Reviewing the MPF System from an Outcome-based …...Reviewing the MPF System from an Outcome-based...

53

Reviewing the MPF System from an Outcome-based Perspective Cheng Yan-chee Chief Corporate Affairs Officer and Executive Director Mandatory Provident Fund Schemes Authority 13 November 2018

Transcript of Reviewing the MPF System from an Outcome-based …...Reviewing the MPF System from an Outcome-based...

Reviewing the MPF System from an Outcome-based Perspective

Cheng Yan-cheeChief Corporate Affairs Officer and Executive Director

Mandatory Provident Fund Schemes Authority13 November 2018

World Bank’s Multi-pillar Retirement Protection Framework

2

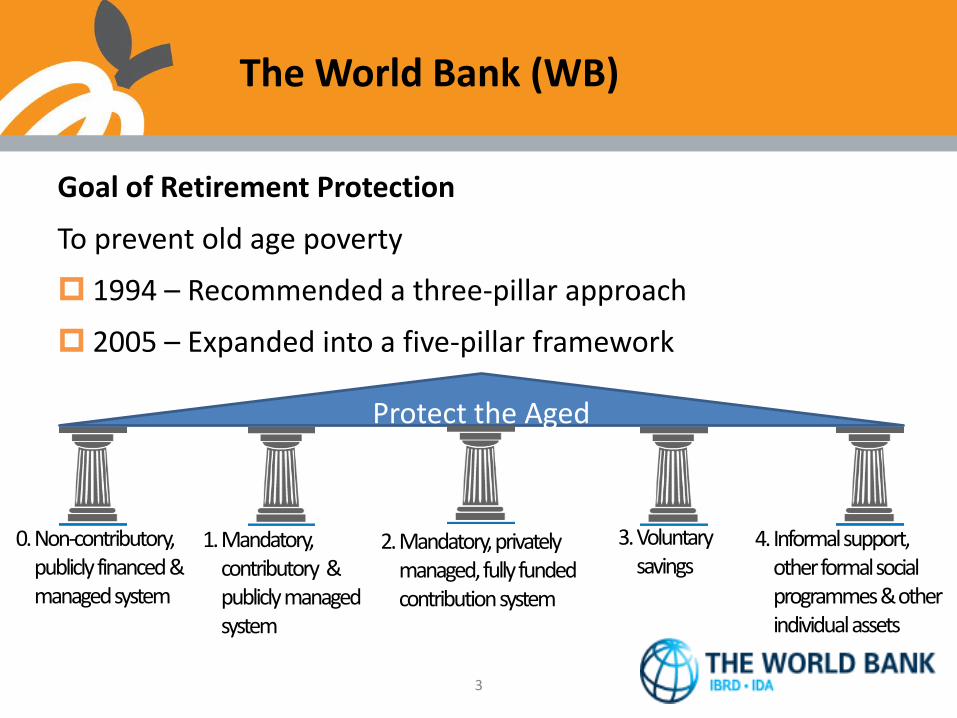

The World Bank (WB)

Goal of Retirement Protection

To prevent old age poverty

1994 – Recommended a three-pillar approach

2005 – Expanded into a five-pillar framework

3

Protect the Aged

0. Non-contributory, publicly financed &managed system

3.Voluntary savings

1.Mandatory, contributory & publicly managed system

2.Mandatory, privately managed, fully funded contribution system

4.Informal support, other formal social programmes & other individual assets

1 2 3 4 5 68

10 1113

1820 21

2325

2830

32 33

0

5

10

15

20

25

30

35

19

81

19

92

19

93

19

94

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

08

20

10

20

11

20

16

Notes:1. “Year” refers to the year in which second pillar systems started operation. 2. Only DC systems are included. 3. Those jurisdictions with second pillar systems discontinued are excluded.

Sources: International Monetary Fund, International Labour Organisation, International Organisation of Pension Supervisors, Maldives PensionAdministration Office, Mesa-Lago, National Pensions Regulatory Authority, OECD, Scherman, Superintendence of Pensions, World Bank.

