Review of the Code of Banking Practice Final Report · Review of the Code of Banking Practice Final...

92

Review of the Code of Banking Practice Final Report October 2001 Richard Viney RTV Consulting Pty Ltd

Transcript of Review of the Code of Banking Practice Final Report · Review of the Code of Banking Practice Final...

Review

of the

Code of

Banking Practice

Final Report

October 2001

Richard Viney RTV Consulting Pty Ltd

Review of the Code of Banking Practice Final Report, October 2001

TABLE OF CONTENTS

ABBREVIATIONS AND DEFINITIONS.............................................................1

SUMMARY OF FINAL RECOMMENDATIONS.................................................3

CHAPTER 1 - INTRODUCTION .....................................................................17

Appointment of the Review..........................................................................17 Terms of Reference .....................................................................................17 The existing Code of Banking Practice........................................................17 The Review Process....................................................................................17 Acknowledgements......................................................................................18 Structure of this Report................................................................................18

CHAPTER 2 – UNCOMPLETED MATTERS ..................................................21

CHAPTER 3 - GENERAL ISSUES..................................................................23

Objectives and Principles ............................................................................23 Fairness.......................................................................................................24 Prudential Principle......................................................................................25 Scope of the Code .......................................................................................26

Definition of “Banking Service”.......................................................................... 26 Definition of “Customer” .................................................................................... 26

Code monitoring and Administration............................................................27 Educating Code Members (and their staff and agents) About the Code .....30 Promoting the Code to Consumers, Consumer Advisors and the Public Generally .....................................................................................................31 Monitoring External Developments including Legislative Changes .............32 Arranging Regular Reviews of the Code .....................................................32 Implementing Changes................................................................................33 Access to Banking Services ........................................................................33 Access to Banking Services for People Unable or Reluctant to Use Atms, Telephone Banking or Internet Banking ......................................................35 Low Cost Accounts for Banking Services ....................................................35

CHAPTER 4 – DISCLOSURE REQUIREMENTS ...........................................37

Introduction..................................................................................................37 “Fleshing Out” the Necessary Detail for PDS ..............................................38 Timing Differences Affecting Notification of Changes .................................39 Which Disclosure Requirements Contained in Existing Clauses Should Remain in the Code? ...................................................................................40 Other Gaps ..................................................................................................43 Statements of Account for Credit Products..................................................43 Statements of Account for Non Credit Products ..........................................44 Shadow Ledgers..........................................................................................45 Staff Training ...............................................................................................46 Copies of Documents...................................................................................46 Customers in Financial Difficulties...............................................................47

Review of the Code of Banking Practice Final Report, October 2001

Debt Recovery............................................................................................. 48 Privacy and Confidentiality.......................................................................... 49 Credit Assessment ...................................................................................... 49 Implementing Family Court Decisions and Family Law Settlements........... 51 Direct Debits from Accounts Other Than Credit Card Accounts ................. 52 Direct Debits from Credit Card Accounts .................................................... 55 Application of Code to Guarantors .............................................................. 56 Provision of Information to Guarantors ....................................................... 57

(i) Consent of principal debtor to provision of information ............................. 57 (ii) Obligations to provide information ......................................................... 58 (iii) Financial Information ............................................................................. 58 (iv) Advice about the operation of the guarantee......................................... 59

Form of Guarantee (Limitations) ................................................................. 61 Right to Cap Liability ................................................................................... 61 Right to Withdraw........................................................................................ 62 Enforcement ................................................................................................ 62 Joint Borrowers ........................................................................................... 63 Subsidiary Cards......................................................................................... 64 Mutuality and Set Off................................................................................... 64 Dispute Resolution...................................................................................... 65 Electronic Communication........................................................................... 67

SCHEDULE 1 - LIST OF SUBMISSIONS....................................................... 69

SCHEDULE 2 - ABA FINAL RESPONSE TO ISSUES PAPER ..................... 71

Review of the Code of Banking Practice Final Report, October 2001 1

ABBREVIATIONS AND DEFINITIONS

ABA Australian Bankers’ Association

ABA Final Response ABA’s annexure to its final response to the Issues Paper submitted in August 2001. (See Schedule 2)

ABIO Australian Banking Industry Ombudsman

ACA Australian Consumers’ Association

ACCC Australian Competition & Consumer Commission

APCA Australian Payments Clearing Association

ASIC Australian Securities & Investments Commission

Code Code of Banking Practice

DDR Direct Debit Request

EFT Code Electronic Funds Transfer Code of Conduct

FSR (the) Financial Services Reform Bill or Act, as the case requires

Hawker Report Hawker Committee Report entitled “Regional Banking Services: Money too far away”

JCS The submission to the review made jointly by:

• Consumer Credit Legal Centre (NSW) Inc

• Consumer Credit Legal Service (Vic) Inc

• Consumer Credit Legal Service (WA) Inc

• Consumer Law Centre Victoria Inc

• Care Inc Financial Counselling Service (ACT)

• Financial Services Consumer Policy Centre Inc

Ledger FI (the) customer’s bank

PDS Product Disclosure Statement(s)

UCCC (the)(Uniform) Consumer Credit Code

Review of the Code of Banking Practice Final Report, October 2001 3

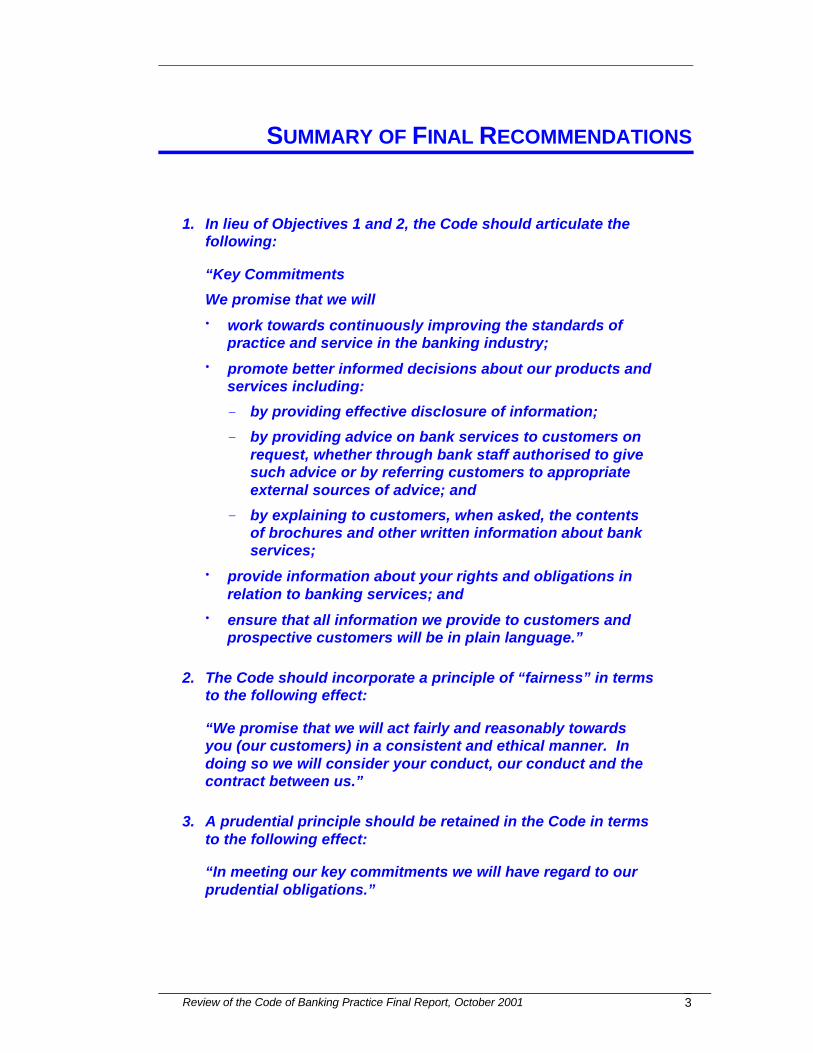

SUMMARY OF FINAL RECOMMENDATIONS

1. In lieu of Objectives 1 and 2, the Code should articulate the following:

“Key Commitments

We promise that we will

• work towards continuously improving the standards of practice and service in the banking industry;

• promote better informed decisions about our products and services including:

by providing effective disclosure of information;

by providing advice on bank services to customers on request, whether through bank staff authorised to give such advice or by referring customers to appropriate external sources of advice; and

by explaining to customers, when asked, the contents of brochures and other written information about bank services;

• provide information about your rights and obligations in relation to banking services; and

• ensure that all information we provide to customers and prospective customers will be in plain language.”

2. The Code should incorporate a principle of “fairness” in terms to the following effect:

“We promise that we will act fairly and reasonably towards you (our customers) in a consistent and ethical manner. In doing so we will consider your conduct, our conduct and the contract between us.”

3. A prudential principle should be retained in the Code in terms to the following effect:

“In meeting our key commitments we will have regard to our prudential obligations.”

