REVIEW OF TIMBERLAND INVESTMENT DRIVERS, GROWTH AND …

49

Jib A. Davidson, C.F. Columbia Timber & Environmental Services United County Real Estate and Auctions Gainesville, FL • 352-375-1473 [email protected] REVIEW OF TIMBERLAND INVESTMENT DRIVERS, GROWTH AND TIMBER PRICES

Transcript of REVIEW OF TIMBERLAND INVESTMENT DRIVERS, GROWTH AND …

Jib A. Davidson, C.F.Columbia Timber & Environmental Services

United County Real Estate and AuctionsGainesville, FL • 352-375-1473

REVIEW OF TIMBERLAND INVESTMENT DRIVERS, GROWTH AND TIMBER PRICES

TIMBERLAND INVESTMENT DRIVERS

•A driver has a material effect upon the activity of another entity¹

•Drivers are unique •Landowner objectives create drivers •Maximize net income, IRR & NPV

¹Kenton, Will (2018). Investopedia. Retrieved from www.Investopedia.com/terms

CAULFIELD DRIVERS

• Jon P. Caulfield, Professor of Forest Business at Warnell School of Forest Resources at UGA

•“Timberland Return Drivers and Investing Styles of an Asset That Has Come of Age” The Quarterly Review of Commercial Finance Techniques. Volume 14, Number 4. Winter 1998.

CAULFIELD DRIVERS

•Land Price Change•Product Price Change•Biological Growth

CAULFIELD DRIVERS

33.3%

6.2%

Biologicalgrowth

Land price appreciation

Product pricechange

60.5%

KPMG DRIVERS

KPMG DRIVERS

•KPMG International•Operates in 153 countries•207,000 employees•Supply audits, assurance practices, mitigates risk, identifies opportunities

