Revolutionizing lending in today's digital world

44

Revolutionizing lending in today’s digital world March 23, 2017

Transcript of Revolutionizing lending in today's digital world

Revolutionizing lending in today’s digital world

March 23, 2017

About our speakers:

Laura DeSoto Senior Vice President, Experian

Steve Smith CEO, Finicity

Reshma Peck Moderator, Experian

1. Today’s lending landscape

2. The role of account aggregation

3. Industry use cases

4. A look at Experian’s Digital Transaction Solutions

5. Q&A

Agenda

• Understand the opportunity to reimagine lending

• Learn how to apply it to various industries

• Discover the power of Experian’s Digital Transaction Solutions

Objective

Partnering to provide innovative solutions

User-permissioned

Access to Data

Robust Analysis

and Insights Integrated

Decisioning and

Delivery

Better Customer

Experience

&

More Efficient

Business Processes

Experian and Finicity Partnership

+ + =

Today’s lending landscape

Trends defining the banking industry in 2017 and beyond

“Long term, banks without legacy

overhangs of branch networks and

heavy ties to paper-based processing

will be advantaged, as those assets will

be increasingly less valued.”

SOURCE: http://www.businessinsider.com/these-are-the-top-trends-that-will-define-the-banking-industry-in-2017-2017-2?pt=385758&ct=Sailthru_BI_Newsletters&mt=8&utm_source=Triggermail&utm_medium=email&

utm_campaign=email_article/#1-onerous-carl-compliance-audit-risk-and-legal-costs-abate-1