Review of the Code of Banking Practice Final Report, October 2001 4

4. The Code should define banking service to mean any financial service provided by a bank to a customer in terms which make it clear that the definition:

• includes any financial service or product provided by a bank whether supplied to a customer directly or through an intermediary; and

• in the case of a financial service or product provided by another party but distributed by a bank, does not extend to that product or service but extends to the bank’s distribution or supply of the service or product to a customer.

5. The Code should define customer as meaning an individual or a small business.

6. The Code should define a small business to mean a business employing:

• less than 100 people if the business is or includes the manufacture of goods; or

• in any other case, less than 20 people.

7. The Code should provide for a monitoring mechanism and sanctions having the criteria detailed in the proposal set out in ABA’s Final Response, subject to it being made clear that:

• complaints about breaches of the Code will be received from consumer organisations and state regulatory agencies;

• the ABIO may refer to the code monitoring body, breaches of the Code detected by ABIO in the course of its dispute resolution function; and

• nothing in these proposals will in any way limit or affect the ABIO’s existing jurisdiction or function.

8. The Code should oblige banks to ensure all relevant staff and agents have an adequate knowledge of its provisions.

9. The Code should require the Code administration body to promote the Code among bank customers, consumer advisors and the public generally.

10. Banks should be obliged to display the Code, and have copies available on request by any person, at all branches.

Review of the Code of Banking Practice Final Report, October 2001 5

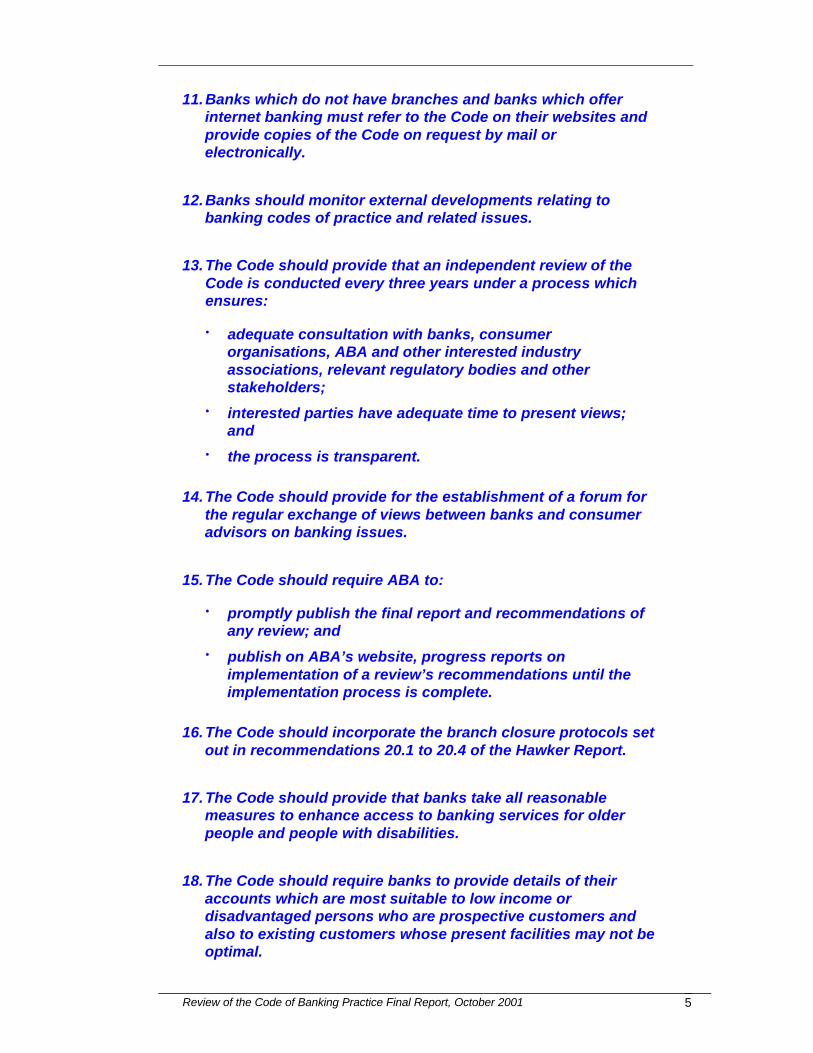

11. Banks which do not have branches and banks which offer internet banking must refer to the Code on their websites and provide copies of the Code on request by mail or electronically.

12. Banks should monitor external developments relating to banking codes of practice and related issues.

13. The Code should provide that an independent review of the Code is conducted every three years under a process which ensures:

• adequate consultation with banks, consumer organisations, ABA and other interested industry associations, relevant regulatory bodies and other stakeholders;

• interested parties have adequate time to present views; and

• the process is transparent.

14. The Code should provide for the establishment of a forum for the regular exchange of views between banks and consumer advisors on banking issues.

15. The Code should require ABA to:

• promptly publish the final report and recommendations of any review; and

• publish on ABA’s website, progress reports on implementation of a review’s recommendations until the implementation process is complete.

16. The Code should incorporate the branch closure protocols set out in recommendations 20.1 to 20.4 of the Hawker Report.

17. The Code should provide that banks take all reasonable measures to enhance access to banking services for older people and people with disabilities.

18. The Code should require banks to provide details of their accounts which are most suitable to low income or disadvantaged persons who are prospective customers and also to existing customers whose present facilities may not be optimal.

Review of the Code of Banking Practice Final Report, October 2001 6

19. Significant overlap between Code provisions and other laws, particularly UCCC and FSR, is undesirable and overlapping provisions should, except where there are special reasons to the contrary, be deleted from the Code.

20. At or near the commencement of the Code, there should be included a statement to the following effect:

“Customers are advised that in addition to their rights under this Code they may have rights under Federal laws, especially the Trade Practices Act and the Financial Services Reform Act and under State and Territory laws, especially the Consumer Credit Code and Fair Trading Acts.”

21. The Code should contain a provision to the following effect:

“We will comply with all relevant laws relating to banking services, including those concerning:

• consumer credit products;

• other financial products and services;

• privacy; and

• discrimination.”