No. of Second Pillar Systems in the World

MPF in Line with the Global Trend

4

World Bank’s Outcome-based Assessment for Private Pension Systems

5

WB’s Outcome-based Assessment (OBA) Framework for Private Pensions

A framework to evaluate the performance of a private pension system (2nd Pillar)

5 key outcomes

Coverage

Sustainability

Security

Efficiency

Adequacy

6

For further details, please refer to Price W, Ashcroft J, Hafeman M. (2016). Outcome Based Assessment for Private Pensions: A Handbook. World Bank, Washington, DC.

How Good is the MPF System in Defending Your Future

7

Outcome 1 : Coverage

8

Outcome 1: Coverage

Maximizing the proportion of the working-age population participating in private pension schemes and the proportion of retirees receiving such financial support in retirement

9

Outcome 1: CoverageEnrolment Rates of the MPF System

99% 100% 99%100% 100% 100%

68% 69% 70%

0%

20%

40%

60%

80%

100%

as at 30.9.2016 as at 30.9.2017 as at 30.9.2018

Enrolment Rates of MPF Schemes

Employers Employees Self-employed persons (SEPs)

The MPF System has very high enrolment rate

10

Outcome 1: CoverageCoverage of Private Pension Schemes in Different Jurisdictions

95%91%

85%* 84% 84% 81%74% 70% 67%

61% 60%

0%

20%

40%

60%

80%

100%

Cove

rage

(a

s a

% o

f E

mp

loye

d / W

ork

ing

Po

pu

lation

)

* Employed population covered under MPF schemes, ORSO schemes and other statutory pension or provident fund schemes

Coverage of Private Pension Schemes

11

Mandatory

Auto-enrolment/collective agreement

Outcome 1: CoverageFactors Contributing to High Coverage

Joined MPF schemes

73%

Joined other retirement schemes (e.g. ORSO) 11%

Exempt persons

13%

Not yet joined any MPF schemes

2%

Mandatory participation (except for exempt persons)

Labour force characteristics (mostly engaged in formal employment)

Geographical factors (densely populated)

Employed Population by Type of Retirement Schemes

Not covered by private pension schemes in Hong Kong, e.g. domestic employees and those aged above 65 or below 18

12

As at end Sep 2018

Outcome 2 : Sustainability

13

Outcome 2: Sustainability

Ensuring that the promised retirement income will be delivered without placing burdens on government, employers, or workers for financing any shortfalls

14

Outcome 2: SustainabilityMPF System: Sustainable by nature

• Universal coverage for employed population (except for exempt persons)

Mandatory

• Independent from Government’s revenue / public financial resources

PrivatelyManaged

• Dedicated assets to meet future pension benefits payable to members

Fully Funded

• Contributions are defined and made by employers and employees (a total of 10% of salary, subject to minimum and maximum relevant income)

DefinedContribution

15

Outcome 2: SustainabilityMPF Gaining Importance in the Economy

As at 30 September 2018, MPF assets reached $858 billion

Representing approximately 32% of Hong Kong’s GDP in 2017

Source: MPFA and Census & Statistics Department

13%

16%

12%

19%21%

18%

22%

24% 25% 25%26%

32%

0%

5%

10%

15%

20%

25%

30%

35%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

MP

F A

sse

ts (

as %

of G

DP

)

16

Outcome 2: SustainabilityPension Sustainability Index – Global

Hong Kong has one of the most sustainable pension systems globally

Source: Allianz Global Investors. (2016). Pension Sustainability Index 2016 (International Pension Paper 1/2016)

0 1 2 3 4 5 6 7 8 9

Thailand

China

Slovenia

Greece

Brazil

Italy

India

Malta

Japan

Spain

Cyprus

South Africa

Portugal

Croatia

Taiwan

Indonesia

Colombia

Ireland

Slovakia

France

Hungary

South Korea

Turkey

Romania

Bulgaria

Belgium

Austria

Russia

Poland

Germany

Singapore

Philippines

Argentina

Malaysia

Czech Republic

Peru

Luxembourg

Finland

Lithuania

Canada

Hong Kong, China

Switzerland

Mexico

United Kingdom

Chile

United States

Estonia

Latvia

New Zealand

Norway

Netherlands

Sweden

Denmark

Australia

Hong Kong ranked 14th out of 54 jurisdictions

Scale from 1 – 10. A jurisdiction with

an overall score of 1 represents the

greatest need for reform and 10

represents the least need for reform.

17

Outcome 2: SustainabilityPension Sustainability Index – Asia

Hong Kong: highly sustainable

Source: Allianz Global Investors. (2016). Pension Sustainability Index 2016 (International Pension Paper 1/2016).

