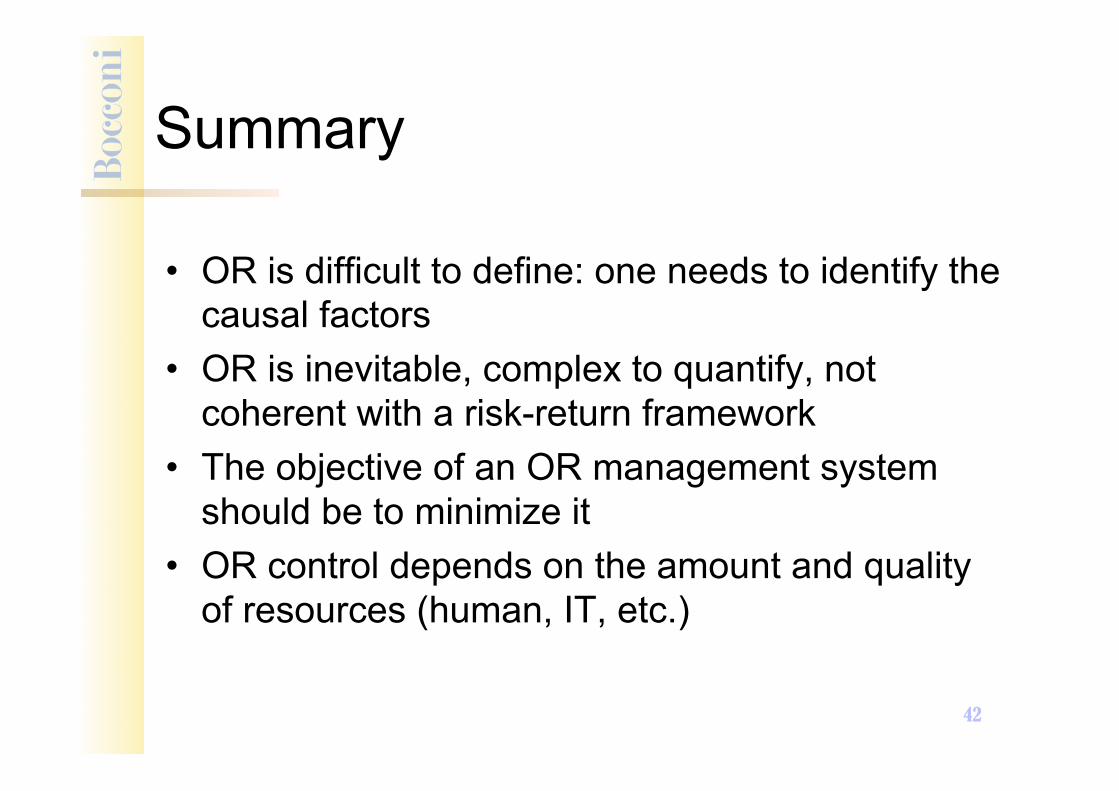

Summary

• OR is difficult to define: one needs to identify the causal factors

• OR is inevitable, complex to quantify, not coherent with a risk-return framework

• The objective of an OR management system should be to minimize it

• OR control depends on the amount and quality of resources (human, IT, etc.)