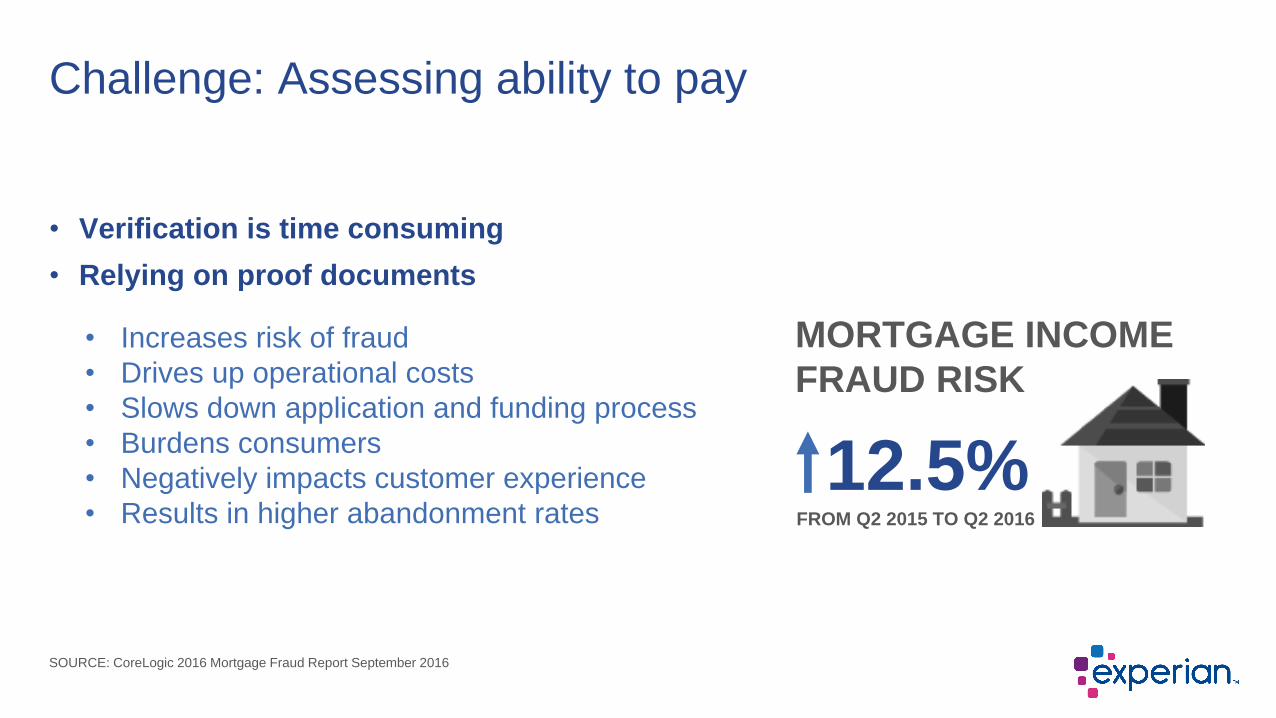

• Verification is time consuming

• Relying on proof documents

Challenge: Assessing ability to pay

MORTGAGE INCOME

FRAUD RISK

12.5% FROM Q2 2015 TO Q2 2016

SOURCE: CoreLogic 2016 Mortgage Fraud Report September 2016

• Increases risk of fraud

• Drives up operational costs

• Slows down application and funding process

• Burdens consumers

• Negatively impacts customer experience

• Results in higher abandonment rates

With the rise of “mobile financial services” consumer’s expect to be able to complete their financial transactions at the click of a button.

Challenge: Shifting consumer expectations

53% Smartphone owners

using mobile banking

28% Smartphone owners

using mobile payments

SOURCE: Federal Reserve, Consumers and Mobile Financial Services March 2016

94%

58%

56%

65%

42%

33%

Checking balances or transactions

Transferring money between accounts

Receiving an alert

Paying bills

Purchasing remotely

Purchasing in a store

“Let me state the matter as clearly as I can here: We believe consumers should be able to access [their financial] information and give their permission for third-party companies to access this information as well.”

- Richard Cordray, Director, CFPB at Money 20/20, October 2016

Challenge: Regulatory pressure

SOURCE: https://www.consumerfinance.gov/about-us/newsroom/prepared-remarks-cfpb-director-richard-cordray-money-2020/

• Financial Institutions/service providers

must create a hassle-free customer

experience.

• To do this they will need to invest

more heavily in digital capabilities and

in technology that removes paper from

the process.

Lenders are forced to adapt

https://thefinancialbrand.com/63617/digital-banking-strategies-fintech-data-analytics/

“Digitization is driving transformation, rewriting the

model as consumer expectations change”

We need to be connected ... very connected

Legacy Business Model

Risk Management Inertia

Innovation Weary

Increased Margins

Tailored Customer Experiences

Speed of Innovation

Digital Laggards Digital Innovators

Cloud - Mobility - Big Data Digital Divide

The role of Account Aggregation What’s new?