KPMG DRIVERS

•Timberland Investment Case• September 2013

•Real rates of return 4 – 6%

KPMG DRIVERS

•Asset Management•Timber pricing•Biological growth

KPMG DRIVERS

25%

25%50%

Asset management

Biologicalgrowth

Timberpricing

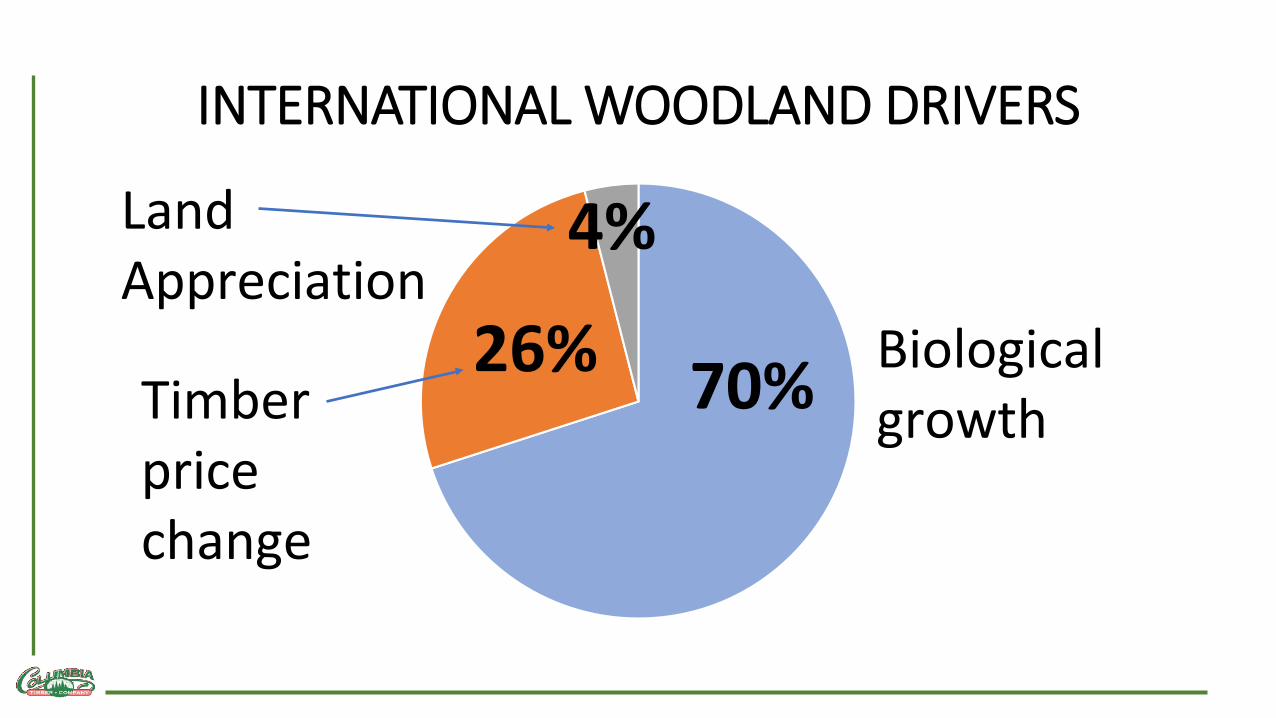

INTERNATIONAL WOODLAND DRIVERS

•International Woodland invests in agriculture and timberland

•Manage 4.5 billion dollars of institutional portfolios

INTERNATIONAL WOODLAND DRIVERS

•Focus on asset management & alternative investments

•Study rates of return and risk

INTERNATIONAL WOODLAND DRIVERS

•Land appreciation•Timber price changes•Biological growth

INTERNATIONAL WOODLAND DRIVERS

•Land appreciation: 2 – 5%•Timber price changes: 25 – 30%•Biological growth: 65 – 75%

INTERNATIONAL WOODLAND DRIVERS

70%26%

4%Land Appreciation

Timber price change

Biologicalgrowth

COLUMBIA TIMBER COMPANY DRIVERS

•Land appreciation•Asset management•Timber price changes•Biological growth

COLUMBIA TIMBER COMPANY DRIVERS

75% Biologicalgrowth

Land Appreciation

Timber prices

AssetManagement

3%10%

12%

Historical and Current Land Management Practices

0

50

100

150

200

250

1940 1950 1960 1970 1980 1990 2000 2010

Establishment period

Volu

me

at h

arve

st (t

ons/

acre

)

Clonal andbiotechnologyTree improvement

Weed control

Fertilization

Site preparation

Planting

Natural stand

Adapted from Fox, T.R., Jokela, and Allen. 2004

ESTABLISHING OPTIMAL ROTATION

CRITERIA FOR SELECTING “PROPER” AGE• Landowner objectives• Age for the “best” size – all timber markets are local• Age for total maximum volume• Age for maximum rate of growth• Maximum economic returns

ESTABLISHING OPTIMAL ROTATION

TRADITIONAL METHODS• Faustmann• Land expectation value, site expectation value, soil

rent & bare land value• Forest rent (maximizes stumpage)• Fisher rotation age (ignores opportunity costs)• Hartman rotation age (non-timber values)• MAI/CAI (no economics)

ESTABLISHING OPTIMAL ROTATION

Rotation age = max (PV benefits – PV costs)