0 1 2 3 4 5 6 7

Thailand

China

India

Japan

Taiwan

Indonesia

South Korea

Singapore

Philippines

Malaysia

Hong Kong, China

Scale from 1 – 10. A jurisdiction with an overall score of 1 represents the

greatest need for reform and 10 represents the least need for reform.

18

Outcome 3 : Security

19

Outcome 3: Security

Minimizing the risk of loss or misappropriation of pension assets before they are withdrawn by members

20

Outcome 3: Security Safeguarding Interests of Scheme Members

Sound Legal & Financial System

Hong Kong’s sound legal framework and financial system serve as the backbone of the MPF System

“Strong and stable financial markets” (WEF, 2017)

Global Competitive Index 2017-18Ranking of Hong Kong (out of 137 economies)• Institutions 9• Macroeconomic Environment 6• Financial Market Development 5

21

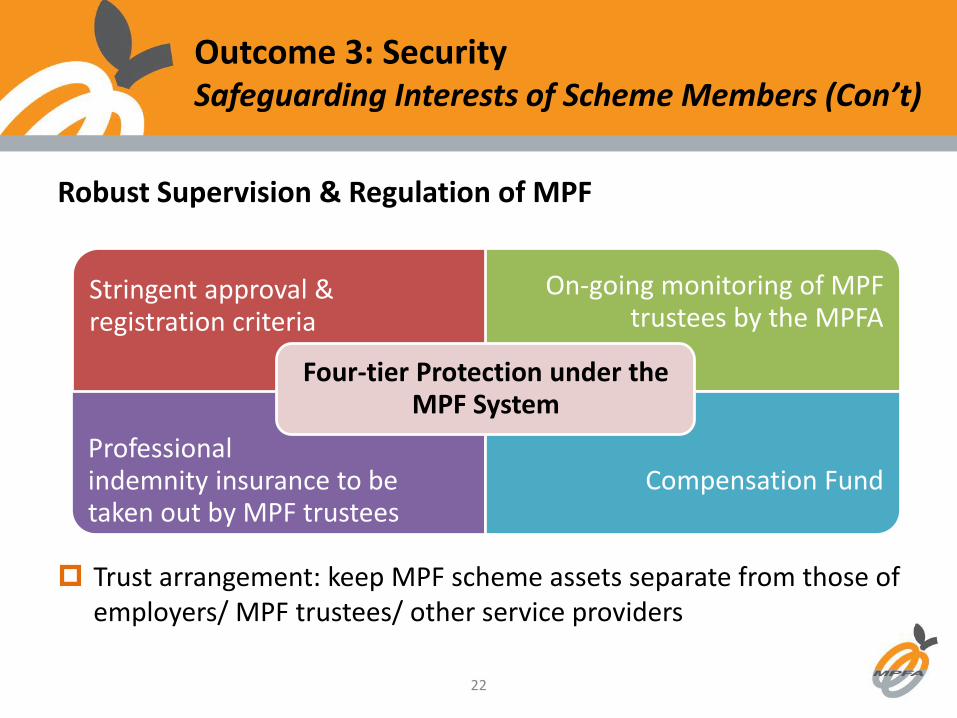

Outcome 3: Security Safeguarding Interests of Scheme Members (Con’t)

Robust Supervision & Regulation of MPF

Trust arrangement: keep MPF scheme assets separate from those of employers/ MPF trustees/ other service providers

Stringent approval & registration criteria

On-going monitoring of MPFtrustees by the MPFA

Professional indemnity insurance to be taken out by MPF trustees

Compensation Fund

Four-tier Protection under the MPF System

22

Outcome 4 : Adequacy

23

Outcome 4: Adequacy

Ensuring people accumulate retirement benefits that could

protect them from poverty;

allow them to share in increased prosperity; and

protect them from a severe drop in living standards at retirement, taking account of other sources of financial support

24

Outcome 4: AdequacyModerate Contribution Rate

6.5%

9.5% 10.0% 10.0%

15%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Mexico Australia Chile Hong Kong Israel

% o

f W

age

s/Ea

rnin

gs

Moderate contribution rate, comparable to similar private pension systems

OECD (2017). Pensions at a Glance 2017: OECD and G20 Indicators.