22. The Code is not the appropriate medium for fleshing out the necessary detail of PDS for the purposes of FSR.

23. UCCC and not the Code should specify the notice requirements for changes to UCCC regulated products.

24. FSR and not the Code should specify the notice requirements for changes relating to fees and charges.

25. The existing Code notice requirements should be retained for all other changes.

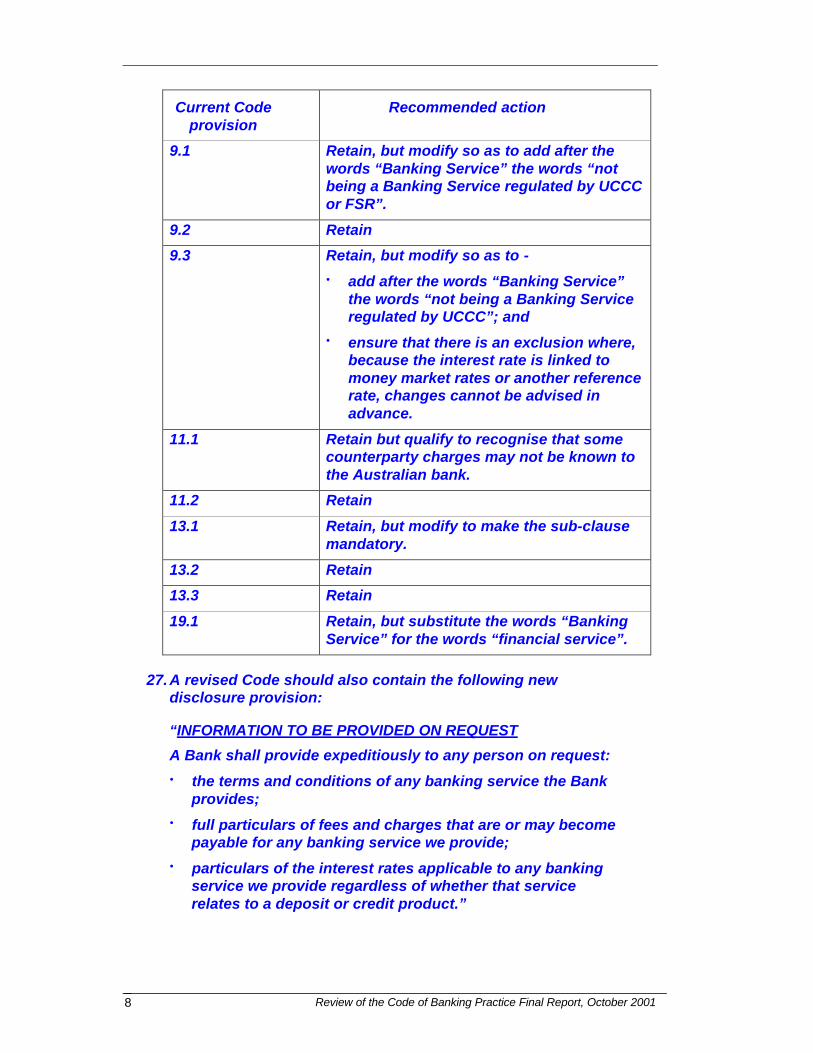

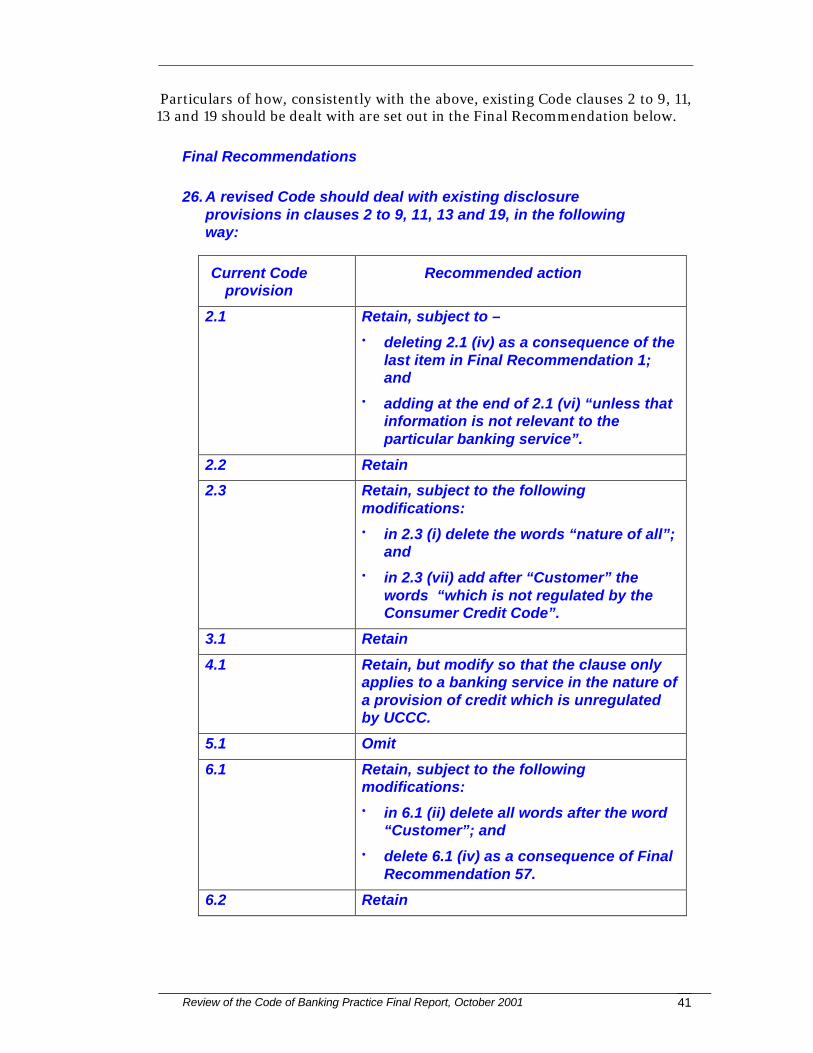

26. A revised Code should deal with existing disclosure provisions contained in clauses 2 to 9, 11, 13 and 19, in the following way:

Review of the Code of Banking Practice Final Report, October 2001 7

Current Code provision

Recommended action

2.1 Retain, subject to –

• deleting 2.1 (iv) as a consequence of the last item in Final Recommendation 1; and

• adding at the end of 2.1 (vi) “unless that information is not relevant to the particular banking service”.

2.2 Retain

2.3 Retain, subject to the following modifications:

• in 2.3 (i) delete the words “nature of all”; and

• in 2.3 (vii) add after “Customer” the words “which is not regulated by the Consumer Credit Code”.

3.1 Retain

4.1 Retain, but modify so that the clause only applies to a banking service in the nature of a provision of credit which is unregulated by UCCC.

5.1 Omit

6.1 Retain, subject to the following modifications:

• in 6.1 (ii) delete all words after the word “Customer”; and

• delete 6.1 (iv) as a consequence of Final Recommendation 57.

6.2 Retain

7.1 Delete, as this sub-clause will be incorporated into a new clause pursuant to Final Recommendation 27.

7.2 Retain

7.3 Retain, but limit the operation of the sub-clause to such of the services presently mentioned as are not covered by FSR.

8.1 Retain

Review of the Code of Banking Practice Final Report, October 2001 8

Current Code provision

Recommended action

9.1 Retain, but modify so as to add after the words “Banking Service” the words “not being a Banking Service regulated by UCCC or FSR”.

9.2 Retain

9.3 Retain, but modify so as to -

• add after the words “Banking Service” the words “not being a Banking Service regulated by UCCC”; and

• ensure that there is an exclusion where, because the interest rate is linked to money market rates or another reference rate, changes cannot be advised in advance.

11.1 Retain but qualify to recognise that some counterparty charges may not be known to the Australian bank.

11.2 Retain

13.1 Retain, but modify to make the sub-clause mandatory.

13.2 Retain

13.3 Retain

19.1 Retain, but substitute the words “Banking Service” for the words “financial service”.

27. A revised Code should also contain the following new disclosure provision:

“INFORMATION TO BE PROVIDED ON REQUEST

A Bank shall provide expeditiously to any person on request:

• the terms and conditions of any banking service the Bank provides;

• full particulars of fees and charges that are or may become payable for any banking service we provide;

• particulars of the interest rates applicable to any banking service we provide regardless of whether that service relates to a deposit or credit product.”

Review of the Code of Banking Practice Final Report, October 2001 9

28. There should be retained in the Code those existing Code disclosure obligations which are not replicated in or superseded by disclosure requirements arising under FSR or UCCC.

29. The Code should apply the substance of the UCCC requirements in sections 31 to 34 (inclusive) to small business statements of account and related information. However, the relevant Code provision should recognise that there are some credit products used by small business to which those UCCC requirements cannot in practice be applied.

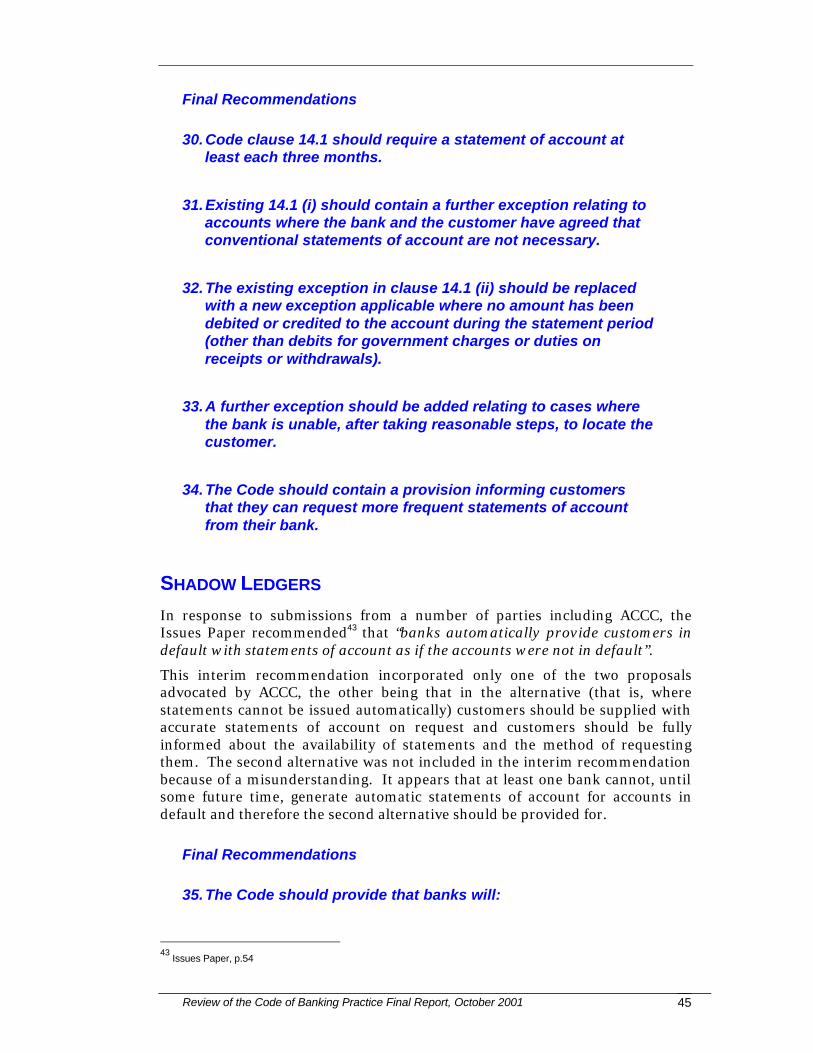

30. Code clause 14.1 should require a statement of account at least each three months.

31. Existing 14.1 (i) should contain a further exception relating to accounts where the bank and the customer have agreed that conventional statements of account are not necessary.