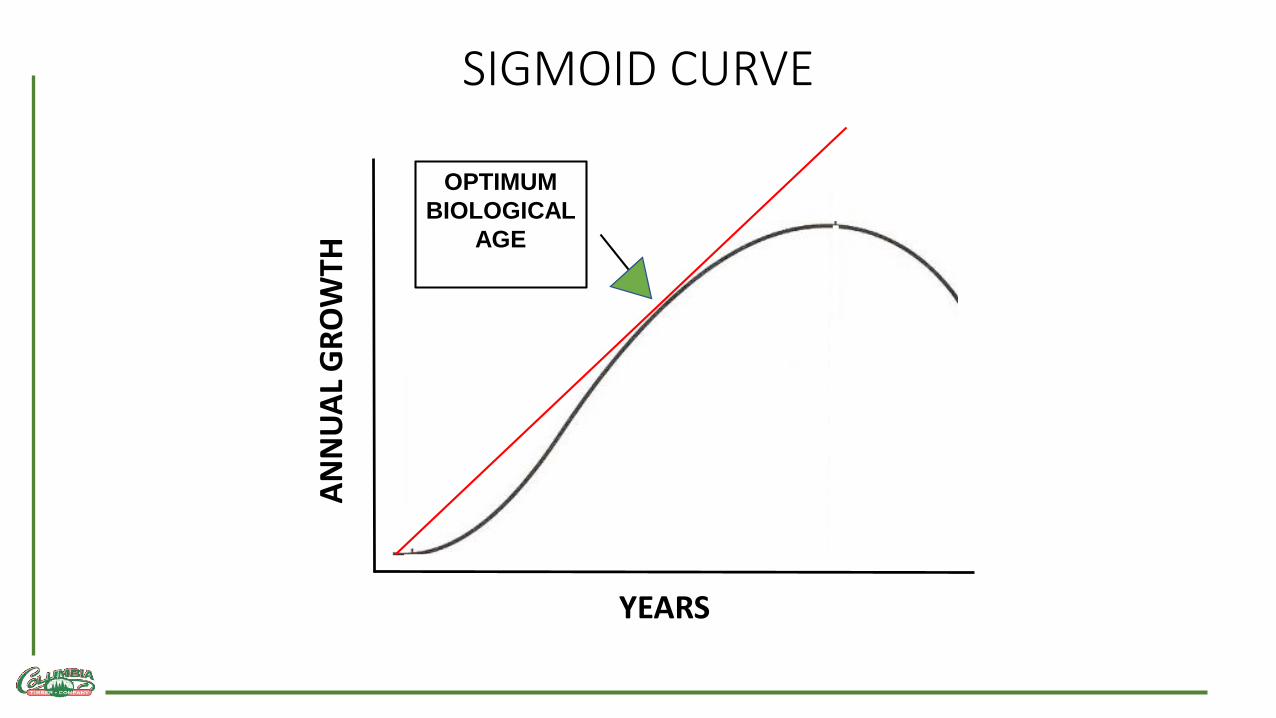

SIGMOID CURVE

ANN

UAL

GRO

WTH

YEARS

SIGMOID CURVE

ANN

UAL

GRO

WTH

YEARS

SEEDLINGESTABLISHMENT

SIGMOID CURVE

ANN

UAL

GRO

WTH

YEARS

TREE GROWTHINCREASES AT ANINCREASING RATE

SIGMOID CURVE

ANN

UAL

GRO

WTH

YEARS

IMPORTANT INFLECTION

POINT

SIGMOID CURVE

ANN

UAL

GRO

WTH

YEARS

TREE GROWTHINCREASES BUT AT ADECREASING RATE

SIGMOID CURVE

ANN

UAL

GRO

WTH

YEARS

MAXIMUMGROWTH

SIGMOID CURVE

ANN

UAL

GRO

WTH

YEARS

OPTIMUM BIOLOGICAL

AGE

MEAN ANNUAL INCREMENT = CURRENT ANNUAL INCREMENT

Zhang, D., &Pearse, H. P. (2011). Figure 7.1 Growth in volume and stumpage vale of a forest stand at it increases in age. Forest Economics. UBC Press, Vancouver, B.C.

CAIMAI

MEAN ANNUAL INCREMENT = CURRENT ANNUAL INCREMENT

Zhang, D., &Pearse, H. P. (2011). Figure 7.1 Growth in volume and stumpage vale of a forest stand at it increases in age. Forest Economics. UBC Press, Vancouver, B.C.

CAIMAI

GROWTH & YIELD EXAMPLE

-

2

4

6

8

10

12

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Gro

wth

tons

/acr

e

Years

GROWTH & YIELD LOBLOLLY PINE

CAI

MAI

SQ = 80600 T/A

GROWTH & YIELD EXAMPLE

-

2

4

6

8

10

12

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Gro

wth

tons

/acr

e

Years

GROWTH & YIELD LOBLOLLY PINE

CAI

MAI

SQ = 80600 T/A

Rotation age = 15

TIMBER PRICING

Delivered prices vs. stumpage?