43

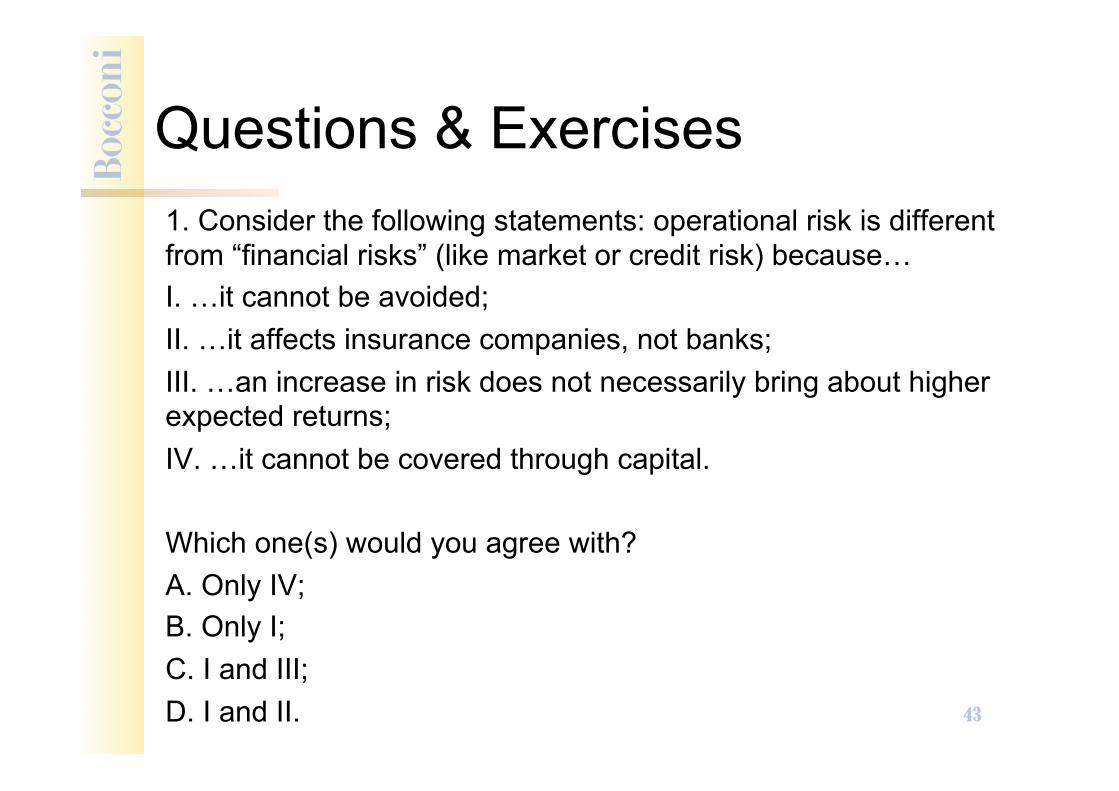

Questions & Exercises 1. Consider the following statements: operational risk is different from “financial risks” (like market or credit risk) because… I. …it cannot be avoided; II. …it affects insurance companies, not banks; III. …an increase in risk does not necessarily bring about higher expected returns; IV. …it cannot be covered through capital. Which one(s) would you agree with? A. Only IV; B. Only I; C. I and III; D. I and II.

44

Questions & Exercises

2. For each of the following loss events, indicate the risk factor(s) (people, systems, processes or external events) to which it can be ascribed: A. the tax rate on the bank’s bestselling certificates of deposit is raised from 10% to 30%, causing a drop in demand; B. some customer files are missing/incomplete and the backup data cannot be reconciled with the original ones; C. an expense item was improperly treated as tax-deductible, leading to undemating taxable profits and to evading taxes, so that the bank now has to pay a fine; D. the bank’s chief treasury officer illegally had some FX profits moved to his personal account in Monte Carlo.

45

Questions & Exercises

3. What is an exposure indicator (EI), when it comes to operational risk? A. A measure of loss experienced by the bank in the past. B. A measure of loss expected by the bank in the future. C. A scale variable, indicating how severe an operational loss could be, if it were to happen in a given business line and/or because of a certain type of risk factor. D. A parameter measuring the correlation among two different business lines and/or risk factors.

46

Questions & Exercises

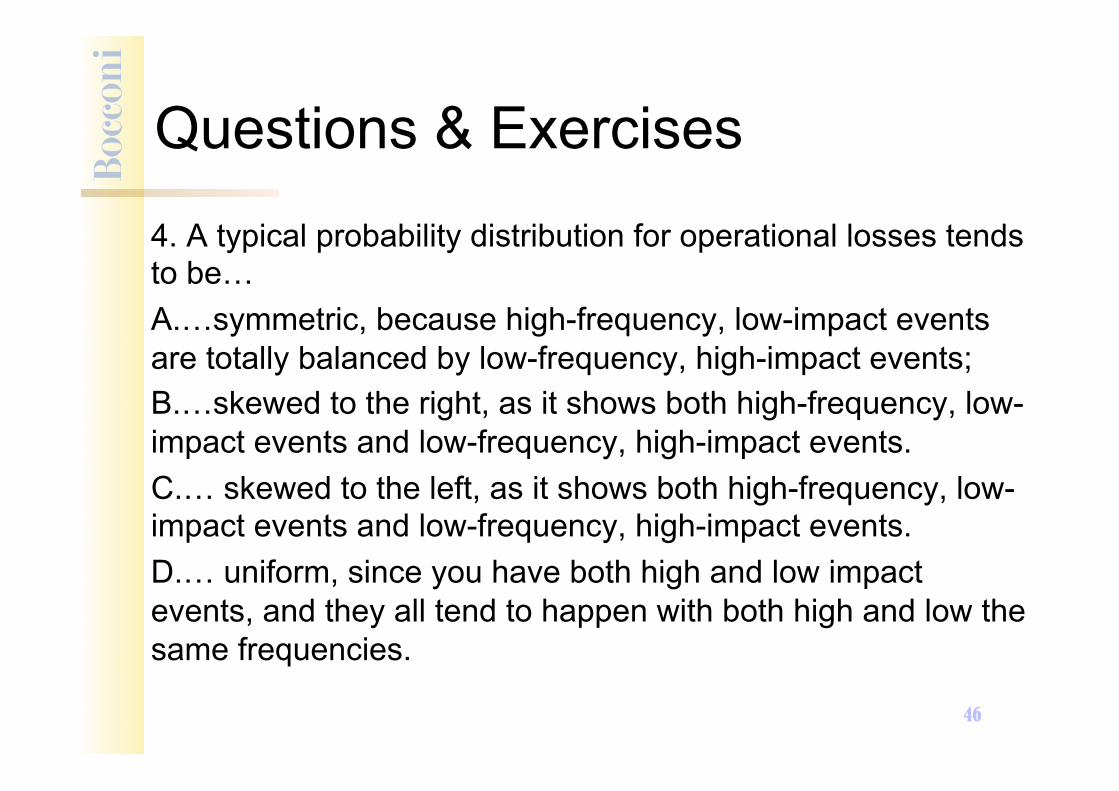

4. A typical probability distribution for operational losses tends to be… A. …symmetric, because high-frequency, low-impact events are totally balanced by low-frequency, high-impact events; B. …skewed to the right, as it shows both high-frequency, low-impact events and low-frequency, high-impact events. C. … skewed to the left, as it shows both high-frequency, low-impact events and low-frequency, high-impact events. D. … uniform, since you have both high and low impact events, and they all tend to happen with both high and low the same frequencies.

47

Questions & Exercises

5. Consider two business lines, both of which face an equal volume of expected losses (e.g., 100,000 euros) due to operational risk. The former estimates a probability of event (PE) of 1%, while the latter has a PE of 5%. The estimated volatility of Loss Given Event (LGE) is 500 euros for both business lines. Compute and compare the volatilities of the operational losses for the two business lines. What does this example teach us, regarding LFHI and HFLI events?