32. The existing exception in clause 14.1 (ii) should be replaced with a new exception applicable where no amount has been debited or credited to the account during the statement period (other than debits for government charges or duties on receipts or withdrawals).

33. A further exception should be added relating to cases where the bank is unable, after taking reasonable steps, to locate the customer.

34. The Code should contain a provision informing customers that they can request more frequent statements of account from their bank.

35. The Code should provide that banks will:

• automatically provide customers in default with statements of account as if the accounts were not in default; or

• where it is not possible to comply with the above, ensure that statements of account are provided in a timely manner to customers on request and ensure that customers are fully informed about the availability of statements and the method of requesting them.

Review of the Code of Banking Practice Final Report, October 2001 10

36. The Code should require banks to ensure that staff are competent to discharge their functions efficiently.

37. The Code should:

• require banks to supply on request, copies of contracts, account statements, notices and other relevant documents to customers, guarantors and persons acting for them, subject to the usual confidentiality and privacy requirements being satisfied;

• provide that the times within which copies are to be provided be modelled on UCCC section 163(2); and

• provide for an exception modelled on UCCC section 163(4).

38. The Code should contain a provision to the following effect:

“With your agreement, we will try and help you overcome your financial difficulties with us, for example, with your co-operation, developing a plan with you for dealing with your difficulties with us and telling you in writing what we have agreed. If the Consumer Credit Code applies to your credit facility with us we will explain the hardship variation provisions of that Code to you.”

39. The Code should require banks to:

• comply with the guideline published in July 1999 by ACCC for debt collection activities; and

• ensure that their agents comply and require their representatives to comply, with the guideline.

40. Clause 12.1 in the existing Code should be retained in the revised Code.

41. In lieu of Clause 15.1, the Code should contain a provision to the following effect:

“Before we offer or give you a credit facility (or increase an existing credit facility), we will exercise the care and skill of a diligent and prudent banker in assessing whether we think you will be able to repay it.”

Review of the Code of Banking Practice Final Report, October 2001 11

42. The Code should provide that a bank shall, no later than 1 July 2002, publish guidelines setting out the manner in which the bank will:

• deal with applications for transfer of mortgages and consents to transfer of title pursuant to a Family Court determination or approval; and

• otherwise enforce debts affected by a family law property settlement.

43. The Code should contain a clause which provides that:

• a bank will accept forthwith a customer’s instruction to cancel a Direct Debit Request and will not direct or suggest that the customer should first seek to cancel the Request by contacting the debit user;

• a bank will accept and proceed to process forthwith in accordance with the BECS regulations and procedures a customer’s complaint that a debit which has occurred was unauthorised or otherwise irregular and will not direct or suggest that the customer should first seek to resolve or raise the complaint directly with the debit user;

• neither of the above rules is intended to prevent a bank which has accepted the customer’s instruction to cancel or customer’s complaint from suggesting that the customer should then also contact the debit user; and

• banks will take all reasonable steps to facilitate the amendment of the APCA rules by no later than 1 July 2002 to provide for a direct debit guarantee with the principal features of the UK guarantee, but subject to such limitations and conditions as are prudentially necessary.

44. On the assumption that MasterCard and Visa rules do not specifically prohibit Australian banks from including in their terms and conditions for credit cards, provisions which permit a customer to cancel a credit direct debit authorization through their bank, the Code should contain a provision which requires banks to include in their terms and conditions a clear right for customers to cancel such authorisations.

45. The Code should require a bank to ensure that the terms and conditions of use of any credit card:

• include general information on the existence and operation of chargeback rights;

Review of the Code of Banking Practice Final Report, October 2001 12

• specify prominently an appropriate time frame for reporting a disputed transaction, being a time frame which would allow the bank to request a chargeback but would not unnecessarily shorten the reporting time; and

• warn the cardholder that the ability to dispute the transaction may, but need not necessarily, be lost if they do not report in time.

46. The Code provisions relating to guarantees should apply to all guarantees given by individuals in respect of facilities or accommodation provided by a bank to an individual or to small business whether incorporated or not. For these purposes “small business” shall be defined to have the same meaning as that proposed in Final Recommendation 6.

47. A bank shall not enter into a contract of guarantee with a guarantor unless the guarantor has first been provided with a copy of the contract and such other information as is required by this Code to be given to the guarantor.

48. The Code should require a bank to provide a prospective guarantor with all relevant information about the principal debtor and the transaction or facility to be guaranteed which:

• is in the possession of the bank; and

• a prospective guarantor would reasonably require in order to decide whether or not to enter the guarantee.

For this purpose, information includes representations with respect to a future matter, and also includes information provided by the principal debtor to the bank and any credit reporting agency reports and other expert reports obtained by the bank. It would not include the bank’s own internal opinions.

49. The Code should require a bank to advise guarantors to seek financial advice.

50. The Code should contain provisions which require:

• a bank to advise the guarantor that the guarantor can refuse to enter into the guarantee, that there are financial risks involved and that the guarantor should obtain independent legal advice;

• a warning notice similar to the UCCC notice to appear directly above the signature of the guarantor to reinforce

Review of the Code of Banking Practice Final Report, October 2001 13

the verbal warning on any guarantee not regulated by UCCC;

• a bank to ensure that unless it is demonstrably impracticable to do so, the guarantor must sign the guarantee in the absence of the principal debtor;

• a guarantor to be given information and advice at least one day before signing the guarantee unless the guarantor has received independent legal advice; and

• a bank to provide a guarantor on request with full statements of the guaranteed account or accounts and copies of any applicable facility documents, securities, guarantees, credit related insurance products and any notices previously given to the principal debtor and the times within which any such document is to be provided shall be modelled on UCCC section 163(2).

51. The Code should provide that a bank shall not accept an all accounts or all monies mortgage unless the mortgage contains a provision that it does not extend to any future contract or facility unless the mortgagor signs an extension of the mortgage after being provided with a copy of the new contract or facility.

52. The Code should:

• require that the guarantor be given a contractual right to vary the guarantee by reducing the cap on liability or limiting the amount or nature of the liabilities guaranteed, subject to appropriate qualifications to protect the bank’s financial position; and

• adopt the requirements set out in UCCC section 54 in relation to the extension of a guarantee to any future contract between the bank and the principal debtor.

53. The Code should confer rights on guarantors to withdraw from a guarantee as set out in UCCC section 53 as in force in all States other than Western Australia.

54. The UCCC rules relating to the enforcement of guarantees should be applied by the Code to all guarantees in respect of all debtors other than small business debtors.

Review of the Code of Banking Practice Final Report, October 2001 14

55. The Code should provide that:

• a bank should not sign up a party as a co-borrower where, on the facts known to the bank, the party will receive no direct benefit under the contract;

• a bank shall, before signing up co-borrowers, take all reasonable steps to ensure that each borrower understands the full extent of his/her liability;

• a bank shall ensure that under any contract it enters into, where each party is jointly and severally liable, either party should be able to terminate that liability unilaterally in respect of future advances or financial accommodation by written notice to the bank. Qualifications may be necessary to protect the bank’s legitimate interests in relation to further advances it is obliged to make and in respect of contingent liabilities which may accrue in the future.

56. The Code should provide that where a primary cardholder advises the issuing bank that it wants a subsidiary card cancelled, the primary cardholder shall not be liable for continuing use of the card, provided the primary cardholder takes all reasonable steps to procure the return of the subsidiary card to the issuing bank.

57. The Code should provide that:

• a bank, when opening a new account for a customer who already has an account(s) with the bank, shall state in writing whether the account will be segregated from the other account(s) and what the consequences are if the account is not segregated; and

• the statement in writing shall be specific to the customer and the customer’s accounts.

58. Internal Complaint Handling

A bank will have an internal process for handling complaints with its customers. This process will:

• be free of charge;

• be consistent with Australian Standard AS 4269-95 or any other industry dispute resolution standard or guidelines which ASIC declares to apply;

• ensure that customers are notified of the name and contact number of a person who is investigating their complaint;

Review of the Code of Banking Practice Final Report, October 2001 15

• specify time frames in line with those specified in clauses 10.5, 10.6 and 10.8 of the revised EFT Code for the completion of investigations and the reporting to complainants in exceptional cases; and

• require the bank to provide written reasons for its decision in respect of a complaint [subject to any Code provisions on election for electronic communications].

The internal process will be available for all complaints other than those that are resolved to the customer’s satisfaction immediately they are drawn to the attention of the bank.

59. External Dispute Resolution

A bank will have available to its customers an external and impartial process for resolving disputes. This process will be free of charge and will be consistent with the regulatory guidelines for the approval of external complaints resolution schemes.

60. Publicising and notifying customers of complaints and dispute resolution processes:

A bank will prominently publicise the availability and accessibility of both its internal and external processes for resolving complaints and disputes.

As a minimum, information about internal and external processes will be readily accessible and on display in bank branches and be accessible through bank Internet sites and bank telephone banking services.