DELIVERED PRICES

TIMBER PRICING

•Timbermart South•Forest2Market•RISI Fastmarkets

TIMBER PRICING

TMS DATA

y = 1.0307x + 22.147R² = 0.9569

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

2 0 0 6 2 0 0 7 2 0 0 8 2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6 2 0 1 7 2 0 1 8

NE FL DELIVERED TIMBER PRICES PULPWOOD

TMS DATA

y = 22.734e0.0353x

R² = 0.9546

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

2 0 0 6 2 0 0 7 2 0 0 8 2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6 2 0 1 7 2 0 1 8

NE FL DELIVERED TIMBER PRICES PULPWOOD

TIMBER PRICE GROWTH RATE

•LINEAR 3.1% •EXPONTIAL 3.5%

THIS IS A NOMINAL GROWTH RATE…IT INCLUDES INFLATION

HISTORICAL INFLATION

-15

-10

-5

0

5

10

15

20

15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 0 5 10 15

INFLATION 1915 - 2018

HISTORICAL INFLATION

-15

-10

-5

0

5

10

15

20

15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 0 5 10 15

INFLATION 1915 - 2018

INFLATION LAST 10 YEARS2008 – 2018

1.6%

REAL TIMBER GROWTH RATE

LINEAR EXPO AVERAGE

TIMBER GROWTH 3.1 3.5 3.3LESS INFLATION (1.9) (1.9) (1.9)REAL TIMBER GROWTH

1.2 1.6 1.4

COMBINE TIMBER PRICE WITH GROWTH

COMBINE TIMBER PRICE WITH GROWTH

$-

$500

$1,000

$1,500

$2,000

$2,500

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

DOLL

AR V

ALU

E

YEARS2 TONS/A/YR 5 TONS/A/YR 8 TONS/A/YR

DOLLAR GROWTH WITH NO TIMBER PRICE INCREASE AT $16 PER TON

COMBINE TIMBER PRICE WITH GROWTH

$-

$500

$1,000

$1,500

$2,000

$2,500

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

DOLL

AR V

ALU

E

YEARS2 TONS/A/YR 5 TONS/A/YR 8 TONS/A/YR

DOLLAR GROWTH WITH NO TIMBER PRICE INCREASE AT $16 PER TON

P₁ = $16P₁₈ = $16

COMBINE TIMBER PRICE WITH GROWTH

$-

$500

$1,000

$1,500

$2,000

$2,500

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

DOLL

AR V

ALU

E

YEARS2 TONS/A/YR 5 TONS/A/YR 8 TONS/A/YR

DOLLAR GROWTH WITH NO TIMBER PRICE INCREASE AT $16 PER TON

P₁ = $16P₁₈ = $16

IRR = 22%

IRR = 28%

IRR = 32%

COMBINE TIMBER PRICE WITH GROWTH

-

500

1,000

1,500

2,000

2,500

3,000

3,500

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

DOLL

AR V

ALU

E

YEARS

DOLLAR GROWTH WITH 1.4% REAL PRICE INCREASE AT $16 PER TON

2 TONS/A/YR 5 TONS/A/YR 8 TONS/A/YR

COMBINE TIMBER PRICE WITH GROWTH

-

500

1,000

1,500

2,000

2,500

3,000

3,500

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

DOLL

AR V

ALU

E

YEARS

DOLLAR GROWTH WITH 1.4% REAL PRICE INCREASE AT $16 PER TON

2 TONS/A/YR 5 TONS/A/YR 8 TONS/A/YR

IRR = 24%

IRR = 30%

IRR = 34%P₁ = $16P₁₈ = $21

IRR SUMMARY

Questions?

![Impact Investing – The ‘Real’ Deal · − Timberland Investment Management Organization [TIMO] founded in 1976 − Differentiated through conservation investment strategy and](https://static.fdocuments.net/doc/165x107/5f09a3087e708231d427c9bc/impact-investing-a-the-areala-deal-a-timberland-investment-management-organization.jpg)