Contribution Rates of Mandatory Private Pension Systems

25

Limitation of MPF

As a Pillar 2 system, the MPF System is intended to provide basic retirement protection for employed population

The different pillars need to work together to provide adequate retirement protection for the entire population

Maximum / Minimum Relevant Income (Max RI / Min RI) Levels

Employers and employees contribute a total of 10%, subject to a cap of $3,000 per month (Max RI at $30,000 / 90th Percentile Earning)

Employees earning <$7,100 per month need not contribute, only employers need to contribute (5%) (Min RI at $7,100 / half of Median Earning)

Max RI adjustment proposal : $30,000 to ???

Min RI adjustment proposal : $7,100 to ???26

Outcome 4: AdequacyBasic Retirement Protection

The RI levels are reviewed regularly and adjusted when necessary to keep up with income changes of the workforce in Hong Kong

Adjustments to the RI levels are crucial for maintaining an appropriate amount of benefits for retirement saving purposes

27

Outcome 4: AdequacyBasic Retirement Protection

To encourage individuals to save more for their retirement, the Financial Secretary has announced tax concession for MPF voluntary contributions and deferred annuities

At the beginning of April 2019, individuals will enjoy concessions on their salary tax by making voluntary contributions to a tax-deductible voluntary contribution (TVC) account

Working with the Government on the relevant legislative changes

Formed a working group with MPF trustees to help them cater for these new TVC accounts

28

Outcome 4: AdequacyBasic Retirement Protection

0

100

200

300

400

500

600

700

800

900

1,000

Accrued Benefits Total Net Contributions Received

HK

$ B

illio

nOutcome 4: AdequacyMPF Assets

A growth of MPF assets since the inception of the System

MPF Accrued Benefits and Net Contributions (1.12.2000 – 30.9.2018)

Investment Returns(net of fees & charges)

$245.20 billion

Contributions(net of amount withdrawn)

$613.11 billion

$858 billion

29

1,974,000

1,547,000

1,227,000

985,000

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

Investment Horizon / Year

4.00

3.00

2.00

1.00

$

Investment Return / %

Projected Final

Accrued Benefits / $

Outcome 4: AdequacyProjected Accrued Benefits of Scheme Members over 40 Years’ Investment Horizon: Hypothetical Examples

Assumptions:• Nominal investment returns are 1%, 2%, 3% and 4% (net of fees and charges) throughout the relevant investment horizon• The monthly salary of 16,700 refers to the median salary of the employed persons aged 18 – 64 as at Q2 2018; no adjustment of monthly

salary throughout the relevant investment horizon• The employer and the employee each contribute 5% of the employee’s relevant income (i.e. 10% of the employee’s relevant income in total)• No adjustment to the existing statutory minimum and maximum relevant income levels, which are 7,100 and 30,000 per month respectively• Inflation rate is assumed as zero (i.e. inflation not accounted for in these examples)

30

Outcome 4: Adequacy

31

Nominal Investment Return / %

Monthly Salary / $

16,700 30,000

1.00 985,000 1,770,000

2.00 1,227,000 2,203,000

3.00 1,547,000 2,778,000

4.00 1,974,000 3,546,000

Projected Accrued Benefits of Scheme Members over 40 Years’ Investment Horizon

Assumptions:• Nominal investment returns are 1%, 2%, 3% and 4% (net of fees and charges) throughout the 40-year investment horizon• The employer and the employee each contribute 5% of the employee’s relevant income (i.e. 10% of the employee’s relevant

income in total)• No adjustment to the existing statutory minimum and maximum relevant income levels, which are 7,100 and 30,000 per month

respectively• No adjustment of monthly salary throughout the 40-year investment horizon• Inflation rate is assumed as zero (i.e. inflation not accounted for in these examples)

Outcome 4: AdequacyDistribution of Accounts by Range of Accrued Benefits

32

* 50 000 accounts had accrued benefits of more than $1,000,000

• It should be noted that as scheme members may have more than one account, the distribution pattern of scheme members’ MPF benefitsmay not be the same as the one shown in the Chart.

• As of December 2017.