In addition, a bank will provide a customer with written information [subject to any Code provisions on election for electronic communications] about:

• the internal process, at the time that a customer makes a complaint that is not immediately resolved to the satisfaction of both the customer and the bank; and

• the external process, at the same time as a customer is informed of the internal process and again at the time that a customer is advised of the final outcome of the internal process if that outcome does not wholly satisfy the customer’s claim.

61. The Code should contain rules which permit banks to provide by electronic means, information required by this Code to be given in writing to a customer, in terms that are consistent with clauses 22.1, 22.2 and 22.3 of the EFT Code.

Review of the Code of Banking Practice Final Report, October 2001 17

CHAPTER 1 - INTRODUCTION

APPOINTMENT OF THE REVIEW

On 12 May 2000, I was appointed by the Australian Bankers’ Association (ABA) to conduct a review of the Code of Banking Practice (Code). The establishment of the review was publicised in press advertisements and by letters sent by ABA to banks, consumer representatives, state ministries of fair trading and consumer affairs, members of parliament and other interested persons and organisations.

TERMS OF REFERENCE

The terms of reference are reproduced in full in Appendix 1 of the Issues Paper.

THE EXISTING CODE OF BANKING PRACTICE

The history of the development of the Code is set out briefly in the Issues Paper. This is the first review of the Code which was adopted by banks in November 1993 but did not become fully operative until November 1996. The existing Code is set out in Appendix 2 of the Issues Paper.

THE REVIEW PROCESS

The review was established on 12 May 2000 and proceeded in the following way:

• The initial five week period allowed for parties to make submissions proved to be inadequate and a series of extensions were granted. In excess of 70 submissions were received and a list of the parties who made submissions is set out in Schedule 1 to this report.

• Extensive negotiations were conducted with various stakeholders, as noted in the Issues Paper.

• A Code review website (www.reviewbankcode.com) was established and the major submissions were published on that website in the interests of enhancing the efficiency and transparency of the review process.

• After receiving the views of a number of stakeholders, I agreed that at the conclusion of receiving and considering submissions, I would publish an Issues Paper indicating my preliminary views on the issues raised.

• The Issues Paper was published at the commencement of March 2001 and final responses were invited with a closing date of 5 June 2001. For various reasons a number of major stakeholders were unable to make that deadline

Review of the Code of Banking Practice Final Report, October 2001 18

with the result that it was not until August that all responses had been received.

In the Issues Paper I noted1 that at least to that stage the participation in the review by banks generally, had been rather limited. It is clear from the Final Response from ABA on behalf of banks (which is set out in Schedule 2 to this report) and responses from some individual banks, that since the publication of the Issues Paper, banks have responded to the process in a responsible and open manner. Banks also entered into fruitful discussions with consumer representatives, which was particularly pleasing having regard to the enormous effort originally put into the process by the consumer representatives.

Banks, through ABA have also indicated that the actual drafting of a revised Code to implement the recommendations already accepted by the banks in their August 2001 response will be conducted in a process which will involve consumer and regulator input.

The great majority of the interim recommendations in the Issues Paper have been fully or substantially accepted by the banks. There are some issues where the responses from ABA and banks have convinced me that the relevant interim recommendation was simply not correct or that an alternative proposal is superior or at least as acceptable. Finally, there are a small number of issues where I regard the banks’ response as disappointing and in respect of which I have maintained the original recommendations. I simply ask that banks reconsider their position on those few issues.

This final report is not the end of the whole process. It will remain for banks to take the necessary steps to arrange for the drafting of a new or revised Code of Practice to give effect to the agreed recommendations. I look forward to the speedy implementation of the recommendations in the form of a redrafted Code.

ACKNOWLEDGEMENTS

The success or otherwise of any review of this nature is ultimately dependent upon the extent to which stakeholders choose to contribute to the process. As is obvious from the Issues Paper, and the submissions posted on the Code review website, very substantial contributions were made by consumer representatives, especially the Legal Centres and other contributors to the Joint Consumer Submission (JCS) and ACA, and by ASIC and ABIO. The process was also assisted by the many submissions from individuals, organisations and State ministers and agencies, listed in Schedule 1. I must also acknowledge the substantial effort made by banks in the latter stages of the review and last but not least, the contribution made by the Australian Bankers’ Association, both in presenting views and in providing administrative and like support in ways which were effective yet respected the independence of the review.

STRUCTURE OF THIS REPORT

This report is intended to be read in conjunction with the Issues Paper. For convenience, the Issues Paper is reprinted with this report so that interested 1 Issues Paper, p.2

Review of the Code of Banking Practice Final Report, October 2001 19

parties will have easy access to it and the source material set out in its various Appendices.

Review of the Code of Banking Practice Final Report, October 2001 21

CHAPTER 2 – UNCOMPLETED MATTERS

There are a number of issues which were raised in the course of the review which it has not been possible to finalise.

Some are of a technical or relatively minor nature which are likely to be resolved in the Code drafting process.

However there are some unresolved issues which should, in my opinion, be the subject of further investigation:

• Whether banks should be obliged to financially compensate customers (possibly through the payment of a flat sum per instance) for shortfalls at ATMs and for direct debiting errors.

• Where a bank normally charges a fee if an entry on a statement disputed by a customer is proved to be correct, whether a sum equivalent to the fee should be credited to a customer’s account if an entry on a statement disputed by the customer is found to be incorrect.

• Whether the Code should require banks to comply with other relevant Codes.

• Whether notification through the media alone of changes to terms or conditions is an effective way of communicating the changes to customers.

• How the needs of consumers with low literacy levels might be met through improved disclosure and other documents.

• Whether customers should be offered the option of being able to place a stop on credit card accounts in certain circumstances.

• Whether a bank in its advertising and point of sale promotion of certain types of accounts should be required to include specific reference to the institution’s contractual right to unilaterally change the terms and conditions.

A recommendation is made in this report2 that the Code should provide for the establishment of a forum for the regular exchange of views between banks and consumer advisors on banking issues. In its Final Response and in subsequent discussions, ABA has indicated that the unresolved matters listed above should not delay the completion of the review and that it supports these matters being referred to that forum for resolution.

2 Final Recommendation 14

Review of the Code of Banking Practice Final Report, October 2001 23

CHAPTER 3 - GENERAL ISSUES

OBJECTIVES AND PRINCIPLES

The Issues Paper sets out at some length3 the criticisms that consumer representatives make of the existing Code and the banks’ views on what should be the objectives and principles of a modernised Code of Banking Practice in Australia. After reviewing those matters and specific submissions on objectives and principles from consumer representatives, the Issues Paper made the following interim recommendations:4

• in lieu of Objective 1, the Code should articulate a commitment to continuous improvement in the standards of practice and service in the banking industry; and

• in lieu of Objective 2, the Code should articulate a commitment to promoting better informed decision making by all means available, including providing effective disclosure and providing appropriate advice.

In broad terms, the ABA Final Response has expressed agreement with that recommendation but in a modified form, as follows:

“Key Commitments

We promise that we will

• work towards continuously improving the standards of practice and service in the banking industry;

• promote better informed decisions about our products and services including by providing effective disclosure of information; and

• provide information about your rights and obligations in relation to banking services.”

As the Note to this proposal in the ABA response5 indicates, banks have a concern about the consequences under FSR of providing financial product advice. While I can understand that concern, I suspect there has been a misunderstanding of the interim recommendation that banks commit to “promoting better informed decisions about bank products by….providing appropriate advice” (emphasis added).

It was not the intention that banks should ensure that each staff member likely to deal with the public must be trained so as to be capable of advising any customer on any bank product. Rather, the term “providing appropriate advice” was intended to mean providing advice, on request, through a person

3 Issues Paper pp 8-11

4 Issues Paper, p.15

5 Schedule 2, p.2

Review of the Code of Banking Practice Final Report, October 2001 24

whose training and knowledge is adequate for the purpose, whether that person is a bank employee whose normal duties include giving advice about the relevant product or some external person to whom the customer is referred by the bank. The original recommendation also had in mind the provision by appropriate bank staff of explanations of banks’ promotional and product disclosure documents to their customers. The final recommendation is in terms which are intended to clarify these matters.

Consumer representatives have also suggested that a fourth key commitment be added to ensure that all information provided by banks to customers and prospective customers will be in plain language.

Final Recommendation

1. In lieu of Objectives 1 and 2, the Code should articulate the following:

“Key Commitments

We promise that we will

• work towards continuously improving the standards of practice and service in the banking industry;

• promote better informed decisions about our products and services including:

by providing effective disclosure of information;

by providing advice on bank services to customers on request, whether through bank staff authorised to give such advice or by referring customers to appropriate external sources of advice; and

by explaining to customers, when asked, the contents of brochures and other written information about bank services;

• provide information about your rights and obligations in relation to banking services; and

• ensure that all information we provide to customers and prospective customers will be in plain language.”

FAIRNESS

The Issues Paper contained a recommendation6 that the revised Code should incorporate an undertaking by banks to act fairly in their dealings with customers. The proposal was to incorporate a slightly modified form of the commitment to fairness contained in the New Zealand Banking Code.