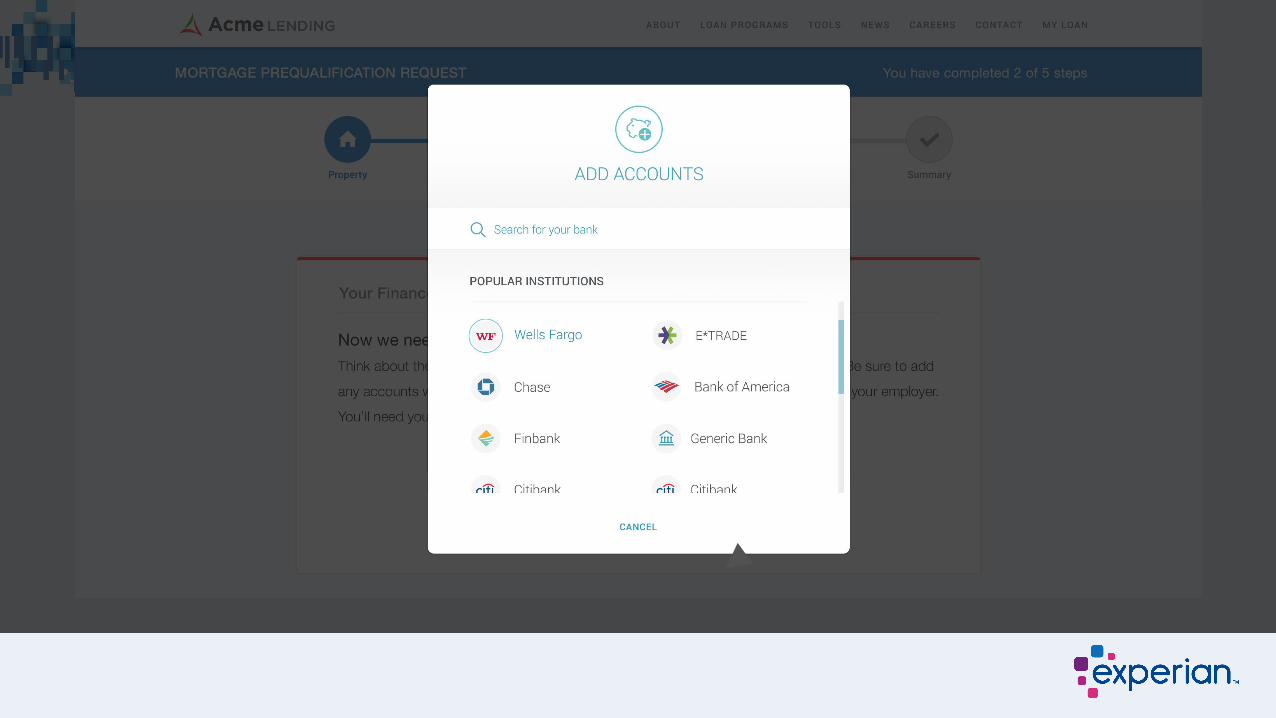

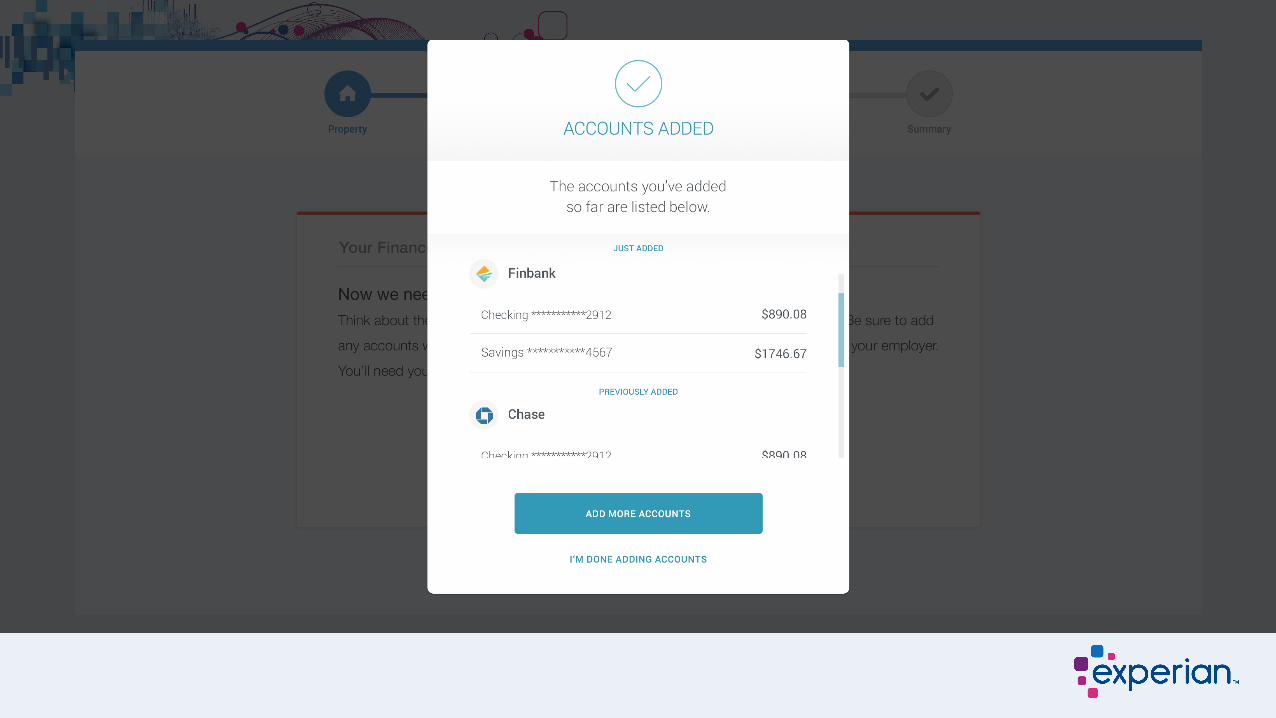

A method that involves compiling information from different accounts.

What is account aggregation?

• Bank accounts, credit card accounts, investment accounts, other consumer or business accounts, into a single place

• FIs and accounts are chosen by the consumer

• Permission is given by the consumer to the aggregator

vs.