The amount of VC has grown substantially over the years

The Government’s proposal to introduce tax concession for VC will help further strengthen the retirement protection function of the MPF System

Outcome 4: AdequacyVoluntary Contribution

2,993(10%)

3,555(11%)

4,253(12%)

4,346(10%)

4,995(13%)

5,934(14%)

6,655(14%)

7,272(14%)

7,735(13%)

8,697(13%)

9,487(14%)

10,411(15%)

0

2,000

4,000

6,000

8,000

10,000

12,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

MPF Voluntary Contribution (% of Total MPF Contribution)HK$m

33

Outcome 5 : Efficiency

34

Outcome 5: Efficiency

Maximizing net-of-fee returns by improving investment performance subject to acceptable risks

35

MPF Landscape

30 MPF schemes privately managed by 14 active trustees (as at 30 Sep 2018)

9.6 million MPF accounts (as at 30 Sep 2018)

4.1 million contribution accounts and 5.6 million personal accounts

Administration cost and expenses accounted for 43% of FER – 2012 Study

Reasons for high scheme administration costs

35 million transactions yearly (high levels of manual and paper-based processing)

Lower industry co-operation to resolve industry-wide problems

36

Outcome 5: EfficiencyInvestment Return of MPF

Hinging on scheme members’ fund choice

(as at 30 Sep 2018)

Past 1 YearPast 5 Years -Annualised

Since 1 Dec 2000

Annualised CumulativeReturn

Volatility

Equity Fund 2.9% 5.9% 5.0% 138.2% 5.3%

Mixed Assets Fund 2.6% 4.2% 4.3% 112.6% 2.7%

Bond Fund -2.2% 0.2% 2.5% 55.0% 0.9%

Guaranteed Fund 0.7% 0.5% 1.1% 22.1% 1.1%

Money Market Fund –Other than MPF Conservative Fund

-0.1% 0.1% 0.5% 9.5% 0.2%

Money Market Fund –MPF Conservative Fund

0.3% 0.1% 0.7% 13.3% 0.1%

Rate of Return of MPF Funds

37

Outcome 5: EfficiencyFees and Charges

2.06 2.10 2.09

2.01 1.99

1.94 1.91

1.84 1.83

1.77 1.73

1.75 1.72

1.70 1.69 1.65

1.62 1.60

1.57 1.57 1.56 1.56 1.53 1.53

1.50

1.60

1.70

1.80

1.90

2.00

2.10

2.20

26%

%

(Over the time period)

The average Fund Expense Ratio (FER) of MPF Funds has decreased over the years

Average FER of MPF Funds (Jul 2007 – Sep 2018)

38

1,999,000

1,732,000

1,510,000

0

500,000

1,000,000

1,500,000

2,000,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

$

Investment Horizon / Year

FER at 0.95%

FER at 1.53%

FER at 2.10%

Outcome 5: EfficiencyImpact of Fees and Charges on Scheme Members’ Accrued Benefits

Estimated Final Accrued Benefits of Scheme Members

Key Assumptions• Gross investment return (before fees and expenses) is 5% per year• Each FER level remains constant throughout the 40-year investment horizon• Monthly salary is $16,700, which was the median salary of employed persons aged 18 - 64 as at Q2 2018; no adjustment of monthly salary• No adjustment to the existing statutory minimum and maximum relevant income levels, which are 7,100 and 30,000 per month respectively• Inflation rate is assumed as zero

A reduction in fees and expenses would improve significantly scheme members’ accrued benefits over the long term

Incr

ease

: $

22

2,0

00

(1

4.7

%)

Incr

ease

: $

48

9,0

00

(3

2.4

%)

39

Encourage consolidation of inefficient schemes & funds to achieve economies of scale

Outcome 5: EfficiencySupply Side Initiatives – Promoting Economies of Scale

51 51 49 48 47 46

40 40 38 3841 40 41 41

38 38 3632 32

0

10

20

30

40

50

60

14

15

16

17

18

19

20

No

. of

Reg

iste

red

Sch

emes

No

. of

Tru

stee

s

No. of Approved Trustees No. of Registered Schemes

40

* Includes an approved trustee which does not operate any MPF scheme and two MPF schemes which are pending termination.