6 Issues Paper p.17

Review of the Code of Banking Practice Final Report, October 2001 25

In its Final Response to the Issues Paper7, ABA proposed to incorporate into the Code a provision committing banks to act fairly in their dealings with customers, but with a somewhat different form of drafting. Some banks which made final responses to the Issues Paper also expressed support for incorporating the principle of fairness. It should be borne in mind in dealing with the matter of fairness, that the Code as revised, will be contractually binding on banks with the result that the obligation will be a serious one.

The terms of the suggestion proposed in the ABA Final Response is as follows:

“We promise that we will act fairly and reasonably towards you (our customers) in a consistent and ethical manner. In doing so we will consider your conduct, our conduct and the contract between us”.

In my view, the ABA proposal has the advantage of being simpler and more succinct than the one proposed in the Issues Paper and will represent, when implemented, a considerable advance in bank customers’ rights.

Final Recommendation

2. The Code should incorporate a principle of “fairness” in terms to the following effect:

“We promise that we will act fairly and reasonably towards you (our customers) in a consistent and ethical manner. In doing so we will consider your conduct, our conduct and the contract between us.”

PRUDENTIAL PRINCIPLE

The Issues Paper recommended8 that the existing Code provision in the preamble under the heading “Principles” should be retained. Consumer representatives have withdrawn any objections they had to the retention of this principle. Accordingly, I believe the concept should be retained in the Code although I see merit in ABA’s suggestion that the drafting be simplified.

Final Recommendation

3. A prudential principle should be retained in the Code in terms to the following effect:

“In meeting our key commitments we will have regard to our prudential obligations.”

7 Schedule 2, p.2

8 Issues Paper, p.17

Review of the Code of Banking Practice Final Report, October 2001 26

SCOPE OF THE CODE

Definition of “Banking Service” The Issues Paper recommended9 that the term “banking service” be defined to mean any service provided by a bank. ABA agreed with that recommendation. The only issues that remain with respect to this definition are:

• whether the definition makes it sufficiently clear that the intended policy is that a bank should have responsibility for any banking service or product of its own which is supplied to a customer either directly or through an intermediary; and

• whether it is also clear that while a bank does not have a responsibility under the Code to stand behind someone else’s product which the bank sells or distributes as an agent, it nonetheless is responsible for any loss caused by shortcomings in the selling process.

Final Recommendation

4. The Code should define banking service to mean any financial service provided by a bank to a customer in terms which make it clear that the definition:

• includes any financial service or product provided by a bank whether supplied to a customer directly or through an intermediary; and

• in the case of a financial service or product provided by another party but distributed by a bank, does not extend to that product or service but extends to the bank’s distribution or supply of the service or product to a customer.

Definition of “Customer” After reviewing at some length the existing limitations on what the term “customer” should mean in a revised Code, the Issues Paper made a number of recommendations10:

• The Code should apply to any banking service provided to an individual, whether alone or jointly with another individual.

• The operation of the Code should be extended to small businesses.

• The Code should define “small business” in the same terms as FSR defines “retail client”.

ABA has proposed what I regard is the simplest and most effective definition. ABA proposes:

9 Issues Paper, p.18

10 Issues Paper, p.19 and p.22

Review of the Code of Banking Practice Final Report, October 2001 27

“Customer means an individual or small business”.11

Moreover, the note to the relevant recommendation in the ABA Final Response makes it plain that this approach is a more progressive solution than that advocated in the Issues Paper in that it simply proposes that a majority of the provisions of the Code could apply equally to a small business as to any other customer. However, it also suggests that there will need to be some modifications of the Code where the small business situation is necessarily different. Examples of where the Code would need modification to apply satisfactorily to small business are confidentiality and privacy and access to low cost accounts.

In my view, this is a most satisfactory solution and far preferable to the proposal in the Issues Paper that the existing voluntary Small Business Principles should be reviewed and as reviewed incorporated into the Code. Although neither FSR nor UCCC will apply so as to require the provision of disclosure in any credit contract for a small business, the existing requirements of Code clause 2.3 (as proposed to be modified) will provide for disclosure of fees and charges, interest charges and methods of calculation and repayment details.

Finally, the ABA response12 proposes that the term “small business” be defined consistently with the definition of that term in FSR.

Final Recommendations

5. The Code should define customer as meaning an individual or a small business.

6. The Code should define a small business to mean a business employing:

• less than 100 people if the business is or includes the manufacture of goods; or

• in any other case, less than 20 people.

CODE MONITORING AND ADMINISTRATION

The proposals for monitoring compliance with the Code and the imposition of sanctions for non-compliance have been the most controversial aspect of the review.

The submissions received from consumer representatives and ASIC all argued for an independent, well resourced Code monitoring agency with a capacity to impose a range of effective sanctions for Code breaches, including breaches which do not cause financial loss to customers.

11

Schedule 2, p.4 12

Schedule 2, p.5

Review of the Code of Banking Practice Final Report, October 2001 28

The way in which this issue is ultimately resolved by the banks will go to the very heart of the efficacy of any revised Code. If the Code is to achieve credibility as an instrument of self-regulation, there must be demonstrable reasons for having confidence that Code subscribers will comply with the Code and will be subject to appropriate sanctions when they do not. It is the absence of any effective monitoring and sanctions under the existing Code which has led to the widespread view, referred to in the Issues Paper, that the present Code lacks credibility and indeed relevance.

In response to those submissions the Issues Paper made the following recommendation:13

“The Code should:

• entitle consumers, consumer advocates, regulatory agencies and dispute resolution schemes to make complaints about non-compliance with the Code;

• detail complaint making investigation and decision-making processes;

• ensure the investigation and decision-making processes are impartial, fair, efficient and accountable;

• provide an adequate range of sanctions;

• provide that the oversight of these processes should rest with the Code monitoring agency.”

In view of the importance of this topic it is convenient to set out in full the text of the relevant part of ABA’s Final Response, as follows:

“5. Monitoring compliance with the Code

All ABA member retail banks are committed to establishing an independent, transparent and efficient process for monitoring banks’ compliance with this Code. Banks see this mechanism as fundamental to an effective Code and have closely examined a range of possible models to achieve this. Set out below are the key criteria of an agreed model14:

1. A committee, the Code Compliance Monitoring Committee, would be set up within the Australian Banking Industry Ombudsman scheme. Agreement of the ABIO to do this would be necessary.

2. The function, powers and composition of the CCMC would be spelt out in the Code. These could change if the Code were changed.

3. The CCMC would operate quite separately from the Ombudsman’s dispute resolution function so as not to adversely affect that function.

13

Issues Paper p.27 14

ABA’s internal Code review working group has held many discussions over possible approaches to monitoring of compliance and have reached a majority consensus on this model. As Commonwealth Bank has submitted in its submission to the Reviewer, it recognises the importance of having independent compliance monitoring. CBA does not necessarily oppose the model proposed by ABA. It however regards as necessary that further analysis, evaluation and consultation take place on the various options to ensure the most effective mechanism is adopted.

Review of the Code of Banking Practice Final Report, October 2001 29

4. The CCMC would be a committee of three:

• One person having had relevant experience at a senior level in retail banking, appointed by the Code subscribing banks;

• One person having relevant experience and knowledge as the representative of the general body of bank customers, appointed by the ABIO.

• One person having had experience in industry, commerce, public administration or government service, appointed jointly by the ABIO and the Code subscribing banks.

5. The CCMC would employ a small secretariat to service the CCMC.

6. All decisions about banks’ compliance with the Code would be the responsibility of the CCMC.

7. To ensure CCMC operated diligently, within power, efficiently and effectively, the CCMC would be required to commission an independent annual audit of its activities and for that audit report to be lodged with ASIC for publication. Agreement of ASIC to perform this role would be required.

8. Banks would continue to prepare their own annual compliance reports and to lodge them with the CCMC.

9. CCMC’s functions and powers would be to:

• Monitor Code compliance by comparing banks’ annual reporting of compliance with CCMC’s own experience gained through “shadow shopping” and the incidence of complaints from customers about banks’ non-compliance.

• Receive complaints about breaches of the Code and refer them to the banks concerned for response and remedial action where necessary.

• Report annually on the level of compliance.

• Report in its annual report un-remedied, serious and systemic breaches by a bank with discretionary power to name the non-complying bank.

6. Sanctions

Sanctions against banks for breaches of the Code irrespective of whether financial loss is incurred by the customer is an issue closely tied to the compliance monitoring function. Disputes where the customer incurs a financial loss are already covered by the Banking Industry Ombudsman Scheme. The proposed compliance monitoring model above also contains proposals for handling serious systemic Code breaches and imposition of a naming sanction for repeat offenders.”

The model proposed in ABA’s Final Response falls short of what was proposed in the interim recommendations, particularly with respect to the sanctions.

Review of the Code of Banking Practice Final Report, October 2001 30

Under the ABA proposal the only sanction contemplated is a public naming of “repeat offenders” by the monitoring body.