Account Aggregation Credit Reporting

• Pulled from a resting database

• May be viewed without consumer’s knowledge

• Data provided by “furnishers”

• Real time data collection

• User permissioned for every access

• Consumer is owner of data

Benefits of Account Aggregation

• Automated, paperless verification process reduces processing times

• Relies on consumer’s permissioning of data and true aggregation technology

• Verification via real-time access into financial systems versus customer provided

paperwork or third-party systems

• Easy-to-use transparent interface for online and mobile experiences

Why our solution is different

• FCRA compliant and delivered by registered and mature CRAs

• Integrated with best in class Decisioning as a Service platform

• Unparalleled data quality with 100% formatted data sources and comes with a Financial Transaction ID

Use Cases

• Lenders require that borrowers income and assets be verified which takes days sometimes weeks

• Current verification process is tedious and time consuming for the borrower

• Borrower intervention increases risk of false documentation and inflated reporting

Mortgage

Verification of Asset Pilot

• Freedom from paper-based processes for validation of assets for first mortgages

• Freedom from representations and warranties

• Greater speed and simplicity, enabling an improved borrower experience

• Lenders often have income threshold stipulations (STIPs) for borrowers with credit scores< 625

• Dealers often required to verify car buyers income to meet lender stipulations (STIPs)

• Consumer overstates or understates income at time of application

• Consumer provides fake or altered paystubs

• Employment verification often required to meet lender stipulations (STIPs)

Automotive

• Lenders require verification of borrowers income which takes times to gather and verify

• Current verification process is tedious and time consuming for the borrower

• Borrower intervention increases risk of false documentation and inflated reporting

Personal loans

Helping organizations across a wide range of industries

Home Loans

Card & Personal Loans

Small Business

Screening

Eliminate paper to move towards

an all-digital mortgage underwriting

process

More precise ability to pay

assessment

Deeper understanding of cash

inflows and outflows

Improved insight into prospective

employees and tenants

Auto Loans Reduced manual verification and

stipulations

New Products • Income Verification

• Asset Verification

• Cash Flow

• Scores and Attributes

Improved Outcomes • Increase consumer satisfaction

• Reduce risk

• Broaden loan availability

• Accelerate loan underwriting

Account Aggregation will power new consumer insights and

digitize the application and lending process

ACCOUNT AGGREGATION API

Auto Loans

Home Loans

Card & Personal Loans Small Business

Screening

Digital

Identity

Employment

Data

DDA

Savings

Credit Accts

Investment

401K

Experian’s Digital Verification Solutions

• Historical transaction data (typically 12-24 months)

• Income report containing attributes:

- Direct deposit income

- Other income

- Average monthly income

- Frequency of income deposits

- Payor

• Verification of account owner

Verification of Income

Verification of Assets • Account balance query across various types:

- Checking (credits and debits)

- Savings/CD’s

- 401K, brokerage account

• Historical transaction data details (typically 90 days)

• Account balance attributes (typically last 90 days)

- Average account balance and trend

- Min and max account balance

• Verification of account owner

Prequalification

Use across the lifecycle of a lending relationship

Underwriting/ Decisioning

Verification Credit Risk

Modeling

Account Review/ Monitoring

Data flow

Multiple

Integration

Options

Checking

Investment

Account

Savings

Re

al-tim

e A

cco

un

t

Ag

gre

ga

tion p

roce

ss Access via Modern

API, NetConnect, or

ATB

Report

ID

Loan

Application Consumer

555-1313

************

****

Jones

What makes us different?

Broad Coverage • 80% certified coverage

• Full spectrum of account types

High Quality Data • 100% formatted data

• Auditable FI Transaction ID’s

Compliant Solutions • Delivered by registered CRA

• Robust security

Reimagining Lending Crosses the credit lifecycle; the uses and benefits are wide-ranging:

Decisioning

Verification

Credit Risk Modeling

Account Review

Prequalification

• Increases consumer satisfaction and loyalty

• Reduces credit and fraud risk • Broadens loan availability • Accelerates loan underwriting • Improves ability to match consumer

to right offer

Q&A

To learn more about Experian’s verification of income and verification of assets solutions: - Reach out to your account executive - Call 1-888-414-1120