Outcome 5: EfficiencySupply Side Initiatives – Retirement Solutions for Achieving Better Saving Outcomes

Default Investment Strategy (DIS)

Ready made strategy balancing long-term risks and returns

Fee caps

Globally diversified investment

NAV in DIS and DIS Constituent Funds: $30 billion (4% of MPF System NAV) (as at end Sep 2018)

1.59m(17%)

8.01m

All MPF accounts

DIS

Non-DIS

No. of MPF accounts in DIS or DIS Constituent Funds

(as at end Jun 2018)

41

Use of digital technology to enhance operational efficiency

Outcome 5: EfficiencySupply Side Initiatives – Streamlining & Simplifying Processes

42

Trustees

• Facilitating Transfer of Benefits Across Schemes

Intermediaries • Promoting Electronic Submission of Statutory Returns

• ePASS (Electronic Portability Automation Services System)

• ePayment for MPF Transfer

• Data Submission using Enhanced TrusNet Platform

• eService for Intermediaries

• Promoting Electronic Submission of Statutory Returns

Outcome 5: EfficiencySupply Side Initiatives – Governance Charter

On 24 May 2018, all 14 MPF trustees pledged their commitment to a Governance Charter advocated by the MPFA, recognizing the importance of good governance and fiduciary responsibilities in protecting the interests of scheme members and providing value for money services

To introduce the implementation of good governance to trustees in phases over the next 12 to 18 months:

Phase 1 – seek MPF trustees’ support of the governance principles and the elaborations underpinning each principle.

Phase 2 – assess whether MPF trustees’ existing governance framework and arrangements are in adherence with the Governance Principles

Phase 3 – provide guidance or training for MPF trustees on the expected standards underpinning each of the Governance Principles43

Outcome 5: EfficiencySupply Side Initiatives – Enhancing Scheme Administration

44

Smart Digital Platform

Digital, flexible and user centric platform

One-stop access

Smart Administration

Standardization, streamlining and automation

Central hub for processing ER and EE’s instructions and transactions

Paperless

Outcome 5: EfficiencySupply Side Initiatives – Enhancing Scheme Administration

45

Development of eMPF is crucial to the reform of the MPF System

Objectives of eMPF:

Enhance members’ experience

Build an open architecture to bring competition

Further fee reduction to the overall MPF System

Pave the way for future MPF reform

Outcome 5: EfficiencyDemand Side Initiatives – Strengthening Employees’ Control

Employee Choice Arrangement (ECA)

Strengthening employees’ autonomy to opt to transfer the accrued benefits derived from employees’ mandatory contributions to the scheme of their own choice

Helping to increase members’ power as consumers

$193 billion of MPF benefits can be transferred under ECA as at end Dec 2017

46

Provision of a centralized database containing key information about MPF schemes and funds

Outcome 5: EfficiencyDemand side Initiatives – Enhancing Information Disclosure

47

Fund Performance Platform (FPP)

Outcome 5: EfficiencyDemand side Initiatives – Enhancing Information Disclosure

48

Outcome 5: EfficiencyDemand Side Initiatives – Consolidation of Personal Accounts

49

e-Enquiry of Personal Account (ePA) (28 Apr 2017)

As at 31 Oct 2018, over 75,000 scheme members have completed the registration process and activated the ePA service

Help scheme members manage MPF personal accounts (PAs) by providing easy access to the following information

• Whereabouts of their MPF personal accounts

• A contact list of all trustees

• Fees and returns of MPF funds

• The latest MPF news

307,000 applications on consolidation of PAs (May 2017 – Sep 2018)

About 70% of all MPF assets ($590 billion)* can be transferred freely between MPF schemes, including:

• 5.49 million personal accounts - $370 billion

• 3.98 million contribution accounts - $214 billion(* as at end 2017)

Enhancing member engagement through promotional and publicity activities

TV, Facebook Messenger Bot, roving exhibition, MPFA website and mobile apps, seminars, workshops, publication materials, etc

Outcome 5: EfficiencyDemand Side Initiatives – Engagement and Education

50

Conclusion

51

52

Major Challenges

Outcomes Performance of the MPF System

Coverage• Very high enrolment rate

(100% for both employers and employees; 70% for SEPs)

Sustainability• Sustainable by design

(mandatory, privately managed, fully funded and defined contribution)

Security• Safeguarded by the sound legal and financial systems as

well as regulatory and supervisory regime of MPF

Adequacy• One of HK’s retirement protection pillars• Level of adequacy will improve as the System matures

Efficiency• Strive for greater efficiency and lower costs of the MPF

System

Conclusion

Thank You