It nonetheless has to be conceded that the proposals in the ABA Final Response are a substantial advance on the present position. In all the circumstances it may be acceptable to give those proposals a chance to operate and review the position after a couple of years experience with them. However, if this is done, it would be useful to clarify firstly, that complaints about breaches of the Code will be able to be received from consumer organisations and State regulatory agencies and secondly, that the ABIO could refer to the monitoring body, breaches of the Code detected by it in the course of ABIO’s dispute resolution function.

Nothing in these proposals should in any way affect the ABIO’s existing jurisdiction and complaint resolution functions.

Final Recommendation

7. The Code should provide for a monitoring mechanism and sanctions having the criteria detailed in the proposal set out in ABA’s Final Response, subject to it being made clear that:

• complaints about breaches of the Code will be received from consumer organisations and state regulatory agencies;

• the ABIO may refer to the code monitoring body, breaches of the Code detected by ABIO in the course of its dispute resolution function; and

• nothing in these proposals will in any way limit or affect the ABIO’s existing jurisdiction or function.

EDUCATING CODE MEMBERS (AND THEIR STAFF AND AGENTS) ABOUT THE CODE

The Issues Paper recommendation15 was that “the Code oblige banks to ensure all relevant staff and agents have an adequate knowledge of its provisions.”

The ABA Final Response16 is in the following terms:

“we will ensure that our staff and agents receive training and documentation so that they are competent to provide the Banking Services they are authorised to provide and that they have an adequate knowledge of the provisions of this Code.”

On analysis, this proposal deals with two separate issues, namely, the provision of training and documentation so that staff are competent and secondly ensuring that staff have an adequate knowledge of the provisions of the Code.

15

Issues Paper, p.28 16

Schedule 2, p.7

Review of the Code of Banking Practice Final Report, October 2001 31

In my view these are two very different issues and thus it is preferable to deal with them quite separately as was done in the Issues Paper. Accordingly, I would prefer to leave the recommendation of the Issues Paper on educating staff about the Code unchanged and deal elsewhere with the broader issue of competency.

Final Recommendation

8. The Code should oblige banks to ensure all relevant staff and agents have an adequate knowledge of its provisions.

PROMOTING THE CODE TO CONSUMERS, CONSUMER ADVISORS

AND THE PUBLIC GENERALLY

The Issues Paper recommendation17 was as follows:

• The Code should require the Code administration body to promote the Code among bank customers, consumer advisors and the public generally.

• Banks should be obliged to display the Code, and have copies available on request by any person at all branches.

The proposal in the ABA’s response18 is quite different:

“ABA will promote the Code including which banks subscribe to it and how to obtain access to the Code.”

The difficulties with the ABA suggestion are firstly that ABA is not bound by the Code and secondly, it implicitly means that banks are not to have any responsibility, at least under the Code, for promoting it and making it available to the customers. In the note to its proposal, ABA draws attention to the fact that some banks do not have branches. While that might be, I believe it is important that copies of the Code be available from bank branches. However, I agree that other means of access should be provided, particularly for banks without branches and as a matter of convenience to customers by receiving requests by telephone or electronically.

Final Recommendations

9. The Code should require the Code administration body to promote the Code among bank customers, consumer advisors and the public generally.

10. Banks should be obliged to display the Code, and have copies available on request by any person, at all branches.

17

Issues Paper, p.28 18

Schedule 2, p.7

Review of the Code of Banking Practice Final Report, October 2001 32

11. Banks which do not have branches and banks which offer internet banking must refer to the Code on their websites and provide copies of the Code on request by mail or electronically.

MONITORING EXTERNAL DEVELOPMENTS INCLUDING LEGISLATIVE CHANGES

The Issues Paper recommended19 that this function be done by the Code monitoring body. ABA agrees20 that monitoring is necessary but believes that banks do this already as a matter of course and the Code could therefore, as an alternative, require subscribing banks to monitor external developments and legislative changes. This appears to be a satisfactory alternative.

Final Recommendation

12. Banks should monitor external developments relating to banking codes of practice and related issues.

ARRANGING REGULAR REVIEWS OF THE CODE

The Issues Paper recommendation21 was to the following effect:

At the minimum, the Code should provide that the review process will ensure:

• Adequate consultation with interested parties;

• Interested parties to have adequate time to present views;

• The review process is transparent.

The Code should establish a forum for regular exchange of views between banks and consumer advisors on banking issues.

The ABA Final Response22 supports the concept of the independent reviews every three years in consultation with a range of stakeholders. In addition, work is already progressing on the establishment by ABA of a consultative forum.

Final Recommendations

13. The Code should provide that an independent review of the Code is conducted every three years under a process which ensures:

19

Issues Paper, p.29 20

Schedule 2, p.7 21

Issues Paper, p.29 22

Schedule 2, p.7

Review of the Code of Banking Practice Final Report, October 2001 33

• adequate consultation with banks, consumer organisations, ABA and other interested industry associations, relevant regulatory bodies and other stakeholders;

• interested parties have adequate time to present views; and

• the process is transparent.

14. The Code should provide for the establishment of a forum for the regular exchange of views between banks and consumer advisors on banking issues.

IMPLEMENTING CHANGES

The Issues Paper recommended23 that the Code should require ABA to promptly publish the final report and recommendations of any review and to publish regular reports on the progress of implementation.

ABA’s Final Response24 accepts that proposal.

Final Recommendation

15. The Code should require ABA to:

• promptly publish the final report and recommendations of any review; and

• publish on ABA’s website, progress reports on implementation of a review’s recommendations until the implementation process is complete.

ACCESS TO BANKING SERVICES

The Issues Paper noted25 the large number of concerns raised by a range of organisations and individuals, including state governments, municipal councils and chambers of commerce, about branch closures, particularly in regional and rural Australia. It noted that branch closure protocols have been dealt with in the Hawker Report which made a number of recommendations.

Recommendation 20 of the Hawker Report read in part as follows:

“The Committee recommends that the industry adopts a branch closure protocol which incorporates the following:

23

Issues Paper, p.30 24

Schedule 2, p.8 25

Issues Paper, pp. 31-33

Review of the Code of Banking Practice Final Report, October 2001 34

1. Banks will give three months notice to customers and relevant community organisations such as Local Councils, of their intention to close a branch.

2. Banks will consult with local communities about trends in the delivery of banking services and, in particular, about developments that have the potential to affect the delivery of services in that region. Included in this will be a genuine desire to use community goodwill to improve the viability of the branch. In the event of a decision to close a branch, banks will consult with the community about preferred options for alternative services and on the training to be provided in using alternative channels.

3. Banks will provide written notice of at least two months before changing the branch that manages an account.

4. In the event of closing or downgrading a branch below agency status, banks will waive any fees or penalties incurred relating to early repayment of loans or closing of accounts.”

The Issues Paper recommended that the Code incorporate the proposals made in recommendations 20.1 to 20.4 of the Hawker Report.

ABA’s response26 to that recommendation is as follows:

“ABA has recently released details of a rural and regional branch closure protocol as part of a more comprehensive set of initiatives to improve access to banking services ………… Banks have agreed that the branch closure protocol should be sign posted through the Code.”

I do not understand that under ABA’s initiative, banks will have (or end up having) an absolute obligation to comply with a branch closure protocol developed under the auspices of ABA and if that is correct, it is questionable what purpose would be served by “sign-posting” the branch closure protocol throughout the Code as suggested.

I remain of the view that the Code should incorporate the proposals made in recommendations from 20.1 to 20.4 of the Hawker Report as a minimum branch closure protocol to be followed by subscriber banks.

Final Recommendation

16. The Code should incorporate the branch closure protocols set out in recommendations 20.1 to 20.4 of the Hawker Report.

26

Schedule 2, p.8

Review of the Code of Banking Practice Final Report, October 2001 35

ACCESS TO BANKING SERVICES FOR PEOPLE UNABLE OR RELUCTANT TO USE ATMS, TELEPHONE BANKING OR INTERNET BANKING

A wide range of submissions were received on the difficulties that advances in technology have brought to people who, for a variety of reasons, are unable or unwilling to use ATMs, telephone banking or internet banking.

This is a topic which does not lend itself, in my view, to the Code mandating specific measures to overcome or alleviate the problem but there is no doubting the seriousness of the problem and the sincerity with which the submissions have been made.

It was for that reason that the Issues Paper recommended that “the Code provide that banks take all reasonable measures to enhance access to banking services for older people and people with disabilities”.

In its response, ABA proposed27 recognising the special needs of elderly and disabled persons to have access to transaction accounts but was somewhat guarded as to the terms in which any commitment should appear in the Code. In part, the submission proposed “we will consider and implement steps we might reasonably take to facilitate access and to educate ……. on the use and benefits of accessing banking services through the new technologies”.

I prefer the original recommendation.

Final Recommendation

17. The Code should provide that banks take all reasonable measures to enhance access to banking services for older people and people with disabilities.

LOW COST ACCOUNTS FOR BANKING SERVICES

The Issues Paper discussed28 the submissions received from consumer representatives that the Code should provide that any person should be able to open a deposit account with any bank and that this right should not be limited by minimum deposit or opening balance requirements or other conditions. The submissions also argued that all subscriber banks should offer a basic banking account with a specified minimum number of fee-free transactions.

The Issues Paper noted that while the UK Banking Code describes a concept of a basic account, it does not oblige subscribers to offer such accounts but rather, provides that if a bank does offer basic accounts it must give any prospective customer information on its basic accounts if the bank thinks the customer might be interested in such an account. The UK Banking Code does not provide

27

Schedule 2. p.8 28

Issues Paper, pp. 37-38

Review of the Code of Banking Practice Final Report, October 2001 36

any detail about the level of account keeping fees or how many fee-free transactions should be features of a basic account.

In my opinion, there is not much point in requiring banks to offer basic or low cost accounts without also specifying detailed minimum features in specific terms. It is for this reason that the interim recommendation29 was that:

The Code require banks to provide details of their accounts which are most suitable to low income or disadvantaged persons who are prospective customers and also to existing customers whose present facilities may not be optimal.

In its Final Response, ABA supports30 the essence of the interim recommendation and added that in March 2001, ABA announced a basic account standard and was proposing an application to ACCC for authorisation for banks to agree to provide accounts that at least meet that standard. In the circumstances I consider that the interim recommendation remains satisfactory.

Final Recommendation

18. The Code should require banks to provide details of their accounts which are most suitable to low income or disadvantaged persons who are prospective customers and also to existing customers whose present facilities may not be optimal.

29

Issues Paper, p.39 30

Schedule 2, p.9

Review of the Code of Banking Practice Final Report, October 2001 37

CHAPTER 4 – DISCLOSURE REQUIREMENTS

INTRODUCTION

The Issues Paper discussed at some length the desirability or otherwise of there being substantial overlap between the Code, UCCC and FSR. It made the following interim recommendations:31

• significant overlap between Code provisions and other laws, particularly UCCC and FSR, is undesirable and overlapping Code provisions should be deleted from the Code;

• there should be included in the Code for information purposes only (and not as substantive provisions), material which advises consumers and bank staff of disclosure rights and obligations arising under UCCC and FSR and other relevant laws and which summarises the principal features of those rights and obligations;

• in order to retain the essence of the current position whereby banks are contractually bound to meet their disclosure obligations under the Code, the Code should contain a provision by which banks contractually bind themselves to their customers to meet their disclosure obligations under FSR, UCCC and other relevant laws.

There was substantial support in the responses to the Issues Paper for the first of these recommendations, namely that overlapping was undesirable.

As to the second recommendation, a number of responses, particularly from banks and ABA, questioned the practicality of including in the Code (whether as an Appendix or otherwise) detail of disclosure rights and obligations which arise under other laws, particularly UCCC and FSR. On reflection I am persuaded that it is not practical to signpost for customers and bank staff in detail, disclosure rights and obligations arising under other laws. However, I believe that at or near the commencement of the Code there should be a concise statement that consumers also have rights under other named laws.

The essence of the third recommendation is addressed effectively by paragraph 15 of the ABA Final Response32 which in part reads:

“15 Customer access to information entitlements and contractual rights

We suggest the following drafting:

We will comply with all relevant laws and regulations relating to banking services including those covering:

31

Issues Paper, p.43 32

Schedule 2, p.9

Review of the Code of Banking Practice Final Report, October 2001 38

• consumer credit products;

• other financial products and services;

• privacy; and

• discrimination”.

Final Recommendations

19. Significant overlap between Code provisions and other laws, particularly UCCC and FSR, is undesirable and overlapping provisions should, except where there are special reasons to the contrary, be deleted from the Code.

20. At or near the commencement of the Code, there should be included a statement to the following effect:

“Customers are advised that in addition to their rights under this Code they may have rights under Federal laws, especially the Trade Practices Act and the Financial Services Reform Act and under State and Territory laws, especially the Consumer Credit Code and Fair Trading Acts.”

21. The Code should contain a provision to the following effect:

“We will comply with all relevant laws relating to banking services, including those concerning:

• consumer credit products;

• other financial products and services;

• privacy; and

• discrimination.”

“FLESHING OUT” THE NECESSARY DETAIL FOR PDS

Having dealt generally with the issue of overlap the Issues Paper then focused on whether it was desirable to use a revised Code as a mechanism for fleshing out the detail of the disclosure requirements under FSR for banking products and services.

The principal interim recommendation was that “the Code is not the appropriate medium for fleshing out the necessary detail of PDS for the purposes of FSR.”33

However, it is important to bear in mind that the extent of overlap is not perhaps as great in practice as might have been assumed.

33

Issues Paper, p.46

Review of the Code of Banking Practice Final Report, October 2001 39

In general terms, the Code requires disclosure of certain things to be achieved by requiring those things to be included in the terms and conditions of a banking service. The Code also requires disclosure of other things to be made to any person, whether an existing customer or not, on request. These requirements serve different purposes than the purposes for which PDS statements are mandated by FSR. In addition, many of the disclosure obligations in the existing Code are of a consumer protection nature in that they warn customers of precautions that should be taken when operating accounts and using various banking services. It may be that some of those warnings might also be required to be described in a PDS as risks associated with the relevant bank product, but the existing provisions of this nature in the Code are succinct and the small amount of overlap is in my view, well justified by the benefit to consumers of retaining the warnings.

Final Recommendation

22. The Code is not the appropriate medium for fleshing out the necessary detail of PDS for the purposes of FSR.

TIMING DIFFERENCES AFFECTING NOTIFICATION OF CHANGES

The Issues Paper noted that if the overlapping disclosure provisions of the Code are deleted in favour of UCCC and FSR provisions, there will be some consequences on the timing of certain disclosures.

Having analysed the extent of the conflicts between the Code and UCCC with respect to the notification of changes, the Issues paper recommended34 that UCCC and not the Code should specify the notice requirements for changes to UCCC regulated products.

A comparative analysis of the FSR and Code provisions for the notification of changes revealed that while the FSR requirements for changes relating to fees and charges were satisfactory, the FSR requirements relating to other changes were significantly less precise or helpful to customers than are the existing Code provisions. For these reasons, the Issues Paper recommended that35:

• FSR and not the Code should specify the notice requirements for changes relating to fees and charges; and

• the existing Code notice requirements should be retained for all other changes.

In its response to the Issues Paper, ABA appears to submit36 that the FSR notice requirements should apply to all changes, not simply those relating to fees and charges. I do not believe that the ABA response demonstrates a good reason to depart from the interim recommendation. As can be seen from the Issues Paper the FSR rules will significantly weaken some of the disclosure requirements for

34

Issues Paper, p.50 35

Issues Paper, p.50 36

Schedule 2, p.10

Review of the Code of Banking Practice Final Report, October 2001 40

non-credit products that have been in the Code since its inception. Banks are currently (and have for some time been) complying with those more rigorous Code requirements and I am not aware of any general bank criticism of those provisions. I therefore see no reason to change the interim recommendation.

Final Recommendations

23. UCCC and not the Code should specify the notice requirements for changes to UCCC regulated products.

24. FSR and not the Code should specify the notice requirements for changes relating to fees and charges.

25. The existing Code notice requirements should be retained for all other changes.

Note: The Issues Paper considered a proposal from ABIO that good banking practice requires that written notice should be given to all affected customers 30 days before the change comes into effect of any change in the minimum balance to which an account keeping fee applies or a change in the interest rate tiers applying to a deposit account. The Issues Paper made an interim recommendation to that effect37.

Final Recommendation 24 is based on an assumption that FSR will require 30 days notice of either type of change. If this assumption is incorrect, the Code should provide for such notice.

WHICH DISCLOSURE REQUIREMENTS CONTAINED IN EXISTING CLAUSES SHOULD REMAIN IN THE CODE?

In this context I am referring to existing Code clauses 2 to 9, 11, 13 and 19.

In my view, there should be retained in the Code any existing disclosure provisions which:

• require the disclosure of information in terms and conditions of banking service;

• require disclosure of information to any person on request; or

• have the principal purpose of warning or advising a customer about features of a banking product or the prudent use of the product.

However, in relation to existing Code provisions which deal with the notifications of changes, any such provisions should be retained only if that is also consistent with Final Recommendations 23, 24 and 25.

37

Issues Paper, p.56

Review of the Code of Banking Practice Final Report, October 2001 41

Particulars of how, consistently with the above, existing Code clauses 2 to 9, 11, 13 and 19 should be dealt with are set out in the Final Recommendation below.

Final Recommendations

26. A revised Code should deal with existing disclosure provisions in clauses 2 to 9, 11, 13 and 19, in the following way:

Current Code provision

Recommended action

2.1 Retain, subject to –

• deleting 2.1 (iv) as a consequence of the last item in Final Recommendation 1; and

• adding at the end of 2.1 (vi) “unless that information is not relevant to the particular banking service”.

2.2 Retain

2.3 Retain, subject to the following modifications: